Financial Reporting: Analysis of Standards, Stakeholders, and Theories

VerifiedAdded on 2021/01/01

|15

|4053

|96

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, starting with its context and purpose within the business world. It delves into the conceptual and regulatory frameworks, including the roles of key bodies like IASB and IFRIC, and explains the key accounting principles such as going concern and accruals. The report identifies and examines the needs of various stakeholders, including employees, customers, investors, and governments, and analyzes how financial reporting supports organizational objectives and growth. It then explains international accounting standards (IAS) and international financial reporting standards (IFRS), highlighting their benefits and evaluating the degree of compliance with IFRS by different organizations. Finally, the report explores the differences in financial reporting across the world and evaluates the use of appropriate theories and models to understand financial reporting practices. The report uses the accounting firm Arnold Hill & Co. as an example throughout.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Analysing context and purpose of financial reporting............................................................1

2. Explanation on conceptual and regulatory framework of financial reporting with principle

to assess its requirement..............................................................................................................2

3. Identification of key stakeholder of organisation and their need for financial reports...........6

4. Analysing value of financial reporting for meeting organisational objectives and growth....7

5. Explanation on international accounting standards and international financial reporting

standards with their benefits........................................................................................................8

6. Evaluation of financial reporting with appropriate theories and models................................9

7. Identifying differences in financial reporting across the world with the evaluation of

differences.................................................................................................................................10

8. Evaluating degree of compliance with IFRS by different organisations across the world...11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Analysing context and purpose of financial reporting............................................................1

2. Explanation on conceptual and regulatory framework of financial reporting with principle

to assess its requirement..............................................................................................................2

3. Identification of key stakeholder of organisation and their need for financial reports...........6

4. Analysing value of financial reporting for meeting organisational objectives and growth....7

5. Explanation on international accounting standards and international financial reporting

standards with their benefits........................................................................................................8

6. Evaluation of financial reporting with appropriate theories and models................................9

7. Identifying differences in financial reporting across the world with the evaluation of

differences.................................................................................................................................10

8. Evaluating degree of compliance with IFRS by different organisations across the world...11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

In order to analyse functioning and day to day operations of multiple departments of the

organisation, financial reporting plays an important role. It is the tool which such multiple

operation through reporting in documents of the company (Kimmel and et.al., 2016). Thus, this

assessment will develop to provide better understanding and purpose of financial reporting.

Chosen reputed accounting firm in this report is Arnold Hill & Co. which deals in providing

financial and legal services to clients. Further, conceptual and regulatory framework of this

accounting will also to be explained by analysing key stakeholder and their need for financial

reporting.

Moreover, explanation will also to be provided on international accounting standards and

international financial reporting standards with its degree of compliance across the nation.

Lastly, in this report through models and theories better understanding relates to financial

reporting will be developed.

MAIN BODY

1. Analysing context and purpose of financial reporting

Financial reporting is considered as vital term which plays an important role in the world

of economies. Main purpose of this accounting is to provide information which is relevant and

useful for owners and stakeholders of the organisation. This is the way of showing financial

ability of company in market among shareholders (Henderson and et.al., 2015). Thus, context of

this reporting is to comply with regulatory frameworks while preparing financial statements of

the company. Its governance includes duties and responsible of officer where manager is

responsible for preparing financial statement and business operation of company and director is

responsible to oversee such method which adopted by management for preparing such

statements.

Therefore, it can be said that in order to show efficiency and effectiveness of company

and to capture more investors, entity needs to comply with rules and regulations of regulatory

frameworks. This also helps directors and management to develop strategy in the area which

needs to improve for obtaining better efficiency of work.

Purpose of financial reporting:

1

In order to analyse functioning and day to day operations of multiple departments of the

organisation, financial reporting plays an important role. It is the tool which such multiple

operation through reporting in documents of the company (Kimmel and et.al., 2016). Thus, this

assessment will develop to provide better understanding and purpose of financial reporting.

Chosen reputed accounting firm in this report is Arnold Hill & Co. which deals in providing

financial and legal services to clients. Further, conceptual and regulatory framework of this

accounting will also to be explained by analysing key stakeholder and their need for financial

reporting.

Moreover, explanation will also to be provided on international accounting standards and

international financial reporting standards with its degree of compliance across the nation.

Lastly, in this report through models and theories better understanding relates to financial

reporting will be developed.

