Financial Reporting: Purpose, Framework, and M&S Analysis

VerifiedAdded on 2020/10/22

|13

|3096

|362

Report

AI Summary

This report delves into the core concepts of financial reporting, examining its purpose, regulatory frameworks, and the key principles that govern it. It identifies and analyzes the main stakeholders of an organization and explains how they benefit from financial information, highlighting the value of financial reporting in achieving organizational objectives and fostering growth. The report includes a comprehensive analysis of financial statements, such as the profit and loss statement, statement of equity, and statement of financial position, with practical examples from Marks and Spencer (M&S). It contrasts IAS and IFRS, emphasizing the benefits of IFRS, and assesses varying degrees of compliance with IFRS standards. The report concludes with a detailed interpretation of M&S's financial statements over two years, offering insights into the company's financial performance and position.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................1

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

1. Purpose of financial reporting.................................................................................................1

2. Requirement, purpose and key principles of regulatory and conceptual framework..............2

3. Main stakeholders of an organisation and how they benefit from the financial information..3

4. Value of financial reporting to meet organisational objective and growth.............................4

5. Financial statements of the organisation..................................................................................4

6. Interpretation of financial statement of two years for Marks and Spencer..............................8

7. Difference between IAS and IFRS..........................................................................................9

8. Benefit of IFRS........................................................................................................................9

9. Ascertain varying degree of compliance with IFRS..............................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Contents...........................................................................................................................................1

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

1. Purpose of financial reporting.................................................................................................1

2. Requirement, purpose and key principles of regulatory and conceptual framework..............2

3. Main stakeholders of an organisation and how they benefit from the financial information..3

4. Value of financial reporting to meet organisational objective and growth.............................4

5. Financial statements of the organisation..................................................................................4

6. Interpretation of financial statement of two years for Marks and Spencer..............................8

7. Difference between IAS and IFRS..........................................................................................9

8. Benefit of IFRS........................................................................................................................9

9. Ascertain varying degree of compliance with IFRS..............................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial reporting is refers to the preparing and disclosing the financial statements like

balance sheet, profit and loss statement and cash flows statement of company to management

and public. These reports are usually prepared on quarterly and annually basis. The main purpose

of report is to to provide vital information to the management so that they can take effective

decision. To better understand this concept company. Marks and Spencer, UK is being selected.

The report covers purpose of financial reporting, requirement and key principles of financial

reporting is discussed in this report. The key stakeholders and values of financial reporting is for

organisational growth is being discussed. As financial statement is also being prepared for

company. There are various difference between IAS and IFRS is discussed in this report. Apart

from this the benefit of IFRS is also being explained in the report.

MAIN BODY

1. Purpose of financial reporting

Financial Reporting:

According to International Accounting Standard Board (IASB), the objective of

financial reporting is to provide information about financial position, performance and changes

in financial position of an enterprise that is useful to a wide range of users in making economic

decisions.

Financial reporting is the process for keeping records of financial related information of

organisation. The IASB defines that business need to prepare financial statements every year to

show the actual status of company to public and shareholders of company. This is very important

for business to present transparent information of company to management so that they can take

effective decision in company. There are different purpose for which M&S can prepare these

reports, these are discussed below:

To provide information to management of company so that they can take effective

decision in company (Kaya, and Koch, 2015).

To provide the transparent information to shareholders and public at large.

To give depth information regarding how an organisation is using and procuring different

resources.

To give information to auditors in order to facilitate audits

1

Financial reporting is refers to the preparing and disclosing the financial statements like

balance sheet, profit and loss statement and cash flows statement of company to management

and public. These reports are usually prepared on quarterly and annually basis. The main purpose

of report is to to provide vital information to the management so that they can take effective

decision. To better understand this concept company. Marks and Spencer, UK is being selected.

The report covers purpose of financial reporting, requirement and key principles of financial

reporting is discussed in this report. The key stakeholders and values of financial reporting is for

organisational growth is being discussed. As financial statement is also being prepared for

company. There are various difference between IAS and IFRS is discussed in this report. Apart

from this the benefit of IFRS is also being explained in the report.

MAIN BODY

1. Purpose of financial reporting

Financial Reporting:

According to International Accounting Standard Board (IASB), the objective of

financial reporting is to provide information about financial position, performance and changes

in financial position of an enterprise that is useful to a wide range of users in making economic

decisions.

