International Financial Reporting: Frameworks, Standards and Analysis

VerifiedAdded on 2021/02/20

|22

|3336

|34

Report

AI Summary

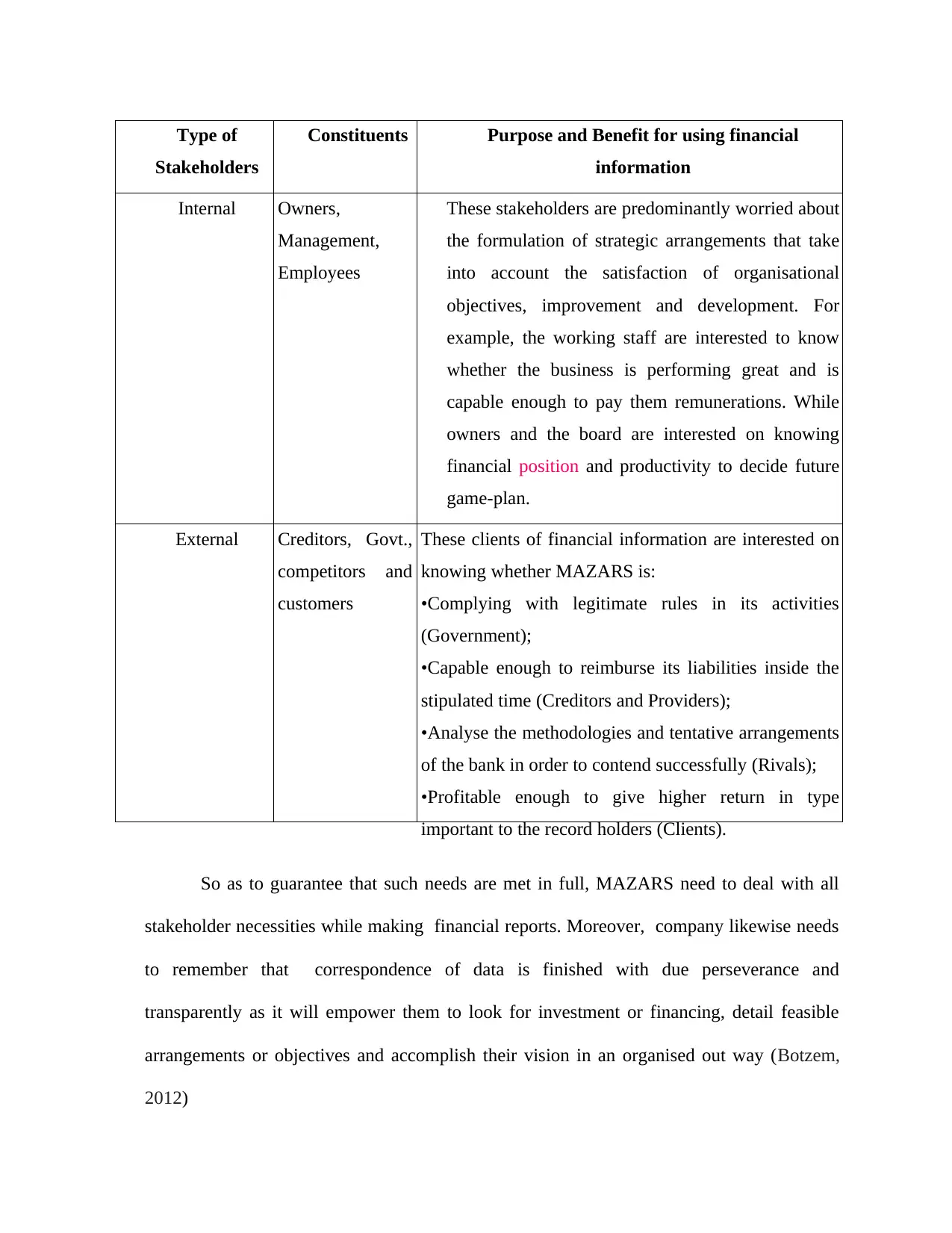

This report provides a comprehensive analysis of international financial reporting, focusing on the application of International Financial Reporting Standards (IFRS) and International Accounting Standards (IAS). It explores the regulatory and conceptual frameworks, qualitative characteristics of financial information, and the role of financial reporting in achieving business objectives. The report examines financial statements, including income statements, balance sheets, and cash flow statements, and provides an interpretation of financial ratios, using Diageo as a case study. It also discusses the benefits of IFRS and IAS, financial reporting and auditing models. The report covers key stakeholders and their needs. This assignment offers insights into the complexities of global financial reporting, making it a valuable resource for students studying finance.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.