Financial Reporting Analysis: Godwin PLC and FTSE 100 Companies

VerifiedAdded on 2020/10/05

|13

|3746

|212

Report

AI Summary

This report provides a comprehensive overview of financial reporting, encompassing its concept, objectives, and the regulatory framework, including IAS and IFRS. It identifies key stakeholders and discusses the value of financial reporting in fostering industrial growth. The report includes the preparation of financial statements, such as the income statement, statement of changes in equity, and financial position for Godwin PLC. Furthermore, it delves into the interpretation of financial ratios for FTSE 100 index companies, offering insights into their profitability, liquidity, and efficiency. The report also clarifies the differences between IAS and IFRS and explains the benefits of IFRS, concluding with a discussion on varying degrees of IFRS compliance by world organizations and their impact on nations. The report is enriched with working notes, detailed calculations and interpretations of the financial data, making it a valuable resource for understanding financial reporting principles and practices.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Ascertaining the concept and objective of financial reporting................................................1

2. Identifying the conceptual and regulatory framework which highlights the purpose and key

principles......................................................................................................................................2

3. Determining the key stakeholder in an organisation and benefits of them in the organisation

.....................................................................................................................................................2

4. Determination of the value of financial reporting for meeting industrial growth and

objectives.....................................................................................................................................3

5. Preparation of financial statements..........................................................................................3

6. Interpretation of ratios of FTSE 100 index companies............................................................7

7. Difference between IAS (International Accounting Standards) and IFRS (International

Financial Reporting Standards)...................................................................................................9

8. Explaining IFRS benefits.........................................................................................................9

9. Varying degree of compliance with IFRS by world organisations and how they impact on

nation.........................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

1. Ascertaining the concept and objective of financial reporting................................................1

2. Identifying the conceptual and regulatory framework which highlights the purpose and key

principles......................................................................................................................................2

3. Determining the key stakeholder in an organisation and benefits of them in the organisation

.....................................................................................................................................................2

4. Determination of the value of financial reporting for meeting industrial growth and

objectives.....................................................................................................................................3

5. Preparation of financial statements..........................................................................................3

6. Interpretation of ratios of FTSE 100 index companies............................................................7

7. Difference between IAS (International Accounting Standards) and IFRS (International

Financial Reporting Standards)...................................................................................................9

8. Explaining IFRS benefits.........................................................................................................9

9. Varying degree of compliance with IFRS by world organisations and how they impact on

nation.........................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

To determine the operational performance and the business objectives here will be necessity

of making adequate financial reports. Thus, these are consisting of various information such as

income, expenditures, assets and liabilities of firm in a particular period. Thus, such information

has been addressed in various accounts which were later being summarized and analysed by the

accounting professionals. In the present report there will be preparation of various accounts

along with the analysis over the importance of such reporting techniques in meeting the

industrial objectives. Moreover, there will be analysis over the financial performance of the

FTSE listed organisation over the period of 2 years.

1. Ascertaining the concept and objective of financial reporting

Financial disclosure consists with preparation of various financial accounts which includes

income statement, balance sheet, cash flows and statement of change in equity. Thus, preparation

of such accounts will be helpful to communicate the business performance among the external

parties (Johnston and Petacchi, 2017). Stakeholders will have appropriate analysis over the data

base on which they can make investments decisions. Along with this, the internal management of

operations will also become soothing and adequate to the professionals in terms of analysing the

cost reduction opportunities.

Objectives behind preparing the financial reports:

To communicate the business information among internal as well as external stakeholder

with a motive to retaining the adequate growth and brand value in the external market. It musts

be consists of clear and transparent information which are to be disclosed among the

professionals with a motive to have appropriate analysis over the data base (Bonsall IV and et.al.,

2017). Moreover, there are various objectives to the financial reporting such as:

Investment decision-making: The main objective of the financial reports is for decision

making, analysing profitability, liquidity and efficiency of the firm. Users of such information

are basically keen to know the dividend pay-out ratio and the profits retained by the firm in a

year. Therefore, they analyse the organisation on the basis of amount of return is being payable

by them in the business.

Cash flow management: The influences of financial reporting have been enacted in

measuring the performance of the organisation. There will be appropriate ascertainment of

1

To determine the operational performance and the business objectives here will be necessity

of making adequate financial reports. Thus, these are consisting of various information such as

income, expenditures, assets and liabilities of firm in a particular period. Thus, such information

has been addressed in various accounts which were later being summarized and analysed by the

accounting professionals. In the present report there will be preparation of various accounts

along with the analysis over the importance of such reporting techniques in meeting the

industrial objectives. Moreover, there will be analysis over the financial performance of the

FTSE listed organisation over the period of 2 years.

1. Ascertaining the concept and objective of financial reporting

Financial disclosure consists with preparation of various financial accounts which includes

income statement, balance sheet, cash flows and statement of change in equity. Thus, preparation

of such accounts will be helpful to communicate the business performance among the external

parties (Johnston and Petacchi, 2017). Stakeholders will have appropriate analysis over the data

base on which they can make investments decisions. Along with this, the internal management of

operations will also become soothing and adequate to the professionals in terms of analysing the

cost reduction opportunities.

Objectives behind preparing the financial reports:

To communicate the business information among internal as well as external stakeholder

with a motive to retaining the adequate growth and brand value in the external market. It musts

be consists of clear and transparent information which are to be disclosed among the

professionals with a motive to have appropriate analysis over the data base (Bonsall IV and et.al.,

2017). Moreover, there are various objectives to the financial reporting such as:

Investment decision-making: The main objective of the financial reports is for decision

making, analysing profitability, liquidity and efficiency of the firm. Users of such information

are basically keen to know the dividend pay-out ratio and the profits retained by the firm in a

year. Therefore, they analyse the organisation on the basis of amount of return is being payable

by them in the business.

Cash flow management: The influences of financial reporting have been enacted in

measuring the performance of the organisation. There will be appropriate ascertainment of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

transactional activities (Cohen, Krishnamoorthy and Wright, 2017). The inflows, outflows of

operating activities will bring outcomes to manage the cash flows of organisation.

Stabilising the financial health: Reporting plays main role in managing the financial

health of the organisation which can have appropriate management and execution of the

operational analysis that will be helpful in meeting the gains of the business. It consists of all

information tat will be helpful to the managers in stabilising the capital structure of the

organisation.

