Financial Reporting Analysis: IAS, IFRS, and Lloyds Banking Group

VerifiedAdded on 2023/01/13

|19

|4994

|51

Report

AI Summary

This report offers a detailed analysis of financial reporting, encompassing its context, purpose, and the frameworks that govern it, including both conceptual and regulatory aspects. It explores the roles and benefits of financial information for various stakeholders, examining how financial reporting contributes to organizational objectives and growth. The report delves into the preparation and presentation of key financial statements, such as the income statement, statement of retained earnings, and balance sheet, adhering to IAS 1 guidelines. Furthermore, it provides an interpretation of financial statements, using Lloyds Banking Group as a case study, and compares international accounting standards (IAS) with international financial reporting standards (IFRS). The benefits of IFRS are highlighted, along with an assessment of global compliance levels. The report concludes with a summary of the key findings and references.

FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Context and Purpose of financial reporting:............................................................................1

2. Conceptual and Regulatory Framework:.................................................................................2

3. Main stakeholders of an organisation and explain how they benefit from financial

information:..................................................................................................................................4

4. Value of financial reporting for meeting organisational objectives and growth:....................4

5. Preparation and presentation of main financial statements as per IAS 1:................................5

6. Interpretation of financial statements of a company which is listed in FTSE 100.:................9

7. Comparison of international accounting standard (IAS) and international financial reporting

standard (IFRS)..........................................................................................................................12

8. Benefits of IFRS (International Financial Reporting Standards)...........................................12

9. Degree of compliance with IFRS by organisation across the world......................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Context and Purpose of financial reporting:............................................................................1

2. Conceptual and Regulatory Framework:.................................................................................2

3. Main stakeholders of an organisation and explain how they benefit from financial

information:..................................................................................................................................4

4. Value of financial reporting for meeting organisational objectives and growth:....................4

5. Preparation and presentation of main financial statements as per IAS 1:................................5

6. Interpretation of financial statements of a company which is listed in FTSE 100.:................9

7. Comparison of international accounting standard (IAS) and international financial reporting

standard (IFRS)..........................................................................................................................12

8. Benefits of IFRS (International Financial Reporting Standards)...........................................12

9. Degree of compliance with IFRS by organisation across the world......................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Every commercial entity or organisation preserve and maintain specific set of accounting

and other business records with respect to accounting or financial period which are

comprehensive and combines crucial fiscal events/transaction that are occurred in enterprise.

This is compulsory for different corporations to expose and provide crucial information to

stakeholders whether internal or external (Abeysekera, 2013). For ensuring consistence and

support comparability, following the process of financial reporting is quite essential by applying

specific formats, assumptions and core principles across the globe. These are commonly

regarded as International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS).

This study report seeks to highlight the main context and basic purposes of entire process

of financial reporting, contains key advantages and manners related ensuring proper

compliances, fixing accountability and core principles. In addition, multiple countries have

analyzed to address for anomalies in Financial Reporting Standards. In this context, a client

named Lloyds Banking Group of accounting firm Grant Thornton Accountancy has been

chosen. Lloyds Banking Group belongs to FTSE 100 group and a leading retail banking

corporation, headquartered in London City, United Kingdom (Representative Client List of

Grant Thornton, 2019). The group is engaged in providing banking services as well as related

financial services to different client across the world.

TASK

1. Context and Purpose of financial reporting:

The word ' Financial Reporting' could be described as presentation and communication of

fiscal information to distinct key stakeholders. Financial reporting is wider aspect which involves

different reports in a specific format to communicate meaningful and relevant information for

different users. Financial reporting process is mainly used in context of companies specially

listed companies in public have invested funds (Albu and Albu, 2012). Main purpose of it is to

support management in effectively reporting the actual financial performance to different

interested parties which are generally known as stakeholders. This entire process is focused on

different standards, guidelines and assumptions which are universally applied by different

1

Every commercial entity or organisation preserve and maintain specific set of accounting

and other business records with respect to accounting or financial period which are

comprehensive and combines crucial fiscal events/transaction that are occurred in enterprise.

This is compulsory for different corporations to expose and provide crucial information to

stakeholders whether internal or external (Abeysekera, 2013). For ensuring consistence and

support comparability, following the process of financial reporting is quite essential by applying

specific formats, assumptions and core principles across the globe. These are commonly

regarded as International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS).

This study report seeks to highlight the main context and basic purposes of entire process

of financial reporting, contains key advantages and manners related ensuring proper

compliances, fixing accountability and core principles. In addition, multiple countries have

analyzed to address for anomalies in Financial Reporting Standards. In this context, a client

named Lloyds Banking Group of accounting firm Grant Thornton Accountancy has been

chosen. Lloyds Banking Group belongs to FTSE 100 group and a leading retail banking

corporation, headquartered in London City, United Kingdom (Representative Client List of

Grant Thornton, 2019). The group is engaged in providing banking services as well as related

financial services to different client across the world.

TASK

1. Context and Purpose of financial reporting:

The word ' Financial Reporting' could be described as presentation and communication of

fiscal information to distinct key stakeholders. Financial reporting is wider aspect which involves

different reports in a specific format to communicate meaningful and relevant information for

different users. Financial reporting process is mainly used in context of companies specially

listed companies in public have invested funds (Albu and Albu, 2012). Main purpose of it is to

support management in effectively reporting the actual financial performance to different

interested parties which are generally known as stakeholders. This entire process is focused on

different standards, guidelines and assumptions which are universally applied by different

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

corporation belongs to different nations. So another major purpose of financial reporting is make

uniformity in accounting practices and presentation of financial statements.

2. Conceptual and Regulatory Framework:

Financial reporting provides two key frameworks for achieve uniformity in accounts

prepared and practices applied. These frameworks are widely applied by different-different

corporations form different geographical locations to attain easiness in financial reporting.

Conceptual and Regulatory are 2 major kind of framework which are used by corporation like

Lloyds Banking Group. Here is a comprehensive discussion of these frameworks in context of

respective corporation, as follows:

Conceptual framework:

The principles of financial reporting are described together with a concrete framework to

aid in the implementation of different standards. The structure is therefore needed to allow

Lloyd's management to build a solid theoretical basis to calculate, present and convey to its

various stakeholders, effectively, the different financial activities they conduct. A conceptual

structure can specifically be used as a declaration of General Acceptable Accounting Principles

(GAAP) in light of financial reporting (Botzem, 2012). These framework serve as the guideline

and benchmark for evaluating and improvising company's existing accounting practices. Failure

to create such kind of framework will enhance the prevalence and the no. of accounting

irregularities significantly through misuse of profits. So, a conceptual framework aid in:

Development and adoption of future or potential standards;

Promoting coherency among accounting rules/regulations and specified standards;

Formation and effective presentation of corporation's Financial Statements to their crucial

stakeholders.

The financial reporting's conceptual framework allows for the preparing and

presentations of financial statements adopted by the IASB as collection of accounting rules. The

conceptual framework relates to the development and decision-making of accounting data to

meet user requirements. Throughout preparation of accounting reports, the conceptual

framework helps to define "best practice."

Regulatory Framework:

A regulatory framework, as its name implies, defines the way wherein financial

information reporting is conducted worldwide among corporations. It emphasises on governance

2

uniformity in accounting practices and presentation of financial statements.

