Financial Reporting and Management - University Assignment Report

VerifiedAdded on 2020/02/17

|14

|4640

|51

Report

AI Summary

This report provides a comprehensive overview of financial reporting and management. It begins with an introduction to financial reporting, emphasizing its importance for stakeholders. The report then delves into valuation techniques as per the guidelines of IASB and IAS 13, discussing the reliability and measurement of fair value, and the disclosure requirements of IFRS 13. It further explores the key definitions and characteristics used to differentiate between debt and equity, as per IAS 32, including the discussion of financial instruments and their recognition in financial statements. The report also addresses the issues related to convoluted financial instruments. The report concludes by summarizing the key findings and providing relevant references.

Financial Reporting And

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Valuation techniques as per the guidelines of IASB for financial reporting and IAS 13 1

1.2 Discussion over the reliability and measurement of fair value technique........................3

1.3 Disclosure requirements as per IFRS 13..........................................................................4

TASK 2............................................................................................................................................5

2.1 Discussion over the key definition of of various terms which are used for differentiating

debt and equity as per IAS 32.................................................................................................5

2.2 Discussion over the key characteristics or the criteria which are used to make

differentiation between debt and equity under IFRS IAS 32. Discussion of type of financial

instruments and how they recognised in financial statements................................................7

2.3 Discuss over the issues which recognises convoluted financial instruments present in

financial instruments..............................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Valuation techniques as per the guidelines of IASB for financial reporting and IAS 13 1

1.2 Discussion over the reliability and measurement of fair value technique........................3

1.3 Disclosure requirements as per IFRS 13..........................................................................4

TASK 2............................................................................................................................................5

2.1 Discussion over the key definition of of various terms which are used for differentiating

debt and equity as per IAS 32.................................................................................................5

2.2 Discussion over the key characteristics or the criteria which are used to make

differentiation between debt and equity under IFRS IAS 32. Discussion of type of financial

instruments and how they recognised in financial statements................................................7

2.3 Discuss over the issues which recognises convoluted financial instruments present in

financial instruments..............................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial reporting should be in a manner so that user or stakeholders can get a complete

information which are required by them in order to take any decisions to invest their money in

any financial instruments. Financial reporting presents an extracted summarised data from all the

parts of financial statement. So that they can get their desired profit or returns on their

investment further stakeholders other than shareholders are also required ton get information

from the financial statements(Agoglia,Doupnik and Tsakumis,2011). Hence as there are a

number of users which frames their decisions as per the basis of figures and facts which are

mentioned there in financial statements so they are required to be credible and reliable. Presented

report is providing evidence regarding whether to use fair market value or to utilize historical

value for the valuation of assets and during the transfer of any liability. The Internal Accounting

Standard Board has framed certain standards which are mandatory to follow during the

preparation financial statements and the concepts which are mentioned in those standards related

with use of fair value is mentioned in this report.

TASK 1

1.1 Valuation techniques as per the guidelines of IASB for financial reporting and IAS 13

The International Accounting Standard Board (IASB) is a privately owned body which

regulates the concepts and principles which can be used by any entity during the formation or

preparation of financial statements. So as to give a better and clear information to its users. For

issuing regulatory laws and to provide information regarding the performance of statement

preparation it have issued a number of standards(Altamuro,and Beatty, 2010). The main work of

this body is to frame IFRS in a way to provide credibility and reliability to its users.

IFRS 13 Fair Value Measurement

This standard has been launched by IASB on 12th May 2011 which deals in fair market

valuation of assets and liabilities. This standard decides some criteria on the basis of which user

can make valuation of its assets and liabilities on fair market value. There is a difference between

fair market value and historical cost as both of this are having some different elements. Fair

market value as per this standard can be defined as that value which a person can get on the sale

of any asset in open market. Which means fair value is that actual cost or value which an asset of

liability possesses on any particular date on which such sale or exchange has been done. On the

other hand historical cost is that cost at which such assets was acquired in past. Historical can be

1

Financial reporting should be in a manner so that user or stakeholders can get a complete

information which are required by them in order to take any decisions to invest their money in

any financial instruments. Financial reporting presents an extracted summarised data from all the

parts of financial statement. So that they can get their desired profit or returns on their

investment further stakeholders other than shareholders are also required ton get information

from the financial statements(Agoglia,Doupnik and Tsakumis,2011). Hence as there are a

number of users which frames their decisions as per the basis of figures and facts which are

mentioned there in financial statements so they are required to be credible and reliable. Presented

report is providing evidence regarding whether to use fair market value or to utilize historical

value for the valuation of assets and during the transfer of any liability. The Internal Accounting

Standard Board has framed certain standards which are mandatory to follow during the

preparation financial statements and the concepts which are mentioned in those standards related

with use of fair value is mentioned in this report.