2. Identifying the conceptual and regulatory framework which highlights the purpose and key

principles

The influences of various elements in financial reporting system which in turn will have impacts

on managing the financial stability in the business. Therefore, it can be analysed as:

Conceptual framework: The framework and funnelling agent which helps accounting

professionals in preparing the statements are basically derived from IFRS. There has been

analysis over transactional data base which can bring accurate information among external users

(Đurković, Dmitrović-Šaponja and Đurković, 2017).

Principles: The accounting and reporting techniques which have been impacted by

various boards and institution to guide the professionals in recoding the transactions at the right

place. It includes guidelines generated by GAAP, IASB, IAS and IFRS which are consisted of

internationally accepted accounting principles and guidelines to manage the operations.

Qualitative characteristics: The method of recording transaction and analysing them to

have accurate outcomes which will help businesses in decision making and bringing reforms in

the performance. Comparability, verifiability, understandability and timeliness of disclosing the

financial information among the users are the prime objectives behind preparing financial

reports.

3. Determining the key stakeholder in an organisation and benefits of them in the organisation

There are various stakeholders which are being associated with the business and are

attentive towards obtaining the information relevant with progress, profitability, liquidity and

efficiency of the firm (Ge and et.al., 2018). However, the main users of the financial information

are:

Owner: The owner in an organisation have full rights to know the financial conditions of

the firm. They make investment in the various operations as well as plans for the business

2

operating activities will bring outcomes to manage the cash flows of organisation.

Stabilising the financial health: Reporting plays main role in managing the financial

health of the organisation which can have appropriate management and execution of the

operational analysis that will be helpful in meeting the gains of the business. It consists of all

information tat will be helpful to the managers in stabilising the capital structure of the

organisation.

2. Identifying the conceptual and regulatory framework which highlights the purpose and key

principles

The influences of various elements in financial reporting system which in turn will have impacts

on managing the financial stability in the business. Therefore, it can be analysed as:

Conceptual framework: The framework and funnelling agent which helps accounting

professionals in preparing the statements are basically derived from IFRS. There has been

analysis over transactional data base which can bring accurate information among external users

(Đurković, Dmitrović-Šaponja and Đurković, 2017).

Principles: The accounting and reporting techniques which have been impacted by

various boards and institution to guide the professionals in recoding the transactions at the right

place. It includes guidelines generated by GAAP, IASB, IAS and IFRS which are consisted of

internationally accepted accounting principles and guidelines to manage the operations.

Qualitative characteristics: The method of recording transaction and analysing them to

have accurate outcomes which will help businesses in decision making and bringing reforms in

the performance. Comparability, verifiability, understandability and timeliness of disclosing the

financial information among the users are the prime objectives behind preparing financial

reports.

3. Determining the key stakeholder in an organisation and benefits of them in the organisation

There are various stakeholders which are being associated with the business and are

attentive towards obtaining the information relevant with progress, profitability, liquidity and

efficiency of the firm (Ge and et.al., 2018). However, the main users of the financial information

are:

Owner: The owner in an organisation have full rights to know the financial conditions of

the firm. They make investment in the various operations as well as plans for the business

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

growth which requires them to analyse the financial health and profitability of the business. The

main use of reports for them in terms of decisions making, changing the policies as well as

governing the operational tasks.

Investors: They fetch the information for investment decision making which have

approaches them in analysing the industrial profitability, solvency and efficiency. The ability of

firm in making dividend payment to their potential investors (Call and et.al., 2017).

Government: They use the financial information basically for determining the taxable

payments made by the organisation in the required time period. The transactional statement has

been presented by the organisation on which government seeks for the profitability and the

proportionate payment for taxes have been made by them in a particular period.

4. Determination of the value of financial reporting for meeting industrial growth and objectives

To analyse the financial growth and stability in the business performance there have been

various importance and benefits of such reporting system. the use of such information among

stakeholders have positive influences in enhancing the operational tendency as well as creating

unique identity in the market. it can be articulated as:

The influences of statutes and regulatory governance will help the business in presenting

the accurate financial outcomes among the society.

It governs the professionals in making adequate planning, benchmarking the targets as

well as making appropriate decisions which will improve financial stability in the

organisation.

The purpose of financial reporting in terms of bidding, governmental supplies and labour

contract are aimed at improving the reporting techniques.