2. Conceptual and Regulatory Framework:

Financial reporting provides two key frameworks for achieve uniformity in accounts

prepared and practices applied. These frameworks are widely applied by different-different

corporations form different geographical locations to attain easiness in financial reporting.

Conceptual and Regulatory are 2 major kind of framework which are used by corporation like

Lloyds Banking Group. Here is a comprehensive discussion of these frameworks in context of

respective corporation, as follows:

Conceptual framework:

The principles of financial reporting are described together with a concrete framework to

aid in the implementation of different standards. The structure is therefore needed to allow

Lloyd's management to build a solid theoretical basis to calculate, present and convey to its

various stakeholders, effectively, the different financial activities they conduct. A conceptual

structure can specifically be used as a declaration of General Acceptable Accounting Principles

(GAAP) in light of financial reporting (Botzem, 2012). These framework serve as the guideline

and benchmark for evaluating and improvising company's existing accounting practices. Failure

to create such kind of framework will enhance the prevalence and the no. of accounting

irregularities significantly through misuse of profits. So, a conceptual framework aid in:

Development and adoption of future or potential standards;

Promoting coherency among accounting rules/regulations and specified standards;

Formation and effective presentation of corporation's Financial Statements to their crucial

stakeholders.

The financial reporting's conceptual framework allows for the preparing and

presentations of financial statements adopted by the IASB as collection of accounting rules. The

conceptual framework relates to the development and decision-making of accounting data to

meet user requirements. Throughout preparation of accounting reports, the conceptual

framework helps to define "best practice."

Regulatory Framework:

A regulatory framework, as its name implies, defines the way wherein financial

information reporting is conducted worldwide among corporations. It emphasises on governance

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

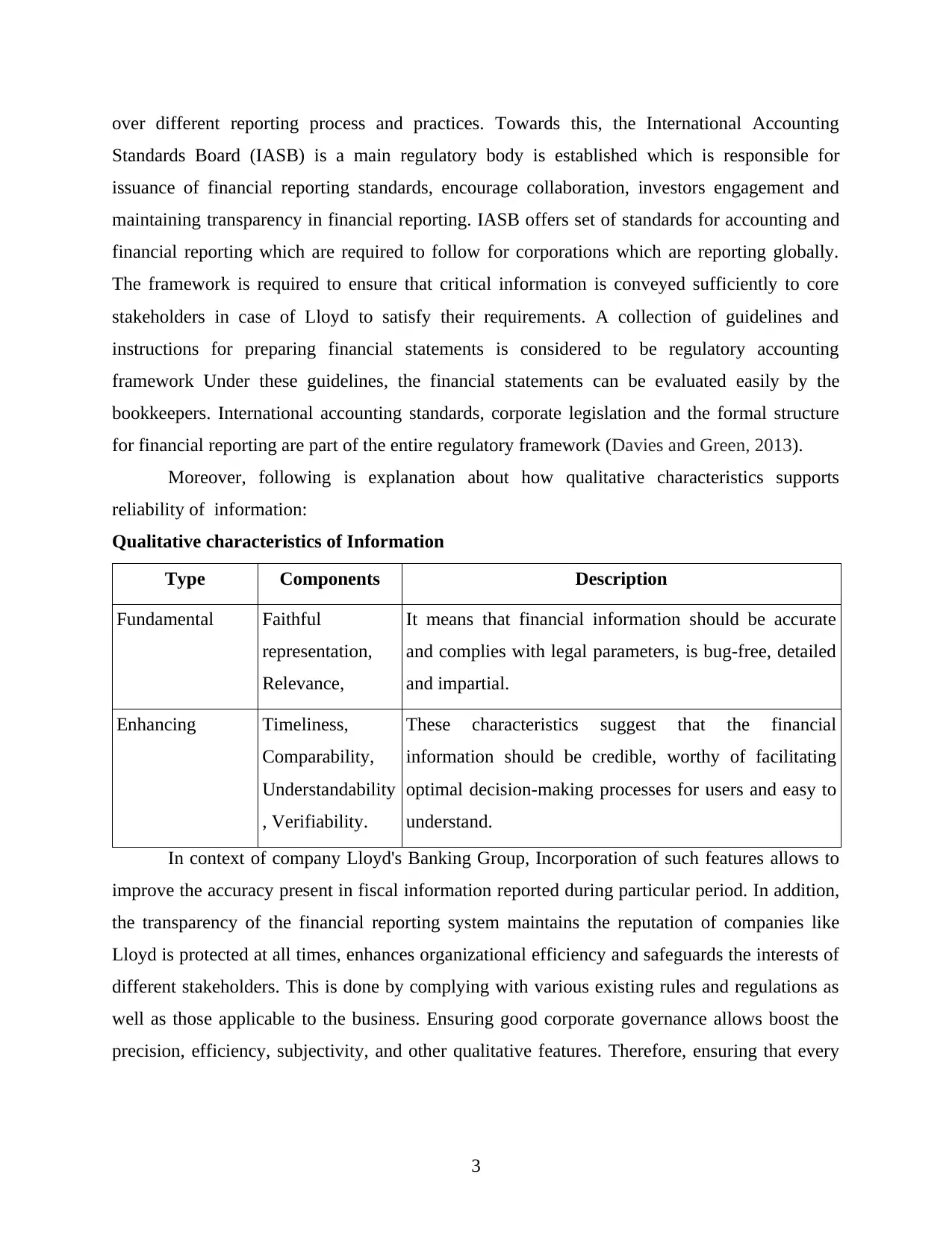

over different reporting process and practices. Towards this, the International Accounting

Standards Board (IASB) is a main regulatory body is established which is responsible for

issuance of financial reporting standards, encourage collaboration, investors engagement and

maintaining transparency in financial reporting. IASB offers set of standards for accounting and

financial reporting which are required to follow for corporations which are reporting globally.

The framework is required to ensure that critical information is conveyed sufficiently to core

stakeholders in case of Lloyd to satisfy their requirements. A collection of guidelines and

instructions for preparing financial statements is considered to be regulatory accounting

framework Under these guidelines, the financial statements can be evaluated easily by the

bookkeepers. International accounting standards, corporate legislation and the formal structure

for financial reporting are part of the entire regulatory framework (Davies and Green, 2013).

Moreover, following is explanation about how qualitative characteristics supports

reliability of information:

Qualitative characteristics of Information

Type Components Description

Fundamental Faithful

representation,

Relevance,

It means that financial information should be accurate

and complies with legal parameters, is bug-free, detailed

and impartial.

Enhancing Timeliness,

Comparability,

Understandability

, Verifiability.

These characteristics suggest that the financial

information should be credible, worthy of facilitating

optimal decision-making processes for users and easy to

understand.

In context of company Lloyd's Banking Group, Incorporation of such features allows to

improve the accuracy present in fiscal information reported during particular period. In addition,

the transparency of the financial reporting system maintains the reputation of companies like

Lloyd is protected at all times, enhances organizational efficiency and safeguards the interests of

different stakeholders. This is done by complying with various existing rules and regulations as

well as those applicable to the business. Ensuring good corporate governance allows boost the

precision, efficiency, subjectivity, and other qualitative features. Therefore, ensuring that every

3

Standards Board (IASB) is a main regulatory body is established which is responsible for

issuance of financial reporting standards, encourage collaboration, investors engagement and

maintaining transparency in financial reporting. IASB offers set of standards for accounting and

financial reporting which are required to follow for corporations which are reporting globally.

