Financial Reporting: Users, Standards, Statements and Analysis Report

VerifiedAdded on 2019/12/03

|13

|3786

|491

Report

AI Summary

This finance report provides a comprehensive overview of financial reporting, examining the various users of financial statements, such as banks, investors, and regulatory bodies, and their respective needs. It delves into the influence of regulatory bodies like IASB and UK GAAP on the preparation of financial statements, emphasizing the importance of uniformity and compliance with accounting standards. The report assesses the implications for users within the conceptual framework, including key assumptions like going concern and consistency. It then explains the reporting standards that businesses must adhere to. The report further includes practical examples, such as preparing financial statements from incomplete records and consolidating statements for subsidiary and holding companies. It also covers ratio analysis, interpreting key financial ratios like gearing, earnings per share, and price-earnings ratio. The report concludes with a summary of the key findings and references used throughout the analysis.

FINANCE

1 | P a g e

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................4

Task 1.........................................................................................................................................4

1.1 Description of different users of financial statements................................................4

1.2 Influence of regulatory body on preparation of financial statements.........................5

1.3 Assessment of implications for users in the conceptual framework...........................5

1.4 Explanation of reporting standards required to be followed by business entities in

dealing with regulatory requirements...............................................................................6

TASK 2......................................................................................................................................7

AC 2.1 Preparation of financial statements from incomplete records..............................7

AC 2.2 Preparation of Financial statements of Sajid's Trader .........................................8

AC 2.3 Preparation of consolidated financial statements of subsidiary and holding

company............................................................................................................................9

TASK 3....................................................................................................................................10

AC 3.1 Different users of financial statements...............................................................10

AC 3.2 Financial statements for various types of organizations....................................10

TASK 4....................................................................................................................................11

AC 4.1 Calculation of Gearing ratio, earning per share and price earnings ratio:..........11

AC 4.2 Interpretation of accounting ratios.....................................................................12

CONCLUSION........................................................................................................................12

REFERENCES.........................................................................................................................13

2 | P a g e

INTRODUCTION......................................................................................................................4

Task 1.........................................................................................................................................4

1.1 Description of different users of financial statements................................................4

1.2 Influence of regulatory body on preparation of financial statements.........................5

1.3 Assessment of implications for users in the conceptual framework...........................5

1.4 Explanation of reporting standards required to be followed by business entities in

dealing with regulatory requirements...............................................................................6

TASK 2......................................................................................................................................7

AC 2.1 Preparation of financial statements from incomplete records..............................7

AC 2.2 Preparation of Financial statements of Sajid's Trader .........................................8

AC 2.3 Preparation of consolidated financial statements of subsidiary and holding

company............................................................................................................................9

TASK 3....................................................................................................................................10

AC 3.1 Different users of financial statements...............................................................10

AC 3.2 Financial statements for various types of organizations....................................10

TASK 4....................................................................................................................................11

AC 4.1 Calculation of Gearing ratio, earning per share and price earnings ratio:..........11

AC 4.2 Interpretation of accounting ratios.....................................................................12

CONCLUSION........................................................................................................................12

REFERENCES.........................................................................................................................13

2 | P a g e

INDEX OF TABLES

Table 1: Table 1: Trading A/C as on 30 September, 2015 (In £)...............................................1

Table 2: Profit and Loss A/C as on 30 September, 2015 (In £).................................................1

Table 3: Balance sheet as on 30 September, 2015 (In £)...........................................................2

Table 4: Trading Account of Sajid Trader for the year ended 31st December, 2014(In £).......2

Table 5: Profit and loss account for the year ended 31st December, 2014 (In £)......................2

Table 6: Balance sheet of Sajid Trader as on 31st December, 2014 (In £)................................2

Table 7: Calculation of profit after interest, tax and preference dividend (In £).......................4

3 | P a g e

Table 1: Table 1: Trading A/C as on 30 September, 2015 (In £)...............................................1

Table 2: Profit and Loss A/C as on 30 September, 2015 (In £).................................................1

Table 3: Balance sheet as on 30 September, 2015 (In £)...........................................................2

Table 4: Trading Account of Sajid Trader for the year ended 31st December, 2014(In £).......2

Table 5: Profit and loss account for the year ended 31st December, 2014 (In £)......................2

Table 6: Balance sheet of Sajid Trader as on 31st December, 2014 (In £)................................2

Table 7: Calculation of profit after interest, tax and preference dividend (In £).......................4

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial statements are prepared to know the profitability and financial position of

business. It is prepared by every business organizations for the recording of financial

information in a proper manner. Present project report is based on the understanding of

regulatory framework for financial reporting. It will include description regarding different

norms to be considered by entities while preparation of financial statements. Financial

statements are statements that are used by various parties, thus business entities are required

to assure that provided statements are reliable and accurate. This report will helps us in

identifying different users of financial statements. In addition to this, the report also describes

that format of financial statements tend to vary according to the nature of business such as

sole proprietorship, partnership and company.

TASK 1

1.1 Description of different users of financial statements

Financial statements prepared by business entities are used by different parties in

order to viable decisions which are linked to the commercial activities. Description of

different users and their needs is as follows-

1. Banks- Financial institutions require information of business in order to assess their

solvency position. By the assessment of financial statements, they are able to

determine capability of company in repayment of loan.

2. Potential investors and shareholders- These party assess financial statement in order

to assess profitability position of the business. By considering this information,

potential investors make decision regarding future investment stock of company

(Gibson, 2010). Further, shareholders decide for reinvestment or divestment in the

equity of company.

3. HMRC- For the purpose of tax evaluation, HMRC consider the financial statement

prepared by the business. Through their evaluation, they assure that manipulation is

not done by company for the purpose of tax evasion (Deakins, Morrison and

Galloway, 2002).

4. Employees- In order to assess, growth opportunities employees of the organization

also assess information in the financial statement. By considering the financial

position of the company they make their decision regarding career and future

employment.