5. Preparation of financial statements

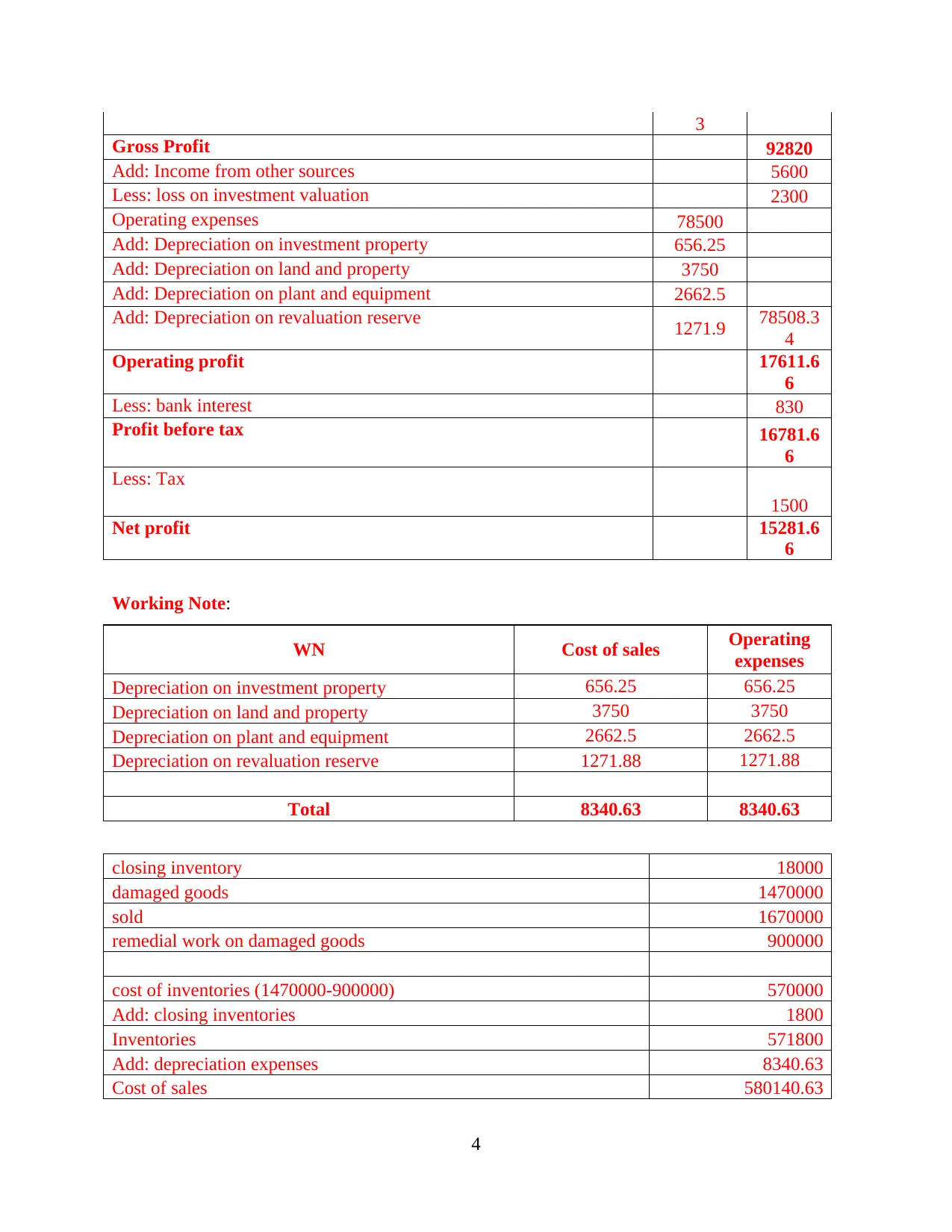

A. Income statement for Godwin Plc:

Income statement

Particulars Details Amount

Revenue 385100

Less: COGS 291700

Less: cost of inventories (1470000-900000) 570000

Add: closing inventories 1800

Inventories 571800

Add: depreciation expenses 8340.63

Cost of sales 580140.6 292280

3

main use of reports for them in terms of decisions making, changing the policies as well as

governing the operational tasks.

Investors: They fetch the information for investment decision making which have

approaches them in analysing the industrial profitability, solvency and efficiency. The ability of

firm in making dividend payment to their potential investors (Call and et.al., 2017).

Government: They use the financial information basically for determining the taxable

payments made by the organisation in the required time period. The transactional statement has

been presented by the organisation on which government seeks for the profitability and the

proportionate payment for taxes have been made by them in a particular period.

4. Determination of the value of financial reporting for meeting industrial growth and objectives

To analyse the financial growth and stability in the business performance there have been

various importance and benefits of such reporting system. the use of such information among

stakeholders have positive influences in enhancing the operational tendency as well as creating

unique identity in the market. it can be articulated as:

The influences of statutes and regulatory governance will help the business in presenting

the accurate financial outcomes among the society.

It governs the professionals in making adequate planning, benchmarking the targets as

well as making appropriate decisions which will improve financial stability in the

organisation.

The purpose of financial reporting in terms of bidding, governmental supplies and labour

contract are aimed at improving the reporting techniques.

5. Preparation of financial statements

A. Income statement for Godwin Plc:

Income statement

Particulars Details Amount

Revenue 385100

Less: COGS 291700

Less: cost of inventories (1470000-900000) 570000

Add: closing inventories 1800

Inventories 571800

Add: depreciation expenses 8340.63

Cost of sales 580140.6 292280

3

3

Gross Profit 92820

Add: Income from other sources 5600

Less: loss on investment valuation 2300

Operating expenses 78500

Add: Depreciation on investment property 656.25

Add: Depreciation on land and property 3750

Add: Depreciation on plant and equipment 2662.5

Add: Depreciation on revaluation reserve 1271.9 78508.3

4

Operating profit 17611.6

6

Less: bank interest 830

Profit before tax 16781.6

6

Less: Tax

1500

Net profit 15281.6

6

Working Note:

WN Cost of sales Operating

expenses

Depreciation on investment property 656.25 656.25

Depreciation on land and property 3750 3750

Depreciation on plant and equipment 2662.5 2662.5

Depreciation on revaluation reserve 1271.88 1271.88

Total 8340.63 8340.63

closing inventory 18000

damaged goods 1470000

sold 1670000

remedial work on damaged goods 900000

cost of inventories (1470000-900000) 570000

Add: closing inventories 1800

Inventories 571800

Add: depreciation expenses 8340.63

Cost of sales 580140.63

4

Gross Profit 92820

Add: Income from other sources 5600

Less: loss on investment valuation 2300

Operating expenses 78500

Add: Depreciation on investment property 656.25

Add: Depreciation on land and property 3750

Add: Depreciation on plant and equipment 2662.5

Add: Depreciation on revaluation reserve 1271.9 78508.3

4

Operating profit 17611.6

6

Less: bank interest 830

Profit before tax 16781.6

6

Less: Tax

1500

Net profit 15281.6

6

Working Note:

