Company and Financial Reporting: Australian Context Analysis

VerifiedAdded on 2020/11/23

|9

|2423

|75

Report

AI Summary

This report provides a detailed analysis of financial reporting, particularly focusing on the Australian Accounting Standards Board (AASB) 15, which governs revenue recognition from contracts with customers. The report explains the regulatory requirements and standard-setting within the Australian context, using National Australian Bank Limited (NAB) as a case study. It outlines the key aspects of AASB 15, including the five-step revenue recognition model, disaggregation of revenue, and contract balances. The report discusses the potential impacts of AASB 15 on NAB, including changes to revenue recognition, and provides an investor's perspective on evaluating the bank's financial performance. The report also examines the implications of the new standard across various areas of the business, such as systems, internal controls, business operations, tax, HR, and investor relations, while concluding that AASB 15 has worked effectively regarding to present financial information of bank.

Company

And

Financial Reporting

And

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

PART B............................................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

PART B............................................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION

Financial reporting reflects the performance to the public and the management. Financial

reports of company has been provided financial information about how they are performing in

any quarter of the year (Noronha and et.al, 2013) . Most of the reports of the company has been

prepared on a quarterly and annual basis. Through these reports management can take effective

decision as well as prepare strategy for company to present data in the report. The objective of

the report to explain the regulatory requirements and standard setting of financial reporting in the

Australian context. To understand the concept national Australian bank limited which is listed

into ASX limited as public bank. In the report consist of revenue recognition and measurement

according to AASB 15. Apart from discuss about potential impact to follow AASB 15 in

National Australian bank limited.

PART A

1) The new revenue standard (AASB 15 Revenues from contracts with customers)

follows by each industry and every business from 1 January 2018. The new standard has been

designed to trading with customer contracts and involve business models, involve contracts that

bundle goods and services, contingency pricing arrangements, goods or services that are

delivered on time, licensing agreements and other complex arrangements. The particular

standards has been affected to individual companies in big way because changes can be

addressed. There are required to AASB 15 to disclose objectives, an entity must disclose

sufficient information to modify users of financial statement to understand the nature, amount,

uncertainty and timing of revenues and cash flows origin from contracts with customers.

The new standard has been introduced because Financial accounting standards board

(FASB) received many feedbacks regarding to revenue recognition guidance was fragmented at

best and confusing at worst. So as responses of feedback they were issued AASB 15 for revenues

with customers. To recognise revenues firstly identify of contract then combination of contract as

well as modify contract in appropriate manner. It further identify performance obligation in

reference to promise in contract with customers and different between goods or services. The

objective to disclose requirements due to sufficient information to alter users of financial

statements in order to understand cash flow, uncertainty, nature, amount and timing (Zeff, 2013)

. There are identified revenue recognition as per AASB 15 -

1

Financial reporting reflects the performance to the public and the management. Financial

reports of company has been provided financial information about how they are performing in

any quarter of the year (Noronha and et.al, 2013) . Most of the reports of the company has been

prepared on a quarterly and annual basis. Through these reports management can take effective

decision as well as prepare strategy for company to present data in the report. The objective of

the report to explain the regulatory requirements and standard setting of financial reporting in the

Australian context. To understand the concept national Australian bank limited which is listed

into ASX limited as public bank. In the report consist of revenue recognition and measurement

according to AASB 15. Apart from discuss about potential impact to follow AASB 15 in

National Australian bank limited.

PART A

1) The new revenue standard (AASB 15 Revenues from contracts with customers)

follows by each industry and every business from 1 January 2018. The new standard has been

designed to trading with customer contracts and involve business models, involve contracts that

bundle goods and services, contingency pricing arrangements, goods or services that are

delivered on time, licensing agreements and other complex arrangements. The particular

standards has been affected to individual companies in big way because changes can be

addressed. There are required to AASB 15 to disclose objectives, an entity must disclose

sufficient information to modify users of financial statement to understand the nature, amount,

uncertainty and timing of revenues and cash flows origin from contracts with customers.