4 | P a g e

Financial statements are prepared to know the profitability and financial position of

business. It is prepared by every business organizations for the recording of financial

information in a proper manner. Present project report is based on the understanding of

regulatory framework for financial reporting. It will include description regarding different

norms to be considered by entities while preparation of financial statements. Financial

statements are statements that are used by various parties, thus business entities are required

to assure that provided statements are reliable and accurate. This report will helps us in

identifying different users of financial statements. In addition to this, the report also describes

that format of financial statements tend to vary according to the nature of business such as

sole proprietorship, partnership and company.

TASK 1

1.1 Description of different users of financial statements

Financial statements prepared by business entities are used by different parties in

order to viable decisions which are linked to the commercial activities. Description of

different users and their needs is as follows-

1. Banks- Financial institutions require information of business in order to assess their

solvency position. By the assessment of financial statements, they are able to

determine capability of company in repayment of loan.

2. Potential investors and shareholders- These party assess financial statement in order

to assess profitability position of the business. By considering this information,

potential investors make decision regarding future investment stock of company

(Gibson, 2010). Further, shareholders decide for reinvestment or divestment in the

equity of company.

3. HMRC- For the purpose of tax evaluation, HMRC consider the financial statement

prepared by the business. Through their evaluation, they assure that manipulation is

not done by company for the purpose of tax evasion (Deakins, Morrison and

Galloway, 2002).

4. Employees- In order to assess, growth opportunities employees of the organization

also assess information in the financial statement. By considering the financial

position of the company they make their decision regarding career and future

employment.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Market and Financial press- Financial statements of the business are useful for the

market for the purpose of competitive analysis (Acca Global, 2015). By considering

the financial statement, performance of organization can be determined in comparison

of rivalry firms.

6. Suppliers- Suppliers assess financial statements for the purpose of assessment of

liquidity position in order to determine their credit policy.

1.2 Influence of regulatory body on preparation of financial statements

Financial statements prepared by business organizations are generally compared by

users for appropriate decision making. Due to this aspect, uniformity in preparation of

financial statement has been promoted by different institutions such as IASB, ASB, IPSAS

and IASC. They have provided standard guidelines which are required by complied by

commercial entities. Accounting regulations in UK is mainly segregated into three parts i.e.

Companies Act 2006, UK Accounting Standards Boards and International accounting

Standards (De Franco and et. al., 2011). There is no mandatory compulsion on sole

proprietorship firms and partnership firms for applicability of these guidelines. However,

corporate entities are mandatory to implement these guidelines for accounting.

In accordance with the guidelines provided by these regulatory bodies, financial

statements are required to be prepared by considering UKGAAP. Along with this, financial

statements must include accounting procedures and policies followed by company (Maes and

et.al., 2012). Main accounting standards are based on the recording of asset and liabilities at

cost and transaction should be recorded on the basis of accrual principle instead of cash

principle (Drake, 2012). In addition to this, businesses should provide clear reflection

regarding uncertainties and risks associated to the business. Further, complete information

should be provided regarding aspects that can affect decision of investor.

1.3 Assessment of implications for users in the conceptual framework

Conceptual framework in accounting provides basic description for the preparation

and presentation of financial statements for external users (Gibson, 2010). These users

require information of business efficiency in discharging their obligations by making use of

their resources along with the information of net cash flow and future cash flow. Conceptual

framework assure that needs of all primary users are satisfied so they can make economic

decisions. This framework also provides guidance regarding basic assumptions and

accountant policies to the users (Gray and et. al., 2013). By considering this information they

5 | P a g e

market for the purpose of competitive analysis (Acca Global, 2015). By considering

the financial statement, performance of organization can be determined in comparison

of rivalry firms.

6. Suppliers- Suppliers assess financial statements for the purpose of assessment of

liquidity position in order to determine their credit policy.

1.2 Influence of regulatory body on preparation of financial statements

Financial statements prepared by business organizations are generally compared by

users for appropriate decision making. Due to this aspect, uniformity in preparation of

financial statement has been promoted by different institutions such as IASB, ASB, IPSAS

and IASC. They have provided standard guidelines which are required by complied by

commercial entities. Accounting regulations in UK is mainly segregated into three parts i.e.

Companies Act 2006, UK Accounting Standards Boards and International accounting

Standards (De Franco and et. al., 2011). There is no mandatory compulsion on sole

proprietorship firms and partnership firms for applicability of these guidelines. However,

corporate entities are mandatory to implement these guidelines for accounting.

In accordance with the guidelines provided by these regulatory bodies, financial

statements are required to be prepared by considering UKGAAP. Along with this, financial

statements must include accounting procedures and policies followed by company (Maes and

et.al., 2012). Main accounting standards are based on the recording of asset and liabilities at

cost and transaction should be recorded on the basis of accrual principle instead of cash

principle (Drake, 2012). In addition to this, businesses should provide clear reflection

regarding uncertainties and risks associated to the business. Further, complete information

should be provided regarding aspects that can affect decision of investor.

1.3 Assessment of implications for users in the conceptual framework

Conceptual framework in accounting provides basic description for the preparation

and presentation of financial statements for external users (Gibson, 2010). These users

require information of business efficiency in discharging their obligations by making use of

their resources along with the information of net cash flow and future cash flow. Conceptual

framework assure that needs of all primary users are satisfied so they can make economic

decisions. This framework also provides guidance regarding basic assumptions and

accountant policies to the users (Gray and et. al., 2013). By considering this information they

5 | P a g e

will be able to make better interpretation and comparison of financial statements to draw

valid conclusion. In this aspect following assumptions are included- Going concern- In accordance with this assumption, organization does not have any

intention to close operational activities in near future. They will operate for indefinite

period. If this presumption is not valid, then organizations are required to follow

different basis of accounting. Prudence- This assumption states that accounting for all possible losses is essential

but effect to probable losses cannot be provided by the company (McLaney and Atrill,

2010). Objective of this presumption is to ensure future possible losses are clearly

stated by business.

Consistency- Accounting policies will be uniformly followed throughout the life of

business. However, changes can be made if it is said by statue or ASB or change in

policy will provide better results.

1.4 Explanation of reporting standards required to be followed by business entities in dealing

with regulatory requirements

In order to provide guidance to business entities for the fulfilment of regulatory

requirements reporting standards have been introduced (Needles and et. al., 2012). Through

these standards guidelines has been developed through which organizations can prepare

financial statements in an effective manner.