WN Cost of sales Operating

expenses

Depreciation on investment property 656.25 656.25

Depreciation on land and property 3750 3750

Depreciation on plant and equipment 2662.5 2662.5

Depreciation on revaluation reserve 1271.88 1271.88

Total 8340.63 8340.63

closing inventory 18000

damaged goods 1470000

sold 1670000

remedial work on damaged goods 900000

cost of inventories (1470000-900000) 570000

Add: closing inventories 1800

Inventories 571800

Add: depreciation expenses 8340.63

Cost of sales 580140.63

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

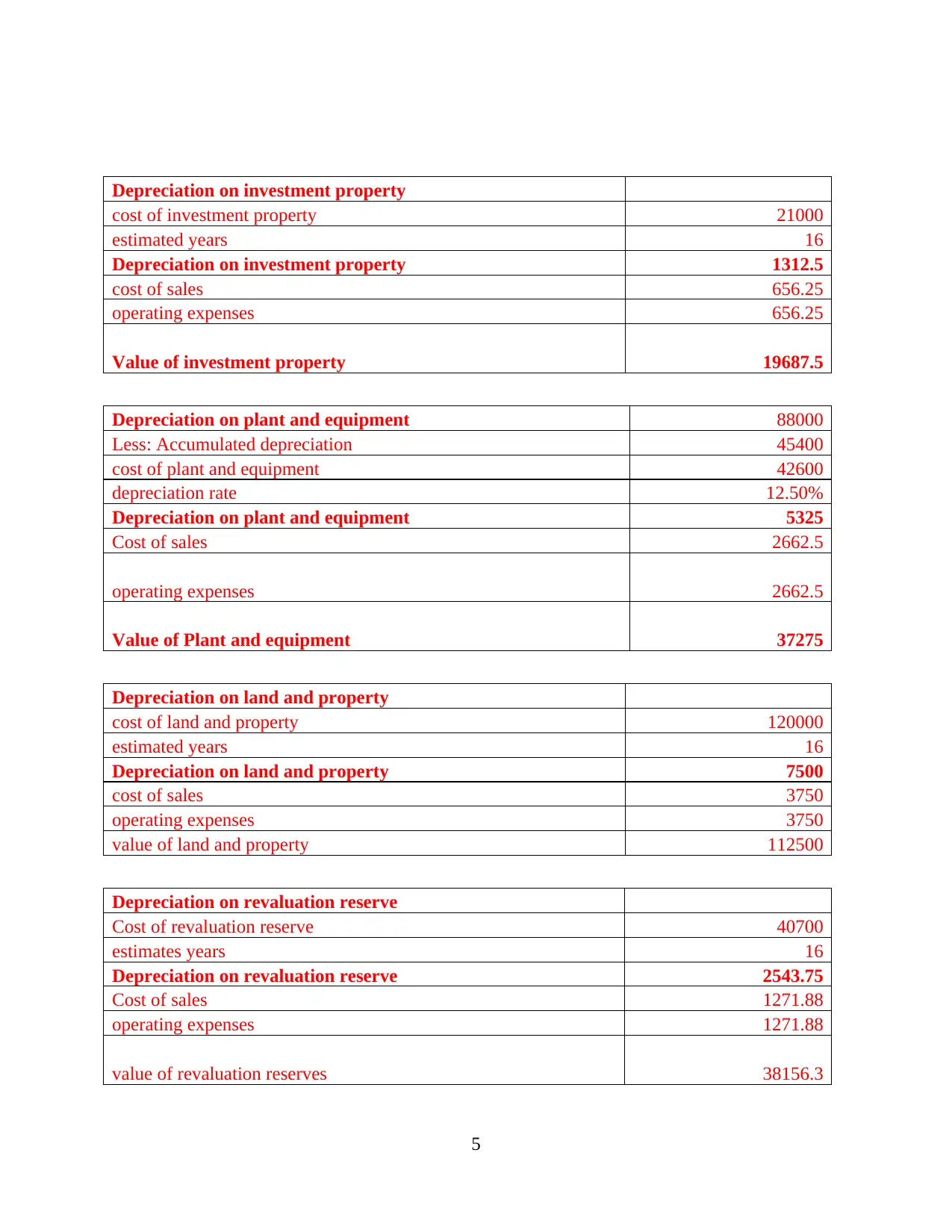

Depreciation on investment property

cost of investment property 21000

estimated years 16

Depreciation on investment property 1312.5

cost of sales 656.25

operating expenses 656.25

Value of investment property 19687.5

Depreciation on plant and equipment 88000

Less: Accumulated depreciation 45400

cost of plant and equipment 42600

depreciation rate 12.50%

Depreciation on plant and equipment 5325

Cost of sales 2662.5

operating expenses 2662.5

Value of Plant and equipment 37275

Depreciation on land and property

cost of land and property 120000

estimated years 16

Depreciation on land and property 7500

cost of sales 3750

operating expenses 3750

value of land and property 112500

Depreciation on revaluation reserve

Cost of revaluation reserve 40700

estimates years 16

Depreciation on revaluation reserve 2543.75

Cost of sales 1271.88

operating expenses 1271.88

value of revaluation reserves 38156.3

5

cost of investment property 21000

estimated years 16

Depreciation on investment property 1312.5

cost of sales 656.25

operating expenses 656.25

Value of investment property 19687.5

Depreciation on plant and equipment 88000

Less: Accumulated depreciation 45400

cost of plant and equipment 42600

depreciation rate 12.50%

Depreciation on plant and equipment 5325

Cost of sales 2662.5

operating expenses 2662.5

Value of Plant and equipment 37275

Depreciation on land and property

cost of land and property 120000

estimated years 16

Depreciation on land and property 7500

cost of sales 3750

operating expenses 3750

value of land and property 112500

Depreciation on revaluation reserve

Cost of revaluation reserve 40700

estimates years 16

Depreciation on revaluation reserve 2543.75

Cost of sales 1271.88

operating expenses 1271.88

value of revaluation reserves 38156.3

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

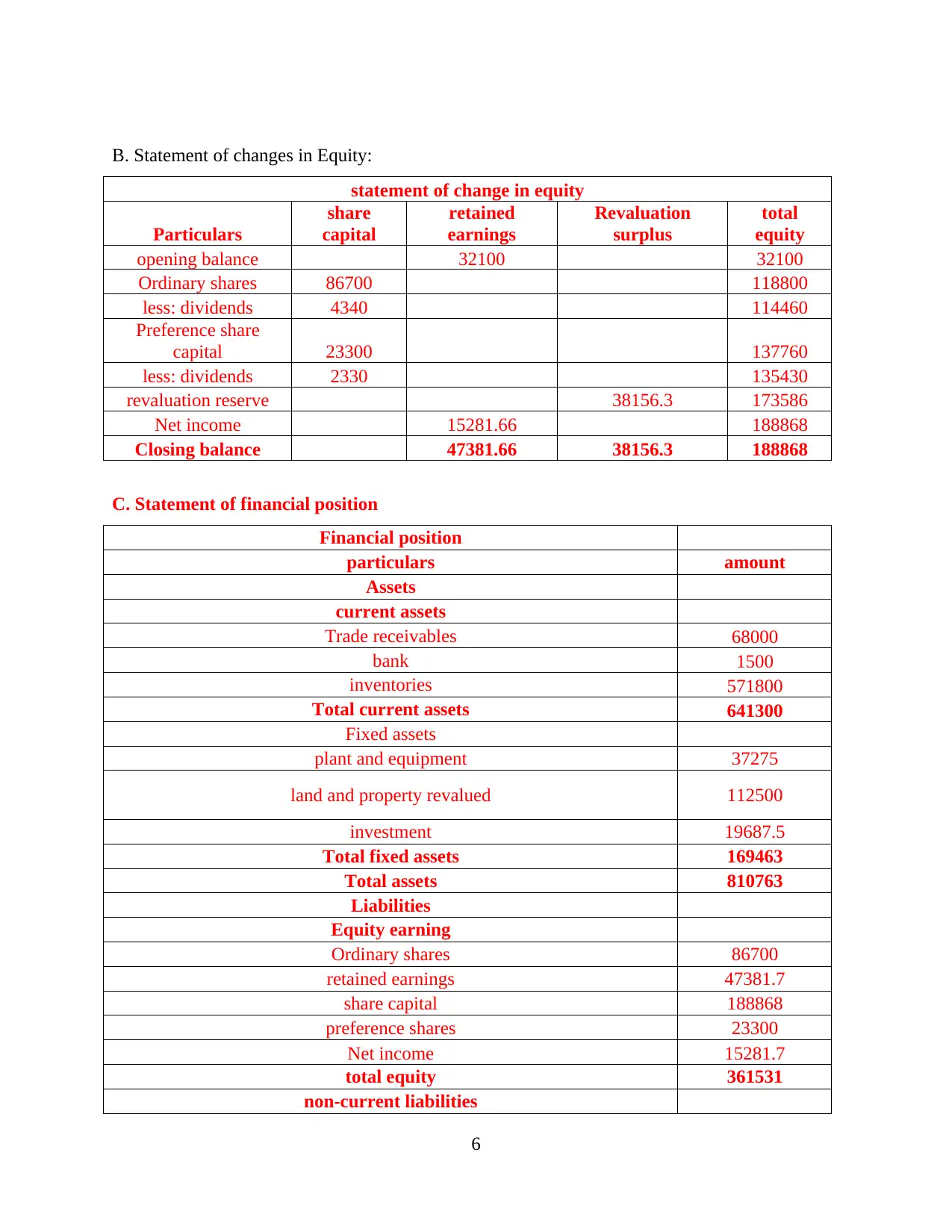

B. Statement of changes in Equity:

statement of change in equity

Particulars

share

capital

retained

earnings

Revaluation

surplus

total

equity

opening balance 32100 32100

Ordinary shares 86700 118800

less: dividends 4340 114460

Preference share

capital 23300 137760

less: dividends 2330 135430

revaluation reserve 38156.3 173586

Net income 15281.66 188868

Closing balance 47381.66 38156.3 188868

C. Statement of financial position

Financial position

particulars amount

Assets

current assets

Trade receivables 68000

bank 1500

inventories 571800

Total current assets 641300

Fixed assets

plant and equipment 37275

land and property revalued 112500

investment 19687.5

Total fixed assets 169463

Total assets 810763

Liabilities

Equity earning

Ordinary shares 86700

retained earnings 47381.7

share capital 188868