MAIN BODY

1. Analysing context and purpose of financial reporting

Financial reporting is considered as vital term which plays an important role in the world

of economies. Main purpose of this accounting is to provide information which is relevant and

useful for owners and stakeholders of the organisation. This is the way of showing financial

ability of company in market among shareholders (Henderson and et.al., 2015). Thus, context of

this reporting is to comply with regulatory frameworks while preparing financial statements of

the company. Its governance includes duties and responsible of officer where manager is

responsible for preparing financial statement and business operation of company and director is

responsible to oversee such method which adopted by management for preparing such

statements.

Therefore, it can be said that in order to show efficiency and effectiveness of company

and to capture more investors, entity needs to comply with rules and regulations of regulatory

frameworks. This also helps directors and management to develop strategy in the area which

needs to improve for obtaining better efficiency of work.

Purpose of financial reporting:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Goal of financial reporting is to meet expectations of shareholders and legislation in order

to evaluate company's performance. This helps investors and shareholders to make effective

decision to managing business operations. Three main goals of reporting includes:

Meet users' expectation and legislation: users and government always in need of

company's financial report so that they will able to analyse operations strategies in order

to reinvest cash in business and to analyse how efficiency business is using its capital.

Tracking of cash flow: through financial statement, managers and owners of company

will able to analyse flow of money in entity. This information helps to evaluate

performance of company for recovering its debt and to achieve growth (Narayanaswamy

2017).

Prediction of future financial position and cash flow: through such statements, managers

and directors will able to monitor assets, liabilities and owner equity by which they will

able to predict future financial position of the company.

