Financial Reporting Analysis: Purpose, Framework, and IFRS

VerifiedAdded on 2021/01/02

|15

|2947

|65

Report

AI Summary

This report provides a comprehensive overview of financial reporting, beginning with its context and purpose, and delving into the conceptual and regulatory framework that underpins it. It examines the benefits of financial reporting for various stakeholders, including owners, employees, creditors, and the government, highlighting its value in meeting organizational objectives and fostering growth. The report then explores financial statements, including their interpretation through ratio analysis, and differentiates between IAS and IFRS. An evaluation of the benefits of IFRS and the varying degrees of compliance are also discussed, offering a complete understanding of the subject. The report emphasizes the importance of financial reporting in providing transparent and reliable financial information to support decision-making and ensure accountability within organizations.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

1 Context and purpose of financial reporting..............................................................................1

2 Conceptual and Regulatory framework of financial reporting.................................................2

3 Benefits of financial reporting to stakeholders.........................................................................3

4 Value of financial reporting for meeting organisation objectives and growth.........................4

5. Financial statements.................................................................................................................5

6. Interpretation of ratios.............................................................................................................7

7 Difference between IAS and IFRS...........................................................................................9

8 Evaluation of benefits of IFRS.................................................................................................9

9. Ascertaining the varying degree of compliance...................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

1 Context and purpose of financial reporting..............................................................................1

2 Conceptual and Regulatory framework of financial reporting.................................................2

3 Benefits of financial reporting to stakeholders.........................................................................3

4 Value of financial reporting for meeting organisation objectives and growth.........................4

5. Financial statements.................................................................................................................5

6. Interpretation of ratios.............................................................................................................7

7 Difference between IAS and IFRS...........................................................................................9

8 Evaluation of benefits of IFRS.................................................................................................9

9. Ascertaining the varying degree of compliance...................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance helps in smooth functioning of various business activities. Structure of every

business differs because of availability of finance with them. As finance is considered as sole of

every business then its management must be done in most efficient manner so that returns are

higher (Al-Matari, 2013). Financial reporting is a document which provides true and fair

information about financial position of different companies by one of biggest accounting firm

Deloitte. In this project report about purpose of financial reporting, conceptual and regulatory

framework of financial reporting, main stakeholders of organisations, value of financial

reporting, interpretation of financial statements, standards and theoretical model and

international differences in financial reporting will be mentioned.

1 Context and purpose of financial reporting

Financial reporting is a process of producing financial statements that presents financial

status of an organisation to its users such as shareholder's, investors, employees. Financial

reporting gives an overview regarding integrity and creditworthiness of a company. Decisions by

internal management of any business is very much connected with financial reporting

information. Reporting incudes detailed information regarding inflows and outflows of a

company by preparation of various financial statements such as profit and loss account, balance

sheet, income statement, cash flow statement etc.

Financial reporting plays very important role in corporate world. Its main purpose is to

provide full financial information to owners of a business when ownership and management of a

company is in two different hands. Large public company arranges their funds for business from

general public and in return of this investment a small portion of ownership is given to them in

terms of share. Different minds have different opinions in every situation and owners want their

investment to grow and earn more returns (Chae and Oh, 2016). To know about investments of

company and returns financial statements are required. Other purpose for which financial

statements are prepared is to calculate financial growth as required by investors to make

investment decisions.

Financial reporting also reflects about frauds or miss-utilisation of funds in a company,

that helps to locate real reason for this miss-utilisation. Reasonable actions will be taken to

resolve this issue when problem is located in time. Financial reporting of one organisation is

1

Finance helps in smooth functioning of various business activities. Structure of every

business differs because of availability of finance with them. As finance is considered as sole of

every business then its management must be done in most efficient manner so that returns are

higher (Al-Matari, 2013). Financial reporting is a document which provides true and fair

information about financial position of different companies by one of biggest accounting firm

Deloitte. In this project report about purpose of financial reporting, conceptual and regulatory

framework of financial reporting, main stakeholders of organisations, value of financial

reporting, interpretation of financial statements, standards and theoretical model and

international differences in financial reporting will be mentioned.

1 Context and purpose of financial reporting

Financial reporting is a process of producing financial statements that presents financial

status of an organisation to its users such as shareholder's, investors, employees. Financial

reporting gives an overview regarding integrity and creditworthiness of a company. Decisions by

internal management of any business is very much connected with financial reporting

information. Reporting incudes detailed information regarding inflows and outflows of a

company by preparation of various financial statements such as profit and loss account, balance

sheet, income statement, cash flow statement etc.

Financial reporting plays very important role in corporate world. Its main purpose is to

provide full financial information to owners of a business when ownership and management of a

company is in two different hands. Large public company arranges their funds for business from

general public and in return of this investment a small portion of ownership is given to them in

terms of share. Different minds have different opinions in every situation and owners want their

investment to grow and earn more returns (Chae and Oh, 2016). To know about investments of

company and returns financial statements are required. Other purpose for which financial

statements are prepared is to calculate financial growth as required by investors to make

investment decisions.