Financial reporting is the process for keeping records of financial related information of

organisation. The IASB defines that business need to prepare financial statements every year to

show the actual status of company to public and shareholders of company. This is very important

for business to present transparent information of company to management so that they can take

effective decision in company. There are different purpose for which M&S can prepare these

reports, these are discussed below:

To provide information to management of company so that they can take effective

decision in company (Kaya, and Koch, 2015).

To provide the transparent information to shareholders and public at large.

To give depth information regarding how an organisation is using and procuring different

resources.

To give information to auditors in order to facilitate audits

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Its main objective is to analyse the present market value, financial status of company so

effective strategies can be formulated by management.

To provide information to various stakeholders regarding performance management of

M&S as how ethically they are performing their duties.

The main purpose is to enhance social welfare by taking care of interest of employees,

trade unions and government (Mohd Nasir and et.al., 2012).

2. Requirement, purpose and key principles of regulatory and conceptual framework.

Regulatory and conceptual framework:

The conceptual framework is an analytical element which includes the qualitative and

quantitative matters. This framework includes purpose of financial reporting, qualitative

characteristics of useful financial information, reporting entity and boundary. Apart from this it

defines measurement bases and guidance on when to use financial reporting, guidance on

disclosure and concepts relating to capital and capital maintenance are being set out in this

framework. The M&S following all regulations which are set by the IASB. These regulations are

imposed in the form of IFRS. The need and purpose of framework is discussed below:

Help in development of future IFRS and monitoring of existing standard by setting by out

the underlying concepts.

This promotes harmony of accounting regulations and standard by cutting down the

number of alternative accounting treatment.

It enables business to prepare financial statements in application of IFRS.

The following advantages of this framework for the companies which adopt them:

IFRS are broadly accepted as a set of high quality and transparent global standards that

are intended to achieve consistency and comparability across the world.

The firm which use IFRS and have their accounts audited in accordance with

International Standard on Auditing will have an enhanced status and reputation.

The International Organisation of Securities Commissions (IOSCO) distinguish IFRS for

listing purposes therefore companies that use IFRS need produce only set of financial

statements for any securities listing for countries which are participative members of

IOSCO.

3. Main stakeholders of an organisation and how they benefit from the financial information

Stakeholders:

2

effective strategies can be formulated by management.

To provide information to various stakeholders regarding performance management of

M&S as how ethically they are performing their duties.

The main purpose is to enhance social welfare by taking care of interest of employees,

trade unions and government (Mohd Nasir and et.al., 2012).

2. Requirement, purpose and key principles of regulatory and conceptual framework.

Regulatory and conceptual framework:

The conceptual framework is an analytical element which includes the qualitative and

quantitative matters. This framework includes purpose of financial reporting, qualitative

characteristics of useful financial information, reporting entity and boundary. Apart from this it

defines measurement bases and guidance on when to use financial reporting, guidance on

disclosure and concepts relating to capital and capital maintenance are being set out in this

framework. The M&S following all regulations which are set by the IASB. These regulations are

imposed in the form of IFRS. The need and purpose of framework is discussed below:

Help in development of future IFRS and monitoring of existing standard by setting by out

the underlying concepts.

This promotes harmony of accounting regulations and standard by cutting down the

number of alternative accounting treatment.

It enables business to prepare financial statements in application of IFRS.

The following advantages of this framework for the companies which adopt them:

IFRS are broadly accepted as a set of high quality and transparent global standards that

are intended to achieve consistency and comparability across the world.

The firm which use IFRS and have their accounts audited in accordance with

International Standard on Auditing will have an enhanced status and reputation.

The International Organisation of Securities Commissions (IOSCO) distinguish IFRS for

listing purposes therefore companies that use IFRS need produce only set of financial

statements for any securities listing for countries which are participative members of

IOSCO.

3. Main stakeholders of an organisation and how they benefit from the financial information

Stakeholders:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The stakeholders are the member of groups without their support the organisation would

cease to exit. A corporate stakeholder can affect or be affected by the action of business as

whole. The stakeholders’ required the financial statement to analyse their equity investment this

help them to take informed decisions. There are two kinds of stakeholders for a business, which

are discussed below:

Internal Stakeholders:

Internal stakeholders are those who are internally and directly related with the company.

