Financial Reporting: Analysis of Marks and Spencer's Statements

VerifiedAdded on 2020/12/09

|14

|3532

|241

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, specifically focusing on the case of Marks & Spencer. It begins with an introduction to the main purposes of financial reporting and delves into the regulatory and conceptual frameworks that govern it. The report identifies and examines the various stakeholders of a company, highlighting the value of financial reporting for growth and development. It includes an analysis of Marks & Spencer's financial statements, including the statement of profit and loss, changes in equity, and financial position. The report also interprets the financial statements of Marks & Spencer and explores the differences between IFRS and IAS, evaluating the benefits of IFRS and ascertaining the degree of compliance. The report emphasizes the importance of financial reporting for investment decisions, internal management, and attracting international investors. The financial statements and analysis provided are crucial for understanding the financial health and performance of the company.

Financial Reporting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

1. Main Purpose of financial reporting........................................................................................1

2. Regulatory and conceptual framework of financial reporting.................................................2

3. Stakeholder of company..........................................................................................................3

4. Values of financial reporting for growth and development.....................................................4

5. Financial statements of the organisation..................................................................................5

6. Interpretation of financial statement of Marks and Spencer....................................................6

7 Difference between IFRS and IAS...........................................................................................7

8. Evaluation of benefits of IFRS................................................................................................7

9 Ascertaining the varying degree of compliance with IFRS......................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

1. Main Purpose of financial reporting........................................................................................1

2. Regulatory and conceptual framework of financial reporting.................................................2

3. Stakeholder of company..........................................................................................................3

4. Values of financial reporting for growth and development.....................................................4

5. Financial statements of the organisation..................................................................................5

6. Interpretation of financial statement of Marks and Spencer....................................................6

7 Difference between IFRS and IAS...........................................................................................7

8. Evaluation of benefits of IFRS................................................................................................7

9 Ascertaining the varying degree of compliance with IFRS......................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial reporting focuses to play an important role of accounting standard and principle

that support in creating valuable report and financial statement of company (Financial statement,

2018). This process is relate to examining, gathering and posting financial information into

balance sheet, cash flow statement and other useful financial documents. This support internal

manager to make crucial decision so that financial strength and position of company could be

improved. To understand the importance of financial reporting Mark & Spenser is selected.

In this project report, the main objective of financial reporting, its basic concept,

regulatory and conceptual standard are discussed. Report shows main stakeholder for company,

importance of reporting and interpretation of last two year financial statements. The main

purpose of report is to describe the importance of IFRS and its difference With IAS.

1. Main Purpose of financial reporting.

In accounting, financial reporting is defined as the process of formulating important

financial statements that disclose the financial strength and position of company during an

accounting year. These statement are presented to shareholder, creditor, investor so that actual

creditworthiness of company can be ascertained. With the help of detail report and statement

internal management of Mark & Spenser are able to make effective plan to improve the

profitability and productivity. It is very crucial that report must be create according to the

accounting standard and must be faithful, transparent and free from any misleading transaction.

The main objective and purpose of financial report to Mark & Spenser are described below:

Financial reporting gives complete and faithful financial information to outside investor

so that they can make investment decision in M&S.

With the support of transparent report, internal management of M&S are able to examine

performance of company during a particular period.

It provide actual outcome of the various business activity to the external stakeholder that

increase profit, market share and sales.

Importance of Financial reporting.

The main significance of financial reporting is to attract international investor so that,

M&S may expand its business at global level (Chae and Oh, 2016).

Financial reporting focuses to play an important role of accounting standard and principle

that support in creating valuable report and financial statement of company (Financial statement,

2018). This process is relate to examining, gathering and posting financial information into

balance sheet, cash flow statement and other useful financial documents. This support internal

manager to make crucial decision so that financial strength and position of company could be

improved. To understand the importance of financial reporting Mark & Spenser is selected.

In this project report, the main objective of financial reporting, its basic concept,

regulatory and conceptual standard are discussed. Report shows main stakeholder for company,

importance of reporting and interpretation of last two year financial statements. The main

purpose of report is to describe the importance of IFRS and its difference With IAS.

1. Main Purpose of financial reporting.

In accounting, financial reporting is defined as the process of formulating important

financial statements that disclose the financial strength and position of company during an

accounting year. These statement are presented to shareholder, creditor, investor so that actual

creditworthiness of company can be ascertained. With the help of detail report and statement

internal management of Mark & Spenser are able to make effective plan to improve the

profitability and productivity. It is very crucial that report must be create according to the

accounting standard and must be faithful, transparent and free from any misleading transaction.

The main objective and purpose of financial report to Mark & Spenser are described below:

Financial reporting gives complete and faithful financial information to outside investor

so that they can make investment decision in M&S.

With the support of transparent report, internal management of M&S are able to examine

performance of company during a particular period.

It provide actual outcome of the various business activity to the external stakeholder that

increase profit, market share and sales.

Importance of Financial reporting.

The main significance of financial reporting is to attract international investor so that,

M&S may expand its business at global level (Chae and Oh, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Decently managed statements are really crucial for bid, government activity and labour

contracts because it help to give summary of the company and its business operation to

external parties.

So, it is very crucial that Mark & Spenser develop final account and statement, that

support them to manage, control business operation and increase the profitability and financial

position. It is very important to analyse the actual performance of company as it support to

execute further project more effectively (Al-Matari, 2013).

2. Regulatory and conceptual framework of financial reporting.

Regulatory and Conceptual Framework: In present era, it is very crucial that company

should use valuable analytical tool and apply accounting standard and principle prepare financial

statement during an accounting year. So regulatory framework are defined as the set of legal

standard and rules implement by UK legal authority. These framework are to be followed by

each and every company performing business in UK. On the other side conceptual framework

are defined as the tool with some variable that help to analyse the performance of business

operation. With the support of conceptual framework mark & Spenser is able to analyse the

overall performance of different business project and operations. Similarly, with the help of

regulatory framework accountant of M&S are able to create faithful financial statement that

further support to ascertain financial position and status during an accounting year.