In accordance with these standards, financial statements must include relevant

information by which decision maker can make their decisions. Relevancy is measured by its

usefulness in context of need of stakeholders. Further, provide information in statements

should be reliable by which user can trust on it (Financial times, 2015). For this aspect,

Companies Act 2006 had introduced provision of external audit that should be conducted by

independent auditor. Provided information should be understandable by the users so they

make their decisions in a proper manner. For the purpose, corporate entities are required to

provide clear description about their accounting policies and assumptions.

Along with this, fundamental assumptions (going concern, prudence and consistency)

are required to be followed by entity (Conceptual Framework for Financial Reporting 2010,

2015). In situation where these assumptions are not followed the company is required to

provide the description for it along with the justified reason (BPP Learning Media, 2014).

6 | P a g e

valid conclusion. In this aspect following assumptions are included- Going concern- In accordance with this assumption, organization does not have any

intention to close operational activities in near future. They will operate for indefinite

period. If this presumption is not valid, then organizations are required to follow

different basis of accounting. Prudence- This assumption states that accounting for all possible losses is essential

but effect to probable losses cannot be provided by the company (McLaney and Atrill,

2010). Objective of this presumption is to ensure future possible losses are clearly

stated by business.

Consistency- Accounting policies will be uniformly followed throughout the life of

business. However, changes can be made if it is said by statue or ASB or change in

policy will provide better results.

1.4 Explanation of reporting standards required to be followed by business entities in dealing

with regulatory requirements

In order to provide guidance to business entities for the fulfilment of regulatory

requirements reporting standards have been introduced (Needles and et. al., 2012). Through

these standards guidelines has been developed through which organizations can prepare

financial statements in an effective manner.

In accordance with these standards, financial statements must include relevant

information by which decision maker can make their decisions. Relevancy is measured by its

usefulness in context of need of stakeholders. Further, provide information in statements

should be reliable by which user can trust on it (Financial times, 2015). For this aspect,

Companies Act 2006 had introduced provision of external audit that should be conducted by

independent auditor. Provided information should be understandable by the users so they

make their decisions in a proper manner. For the purpose, corporate entities are required to

provide clear description about their accounting policies and assumptions.

Along with this, fundamental assumptions (going concern, prudence and consistency)

are required to be followed by entity (Conceptual Framework for Financial Reporting 2010,

2015). In situation where these assumptions are not followed the company is required to

provide the description for it along with the justified reason (BPP Learning Media, 2014).

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

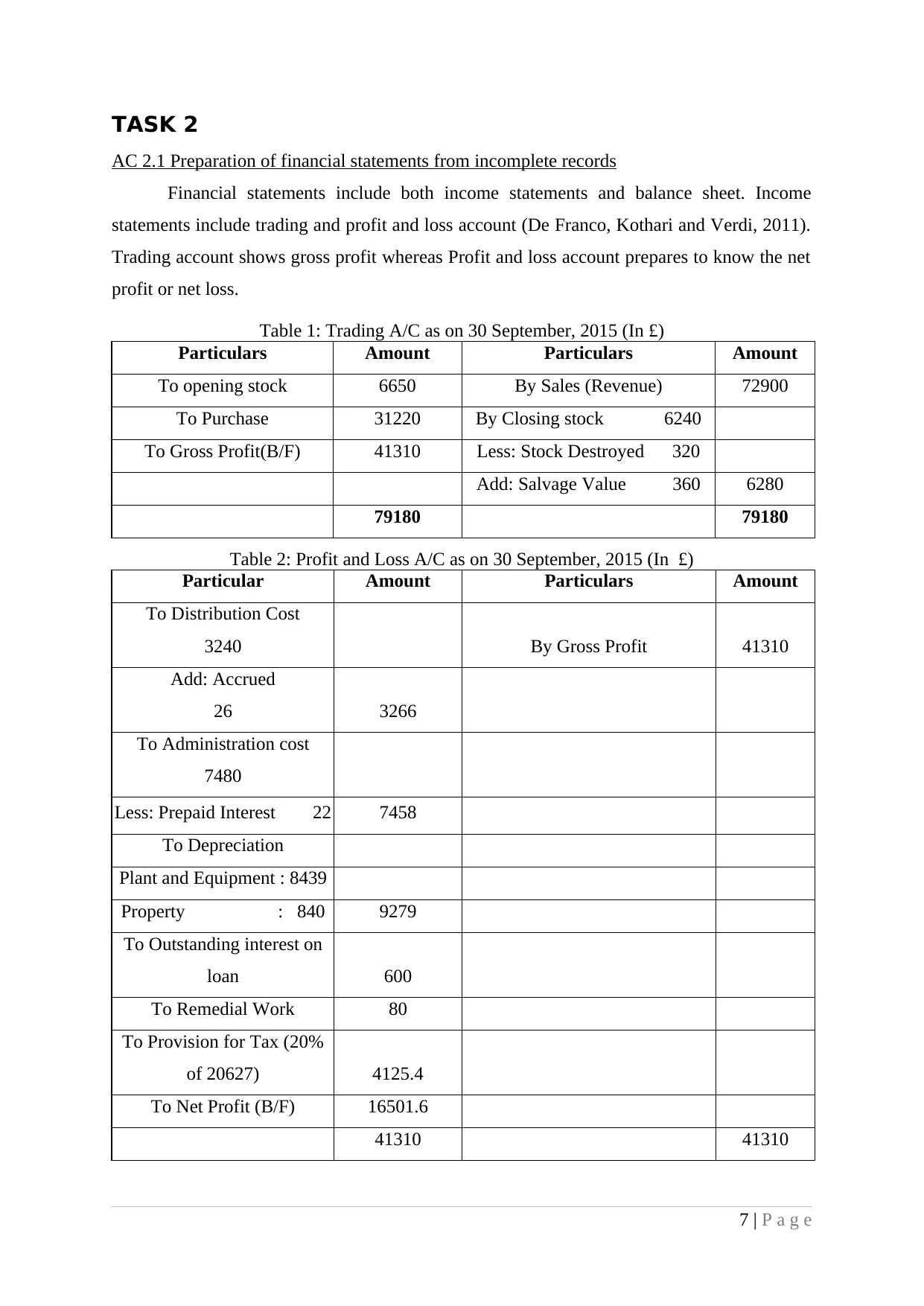

AC 2.1 Preparation of financial statements from incomplete records

Financial statements include both income statements and balance sheet. Income

statements include trading and profit and loss account (De Franco, Kothari and Verdi, 2011).