The organisation is affected by the very small action of internal stakeholder. Internal

stakeholders are employees or groups in organisation who have an interest in a strategy plan,

program, product, project and process. The internal stakeholders are described below:

Board of Director:

The board of director of an organisation is an internal stakeholder for company. As they

can conduct internal investigation and require information or the participation of employees and

teams. The stakeholder has direct impact on business strategy of company. The board director

need the financial information and reports on time as this is very helpful for them to take

decision by considering these internal statements (Norwani and Chek, 2011).

Auditors:

The auditors also have direct interest with company’s various financial related

transactions. As auditors audit financial statement of company and then according to that

auditors find the deviation and correct these deviations. So financial reporting is very beneficial

for the auditors as it helps them to take better decision.

External Stakeholders:

The external stakeholders are those who does not affect the business directly but they can

make huge impact on the organisational decision making process. These are described below:

Customers:

Customers are the king of market and there need is fulfilled with high priorities. As they

are the external shareholder for business organisation and they have direct impact on business

organisation. If company is fulfilling customers need than they can get new heights. As a

customer, it is very important to have financial information of company so that they make any

investment in company accordingly. As customer prefer to invest in company which has good

growth and financial stability.

3

cease to exit. A corporate stakeholder can affect or be affected by the action of business as

whole. The stakeholders’ required the financial statement to analyse their equity investment this

help them to take informed decisions. There are two kinds of stakeholders for a business, which

are discussed below:

Internal Stakeholders:

Internal stakeholders are those who are internally and directly related with the company.

The organisation is affected by the very small action of internal stakeholder. Internal

stakeholders are employees or groups in organisation who have an interest in a strategy plan,

program, product, project and process. The internal stakeholders are described below:

Board of Director:

The board of director of an organisation is an internal stakeholder for company. As they

can conduct internal investigation and require information or the participation of employees and

teams. The stakeholder has direct impact on business strategy of company. The board director

need the financial information and reports on time as this is very helpful for them to take

decision by considering these internal statements (Norwani and Chek, 2011).

Auditors:

The auditors also have direct interest with company’s various financial related

transactions. As auditors audit financial statement of company and then according to that

auditors find the deviation and correct these deviations. So financial reporting is very beneficial

for the auditors as it helps them to take better decision.

External Stakeholders:

The external stakeholders are those who does not affect the business directly but they can

make huge impact on the organisational decision making process. These are described below:

Customers:

Customers are the king of market and there need is fulfilled with high priorities. As they

are the external shareholder for business organisation and they have direct impact on business

organisation. If company is fulfilling customers need than they can get new heights. As a

customer, it is very important to have financial information of company so that they make any

investment in company accordingly. As customer prefer to invest in company which has good

growth and financial stability.

3

Shareholders:

The shareholders are those who buy some share and have holding in company. They can

make direct impact on the company. This is important for company to provide financial

information to shareholder so they should be aware about the company/s financial position so

that they can take decision accordingly.

Supplier:

The suppliers are the external stakeholder for business and they do not require much

financial information. As they just need to assure that company will not become insolvent in

forthcoming year.

4. Value of financial reporting to meet organisational objective and growth

Financial reporting is very important now day to achieve overall objective and growth of

organisation. It is important for organisation to prepare financial statement and then present this

statement to the management of company so that they can achieve the organisation. Financial

reporting is reporting of financial works to their seniors and team leaders on regular basis so that

leaders and managers can take decision on the basis of these financial reports. The main aim of

this financial reporting is to take effective decisions in organisation. These reporting can be

helpful for the company in order to facilitate organisation to take better decisions. As better

decisions would be helpful for company to meet its goals and growth. Financial reporting shows

a clear picture to management regarding the financial position of company. This helps higher

authority of company to formulate strategy according to financial position of company so that

goals can be achieved easily. The financial reporting is backbone for financial planning, analysis,

benchmarking and decision making. This is very helpful in the raising company’s fund in both

local and international market. Financial reporting is valuable for the purpose of bidding, labour

contract and government supplies etc. As organizations are required to prepare and present

financial reports and statements (Pucheta‐Martínez and García‐Meca, 2014).