Financial reporting also reflects about frauds or miss-utilisation of funds in a company,

that helps to locate real reason for this miss-utilisation. Reasonable actions will be taken to

resolve this issue when problem is located in time. Financial reporting of one organisation is

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

used by another competitive organisation to always be updated with financial growth of

competitor. Government also uses financial information to calculate taxes of companies as this is

main source of revenue for government.

2 Conceptual and Regulatory framework of financial reporting

Conceptual framework is an analytical tool which serves set concepts and theories on the

basis of which financial reporting is prepared. Data prepared on conceptual framework make it

easy to report and understand. Various definitions and rules are mentioned is this which provides

basis for measurement and boundary that needed to be followed. Conceptual framework is

revised to improve quality of financial reporting. Revisions such as alteration in definition of

assets and liabilities is done. A conceptual framework regarding factors to be considered when

basis is selected for measurement is provided in revised framework.

Some qualities that makes conceptual framework important is-

All information provided is based on a concept and easy to understand.

Purpose of all the users to get qualitative information for their use is fulfilled.

Increase confidence of users in financial information (Duncan, 2014).

Regulates behaviour of companies and directors for investors.

Regulatory framework is a model of set rules and principles that are required to be

followed for reporting. Every country has difference in their legal system, in laws, policies an all

these are to be complied when financial reporting is done. This framework makes a reporting to

be valid in throughout a country for which they are prepared.

In UK conceptual framework is governed by IFRS (International Financial Reporting

Standards). These standards provide a set format on basis of which financial reports are prepared

but these standards are also followed by some legal and marketing standards which makes

reporting more strong and correct. Quality of a report makes it more relevant for its different

users. Qualitative characteristic of financial reporting is divided in two parts as-

Fundamental qualitative characteristic makes difference in financial reporting

information by separating useful information from that of misleading information. These

are of two types-

Relevance – a information is said to be relevant when it proves useful for user and helps

to take a decision which is different from decision taken before this information. Productive

2

competitor. Government also uses financial information to calculate taxes of companies as this is

main source of revenue for government.

2 Conceptual and Regulatory framework of financial reporting

Conceptual framework is an analytical tool which serves set concepts and theories on the

basis of which financial reporting is prepared. Data prepared on conceptual framework make it

easy to report and understand. Various definitions and rules are mentioned is this which provides

basis for measurement and boundary that needed to be followed. Conceptual framework is

revised to improve quality of financial reporting. Revisions such as alteration in definition of

assets and liabilities is done. A conceptual framework regarding factors to be considered when

basis is selected for measurement is provided in revised framework.

Some qualities that makes conceptual framework important is-

All information provided is based on a concept and easy to understand.

Purpose of all the users to get qualitative information for their use is fulfilled.

Increase confidence of users in financial information (Duncan, 2014).

Regulates behaviour of companies and directors for investors.

Regulatory framework is a model of set rules and principles that are required to be

followed for reporting. Every country has difference in their legal system, in laws, policies an all

these are to be complied when financial reporting is done. This framework makes a reporting to

be valid in throughout a country for which they are prepared.

In UK conceptual framework is governed by IFRS (International Financial Reporting

Standards). These standards provide a set format on basis of which financial reports are prepared

but these standards are also followed by some legal and marketing standards which makes

reporting more strong and correct. Quality of a report makes it more relevant for its different

users. Qualitative characteristic of financial reporting is divided in two parts as-

Fundamental qualitative characteristic makes difference in financial reporting

information by separating useful information from that of misleading information. These

are of two types-

Relevance – a information is said to be relevant when it proves useful for user and helps

to take a decision which is different from decision taken before this information. Productive

2

information always leads to take right decision to its users and helps to earn more in their

respective way.

Faithful representation- financial reports of an organisation reflect its position in words

and numbers. These reports should reflect real position of finances available in business. More

correct information leads to fair decision making in business and also investors can make a fair

decision for investing their money (Eker and Aytaç, 2016).

Enhancing qualitative characteristic brings out more useful information from less useful

information. This is divided into four attribute-

Comparability- information about reporting entity is more useful when it can be

compared with other entities and with itself for different time duration. As a competitor

knowledge regarding competitors position is necessary to compete better. And also company can

self-analyse its growth.

Verifiability- Company’s financial statements should always reflect same position when

accounts are reproducing by taking same assumptions. More verifiable reports a positive image

in public at large and also in eyes of interested investors and government.

Timeliness- when information is provided on time then before taking decisions that must

be considered but after passing of that time it will become of no use. Timely information helps

investors to make investing decision when opportunities arises. Company can also use financial

statements as a proof to n show their performance.

Under stability- financial reporting presents information in a simple way which makes it

easy to understand by public at large, even they do no poses financial qualification. This

increases use of financial reporting for general public and also to interested investors.