The framework is required to ensure that critical information is conveyed sufficiently to core

stakeholders in case of Lloyd to satisfy their requirements. A collection of guidelines and

instructions for preparing financial statements is considered to be regulatory accounting

framework Under these guidelines, the financial statements can be evaluated easily by the

bookkeepers. International accounting standards, corporate legislation and the formal structure

for financial reporting are part of the entire regulatory framework (Davies and Green, 2013).

Moreover, following is explanation about how qualitative characteristics supports

reliability of information:

Qualitative characteristics of Information

Type Components Description

Fundamental Faithful

representation,

Relevance,

It means that financial information should be accurate

and complies with legal parameters, is bug-free, detailed

and impartial.

Enhancing Timeliness,

Comparability,

Understandability

, Verifiability.

These characteristics suggest that the financial

information should be credible, worthy of facilitating

optimal decision-making processes for users and easy to

understand.

In context of company Lloyd's Banking Group, Incorporation of such features allows to

improve the accuracy present in fiscal information reported during particular period. In addition,

the transparency of the financial reporting system maintains the reputation of companies like

Lloyd is protected at all times, enhances organizational efficiency and safeguards the interests of

different stakeholders. This is done by complying with various existing rules and regulations as

well as those applicable to the business. Ensuring good corporate governance allows boost the

precision, efficiency, subjectivity, and other qualitative features. Therefore, ensuring that every

3

form of misrepresentation or mistake is avoided from happening, and successful internal controls

are preserved (Eccles, Krzus, Rogers and Serafeim, 2012).

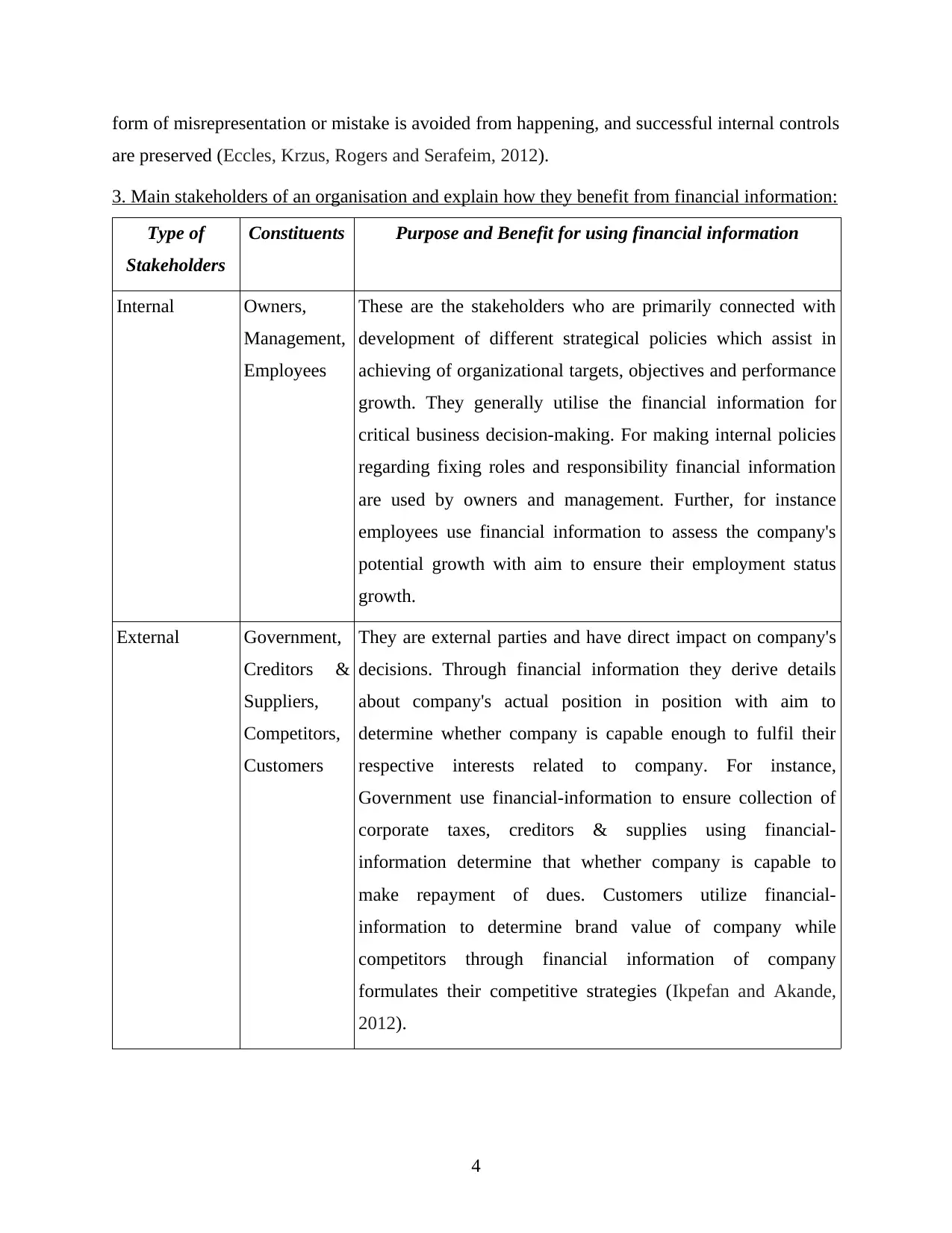

3. Main stakeholders of an organisation and explain how they benefit from financial information:

Type of

Stakeholders

Constituents Purpose and Benefit for using financial information

Internal Owners,

Management,

Employees

These are the stakeholders who are primarily connected with

development of different strategical policies which assist in

achieving of organizational targets, objectives and performance

growth. They generally utilise the financial information for

critical business decision-making. For making internal policies

regarding fixing roles and responsibility financial information

are used by owners and management. Further, for instance

employees use financial information to assess the company's

potential growth with aim to ensure their employment status

growth.

External Government,

Creditors &

Suppliers,

Competitors,

Customers

They are external parties and have direct impact on company's

decisions. Through financial information they derive details

about company's actual position in position with aim to

determine whether company is capable enough to fulfil their

respective interests related to company. For instance,

Government use financial-information to ensure collection of

corporate taxes, creditors & supplies using financial-

information determine that whether company is capable to

make repayment of dues. Customers utilize financial-

information to determine brand value of company while

competitors through financial information of company

formulates their competitive strategies (Ikpefan and Akande,

2012).

4

are preserved (Eccles, Krzus, Rogers and Serafeim, 2012).

3. Main stakeholders of an organisation and explain how they benefit from financial information:

Type of

Stakeholders

Constituents Purpose and Benefit for using financial information

Internal Owners,

Management,

Employees

These are the stakeholders who are primarily connected with

development of different strategical policies which assist in

achieving of organizational targets, objectives and performance

growth. They generally utilise the financial information for

critical business decision-making. For making internal policies

regarding fixing roles and responsibility financial information

are used by owners and management. Further, for instance

employees use financial information to assess the company's

potential growth with aim to ensure their employment status

growth.

