Financial Reporting Analysis: AASB 15, IFRS 15, and Exposure Draft

VerifiedAdded on 2023/01/18

|12

|3461

|38

Report

AI Summary

This report provides a detailed analysis of the accounting standards IFRS 15 and AASB 15, focusing on revenue recognition and the impact of the new standards on financial reporting. The report examines the key issues discussed in a news article by KPMG Australia, including the transition approaches and disclosure requirements for companies. It applies relevant theoretical frameworks, such as the conceptual accounting framework, to evaluate these issues. The report also analyzes an exposure draft related to onerous contracts and the application of public interest theory to explain the behavior of regulators. Furthermore, it outlines the views presented in comment letters regarding the exposure draft, highlighting areas of agreement and disagreement. The analysis covers the implications of the standards, transition approaches, and the five-step model for revenue recognition, providing a comprehensive overview of the changes in financial reporting. The report concludes by summarizing the key findings and emphasizing the importance of understanding and implementing these new standards.

1

Current Development and accounting thought

Current Development and accounting thought

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Answer to Question 1

Introduction

This report is being developed for undertaking an analysis of a news article related to the

accounting news for developing a theoretical insight into the key issues discussed within the

article. The overall analysis has been conducted from the perspective of CEO for providing

assistance to understand the key issues discussed to be presented at an upcoming conference. In

this context, the article selected for analysis purpose is entitled as ‘AASB 15: New revenue

disclosures for half year accounts’ published by KPMG Australia. The analysis presented below

has primarily examined the key themes discussed within the article and thereby has applied

relevant theoretical frameworks for detailed evaluation of the issues identified.

Analysis of the Key Issues of the Article

The Accountings standards of IFRS 15, that is, for revenue recognition from contracts

with customers, has been developed by IASB for replacing previous IAS and USGAAP

standards in this respect and to introduce significant changes for accounting of revenues. The

implementation of the new accounting standard of IFRS 15 would have a significant impact on

the accounting and reporting methods used by companies for disclosures regarding revenue

recognition. The new standard has come into effect from January 2018 and has largely impacted

the disclosures patterns in the annual reports of the companies regarding the pattern of revenue

recognition. The Australian companies have to implement AASB 15 in compliance with IFRS 15

and the selected article has analyzed the transitional approaches and the disclosure requirements

of the new standard for the companies. The article has identified and stated three transition

approaches that could be implemented by companies for complying with AASB 15 standard

requirements (Heng & Rinarelli, 2019). These are stated as follows:

Full retrospective: restating comparativeness on the basis of new standard application

Modified retrospective: restating comparativeness using practical expedients

Cumulative: Restating comparativeness

The companies are adopting the use of cumulative approach so that they do not have to re-

assess the impacts of the new standard on their previous financial periods. In this context, as

stated in the article there has also been the development of AASB 134 Interim Financial

Reporting that need to be applied within half year accounts. As per the standard, a reporting

entity needs to disclose explanations regarding the events that have caused changes in the

financial position and description of new accounting policies as per the standard. The transition

approach selected by the company in complying with the new standards need to be disclosed for

depicting the changes in revenue numbers that have been occurred in the balance sheet. The new

accounting policies need to be discussed in comparison with the previous ones for reflecting the

changes that have been introduced in the accounting standard as per the new accounting policies

(KPMG Australia, 2018).

Answer to Question 1

Introduction

This report is being developed for undertaking an analysis of a news article related to the

accounting news for developing a theoretical insight into the key issues discussed within the

article. The overall analysis has been conducted from the perspective of CEO for providing

assistance to understand the key issues discussed to be presented at an upcoming conference. In

this context, the article selected for analysis purpose is entitled as ‘AASB 15: New revenue

disclosures for half year accounts’ published by KPMG Australia. The analysis presented below

has primarily examined the key themes discussed within the article and thereby has applied

relevant theoretical frameworks for detailed evaluation of the issues identified.

Analysis of the Key Issues of the Article

The Accountings standards of IFRS 15, that is, for revenue recognition from contracts

with customers, has been developed by IASB for replacing previous IAS and USGAAP

standards in this respect and to introduce significant changes for accounting of revenues. The

implementation of the new accounting standard of IFRS 15 would have a significant impact on

the accounting and reporting methods used by companies for disclosures regarding revenue

recognition. The new standard has come into effect from January 2018 and has largely impacted

the disclosures patterns in the annual reports of the companies regarding the pattern of revenue

recognition. The Australian companies have to implement AASB 15 in compliance with IFRS 15

and the selected article has analyzed the transitional approaches and the disclosure requirements

of the new standard for the companies. The article has identified and stated three transition

approaches that could be implemented by companies for complying with AASB 15 standard

requirements (Heng & Rinarelli, 2019). These are stated as follows:

Full retrospective: restating comparativeness on the basis of new standard application

Modified retrospective: restating comparativeness using practical expedients

Cumulative: Restating comparativeness

The companies are adopting the use of cumulative approach so that they do not have to re-

assess the impacts of the new standard on their previous financial periods. In this context, as

stated in the article there has also been the development of AASB 134 Interim Financial

Reporting that need to be applied within half year accounts. As per the standard, a reporting

entity needs to disclose explanations regarding the events that have caused changes in the

financial position and description of new accounting policies as per the standard. The transition

approach selected by the company in complying with the new standards need to be disclosed for

depicting the changes in revenue numbers that have been occurred in the balance sheet. The new

accounting policies need to be discussed in comparison with the previous ones for reflecting the

changes that have been introduced in the accounting standard as per the new accounting policies

(KPMG Australia, 2018).