3 Benefits of financial reporting to stakeholders

Stakeholders are those persons who are affected by action taken by a business

organisation. Every organisation has two types of stakeholders and they are-

Internal stakeholders are those who are working in the organisation and serving it. These

includes directors, managers, owners and they all are directly affected by every action

taken by organisation. Benefits of financial reporting to internal stakeholders-

Owners – businesses are managed by different hands and owners are much concerned

about performance of business as funds invested belongs to them. Financial reporting helps them

to know about financial position of business and also effective utilisation of capital invested.

3

respective way.

Faithful representation- financial reports of an organisation reflect its position in words

and numbers. These reports should reflect real position of finances available in business. More

correct information leads to fair decision making in business and also investors can make a fair

decision for investing their money (Eker and Aytaç, 2016).

Enhancing qualitative characteristic brings out more useful information from less useful

information. This is divided into four attribute-

Comparability- information about reporting entity is more useful when it can be

compared with other entities and with itself for different time duration. As a competitor

knowledge regarding competitors position is necessary to compete better. And also company can

self-analyse its growth.

Verifiability- Company’s financial statements should always reflect same position when

accounts are reproducing by taking same assumptions. More verifiable reports a positive image

in public at large and also in eyes of interested investors and government.

Timeliness- when information is provided on time then before taking decisions that must

be considered but after passing of that time it will become of no use. Timely information helps

investors to make investing decision when opportunities arises. Company can also use financial

statements as a proof to n show their performance.

Under stability- financial reporting presents information in a simple way which makes it

easy to understand by public at large, even they do no poses financial qualification. This

increases use of financial reporting for general public and also to interested investors.

3 Benefits of financial reporting to stakeholders

Stakeholders are those persons who are affected by action taken by a business

organisation. Every organisation has two types of stakeholders and they are-

Internal stakeholders are those who are working in the organisation and serving it. These

includes directors, managers, owners and they all are directly affected by every action

taken by organisation. Benefits of financial reporting to internal stakeholders-

Owners – businesses are managed by different hands and owners are much concerned

about performance of business as funds invested belongs to them. Financial reporting helps them

to know about financial position of business and also effective utilisation of capital invested.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Employees – growth of an employee is very much affected by growth of a company in

which work is performed. Financial growth is very much concerned as when a company itself

grows well then more opportunities will be available to employees working in company.

External stakeholders are those who are not directly related to company but are affected

by business decisions as they are ultimate consumers (Elbayoumi and Awadallah, 2017).

And long term success will be affected by external shareholders such as government,

consumers, creditors, suppliers.

Creditors- financial position of a company is prime concern of every creditor as

company is liable to pay amount due. Good financial conditions secure creditors regarding

repayment of their funds as probability of debt gets reduced and creditworthiness of company

will increase.

Government- taxes charged by government from business is a main source of revenue.

Increasing financial position of every business concern will also contribute more towards

government taxes and more revenue will be there. So to know financial condition of every

business financial report will be concerned.

4 Value of financial reporting for meeting organisation objectives and growth

Every organisation has different objectives that are achieved by short-term and long-term

plans. Core objective of businesses is to earn profits and grow more. Financial report discloses

fair view of organisation that helps to achieve its term plans. Planning requires past data together

with that current position and financial reporting helps to provide reliable data that helps to make

future plans. Fair view of financial position of company helps management to predict future to

some extent and prepare its future plan. Objective of profit maximisation is evaluated by

financial performance of organisation which requires financial report for analysis. A satisfied

investor will bring more funds to invest in business and this will only be possible when a true

financial reporting is provided.

4

which work is performed. Financial growth is very much concerned as when a company itself

grows well then more opportunities will be available to employees working in company.

External stakeholders are those who are not directly related to company but are affected

by business decisions as they are ultimate consumers (Elbayoumi and Awadallah, 2017).

And long term success will be affected by external shareholders such as government,

consumers, creditors, suppliers.

Creditors- financial position of a company is prime concern of every creditor as

company is liable to pay amount due. Good financial conditions secure creditors regarding

repayment of their funds as probability of debt gets reduced and creditworthiness of company

will increase.

Government- taxes charged by government from business is a main source of revenue.

Increasing financial position of every business concern will also contribute more towards

government taxes and more revenue will be there. So to know financial condition of every

business financial report will be concerned.