The new standard has been introduced because Financial accounting standards board

(FASB) received many feedbacks regarding to revenue recognition guidance was fragmented at

best and confusing at worst. So as responses of feedback they were issued AASB 15 for revenues

with customers. To recognise revenues firstly identify of contract then combination of contract as

well as modify contract in appropriate manner. It further identify performance obligation in

reference to promise in contract with customers and different between goods or services. The

objective to disclose requirements due to sufficient information to alter users of financial

statements in order to understand cash flow, uncertainty, nature, amount and timing (Zeff, 2013)

. There are identified revenue recognition as per AASB 15 -

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contracts with Customer – There is need to revenue recognition because all amounts

related to income statement which have been disclosed to preparing report unless those

amounts are presented separately in the statement of comprehensive income as per new

standards. (1) The revenue has been recognised from contracts with customers, which the

entity shall disclose separately from its other sources of revenues. (2) To know

impairment loss need to analysis revenues on the basis of receivables or contract assets

origin. These are generated from different customers entity which can recognised

separately from other contracts.

Disaggregation of Revenue – (1) Through an entity identified revenues which is related

to contracts with customer into divided that depict bout the nature, amount, timing and

uncertainty of revenues and there are cash flow affect by economic factors. An entity

shall can follow the guidance in particular paragraphs and there is categorised to use to

disaggregation revenue. (2) It further an entity can disclose all sufficient information in

front of users of financial statement because with the help of these information they can

understand relationship between the disclosure of disaggregated revenue. All specific

revenue information is disclosed for each reportable segment (Tanyi and Smith, 2014) .

Contract balances – There are revenue recognised in the reporting period because it has

been included into contract liability balance at the starting of the period. As well as the

revenue recognised in the reporting time period because performance obligation need to

satisfied on the basis of previous period.

As per the AASB 15 need to require of revenues recognition in order to contract with

customers, disaggregation of revenues as well as for contract balances.

(2) Measurement of revenues means all types revenues has been measured on fair value

to receivables of consideration. The particular amount arisen on a transaction which is usually

determined through agreement between the entity and buyer or user of the assets. In the new

comprehensive framework of AASB 15 apply five steps revenue recognition model which can

help to recognise revenues as well as in measurement. These are -

2

related to income statement which have been disclosed to preparing report unless those

amounts are presented separately in the statement of comprehensive income as per new

standards. (1) The revenue has been recognised from contracts with customers, which the

entity shall disclose separately from its other sources of revenues. (2) To know

impairment loss need to analysis revenues on the basis of receivables or contract assets

origin. These are generated from different customers entity which can recognised

separately from other contracts.

Disaggregation of Revenue – (1) Through an entity identified revenues which is related

to contracts with customer into divided that depict bout the nature, amount, timing and

uncertainty of revenues and there are cash flow affect by economic factors. An entity

shall can follow the guidance in particular paragraphs and there is categorised to use to

disaggregation revenue. (2) It further an entity can disclose all sufficient information in

front of users of financial statement because with the help of these information they can

understand relationship between the disclosure of disaggregated revenue. All specific

revenue information is disclosed for each reportable segment (Tanyi and Smith, 2014) .

Contract balances – There are revenue recognised in the reporting period because it has

been included into contract liability balance at the starting of the period. As well as the

revenue recognised in the reporting time period because performance obligation need to

satisfied on the basis of previous period.

As per the AASB 15 need to require of revenues recognition in order to contract with

customers, disaggregation of revenues as well as for contract balances.

(2) Measurement of revenues means all types revenues has been measured on fair value

to receivables of consideration. The particular amount arisen on a transaction which is usually

determined through agreement between the entity and buyer or user of the assets. In the new

comprehensive framework of AASB 15 apply five steps revenue recognition model which can