Purpose of regulatory and conceptual framework:

The main significance of Regulatory frameworks is to help internal manager to formulate

statements in suitable manner.

And main purpose of Conceptual framework is to examine the actual performance of

company that is displayed to stakeholder so that investment decision are made in M&S.

Mark & Spenser is applying different set of regulation to maintain financial record that

are set By IASB that are imposed in the form of IFRS. International financial reporting standard

are set of key principle that are set by authority. Some of Key principle are discussed below:

IFRS 3: These are related to actual concept of business combination of consolidation and

acquisition. It guide manager to combine all there liabilities and assets that help to pay

debt of company (Duncan, 2014).

IFRS 9: This is related the set of rules that describe the treatment of different transaction.

It help to protection of accounting and damage of financial assets within company.

contracts because it help to give summary of the company and its business operation to

external parties.

So, it is very crucial that Mark & Spenser develop final account and statement, that

support them to manage, control business operation and increase the profitability and financial

position. It is very important to analyse the actual performance of company as it support to

execute further project more effectively (Al-Matari, 2013).

2. Regulatory and conceptual framework of financial reporting.

Regulatory and Conceptual Framework: In present era, it is very crucial that company

should use valuable analytical tool and apply accounting standard and principle prepare financial

statement during an accounting year. So regulatory framework are defined as the set of legal

standard and rules implement by UK legal authority. These framework are to be followed by

each and every company performing business in UK. On the other side conceptual framework

are defined as the tool with some variable that help to analyse the performance of business

operation. With the support of conceptual framework mark & Spenser is able to analyse the

overall performance of different business project and operations. Similarly, with the help of

regulatory framework accountant of M&S are able to create faithful financial statement that

further support to ascertain financial position and status during an accounting year.

Purpose of regulatory and conceptual framework:

The main significance of Regulatory frameworks is to help internal manager to formulate

statements in suitable manner.

And main purpose of Conceptual framework is to examine the actual performance of

company that is displayed to stakeholder so that investment decision are made in M&S.

Mark & Spenser is applying different set of regulation to maintain financial record that

are set By IASB that are imposed in the form of IFRS. International financial reporting standard

are set of key principle that are set by authority. Some of Key principle are discussed below:

IFRS 3: These are related to actual concept of business combination of consolidation and

acquisition. It guide manager to combine all there liabilities and assets that help to pay

debt of company (Duncan, 2014).

IFRS 9: This is related the set of rules that describe the treatment of different transaction.

It help to protection of accounting and damage of financial assets within company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Qualitative features of financial reporting.

Relevance: It is key significance that companies should record financial data into

financial account and statement that aid to compare actual performance and position. Financial

report are help that recorded information is more reliable and accurate.

Faithful Presentation: This is beneficial for M&S as financial reporting assist to give

detail appropriate information to external shareholder so that investment decision are made.

3. Stakeholder of company.

Stakeholder are defined as the valuable part for company as they make important

investment decision in company that support to run business operation in appropriate manner.

These external and internal parties have full right to get correct financial information about

company business. M&S have different kind of stakeholder such as investors, manager,

employees government etc. Financial reporting provide valuable benefit to these stakeholder that

are defined below:

Internal: These stakeholder are directly related to different business operation performed

in Mark and Spenser. Some of these are :

Shareholder: These group of individual are the owner of business that gives suitable

amount to run business activity of company (Eker and Aytaç, 2016). In M&S, with the help of

accurate financial statements shareholder analyse and figure out that weather money is

effectively used and give best result in future.

Manager: In M&S Manager use financial statement to analyse the performance of

different business operation and employees. In case if company is lacking because of any reason

then manager make effective plans to improve the performance.

External: These stakeholder are not part of company but have right to get the financial

information for an accounting year.

Investor: These group of individual make investment in companies in order to acquire

higher profit. Financial information help inverter to ascertain the financial status of of Mark &

Spenser and make investment decision. As company is doing well so there are more number of

investor.

Customer: They are consider to be the backbone for company. As more number of

customer company is going to earn more profit. Financial information help customer to

Relevance: It is key significance that companies should record financial data into

financial account and statement that aid to compare actual performance and position. Financial

report are help that recorded information is more reliable and accurate.

Faithful Presentation: This is beneficial for M&S as financial reporting assist to give

detail appropriate information to external shareholder so that investment decision are made.

3. Stakeholder of company.

Stakeholder are defined as the valuable part for company as they make important

investment decision in company that support to run business operation in appropriate manner.

These external and internal parties have full right to get correct financial information about

company business. M&S have different kind of stakeholder such as investors, manager,

employees government etc. Financial reporting provide valuable benefit to these stakeholder that

are defined below:

Internal: These stakeholder are directly related to different business operation performed

in Mark and Spenser. Some of these are :

Shareholder: These group of individual are the owner of business that gives suitable

amount to run business activity of company (Eker and Aytaç, 2016). In M&S, with the help of

accurate financial statements shareholder analyse and figure out that weather money is

effectively used and give best result in future.

Manager: In M&S Manager use financial statement to analyse the performance of

different business operation and employees. In case if company is lacking because of any reason

then manager make effective plans to improve the performance.

External: These stakeholder are not part of company but have right to get the financial

information for an accounting year.

Investor: These group of individual make investment in companies in order to acquire

higher profit. Financial information help inverter to ascertain the financial status of of Mark &

Spenser and make investment decision. As company is doing well so there are more number of

investor.