3

The changes in the financial reporting that have been brought by the development of new

standard of AASB 15 are the key issue that is discussed within the given article. The

introduction of new accounting standards would have a huge impact on the financial statements.

In this context, ASIC (Australian Securities Investment Commission) in developing an

understanding of the accounting changes and providing disclosures as per the new accounting

standards to meet all its requirements. The business entities need to gain an understanding of the

changes in the financial reporting system related to recognition, measurement and presentation of

revenue in the financial statements (Heng & Rinarelli, 2019).

Examination of the Key Issues Discussed in the Article by the Application of Relevant

Theories

The key issue emphasized within the selected article is the transition approaches and

disclosure changes that are required by the companies to be followed for meeting the new

standard requirements (Heng & Rinarelli, 2019). The objective of the financial reporting as per

the conceptual accounting theoretical framework is to depict the financial position of a company

to its end-users for guiding them to take economic decisions. The information presented should

be highly useful for determining the capacity of a company to generate future cash flows and

providing returns to the investors. The conceptual accounting framework has provided the

qualitative principles of relevancy, comparability, faithfulness, verifiability, timeliness and

understandability that should be presented within the financial reports developed by companies

for meeting the objective of financial reporting. The theoretical principles provided by the

conceptual accounting framework mainly intend to improve the quality of financial reporting.

The IASB has developed and implemented the conceptual accounting framework within the

financial reporting system to ensure the protection of the interests of the end-users. In this

context, IASB has developed new IFRS 15 standard for improving the quality of financial

reporting as per the conceptual accounting framework theoretical model (Grosu & Socoliuc,

2012).

The new IFRS 15 standard mainly intends to adopt two new approaches of revue

recognition in the financial reporting systems. The first approach is recognition of revenue at a

point in time and the second approach is gradual recognition over time. The IFRS 15 accounting

standard has facilitated the application of a five-step model that will help in determining the

transitional approaches and the disclosures changes that the new companies are required to adopt

as per the IFRS 15 standard adoption. The five-step mold can be used for analysis of the

financial transactions and determining the amount of revenue to be recognized at the time when

they were derived and also at a subsequent time The model consist of the five steps, that is,

identifying the contract with a customer which is followed by identification of its performance

obligations. The next step is determining the transaction price and then allocating the

performance obligations in the contract and lastly recognizing revenue by meeting the

undertakings and provision specified in the contract (Hardidge & Subramanian, 2017).

The changes in the financial reporting that have been brought by the development of new

standard of AASB 15 are the key issue that is discussed within the given article. The

introduction of new accounting standards would have a huge impact on the financial statements.

In this context, ASIC (Australian Securities Investment Commission) in developing an

understanding of the accounting changes and providing disclosures as per the new accounting

standards to meet all its requirements. The business entities need to gain an understanding of the

changes in the financial reporting system related to recognition, measurement and presentation of

revenue in the financial statements (Heng & Rinarelli, 2019).

Examination of the Key Issues Discussed in the Article by the Application of Relevant

Theories

The key issue emphasized within the selected article is the transition approaches and

disclosure changes that are required by the companies to be followed for meeting the new

standard requirements (Heng & Rinarelli, 2019). The objective of the financial reporting as per

the conceptual accounting theoretical framework is to depict the financial position of a company

to its end-users for guiding them to take economic decisions. The information presented should

be highly useful for determining the capacity of a company to generate future cash flows and

providing returns to the investors. The conceptual accounting framework has provided the

qualitative principles of relevancy, comparability, faithfulness, verifiability, timeliness and

understandability that should be presented within the financial reports developed by companies

for meeting the objective of financial reporting. The theoretical principles provided by the

conceptual accounting framework mainly intend to improve the quality of financial reporting.

The IASB has developed and implemented the conceptual accounting framework within the

financial reporting system to ensure the protection of the interests of the end-users. In this

context, IASB has developed new IFRS 15 standard for improving the quality of financial

reporting as per the conceptual accounting framework theoretical model (Grosu & Socoliuc,

2012).