help to recognise revenues as well as in measurement. These are -

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

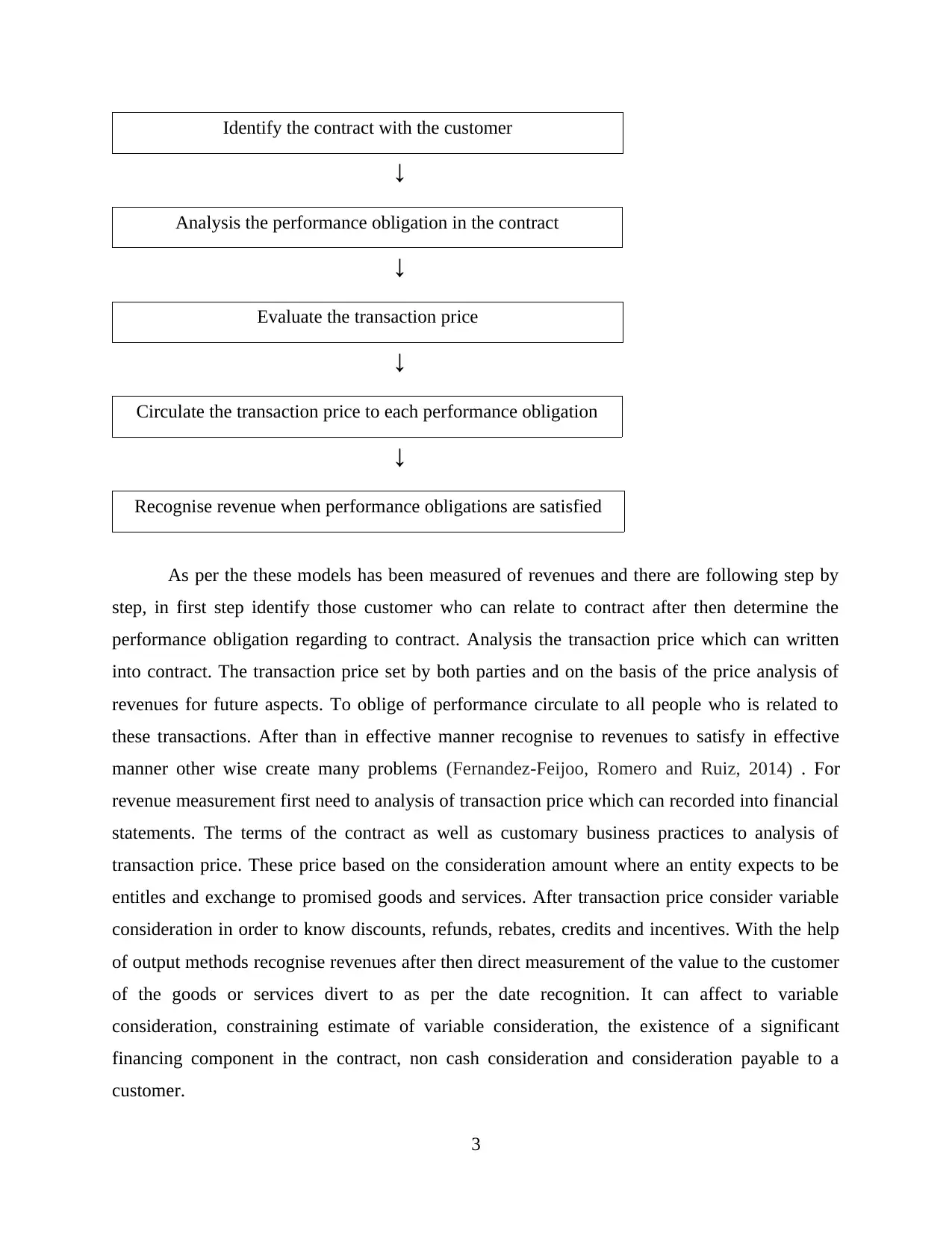

Identify the contract with the customer

↓

Analysis the performance obligation in the contract

↓

Evaluate the transaction price

↓

Circulate the transaction price to each performance obligation

↓

Recognise revenue when performance obligations are satisfied

As per the these models has been measured of revenues and there are following step by

step, in first step identify those customer who can relate to contract after then determine the

performance obligation regarding to contract. Analysis the transaction price which can written

into contract. The transaction price set by both parties and on the basis of the price analysis of

revenues for future aspects. To oblige of performance circulate to all people who is related to

these transactions. After than in effective manner recognise to revenues to satisfy in effective

manner other wise create many problems (Fernandez-Feijoo, Romero and Ruiz, 2014) . For

revenue measurement first need to analysis of transaction price which can recorded into financial

statements. The terms of the contract as well as customary business practices to analysis of

transaction price. These price based on the consideration amount where an entity expects to be

entitles and exchange to promised goods and services. After transaction price consider variable

consideration in order to know discounts, refunds, rebates, credits and incentives. With the help

of output methods recognise revenues after then direct measurement of the value to the customer

of the goods or services divert to as per the date recognition. It can affect to variable

consideration, constraining estimate of variable consideration, the existence of a significant

financing component in the contract, non cash consideration and consideration payable to a

customer.