Customer: They are consider to be the backbone for company. As more number of

customer company is going to earn more profit. Financial information help customer to

determine the market status and image of Mark & Spencer so that they may attracted to buy

product.

Creditor: These are people who provide raw material and goods to Mark & Spenser.

With the help of financial information supplier are able to ascertain the pay back ability of

company.

4. Values of financial reporting for growth and development.

Financial reporting support to accomplish main objective and determine the growth and

development opportunities for companies (Elbayoumi and Awadallah, 2017). As, main objective

of M&S is to build best goodwill, attract more creditor, customer and expand business operation

at global level that will further support to maximise profit. These all certain objective could be

achieved if financial report and statement of companies are transparent, accurate and provide

valuable information to all external parties. It is very common that investor are attracted to those

companies which are performing well in market and provide return at high rates. Some of the

basic objective of Mark & Spenser are discussed below:

Profit maximisation: Financial statement help Mark & Spenser to analyse that they are

performing well in market. Accurate and appropriate statement will support to earn competitive

advantage in market and earn huge profit. Closing accounts of Marks and Spencer aid to examine

organisational efficiency and profits during a period. The internal manager ascertain the actual

position of funds that are used by M&S and determine the expenses on different project that help

to enhance sales and maintain profit.

Customer satisfaction: Customer are satisfied when company provide valuable goods

and services at faithful rate and with best quality. Financial statement help new customer to

ascertain that M&S have good market image, as they are providing best quality of goods.

Therefore large number of consumer will move to use product and services provide by M&S.

Build global image: Financial statement help companies to determine the position in

market and support them to build strategies to grow business and expand business at global level.

With the good market image Mark & Spenser are able to attract more number of consumer and

attain higher market share (Formisano, Fedele and Calabrese, 2018.).

5. Financial statements of the organisation

A: Statement of profit and loss:

Particular Amount

product.

Creditor: These are people who provide raw material and goods to Mark & Spenser.

With the help of financial information supplier are able to ascertain the pay back ability of

company.

4. Values of financial reporting for growth and development.

Financial reporting support to accomplish main objective and determine the growth and

development opportunities for companies (Elbayoumi and Awadallah, 2017). As, main objective

of M&S is to build best goodwill, attract more creditor, customer and expand business operation

at global level that will further support to maximise profit. These all certain objective could be

achieved if financial report and statement of companies are transparent, accurate and provide

valuable information to all external parties. It is very common that investor are attracted to those

companies which are performing well in market and provide return at high rates. Some of the

basic objective of Mark & Spenser are discussed below:

Profit maximisation: Financial statement help Mark & Spenser to analyse that they are

performing well in market. Accurate and appropriate statement will support to earn competitive

advantage in market and earn huge profit. Closing accounts of Marks and Spencer aid to examine

organisational efficiency and profits during a period. The internal manager ascertain the actual

position of funds that are used by M&S and determine the expenses on different project that help

to enhance sales and maintain profit.

Customer satisfaction: Customer are satisfied when company provide valuable goods

and services at faithful rate and with best quality. Financial statement help new customer to

ascertain that M&S have good market image, as they are providing best quality of goods.

Therefore large number of consumer will move to use product and services provide by M&S.

Build global image: Financial statement help companies to determine the position in

market and support them to build strategies to grow business and expand business at global level.

With the good market image Mark & Spenser are able to attract more number of consumer and

attain higher market share (Formisano, Fedele and Calabrese, 2018.).

5. Financial statements of the organisation

A: Statement of profit and loss:

