Accounting 15 Assignment: Financial Accounting Concepts

VerifiedAdded on 2020/03/16

|13

|1686

|37

Homework Assignment

AI Summary

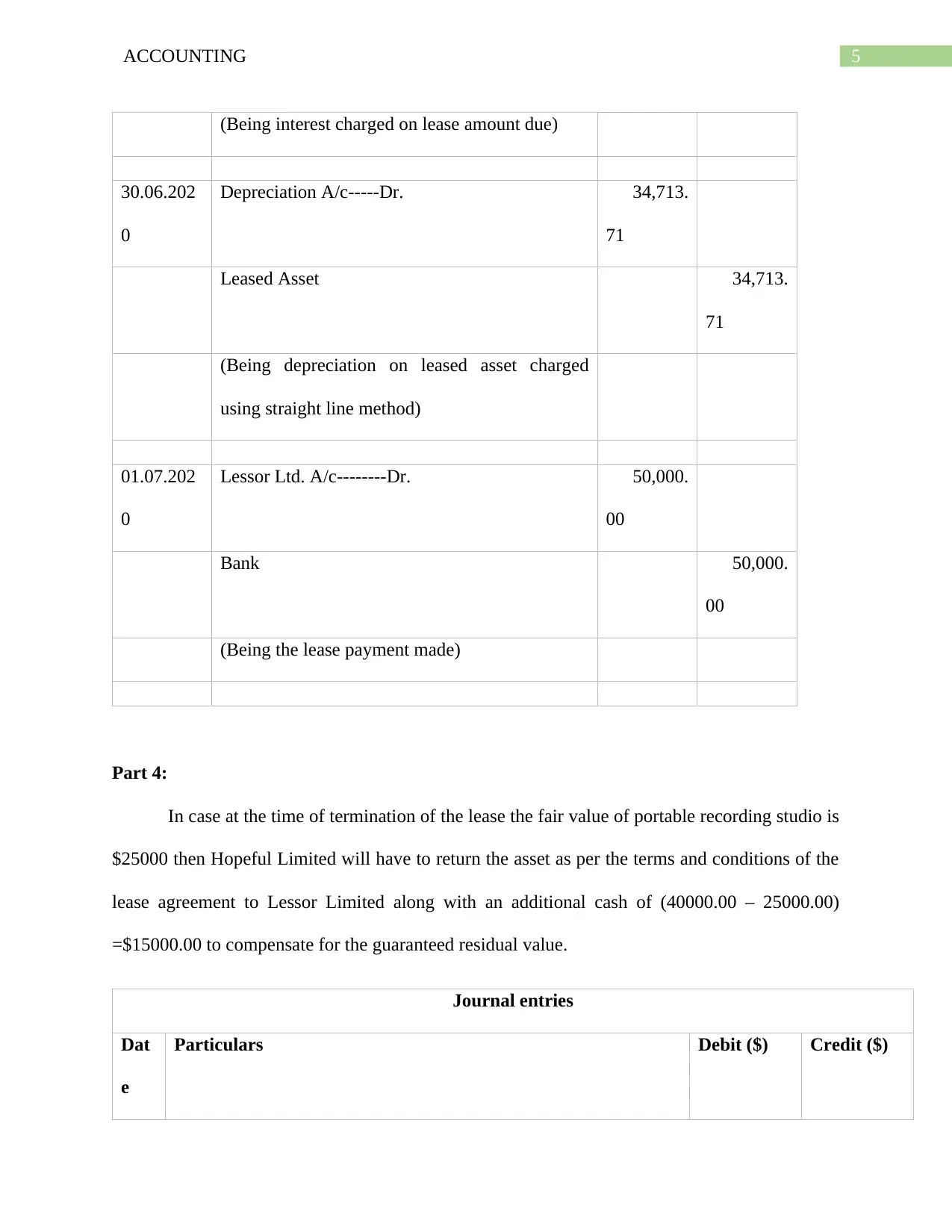

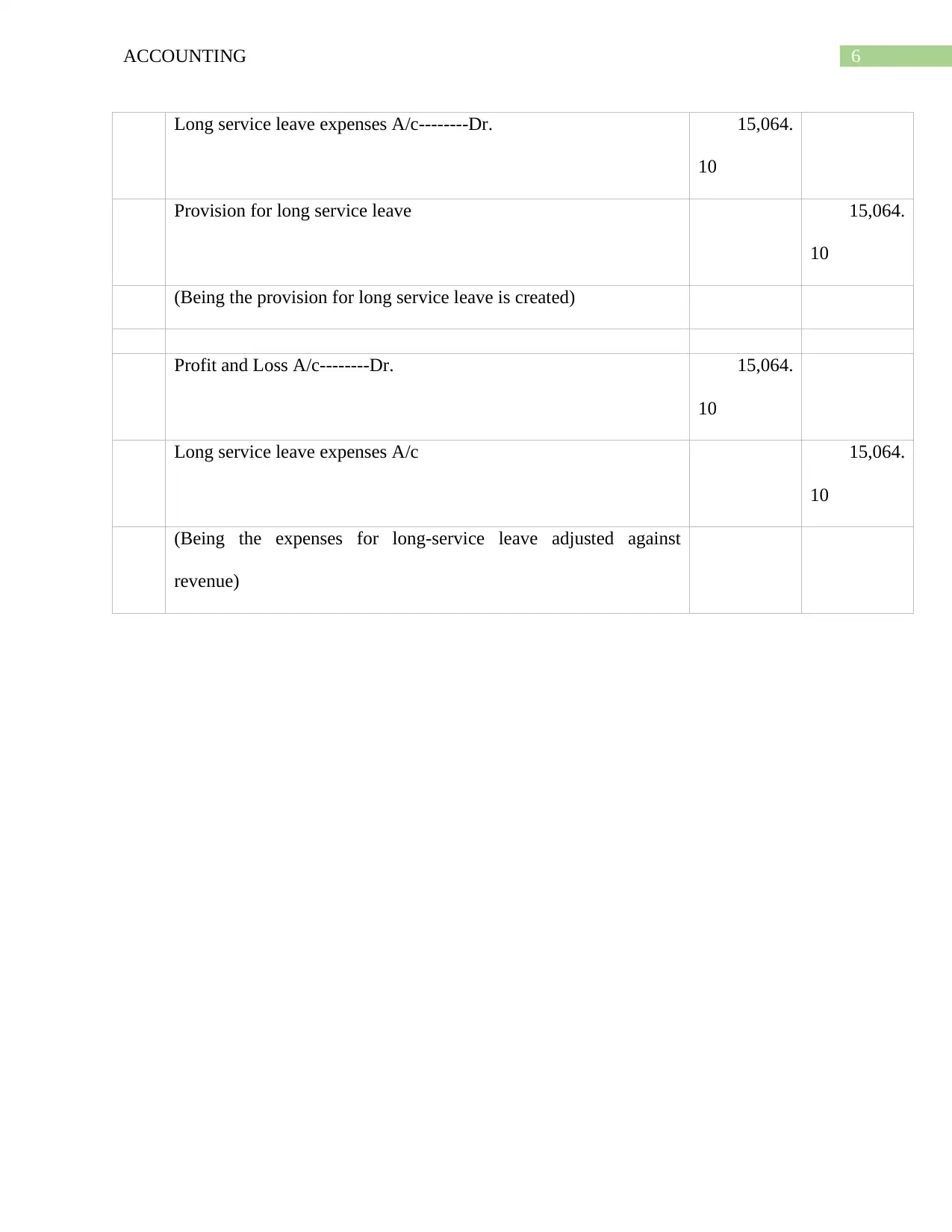