TASK 1

1.1 Valuation techniques as per the guidelines of IASB for financial reporting and IAS 13

The International Accounting Standard Board (IASB) is a privately owned body which

regulates the concepts and principles which can be used by any entity during the formation or

preparation of financial statements. So as to give a better and clear information to its users. For

issuing regulatory laws and to provide information regarding the performance of statement

preparation it have issued a number of standards(Altamuro,and Beatty, 2010). The main work of

this body is to frame IFRS in a way to provide credibility and reliability to its users.

IFRS 13 Fair Value Measurement

This standard has been launched by IASB on 12th May 2011 which deals in fair market

valuation of assets and liabilities. This standard decides some criteria on the basis of which user

can make valuation of its assets and liabilities on fair market value. There is a difference between

fair market value and historical cost as both of this are having some different elements. Fair

market value as per this standard can be defined as that value which a person can get on the sale

of any asset in open market. Which means fair value is that actual cost or value which an asset of

liability possesses on any particular date on which such sale or exchange has been done. On the

other hand historical cost is that cost at which such assets was acquired in past. Historical can be

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

considered irrelevant during making any decision as in this depreciation factor or diminishing

value factor has been ignored. Hence because of this it can be said that the historical value cant

be considered as that value which an asset or liability can fetch if they gets exchanged in the

open market.

As per this standard there may be some issues which an user can face while calculating

the fair market value of any holding or possession(Armstrong, Guay and Weber, 2010). It may

be possible that there is no availability of an active market through which they can evaluate their

assets and liabilities in way which can provide them the accurate value at which their assets can

be get sold and their liabilities can be get exchanged.

Techniques of measurement of fair value

There are some techniques through which an entity can get an accurate value which their

assets are possessing at present. Measurement can be defined as a process for the determination

of a material amount at which the data or the elements of financial statements should be

represented. For example valuation of any fixed asset which is used by an entity during the

production process such measurement techniques can give a value at which that fixed asset can

be shown in statement of changes in financial position. IASB Framework and its para 100

provides a number of different techniques which can be get utilized for the valuation of current

and non current assets and liabilities(Barth and Landsman,2010). These are mentioned below : Historical Cost : Assets gets recorded at an amount which is either cash or cash

equivalent which is paid to the supplier at the time of their acquisition. Liabilities are

recorded at that amount which an entity has get against any obligation. Current Cost: Sometimes assets are recorded at an amount at which the same asset can

be acquired during the current period or as on that date. Settlement or realisable value: It means that amount which the entity can get by the

ordinary disposal of available asset. Liabilities can also be get recorded in the books of

account at a value at which these can be get settled. Hence for getting the settlement

amount total obligatory amount requires to be get reduced by the amount of discount

which is available.

Present Value: Assets can be valued at their present value by multiplying the appropriate

discounting factor with the future net cash inflow. As the time value of money is

2

value factor has been ignored. Hence because of this it can be said that the historical value cant

be considered as that value which an asset or liability can fetch if they gets exchanged in the

open market.

As per this standard there may be some issues which an user can face while calculating

the fair market value of any holding or possession(Armstrong, Guay and Weber, 2010). It may

be possible that there is no availability of an active market through which they can evaluate their

assets and liabilities in way which can provide them the accurate value at which their assets can

be get sold and their liabilities can be get exchanged.

Techniques of measurement of fair value

There are some techniques through which an entity can get an accurate value which their

assets are possessing at present. Measurement can be defined as a process for the determination

of a material amount at which the data or the elements of financial statements should be

represented. For example valuation of any fixed asset which is used by an entity during the

production process such measurement techniques can give a value at which that fixed asset can

be shown in statement of changes in financial position. IASB Framework and its para 100

provides a number of different techniques which can be get utilized for the valuation of current

and non current assets and liabilities(Barth and Landsman,2010). These are mentioned below : Historical Cost : Assets gets recorded at an amount which is either cash or cash

equivalent which is paid to the supplier at the time of their acquisition. Liabilities are

recorded at that amount which an entity has get against any obligation. Current Cost: Sometimes assets are recorded at an amount at which the same asset can

be acquired during the current period or as on that date. Settlement or realisable value: It means that amount which the entity can get by the

ordinary disposal of available asset. Liabilities can also be get recorded in the books of

account at a value at which these can be get settled. Hence for getting the settlement

amount total obligatory amount requires to be get reduced by the amount of discount

which is available.