3

↓

Analysis the performance obligation in the contract

↓

Evaluate the transaction price

↓

Circulate the transaction price to each performance obligation

↓

Recognise revenue when performance obligations are satisfied

As per the these models has been measured of revenues and there are following step by

step, in first step identify those customer who can relate to contract after then determine the

performance obligation regarding to contract. Analysis the transaction price which can written

into contract. The transaction price set by both parties and on the basis of the price analysis of

revenues for future aspects. To oblige of performance circulate to all people who is related to

these transactions. After than in effective manner recognise to revenues to satisfy in effective

manner other wise create many problems (Fernandez-Feijoo, Romero and Ruiz, 2014) . For

revenue measurement first need to analysis of transaction price which can recorded into financial

statements. The terms of the contract as well as customary business practices to analysis of

transaction price. These price based on the consideration amount where an entity expects to be

entitles and exchange to promised goods and services. After transaction price consider variable

consideration in order to know discounts, refunds, rebates, credits and incentives. With the help

of output methods recognise revenues after then direct measurement of the value to the customer

of the goods or services divert to as per the date recognition. It can affect to variable

consideration, constraining estimate of variable consideration, the existence of a significant

financing component in the contract, non cash consideration and consideration payable to a

customer.

3

PART B

The particular new standard is designed for industry and all enterprises have to apply the

same model and there are not provided specific guidance regarding to standards in reference to

any company. However, it is based on the nature of contracts which is different for all industries

in specific manner to these model might have more significant impacts as per the industries

rather than to others. In reference to annual report of national Australian bank limited, AASB 15

which name is “Revenues from contracts with customers” has been based on five step model and

apply on the bank to recognise revenues and introduce the concept of revenues measurement to

provide satisfaction through obligation. For prepare of financial report of the bank that time can

not applied because it can not effective (Huang, Tsaih and Yu, 2014) . The future impact of the

particular standard is still being determined and it can not applicable until 1 October 2018.

On the basis of annual report of 2018, group of bank followed AASB 15 from 1 October

2018. Following commission considers as basic revenue stream which can impact by the

transition to AASB 15 and the group of the bank analysis that it has no substantive ongoing

performance obligation in order to trailing commission and therefore is need to forecast the

present value of trailing commission it is entitled to gather and identify that forecast as a contract

asset. In the contact of asset has been adjusted to retained earnings which are not material to the

group's financial statements. There are not recognised material transition adjustments were

analysed.

As per the investor perspectives evaluate the financial performance and financial position

of the bank which can help to investors to determine performance of company. The bank adopted

on 1 October 2018 AASB 15 after that analysis all contracts with customers and statement of

comprehensive income present net profit for the year from continuing operations which is $5219

in 2018 as compare to 2017 in $4975. So after implementation there are not coming effective

effect. The particular standard after implication impact on the bank as timing and amount basis to

identified revenues. The particular changes has been showed implications in numerous number

to across the area in the business. There are point out some particular areas which is related to

implement business in effective manner -

Systems and Processes – After apply the standard improve system to arrange financial

information and expand to reports as per requirement in additional way.

4

The particular new standard is designed for industry and all enterprises have to apply the

same model and there are not provided specific guidance regarding to standards in reference to

any company. However, it is based on the nature of contracts which is different for all industries

in specific manner to these model might have more significant impacts as per the industries

rather than to others. In reference to annual report of national Australian bank limited, AASB 15

which name is “Revenues from contracts with customers” has been based on five step model and

apply on the bank to recognise revenues and introduce the concept of revenues measurement to

provide satisfaction through obligation. For prepare of financial report of the bank that time can

not applied because it can not effective (Huang, Tsaih and Yu, 2014) . The future impact of the

particular standard is still being determined and it can not applicable until 1 October 2018.

On the basis of annual report of 2018, group of bank followed AASB 15 from 1 October

2018. Following commission considers as basic revenue stream which can impact by the

transition to AASB 15 and the group of the bank analysis that it has no substantive ongoing

performance obligation in order to trailing commission and therefore is need to forecast the

present value of trailing commission it is entitled to gather and identify that forecast as a contract

asset. In the contact of asset has been adjusted to retained earnings which are not material to the

group's financial statements. There are not recognised material transition adjustments were

analysed.