5. Financial statements of the organisation

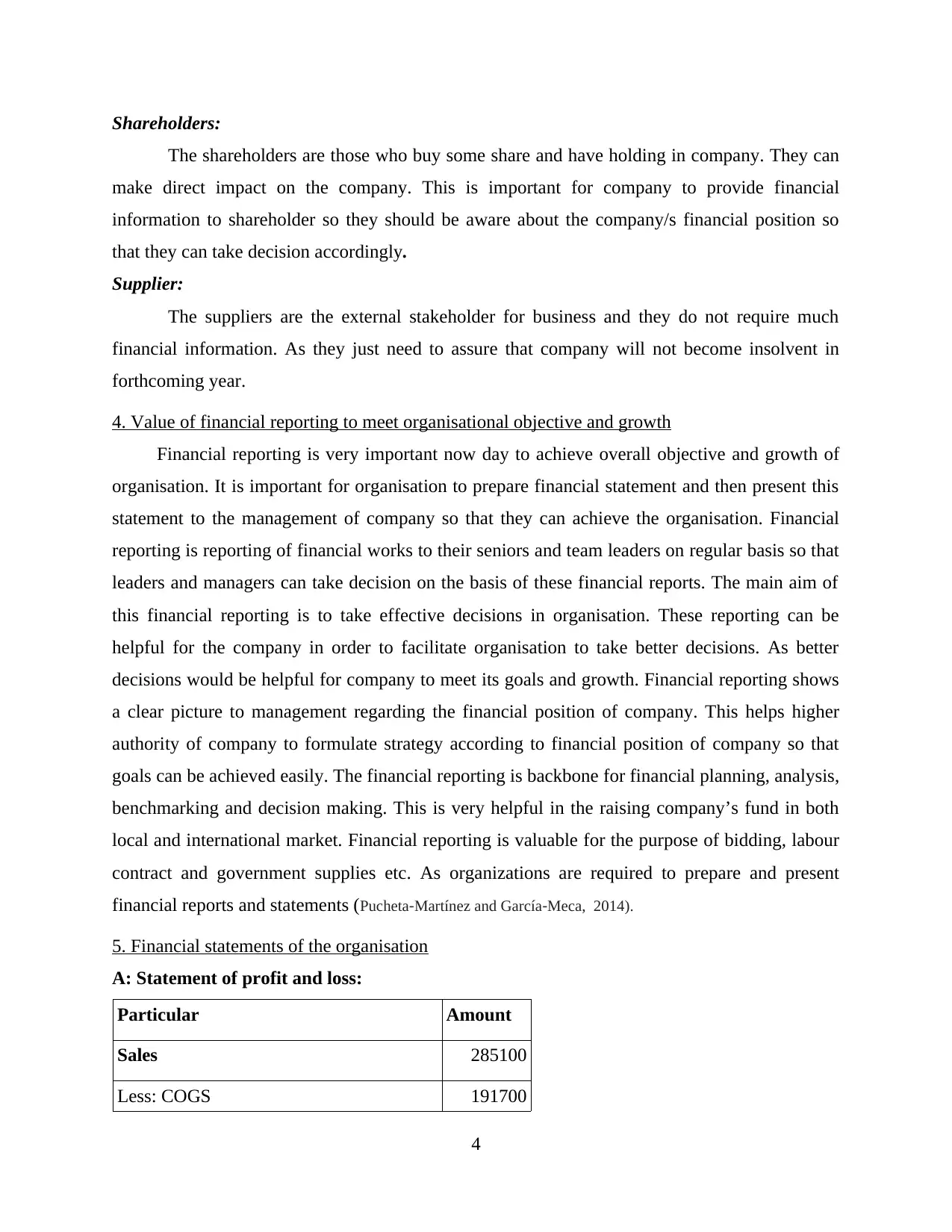

A: Statement of profit and loss:

Particular Amount

Sales 285100

Less: COGS 191700

4

The shareholders are those who buy some share and have holding in company. They can

make direct impact on the company. This is important for company to provide financial

information to shareholder so they should be aware about the company/s financial position so

that they can take decision accordingly.

Supplier:

The suppliers are the external stakeholder for business and they do not require much

financial information. As they just need to assure that company will not become insolvent in

forthcoming year.

