Accounting and Financial Reporting: University Report Analysis

VerifiedAdded on 2023/01/11

|8

|464

|90

Report

AI Summary

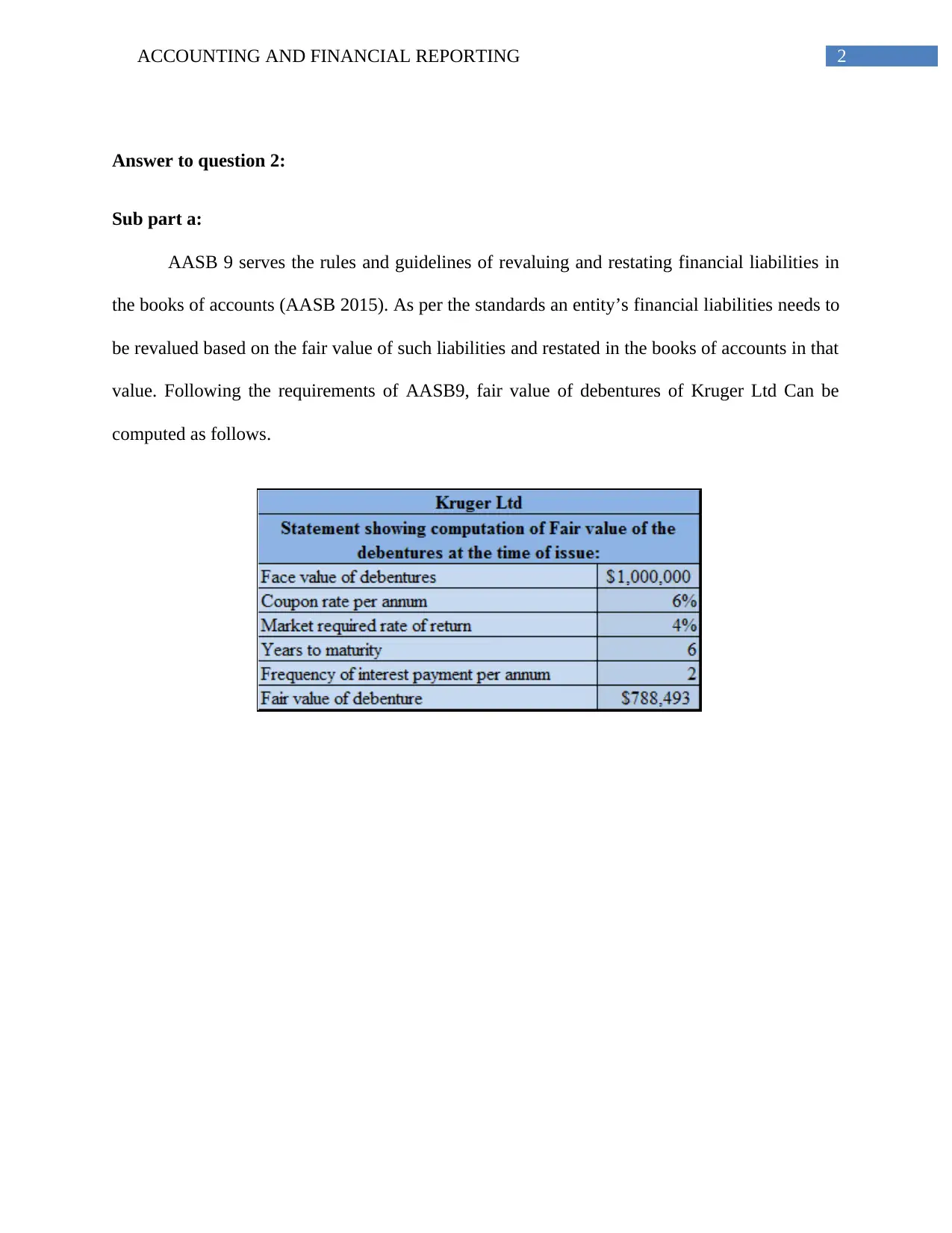

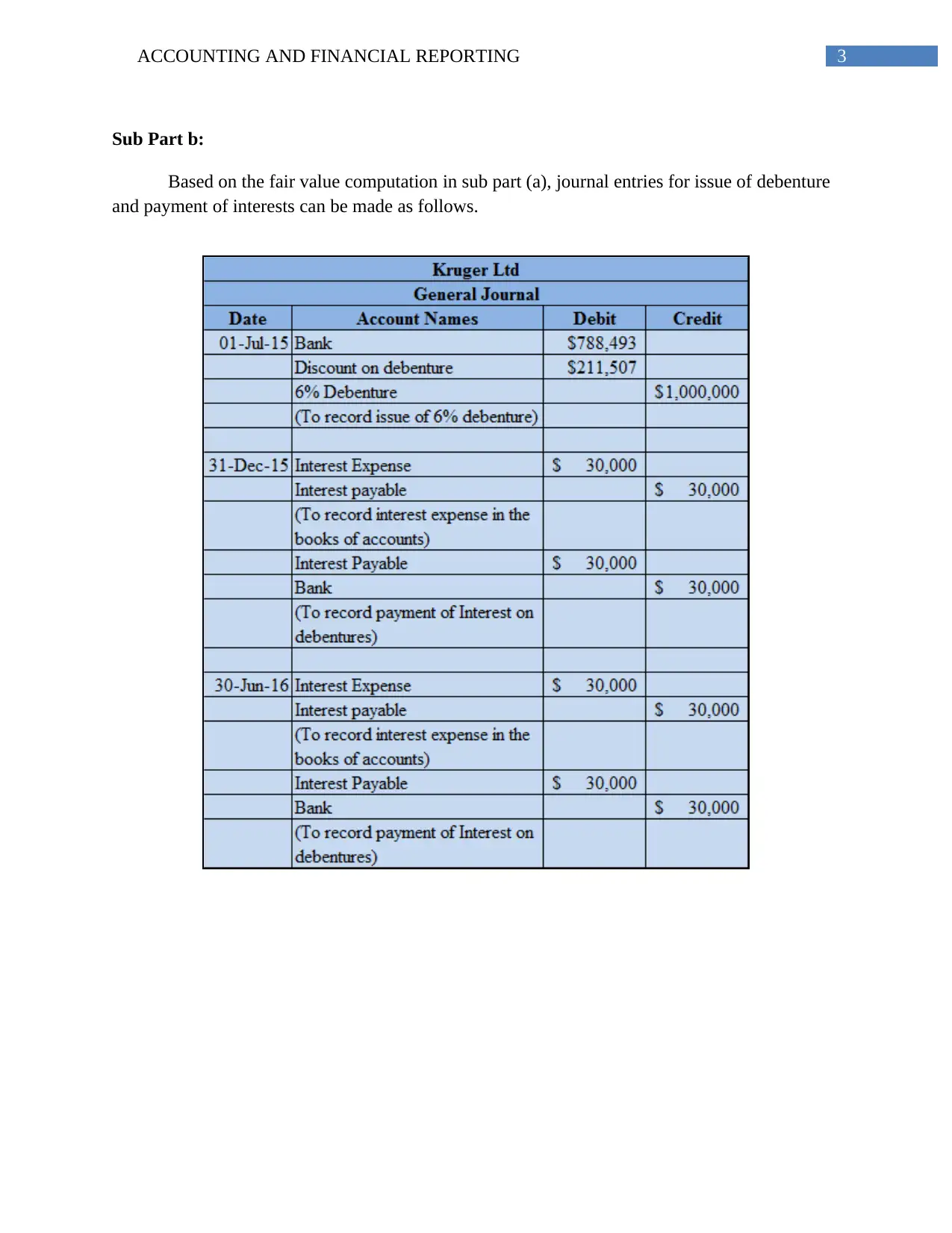

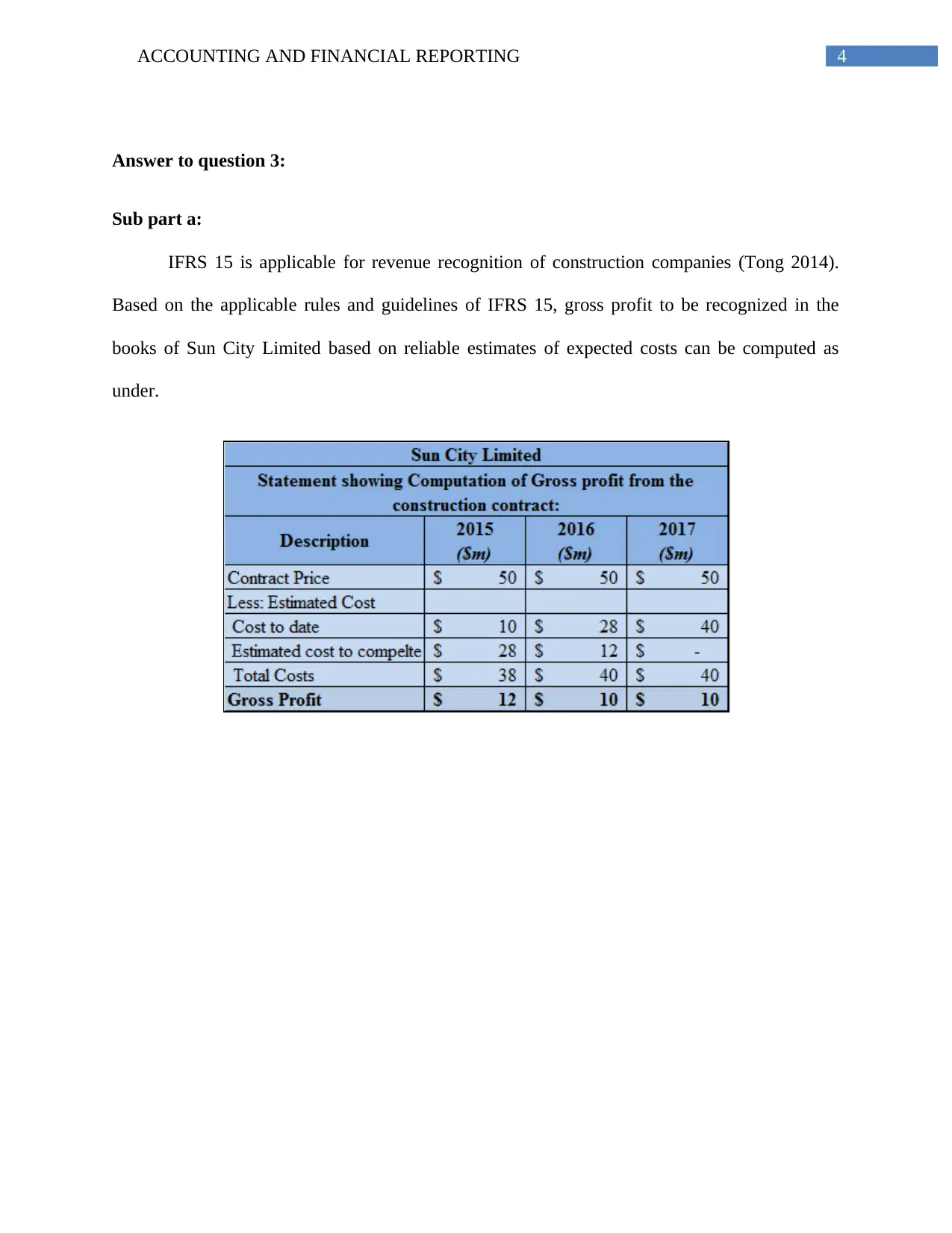