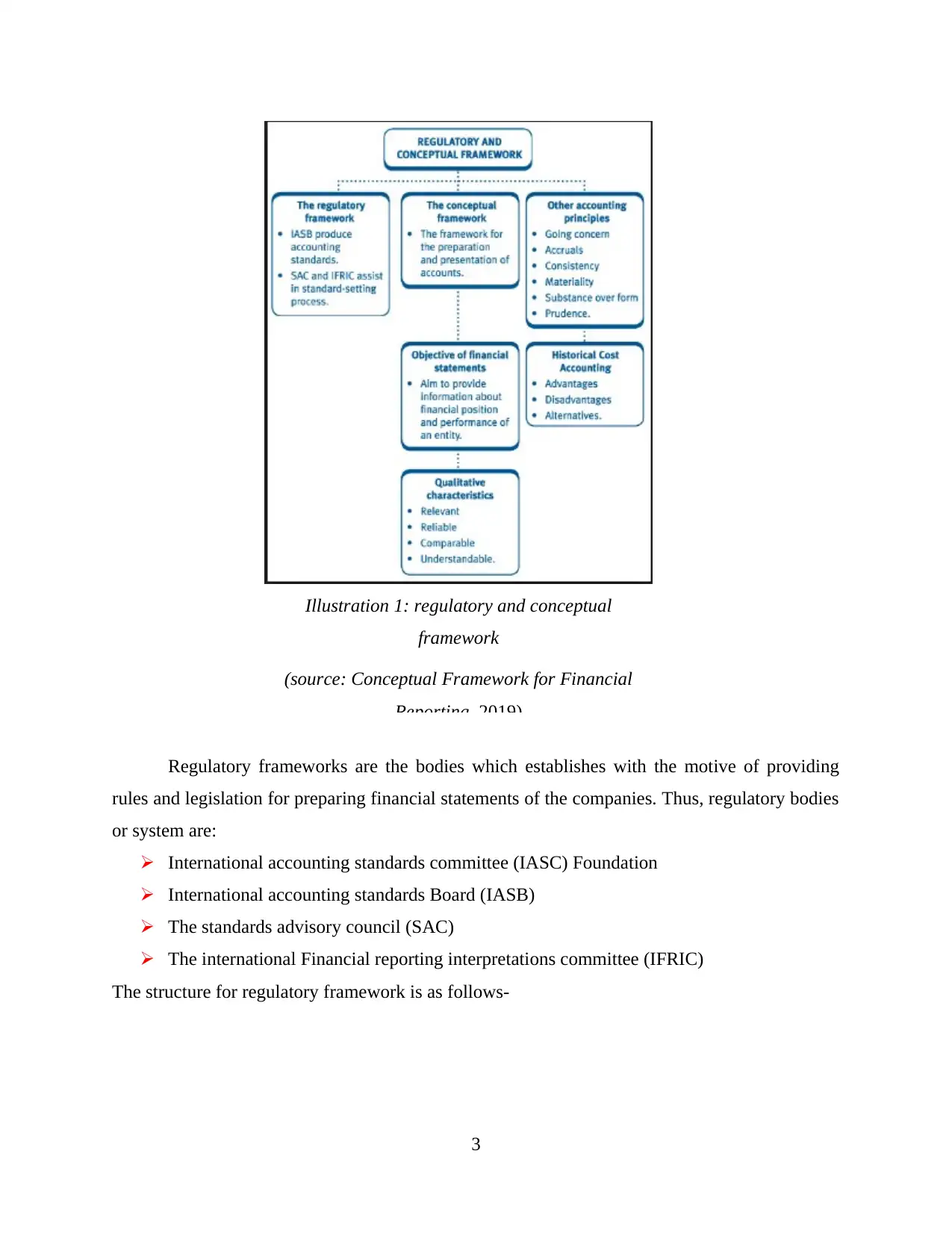

2. Explanation on conceptual and regulatory framework of financial reporting with principle to

assess its requirement

2

to evaluate company's performance. This helps investors and shareholders to make effective

decision to managing business operations. Three main goals of reporting includes:

Meet users' expectation and legislation: users and government always in need of

company's financial report so that they will able to analyse operations strategies in order

to reinvest cash in business and to analyse how efficiency business is using its capital.

Tracking of cash flow: through financial statement, managers and owners of company

will able to analyse flow of money in entity. This information helps to evaluate

performance of company for recovering its debt and to achieve growth (Narayanaswamy

2017).

Prediction of future financial position and cash flow: through such statements, managers

and directors will able to monitor assets, liabilities and owner equity by which they will

able to predict future financial position of the company.

2. Explanation on conceptual and regulatory framework of financial reporting with principle to

assess its requirement

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Regulatory frameworks are the bodies which establishes with the motive of providing

rules and legislation for preparing financial statements of the companies. Thus, regulatory bodies

or system are:

International accounting standards committee (IASC) Foundation

International accounting standards Board (IASB)

The standards advisory council (SAC)

The international Financial reporting interpretations committee (IFRIC)