Particular Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

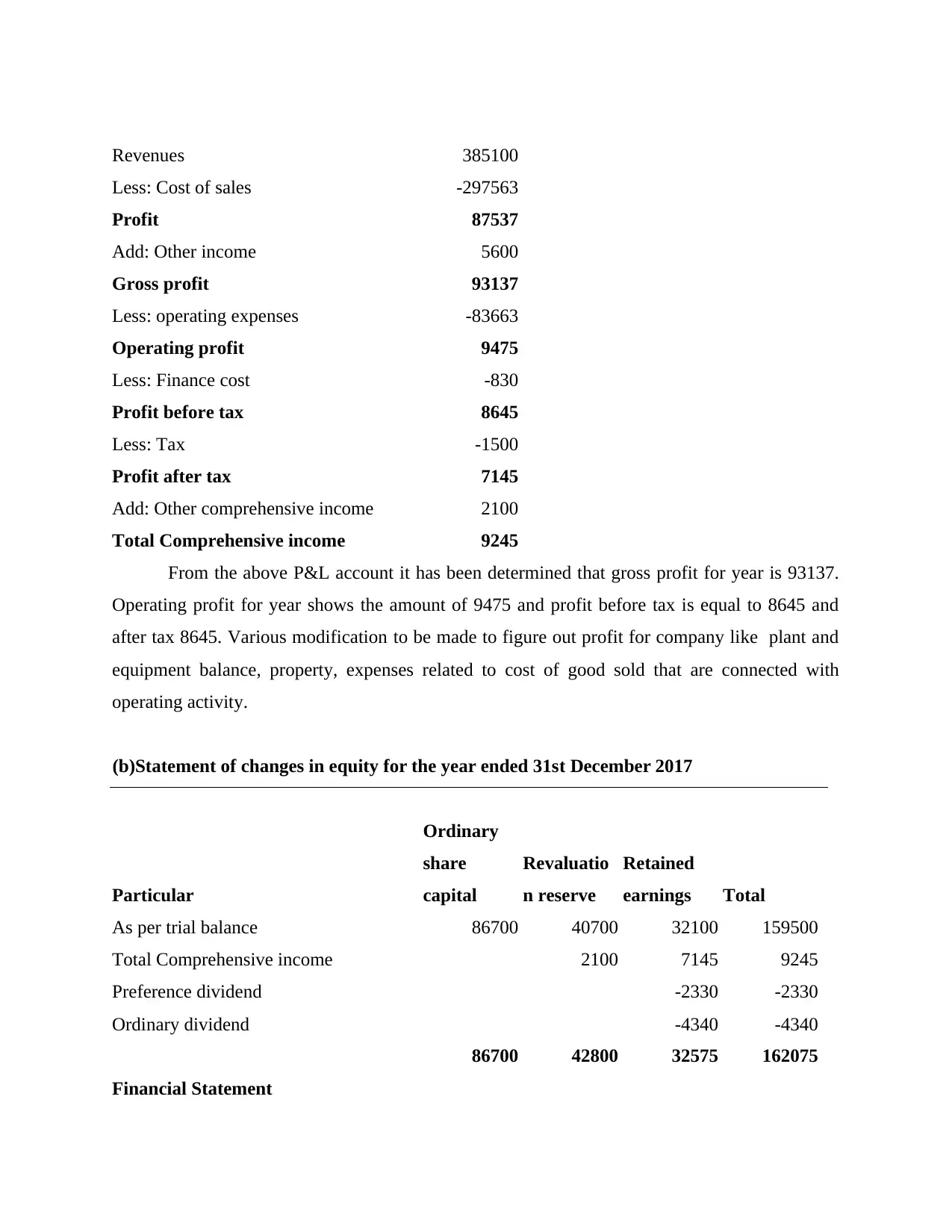

Revenues 385100

Less: Cost of sales -297563

Profit 87537

Add: Other income 5600

Gross profit 93137

Less: operating expenses -83663

Operating profit 9475

Less: Finance cost -830

Profit before tax 8645

Less: Tax -1500

Profit after tax 7145

Add: Other comprehensive income 2100

Total Comprehensive income 9245

From the above P&L account it has been determined that gross profit for year is 93137.

Operating profit for year shows the amount of 9475 and profit before tax is equal to 8645 and

after tax 8645. Various modification to be made to figure out profit for company like plant and

equipment balance, property, expenses related to cost of good sold that are connected with

operating activity.

(b)Statement of changes in equity for the year ended 31st December 2017

Particular

Ordinary

share

capital

Revaluatio

n reserve

Retained

earnings Total

As per trial balance 86700 40700 32100 159500

Total Comprehensive income 2100 7145 9245

Preference dividend -2330 -2330

Ordinary dividend -4340 -4340

86700 42800 32575 162075

Financial Statement

Less: Cost of sales -297563

Profit 87537

Add: Other income 5600

Gross profit 93137

Less: operating expenses -83663

Operating profit 9475

Less: Finance cost -830

Profit before tax 8645

Less: Tax -1500

Profit after tax 7145

Add: Other comprehensive income 2100

Total Comprehensive income 9245

From the above P&L account it has been determined that gross profit for year is 93137.

Operating profit for year shows the amount of 9475 and profit before tax is equal to 8645 and

after tax 8645. Various modification to be made to figure out profit for company like plant and

equipment balance, property, expenses related to cost of good sold that are connected with

operating activity.