preference shares 23300

Net income 15281.7

total equity 361531

non-current liabilities

6

statement of change in equity

Particulars

share

capital

retained

earnings

Revaluation

surplus

total

equity

opening balance 32100 32100

Ordinary shares 86700 118800

less: dividends 4340 114460

Preference share

capital 23300 137760

less: dividends 2330 135430

revaluation reserve 38156.3 173586

Net income 15281.66 188868

Closing balance 47381.66 38156.3 188868

C. Statement of financial position

Financial position

particulars amount

Assets

current assets

Trade receivables 68000

bank 1500

inventories 571800

Total current assets 641300

Fixed assets

plant and equipment 37275

land and property revalued 112500

investment 19687.5

Total fixed assets 169463

Total assets 810763

Liabilities

Equity earning

Ordinary shares 86700

retained earnings 47381.7

share capital 188868

preference shares 23300

Net income 15281.7

total equity 361531

non-current liabilities

6

deferred income tax 8900

revaluation reserve 38156.3

total non-current liabilities 47056.3

current liabilities

trade payables 385100

Provision for tax 17076

total current liabilities 402175

Total liabilities 810763

D. Types of information used in cash flow statement

There has been use of various information in a cash flow statement that were listed in the

income statement. In cash flow statement there has been use of income and expenditure

information which will be used in the statements. On the other side, as per considering the

information used in statement of changes in equity on which there have been ascertainment of

capital invested in the business. Thus, cash also have transaction based on investing activities.

6. Interpretation of ratios of FTSE 100 index companies

Just Eat PLC Kingfisher PLC

Particulars Formula 2016 2017 2016 2017

Profitability ratios

Gross profit ratio

(in %) Gross profit / Revenue *100 90.6 82.4 37.3 37.2

Net profit ratio (in

%) Net profit / Revenue *100 19.08 -18.8 3.95 5.43

Return on Assets

(ROA) (in %) Net profit / Assets * 100 7.9 -9.96 4.25 6.12

Return on Equity

(ROE) (in %) Net profit / Stockholders' Equity 9.93 -13.37 6.64 9.42

Liquidity Ratios

Current ratio Current assets / Current liabilities 1.05 1.18 1.28 1.3

Quick ratio Liquid Assets / Current liabilities 0.73 0.89 0.47 0.44

Efficiency Ratios

Inventory ratio

Cost of goods manufactured /

Average inventory 24.28 42.67 3.29 3.41

Receivables

turnover ratio Credit sales / Average receivables 221 260.14 184.8 190.25

Payables turnover

ratio

Credit purchases / Average

payables 553.2 222.04 75.43 71.71

7

revaluation reserve 38156.3

total non-current liabilities 47056.3

current liabilities

trade payables 385100

Provision for tax 17076

total current liabilities 402175

Total liabilities 810763

D. Types of information used in cash flow statement

There has been use of various information in a cash flow statement that were listed in the

income statement. In cash flow statement there has been use of income and expenditure

information which will be used in the statements. On the other side, as per considering the

information used in statement of changes in equity on which there have been ascertainment of

capital invested in the business. Thus, cash also have transaction based on investing activities.