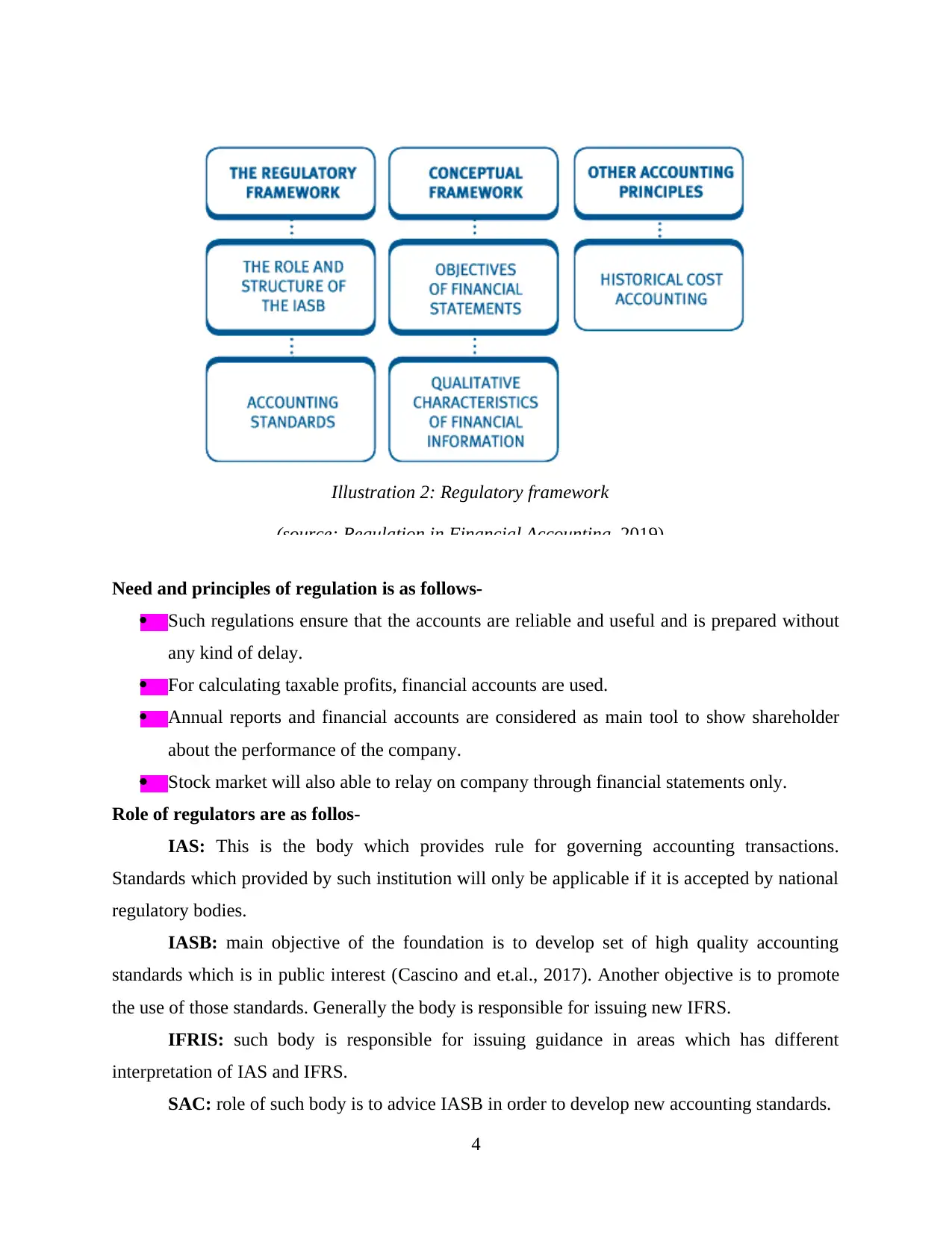

The structure for regulatory framework is as follows-

3

Illustration 1: regulatory and conceptual

framework

(source: Conceptual Framework for Financial

Reporting, 2019)

rules and legislation for preparing financial statements of the companies. Thus, regulatory bodies

or system are:

International accounting standards committee (IASC) Foundation

International accounting standards Board (IASB)

The standards advisory council (SAC)

The international Financial reporting interpretations committee (IFRIC)

The structure for regulatory framework is as follows-

3

Illustration 1: regulatory and conceptual

framework

(source: Conceptual Framework for Financial

Reporting, 2019)

Need and principles of regulation is as follows-

Such regulations ensure that the accounts are reliable and useful and is prepared without

any kind of delay.

For calculating taxable profits, financial accounts are used.

Annual reports and financial accounts are considered as main tool to show shareholder

about the performance of the company.

Stock market will also able to relay on company through financial statements only.

Role of regulators are as follos-

IAS: This is the body which provides rule for governing accounting transactions.

Standards which provided by such institution will only be applicable if it is accepted by national

regulatory bodies.

IASB: main objective of the foundation is to develop set of high quality accounting

standards which is in public interest (Cascino and et.al., 2017). Another objective is to promote

the use of those standards. Generally the body is responsible for issuing new IFRS.

IFRIS: such body is responsible for issuing guidance in areas which has different

interpretation of IAS and IFRS.

SAC: role of such body is to advice IASB in order to develop new accounting standards.

4

Illustration 2: Regulatory framework

(source: Regulation in Financial Accounting, 2019)

Such regulations ensure that the accounts are reliable and useful and is prepared without

any kind of delay.

For calculating taxable profits, financial accounts are used.

Annual reports and financial accounts are considered as main tool to show shareholder

about the performance of the company.

Stock market will also able to relay on company through financial statements only.

Role of regulators are as follos-

IAS: This is the body which provides rule for governing accounting transactions.

Standards which provided by such institution will only be applicable if it is accepted by national

regulatory bodies.

IASB: main objective of the foundation is to develop set of high quality accounting

standards which is in public interest (Cascino and et.al., 2017). Another objective is to promote

the use of those standards. Generally the body is responsible for issuing new IFRS.

IFRIS: such body is responsible for issuing guidance in areas which has different

interpretation of IAS and IFRS.

SAC: role of such body is to advice IASB in order to develop new accounting standards.

4

Illustration 2: Regulatory framework

(source: Regulation in Financial Accounting, 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The conceptual framework:

To assist IASB board for developing or issuing new standards and to review existing one.

For developing harmonising accounting standards and procedure for preparing effective

accounting statements.

To help accountant in order to comply with new set of accounting standards while

preparing financial statements of the company.

Key accounting principles are as follows-

Going Concern This assumption states that business will continue with

operations for foreseeable future.

Accruals/Matching This concept assumes that income and expenses must matched

against each other within accounting period.

Consistency It assumes that item must be treated in same way in same year.

Materiality Information which is important must be demanded of all

information in financial statements.

Substance over form It assumes that economic substance of transaction must be

recorded (Harrison and van der Laan Smith, 2015).

Prudence It states that asset and income must not be overstated and

liabilities must not be understated.

5

To assist IASB board for developing or issuing new standards and to review existing one.

For developing harmonising accounting standards and procedure for preparing effective

accounting statements.

To help accountant in order to comply with new set of accounting standards while

preparing financial statements of the company.

Key accounting principles are as follows-

Going Concern This assumption states that business will continue with

operations for foreseeable future.

Accruals/Matching This concept assumes that income and expenses must matched

against each other within accounting period.