Trading account shows gross profit whereas Profit and loss account prepares to know the net

profit or net loss.

Table 1: Trading A/C as on 30 September, 2015 (In £)

Particulars Amount Particulars Amount

To opening stock 6650 By Sales (Revenue) 72900

To Purchase 31220 By Closing stock 6240

To Gross Profit(B/F) 41310 Less: Stock Destroyed 320

Add: Salvage Value 360 6280

79180 79180

Table 2: Profit and Loss A/C as on 30 September, 2015 (In £)

Particular Amount Particulars Amount

To Distribution Cost

3240 By Gross Profit 41310

Add: Accrued

26 3266

To Administration cost

7480

Less: Prepaid Interest 22 7458

To Depreciation

Plant and Equipment : 8439

Property : 840 9279

To Outstanding interest on

loan 600

To Remedial Work 80

To Provision for Tax (20%

of 20627) 4125.4

To Net Profit (B/F) 16501.6

41310 41310

7 | P a g e

AC 2.1 Preparation of financial statements from incomplete records

Financial statements include both income statements and balance sheet. Income

statements include trading and profit and loss account (De Franco, Kothari and Verdi, 2011).

Trading account shows gross profit whereas Profit and loss account prepares to know the net

profit or net loss.

Table 1: Trading A/C as on 30 September, 2015 (In £)

Particulars Amount Particulars Amount

To opening stock 6650 By Sales (Revenue) 72900

To Purchase 31220 By Closing stock 6240

To Gross Profit(B/F) 41310 Less: Stock Destroyed 320

Add: Salvage Value 360 6280

79180 79180

Table 2: Profit and Loss A/C as on 30 September, 2015 (In £)

Particular Amount Particulars Amount

To Distribution Cost

3240 By Gross Profit 41310

Add: Accrued

26 3266

To Administration cost

7480

Less: Prepaid Interest 22 7458

To Depreciation

Plant and Equipment : 8439

Property : 840 9279

To Outstanding interest on

loan 600

To Remedial Work 80

To Provision for Tax (20%

of 20627) 4125.4

To Net Profit (B/F) 16501.6

41310 41310

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

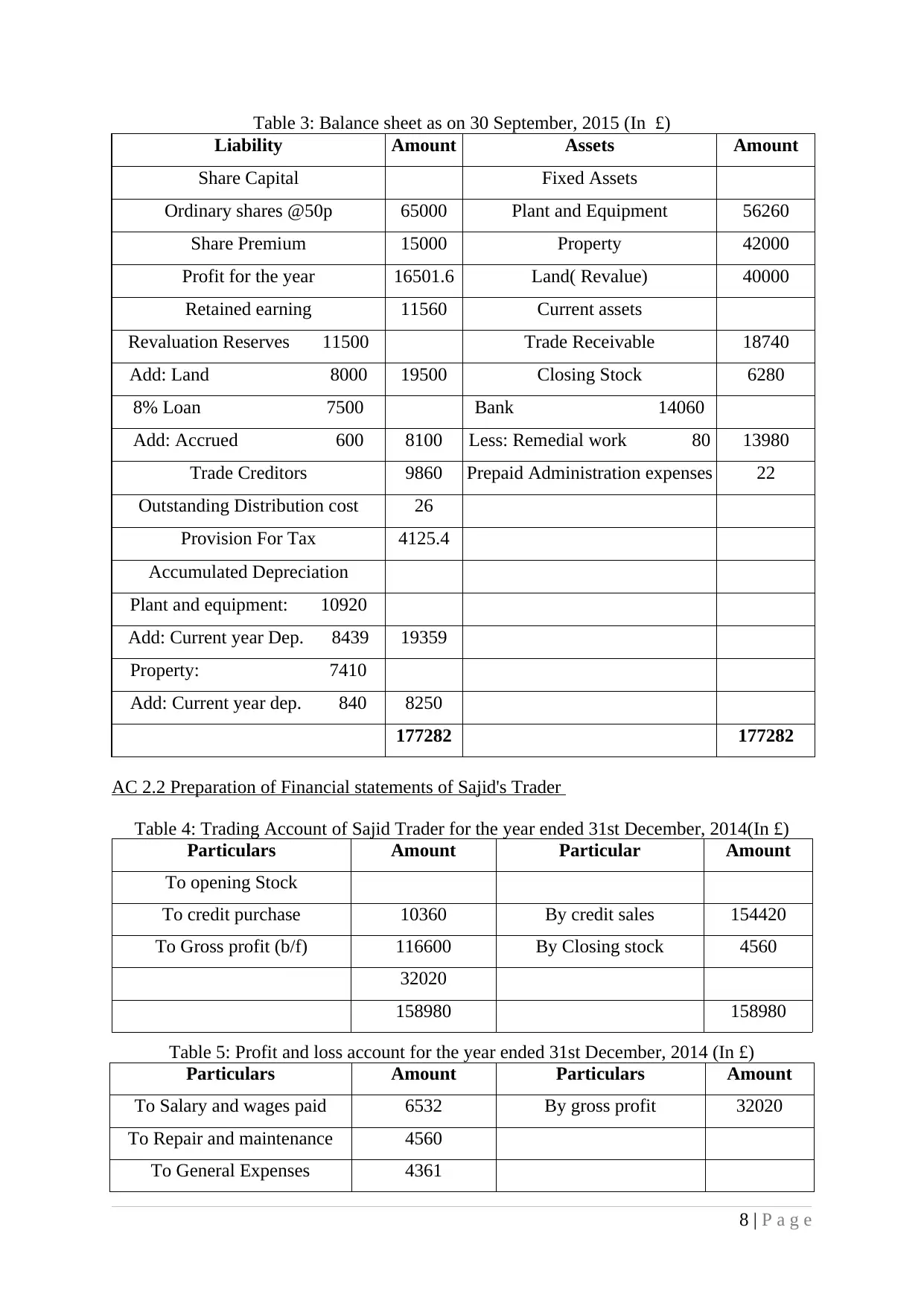

Table 3: Balance sheet as on 30 September, 2015 (In £)