The new IFRS 15 standard mainly intends to adopt two new approaches of revue

recognition in the financial reporting systems. The first approach is recognition of revenue at a

point in time and the second approach is gradual recognition over time. The IFRS 15 accounting

standard has facilitated the application of a five-step model that will help in determining the

transitional approaches and the disclosures changes that the new companies are required to adopt

as per the IFRS 15 standard adoption. The five-step mold can be used for analysis of the

financial transactions and determining the amount of revenue to be recognized at the time when

they were derived and also at a subsequent time The model consist of the five steps, that is,

identifying the contract with a customer which is followed by identification of its performance

obligations. The next step is determining the transaction price and then allocating the

performance obligations in the contract and lastly recognizing revenue by meeting the

undertakings and provision specified in the contract (Hardidge & Subramanian, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

The model will assist the companies to preparation of their financial statements as per the

new standard requirements of IFRS 15. It has stated that entities must recognize revenues at the

time when transfer of goods occurs and expressed by the amount considered or payment that the

entity is likely to receive. The adoption of five step model provided by the new IFRS 15 standard

will help in enhancing the quality of financial reports by improving the comparability of the

financial information disclosed. The optimization of the information in reference to revenue that

was previously not expressed will help in improving the quality of financial reporting. The new

standard has emphasized that the revenue must be recognized by an entity only when there is

probability of realizing future economic benefits by increasing the value of an asset or declining

the liability (Tadros, 2018). Also, the revenue measurement should be done reliably and with

adequate certainty for reflecting the economic reality and protecting the interests of the end-

users. The IASB is also assisting the companies in implementation of IFRS 15 for the first time

and has slowed the adoption of simplification techniques such as commutative effect approach as

discussed in the article for avoiding the re-exposure of the past financial years from the

application of the new standard. In addition to this, IASB and FASB have also lead to the

development of a Joint Transition Resource Group for Revenue Recognition for identification

and discussion of the potential issue that could impact its implementation (Grosu & Socoliuc,

2012).

Conclusion

It can be restated in the end that the article selected has emphasized on the problem of

transition approaches and disclosure requirements that the companies have to implement with the

adoption of IFRS 15 strand. In this context, IASB has developed and presented a five-step model

to guide the companies in the adoption process of IFRS 15 so that they are able to easily identify

and implement changes within their financial statements in compliance with the new standard

requirements.

The model will assist the companies to preparation of their financial statements as per the

new standard requirements of IFRS 15. It has stated that entities must recognize revenues at the

time when transfer of goods occurs and expressed by the amount considered or payment that the

entity is likely to receive. The adoption of five step model provided by the new IFRS 15 standard

will help in enhancing the quality of financial reports by improving the comparability of the

financial information disclosed. The optimization of the information in reference to revenue that

was previously not expressed will help in improving the quality of financial reporting. The new

standard has emphasized that the revenue must be recognized by an entity only when there is

probability of realizing future economic benefits by increasing the value of an asset or declining

the liability (Tadros, 2018). Also, the revenue measurement should be done reliably and with

adequate certainty for reflecting the economic reality and protecting the interests of the end-

users. The IASB is also assisting the companies in implementation of IFRS 15 for the first time

and has slowed the adoption of simplification techniques such as commutative effect approach as

discussed in the article for avoiding the re-exposure of the past financial years from the

application of the new standard. In addition to this, IASB and FASB have also lead to the

development of a Joint Transition Resource Group for Revenue Recognition for identification

and discussion of the potential issue that could impact its implementation (Grosu & Socoliuc,

2012).

Conclusion

It can be restated in the end that the article selected has emphasized on the problem of

transition approaches and disclosure requirements that the companies have to implement with the

adoption of IFRS 15 strand. In this context, IASB has developed and presented a five-step model

to guide the companies in the adoption process of IFRS 15 so that they are able to easily identify

and implement changes within their financial statements in compliance with the new standard

requirements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Answer to Question 2

To answer this question there is need to select exposure draft and any four comment

letters on the exposure draft. There are two international accounting bodies (IASB and FASB)

that are authorized to propose and modify the accounting standard. Exposure draft selected is

maintenance project undertaken by IFRS Foundation to make the proposed amendment in

accounting standard IAS37: Provisions, Contingent Liabilities and Contingent Assets.

Name of Exposure Draft: “ED/2018/2: Onerous Contracts-Cost of Fulfilling a Contract” (IFRS

Foundation, 2018).

Part A: Major issues covered in the exposure draft (Changes introduced or changed by the

Exposure draft)

On the plain reading of Exposure Draft on Onerous Contracts it has been found that the

purpose of this exposure draft is to make amendment in the accounting standard IAS 37. The

main objective of this amendment is to specify the costs that organization or entity must consider

while calculating the “cost of fulfilling” a contract in order to identify whether the contract is

onerous or not (About: Onerous Contract, 2019). In this regard onerous contract has been defined

by IAS37 as the contract under which cost that cannot be avoided (Unavoidable Cost) exceeds

the economic benefits expected to be received in such contract. Unavoidable cost has also been

defined under IAS37 as least net cost required to be paid for fulfilling the contract which is lower

of cost to fulfill the contract and penalties required to b paid when contract is not fulfilled. In this

context, IAS37 has failed to disclose what costs need to be included while calculating the cost of

fulfilling the contract (IFRS Foundation, 2018, p.4).

Various requests have been received by the IFRS Interpretation Committee (IASB

Committee) to review and provide detail information on which cost need to be included while

estimating fulfilling the contract. To the specific major requests have been raised for the

construction contracts to specify the costs while estimating cost of fulfilling the contract.