6. Interpretation of ratios of FTSE 100 index companies

Just Eat PLC Kingfisher PLC

Particulars Formula 2016 2017 2016 2017

Profitability ratios

Gross profit ratio

(in %) Gross profit / Revenue *100 90.6 82.4 37.3 37.2

Net profit ratio (in

%) Net profit / Revenue *100 19.08 -18.8 3.95 5.43

Return on Assets

(ROA) (in %) Net profit / Assets * 100 7.9 -9.96 4.25 6.12

Return on Equity

(ROE) (in %) Net profit / Stockholders' Equity 9.93 -13.37 6.64 9.42

Liquidity Ratios

Current ratio Current assets / Current liabilities 1.05 1.18 1.28 1.3

Quick ratio Liquid Assets / Current liabilities 0.73 0.89 0.47 0.44

Efficiency Ratios

Inventory ratio

Cost of goods manufactured /

Average inventory 24.28 42.67 3.29 3.41

Receivables

turnover ratio Credit sales / Average receivables 221 260.14 184.8 190.25

Payables turnover

ratio

Credit purchases / Average

payables 553.2 222.04 75.43 71.71

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

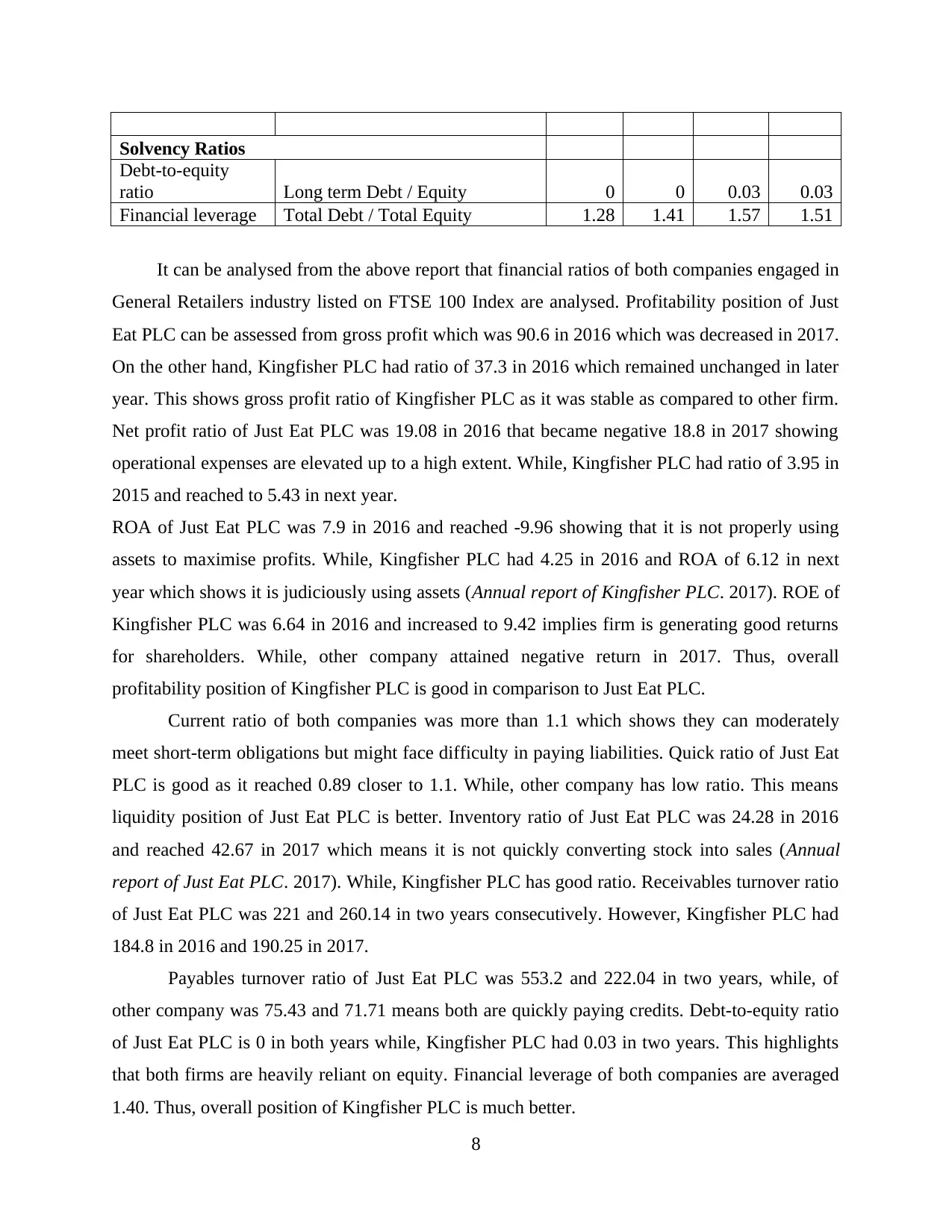

Solvency Ratios

Debt-to-equity

ratio Long term Debt / Equity 0 0 0.03 0.03

Financial leverage Total Debt / Total Equity 1.28 1.41 1.57 1.51

It can be analysed from the above report that financial ratios of both companies engaged in

General Retailers industry listed on FTSE 100 Index are analysed. Profitability position of Just

Eat PLC can be assessed from gross profit which was 90.6 in 2016 which was decreased in 2017.

On the other hand, Kingfisher PLC had ratio of 37.3 in 2016 which remained unchanged in later

year. This shows gross profit ratio of Kingfisher PLC as it was stable as compared to other firm.

Net profit ratio of Just Eat PLC was 19.08 in 2016 that became negative 18.8 in 2017 showing

operational expenses are elevated up to a high extent. While, Kingfisher PLC had ratio of 3.95 in

2015 and reached to 5.43 in next year.

ROA of Just Eat PLC was 7.9 in 2016 and reached -9.96 showing that it is not properly using

assets to maximise profits. While, Kingfisher PLC had 4.25 in 2016 and ROA of 6.12 in next

year which shows it is judiciously using assets (Annual report of Kingfisher PLC. 2017). ROE of

Kingfisher PLC was 6.64 in 2016 and increased to 9.42 implies firm is generating good returns

for shareholders. While, other company attained negative return in 2017. Thus, overall

profitability position of Kingfisher PLC is good in comparison to Just Eat PLC.

Current ratio of both companies was more than 1.1 which shows they can moderately

meet short-term obligations but might face difficulty in paying liabilities. Quick ratio of Just Eat

PLC is good as it reached 0.89 closer to 1.1. While, other company has low ratio. This means

liquidity position of Just Eat PLC is better. Inventory ratio of Just Eat PLC was 24.28 in 2016

and reached 42.67 in 2017 which means it is not quickly converting stock into sales (Annual

report of Just Eat PLC. 2017). While, Kingfisher PLC has good ratio. Receivables turnover ratio

of Just Eat PLC was 221 and 260.14 in two years consecutively. However, Kingfisher PLC had

184.8 in 2016 and 190.25 in 2017.