Liability Amount Assets Amount

Share Capital Fixed Assets

Ordinary shares @50p 65000 Plant and Equipment 56260

Share Premium 15000 Property 42000

Profit for the year 16501.6 Land( Revalue) 40000

Retained earning 11560 Current assets

Revaluation Reserves 11500 Trade Receivable 18740

Add: Land 8000 19500 Closing Stock 6280

8% Loan 7500 Bank 14060

Add: Accrued 600 8100 Less: Remedial work 80 13980

Trade Creditors 9860 Prepaid Administration expenses 22

Outstanding Distribution cost 26

Provision For Tax 4125.4

Accumulated Depreciation

Plant and equipment: 10920

Add: Current year Dep. 8439 19359

Property: 7410

Add: Current year dep. 840 8250

177282 177282

AC 2.2 Preparation of Financial statements of Sajid's Trader

Table 4: Trading Account of Sajid Trader for the year ended 31st December, 2014(In £)

Particulars Amount Particular Amount

To opening Stock

To credit purchase 10360 By credit sales 154420

To Gross profit (b/f) 116600 By Closing stock 4560

32020

158980 158980

Table 5: Profit and loss account for the year ended 31st December, 2014 (In £)

Particulars Amount Particulars Amount

To Salary and wages paid 6532 By gross profit 32020

To Repair and maintenance 4560

To General Expenses 4361

8 | P a g e

Liability Amount Assets Amount

Share Capital Fixed Assets

Ordinary shares @50p 65000 Plant and Equipment 56260

Share Premium 15000 Property 42000

Profit for the year 16501.6 Land( Revalue) 40000

Retained earning 11560 Current assets

Revaluation Reserves 11500 Trade Receivable 18740

Add: Land 8000 19500 Closing Stock 6280

8% Loan 7500 Bank 14060

Add: Accrued 600 8100 Less: Remedial work 80 13980

Trade Creditors 9860 Prepaid Administration expenses 22

Outstanding Distribution cost 26

Provision For Tax 4125.4

Accumulated Depreciation

Plant and equipment: 10920

Add: Current year Dep. 8439 19359

Property: 7410

Add: Current year dep. 840 8250

177282 177282

AC 2.2 Preparation of Financial statements of Sajid's Trader

Table 4: Trading Account of Sajid Trader for the year ended 31st December, 2014(In £)

Particulars Amount Particular Amount

To opening Stock

To credit purchase 10360 By credit sales 154420

To Gross profit (b/f) 116600 By Closing stock 4560

32020

158980 158980

Table 5: Profit and loss account for the year ended 31st December, 2014 (In £)

Particulars Amount Particulars Amount

To Salary and wages paid 6532 By gross profit 32020

To Repair and maintenance 4560

To General Expenses 4361

8 | P a g e

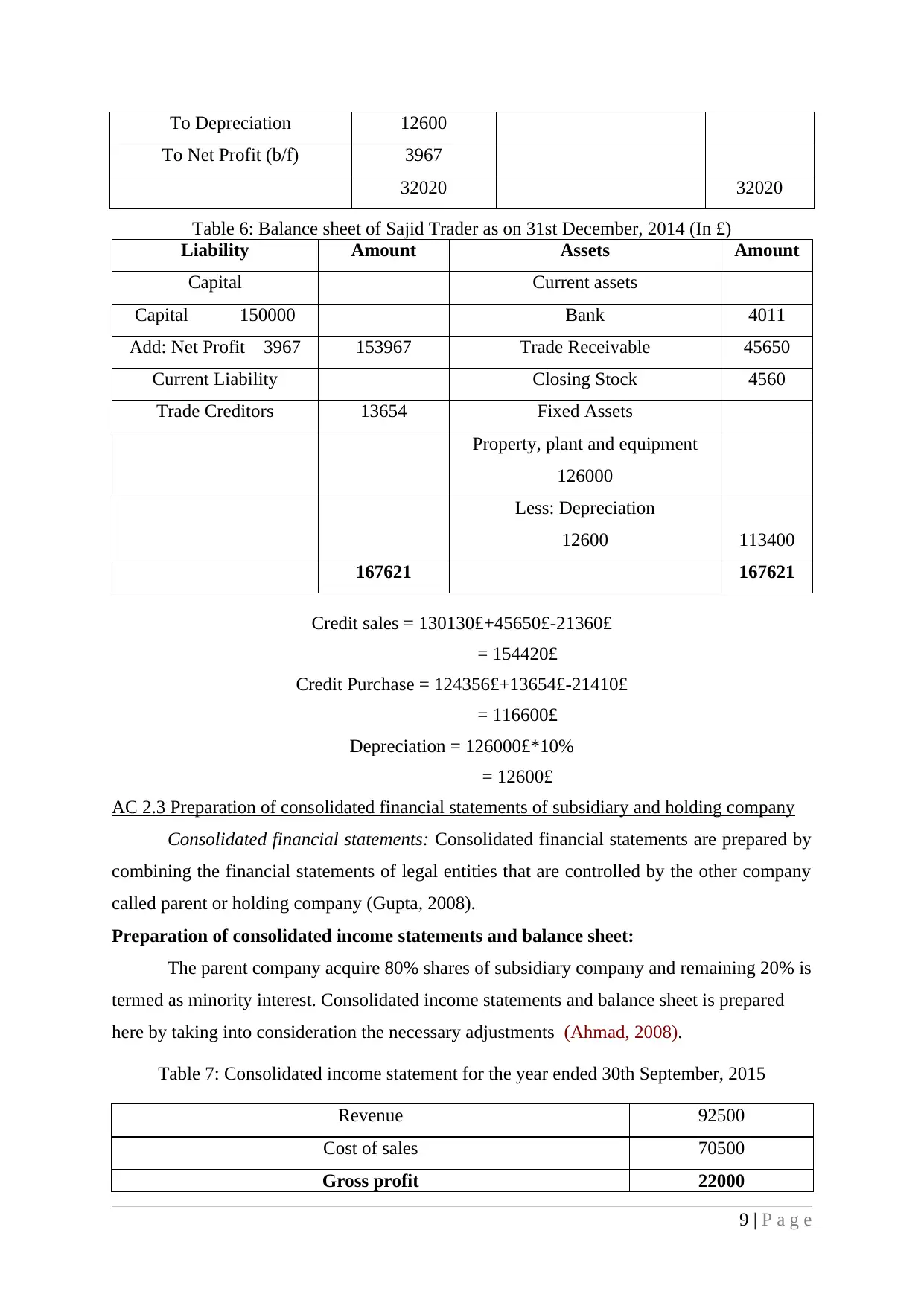

To Depreciation 12600

To Net Profit (b/f) 3967

32020 32020

Table 6: Balance sheet of Sajid Trader as on 31st December, 2014 (In £)