Information about the onerous contract has been initially included in the IAS11: Construction

Contracts but from 1 January, 2018, IAS37 has to be used to assess whether contracts are

onerous or not (In Brief- Onerous contracts, 2018). All requests received by the IASB

Committee have been reviewed and it was noticed that there are different views on costs to be

included while estimating cost of fulfilling the contract and there is major possibility that it could

lead to material differences in estimating the cost. Committee refers this case to Board and ask to

clarify the costs to be included and on this Board has accepted the recommendation and make

necessary changes which is then open for public comments through Exposure Draft ED/2018/2

(IFRS Foundation, 2018).

Part B: Application of public interest theory to explain the behaviour of regulator in

introducing the selected exposure draft

Answer to Question 2

To answer this question there is need to select exposure draft and any four comment

letters on the exposure draft. There are two international accounting bodies (IASB and FASB)

that are authorized to propose and modify the accounting standard. Exposure draft selected is

maintenance project undertaken by IFRS Foundation to make the proposed amendment in

accounting standard IAS37: Provisions, Contingent Liabilities and Contingent Assets.

Name of Exposure Draft: “ED/2018/2: Onerous Contracts-Cost of Fulfilling a Contract” (IFRS

Foundation, 2018).

Part A: Major issues covered in the exposure draft (Changes introduced or changed by the

Exposure draft)

On the plain reading of Exposure Draft on Onerous Contracts it has been found that the

purpose of this exposure draft is to make amendment in the accounting standard IAS 37. The

main objective of this amendment is to specify the costs that organization or entity must consider

while calculating the “cost of fulfilling” a contract in order to identify whether the contract is

onerous or not (About: Onerous Contract, 2019). In this regard onerous contract has been defined

by IAS37 as the contract under which cost that cannot be avoided (Unavoidable Cost) exceeds

the economic benefits expected to be received in such contract. Unavoidable cost has also been

defined under IAS37 as least net cost required to be paid for fulfilling the contract which is lower

of cost to fulfill the contract and penalties required to b paid when contract is not fulfilled. In this

context, IAS37 has failed to disclose what costs need to be included while calculating the cost of

fulfilling the contract (IFRS Foundation, 2018, p.4).

Various requests have been received by the IFRS Interpretation Committee (IASB

Committee) to review and provide detail information on which cost need to be included while

estimating fulfilling the contract. To the specific major requests have been raised for the

construction contracts to specify the costs while estimating cost of fulfilling the contract.

Information about the onerous contract has been initially included in the IAS11: Construction

Contracts but from 1 January, 2018, IAS37 has to be used to assess whether contracts are

onerous or not (In Brief- Onerous contracts, 2018). All requests received by the IASB

Committee have been reviewed and it was noticed that there are different views on costs to be

included while estimating cost of fulfilling the contract and there is major possibility that it could

lead to material differences in estimating the cost. Committee refers this case to Board and ask to

clarify the costs to be included and on this Board has accepted the recommendation and make

necessary changes which is then open for public comments through Exposure Draft ED/2018/2

(IFRS Foundation, 2018).

Part B: Application of public interest theory to explain the behaviour of regulator in

introducing the selected exposure draft

6

Deegan (2014, pp. 45-47), provides regulators are assumed to act in the interest of public

and only such regulation will be introduced that will benefit the public at large and it is believed

to be greater than cost. Any regulation that is introduced is not to promote any self interest of

regulator or any particular interest in vested while proposing any regulation (Deegan, 2014).

IFRS Foundation is not for profit organization set up primarily to provide the accounting

standards in the public interest (About US: How we work in the public interest, 2019). The

governance structure of IFRS Foundation ensures the standard setting process remains

independent and it should be impacts by any stakeholder group. It means behaviour of regulator

is in public interest and introduction of selected exposure draft is only for the public interest not

for any specific group of people (Deegan, 2014, pp. 45-47).

Part C: Outlining of the views presented in the comment letters highlighting the areas of