External Government,

Creditors &

Suppliers,

Competitors,

Customers

They are external parties and have direct impact on company's

decisions. Through financial information they derive details

about company's actual position in position with aim to

determine whether company is capable enough to fulfil their

respective interests related to company. For instance,

Government use financial-information to ensure collection of

corporate taxes, creditors & supplies using financial-

information determine that whether company is capable to

make repayment of dues. Customers utilize financial-

information to determine brand value of company while

competitors through financial information of company

formulates their competitive strategies (Ikpefan and Akande,

2012).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Value of financial reporting for meeting organisational objectives and growth:

Financial reporting is crucial aspect of every entity's organisational structure as it defines

the performance growth and goals. It involves all the major financial and accounting elements of

an organisation which support management in taking decisions and setting goals. As in

corporation Lloyds Banking Group, managers through financial reporting determine their current

performance and capabilities, which further assist them in achievement of targeted growth and

pre-determined objectives. With the help of income statement, stakeholders able to evaluate the

overall profit of the company for the accounting period. Along with this, it provide the clear

understand that how much expenses company occur due to production or administration period.

In addition, with the help of balance sheet, external parties able to analyse the financial position

of the company and attract potential investors who can invest in the business or maximise the

liquidity of the organization. So with the help of financial reporting, business able to achieve

organizational goals & objectives (Leuz and Wysocki, 2016).

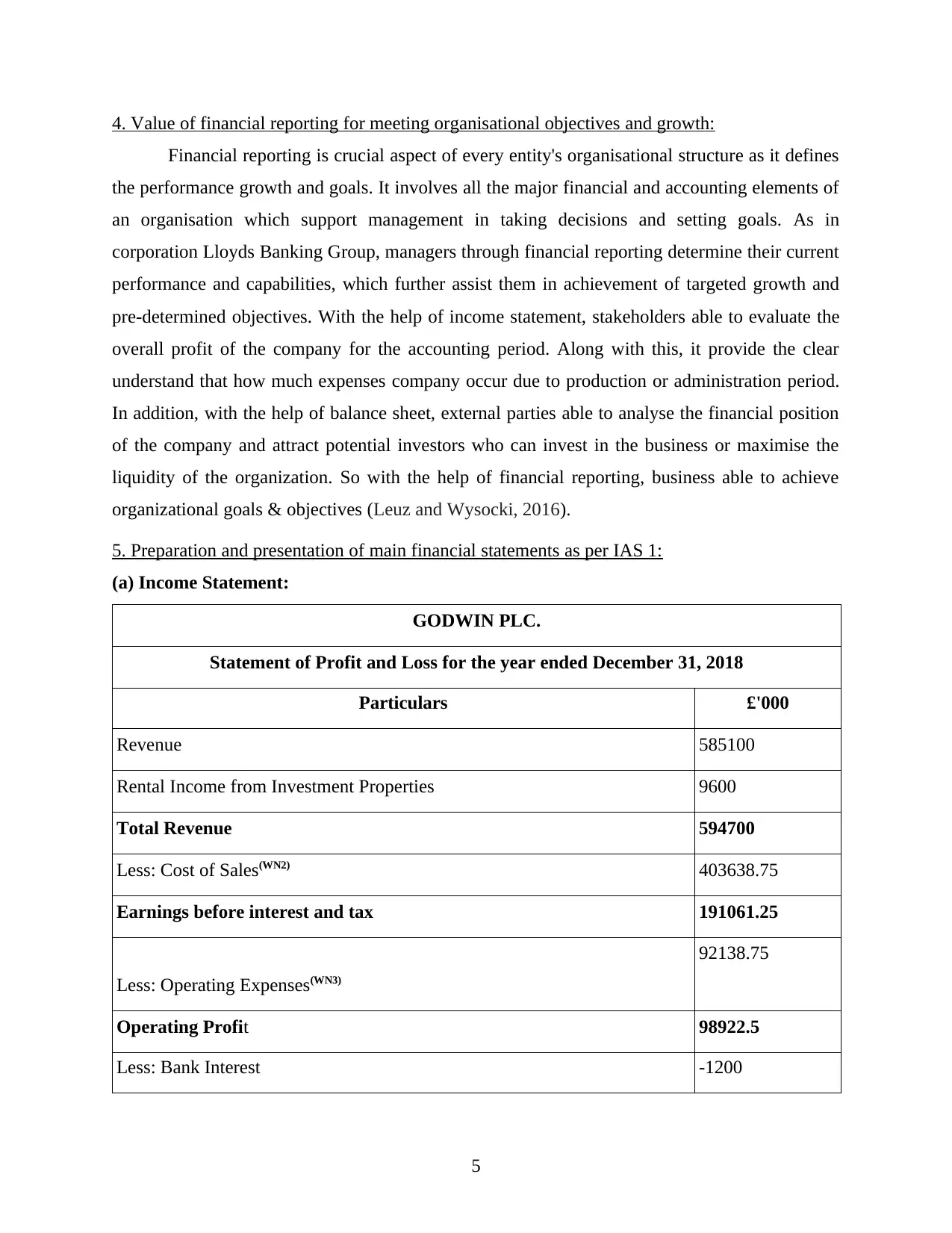

5. Preparation and presentation of main financial statements as per IAS 1:

(a) Income Statement:

GODWIN PLC.