Liability Amount Assets Amount

Capital Current assets

Capital 150000 Bank 4011

Add: Net Profit 3967 153967 Trade Receivable 45650

Current Liability Closing Stock 4560

Trade Creditors 13654 Fixed Assets

Property, plant and equipment

126000

Less: Depreciation

12600 113400

167621 167621

Credit sales = 130130£+45650£-21360£

= 154420£

Credit Purchase = 124356£+13654£-21410£

= 116600£

Depreciation = 126000£*10%

= 12600£

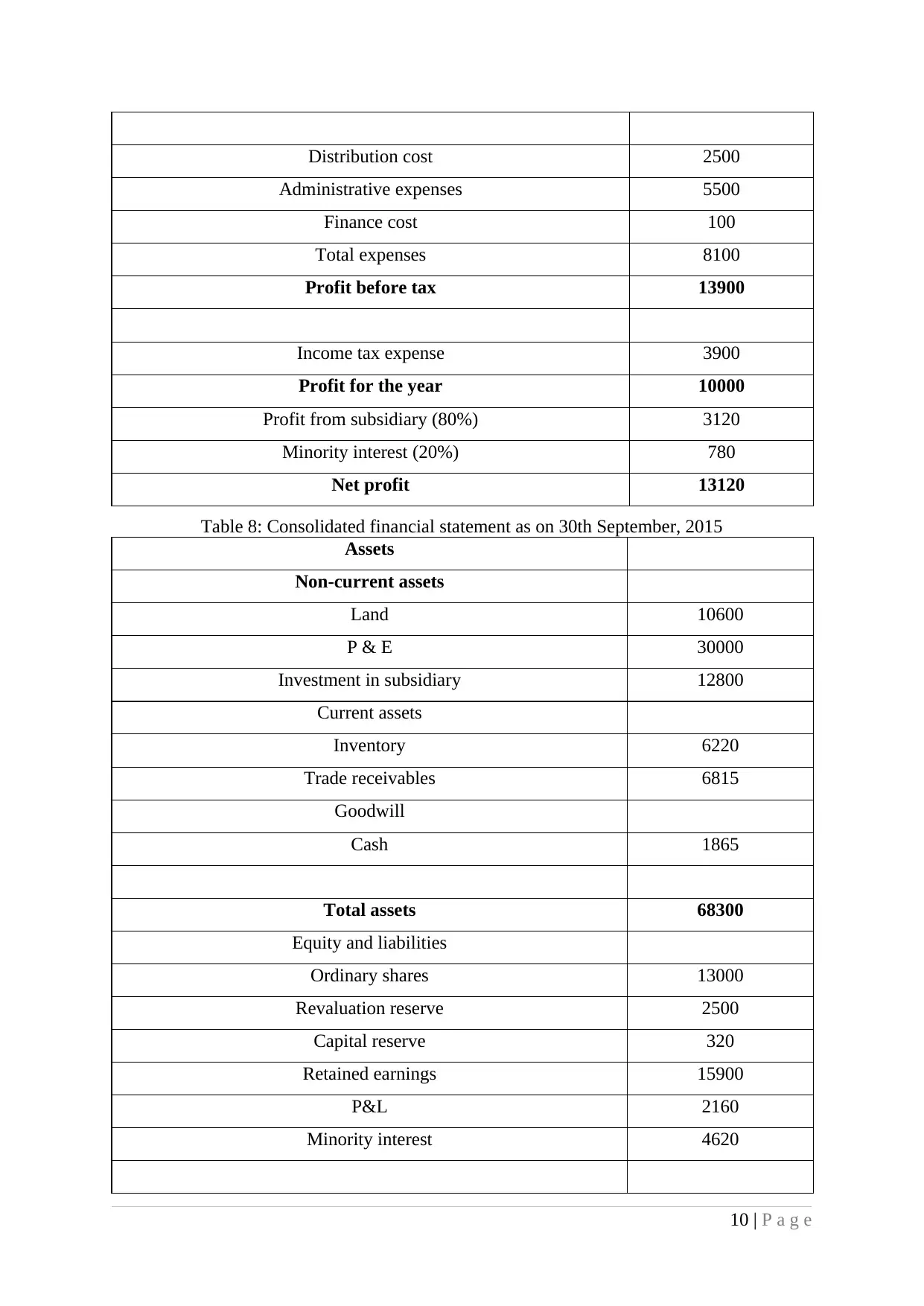

AC 2.3 Preparation of consolidated financial statements of subsidiary and holding company

Consolidated financial statements: Consolidated financial statements are prepared by

combining the financial statements of legal entities that are controlled by the other company

called parent or holding company (Gupta, 2008).

Preparation of consolidated income statements and balance sheet:

The parent company acquire 80% shares of subsidiary company and remaining 20% is

termed as minority interest. Consolidated income statements and balance sheet is prepared

here by taking into consideration the necessary adjustments (Ahmad, 2008).