4 Value of financial reporting for meeting organisation objectives and growth

Every organisation has different objectives that are achieved by short-term and long-term

plans. Core objective of businesses is to earn profits and grow more. Financial report discloses

fair view of organisation that helps to achieve its term plans. Planning requires past data together

with that current position and financial reporting helps to provide reliable data that helps to make

future plans. Fair view of financial position of company helps management to predict future to

some extent and prepare its future plan. Objective of profit maximisation is evaluated by

financial performance of organisation which requires financial report for analysis. A satisfied

investor will bring more funds to invest in business and this will only be possible when a true

financial reporting is provided.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

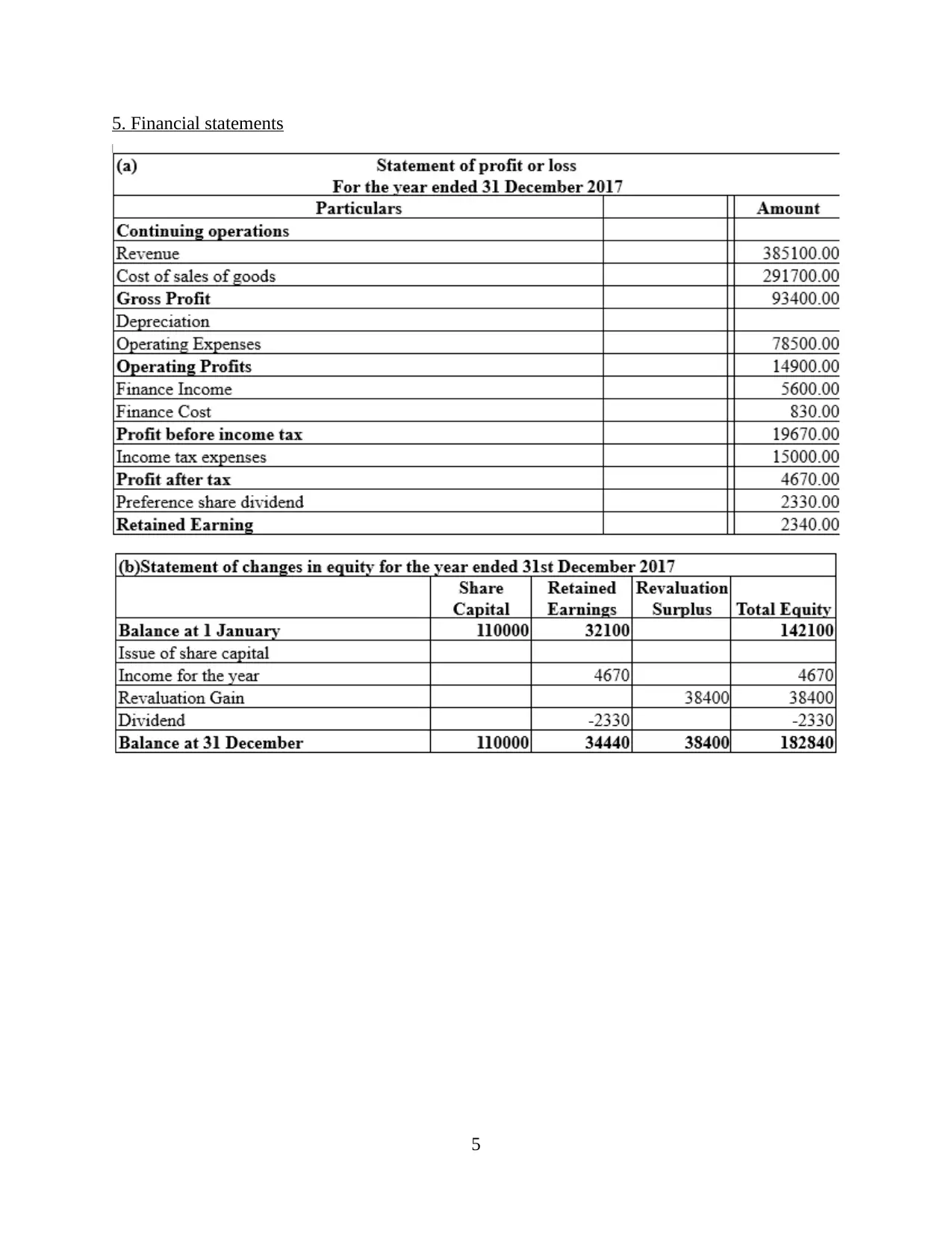