Statement of Profit and Loss for the year ended December 31, 2018

Particulars £'000

Revenue 585100

Rental Income from Investment Properties 9600

Total Revenue 594700

Less: Cost of Sales(WN2) 403638.75

Earnings before interest and tax 191061.25

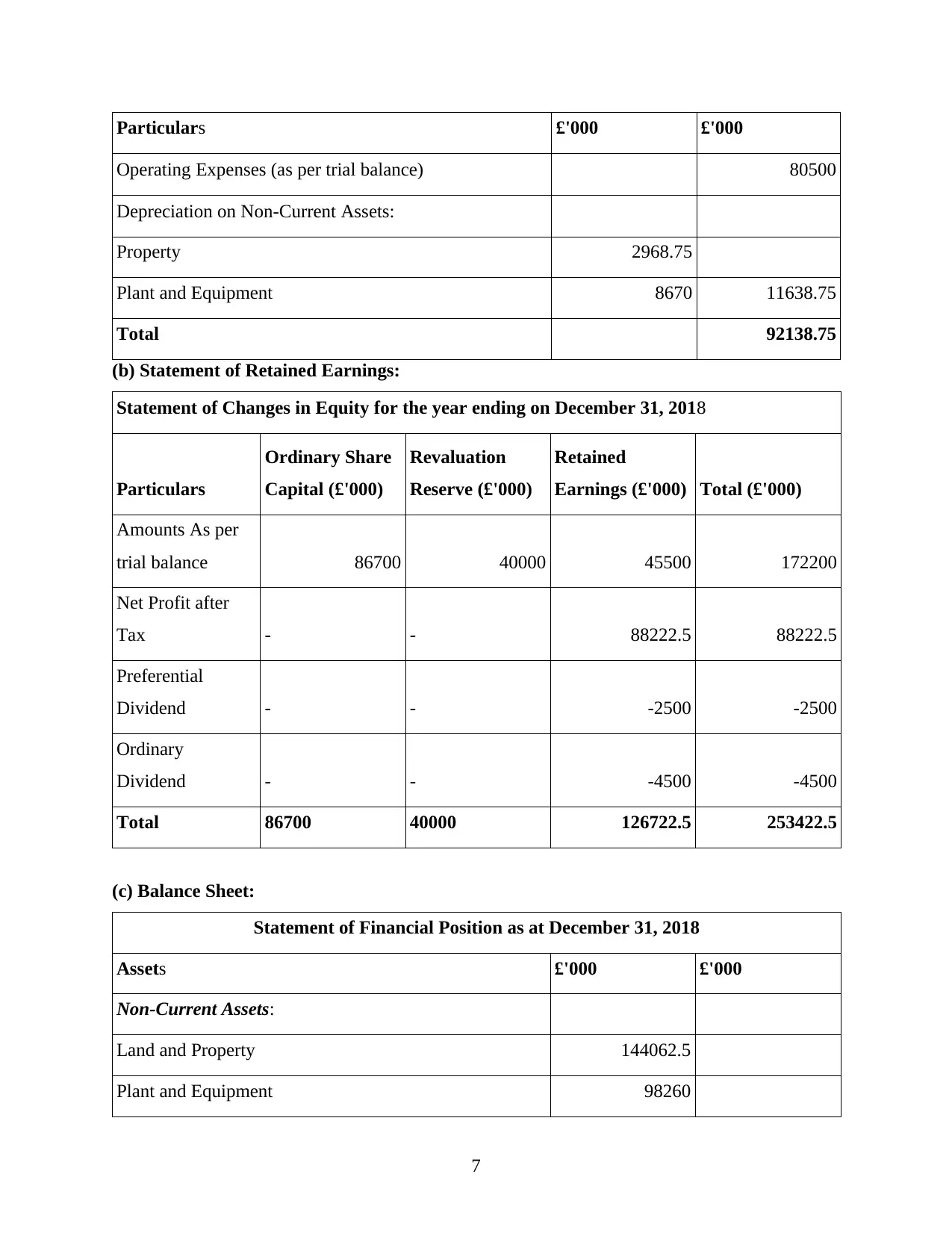

Less: Operating Expenses(WN3)

92138.75

Operating Profit 98922.5

Less: Bank Interest -1200

5

Financial reporting is crucial aspect of every entity's organisational structure as it defines

the performance growth and goals. It involves all the major financial and accounting elements of

an organisation which support management in taking decisions and setting goals. As in

corporation Lloyds Banking Group, managers through financial reporting determine their current

performance and capabilities, which further assist them in achievement of targeted growth and

pre-determined objectives. With the help of income statement, stakeholders able to evaluate the

overall profit of the company for the accounting period. Along with this, it provide the clear

understand that how much expenses company occur due to production or administration period.

In addition, with the help of balance sheet, external parties able to analyse the financial position

of the company and attract potential investors who can invest in the business or maximise the

liquidity of the organization. So with the help of financial reporting, business able to achieve

organizational goals & objectives (Leuz and Wysocki, 2016).

5. Preparation and presentation of main financial statements as per IAS 1:

(a) Income Statement:

GODWIN PLC.

Statement of Profit and Loss for the year ended December 31, 2018

Particulars £'000

Revenue 585100

Rental Income from Investment Properties 9600

Total Revenue 594700

Less: Cost of Sales(WN2) 403638.75

Earnings before interest and tax 191061.25

Less: Operating Expenses(WN3)

92138.75

Operating Profit 98922.5

Less: Bank Interest -1200

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

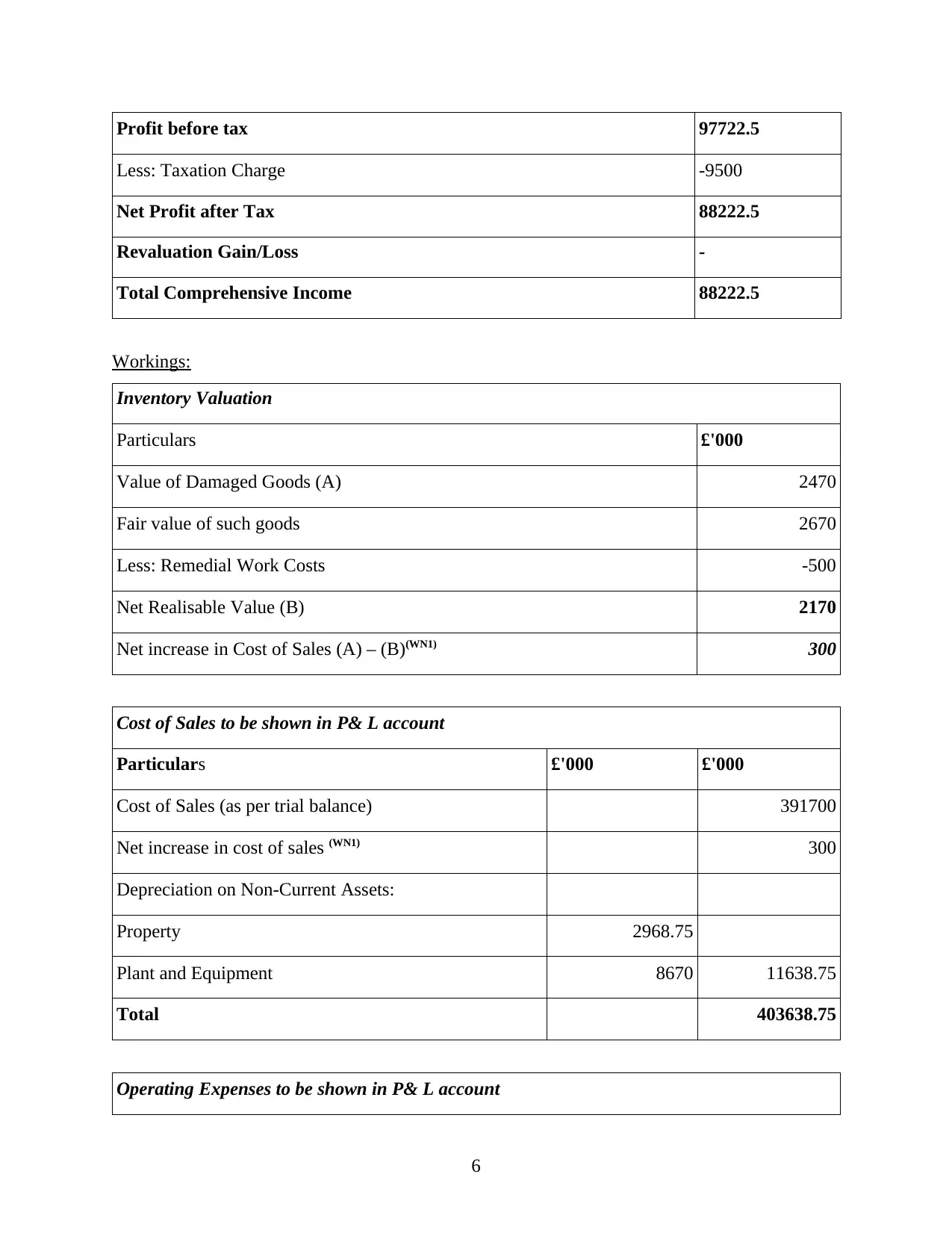

Profit before tax 97722.5

Less: Taxation Charge -9500

Net Profit after Tax 88222.5

Revaluation Gain/Loss -

Total Comprehensive Income 88222.5

Workings:

Inventory Valuation

Particulars £'000

Value of Damaged Goods (A) 2470

Fair value of such goods 2670

Less: Remedial Work Costs -500

Net Realisable Value (B) 2170

Net increase in Cost of Sales (A) – (B)(WN1) 300

Cost of Sales to be shown in P& L account

Particulars £'000 £'000

Cost of Sales (as per trial balance) 391700

Net increase in cost of sales (WN1) 300

Depreciation on Non-Current Assets:

Property 2968.75

Plant and Equipment 8670 11638.75

Total 403638.75

Operating Expenses to be shown in P& L account

6

Less: Taxation Charge -9500

Net Profit after Tax 88222.5

Revaluation Gain/Loss -

Total Comprehensive Income 88222.5

Workings:

Inventory Valuation

Particulars £'000

Value of Damaged Goods (A) 2470

Fair value of such goods 2670

Less: Remedial Work Costs -500

Net Realisable Value (B) 2170

Net increase in Cost of Sales (A) – (B)(WN1) 300

Cost of Sales to be shown in P& L account

Particulars £'000 £'000

Cost of Sales (as per trial balance) 391700

Net increase in cost of sales (WN1) 300

Depreciation on Non-Current Assets:

Property 2968.75

Plant and Equipment 8670 11638.75

Total 403638.75

Operating Expenses to be shown in P& L account

6

Particulars £'000 £'000

Operating Expenses (as per trial balance) 80500

Depreciation on Non-Current Assets:

Property 2968.75

Plant and Equipment 8670 11638.75

Total 92138.75

(b) Statement of Retained Earnings:

Statement of Changes in Equity for the year ending on December 31, 2018

Particulars

Ordinary Share

Capital (£'000)

Revaluation

Reserve (£'000)

Retained

Earnings (£'000) Total (£'000)

Amounts As per

trial balance 86700 40000 45500 172200

Net Profit after

Tax - - 88222.5 88222.5

Preferential

Dividend - - -2500 -2500

Ordinary

Dividend - - -4500 -4500

Total 86700 40000 126722.5 253422.5

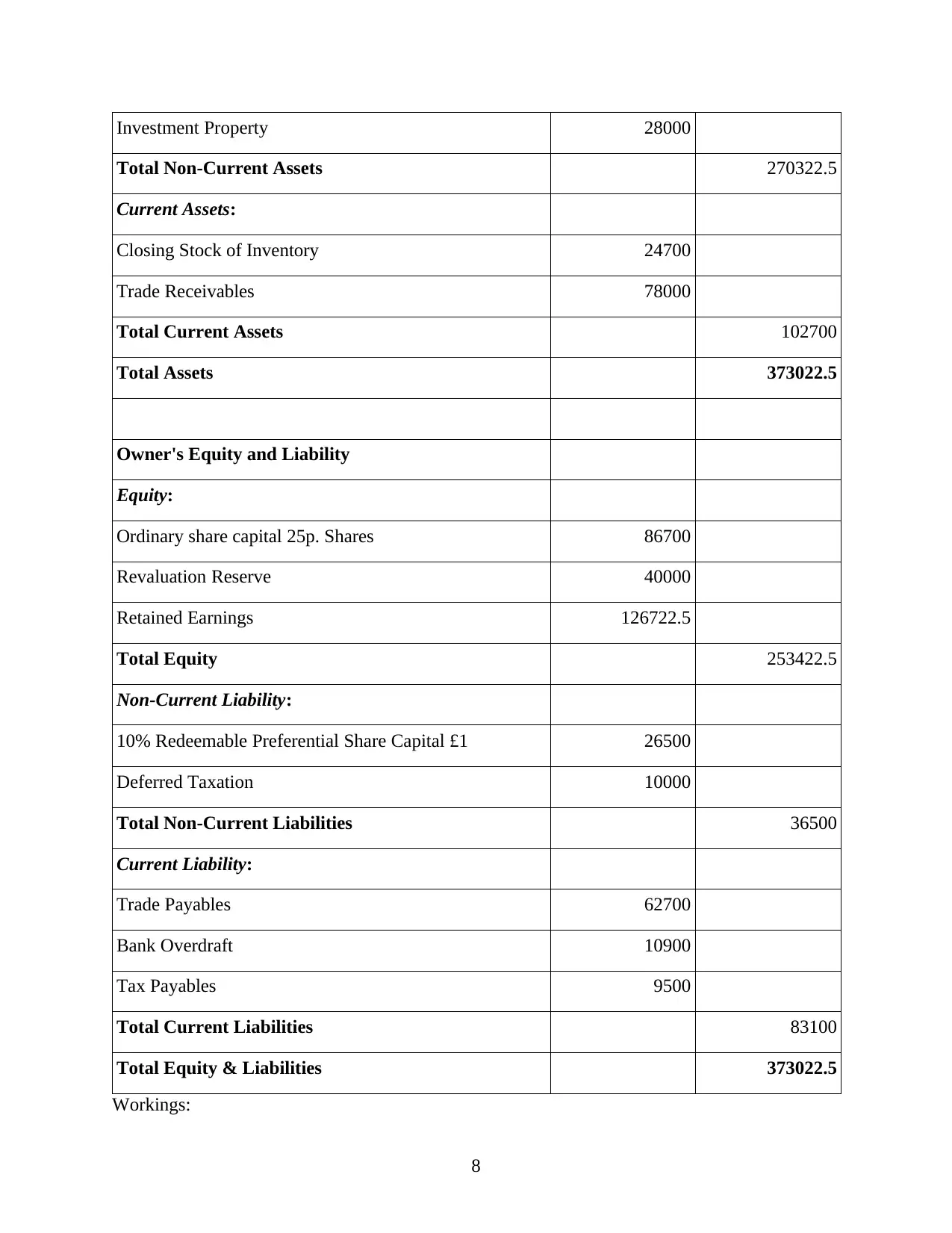

(c) Balance Sheet:

Statement of Financial Position as at December 31, 2018

Assets £'000 £'000

Non-Current Assets:

Land and Property 144062.5

Plant and Equipment 98260

7

Operating Expenses (as per trial balance) 80500

Depreciation on Non-Current Assets:

Property 2968.75

Plant and Equipment 8670 11638.75

Total 92138.75

(b) Statement of Retained Earnings:

Statement of Changes in Equity for the year ending on December 31, 2018

Particulars

Ordinary Share

Capital (£'000)

Revaluation

Reserve (£'000)

Retained

Earnings (£'000) Total (£'000)

Amounts As per

trial balance 86700 40000 45500 172200

Net Profit after

Tax - - 88222.5 88222.5

Preferential

Dividend - - -2500 -2500

Ordinary

Dividend - - -4500 -4500

Total 86700 40000 126722.5 253422.5

(c) Balance Sheet:

Statement of Financial Position as at December 31, 2018

Assets £'000 £'000

Non-Current Assets:

Land and Property 144062.5

Plant and Equipment 98260

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Investment Property 28000

Total Non-Current Assets 270322.5

Current Assets:

Closing Stock of Inventory 24700

Trade Receivables 78000

Total Current Assets 102700

Total Assets 373022.5

Owner's Equity and Liability

Equity:

Ordinary share capital 25p. Shares 86700

Revaluation Reserve 40000

Retained Earnings 126722.5

Total Equity 253422.5

Non-Current Liability:

10% Redeemable Preferential Share Capital £1 26500

Deferred Taxation 10000

Total Non-Current Liabilities 36500

Current Liability:

Trade Payables 62700

Bank Overdraft 10900

Tax Payables 9500

Total Current Liabilities 83100

Total Equity & Liabilities 373022.5

Workings:

8

Total Non-Current Assets 270322.5

Current Assets:

Closing Stock of Inventory 24700

Trade Receivables 78000

Total Current Assets 102700

Total Assets 373022.5

Owner's Equity and Liability

Equity:

Ordinary share capital 25p. Shares 86700

Revaluation Reserve 40000

Retained Earnings 126722.5

Total Equity 253422.5

Non-Current Liability:

10% Redeemable Preferential Share Capital £1 26500

Deferred Taxation 10000

Total Non-Current Liabilities 36500

Current Liability:

Trade Payables 62700

Bank Overdraft 10900

Tax Payables 9500

Total Current Liabilities 83100

Total Equity & Liabilities 373022.5

Workings:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

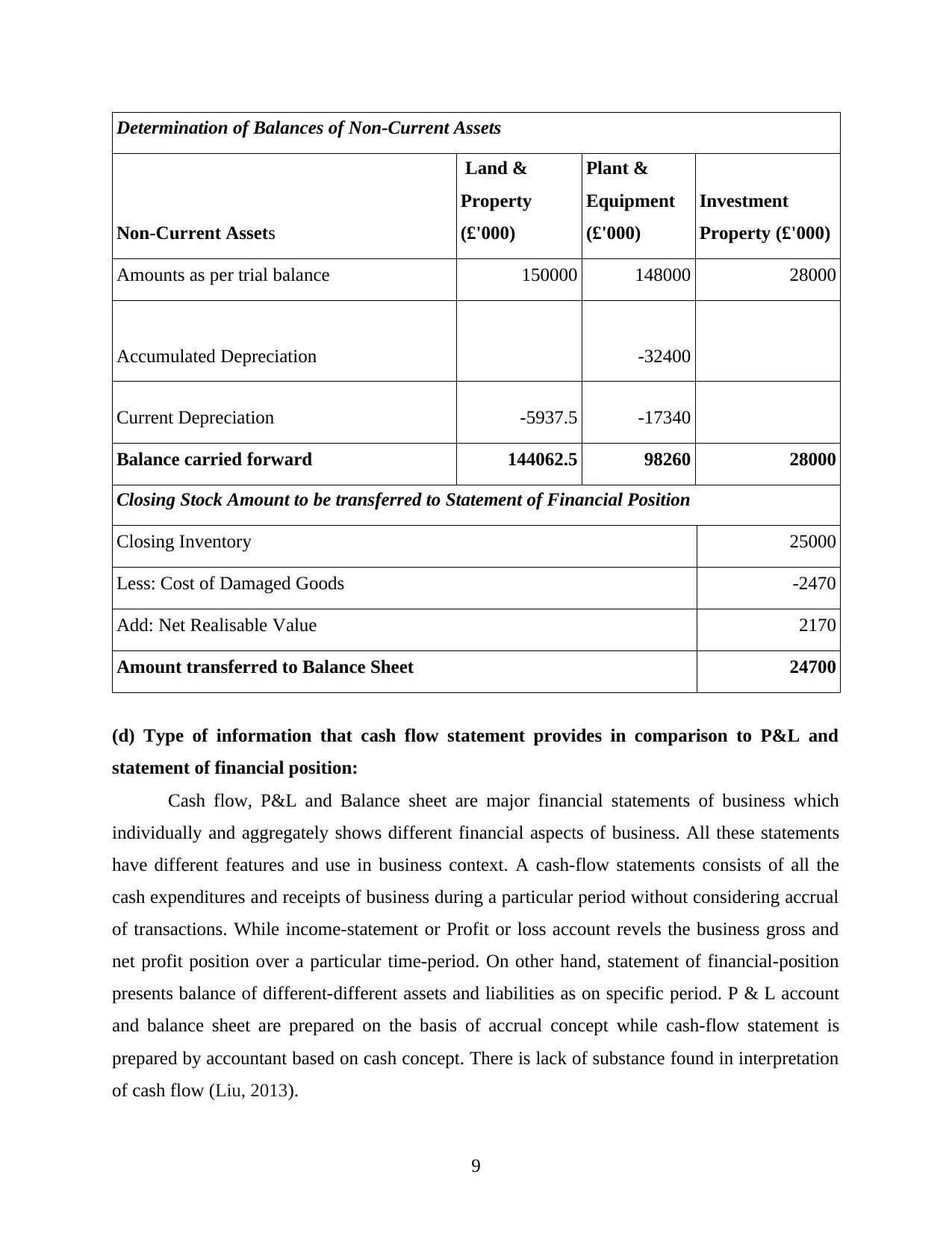

Determination of Balances of Non-Current Assets

Non-Current Assets

Land &

Property

(£'000)

Plant &

Equipment

(£'000)

Investment

Property (£'000)

Amounts as per trial balance 150000 148000 28000

Accumulated Depreciation -32400

Current Depreciation -5937.5 -17340

Balance carried forward 144062.5 98260 28000

Closing Stock Amount to be transferred to Statement of Financial Position

Closing Inventory 25000

Less: Cost of Damaged Goods -2470

Add: Net Realisable Value 2170

Amount transferred to Balance Sheet 24700

(d) Type of information that cash flow statement provides in comparison to P&L and

statement of financial position:

Cash flow, P&L and Balance sheet are major financial statements of business which

individually and aggregately shows different financial aspects of business. All these statements

have different features and use in business context. A cash-flow statements consists of all the

cash expenditures and receipts of business during a particular period without considering accrual

of transactions. While income-statement or Profit or loss account revels the business gross and

net profit position over a particular time-period. On other hand, statement of financial-position

presents balance of different-different assets and liabilities as on specific period. P & L account

and balance sheet are prepared on the basis of accrual concept while cash-flow statement is

prepared by accountant based on cash concept. There is lack of substance found in interpretation

of cash flow (Liu, 2013).

9

Non-Current Assets

Land &

Property

(£'000)

Plant &

Equipment

(£'000)

Investment

Property (£'000)

Amounts as per trial balance 150000 148000 28000

Accumulated Depreciation -32400

Current Depreciation -5937.5 -17340

Balance carried forward 144062.5 98260 28000

Closing Stock Amount to be transferred to Statement of Financial Position

Closing Inventory 25000

Less: Cost of Damaged Goods -2470

Add: Net Realisable Value 2170

Amount transferred to Balance Sheet 24700

(d) Type of information that cash flow statement provides in comparison to P&L and

statement of financial position:

Cash flow, P&L and Balance sheet are major financial statements of business which

individually and aggregately shows different financial aspects of business. All these statements

have different features and use in business context. A cash-flow statements consists of all the

cash expenditures and receipts of business during a particular period without considering accrual

of transactions. While income-statement or Profit or loss account revels the business gross and

net profit position over a particular time-period. On other hand, statement of financial-position

presents balance of different-different assets and liabilities as on specific period. P & L account

and balance sheet are prepared on the basis of accrual concept while cash-flow statement is

prepared by accountant based on cash concept. There is lack of substance found in interpretation

of cash flow (Liu, 2013).