Table 7: Consolidated income statement for the year ended 30th September, 2015

Revenue 92500

Cost of sales 70500

Gross profit 22000

9 | P a g e

To Net Profit (b/f) 3967

32020 32020

Table 6: Balance sheet of Sajid Trader as on 31st December, 2014 (In £)

Liability Amount Assets Amount

Capital Current assets

Capital 150000 Bank 4011

Add: Net Profit 3967 153967 Trade Receivable 45650

Current Liability Closing Stock 4560

Trade Creditors 13654 Fixed Assets

Property, plant and equipment

126000

Less: Depreciation

12600 113400

167621 167621

Credit sales = 130130£+45650£-21360£

= 154420£

Credit Purchase = 124356£+13654£-21410£

= 116600£

Depreciation = 126000£*10%

= 12600£

AC 2.3 Preparation of consolidated financial statements of subsidiary and holding company

Consolidated financial statements: Consolidated financial statements are prepared by

combining the financial statements of legal entities that are controlled by the other company

called parent or holding company (Gupta, 2008).

Preparation of consolidated income statements and balance sheet:

The parent company acquire 80% shares of subsidiary company and remaining 20% is

termed as minority interest. Consolidated income statements and balance sheet is prepared

here by taking into consideration the necessary adjustments (Ahmad, 2008).

Table 7: Consolidated income statement for the year ended 30th September, 2015

Revenue 92500

Cost of sales 70500

Gross profit 22000

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Distribution cost 2500

Administrative expenses 5500

Finance cost 100

Total expenses 8100

Profit before tax 13900

Income tax expense 3900

Profit for the year 10000

Profit from subsidiary (80%) 3120

Minority interest (20%) 780

Net profit 13120

Table 8: Consolidated financial statement as on 30th September, 2015

Assets

Non-current assets

Land 10600

P & E 30000

Investment in subsidiary 12800

Current assets

Inventory 6220

Trade receivables 6815

Goodwill

Cash 1865

Total assets 68300

Equity and liabilities

Ordinary shares 13000

Revaluation reserve 2500

Capital reserve 320

Retained earnings 15900

P&L 2160

Minority interest 4620

10 | P a g e

Administrative expenses 5500

Finance cost 100

Total expenses 8100

Profit before tax 13900

Income tax expense 3900

Profit for the year 10000

Profit from subsidiary (80%) 3120

Minority interest (20%) 780

Net profit 13120

Table 8: Consolidated financial statement as on 30th September, 2015

Assets

Non-current assets

Land 10600

P & E 30000

Investment in subsidiary 12800

Current assets

Inventory 6220

Trade receivables 6815

Goodwill

Cash 1865

Total assets 68300

Equity and liabilities

Ordinary shares 13000

Revaluation reserve 2500

Capital reserve 320

Retained earnings 15900

P&L 2160

Minority interest 4620

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Noncurrent liabilities

10% loans 13000

Current liabilities

Trade payable 12000

Bank overdraft 875

Tax 3925

Total liabilities and equities 68300

TASK 3

AC 3.1 Different users of financial statements

Shareholders and investors: Shareholders are the owners of company. They need

financial information to know their investment potential in order to acquire higher return.

Government: Government analyses the financial statements to know the tax liabilities

of company. It helps the government in making economic planning and decisions (Meynard,

2013).

Competitor: Competitors analyse financial statements so as to compare their own

performance with the competitors firms in order to take fruitful decisions.

Financial Institution: Banks and other institutions need financial information to know

the credit worthiness of business to take decision about providing loan facilities.

Manager: They use financial information to know the profitability and financial status

of company. They analyse the extent to which company is operating well to make effective

and strategic planning (Zager and Zager, 2006).

AC 3.2 Financial statements for various types of organizations

Sole Proprietorship: It is the most common type of organization where owner invests

his own fund so that the entire profits and losses will be available for him (Brayan, 2010). He

simply makes trading and profit and loss account as his income statement and the balance

sheet as well.

Partnership: This form of organization can be established by two or more persons.

They share profit and loss in the agreed ratio. Therefore, they prepare partner's capital

account, profit and loss appropriation account and balance sheet.

Company: Company is established by following the legal requirement of company’s

act (Bebbington, Gray and Laughlin, 2001). It prepares its statements according to the law of

act in which it is incorporated in order to satisfy the needs of all users.

11 | P a g e

10% loans 13000

Current liabilities

Trade payable 12000

Bank overdraft 875

Tax 3925

Total liabilities and equities 68300

TASK 3

AC 3.1 Different users of financial statements

Shareholders and investors: Shareholders are the owners of company. They need

financial information to know their investment potential in order to acquire higher return.

Government: Government analyses the financial statements to know the tax liabilities

of company. It helps the government in making economic planning and decisions (Meynard,

2013).

Competitor: Competitors analyse financial statements so as to compare their own

performance with the competitors firms in order to take fruitful decisions.

Financial Institution: Banks and other institutions need financial information to know

the credit worthiness of business to take decision about providing loan facilities.

Manager: They use financial information to know the profitability and financial status

of company. They analyse the extent to which company is operating well to make effective

and strategic planning (Zager and Zager, 2006).

AC 3.2 Financial statements for various types of organizations

Sole Proprietorship: It is the most common type of organization where owner invests

his own fund so that the entire profits and losses will be available for him (Brayan, 2010). He

simply makes trading and profit and loss account as his income statement and the balance

sheet as well.

Partnership: This form of organization can be established by two or more persons.

They share profit and loss in the agreed ratio. Therefore, they prepare partner's capital

account, profit and loss appropriation account and balance sheet.

Company: Company is established by following the legal requirement of company’s

act (Bebbington, Gray and Laughlin, 2001). It prepares its statements according to the law of

act in which it is incorporated in order to satisfy the needs of all users.