Payables turnover ratio of Just Eat PLC was 553.2 and 222.04 in two years, while, of

other company was 75.43 and 71.71 means both are quickly paying credits. Debt-to-equity ratio

of Just Eat PLC is 0 in both years while, Kingfisher PLC had 0.03 in two years. This highlights

that both firms are heavily reliant on equity. Financial leverage of both companies are averaged

1.40. Thus, overall position of Kingfisher PLC is much better.

8

Debt-to-equity

ratio Long term Debt / Equity 0 0 0.03 0.03

Financial leverage Total Debt / Total Equity 1.28 1.41 1.57 1.51

It can be analysed from the above report that financial ratios of both companies engaged in

General Retailers industry listed on FTSE 100 Index are analysed. Profitability position of Just

Eat PLC can be assessed from gross profit which was 90.6 in 2016 which was decreased in 2017.

On the other hand, Kingfisher PLC had ratio of 37.3 in 2016 which remained unchanged in later

year. This shows gross profit ratio of Kingfisher PLC as it was stable as compared to other firm.

Net profit ratio of Just Eat PLC was 19.08 in 2016 that became negative 18.8 in 2017 showing

operational expenses are elevated up to a high extent. While, Kingfisher PLC had ratio of 3.95 in

2015 and reached to 5.43 in next year.

ROA of Just Eat PLC was 7.9 in 2016 and reached -9.96 showing that it is not properly using

assets to maximise profits. While, Kingfisher PLC had 4.25 in 2016 and ROA of 6.12 in next

year which shows it is judiciously using assets (Annual report of Kingfisher PLC. 2017). ROE of

Kingfisher PLC was 6.64 in 2016 and increased to 9.42 implies firm is generating good returns

for shareholders. While, other company attained negative return in 2017. Thus, overall

profitability position of Kingfisher PLC is good in comparison to Just Eat PLC.

Current ratio of both companies was more than 1.1 which shows they can moderately

meet short-term obligations but might face difficulty in paying liabilities. Quick ratio of Just Eat

PLC is good as it reached 0.89 closer to 1.1. While, other company has low ratio. This means

liquidity position of Just Eat PLC is better. Inventory ratio of Just Eat PLC was 24.28 in 2016

and reached 42.67 in 2017 which means it is not quickly converting stock into sales (Annual

report of Just Eat PLC. 2017). While, Kingfisher PLC has good ratio. Receivables turnover ratio

of Just Eat PLC was 221 and 260.14 in two years consecutively. However, Kingfisher PLC had

184.8 in 2016 and 190.25 in 2017.

Payables turnover ratio of Just Eat PLC was 553.2 and 222.04 in two years, while, of

other company was 75.43 and 71.71 means both are quickly paying credits. Debt-to-equity ratio

of Just Eat PLC is 0 in both years while, Kingfisher PLC had 0.03 in two years. This highlights

that both firms are heavily reliant on equity. Financial leverage of both companies are averaged

1.40. Thus, overall position of Kingfisher PLC is much better.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

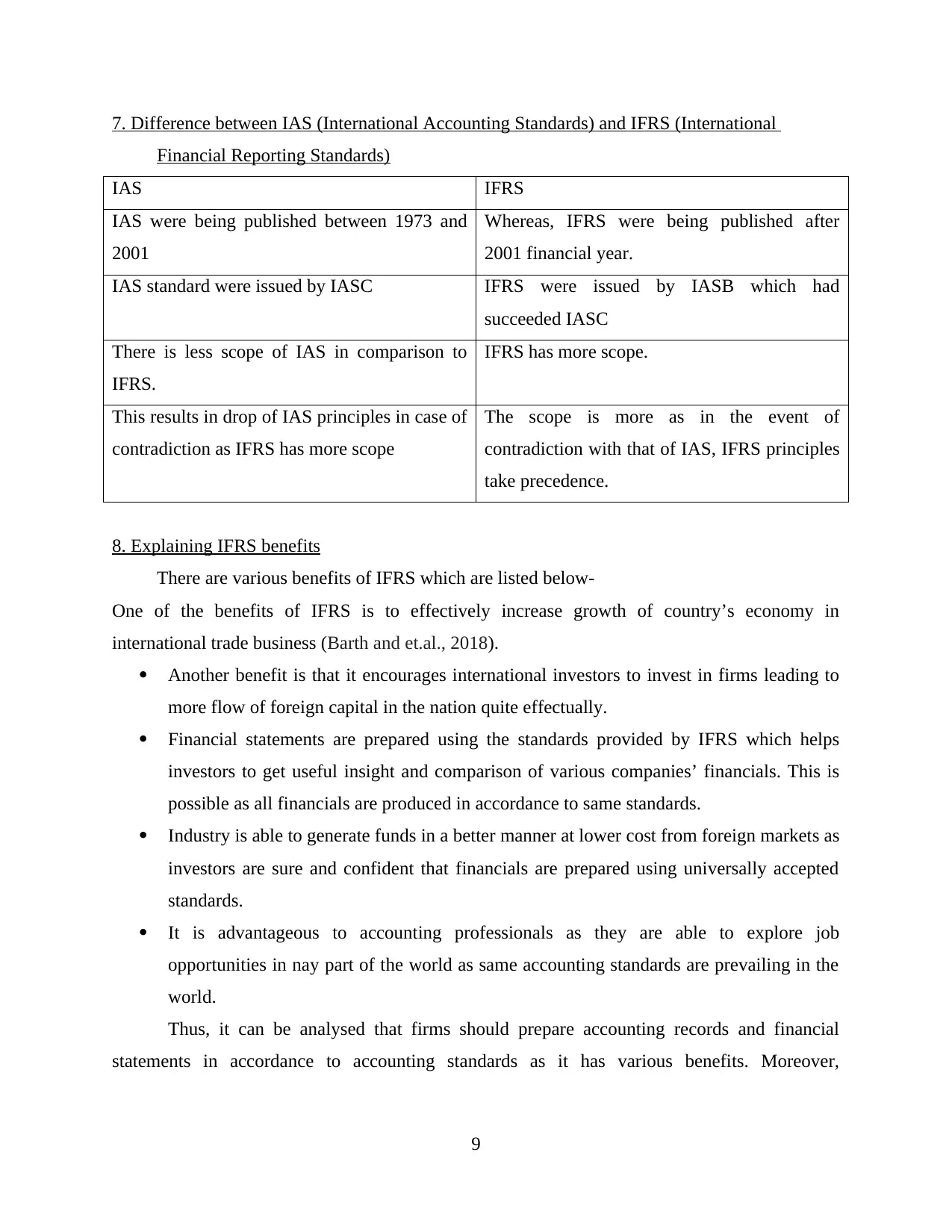

7. Difference between IAS (International Accounting Standards) and IFRS (International

Financial Reporting Standards)

IAS IFRS

IAS were being published between 1973 and

2001

Whereas, IFRS were being published after

2001 financial year.