Consistency It assumes that item must be treated in same way in same year.

Materiality Information which is important must be demanded of all

information in financial statements.

Substance over form It assumes that economic substance of transaction must be

recorded (Harrison and van der Laan Smith, 2015).

Prudence It states that asset and income must not be overstated and

liabilities must not be understated.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

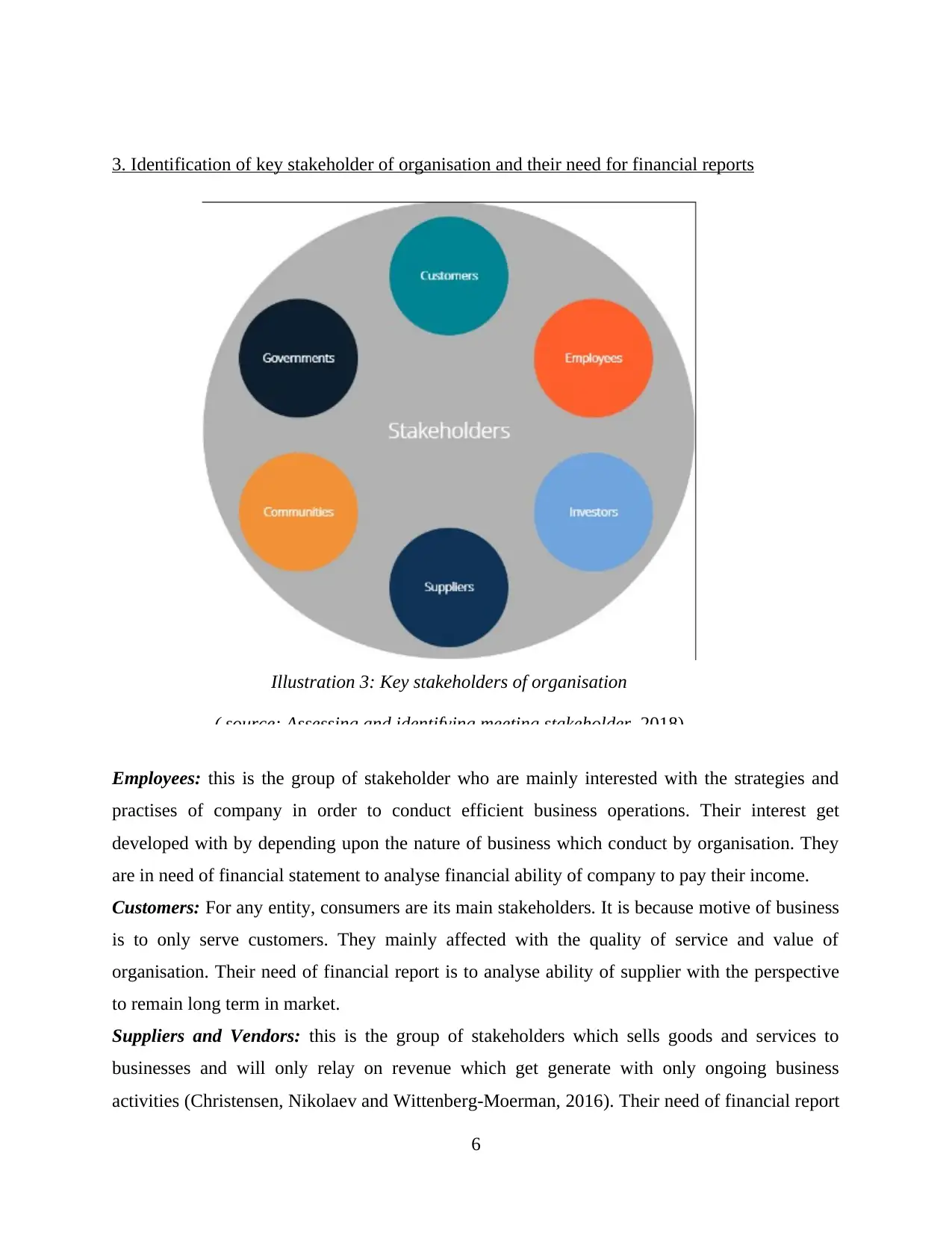

3. Identification of key stakeholder of organisation and their need for financial reports

Employees: this is the group of stakeholder who are mainly interested with the strategies and

practises of company in order to conduct efficient business operations. Their interest get

developed with by depending upon the nature of business which conduct by organisation. They

are in need of financial statement to analyse financial ability of company to pay their income.