11 | P a g e

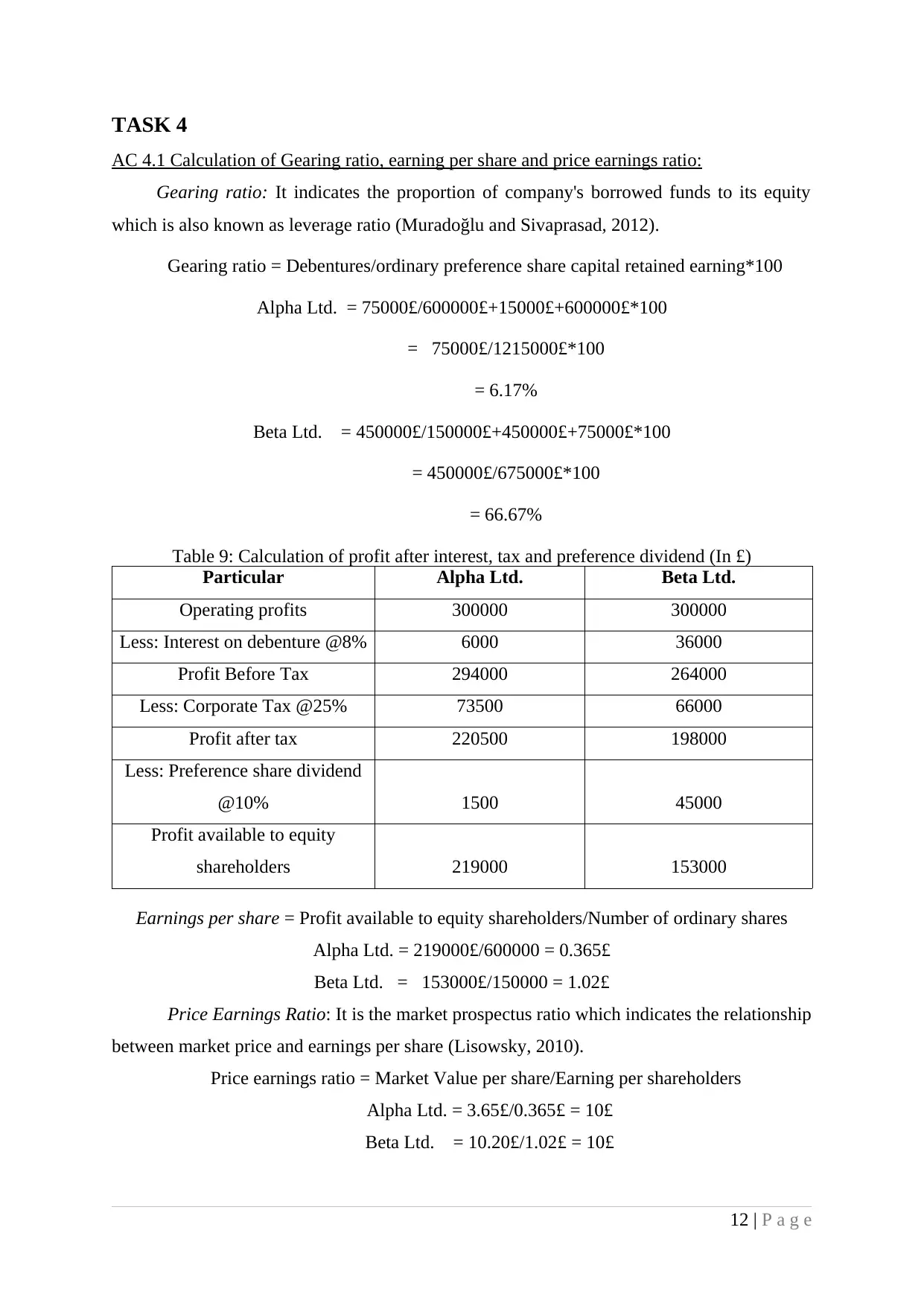

TASK 4

AC 4.1 Calculation of Gearing ratio, earning per share and price earnings ratio:

Gearing ratio: It indicates the proportion of company's borrowed funds to its equity

which is also known as leverage ratio (Muradoğlu and Sivaprasad, 2012).

Gearing ratio = Debentures/ordinary preference share capital retained earning*100

Alpha Ltd. = 75000£/600000£+15000£+600000£*100

= 75000£/1215000£*100

= 6.17%

Beta Ltd. = 450000£/150000£+450000£+75000£*100

= 450000£/675000£*100

= 66.67%

Table 9: Calculation of profit after interest, tax and preference dividend (In £)

Particular Alpha Ltd. Beta Ltd.

Operating profits 300000 300000

Less: Interest on debenture @8% 6000 36000

Profit Before Tax 294000 264000

Less: Corporate Tax @25% 73500 66000

Profit after tax 220500 198000

Less: Preference share dividend

@10% 1500 45000

Profit available to equity

shareholders 219000 153000

Earnings per share = Profit available to equity shareholders/Number of ordinary shares

Alpha Ltd. = 219000£/600000 = 0.365£

Beta Ltd. = 153000£/150000 = 1.02£

Price Earnings Ratio: It is the market prospectus ratio which indicates the relationship

between market price and earnings per share (Lisowsky, 2010).

Price earnings ratio = Market Value per share/Earning per shareholders

Alpha Ltd. = 3.65£/0.365£ = 10£

Beta Ltd. = 10.20£/1.02£ = 10£

12 | P a g e

AC 4.1 Calculation of Gearing ratio, earning per share and price earnings ratio:

Gearing ratio: It indicates the proportion of company's borrowed funds to its equity

which is also known as leverage ratio (Muradoğlu and Sivaprasad, 2012).

Gearing ratio = Debentures/ordinary preference share capital retained earning*100

Alpha Ltd. = 75000£/600000£+15000£+600000£*100

= 75000£/1215000£*100

= 6.17%

Beta Ltd. = 450000£/150000£+450000£+75000£*100

= 450000£/675000£*100

= 66.67%

Table 9: Calculation of profit after interest, tax and preference dividend (In £)

Particular Alpha Ltd. Beta Ltd.

Operating profits 300000 300000

Less: Interest on debenture @8% 6000 36000

Profit Before Tax 294000 264000

Less: Corporate Tax @25% 73500 66000

Profit after tax 220500 198000

Less: Preference share dividend

@10% 1500 45000

Profit available to equity

shareholders 219000 153000

Earnings per share = Profit available to equity shareholders/Number of ordinary shares

Alpha Ltd. = 219000£/600000 = 0.365£

Beta Ltd. = 153000£/150000 = 1.02£

Price Earnings Ratio: It is the market prospectus ratio which indicates the relationship

between market price and earnings per share (Lisowsky, 2010).

Price earnings ratio = Market Value per share/Earning per shareholders

Alpha Ltd. = 3.65£/0.365£ = 10£

Beta Ltd. = 10.20£/1.02£ = 10£

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.