4. Value of financial reporting to meet organisational objective and growth

Financial reporting is very important now day to achieve overall objective and growth of

organisation. It is important for organisation to prepare financial statement and then present this

statement to the management of company so that they can achieve the organisation. Financial

reporting is reporting of financial works to their seniors and team leaders on regular basis so that

leaders and managers can take decision on the basis of these financial reports. The main aim of

this financial reporting is to take effective decisions in organisation. These reporting can be

helpful for the company in order to facilitate organisation to take better decisions. As better

decisions would be helpful for company to meet its goals and growth. Financial reporting shows

a clear picture to management regarding the financial position of company. This helps higher

authority of company to formulate strategy according to financial position of company so that

goals can be achieved easily. The financial reporting is backbone for financial planning, analysis,

benchmarking and decision making. This is very helpful in the raising company’s fund in both

local and international market. Financial reporting is valuable for the purpose of bidding, labour

contract and government supplies etc. As organizations are required to prepare and present

financial reports and statements (Pucheta‐Martínez and García‐Meca, 2014).

5. Financial statements of the organisation

A: Statement of profit and loss:

Particular Amount

Sales 285100

Less: COGS 191700

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gross profits 93400

Rental income 1600

Loss on revaluation of investment

property 3300

Loss on sale of inventory 400

Operating expenses 43100

Profit from operation 44600

Bank interest 1030

Preference dividend 1330

PBT 42240

Tax expenses 12000

Profit after tax for equity shareholders 30240

Working note:

Calculation of Depreciation: Amount

On Land and property:

Property 4000

Plant and equipment 48000-22400*12.5% 3200

Total 7200

Charged to cost of sales 3600

Charged to operating expenses 3600

Profit and loss account for organisation during a financial year assists to determine the

net profit or net loss after making all adjustment such as tax, depreciation and rent etc. The above

mention P&L account for the company shows gross profit of 93400, profit after deducting

operating expenses is 44600, profit before tax shows a balance of 42240 and profit after

5

Rental income 1600

Loss on revaluation of investment

property 3300

Loss on sale of inventory 400

Operating expenses 43100

Profit from operation 44600

Bank interest 1030

Preference dividend 1330

PBT 42240

Tax expenses 12000

Profit after tax for equity shareholders 30240

Working note:

Calculation of Depreciation: Amount

On Land and property:

Property 4000

Plant and equipment 48000-22400*12.5% 3200

Total 7200

Charged to cost of sales 3600

Charged to operating expenses 3600

Profit and loss account for organisation during a financial year assists to determine the

net profit or net loss after making all adjustment such as tax, depreciation and rent etc. The above

mention P&L account for the company shows gross profit of 93400, profit after deducting

operating expenses is 44600, profit before tax shows a balance of 42240 and profit after

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

deducting tax amount 30240. As the indirect expenses have been deducted from gross profit in

order to get net profit. There are different adjustments have been made while calculated profit for

the firm such as property, plant and equipment balance, charges related to cost of goods sold and

expenses that are linked with operating activity.