Customers: For any entity, consumers are its main stakeholders. It is because motive of business

is to only serve customers. They mainly affected with the quality of service and value of

organisation. Their need of financial report is to analyse ability of supplier with the perspective

to remain long term in market.

Suppliers and Vendors: this is the group of stakeholders which sells goods and services to

businesses and will only relay on revenue which get generate with only ongoing business

activities (Christensen, Nikolaev and Wittenberg‐Moerman, 2016). Their need of financial report

6

Illustration 3: Key stakeholders of organisation

( source: Assessing and identifying meeting stakeholder, 2018)

Employees: this is the group of stakeholder who are mainly interested with the strategies and

practises of company in order to conduct efficient business operations. Their interest get

developed with by depending upon the nature of business which conduct by organisation. They

are in need of financial statement to analyse financial ability of company to pay their income.

Customers: For any entity, consumers are its main stakeholders. It is because motive of business

is to only serve customers. They mainly affected with the quality of service and value of

organisation. Their need of financial report is to analyse ability of supplier with the perspective

to remain long term in market.

Suppliers and Vendors: this is the group of stakeholders which sells goods and services to

businesses and will only relay on revenue which get generate with only ongoing business

activities (Christensen, Nikolaev and Wittenberg‐Moerman, 2016). Their need of financial report

6

Illustration 3: Key stakeholders of organisation

( source: Assessing and identifying meeting stakeholder, 2018)

indicates that they have to decide whether is it safe to extend credit and to estimate ability of

business to pay back their loan.

Investors: this group include both stakeholder and debt holders. Their motive for investing in

company is with the expectation of earning a certain amount on rate of return on capital. Their

need of financial report is to analyse financial ability of company. They develop decision on

whether to invest more or to stop such investment which has been done previously.

Government: for entities, this is the another group of stakeholder which have interest in business

operations and in entities financial statements in order to analyse that whether such firm has paid

corporate tax or not or to establish tax upon income which has been earned by entities.

Communities: in large type of businesses, these are the major stakeholder of group which are

impacted by large range of things such as employment, economic development and also on

health and safety (Lev, 2018). These group require financial statements to analyse contribution

towards development of society and environment where business is established.

4. Analysing value of financial reporting for meeting organisational objectives and growth

Main function of financial reporting is to provide information about performance of the

entity in business market. It discloses information which is based on the ability of company to

meet its objectives and goals (Anderson, 2018). Hence, it is considered as end product of

accounting which discloses information through main three components that is balance sheet,

profit and loss and cash flow. Financial reporting also helps management for developing

economic decision with the proper evaluation and prediction of future perspective in order to

achieve organisational goals.

Importance of financial reporting cannot be overemphasized because it is the need of

every stakeholder in accordance with various types of reason. One among such reason is

regarding development of investment decision in company. Therefore, following are the points

which highlights importance of financial reporting in order to achieve organisational growth and

objectives-

It helps organisation to comply various rules and regulation which is a regulatory

requirement. Organisations needs to file their financial statements to registrar of

companies and to government agencies so that they will able to evaluate business income

of the entity.

7

business to pay back their loan.

Investors: this group include both stakeholder and debt holders. Their motive for investing in

company is with the expectation of earning a certain amount on rate of return on capital. Their

need of financial report is to analyse financial ability of company. They develop decision on

whether to invest more or to stop such investment which has been done previously.

Government: for entities, this is the another group of stakeholder which have interest in business

operations and in entities financial statements in order to analyse that whether such firm has paid

corporate tax or not or to establish tax upon income which has been earned by entities.

Communities: in large type of businesses, these are the major stakeholder of group which are

impacted by large range of things such as employment, economic development and also on

health and safety (Lev, 2018). These group require financial statements to analyse contribution

towards development of society and environment where business is established.

4. Analysing value of financial reporting for meeting organisational objectives and growth

Main function of financial reporting is to provide information about performance of the

entity in business market. It discloses information which is based on the ability of company to

meet its objectives and goals (Anderson, 2018). Hence, it is considered as end product of

accounting which discloses information through main three components that is balance sheet,

profit and loss and cash flow. Financial reporting also helps management for developing

economic decision with the proper evaluation and prediction of future perspective in order to

achieve organisational goals.

Importance of financial reporting cannot be overemphasized because it is the need of

every stakeholder in accordance with various types of reason. One among such reason is

regarding development of investment decision in company. Therefore, following are the points

which highlights importance of financial reporting in order to achieve organisational growth and

objectives-

It helps organisation to comply various rules and regulation which is a regulatory

requirement. Organisations needs to file their financial statements to registrar of

companies and to government agencies so that they will able to evaluate business income

of the entity.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is the tool by which entity will able to facilitate statutory audit. Such audit is

required so that auditor will able to express his/ her opinion on financial position of the

company.