Present Value: Assets can be valued at their present value by multiplying the appropriate

discounting factor with the future net cash inflow. As the time value of money is

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

considered in this valuation technique hence it can be said that present value technique of

valuation presents a much better position of assets and liabilities in terms of money.

Level 1 Input : It can be defined as the quoted price in the open market which an asset or

liability can fetch on selling them in open market. In this identical assets and liabilities

are evaluated for finding the accurate fair value of any holdings and obligations.

Level 2 Inputs : These inputs can be explained as the value other than quoted market

price of any asset or liability. It contains those values which are not contains in level 1

input.

1.2 Discussion over the reliability and measurement of fair value technique

Fair value as per IAS 13 gives a better and reliable value as the amount which is

calculated as per the guidelines of this standard. As this standard provides various formulas

which are universally accepted and are based on some scientific formulas(Beyer,and et.al.,

2010). Hence through this user can frame a better plan over its investment through which it can

deal with the trends or fluctuations which are there in values.

If an entity is following the international financial reporting frame work then they should

follow all the guidelines or rules which are mentioned there in the these standards. For example

in IAS 13 there are some criteria which are mentioned there in which provides information

regarding on which assets and liabilities fair value has been applied and in some other standards

there is some in information are presented which provides the guidelines over the use of present

value techniques. Some times it has been said that present value technique is controversial as in

many standards it is not used for the valuation of fair value instead of it they are guiding this

technique for some different calculation.

There are two different terms which are described in this IAS 13, which are exit price and

transaction price. The concepts of these two terms can be explained as Entry price and exit price

can be of same level which means due to trends and fluctuation in market it may be possible that

exit value of an asset is same as entry price, sometimes it may be lower then the entry price but

comparatively higher than the fair value. On the other hand transaction price possess a distinct

concept as in this value of holdings and obligations are not fetched.

Fair value provide some credible data which can relied upon. As provided above, fair

value is that amount at which an asset can be sold out and proceeds can be received. There are

some major features of IFRSC which are listed below :

3

valuation presents a much better position of assets and liabilities in terms of money.

Level 1 Input : It can be defined as the quoted price in the open market which an asset or

liability can fetch on selling them in open market. In this identical assets and liabilities

are evaluated for finding the accurate fair value of any holdings and obligations.

Level 2 Inputs : These inputs can be explained as the value other than quoted market

price of any asset or liability. It contains those values which are not contains in level 1

input.

1.2 Discussion over the reliability and measurement of fair value technique

Fair value as per IAS 13 gives a better and reliable value as the amount which is

calculated as per the guidelines of this standard. As this standard provides various formulas

which are universally accepted and are based on some scientific formulas(Beyer,and et.al.,

2010). Hence through this user can frame a better plan over its investment through which it can

deal with the trends or fluctuations which are there in values.

If an entity is following the international financial reporting frame work then they should

follow all the guidelines or rules which are mentioned there in the these standards. For example

in IAS 13 there are some criteria which are mentioned there in which provides information

regarding on which assets and liabilities fair value has been applied and in some other standards

there is some in information are presented which provides the guidelines over the use of present

value techniques. Some times it has been said that present value technique is controversial as in

many standards it is not used for the valuation of fair value instead of it they are guiding this

technique for some different calculation.

There are two different terms which are described in this IAS 13, which are exit price and

transaction price. The concepts of these two terms can be explained as Entry price and exit price

can be of same level which means due to trends and fluctuation in market it may be possible that

exit value of an asset is same as entry price, sometimes it may be lower then the entry price but

comparatively higher than the fair value. On the other hand transaction price possess a distinct

concept as in this value of holdings and obligations are not fetched.

Fair value provide some credible data which can relied upon. As provided above, fair

value is that amount at which an asset can be sold out and proceeds can be received. There are

some major features of IFRSC which are listed below :

3

IAS 16 can be used by an enterprise in order to compute the value of any property, plant

and machinery which can be used by it for its production and operating process.

IAS 36 has a concept of asset impairment and its reversal for adjusting the given amount

up to its fair value.

In IAS 38 there are some principles are given which supports the impairment of

intangible assets for its valuation.

Further it also provides a basic rule that if market price is available for any intangible

asset then it should be value at that amount only because market value provide a better

price which can be pointed at a price which such asset can fetch, if sold in open market.

There are some issues which are related with the reliability of fair value as it is a bit

controversial so its credibility can be questioned. Proponents of using fair market value for the

valuation of assets and liabilities appeals that it contains many desirable imputes. The factors

which creates the first element through which its reliability can be questioned is absence of

active market. As in this case an organisation or user cannot determine the accurate fair value of

an asset at which it can be sold or in case of any liability at which it can be exchanged.