As per the investor perspectives evaluate the financial performance and financial position

of the bank which can help to investors to determine performance of company. The bank adopted

on 1 October 2018 AASB 15 after that analysis all contracts with customers and statement of

comprehensive income present net profit for the year from continuing operations which is $5219

in 2018 as compare to 2017 in $4975. So after implementation there are not coming effective

effect. The particular standard after implication impact on the bank as timing and amount basis to

identified revenues. The particular changes has been showed implications in numerous number

to across the area in the business. There are point out some particular areas which is related to

implement business in effective manner -

Systems and Processes – After apply the standard improve system to arrange financial

information and expand to reports as per requirement in additional way.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Internal control – It will influence to end to end process to modify principles which is

related to financial information (Serafeim,2015) .

Business Operations and contracts – There is modifying to contracting procedure as well

as legal terms that will impact on potential deals and transactions.

Tax – There are considering timing of revenue recognition that can affect to cash tax

paid. The tax has been showed how much profit earn by bank after on particular revenue

apply tax at fixed rate after that Remaining amount known as net profit of the year

(Trigo, Belfo and Estébanez, 2014).

HR and remuneration structure – The compensation and short term incentive plans and

structure. There are formulating and apply efficient communication to produce plans to

affected business and stakeholders. There are developing and delivering training and

financial tools to understand the standards in efficient manner.

Investor Relations – When bank has been presented reports in effective manner so they

are attracting from company and take interest to invest in company. To provide guidance

use key performance indicator which can show financial and non financial indicator. It

can fulfil the expectation of after adaptation of particular standard in impressive manner.

To analysis financial performance calculate financial ratio of the bank which can provide all

appropriate information and help to analysis potential impact of a bank, which is -

Profitably Ratio – The particular ratio has been classified in financial metrics which is

used to analysis of capability of business to gain much more earning and relative their revenues,

operating cost, balance sheet assets and shareholders equity over time to apply data from a

particular time period (Cheng and et.al, 2014) . There are calculate ratio of bank -

Net profit margin = Net profit / sales *100

5288 / 8986*100 = 58.84

After apply the new standard get much more benefits and they can take all appropriate

information which is related to financial performance. In 2019, annual report impact in positive

way and create good relation with investors and build up effective income statement where

present information in appropriate manner. From financial report it is getting that bank has been

fulfil their objectives and get sufficient amount of profitability. After apply the new standard the

bank has been use five model approach to show all transaction fees and show contacts with

5

related to financial information (Serafeim,2015) .

Business Operations and contracts – There is modifying to contracting procedure as well

as legal terms that will impact on potential deals and transactions.

Tax – There are considering timing of revenue recognition that can affect to cash tax

paid. The tax has been showed how much profit earn by bank after on particular revenue

apply tax at fixed rate after that Remaining amount known as net profit of the year

(Trigo, Belfo and Estébanez, 2014).

HR and remuneration structure – The compensation and short term incentive plans and

structure. There are formulating and apply efficient communication to produce plans to

affected business and stakeholders. There are developing and delivering training and

financial tools to understand the standards in efficient manner.

Investor Relations – When bank has been presented reports in effective manner so they

are attracting from company and take interest to invest in company. To provide guidance

use key performance indicator which can show financial and non financial indicator. It

can fulfil the expectation of after adaptation of particular standard in impressive manner.

To analysis financial performance calculate financial ratio of the bank which can provide all

appropriate information and help to analysis potential impact of a bank, which is -

Profitably Ratio – The particular ratio has been classified in financial metrics which is

used to analysis of capability of business to gain much more earning and relative their revenues,

operating cost, balance sheet assets and shareholders equity over time to apply data from a

particular time period (Cheng and et.al, 2014) . There are calculate ratio of bank -

Net profit margin = Net profit / sales *100

5288 / 8986*100 = 58.84

After apply the new standard get much more benefits and they can take all appropriate

information which is related to financial performance. In 2019, annual report impact in positive

way and create good relation with investors and build up effective income statement where

present information in appropriate manner. From financial report it is getting that bank has been

fulfil their objectives and get sufficient amount of profitability. After apply the new standard the

bank has been use five model approach to show all transaction fees and show contacts with

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

customers to their investors to attract for investment purpose and the standard make financial

performance strong.

CONCLUSION

As per the above report it has been concluded that the new standard AASB 15 has been

worked in effective manner regarding to present financial information of bank. The standard to

apply on the financial statement that to establish the principles that an entity shall apply to report

useful information to users of financial statements about the nature, amount, timing and

uncertainty of revenues and cash flow arising to tackle different types of customer. After

implication of particular standard on the company it can show good effect and help to shoe

financial information in effective manner. Readers easily get all appropriate information in

reference to revenue recognition and measurement.