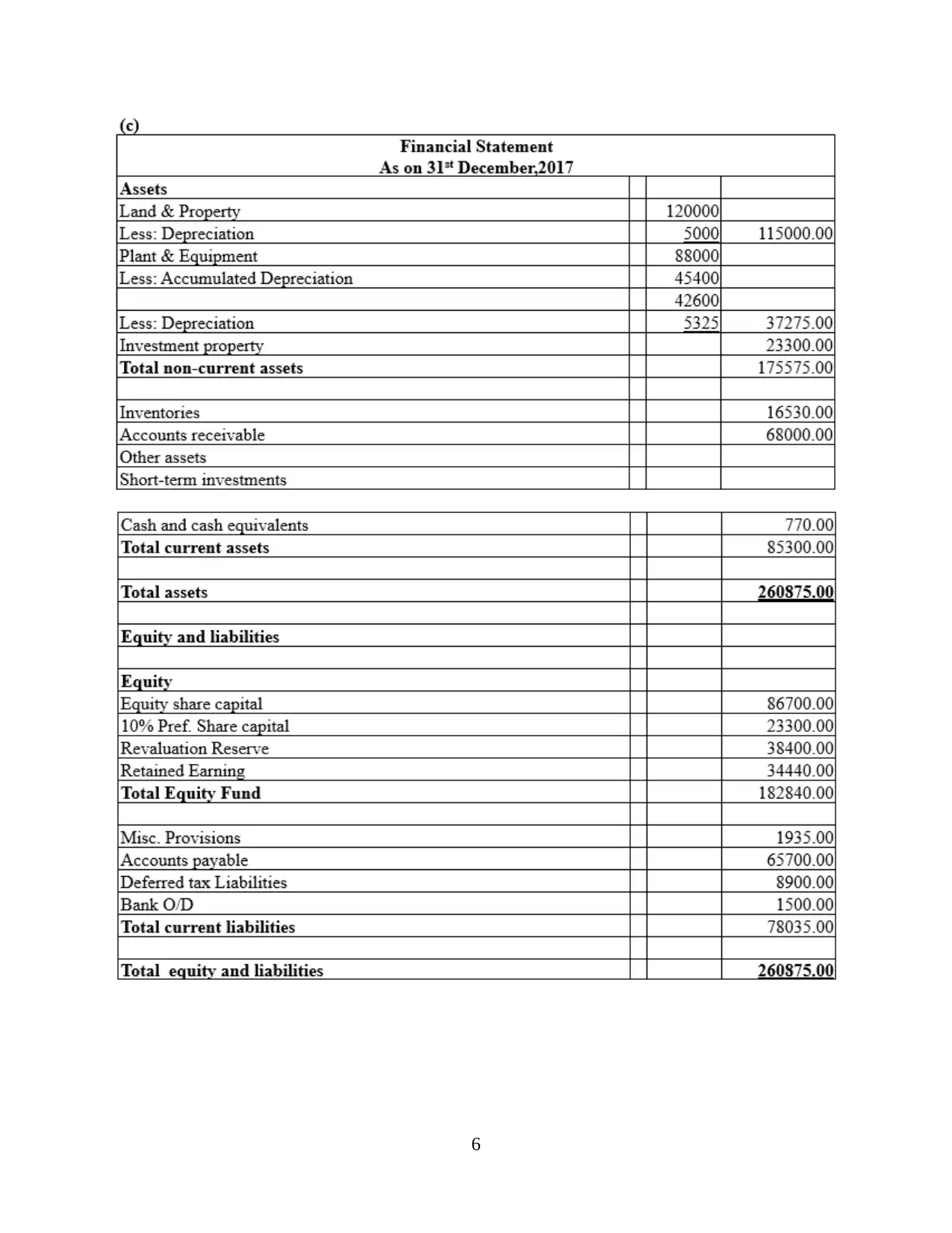

5. Financial statements

5

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

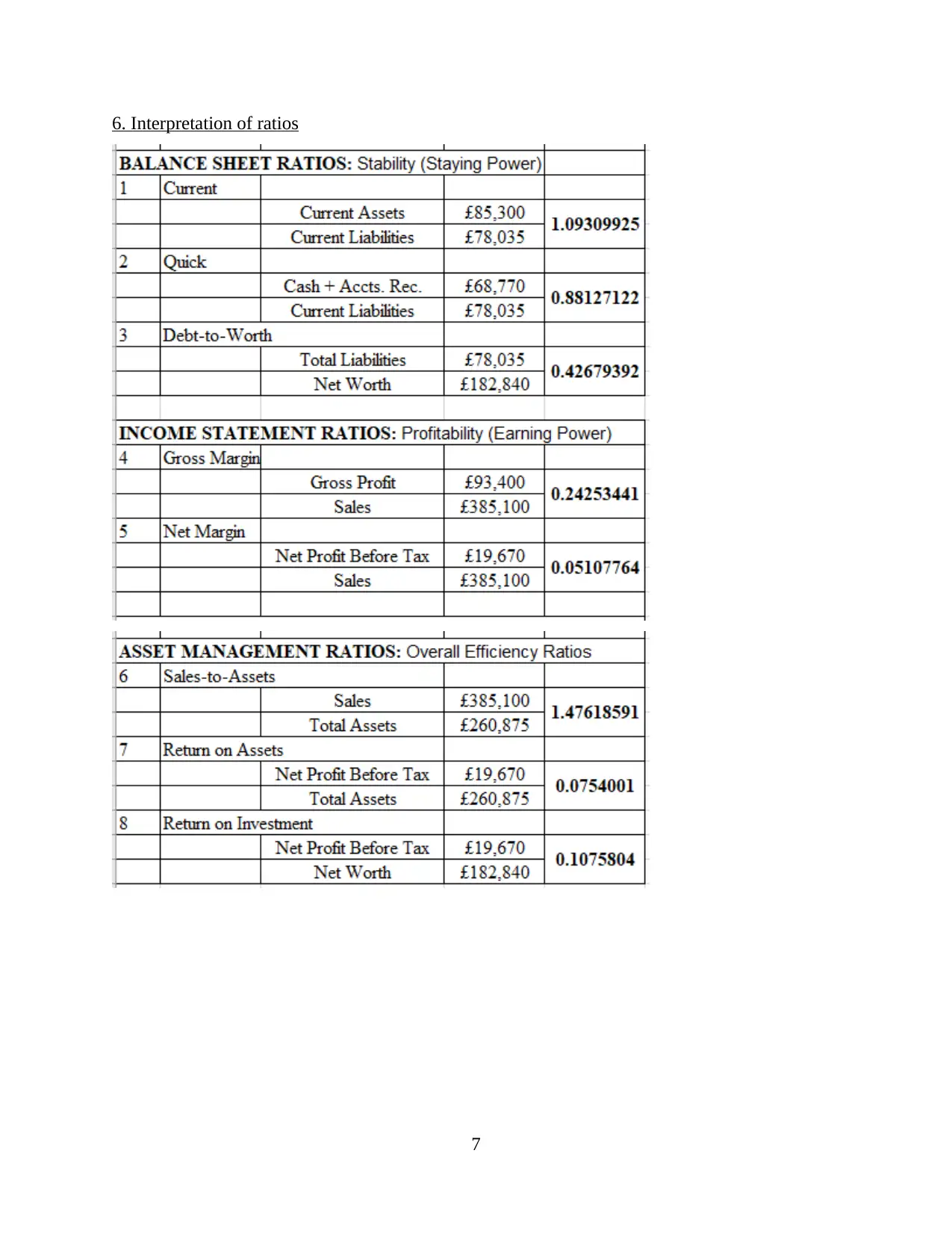

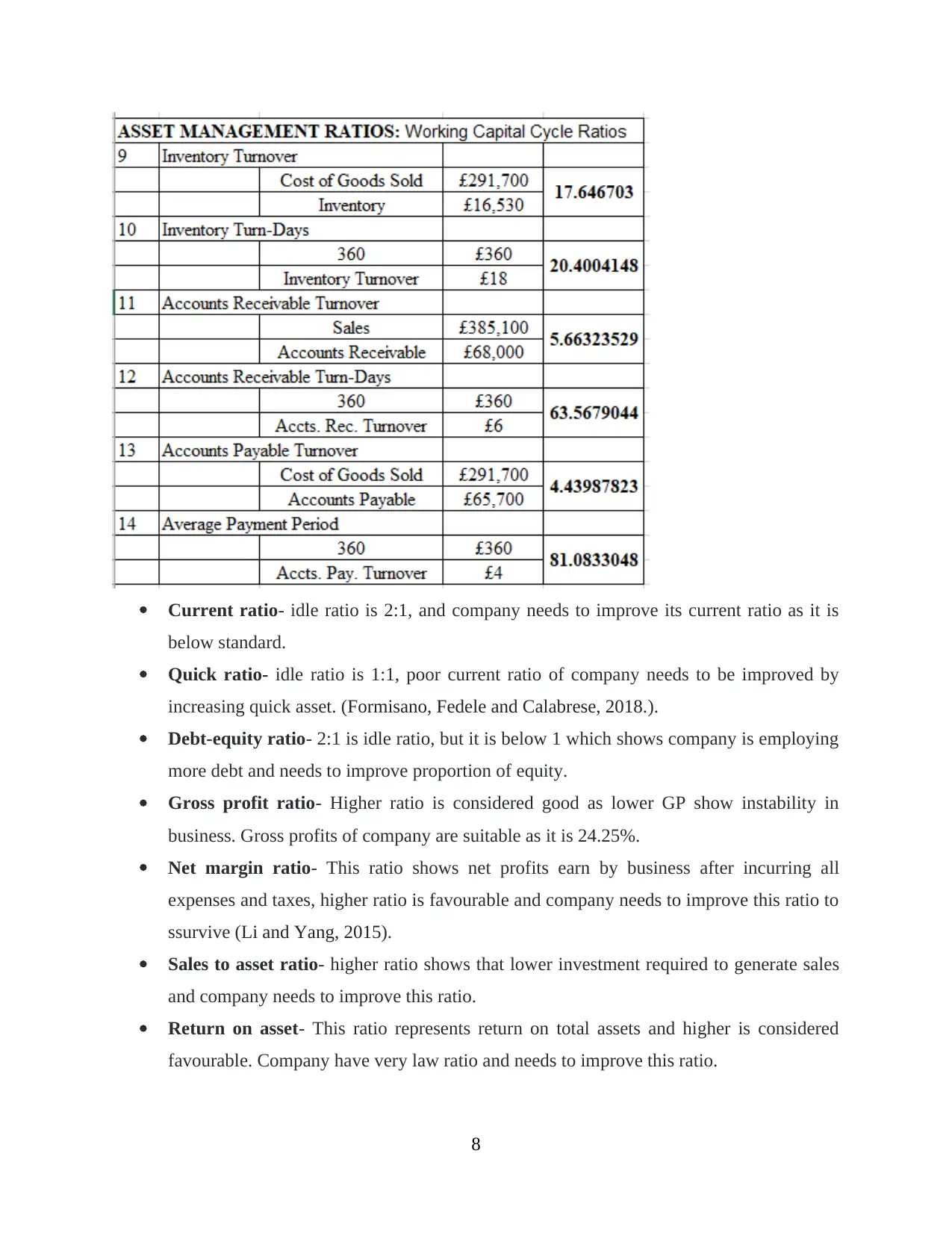

6. Interpretation of ratios

7

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current ratio- idle ratio is 2:1, and company needs to improve its current ratio as it is

below standard.

Quick ratio- idle ratio is 1:1, poor current ratio of company needs to be improved by

increasing quick asset. (Formisano, Fedele and Calabrese, 2018.).

Debt-equity ratio- 2:1 is idle ratio, but it is below 1 which shows company is employing

more debt and needs to improve proportion of equity.

Gross profit ratio- Higher ratio is considered good as lower GP show instability in

business. Gross profits of company are suitable as it is 24.25%.

Net margin ratio- This ratio shows net profits earn by business after incurring all

expenses and taxes, higher ratio is favourable and company needs to improve this ratio to