1.3 Disclosure requirements as per IFRS 13

There are some disclosure requirements and supporting guidelines are there which is

mentioned in International financial reporting standards 13. Disclosure requirements is to be

fulfilled so that financial statements can provide more reliable information to the users or the

stakeholder so that the user can make more better decisions in order to invest their money or time

in any entity. Certain disclosure requirements are mentioned below :

Disclosure requirement for such assets and liabilities which are actually measured at fair

value on some recurring and non recurring basis in balance sheets after the recognition at

beginning.

For recurring fair value measurements through significant unobservable inputs. Which

have certain impact over the measurement of profit or loss during a certain period.

For non recurring fair value fair value measurements organisation need to provide the

reasons for the valuation of assets on non recurring basis.

Further for recurring fair value they require to address the a hierarchy has been made

which is categorised in three different levels. A narrative description related with the

sensitivity of fair value measurements is required to mention. Financial assets and

4

and machinery which can be used by it for its production and operating process.

IAS 36 has a concept of asset impairment and its reversal for adjusting the given amount

up to its fair value.

In IAS 38 there are some principles are given which supports the impairment of

intangible assets for its valuation.

Further it also provides a basic rule that if market price is available for any intangible

asset then it should be value at that amount only because market value provide a better

price which can be pointed at a price which such asset can fetch, if sold in open market.

There are some issues which are related with the reliability of fair value as it is a bit

controversial so its credibility can be questioned. Proponents of using fair market value for the

valuation of assets and liabilities appeals that it contains many desirable imputes. The factors

which creates the first element through which its reliability can be questioned is absence of

active market. As in this case an organisation or user cannot determine the accurate fair value of

an asset at which it can be sold or in case of any liability at which it can be exchanged.

1.3 Disclosure requirements as per IFRS 13

There are some disclosure requirements and supporting guidelines are there which is

mentioned in International financial reporting standards 13. Disclosure requirements is to be

fulfilled so that financial statements can provide more reliable information to the users or the

stakeholder so that the user can make more better decisions in order to invest their money or time

in any entity. Certain disclosure requirements are mentioned below :

Disclosure requirement for such assets and liabilities which are actually measured at fair

value on some recurring and non recurring basis in balance sheets after the recognition at

beginning.

For recurring fair value measurements through significant unobservable inputs. Which

have certain impact over the measurement of profit or loss during a certain period.

For non recurring fair value fair value measurements organisation need to provide the

reasons for the valuation of assets on non recurring basis.

Further for recurring fair value they require to address the a hierarchy has been made

which is categorised in three different levels. A narrative description related with the

sensitivity of fair value measurements is required to mention. Financial assets and

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

liabilities in case of change in observable value should reflect possible alternative

assumptions.

These disclosure requirements are mandatory to follow hence any entity cannot ignore

such a legal and statutory requirements (Agoglia, Doupnik and Tsakumis, 2011). It they do so

then it will be considered as an offence and then the financial statements will not provide the

accurate information which are required to be stated there in.

For the increment in consistency and comparability regarding fair value measurement and

other disclosures related with it. International financial reporting standards had established a fair

value hierarchy. Such hierarchy is categorised into three levels. This gives highest priority to

unadjusted prices in which no any adjustments are worked out. Such price is quoted open market

of identical assets and liabilities and the lowest priority is given to unobservable inputs. There

are three levels which are categorised as below :

Level one : Quoted Price

Level two : Inputs other than quoted price

Level three : Unobservable inputs

TASK 2

2.1 Discussion over the key definition of of various terms which are used for differentiating debt

and equity as per IAS 32

As per IAS 32 debt and equity has different definition. But in normal sense, Debt reflects

the obligations in terms of money which are related with the outsiders. The cost associated with

such debts can be considered as a charge against profit (Altamuro and Beatty, 2010). For

instance debentures, are one of the example of debt as it is basically a long term loan. Debentures

are having a fixed charge i.e. rate of interest which remains fixed during the total period of

debentures. They may carry right against the property of company as debentures are sometimes

secured against some assets. On the other hand, equity can be considered as the owners fund or

liabilities and obligations which are related with the insiders or the owners. Because of the

separate entity concepts, owners and the enterprises are considered as separate from each other

hence the capital or fund which is invested in business by its owner is recognised as a liability for

the business entity.

5

assumptions.

These disclosure requirements are mandatory to follow hence any entity cannot ignore

such a legal and statutory requirements (Agoglia, Doupnik and Tsakumis, 2011). It they do so

then it will be considered as an offence and then the financial statements will not provide the

accurate information which are required to be stated there in.