This is the main backbone for financial planning, analysis, bench marking and for

decision-making which is used by various types of stakeholders.

It helps organisation to raise capital in both domestic as well as in overseas.

It is also true that on the basis of financials, stakeholders and public analysed

performance and financial ability of the company in the business market (Brennan and

Merkl-Davies, 2018).

Financial reporting also helps in tracking amount of flow of money in organisation where

proper information get generated regarding money which comes in and out. It also helps

in analysing profit and loss of the company which they incurred from their business

operations.

Thus, these are the importance of financial reporting through which entity will able to achieve its

organisational objectives and will able to develop strategies which helps in meeting future goals.

5. Explanation on international accounting standards and international financial reporting

standards with their benefits

International accounting standards:

These are the older set of accounting standards which was replaced by international

financial reporting standards in 2001. The main purpose of such standards is to ensure that

entities across the nation becomes more interconnected and will only use global financial

reporting frameworks while preparing book of accounts (Cañibano, 2018). The foundation

provides guidelines to entities regarding transactions of accounting standards which needs to be

recorded and reported in financial statements of the organisation.

Its benefits are as follows-

It facilitates ethical compliance:

This is the body which provides uniform code of accounting standards so that a business

world operates its function in appropriate behaviour. It is important because countries around the

world has their culture and practise and to understand financial statements of companies

investors will easily able to identify.

It improves international investment:

8

required so that auditor will able to express his/ her opinion on financial position of the

company.

This is the main backbone for financial planning, analysis, bench marking and for

decision-making which is used by various types of stakeholders.

It helps organisation to raise capital in both domestic as well as in overseas.

It is also true that on the basis of financials, stakeholders and public analysed

performance and financial ability of the company in the business market (Brennan and

Merkl-Davies, 2018).

Financial reporting also helps in tracking amount of flow of money in organisation where

proper information get generated regarding money which comes in and out. It also helps

in analysing profit and loss of the company which they incurred from their business

operations.

Thus, these are the importance of financial reporting through which entity will able to achieve its

organisational objectives and will able to develop strategies which helps in meeting future goals.

5. Explanation on international accounting standards and international financial reporting

standards with their benefits

International accounting standards:

These are the older set of accounting standards which was replaced by international

financial reporting standards in 2001. The main purpose of such standards is to ensure that

entities across the nation becomes more interconnected and will only use global financial

reporting frameworks while preparing book of accounts (Cañibano, 2018). The foundation

provides guidelines to entities regarding transactions of accounting standards which needs to be

recorded and reported in financial statements of the organisation.

Its benefits are as follows-

It facilitates ethical compliance:

This is the body which provides uniform code of accounting standards so that a business

world operates its function in appropriate behaviour. It is important because countries around the

world has their culture and practise and to understand financial statements of companies

investors will easily able to identify.

It improves international investment:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Investors and stakeholder of the companies finds it more convenient when they compare

business performance with other international companies. Thus, this analysis makes it easier and

cheaper for entities for raising business capital from foreign investors.

International financial reporting standards:

These are the set of accounting standards which state how particular type of transactions

and other event must be recorded in the books of accounts of entity. Such standards are issued by

IAS where proper guidelines is been provided to accountants to in order specify exactly how

financial reports needs to be maintained (De George, Li and Shivakumar, 2016). Main motive of

creating this regulation is to develop common accounting language which will be understood by

entities across the world. According to this guidelines' accountant must maintain book which is

comparable, understandable, reliable and relevant.

Its benefit are as follows-

It creates more flexibly:

These are the regulations which is based upon principles therefore, its goals is to arrive at

reasonable valuation with the various ways to accomplishing tasks. For organisations, there is

freedom for its adoption because of that statements are more easily readable and useful.

It allows greater comparability:

Businesses which use similar kind of standards for preparing financial statements will

specifically able to compare financial statements accurately. Therefore, these regulations helps

foreign investors to easily understand financial statements of company and to easily develop

their economic decision.

6. Evaluation of financial reporting with appropriate theories and models

Importance of financial accounting for organisations will be more understandable with

following theories:-

Equity theory-

This is the theory which assumes that the shareholders in company are real owners.

According to this theory residual equity and net income of the shareholders is calculated by

subtracting claim of preference shareholder from the assets of the company. This theory assumes

that common shareholders takes the greatest risk because they are the one which are fully aware

of financial ability and performance of the organisation. For financial reporting, this theory has

9

business performance with other international companies. Thus, this analysis makes it easier and

cheaper for entities for raising business capital from foreign investors.