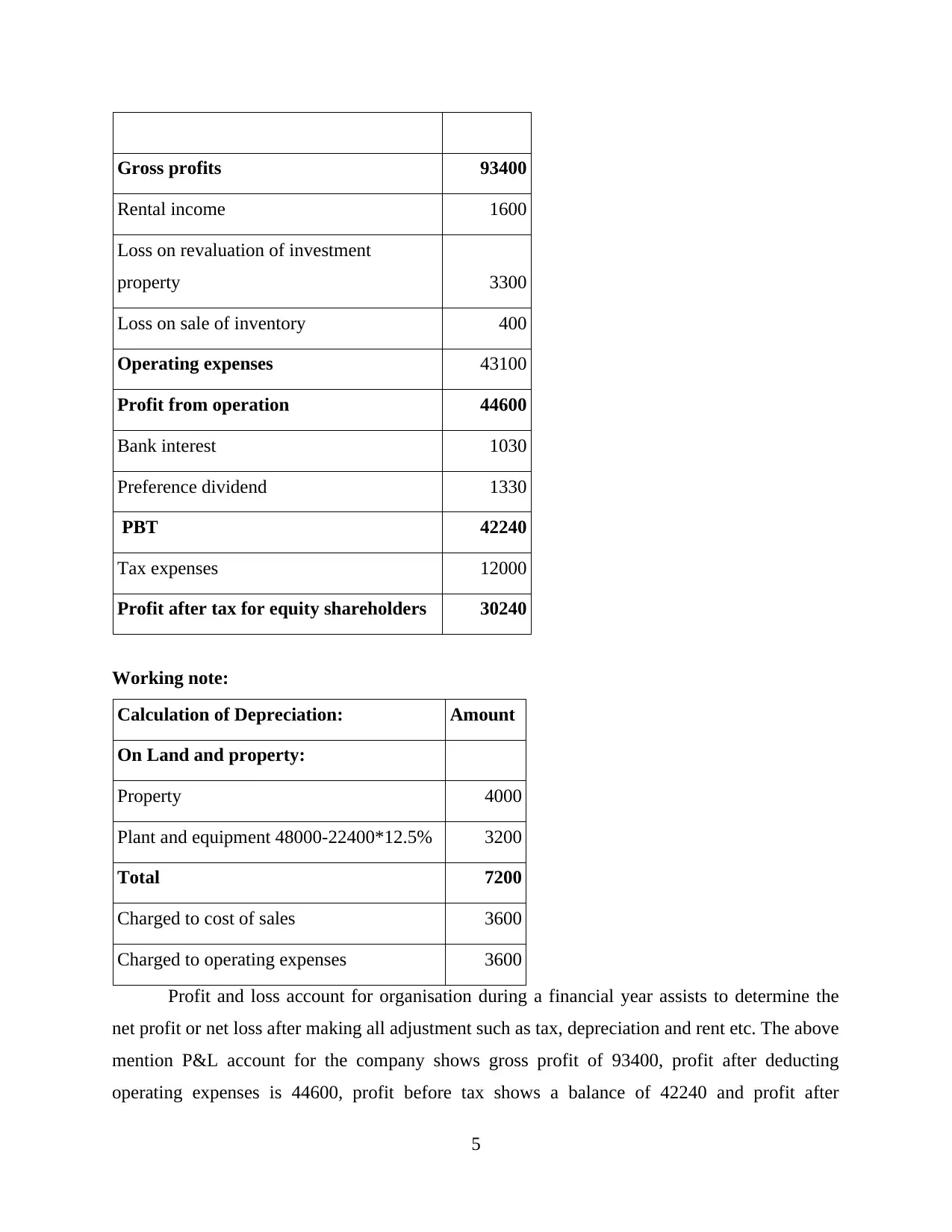

B: Statement of equity:

Statement of change in equity

Particulars Ordinary capital Retained earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

Statement of equity:

The statement of equity help in ascertaining the total amount company is offering to its

investors during a particular period of time. The statement described above shows the opening

balance of about 26700 and retained earnings of amount 23300. The dividend paid during an

accounting year is 5340. So the profit ascertained for the current year is 30240. The statement of

equity shows the closing capital balance of amount 26700 and closing retained earning balance

48200.

6

order to get net profit. There are different adjustments have been made while calculated profit for

the firm such as property, plant and equipment balance, charges related to cost of goods sold and

expenses that are linked with operating activity.

B: Statement of equity:

Statement of change in equity

Particulars Ordinary capital Retained earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

Statement of equity:

The statement of equity help in ascertaining the total amount company is offering to its

investors during a particular period of time. The statement described above shows the opening

balance of about 26700 and retained earnings of amount 23300. The dividend paid during an

accounting year is 5340. So the profit ascertained for the current year is 30240. The statement of

equity shows the closing capital balance of amount 26700 and closing retained earning balance

48200.

6

Statement of Financial Position:

The balance sheet shows actual financial health of company as it is prepared by every

company at the end of an accounting period in order to know actual position of business. This is

consisting of liabilities and assets. The liabilities and assets should be equal is considered as a

fair balance sheet. This can be seen that company has total current assets amounting 30400 and

7

The balance sheet shows actual financial health of company as it is prepared by every

company at the end of an accounting period in order to know actual position of business. This is

consisting of liabilities and assets. The liabilities and assets should be equal is considered as a

fair balance sheet. This can be seen that company has total current assets amounting 30400 and

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

total noncurrent assets are 120400. Apart from this company has total current liabilities of 34600

and non current liabilities are 116200.

D. Which kind of information cash flow provides

Cash flow statement helps in knowing that how changes in balance sheet affects cash and

cash equivalent. It is majorly concerned with inflow and out flows of cash only. This captures

both operating result and accompanying changes in balance sheet. This is useful to know short

term viability of company and its ability to pay bills (Norwani, Zam and Chek, 2011).