For the increment in consistency and comparability regarding fair value measurement and

other disclosures related with it. International financial reporting standards had established a fair

value hierarchy. Such hierarchy is categorised into three levels. This gives highest priority to

unadjusted prices in which no any adjustments are worked out. Such price is quoted open market

of identical assets and liabilities and the lowest priority is given to unobservable inputs. There

are three levels which are categorised as below :

Level one : Quoted Price

Level two : Inputs other than quoted price

Level three : Unobservable inputs

TASK 2

2.1 Discussion over the key definition of of various terms which are used for differentiating debt

and equity as per IAS 32

As per IAS 32 debt and equity has different definition. But in normal sense, Debt reflects

the obligations in terms of money which are related with the outsiders. The cost associated with

such debts can be considered as a charge against profit (Altamuro and Beatty, 2010). For

instance debentures, are one of the example of debt as it is basically a long term loan. Debentures

are having a fixed charge i.e. rate of interest which remains fixed during the total period of

debentures. They may carry right against the property of company as debentures are sometimes

secured against some assets. On the other hand, equity can be considered as the owners fund or

liabilities and obligations which are related with the insiders or the owners. Because of the

separate entity concepts, owners and the enterprises are considered as separate from each other

hence the capital or fund which is invested in business by its owner is recognised as a liability for

the business entity.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In IAS 32 several terms are used which have different meanings through which user can

identify the headings in which they should get categorised. These terms are mentioned below:

Financial asset : Financial asset can be described as any asset which carry :-

◦ Cash

◦ Equity instrument which is related with some other firm or entity

◦ Investments made in some commodities

◦ Financial asset also include contractual rights over any entity for receipt of

payment .

◦ Contractual rights also includes exchange of financial rights or financial obligations

in other words it can be referred as the exchange of assets and liabilities.

Financial Liabilities : These are also defined in IAS 32, these can be referred as :

◦ Any contractual obligations related with payment of cash or any other financial

assets which are related with some other firm.

◦ Obligation in relation with exchange of assets with some other entity.

◦ Non derivative contract that may be get settled in own equity of entity.

◦ Derivative which can be get settled other than through exchange of fixed amount,

cash or some other financial holdings. Discuss over the issues which recognises

convoluted financial instruments present in financial instruments.

Equity Instruments: These instruments can be defined as the instruments which shows

the ownership of any person over the entity. Equity instruments consists voting rights.

Share certificate is given to the owner of the equity shares.

Debt is the outsiders right over the entity. Debt security holder cannot get the share of

profit but they carries less risk as compared with equity owners. Total equity consists of the

amount of equity shares, preference shares and retained earnings (Armstrong, Guay and Weber,

2010). Equity share can be considered as the holders fund. Issuer of financial instrument can

classify the instrument and its components. As on the initial recognition of financial liability,

financial asset as per the conditions which are mentioned there in the contractual agreement

between the holder of financial asset or bearer of liability and the person or entity with which

such asset and liability is related. Equity can be considered as the owners fund which can also be

categorised internal liability for which entity have less obligations. The outsider liabilities are

considered as preferable than internal liability holders.

6

identify the headings in which they should get categorised. These terms are mentioned below:

Financial asset : Financial asset can be described as any asset which carry :-

◦ Cash

◦ Equity instrument which is related with some other firm or entity

◦ Investments made in some commodities

◦ Financial asset also include contractual rights over any entity for receipt of

payment .

◦ Contractual rights also includes exchange of financial rights or financial obligations

in other words it can be referred as the exchange of assets and liabilities.

Financial Liabilities : These are also defined in IAS 32, these can be referred as :

◦ Any contractual obligations related with payment of cash or any other financial

assets which are related with some other firm.

◦ Obligation in relation with exchange of assets with some other entity.

◦ Non derivative contract that may be get settled in own equity of entity.

◦ Derivative which can be get settled other than through exchange of fixed amount,

cash or some other financial holdings. Discuss over the issues which recognises

convoluted financial instruments present in financial instruments.

Equity Instruments: These instruments can be defined as the instruments which shows

the ownership of any person over the entity. Equity instruments consists voting rights.

Share certificate is given to the owner of the equity shares.

Debt is the outsiders right over the entity. Debt security holder cannot get the share of

profit but they carries less risk as compared with equity owners. Total equity consists of the

amount of equity shares, preference shares and retained earnings (Armstrong, Guay and Weber,

2010). Equity share can be considered as the holders fund. Issuer of financial instrument can

classify the instrument and its components. As on the initial recognition of financial liability,

financial asset as per the conditions which are mentioned there in the contractual agreement

between the holder of financial asset or bearer of liability and the person or entity with which

such asset and liability is related. Equity can be considered as the owners fund which can also be

categorised internal liability for which entity have less obligations. The outsider liabilities are

considered as preferable than internal liability holders.