agreement and disagreement with the exposure draft

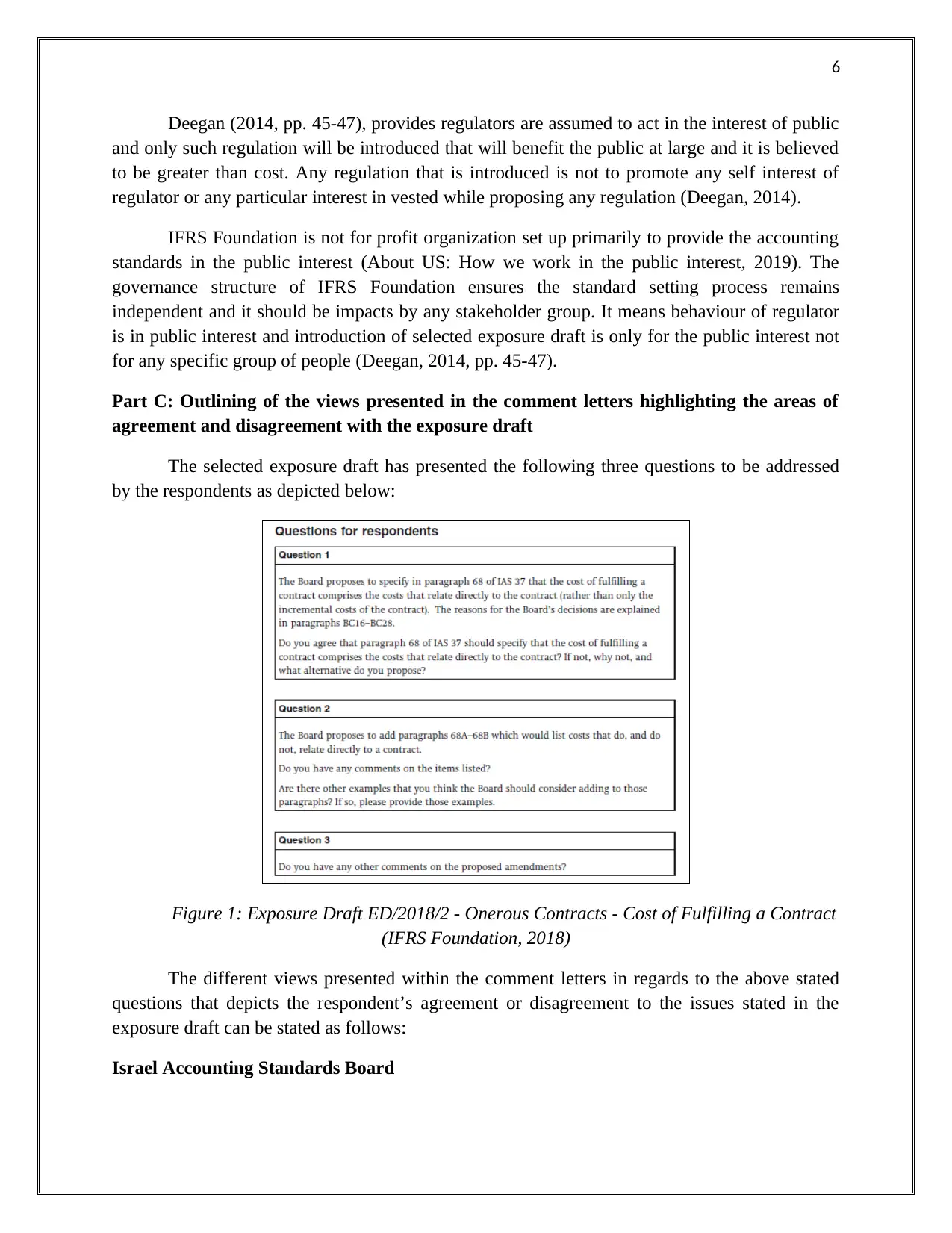

The selected exposure draft has presented the following three questions to be addressed

by the respondents as depicted below:

Figure 1: Exposure Draft ED/2018/2 - Onerous Contracts - Cost of Fulfilling a Contract

(IFRS Foundation, 2018)

The different views presented within the comment letters in regards to the above stated

questions that depicts the respondent’s agreement or disagreement to the issues stated in the

exposure draft can be stated as follows:

Israel Accounting Standards Board

Deegan (2014, pp. 45-47), provides regulators are assumed to act in the interest of public

and only such regulation will be introduced that will benefit the public at large and it is believed

to be greater than cost. Any regulation that is introduced is not to promote any self interest of

regulator or any particular interest in vested while proposing any regulation (Deegan, 2014).

IFRS Foundation is not for profit organization set up primarily to provide the accounting

standards in the public interest (About US: How we work in the public interest, 2019). The

governance structure of IFRS Foundation ensures the standard setting process remains

independent and it should be impacts by any stakeholder group. It means behaviour of regulator

is in public interest and introduction of selected exposure draft is only for the public interest not

for any specific group of people (Deegan, 2014, pp. 45-47).

Part C: Outlining of the views presented in the comment letters highlighting the areas of

agreement and disagreement with the exposure draft

The selected exposure draft has presented the following three questions to be addressed

by the respondents as depicted below:

Figure 1: Exposure Draft ED/2018/2 - Onerous Contracts - Cost of Fulfilling a Contract

(IFRS Foundation, 2018)

The different views presented within the comment letters in regards to the above stated

questions that depicts the respondent’s agreement or disagreement to the issues stated in the

exposure draft can be stated as follows:

Israel Accounting Standards Board

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Figure 2: Exposure Draft ED/2018/2 - Onerous Contracts - Cost of Fulfilling a Contract

Israel Accounting Standards Board (Sapir, 2019)

The comment letter of Israel Accounting Board has expressed its disagreement in relation

to amendment of the paragraph 68 of IAS 37. As per the comment letters, the Board believes that

the amending of this paragraph stating that the cost of fulfilling a contract comprises of all the

costs that directly relate to the contracts are in contradiction of the model IAS 37. The current

model of IAS 36 has required that an entity having an onerous contract should report a lost only

of the unavoidable costs of meeting the obligations exceeds the economic benefits related to it.