ssurvive (Li and Yang, 2015).

Sales to asset ratio- higher ratio shows that lower investment required to generate sales

and company needs to improve this ratio.

Return on asset- This ratio represents return on total assets and higher is considered

favourable. Company have very law ratio and needs to improve this ratio.

8

below standard.

Quick ratio- idle ratio is 1:1, poor current ratio of company needs to be improved by

increasing quick asset. (Formisano, Fedele and Calabrese, 2018.).

Debt-equity ratio- 2:1 is idle ratio, but it is below 1 which shows company is employing

more debt and needs to improve proportion of equity.

Gross profit ratio- Higher ratio is considered good as lower GP show instability in

business. Gross profits of company are suitable as it is 24.25%.

Net margin ratio- This ratio shows net profits earn by business after incurring all

expenses and taxes, higher ratio is favourable and company needs to improve this ratio to

ssurvive (Li and Yang, 2015).

Sales to asset ratio- higher ratio shows that lower investment required to generate sales

and company needs to improve this ratio.

Return on asset- This ratio represents return on total assets and higher is considered

favourable. Company have very law ratio and needs to improve this ratio.

8

Return on investment- This ratio evaluate efficiency of investments to earn, higher is

more favourable. Companies ratio is 10.7 % which can be further increased.

Inventory turnover ratio- Poor ratio reflects inefficiency of business as stock is excess

as per requirement. Company have good inventory ratio and shows efficiency in

inventories management.

Account receivable turnover ratio- This ratio reflects collection made from debtors for

credit sales and company’s collection period is normal.

Accounts payable ratio- This ratio reflects payment made to creditors for credit

purchases. As more time is taken to pay as compare to receivables make company

financially strong.