International financial reporting standards:

These are the set of accounting standards which state how particular type of transactions

and other event must be recorded in the books of accounts of entity. Such standards are issued by

IAS where proper guidelines is been provided to accountants to in order specify exactly how

financial reports needs to be maintained (De George, Li and Shivakumar, 2016). Main motive of

creating this regulation is to develop common accounting language which will be understood by

entities across the world. According to this guidelines' accountant must maintain book which is

comparable, understandable, reliable and relevant.

Its benefit are as follows-

It creates more flexibly:

These are the regulations which is based upon principles therefore, its goals is to arrive at

reasonable valuation with the various ways to accomplishing tasks. For organisations, there is

freedom for its adoption because of that statements are more easily readable and useful.

It allows greater comparability:

Businesses which use similar kind of standards for preparing financial statements will

specifically able to compare financial statements accurately. Therefore, these regulations helps

foreign investors to easily understand financial statements of company and to easily develop

their economic decision.

6. Evaluation of financial reporting with appropriate theories and models

Importance of financial accounting for organisations will be more understandable with

following theories:-

Equity theory-

This is the theory which assumes that the shareholders in company are real owners.

According to this theory residual equity and net income of the shareholders is calculated by

subtracting claim of preference shareholder from the assets of the company. This theory assumes

that common shareholders takes the greatest risk because they are the one which are fully aware

of financial ability and performance of the organisation. For financial reporting, this theory has

9

the same perspective of providing relevant information for retaining shareholder on long term

basis (Christensen and et.al., 2015).

Shareholders only get attracted in company when they full knowledge regarding business

operations of the company and equity theory also state that shareholder will only take great risk

when they are fully aware about entity's business operations.

Legitimacy theory-

This is the theory which is based on the assumption that action of the entity are desirable,

proper or appropriate within some norms, values, beliefs and definition. Normally this theory has

been used for explaining social and environmental reporting disclosure. This is considered as

useful concept for explaining corporate behaviour thorough report. For society or for

stakeholders, this theory is considered for external perception. Legitimacy is always present in

the type of disclosure which company chooses to present in financial statements. Thus, this

theory has been considered as a theoretical framework regarding level of disclosure adopted by

the company for its development.

Therefore, these are the two theories in context of financial reporting through which

proper guidelines for preparing financial report get developed.

7. Identifying differences in financial reporting across the world with the evaluation of

differences

In the beginning entity only comply with its internal reporting only but when it found that

more and more companies are ending because of large financial problems, it becomes necessary

for entities to comply with financial reporting standards where individual nation have created

their own standards for companies (Florou and Kosi, 2015). Further, when the term globalisation

has introduced more entities grasp the opportunity to expand their business globally by again

financial problems get arises to comply with rules and regulations of different countries. Thus,

this is the main problem which creating main difference in financial reporting across the world. It

is found that in every country there is a different culture and each society has their own

principles and norms and customs and these are developed in accordance with expectation of

society which create difference for entities to prepare their financial statements. Basis of

difference are as follows-

Shareholder orientation:

10

basis (Christensen and et.al., 2015).

Shareholders only get attracted in company when they full knowledge regarding business

operations of the company and equity theory also state that shareholder will only take great risk

when they are fully aware about entity's business operations.

Legitimacy theory-

This is the theory which is based on the assumption that action of the entity are desirable,

proper or appropriate within some norms, values, beliefs and definition. Normally this theory has

been used for explaining social and environmental reporting disclosure. This is considered as

useful concept for explaining corporate behaviour thorough report. For society or for

stakeholders, this theory is considered for external perception. Legitimacy is always present in

the type of disclosure which company chooses to present in financial statements. Thus, this

theory has been considered as a theoretical framework regarding level of disclosure adopted by

the company for its development.

Therefore, these are the two theories in context of financial reporting through which

proper guidelines for preparing financial report get developed.

7. Identifying differences in financial reporting across the world with the evaluation of

differences

In the beginning entity only comply with its internal reporting only but when it found that

more and more companies are ending because of large financial problems, it becomes necessary

for entities to comply with financial reporting standards where individual nation have created

their own standards for companies (Florou and Kosi, 2015). Further, when the term globalisation

has introduced more entities grasp the opportunity to expand their business globally by again

financial problems get arises to comply with rules and regulations of different countries. Thus,

this is the main problem which creating main difference in financial reporting across the world. It

is found that in every country there is a different culture and each society has their own

principles and norms and customs and these are developed in accordance with expectation of

society which create difference for entities to prepare their financial statements. Basis of

difference are as follows-

Shareholder orientation:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.