(b)Statement of changes in equity for the year ended 31st December 2017

Particular

Ordinary

share

capital

Revaluatio

n reserve

Retained

earnings Total

As per trial balance 86700 40700 32100 159500

Total Comprehensive income 2100 7145 9245

Preference dividend -2330 -2330

Ordinary dividend -4340 -4340

86700 42800 32575 162075

Financial Statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

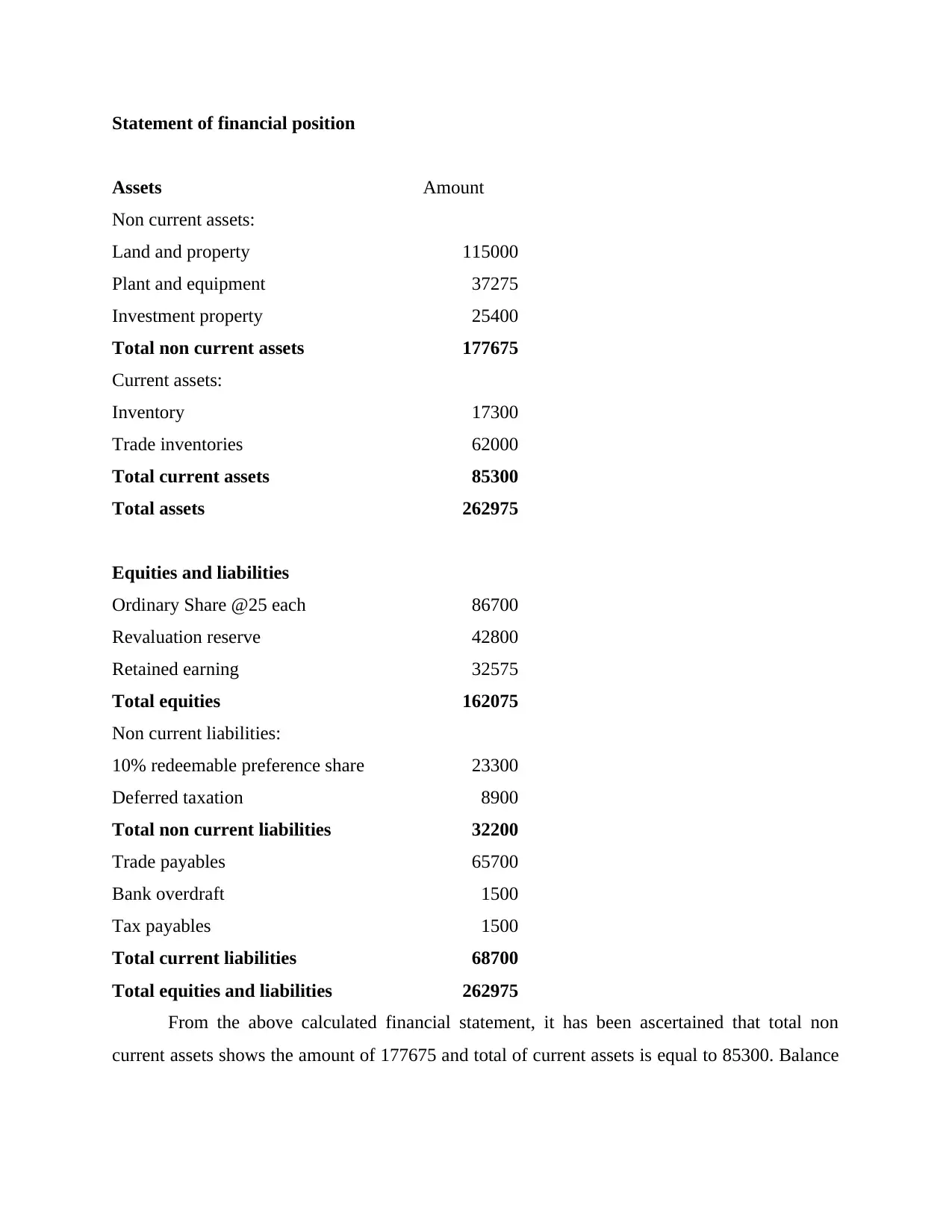

Statement of financial position

Assets Amount

Non current assets:

Land and property 115000

Plant and equipment 37275

Investment property 25400

Total non current assets 177675

Current assets:

Inventory 17300

Trade inventories 62000

Total current assets 85300

Total assets 262975

Equities and liabilities

Ordinary Share @25 each 86700

Revaluation reserve 42800

Retained earning 32575

Total equities 162075

Non current liabilities:

10% redeemable preference share 23300

Deferred taxation 8900

Total non current liabilities 32200

Trade payables 65700

Bank overdraft 1500

Tax payables 1500

Total current liabilities 68700

Total equities and liabilities 262975

From the above calculated financial statement, it has been ascertained that total non

current assets shows the amount of 177675 and total of current assets is equal to 85300. Balance

Assets Amount

Non current assets:

Land and property 115000

Plant and equipment 37275

Investment property 25400

Total non current assets 177675

Current assets:

Inventory 17300

Trade inventories 62000

Total current assets 85300

Total assets 262975

Equities and liabilities

Ordinary Share @25 each 86700

Revaluation reserve 42800

Retained earning 32575

Total equities 162075

Non current liabilities:

10% redeemable preference share 23300

Deferred taxation 8900

Total non current liabilities 32200

Trade payables 65700

Bank overdraft 1500

Tax payables 1500

Total current liabilities 68700

Total equities and liabilities 262975

From the above calculated financial statement, it has been ascertained that total non

current assets shows the amount of 177675 and total of current assets is equal to 85300. Balance

of total current liabilities 32200 and total equity and liabilities shows the balance of 262975 that

is equal to total assets.