This implies making a rationale decision regarding entering into the contract only under the

condition of revue derived from the contract exceeds the incremental cost. There is a clear

provision of recognition of future operating losses as peer the current model. However, the

proposed changes would requires considering all the fixed costs and their inclusion in

determination of losses that could be realized from onerous contracts would result in recognition

of cretin future operating losses that are not permitted under IAS 37. As such, the Board has

required clarification in regard to the proposed amendment and that does not support the changes

in IAS 37 model (Sapir, 2019, p.2).

The Institute of Chartered Accountants of India

Figure 2: Exposure Draft ED/2018/2 - Onerous Contracts - Cost of Fulfilling a Contract

Israel Accounting Standards Board (Sapir, 2019)

The comment letter of Israel Accounting Board has expressed its disagreement in relation

to amendment of the paragraph 68 of IAS 37. As per the comment letters, the Board believes that

the amending of this paragraph stating that the cost of fulfilling a contract comprises of all the

costs that directly relate to the contracts are in contradiction of the model IAS 37. The current

model of IAS 36 has required that an entity having an onerous contract should report a lost only

of the unavoidable costs of meeting the obligations exceeds the economic benefits related to it.

This implies making a rationale decision regarding entering into the contract only under the

condition of revue derived from the contract exceeds the incremental cost. There is a clear

provision of recognition of future operating losses as peer the current model. However, the

proposed changes would requires considering all the fixed costs and their inclusion in

determination of losses that could be realized from onerous contracts would result in recognition

of cretin future operating losses that are not permitted under IAS 37. As such, the Board has

required clarification in regard to the proposed amendment and that does not support the changes

in IAS 37 model (Sapir, 2019, p.2).

The Institute of Chartered Accountants of India

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Figure 3: Exposure Draft ED/2018/2 - Onerous Contracts - Cost of Fulfilling a Contract

ICAI (Kumar, 2019)

This comment letter has stated that ICAI has presented an agreement in relation to the

proposed changes within Onerous Contracts as presented in the Exposure Draft. The companies

Act 2013 have required the application of IFRS standards for public interest entities within India.

The Board has agreed in relation to first and second proposed changes within IAS 37 and has

sated a comment in respect to third question stated in the exposure draft requiring clarification

about measuring an onerous contract provision by an entity on the same costs as is required for

the identifying the contracts as onerous (Kumar, 2019).

McCain Foods Limited

Figure 3: Exposure Draft ED/2018/2 - Onerous Contracts - Cost of Fulfilling a Contract

ICAI (Kumar, 2019)

This comment letter has stated that ICAI has presented an agreement in relation to the

proposed changes within Onerous Contracts as presented in the Exposure Draft. The companies

Act 2013 have required the application of IFRS standards for public interest entities within India.

The Board has agreed in relation to first and second proposed changes within IAS 37 and has

sated a comment in respect to third question stated in the exposure draft requiring clarification

about measuring an onerous contract provision by an entity on the same costs as is required for

the identifying the contracts as onerous (Kumar, 2019).

McCain Foods Limited

9

Figure 4: Exposure Draft ED/2018/2 - Onerous Contracts - Cost of Fulfilling a Contract

McCain Foods Limited (Burton, 2019)

This comment letter ahs intended to provide an explanation regarding the impact of the

proposed changes within the exposure draft in IAS 37 on the listed companies. McCain Foods

Limited has expressed agreement in reference to the first question presented within the exposure

draft but has asked for the clarification about the second stated question that propose changes

about not requiring any mention of allocation of indirect costs other than depreciation (Burton,

2019).

Volkswagen

Figure 5: Exposure Draft ED/2018/2 - Onerous Contracts - Cost of Fulfilling a Contract

Volkswagen (Bartölke, 2019)

Volkswagen has expressed agreement in relation to the first and second question

presented within the exposure draft and has required a clear distinction between general

administration costs and administration costs directly related to a contract in repose to the

question 3 (Bartölke, 2019, p.3).

Part D: Application of the Regulation Theories to the Comment Letters

The regulation theories such as public interest capture and private interest theory can be

used for addressing the issues discussed within the comment letters. As per the public interest

theory, the regulators should act in the interests of the general public while aiming to introduce

Figure 4: Exposure Draft ED/2018/2 - Onerous Contracts - Cost of Fulfilling a Contract

McCain Foods Limited (Burton, 2019)

This comment letter ahs intended to provide an explanation regarding the impact of the

proposed changes within the exposure draft in IAS 37 on the listed companies. McCain Foods

Limited has expressed agreement in reference to the first question presented within the exposure

draft but has asked for the clarification about the second stated question that propose changes

about not requiring any mention of allocation of indirect costs other than depreciation (Burton,

2019).

Volkswagen

Figure 5: Exposure Draft ED/2018/2 - Onerous Contracts - Cost of Fulfilling a Contract

Volkswagen (Bartölke, 2019)

Volkswagen has expressed agreement in relation to the first and second question

presented within the exposure draft and has required a clear distinction between general

administration costs and administration costs directly related to a contract in repose to the

question 3 (Bartölke, 2019, p.3).