9

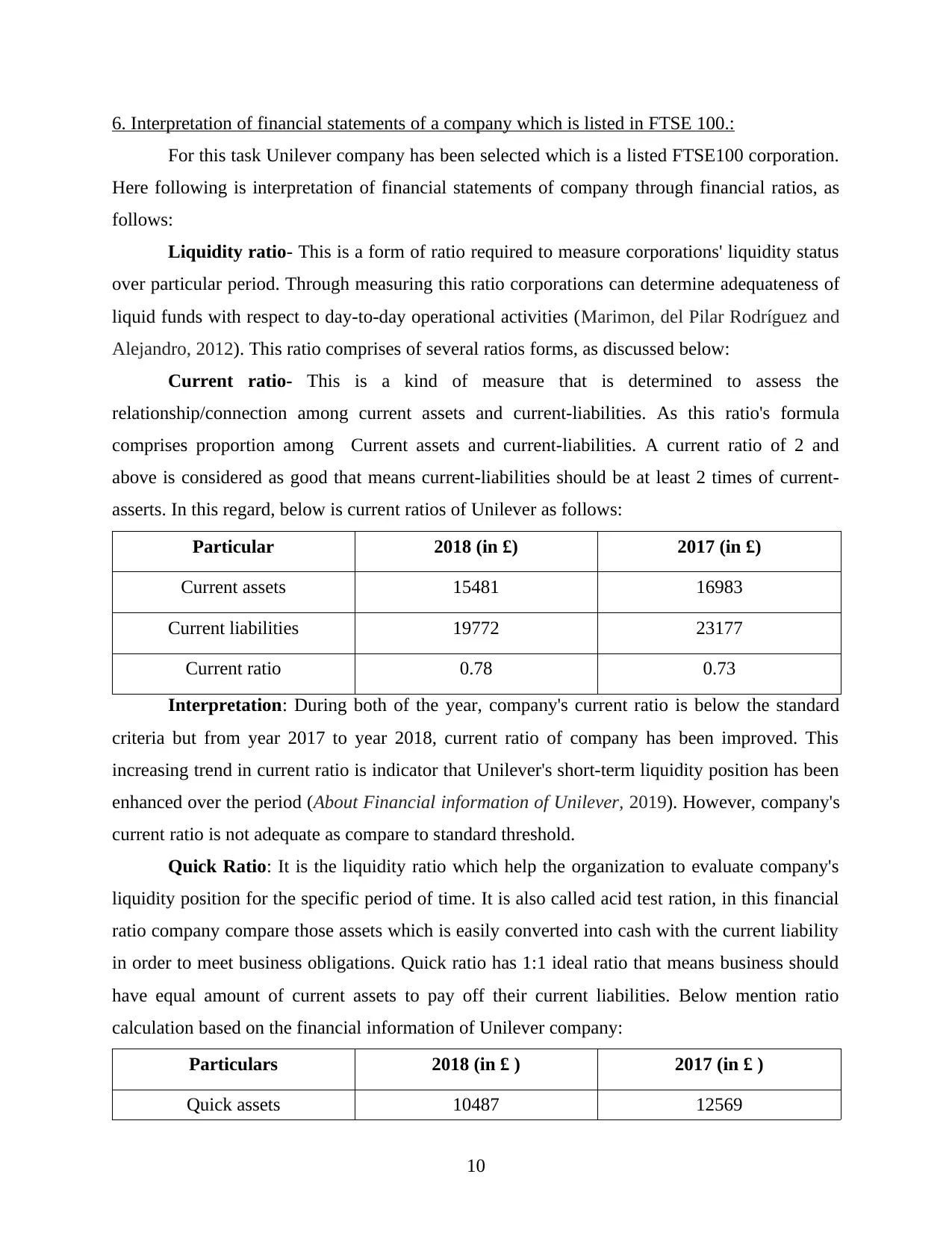

6. Interpretation of financial statements of a company which is listed in FTSE 100.:

For this task Unilever company has been selected which is a listed FTSE100 corporation.

Here following is interpretation of financial statements of company through financial ratios, as

follows:

Liquidity ratio- This is a form of ratio required to measure corporations' liquidity status

over particular period. Through measuring this ratio corporations can determine adequateness of

liquid funds with respect to day-to-day operational activities (Marimon, del Pilar Rodríguez and

Alejandro, 2012). This ratio comprises of several ratios forms, as discussed below:

Current ratio- This is a kind of measure that is determined to assess the

relationship/connection among current assets and current-liabilities. As this ratio's formula

comprises proportion among Current assets and current-liabilities. A current ratio of 2 and

above is considered as good that means current-liabilities should be at least 2 times of current-

asserts. In this regard, below is current ratios of Unilever as follows:

Particular 2018 (in £) 2017 (in £)

Current assets 15481 16983

Current liabilities 19772 23177

Current ratio 0.78 0.73

Interpretation: During both of the year, company's current ratio is below the standard

criteria but from year 2017 to year 2018, current ratio of company has been improved. This

increasing trend in current ratio is indicator that Unilever's short-term liquidity position has been

enhanced over the period (About Financial information of Unilever, 2019). However, company's

current ratio is not adequate as compare to standard threshold.

Quick Ratio: It is the liquidity ratio which help the organization to evaluate company's

liquidity position for the specific period of time. It is also called acid test ration, in this financial

ratio company compare those assets which is easily converted into cash with the current liability

in order to meet business obligations. Quick ratio has 1:1 ideal ratio that means business should

have equal amount of current assets to pay off their current liabilities. Below mention ratio

calculation based on the financial information of Unilever company:

Particulars 2018 (in £ ) 2017 (in £ )

Quick assets 10487 12569

10

For this task Unilever company has been selected which is a listed FTSE100 corporation.

Here following is interpretation of financial statements of company through financial ratios, as

follows:

Liquidity ratio- This is a form of ratio required to measure corporations' liquidity status

over particular period. Through measuring this ratio corporations can determine adequateness of

liquid funds with respect to day-to-day operational activities (Marimon, del Pilar Rodríguez and

Alejandro, 2012). This ratio comprises of several ratios forms, as discussed below:

Current ratio- This is a kind of measure that is determined to assess the

relationship/connection among current assets and current-liabilities. As this ratio's formula

comprises proportion among Current assets and current-liabilities. A current ratio of 2 and

above is considered as good that means current-liabilities should be at least 2 times of current-

asserts. In this regard, below is current ratios of Unilever as follows:

Particular 2018 (in £) 2017 (in £)

Current assets 15481 16983

Current liabilities 19772 23177

Current ratio 0.78 0.73

Interpretation: During both of the year, company's current ratio is below the standard

criteria but from year 2017 to year 2018, current ratio of company has been improved. This

increasing trend in current ratio is indicator that Unilever's short-term liquidity position has been

enhanced over the period (About Financial information of Unilever, 2019). However, company's

current ratio is not adequate as compare to standard threshold.

Quick Ratio: It is the liquidity ratio which help the organization to evaluate company's

liquidity position for the specific period of time. It is also called acid test ration, in this financial

ratio company compare those assets which is easily converted into cash with the current liability

in order to meet business obligations. Quick ratio has 1:1 ideal ratio that means business should

have equal amount of current assets to pay off their current liabilities. Below mention ratio

calculation based on the financial information of Unilever company:

Particulars 2018 (in £ ) 2017 (in £ )

Quick assets 10487 12569

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.