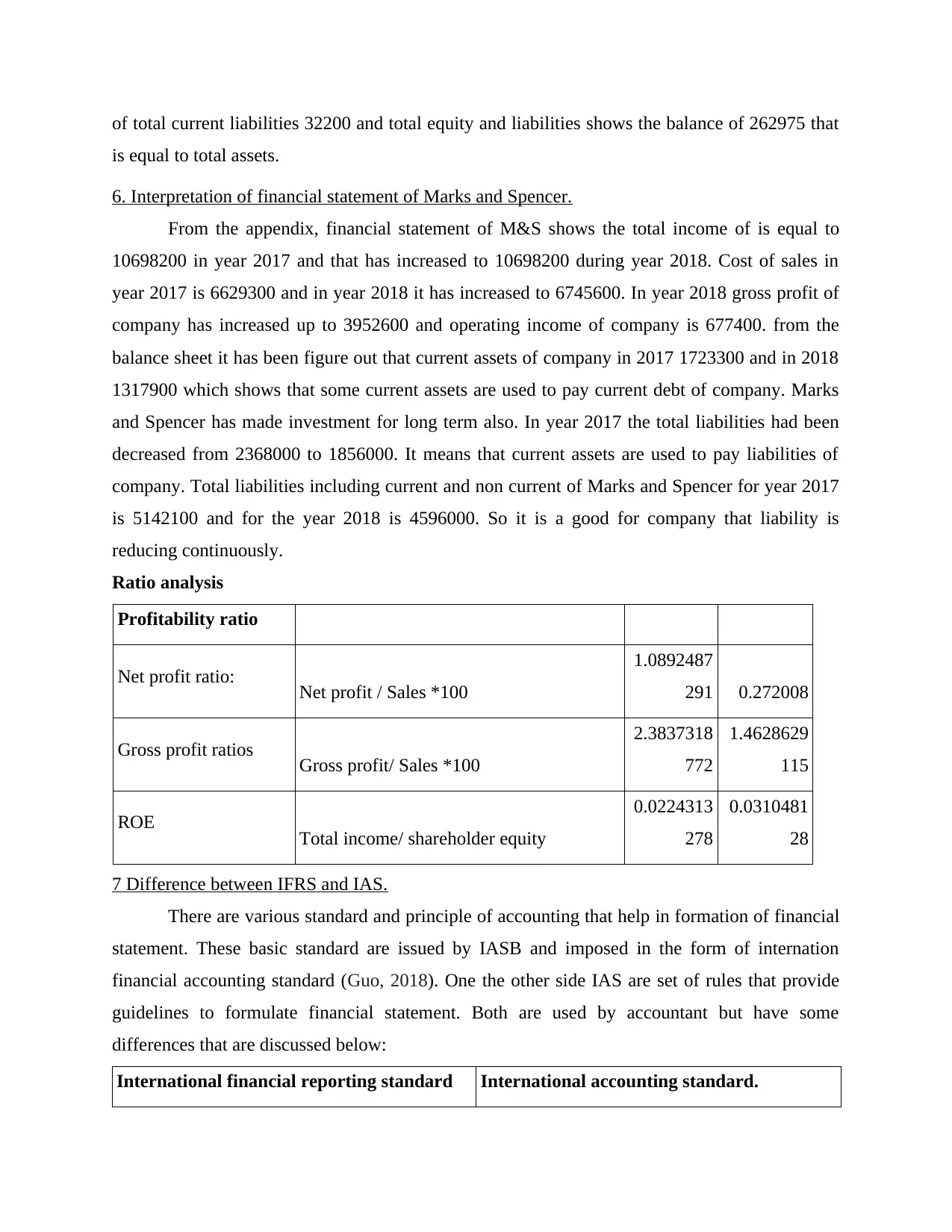

6. Interpretation of financial statement of Marks and Spencer.

From the appendix, financial statement of M&S shows the total income of is equal to

10698200 in year 2017 and that has increased to 10698200 during year 2018. Cost of sales in

year 2017 is 6629300 and in year 2018 it has increased to 6745600. In year 2018 gross profit of

company has increased up to 3952600 and operating income of company is 677400. from the

balance sheet it has been figure out that current assets of company in 2017 1723300 and in 2018

1317900 which shows that some current assets are used to pay current debt of company. Marks

and Spencer has made investment for long term also. In year 2017 the total liabilities had been

decreased from 2368000 to 1856000. It means that current assets are used to pay liabilities of

company. Total liabilities including current and non current of Marks and Spencer for year 2017

is 5142100 and for the year 2018 is 4596000. So it is a good for company that liability is

reducing continuously.

Ratio analysis

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.0892487

291 0.272008

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

7 Difference between IFRS and IAS.

There are various standard and principle of accounting that help in formation of financial

statement. These basic standard are issued by IASB and imposed in the form of internation

financial accounting standard (Guo, 2018). One the other side IAS are set of rules that provide

guidelines to formulate financial statement. Both are used by accountant but have some

differences that are discussed below:

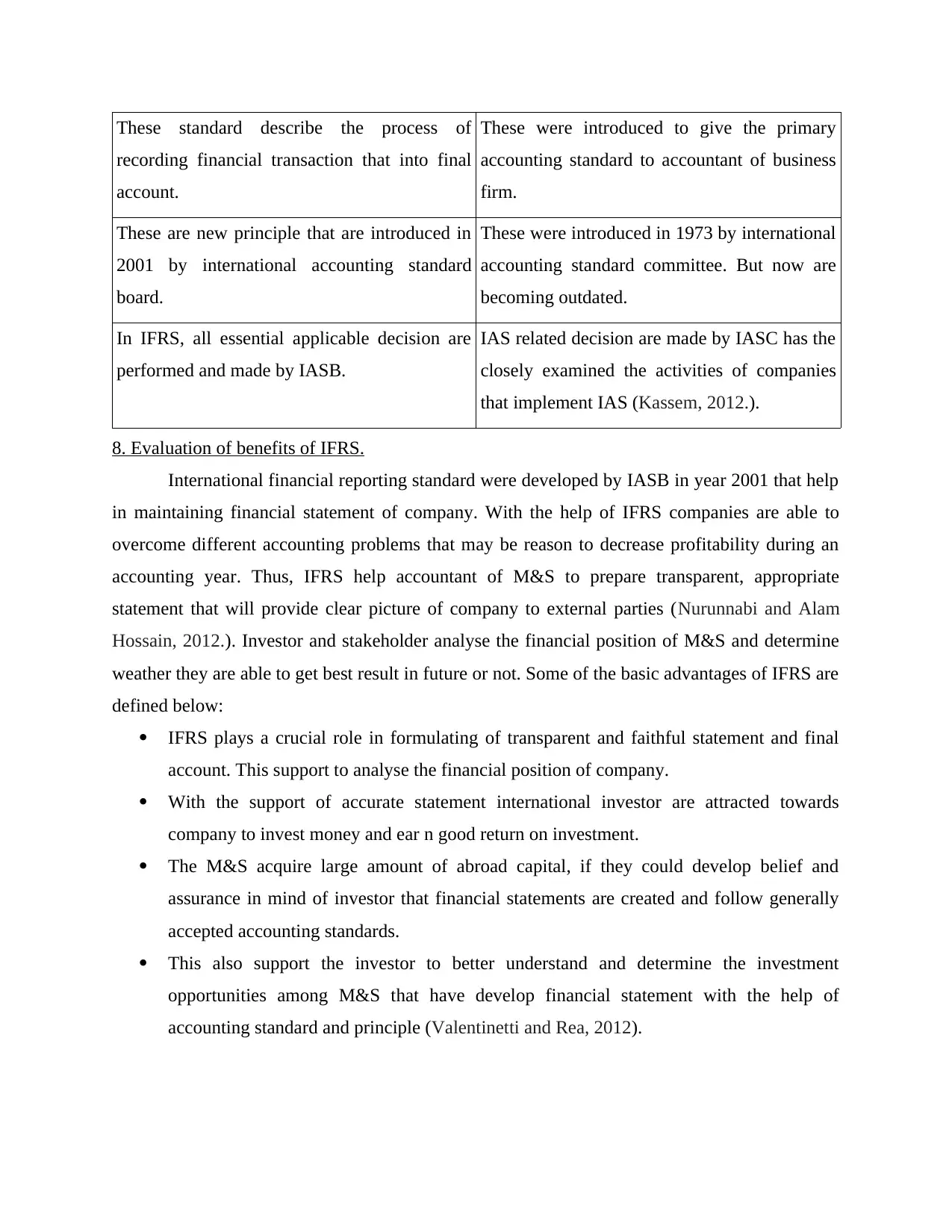

International financial reporting standard International accounting standard.

is equal to total assets.