IAS standard were issued by IASC IFRS were issued by IASB which had

succeeded IASC

There is less scope of IAS in comparison to

IFRS.

IFRS has more scope.

This results in drop of IAS principles in case of

contradiction as IFRS has more scope

The scope is more as in the event of

contradiction with that of IAS, IFRS principles

take precedence.

8. Explaining IFRS benefits

There are various benefits of IFRS which are listed below-

One of the benefits of IFRS is to effectively increase growth of country’s economy in

international trade business (Barth and et.al., 2018).

Another benefit is that it encourages international investors to invest in firms leading to

more flow of foreign capital in the nation quite effectually.

Financial statements are prepared using the standards provided by IFRS which helps

investors to get useful insight and comparison of various companies’ financials. This is

possible as all financials are produced in accordance to same standards.

Industry is able to generate funds in a better manner at lower cost from foreign markets as

investors are sure and confident that financials are prepared using universally accepted

standards.

It is advantageous to accounting professionals as they are able to explore job

opportunities in nay part of the world as same accounting standards are prevailing in the

world.

Thus, it can be analysed that firms should prepare accounting records and financial

statements in accordance to accounting standards as it has various benefits. Moreover,

9

Financial Reporting Standards)

IAS IFRS

IAS were being published between 1973 and

2001

Whereas, IFRS were being published after

2001 financial year.

IAS standard were issued by IASC IFRS were issued by IASB which had

succeeded IASC

There is less scope of IAS in comparison to

IFRS.

IFRS has more scope.

This results in drop of IAS principles in case of

contradiction as IFRS has more scope

The scope is more as in the event of

contradiction with that of IAS, IFRS principles

take precedence.

8. Explaining IFRS benefits

There are various benefits of IFRS which are listed below-

One of the benefits of IFRS is to effectively increase growth of country’s economy in

international trade business (Barth and et.al., 2018).

Another benefit is that it encourages international investors to invest in firms leading to

more flow of foreign capital in the nation quite effectually.

Financial statements are prepared using the standards provided by IFRS which helps

investors to get useful insight and comparison of various companies’ financials. This is

possible as all financials are produced in accordance to same standards.

Industry is able to generate funds in a better manner at lower cost from foreign markets as

investors are sure and confident that financials are prepared using universally accepted

standards.

It is advantageous to accounting professionals as they are able to explore job

opportunities in nay part of the world as same accounting standards are prevailing in the

world.

Thus, it can be analysed that firms should prepare accounting records and financial

statements in accordance to accounting standards as it has various benefits. Moreover,

9

transparency and reliability of the data helps investors and other stakeholders of company to take

best decisions which are of their interest. Hence, IFRS has widespread benefits.

9. Varying degree of compliance with IFRS by world organisations and how they impact on

nation

The accounting standards as provided by the IFRS are widely accepted on a global level

(Pownall and Wieczynska, 2018). The multinational firms are required to effectively abide by

the laws and standards provided by IFRS so that transparent and accurate financial performance

may be highlighted in the best manner possible of company with ease. This is required so that

investors may take informed decisions by seeking financial statements such as cash flow

statement, income statement and balance sheet quite effectually.

IFRS has varying degree of compliance which has to be followed by the firms for

attaining liquidity in the best manner possible. It can be analysed that the level of compliance is

an assurance to investors that information they are seeking are accurate in every manner and no

manipulation is done with reference to it. This helps them to take sound decisions and it benefits

them as financial statements prepared by complying with IFRS are reliable to make decisions.

On the other hand, national standards have to be boycotted in order to have similar accuracy

which help investors for seeking information. Thus, varying degree of compliance has to be

complied with that of nation so that reliable information may be revealed to stakeholders.

CONCLUSION

Hereby it can be concluded that financial reporting is crucial task to be done by management

of company not for highlighting its performance and take decisions accordingly. But is also

important for stakeholders who have concern about earnings and prospectus of business up to a

high extent. The outcome that can be generated from report is that financial regulations and

framework as governed by IFRS are of great importance to firms and complying with the same

increases transparency of performance of firm to shareholders. Furthermore, ratio analysis helps

to assess overall financial health of two listed companies taken i.e. Just Eat PLC and Kingfisher

PLC. Thus, financial reporting is much essential for stakeholders.

10

best decisions which are of their interest. Hence, IFRS has widespread benefits.

9. Varying degree of compliance with IFRS by world organisations and how they impact on

nation

The accounting standards as provided by the IFRS are widely accepted on a global level

(Pownall and Wieczynska, 2018). The multinational firms are required to effectively abide by

the laws and standards provided by IFRS so that transparent and accurate financial performance

may be highlighted in the best manner possible of company with ease. This is required so that

investors may take informed decisions by seeking financial statements such as cash flow

statement, income statement and balance sheet quite effectually.

IFRS has varying degree of compliance which has to be followed by the firms for

attaining liquidity in the best manner possible. It can be analysed that the level of compliance is

an assurance to investors that information they are seeking are accurate in every manner and no

manipulation is done with reference to it. This helps them to take sound decisions and it benefits

them as financial statements prepared by complying with IFRS are reliable to make decisions.

On the other hand, national standards have to be boycotted in order to have similar accuracy

which help investors for seeking information. Thus, varying degree of compliance has to be

complied with that of nation so that reliable information may be revealed to stakeholders.

CONCLUSION

Hereby it can be concluded that financial reporting is crucial task to be done by management

of company not for highlighting its performance and take decisions accordingly. But is also

important for stakeholders who have concern about earnings and prospectus of business up to a

high extent. The outcome that can be generated from report is that financial regulations and

framework as governed by IFRS are of great importance to firms and complying with the same

increases transparency of performance of firm to shareholders. Furthermore, ratio analysis helps

to assess overall financial health of two listed companies taken i.e. Just Eat PLC and Kingfisher

PLC. Thus, financial reporting is much essential for stakeholders.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.