6

When an issuer applies the definition in paragraph 11 which classify whether financial

instrument is to be put in the category of equity, debt or as an asset.

Those instruments which doesn't contain any obligations which are related with any

contract

Debt instrument contains obligations which are to be paid back to the owner of that debt

instruments (Barth and Landsman, 2010). These are also having some fixed as well as

floating charges.

2.2 Discussion over the key characteristics or the criteria which are used to make differentiation

between debt and equity under IFRS IAS 32. Discussion of type of financial instruments

and how they recognised in financial statements.

Principle of IAS 32 define that the classification of financial instruments should be done either as

financial liabilities or as financial equity and it should not be in its legal form.

Equity instruments are considered as financial instrument only when-

a)There is no obligation in delivering in cash,

b)The is done by the issuer's equity instrument. It includes the following.

i)no contractual obligation should be there for the issuer for a non derivatives.

ii)by exchanging fixed amount of cash only a derivatives get settled.

Financial Instruments.

Equity Shares- This shares define the ownership of a shareholder in a particular organisation.

The holders has the rights to contribute their views and time. They also has the voting right.

Those who holds the equity shares have to bear all the losses as well as can enjoy the

benefits of the profit as per the ratio of the share held by him/her.

Preference shares- A person who hold preference share just get a fixed rate of dividend.

Preference share holder gets the priority in the sharing of the dividends as compared to the

ordinary shares (Bédard and Gendron, 2010). In case any kind of issue occurs as such

bankruptcy then too the preference share holders gets their share of fixed dividends.

7

instrument is to be put in the category of equity, debt or as an asset.

Those instruments which doesn't contain any obligations which are related with any

contract

Debt instrument contains obligations which are to be paid back to the owner of that debt

instruments (Barth and Landsman, 2010). These are also having some fixed as well as

floating charges.

2.2 Discussion over the key characteristics or the criteria which are used to make differentiation

between debt and equity under IFRS IAS 32. Discussion of type of financial instruments

and how they recognised in financial statements.

Principle of IAS 32 define that the classification of financial instruments should be done either as

financial liabilities or as financial equity and it should not be in its legal form.

Equity instruments are considered as financial instrument only when-

a)There is no obligation in delivering in cash,

b)The is done by the issuer's equity instrument. It includes the following.

i)no contractual obligation should be there for the issuer for a non derivatives.

ii)by exchanging fixed amount of cash only a derivatives get settled.

Financial Instruments.

Equity Shares- This shares define the ownership of a shareholder in a particular organisation.

The holders has the rights to contribute their views and time. They also has the voting right.

Those who holds the equity shares have to bear all the losses as well as can enjoy the

benefits of the profit as per the ratio of the share held by him/her.

Preference shares- A person who hold preference share just get a fixed rate of dividend.

Preference share holder gets the priority in the sharing of the dividends as compared to the

ordinary shares (Bédard and Gendron, 2010). In case any kind of issue occurs as such

bankruptcy then too the preference share holders gets their share of fixed dividends.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debentures- It is a long term security which has a fixed interest rate and it is issued and secured

against the assets. It is not issued to everyone, the person with good reputation and has good

credit worthiness are preferred for debentures.

Bonds- It is a kind of debt investment in which the money is lend by the investors to the

person(A businessmen or any government profile holder) who borrows for a variable or

fixed time period.