6

performance strong.

CONCLUSION

As per the above report it has been concluded that the new standard AASB 15 has been

worked in effective manner regarding to present financial information of bank. The standard to

apply on the financial statement that to establish the principles that an entity shall apply to report

useful information to users of financial statements about the nature, amount, timing and

uncertainty of revenues and cash flow arising to tackle different types of customer. After

implication of particular standard on the company it can show good effect and help to shoe

financial information in effective manner. Readers easily get all appropriate information in

reference to revenue recognition and measurement.

6

REFERENCES

Books and Journals

Noronha, C. and et.al, 2013. Corporate social responsibility reporting in China: An overview and

comparison with major trends. Corporate Social Responsibility and Environmental

Management. 20(1). pp.29-42.

Zeff, S. A., 2013. The objectives of financial reporting: a historical survey and

analysis. Accounting and Business Research. 43(4). pp.262-327.

Tanyi, P. N. and Smith, D. B., 2014. Busyness, expertise, and financial reporting quality of audit

committee chairs and financial experts. Auditing: A Journal of Practice & Theory.

34(2). pp.59-89.

Fernandez-Feijoo, B., Romero, S. and Ruiz, S., 2014. Commitment to corporate social

responsibility measured through global reporting initiative reporting: Factors affecting

the behavior of companies. Journal of Cleaner Production. 81. pp.244-254.

Huang, S. Y., Tsaih, R. H. and Yu, F., 2014. Topological pattern discovery and feature extraction

for fraudulent financial reporting. Expert systems with applications. 41(9). pp.4360-

4372.

Serafeim, G., 2015. Integrated reporting and investor clientele. Journal of Applied Corporate

Finance. 27(2). pp.34-51.

Cheng, M. and et.al, 2014. The international integrated reporting framework: key issues and

future research opportunities. Journal of International Financial Management &

Accounting. 25(1). pp.90-119.

Trigo, A., Belfo, F. and Estébanez, R. P., 2014. Accounting information systems: The challenge

of the real-time reporting. Procedia Technology. 16. pp.118-127.

Online

National Australian bank limited. 2018. [Online]. Available through:

<https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/2018-

annual-financial-report.pdf.

National Australian bank limited. 2017. [Online]. Available through:

<https://capital.nab.com.au/docs/NAB-2017-annual-financial-report.pdf>

7

Books and Journals

Noronha, C. and et.al, 2013. Corporate social responsibility reporting in China: An overview and

comparison with major trends. Corporate Social Responsibility and Environmental

Management. 20(1). pp.29-42.

Zeff, S. A., 2013. The objectives of financial reporting: a historical survey and

analysis. Accounting and Business Research. 43(4). pp.262-327.

Tanyi, P. N. and Smith, D. B., 2014. Busyness, expertise, and financial reporting quality of audit

committee chairs and financial experts. Auditing: A Journal of Practice & Theory.

34(2). pp.59-89.

Fernandez-Feijoo, B., Romero, S. and Ruiz, S., 2014. Commitment to corporate social

responsibility measured through global reporting initiative reporting: Factors affecting

the behavior of companies. Journal of Cleaner Production. 81. pp.244-254.

Huang, S. Y., Tsaih, R. H. and Yu, F., 2014. Topological pattern discovery and feature extraction

for fraudulent financial reporting. Expert systems with applications. 41(9). pp.4360-

4372.

Serafeim, G., 2015. Integrated reporting and investor clientele. Journal of Applied Corporate

Finance. 27(2). pp.34-51.

Cheng, M. and et.al, 2014. The international integrated reporting framework: key issues and

future research opportunities. Journal of International Financial Management &

Accounting. 25(1). pp.90-119.

Trigo, A., Belfo, F. and Estébanez, R. P., 2014. Accounting information systems: The challenge

of the real-time reporting. Procedia Technology. 16. pp.118-127.

Online

National Australian bank limited. 2018. [Online]. Available through:

<https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/2018-

annual-financial-report.pdf.

National Australian bank limited. 2017. [Online]. Available through:

<https://capital.nab.com.au/docs/NAB-2017-annual-financial-report.pdf>

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.