Part D: Application of the Regulation Theories to the Comment Letters

The regulation theories such as public interest capture and private interest theory can be

used for addressing the issues discussed within the comment letters. As per the public interest

theory, the regulators should act in the interests of the general public while aiming to introduce

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

any new accounting regulation (Deegan, 2014, p. 79-80). The accounting bodies such as Israel

Accounting Standards Board and ICAI are acting in the interest of general public as per this

theory by seeking to develop accounting standard that benefits the general public by providing

them accurate financial formation.

On the other hand, companies such as Volkswagen and McCain Foods Limited are acting

in their own self-interest as per the private interest theory for making their issues known to the

IASB in adoption of the changes introduced within IAS 37 (Deegan, 2014, p. 83-93). Lastly, the

capture theory has stated that accounting regulations are introduced for protecting the public

interests however; the regulated parties tend to act for promoting their self-benefit (Deegan,

2014, p. 80-87). It can be stated that there is no accounting body that has acted as per the capture

theory in relation to the exposure draft provided. Thus, private and public interest theory are best

suited for addressing the issue presented within the comment letters.

any new accounting regulation (Deegan, 2014, p. 79-80). The accounting bodies such as Israel

Accounting Standards Board and ICAI are acting in the interest of general public as per this

theory by seeking to develop accounting standard that benefits the general public by providing

them accurate financial formation.

On the other hand, companies such as Volkswagen and McCain Foods Limited are acting

in their own self-interest as per the private interest theory for making their issues known to the

IASB in adoption of the changes introduced within IAS 37 (Deegan, 2014, p. 83-93). Lastly, the

capture theory has stated that accounting regulations are introduced for protecting the public

interests however; the regulated parties tend to act for promoting their self-benefit (Deegan,

2014, p. 80-87). It can be stated that there is no accounting body that has acted as per the capture

theory in relation to the exposure draft provided. Thus, private and public interest theory are best

suited for addressing the issue presented within the comment letters.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

References

About US: How we work in the public interest. (2019). IFRS Foundation. Retrieved on May 14,

2019, from https://www.ifrs.org/about-us/the-public-interest/

About: Onerous Contract. (2019). IFRS Foundation. Retrieved on May 14, 2019, from

https://www.ifrs.org/projects/work-plan/onerous-contracts-cost-of-fulfilling-a-contract/

#about

Bartölke, I. (2019, 11 April). Exposure Draft ED/2018/2 – Onerous Contracts – Cost of Fulfilling

a Contract. Retrieved on May 14, 2019, from

http://eifrs.ifrs.org/eifrs/comment_letters//527/527_25335_ANDREASGATTUNGVolks

wagenGroupVG_0_CommentLetterVolkswagenAGOnerousContracts.pdf

Burton, R.N. (2019, 11 April). Onerous contracts - cost of fulfilling a contract. Retrieved on May

14, 2019, from

http://eifrs.ifrs.org/eifrs/comment_letters//527/527_25350_RichardNBurtonMcCainFoods

_0_Onerouscontractscostoffulfillingacontract.pdf

Deegan, C. (2014). Financial Accounting Theory (4th ed.). McGraw-Hill: Sydney.

Grosu, V. & Socoliuc, M. (2012). Effects And Implications Of The Implementation Of Ifrs 15 -

Revenue From Contracts With Customers. Retrieved 13 May, 2019, from

http://www.strategiimanageriale.ro/images/images_site/articole/article_6db6e593597daec

5e7db3ba8260e5b07.pdf

Hardidge, D. & Subramanian, R. (2017). Everything you need to prepare for IFRS 15. Retrieved

13 May, 2019, from https://www.intheblack.com/articles/2017/03/14/everything-you-

need-to-prepare-for-ifrs-15

Heng, K. & Rinarelli, J. (2019). AASB 15: New revenue disclosures for half year accounts.

Retrieved 13 May, 2019, from https://home.kpmg/au/en/home/insights/2019/01/aasb-15-

revenue-disclosures-transition-approach.html

IFRS Foundation. (2018). IFRS Standards Exposure Draft ED/2018/2 Onerous Contracts- Cost

of Fulfilling a Contract. Proposed amendments to IAS 37. Retrieved on May 14, 2019,

from https://www.ifrs.org/-/media/project/onerous-contracts-cost-of-fulfilling-a-contract-

amendments-to-ias-37/ed-onerous-contracts-december-2018.pdf

In Brief- Onerous contracts. (2018). IFRS Foundation: Proposals to clarify IAS 37 Provisions,

Contingent Liabilities and Contingent Assets. Retrieved on May 14, 2019, from

https://www.ifrs.org/-/media/project/onerous-contracts-cost-of-fulfilling-a-contract-

amendments-to-ias-37/ed-onerous-contracts-factsheet-dec-2018.pdf

References

About US: How we work in the public interest. (2019). IFRS Foundation. Retrieved on May 14,

2019, from https://www.ifrs.org/about-us/the-public-interest/

About: Onerous Contract. (2019). IFRS Foundation. Retrieved on May 14, 2019, from

https://www.ifrs.org/projects/work-plan/onerous-contracts-cost-of-fulfilling-a-contract/

#about

Bartölke, I. (2019, 11 April). Exposure Draft ED/2018/2 – Onerous Contracts – Cost of Fulfilling

a Contract. Retrieved on May 14, 2019, from

http://eifrs.ifrs.org/eifrs/comment_letters//527/527_25335_ANDREASGATTUNGVolks

wagenGroupVG_0_CommentLetterVolkswagenAGOnerousContracts.pdf

Burton, R.N. (2019, 11 April). Onerous contracts - cost of fulfilling a contract. Retrieved on May

14, 2019, from

http://eifrs.ifrs.org/eifrs/comment_letters//527/527_25350_RichardNBurtonMcCainFoods

_0_Onerouscontractscostoffulfillingacontract.pdf

Deegan, C. (2014). Financial Accounting Theory (4th ed.). McGraw-Hill: Sydney.