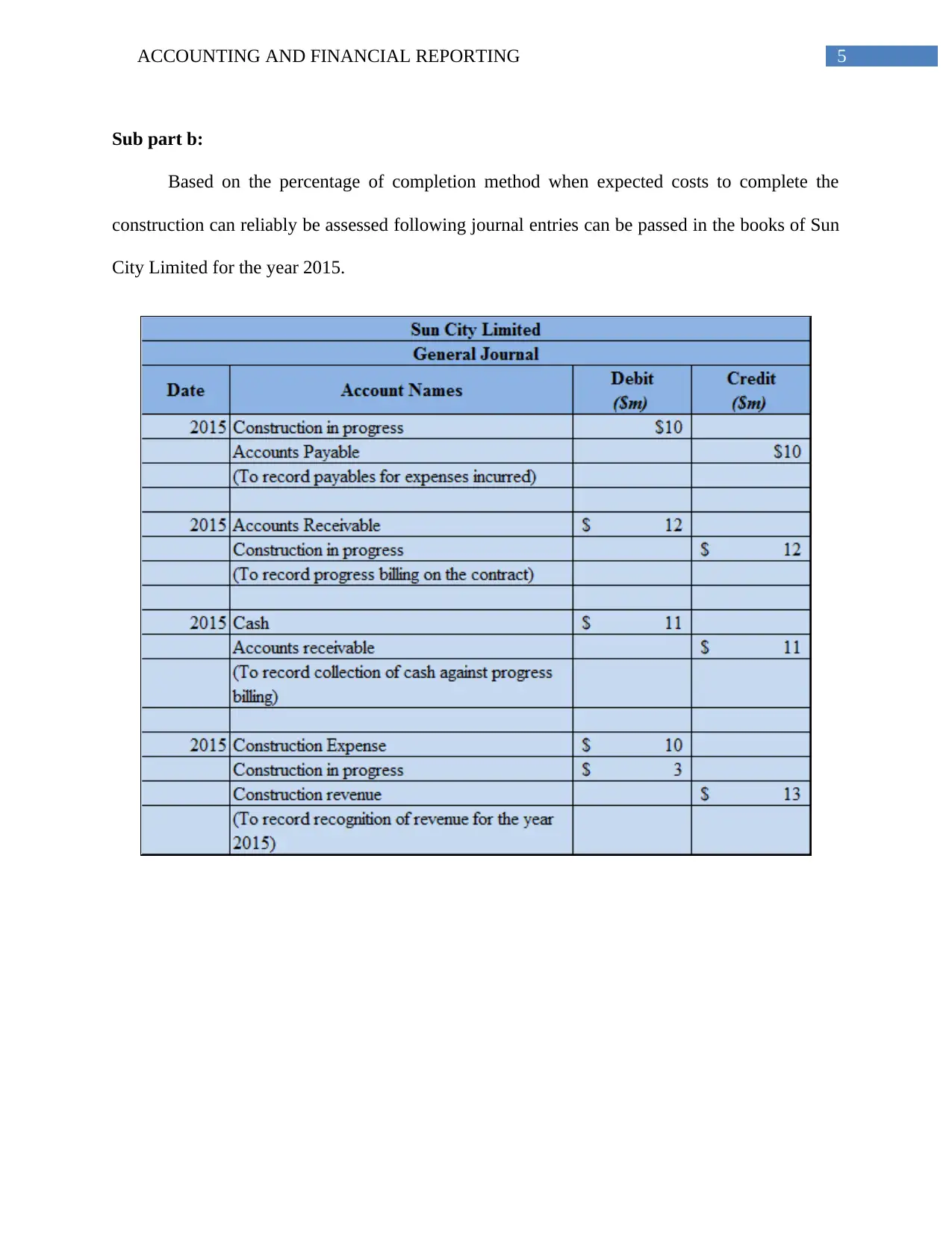

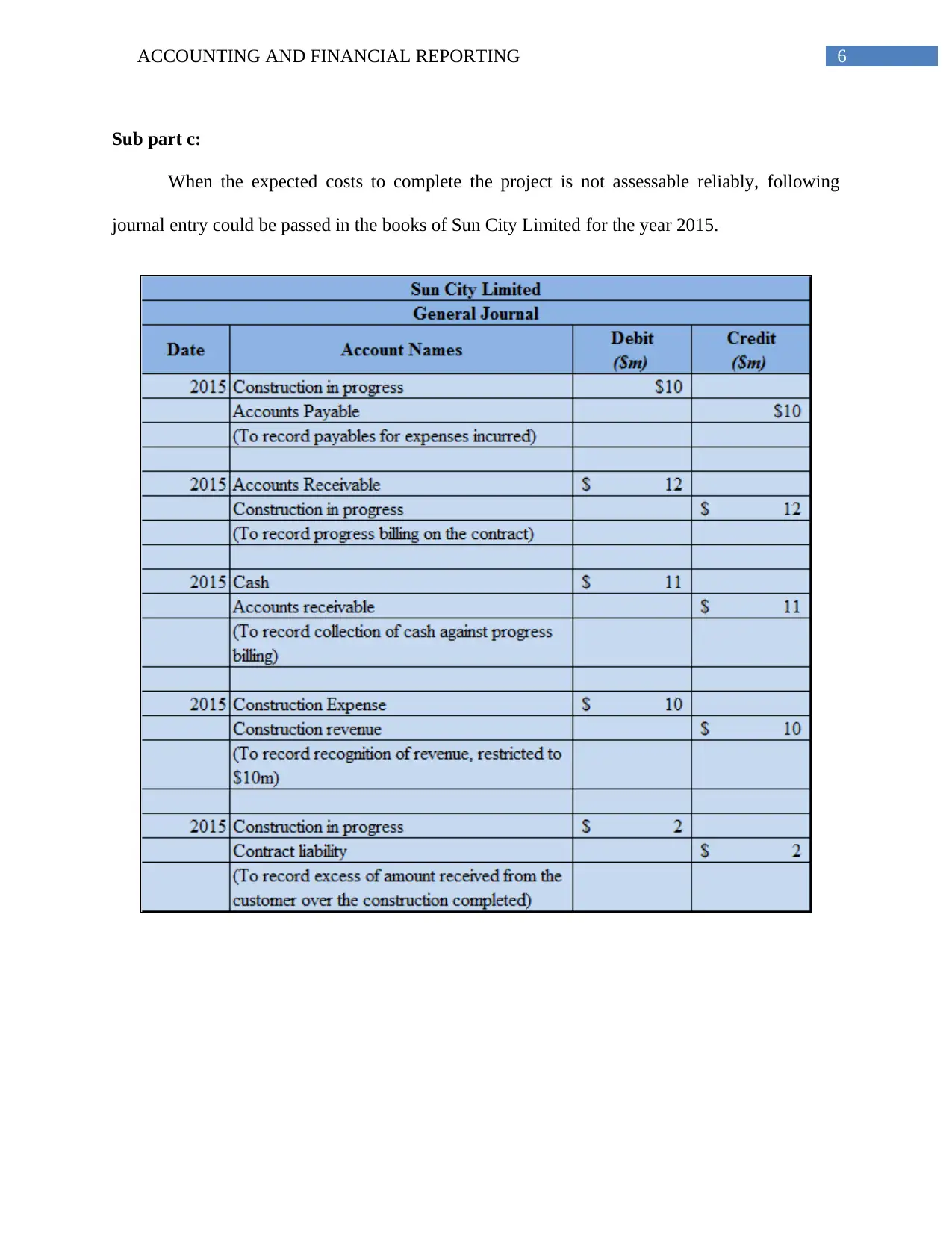

This report presents a detailed analysis of accounting and financial reporting principles, focusing on specific standards and their applications. The assignment addresses key topics such as the revaluation of financial liabilities under AASB 9, including the calculation of fair value for debentures and the corresponding journal entries for their issuance and interest payments. Additionally, the report examines revenue recognition in construction companies according to IFRS 15, detailing the calculation of gross profit using the percentage of completion method and the relevant journal entries. It also considers scenarios where the expected costs to complete a project cannot be reliably assessed. The report includes references to relevant accounting standards and academic sources.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.