6. Interpretation of financial statement of two years for Marks and Spencer

The profit and loss statement is statement which shows net profit or net loss for a particular

period of time. As this is prepared by M&S in order to know viability of business and its

profitability. The has profit before adjusting items amount of 670.6 for year 2018 and after

adjusting items like rent, taxes and deprecations etc. Amount of 514.1, net earning for company

comes to 156.5 for the year 2018. As for year 2017 company has earned operating profit of 253.2

so it can be said company has bearded some big expenditure in year 2018 due to that profit of

company has fallen to this amount. As earning per share for company in 2018 is 1.6 per share

and for year 2017 it was 7.2 per share. So EPS of company has also decreased which does not

considered as good result. The comprehensive income for company for year 2018 is 91.8 and for

the year 2017 it was 70.8 so it has increased from previous year which shows a good symbol for

company. The balance sheet is crucial financial statement shows actual position of business as it

is prepared by every business in order to know actual financial position. As balance sheet consist

of assets and liabilities and at end of balance sheet, both asset and liability side amount should be

equal. Non current asset for M&S for year 2017 is 6569.2, as this includes the intangible assets,

fixed assets, financial assets and investment in joint venture. For the year 2018 noncurrent asset

of company comes to 6232.3. so it shows company has sold its some of fixed assets in order to

pay off liabilities. As current assets for the year 2017 were amounting 468.6 and for year 2018 it

has come to 207.7 which shows company has sold it’s some of current assets for pay off current

liabilities. The total assets for company are 7550.2 for year 2018 and for 2017 it was 8292.5. As

current liabilities for the company for year 2018 is 1826 and for year 2017 it was 2368 as it has

reduced from previous year which means company has paid some of current liabilities. The total

liabilities for year 2018 is 4596 and for year2017 it was 5142.1. The shareholder equity for

company is 2956.7 for 2018 and for year 2017 it was 3156.3 and after deducting non controlling

8

and non current liabilities are 116200.

D. Which kind of information cash flow provides

Cash flow statement helps in knowing that how changes in balance sheet affects cash and

cash equivalent. It is majorly concerned with inflow and out flows of cash only. This captures

both operating result and accompanying changes in balance sheet. This is useful to know short

term viability of company and its ability to pay bills (Norwani, Zam and Chek, 2011).

6. Interpretation of financial statement of two years for Marks and Spencer

The profit and loss statement is statement which shows net profit or net loss for a particular

period of time. As this is prepared by M&S in order to know viability of business and its

profitability. The has profit before adjusting items amount of 670.6 for year 2018 and after

adjusting items like rent, taxes and deprecations etc. Amount of 514.1, net earning for company

comes to 156.5 for the year 2018. As for year 2017 company has earned operating profit of 253.2

so it can be said company has bearded some big expenditure in year 2018 due to that profit of

company has fallen to this amount. As earning per share for company in 2018 is 1.6 per share

and for year 2017 it was 7.2 per share. So EPS of company has also decreased which does not

considered as good result. The comprehensive income for company for year 2018 is 91.8 and for

the year 2017 it was 70.8 so it has increased from previous year which shows a good symbol for

company. The balance sheet is crucial financial statement shows actual position of business as it

is prepared by every business in order to know actual financial position. As balance sheet consist

of assets and liabilities and at end of balance sheet, both asset and liability side amount should be

equal. Non current asset for M&S for year 2017 is 6569.2, as this includes the intangible assets,

fixed assets, financial assets and investment in joint venture. For the year 2018 noncurrent asset

of company comes to 6232.3. so it shows company has sold its some of fixed assets in order to

pay off liabilities. As current assets for the year 2017 were amounting 468.6 and for year 2018 it

has come to 207.7 which shows company has sold it’s some of current assets for pay off current

liabilities. The total assets for company are 7550.2 for year 2018 and for 2017 it was 8292.5. As

current liabilities for the company for year 2018 is 1826 and for year 2017 it was 2368 as it has

reduced from previous year which means company has paid some of current liabilities. The total

liabilities for year 2018 is 4596 and for year2017 it was 5142.1. The shareholder equity for

company is 2956.7 for 2018 and for year 2017 it was 3156.3 and after deducting non controlling

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interest 2.5 for 2018 and 5.9 for 2017. This has become to 2954.2 for 2018 and 3150.4 for the

2017.