6. Interpretation of financial statement of Marks and Spencer.

From the appendix, financial statement of M&S shows the total income of is equal to

10698200 in year 2017 and that has increased to 10698200 during year 2018. Cost of sales in

year 2017 is 6629300 and in year 2018 it has increased to 6745600. In year 2018 gross profit of

company has increased up to 3952600 and operating income of company is 677400. from the

balance sheet it has been figure out that current assets of company in 2017 1723300 and in 2018

1317900 which shows that some current assets are used to pay current debt of company. Marks

and Spencer has made investment for long term also. In year 2017 the total liabilities had been

decreased from 2368000 to 1856000. It means that current assets are used to pay liabilities of

company. Total liabilities including current and non current of Marks and Spencer for year 2017

is 5142100 and for the year 2018 is 4596000. So it is a good for company that liability is

reducing continuously.

Ratio analysis

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.0892487

291 0.272008

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

7 Difference between IFRS and IAS.

There are various standard and principle of accounting that help in formation of financial

statement. These basic standard are issued by IASB and imposed in the form of internation

financial accounting standard (Guo, 2018). One the other side IAS are set of rules that provide

guidelines to formulate financial statement. Both are used by accountant but have some

differences that are discussed below:

International financial reporting standard International accounting standard.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

These standard describe the process of

recording financial transaction that into final

account.

These were introduced to give the primary

accounting standard to accountant of business

firm.

These are new principle that are introduced in

2001 by international accounting standard

board.

These were introduced in 1973 by international

accounting standard committee. But now are

becoming outdated.

In IFRS, all essential applicable decision are

performed and made by IASB.

IAS related decision are made by IASC has the

closely examined the activities of companies

that implement IAS (Kassem, 2012.).

8. Evaluation of benefits of IFRS.

International financial reporting standard were developed by IASB in year 2001 that help

in maintaining financial statement of company. With the help of IFRS companies are able to

overcome different accounting problems that may be reason to decrease profitability during an

accounting year. Thus, IFRS help accountant of M&S to prepare transparent, appropriate

statement that will provide clear picture of company to external parties (Nurunnabi and Alam

Hossain, 2012.). Investor and stakeholder analyse the financial position of M&S and determine

weather they are able to get best result in future or not. Some of the basic advantages of IFRS are

defined below:

IFRS plays a crucial role in formulating of transparent and faithful statement and final

account. This support to analyse the financial position of company.

With the support of accurate statement international investor are attracted towards

company to invest money and ear n good return on investment.

The M&S acquire large amount of abroad capital, if they could develop belief and

assurance in mind of investor that financial statements are created and follow generally

accepted accounting standards.

This also support the investor to better understand and determine the investment

opportunities among M&S that have develop financial statement with the help of

accounting standard and principle (Valentinetti and Rea, 2012).

recording financial transaction that into final

account.

These were introduced to give the primary

accounting standard to accountant of business

firm.

These are new principle that are introduced in

2001 by international accounting standard

board.

These were introduced in 1973 by international

accounting standard committee. But now are

becoming outdated.

In IFRS, all essential applicable decision are

performed and made by IASB.

IAS related decision are made by IASC has the

closely examined the activities of companies

that implement IAS (Kassem, 2012.).

8. Evaluation of benefits of IFRS.

International financial reporting standard were developed by IASB in year 2001 that help

in maintaining financial statement of company. With the help of IFRS companies are able to

overcome different accounting problems that may be reason to decrease profitability during an

accounting year. Thus, IFRS help accountant of M&S to prepare transparent, appropriate

statement that will provide clear picture of company to external parties (Nurunnabi and Alam

Hossain, 2012.). Investor and stakeholder analyse the financial position of M&S and determine

weather they are able to get best result in future or not. Some of the basic advantages of IFRS are

defined below:

IFRS plays a crucial role in formulating of transparent and faithful statement and final

account. This support to analyse the financial position of company.

With the support of accurate statement international investor are attracted towards

company to invest money and ear n good return on investment.

The M&S acquire large amount of abroad capital, if they could develop belief and

assurance in mind of investor that financial statements are created and follow generally

accepted accounting standards.

This also support the investor to better understand and determine the investment

opportunities among M&S that have develop financial statement with the help of

accounting standard and principle (Valentinetti and Rea, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9 Ascertaining the varying degree of compliance with IFRS.

In recent time, financial reporting is used by almost every companies at global level.

These are basically formed with the help of internation financial reporting standard that guide

accountant of companies to prepare and maintain their financial account in appropriate manner.

Recently there are 13 IFRS and 29 IAS that are being implemented by different companies at

world wide level. Companies weather small and big has to follow accounting standard that will

support investor to make investment after analysing the useful information. So Marks and

Spencer has been implementing IFRS to formulate financial statement during an accounting year

and these also very implement al for to take decisions regarding financing and investing (Koh,

2011).

Recently, UK government have applied various crucial accounting rules and standard that

has to be followed by every companies. Marks and Spencer is operating its business at global

level, therefore it is important to use international financial reporting standard in their financial

statement that could be used at global level. These are also accepted universally. So when a

country does not follow any IFRS standard in their reporting then there must be chance of

misrepresentation's of reports and statement.

1102.