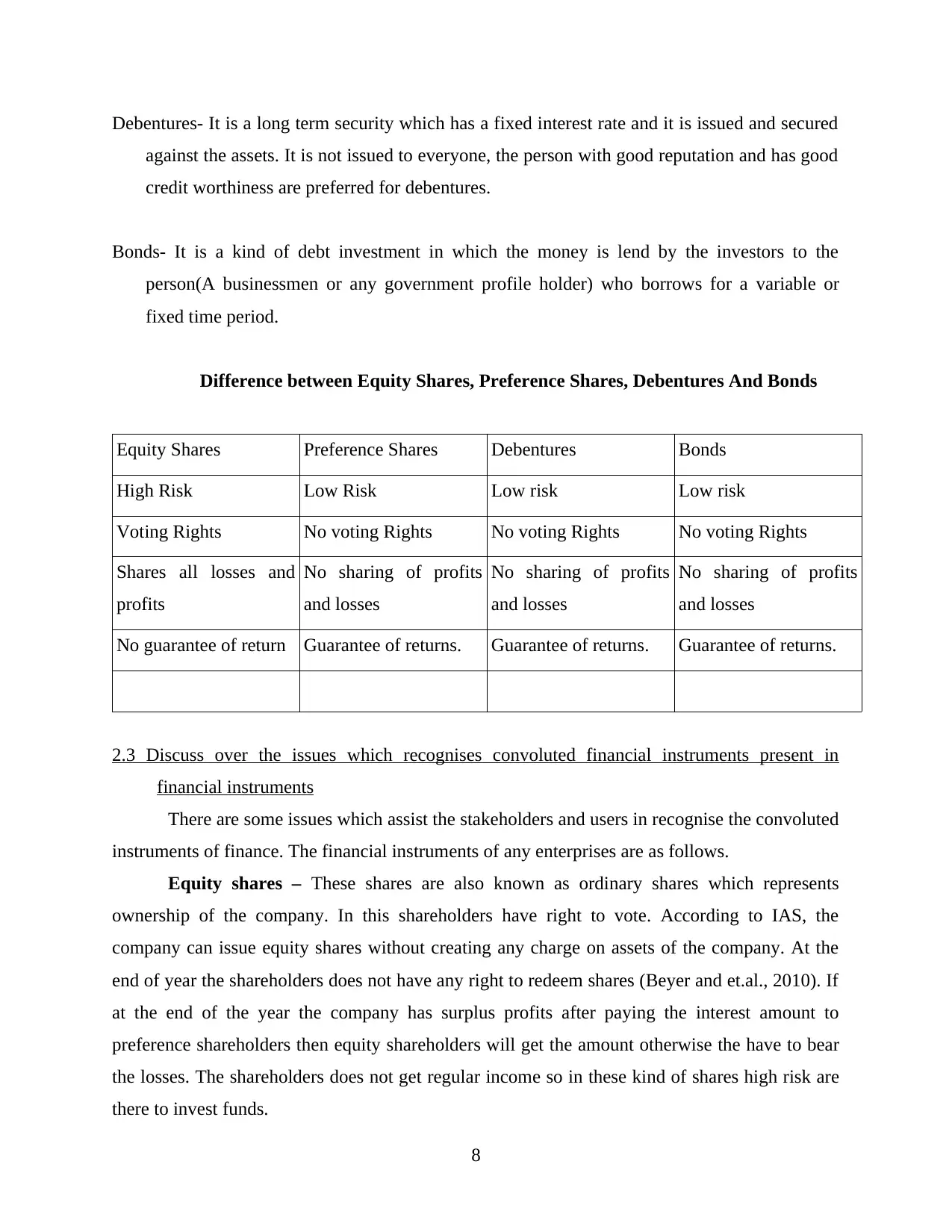

Difference between Equity Shares, Preference Shares, Debentures And Bonds

Equity Shares Preference Shares Debentures Bonds

High Risk Low Risk Low risk Low risk

Voting Rights No voting Rights No voting Rights No voting Rights

Shares all losses and

profits

No sharing of profits

and losses

No sharing of profits

and losses

No sharing of profits

and losses

No guarantee of return Guarantee of returns. Guarantee of returns. Guarantee of returns.

2.3 Discuss over the issues which recognises convoluted financial instruments present in

financial instruments

There are some issues which assist the stakeholders and users in recognise the convoluted

instruments of finance. The financial instruments of any enterprises are as follows.

Equity shares – These shares are also known as ordinary shares which represents

ownership of the company. In this shareholders have right to vote. According to IAS, the

company can issue equity shares without creating any charge on assets of the company. At the

end of year the shareholders does not have any right to redeem shares (Beyer and et.al., 2010). If

at the end of the year the company has surplus profits after paying the interest amount to

preference shareholders then equity shareholders will get the amount otherwise the have to bear

the losses. The shareholders does not get regular income so in these kind of shares high risk are

there to invest funds.

8

against the assets. It is not issued to everyone, the person with good reputation and has good

credit worthiness are preferred for debentures.

Bonds- It is a kind of debt investment in which the money is lend by the investors to the

person(A businessmen or any government profile holder) who borrows for a variable or

fixed time period.

Difference between Equity Shares, Preference Shares, Debentures And Bonds

Equity Shares Preference Shares Debentures Bonds

High Risk Low Risk Low risk Low risk

Voting Rights No voting Rights No voting Rights No voting Rights

Shares all losses and

profits

No sharing of profits

and losses

No sharing of profits

and losses

No sharing of profits

and losses

No guarantee of return Guarantee of returns. Guarantee of returns. Guarantee of returns.

2.3 Discuss over the issues which recognises convoluted financial instruments present in

financial instruments

There are some issues which assist the stakeholders and users in recognise the convoluted

instruments of finance. The financial instruments of any enterprises are as follows.