7. Difference between IAS and IFRS

To prepare financial statement and financial reports there are different kind of principle

which needs to followed by organisations. These principles and standards are issues by

International Accounting Standard Board (IASB). This is a set of those particular standard and

principle which facilitate about the recording and preparing of transaction and other financial

statements. After evolution of accounting in 2001, now new principles and standard has come

which is known as International Financial Reporting Standards. As business organisations and

accountants are confused between IAS an IFRS. But these are totally different and difference is

discussed below:

International Financial reporting standard International Accounting standard

This assist business and accountant to report

transaction in final account.

These standard provides the basic accounting

principles

These were published by International

Accounting Standard Board after 2001

And these were published by International

Accounting Standard Committee between 1973

and 2001 (Glancy and Yadav, 2011).

In IFRS, The crucial decisions are performed

by IASB

The IAS made decisions and then evaluated by

IASC

8. Benefit of IFRS

An international financial reporting standard is set of principle which is set up by IASB

and further developed by FRS 102 in recent time period. These regulation are supported on the

sound and intelligibly declared rule which welfare all shareholder. The benefits of IFRS are

discussed below:

This is helpful in growth of economy as by increasing its growth of its international

business.

This is helpful in encouraging international capitalist to invest and this leads to foreign

capital flow to country.

It offers more accounting opportunity to accounting professional by following same

accounting practice throughout world.

9

2017.

7. Difference between IAS and IFRS

To prepare financial statement and financial reports there are different kind of principle

which needs to followed by organisations. These principles and standards are issues by

International Accounting Standard Board (IASB). This is a set of those particular standard and

principle which facilitate about the recording and preparing of transaction and other financial

statements. After evolution of accounting in 2001, now new principles and standard has come

which is known as International Financial Reporting Standards. As business organisations and

accountants are confused between IAS an IFRS. But these are totally different and difference is

discussed below:

International Financial reporting standard International Accounting standard

This assist business and accountant to report

transaction in final account.

These standard provides the basic accounting

principles

These were published by International

Accounting Standard Board after 2001

And these were published by International

Accounting Standard Committee between 1973

and 2001 (Glancy and Yadav, 2011).

In IFRS, The crucial decisions are performed

by IASB

The IAS made decisions and then evaluated by

IASC

8. Benefit of IFRS

An international financial reporting standard is set of principle which is set up by IASB

and further developed by FRS 102 in recent time period. These regulation are supported on the

sound and intelligibly declared rule which welfare all shareholder. The benefits of IFRS are

discussed below:

This is helpful in growth of economy as by increasing its growth of its international

business.

This is helpful in encouraging international capitalist to invest and this leads to foreign

capital flow to country.

It offers more accounting opportunity to accounting professional by following same

accounting practice throughout world.

9

9. Ascertain varying degree of compliance with IFRS

As IFRS is becoming world wide standard which is accepted at global level by every nation

to present and prepare their financial statements. Previously there are 13 IFRS and 29 IAS which

are followed by small to big size organisation. It has been observed that M&S adapted the IFRS

in order to prepare their financial statement so that they can make effective decisions. In general

compliance is related with laws and legislation. The IFRS standard has set according to

disclosure of compliance in context of both specific disclosure need and increasing level of

principle of disclosure (Costello and WITTENBERG, 2011).

CONCLUSION

In the conclusion it can be said that accounting and financial principle plays an important

role to prepare financial statements. There are various conceptual framework and governance of

financial reporting. The financial reporting is helpful to meet organisational objectives. It is

important to prepare financial statement for company. The company can get various benefits if

they follows IFRS for preparing financial statements.

10

As IFRS is becoming world wide standard which is accepted at global level by every nation

to present and prepare their financial statements. Previously there are 13 IFRS and 29 IAS which

are followed by small to big size organisation. It has been observed that M&S adapted the IFRS

in order to prepare their financial statement so that they can make effective decisions. In general

compliance is related with laws and legislation. The IFRS standard has set according to

disclosure of compliance in context of both specific disclosure need and increasing level of

principle of disclosure (Costello and WITTENBERG, 2011).

CONCLUSION

In the conclusion it can be said that accounting and financial principle plays an important

role to prepare financial statements. There are various conceptual framework and governance of

financial reporting. The financial reporting is helpful to meet organisational objectives. It is

important to prepare financial statement for company. The company can get various benefits if

they follows IFRS for preparing financial statements.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.