CONCLUSION

From the above report, it has been concluded that financial statement plays a crucial role

as it help to analyse the financial status of company to internal and external stakeholder of

company. Therefore IFRS must be implemented by accountant of M&S in order to maintain

accounting report. It is also observed that financial reporting help to attain the objective of

company and determine the growth opportunities. With aid of interpretation of statement

company can draw an helpful decision. There standard which are fit by IFRS and IAS

necessarily to be followed by institution to execute better at global level.

In recent time, financial reporting is used by almost every companies at global level.

These are basically formed with the help of internation financial reporting standard that guide

accountant of companies to prepare and maintain their financial account in appropriate manner.

Recently there are 13 IFRS and 29 IAS that are being implemented by different companies at

world wide level. Companies weather small and big has to follow accounting standard that will

support investor to make investment after analysing the useful information. So Marks and

Spencer has been implementing IFRS to formulate financial statement during an accounting year

and these also very implement al for to take decisions regarding financing and investing (Koh,

2011).

Recently, UK government have applied various crucial accounting rules and standard that

has to be followed by every companies. Marks and Spencer is operating its business at global

level, therefore it is important to use international financial reporting standard in their financial

statement that could be used at global level. These are also accepted universally. So when a

country does not follow any IFRS standard in their reporting then there must be chance of

misrepresentation's of reports and statement.

1102.

CONCLUSION

From the above report, it has been concluded that financial statement plays a crucial role

as it help to analyse the financial status of company to internal and external stakeholder of

company. Therefore IFRS must be implemented by accountant of M&S in order to maintain

accounting report. It is also observed that financial reporting help to attain the objective of

company and determine the growth opportunities. With aid of interpretation of statement

company can draw an helpful decision. There standard which are fit by IFRS and IAS

necessarily to be followed by institution to execute better at global level.

REFERENCES

Books and Journals

Al-Matari, Y. A. A. T., 2013. Board of Directors, Audit Committee Characteristics and The

Performance of Public Listed Companies in Saudi Arabia (Doctoral dissertation,

Universiti Utara Malaysia).

Chae, S. J. and Oh, K., 2016. The Effect Of Family Firm On The Credit Rating: Evidence From

Republic Of Korea. Journal of Applied Business Research. 32(6). p.1575.

Duncan, K., 2014. Relationship between the audit function and effective governance.

Eker, M. and Aytaç, A., 2016. Effects of interaction between ERP and advanced managerial

accounting techniques on firm performance: Evidence From Turkey. Muhasebe ve

Finansman Dergisi. (72), pp.187-210.

Elbayoumi, A. F. and Awadallah, E. A., 2017. The Usefulness of Different Accounting Earnings

Measures: The Case of Egypt. GSTF Journal on Business Review (GBR). 2(2).

Formisano, V., Fedele, M. and Calabrese, M., 2018. The strategic priorities in the materiality

matrix of the banking enterprise. The TQM Journal.

Guo, N., 2018. Revisiting Corporate Financial Policy and the Value of Cash.

Kassem, R., 2012. Earnings Management and Financial Reporting Fraud: Can External Auditors

Spot the Difference?.

Koh, K., 2011. Value or glamour? An empirical investigation of the effect of celebrity CEOs on

financial reporting practices and firm performance. Accounting & Finance. 51(2).

pp.517-547.

Nurunnabi, M. and Alam Hossain, M., 2012. The voluntary disclosure of internet financial

reporting (IFR) in an emerging economy: a case of digital Bangladesh. Journal of Asia

Business Studies. 6(1). pp.17-42.

Valentinetti, D. and Rea, M. A., 2012. IFRS Taxonomy and financial reporting practices: The

case of Italian listed companies. International Journal of Accounting Information

Systems. 13(2). pp.163-180.

Online

Financial statement. 2018. [Online]. Available through:

<https://in.finance.yahoo.com/quote/MKS.L/financials?p=MKS.L>

Books and Journals

Al-Matari, Y. A. A. T., 2013. Board of Directors, Audit Committee Characteristics and The

Performance of Public Listed Companies in Saudi Arabia (Doctoral dissertation,

Universiti Utara Malaysia).

Chae, S. J. and Oh, K., 2016. The Effect Of Family Firm On The Credit Rating: Evidence From

Republic Of Korea. Journal of Applied Business Research. 32(6). p.1575.

Duncan, K., 2014. Relationship between the audit function and effective governance.

Eker, M. and Aytaç, A., 2016. Effects of interaction between ERP and advanced managerial

accounting techniques on firm performance: Evidence From Turkey. Muhasebe ve

Finansman Dergisi. (72), pp.187-210.

Elbayoumi, A. F. and Awadallah, E. A., 2017. The Usefulness of Different Accounting Earnings

Measures: The Case of Egypt. GSTF Journal on Business Review (GBR). 2(2).

Formisano, V., Fedele, M. and Calabrese, M., 2018. The strategic priorities in the materiality

matrix of the banking enterprise. The TQM Journal.

Guo, N., 2018. Revisiting Corporate Financial Policy and the Value of Cash.

Kassem, R., 2012. Earnings Management and Financial Reporting Fraud: Can External Auditors

Spot the Difference?.

Koh, K., 2011. Value or glamour? An empirical investigation of the effect of celebrity CEOs on

financial reporting practices and firm performance. Accounting & Finance. 51(2).

pp.517-547.

Nurunnabi, M. and Alam Hossain, M., 2012. The voluntary disclosure of internet financial

reporting (IFR) in an emerging economy: a case of digital Bangladesh. Journal of Asia

Business Studies. 6(1). pp.17-42.

Valentinetti, D. and Rea, M. A., 2012. IFRS Taxonomy and financial reporting practices: The

case of Italian listed companies. International Journal of Accounting Information

Systems. 13(2). pp.163-180.

Online

Financial statement. 2018. [Online]. Available through:

<https://in.finance.yahoo.com/quote/MKS.L/financials?p=MKS.L>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.