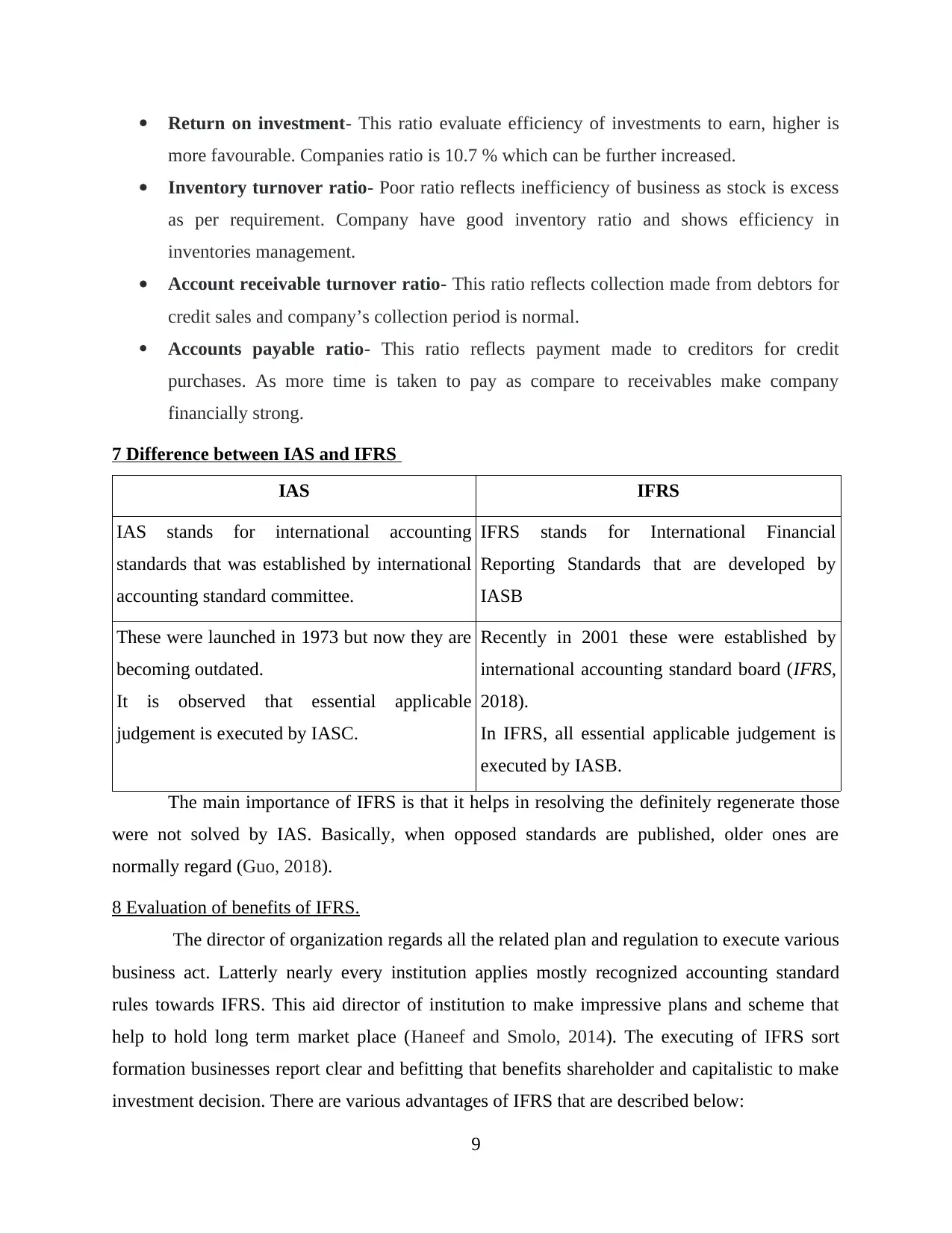

7 Difference between IAS and IFRS

IAS IFRS

IAS stands for international accounting

standards that was established by international

accounting standard committee.

IFRS stands for International Financial

Reporting Standards that are developed by

IASB

These were launched in 1973 but now they are

becoming outdated.

It is observed that essential applicable

judgement is executed by IASC.

Recently in 2001 these were established by

international accounting standard board (IFRS,

2018).

In IFRS, all essential applicable judgement is

executed by IASB.

The main importance of IFRS is that it helps in resolving the definitely regenerate those

were not solved by IAS. Basically, when opposed standards are published, older ones are

normally regard (Guo, 2018).

8 Evaluation of benefits of IFRS.

The director of organization regards all the related plan and regulation to execute various

business act. Latterly nearly every institution applies mostly recognized accounting standard

rules towards IFRS. This aid director of institution to make impressive plans and scheme that

help to hold long term market place (Haneef and Smolo, 2014). The executing of IFRS sort

formation businesses report clear and befitting that benefits shareholder and capitalistic to make

investment decision. There are various advantages of IFRS that are described below:

9

more favourable. Companies ratio is 10.7 % which can be further increased.

Inventory turnover ratio- Poor ratio reflects inefficiency of business as stock is excess

as per requirement. Company have good inventory ratio and shows efficiency in

inventories management.

Account receivable turnover ratio- This ratio reflects collection made from debtors for

credit sales and company’s collection period is normal.

Accounts payable ratio- This ratio reflects payment made to creditors for credit

purchases. As more time is taken to pay as compare to receivables make company

financially strong.

7 Difference between IAS and IFRS

IAS IFRS

IAS stands for international accounting

standards that was established by international

accounting standard committee.

IFRS stands for International Financial

Reporting Standards that are developed by

IASB

These were launched in 1973 but now they are

becoming outdated.

It is observed that essential applicable

judgement is executed by IASC.

Recently in 2001 these were established by

international accounting standard board (IFRS,

2018).

In IFRS, all essential applicable judgement is

executed by IASB.

The main importance of IFRS is that it helps in resolving the definitely regenerate those

were not solved by IAS. Basically, when opposed standards are published, older ones are

normally regard (Guo, 2018).

8 Evaluation of benefits of IFRS.

The director of organization regards all the related plan and regulation to execute various

business act. Latterly nearly every institution applies mostly recognized accounting standard

rules towards IFRS. This aid director of institution to make impressive plans and scheme that

help to hold long term market place (Haneef and Smolo, 2014). The executing of IFRS sort

formation businesses report clear and befitting that benefits shareholder and capitalistic to make

investment decision. There are various advantages of IFRS that are described below:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.