Grosu, V. & Socoliuc, M. (2012). Effects And Implications Of The Implementation Of Ifrs 15 -

Revenue From Contracts With Customers. Retrieved 13 May, 2019, from

http://www.strategiimanageriale.ro/images/images_site/articole/article_6db6e593597daec

5e7db3ba8260e5b07.pdf

Hardidge, D. & Subramanian, R. (2017). Everything you need to prepare for IFRS 15. Retrieved

13 May, 2019, from https://www.intheblack.com/articles/2017/03/14/everything-you-

need-to-prepare-for-ifrs-15

Heng, K. & Rinarelli, J. (2019). AASB 15: New revenue disclosures for half year accounts.

Retrieved 13 May, 2019, from https://home.kpmg/au/en/home/insights/2019/01/aasb-15-

revenue-disclosures-transition-approach.html

IFRS Foundation. (2018). IFRS Standards Exposure Draft ED/2018/2 Onerous Contracts- Cost

of Fulfilling a Contract. Proposed amendments to IAS 37. Retrieved on May 14, 2019,

from https://www.ifrs.org/-/media/project/onerous-contracts-cost-of-fulfilling-a-contract-

amendments-to-ias-37/ed-onerous-contracts-december-2018.pdf

In Brief- Onerous contracts. (2018). IFRS Foundation: Proposals to clarify IAS 37 Provisions,

Contingent Liabilities and Contingent Assets. Retrieved on May 14, 2019, from

https://www.ifrs.org/-/media/project/onerous-contracts-cost-of-fulfilling-a-contract-

amendments-to-ias-37/ed-onerous-contracts-factsheet-dec-2018.pdf

12

KPMG Australia. (2018). Example financial statements for public companies. Retrieved 13 May,

2019, from https://home.kpmg/au/en/home/insights/2015/11/example-financial-

statements-public-company.html

Kumar, V. (2019, 5 April). Comments of the Institute of Chartered Accountants of India (ICAI)

on IASB's Exposure Draft ‘Onerous Contracts- Cost of fulfilling a contract - Proposed

amendments to IAS 37. Retrieved on May 14, 2019, from

http://eifrs.ifrs.org/eifrs/comment_letters//527/527_25323_CAMPVijayKumarTheInstitut

eofCharteredAccountantsofIndiaICAI_0_CommentsonIAS37ED.pdf

Sapir, D. (2019, 21 March). Exposure Draft ED/2018/2 – Onerous Contracts – Cost of Fulfilling

a Contract – Proposed amendments to IAS 37. Retrieved on May 14, 2019, from

http://eifrs.ifrs.org/eifrs/comment_letters//527/527_25310_DOVSAPIRIsraelAccounting

StandardsBoardIASB_0_IsraelAccountingStandardsBoardsCommentletterproposedamen

dementstoIAS37.pdf

Tadros, E. (2018). Companies lagging on revenue recognition accounting changes. Retrieved 13

May, 2019, from https://www.afr.com/business/accounting/companies-lagging-on-

revenue-recognition-accounting-changes-20180607-h11450

KPMG Australia. (2018). Example financial statements for public companies. Retrieved 13 May,

2019, from https://home.kpmg/au/en/home/insights/2015/11/example-financial-

statements-public-company.html

Kumar, V. (2019, 5 April). Comments of the Institute of Chartered Accountants of India (ICAI)

on IASB's Exposure Draft ‘Onerous Contracts- Cost of fulfilling a contract - Proposed

amendments to IAS 37. Retrieved on May 14, 2019, from

http://eifrs.ifrs.org/eifrs/comment_letters//527/527_25323_CAMPVijayKumarTheInstitut

eofCharteredAccountantsofIndiaICAI_0_CommentsonIAS37ED.pdf

Sapir, D. (2019, 21 March). Exposure Draft ED/2018/2 – Onerous Contracts – Cost of Fulfilling

a Contract – Proposed amendments to IAS 37. Retrieved on May 14, 2019, from

http://eifrs.ifrs.org/eifrs/comment_letters//527/527_25310_DOVSAPIRIsraelAccounting

StandardsBoardIASB_0_IsraelAccountingStandardsBoardsCommentletterproposedamen

dementstoIAS37.pdf

Tadros, E. (2018). Companies lagging on revenue recognition accounting changes. Retrieved 13

May, 2019, from https://www.afr.com/business/accounting/companies-lagging-on-

revenue-recognition-accounting-changes-20180607-h11450

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.