Equity shares – These shares are also known as ordinary shares which represents

ownership of the company. In this shareholders have right to vote. According to IAS, the

company can issue equity shares without creating any charge on assets of the company. At the

end of year the shareholders does not have any right to redeem shares (Beyer and et.al., 2010). If

at the end of the year the company has surplus profits after paying the interest amount to

preference shareholders then equity shareholders will get the amount otherwise the have to bear

the losses. The shareholders does not get regular income so in these kind of shares high risk are

there to invest funds.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Preference shares – These are those shares in which shareholders have preferential

rights over the dividends. The shareholders who had invest the money in these shares have

voting right to vote in the shareholder meeting and even they can speak also. There are two kind

of preference shares i.e. redeemable and irredeemable. In redeemable preference shares the

shareholders get the amount at particular point of time period. But in irredeemable preference

shares when the company goes into liquidation the these shares are redeem at that time period.

The shareholders get profits before the equity shareholders (Chen and et. al., 2010). Preference

shares doesn't carry risk. When investors or company issues these kind of shares then they does

not have to mortgage any property of the organisation.

Debentures – These are the debt instruments which help the company to raise the funds.

At the time of incorporation of the company can cannot issue the debenture on discount rate for

one year. Debentures are of two types secured and unsecured. In secured debentures the

company has to mortgage some property. But on unsecured debentures the company does not

have to mortgage and property (Dyreng, Mayew and Williams, 2012). In this the investors get

the regular income even after profits are not available by the company.

Separations of Debt and Equity

There are several factors through which it can be said that both debt and equity are two

different terms. The very first fact which can separate them out of each other is Debt is outsiders

liability and equity can categorised as internal liabilities. External liabilities are always preferred

over the internal liabilities. Equity shares and preference shares as owners capital can be put in

the category of Equity. And debentures and other long term loans and short term liabilities like

creditors for goods etc. can be classified in the category of debt.

CONCLUSION

As per the above mentioned facts and concepts it can be concluded that when the user

uses and follows the guidelines which are mentioned in IFRS which have been issued by the

IASB. Then it can be said that through following these guidelines an entity can show or present a

better view in front of its users or stakeholder. As per the given facts it can be observed that if an

entity follows the rules and guidelines mentioned there in the IFRS.

9

rights over the dividends. The shareholders who had invest the money in these shares have

voting right to vote in the shareholder meeting and even they can speak also. There are two kind

of preference shares i.e. redeemable and irredeemable. In redeemable preference shares the

shareholders get the amount at particular point of time period. But in irredeemable preference

shares when the company goes into liquidation the these shares are redeem at that time period.

The shareholders get profits before the equity shareholders (Chen and et. al., 2010). Preference

shares doesn't carry risk. When investors or company issues these kind of shares then they does

not have to mortgage any property of the organisation.

Debentures – These are the debt instruments which help the company to raise the funds.

At the time of incorporation of the company can cannot issue the debenture on discount rate for

one year. Debentures are of two types secured and unsecured. In secured debentures the

company has to mortgage some property. But on unsecured debentures the company does not

have to mortgage and property (Dyreng, Mayew and Williams, 2012). In this the investors get

the regular income even after profits are not available by the company.

Separations of Debt and Equity

There are several factors through which it can be said that both debt and equity are two

different terms. The very first fact which can separate them out of each other is Debt is outsiders

liability and equity can categorised as internal liabilities. External liabilities are always preferred

over the internal liabilities. Equity shares and preference shares as owners capital can be put in

the category of Equity. And debentures and other long term loans and short term liabilities like

creditors for goods etc. can be classified in the category of debt.

CONCLUSION

As per the above mentioned facts and concepts it can be concluded that when the user

uses and follows the guidelines which are mentioned in IFRS which have been issued by the

IASB. Then it can be said that through following these guidelines an entity can show or present a

better view in front of its users or stakeholder. As per the given facts it can be observed that if an

entity follows the rules and guidelines mentioned there in the IFRS.

9

REFERENCES

Books and Journals

Agoglia, C. P., Doupnik, T. S. and Tsakumis, G. T., 2011. Principles-based versus rules-based

accounting standards: The influence of standard precision and audit committee strength

on financial reporting decisions. The accounting review. 86(3). pp.747-767.

10

Books and Journals

Agoglia, C. P., Doupnik, T. S. and Tsakumis, G. T., 2011. Principles-based versus rules-based

accounting standards: The influence of standard precision and audit committee strength

on financial reporting decisions. The accounting review. 86(3). pp.747-767.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.