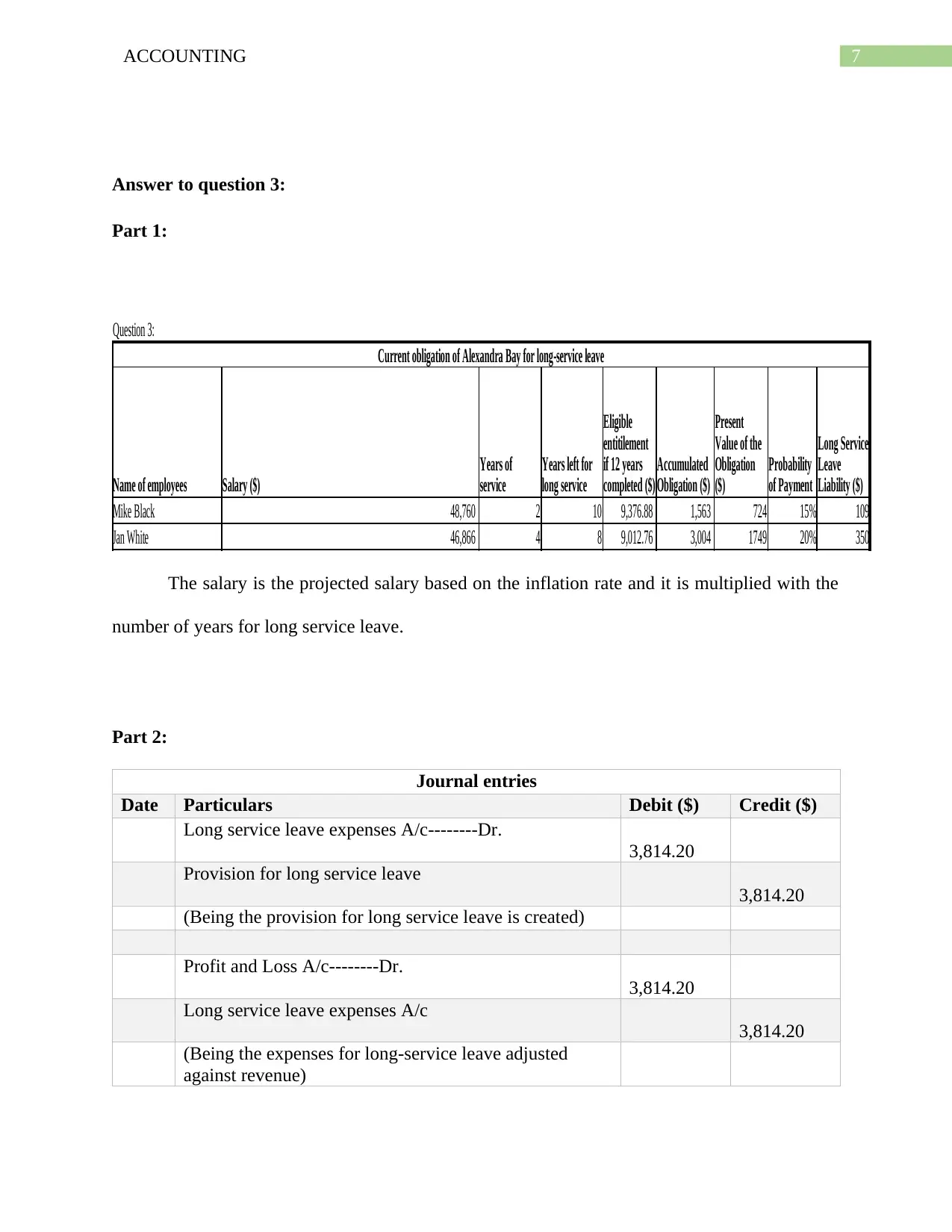

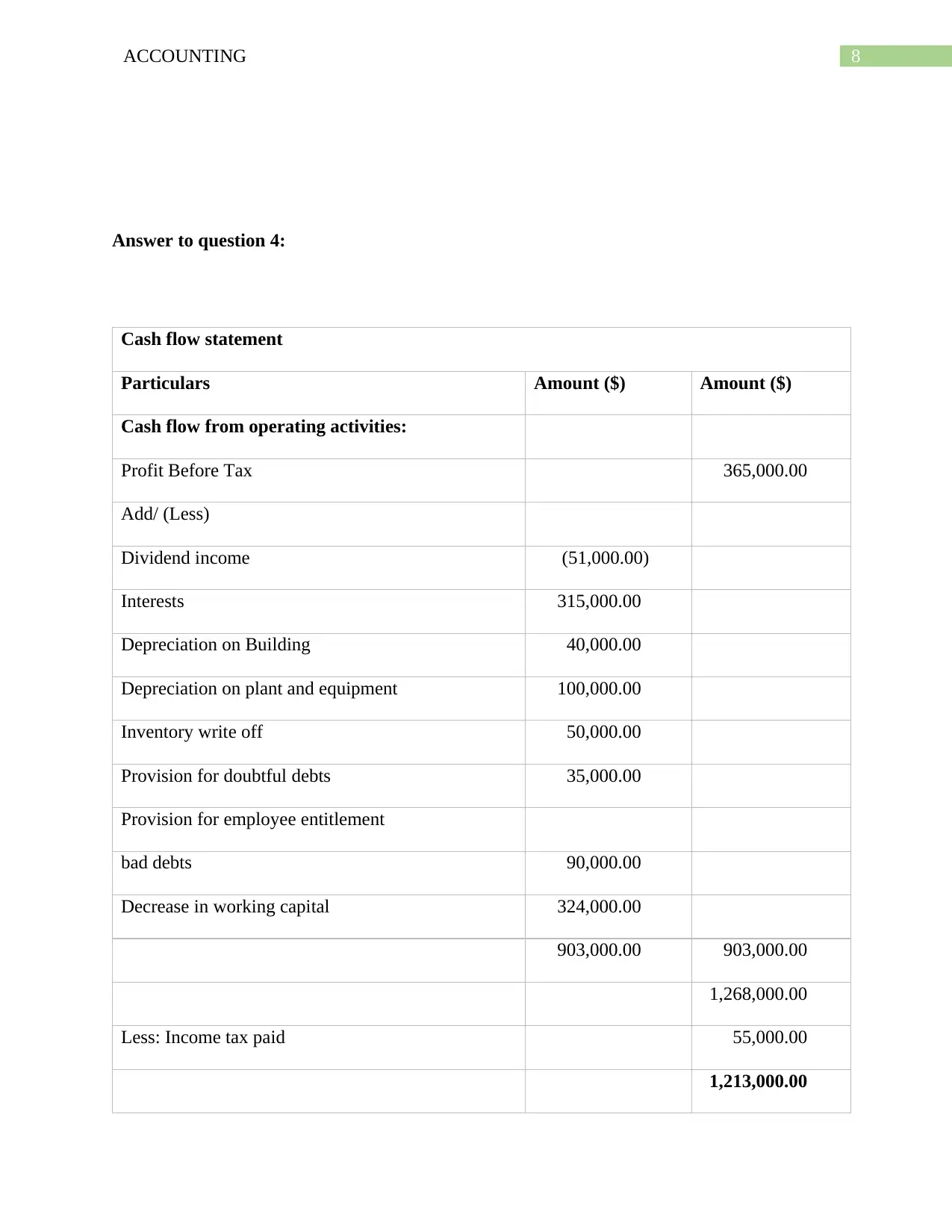

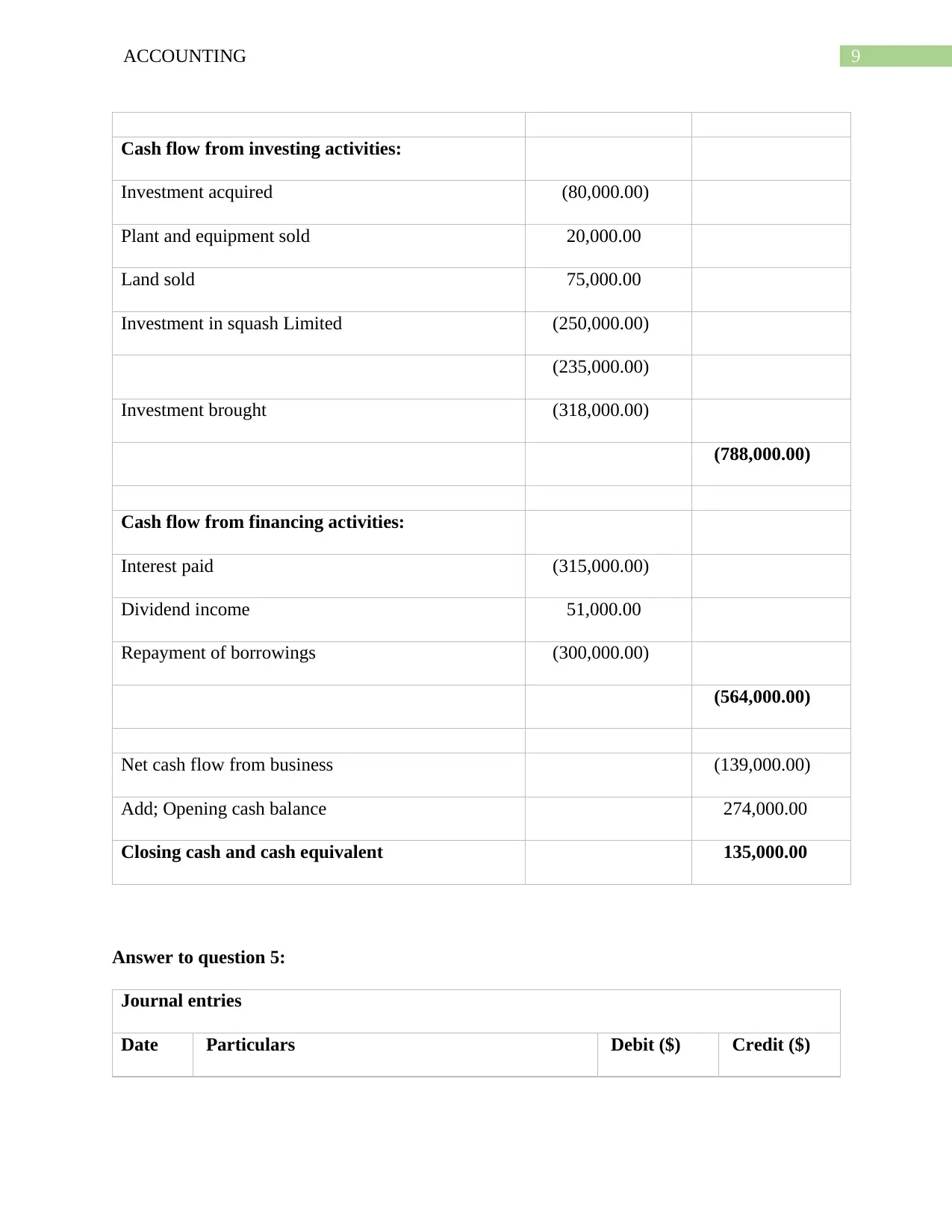

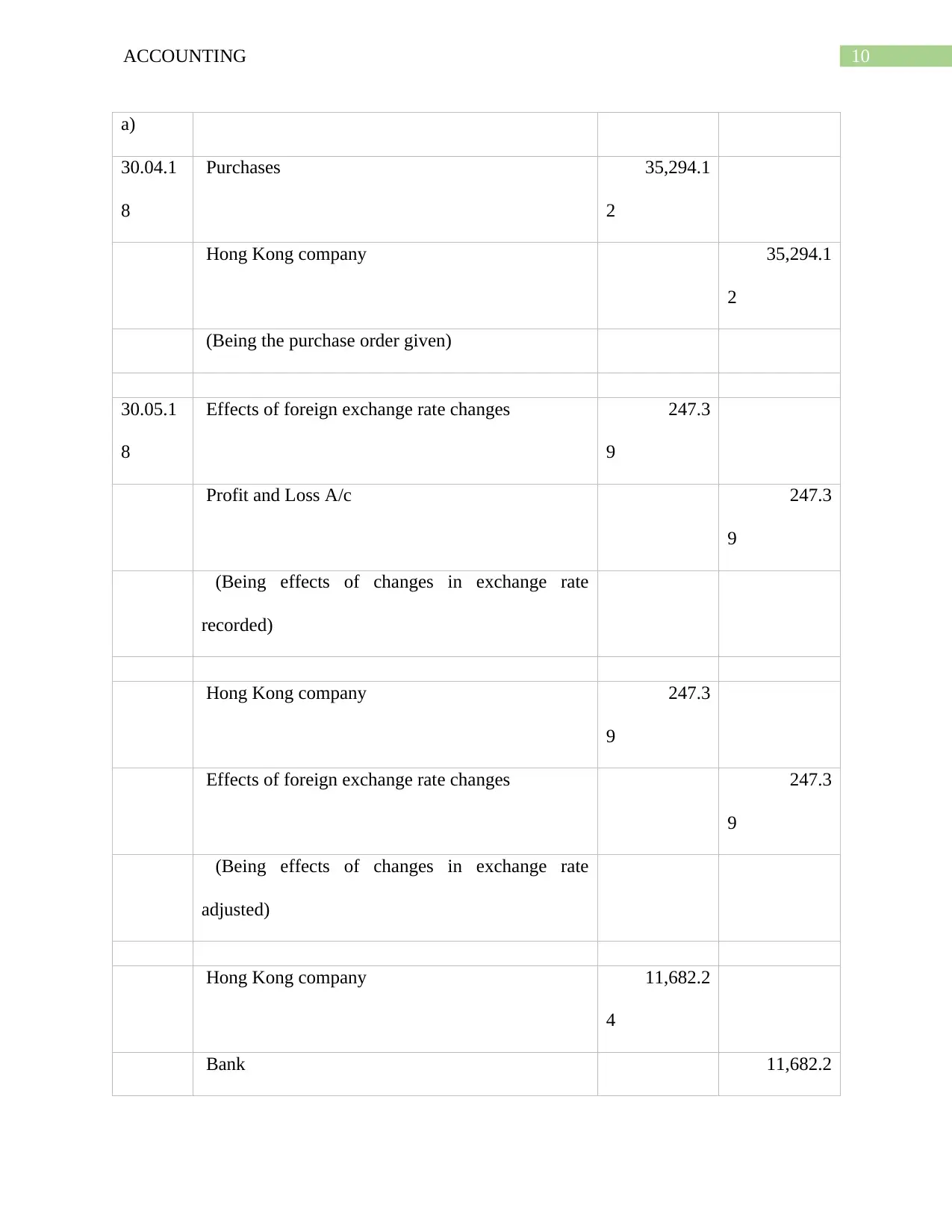

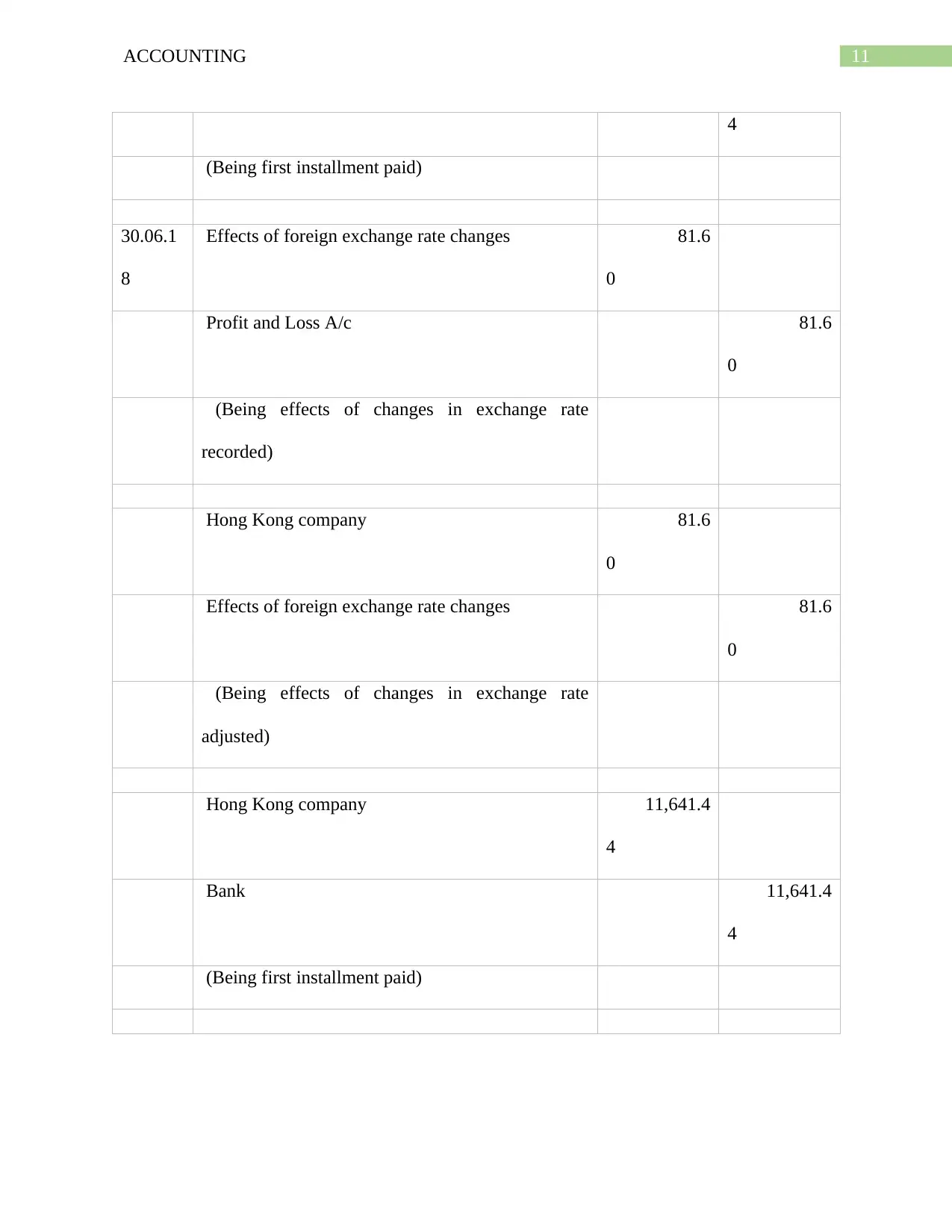

This accounting assignment solution addresses several key areas of financial accounting. It begins by discussing the importance of annual reports and the accounting treatment of litigation settlements, including journal entries and financial statement presentation. The assignment then delves into lease accounting, calculating the fair value of a recording studio, creating amortization schedules, and preparing journal entries for lease transactions, including the impact of a guaranteed residual value. Further, the solution covers long service leave calculations and journal entries. A cash flow statement is prepared, detailing cash flows from operating, investing, and financing activities. Finally, the assignment tackles foreign exchange transactions, preparing journal entries to account for currency fluctuations on purchases, engine contracts, and hedging activities. The solution concludes with a reference list of relevant accounting literature.

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.