Financial Reporting: Stakeholders, IFRS, and Performance Analysis

VerifiedAdded on 2020/06/04

|13

|3955

|43

Report

AI Summary

This report provides a comprehensive overview of financial reporting, beginning with its context and purpose, and then delving into the examination of reporting frameworks, particularly focusing on IFRS. It identifies the main stakeholders of an organization and discusses the benefits of financial reporting in meeting organizational goals. The report outlines the main financial statements, including the statement of profit and loss, statement of equity, and statement of financial position, and then applies this knowledge to interpret the financial performance of M&S. It also highlights the differences between IFRS and IAS, and the benefits of IFRS adoption, concluding with an identification of varying degrees of compliance with IFRS. The report uses examples from the provided financial statements, including profit and loss, balance sheet, and cash flow statements, to illustrate key concepts and principles. The conclusion summarizes the key findings, and the report is thoroughly referenced.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Q1: Context and purpose of financial reporting..........................................................................1

Q2: Examination of reporting framework...................................................................................2

Q3: Identification of main stakeholders of an organisation and its benefits...............................3

Q4: Value of financial reporting for meeting organisation goals...............................................4

Q5: Main financial statements....................................................................................................5

A: Statement of profit and loss:..................................................................................................5

B: Statement of equity:................................................................................................................5

C: Statement of financial position:..............................................................................................6

Q6: Interpretation of financial performance of M&S.................................................................7

Q7: Difference among IFRS and IAS.........................................................................................8

Q8: Benefits of IFRS...................................................................................................................9

Q9: Identify the varying degrees of compliance with IFRS.......................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

Q1: Context and purpose of financial reporting..........................................................................1

Q2: Examination of reporting framework...................................................................................2

Q3: Identification of main stakeholders of an organisation and its benefits...............................3

Q4: Value of financial reporting for meeting organisation goals...............................................4

Q5: Main financial statements....................................................................................................5

A: Statement of profit and loss:..................................................................................................5

B: Statement of equity:................................................................................................................5

C: Statement of financial position:..............................................................................................6

Q6: Interpretation of financial performance of M&S.................................................................7

Q7: Difference among IFRS and IAS.........................................................................................8

Q8: Benefits of IFRS...................................................................................................................9

Q9: Identify the varying degrees of compliance with IFRS.......................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial reporting is a crucial aspects of any business organisation by which

management can formulate their every day transactions. It record various financial activities of a

business, individual and other valuable entries. It is mainly related to internal level in an

organisation but sometimes, it is prepared for the external users also. Such as shareholders,

lenders, suppliers and financial analysts (Council, 2012). This project report explain various

information about financial reporting and framework required during preparation. Examination

of stakeholders of an organisation and its benefits. Computation of different financial statements

in order to analyse the current year performance of the company. Understanding of IFRS and

there advantages are evaluated in this project report.

Q1: Context and purpose of financial reporting

Financial reporting is an important to be carried out any business organisation whether

small or large. It will be easy for them to determine there ongoing performances throughout the

year. It is necessary to perform the reporting of its financial performance in well organise

financial statement. Likewise, it is not efficient to only think for representing financial

performance of the company. But at the same time, it is highly essential that material facts and

suggestion can also provide more positive image of the company.

During preparation of financial report, managers should always determine that biasses

would not be involved. In the world economic it plays a vital role in formulation of financial

report. It is utmost crucial to provide relevant and reliable data to the proprietor of a company

where there is section among ownership and control (Chen and et. al 2011). This is mostly

related with public limited organisation, where share capital is sell to the public through a stock

market. The owners attain a yearly financial statement which is summarising the performance

and position of their company so that they can measure how effectively their investment are

performing during the year.

Importance:

It will be helpful in statutory audit the financial statements of a company to provide their

opinion. It is essential for raising capital at national or international level.

Purpose of financial reporting:

1

Financial reporting is a crucial aspects of any business organisation by which

management can formulate their every day transactions. It record various financial activities of a

business, individual and other valuable entries. It is mainly related to internal level in an

organisation but sometimes, it is prepared for the external users also. Such as shareholders,

lenders, suppliers and financial analysts (Council, 2012). This project report explain various

information about financial reporting and framework required during preparation. Examination

of stakeholders of an organisation and its benefits. Computation of different financial statements

in order to analyse the current year performance of the company. Understanding of IFRS and

there advantages are evaluated in this project report.

Q1: Context and purpose of financial reporting

Financial reporting is an important to be carried out any business organisation whether

small or large. It will be easy for them to determine there ongoing performances throughout the

year. It is necessary to perform the reporting of its financial performance in well organise

financial statement. Likewise, it is not efficient to only think for representing financial

performance of the company. But at the same time, it is highly essential that material facts and

suggestion can also provide more positive image of the company.

During preparation of financial report, managers should always determine that biasses

would not be involved. In the world economic it plays a vital role in formulation of financial

report. It is utmost crucial to provide relevant and reliable data to the proprietor of a company

where there is section among ownership and control (Chen and et. al 2011). This is mostly

related with public limited organisation, where share capital is sell to the public through a stock

market. The owners attain a yearly financial statement which is summarising the performance

and position of their company so that they can measure how effectively their investment are

performing during the year.

Importance:

It will be helpful in statutory audit the financial statements of a company to provide their

opinion. It is essential for raising capital at national or international level.

Purpose of financial reporting:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The main objective of reporting is to deliver financial data regarding reporting entity that

is more effective to existing and potential investors in order take valuable decision.

It is framework developed to meet out common financial requirement for large range of

users (Rajgopal and Venkatachalam, 2011).

Financial reports are submitted to gain credit or loan from financial institutions.

Certain specific decision related with buying, selling or holding equity and debts

instrument and other way of credit.

It will help to provide necessary information about economic resources and effective

utilisation of those over a period of time.

Q2: Examination of reporting framework

It has been seen that IFRS framework is providing basic concept that underlie the

preparation of financial statement for outside users. It serves as a guide to board in developing

bright future IFRS and make efforts to resolve accounting problem that are not solved directly in

an international accounting standard (IAS). The conceptual framework is relies on the primary

concept that is used for the preparation and formation of financial statements for outside users. It

mainly deal with:

The purpose of financial reporting is related with financial data regarding reporting

activities which is helpful to existing and potential investors other parties to take

necessary decision-making.

The qualitative characteristics of valuable financial data is based on relevance and

understandability of every department.

It is more valuable to the auditors and other users to help interested parties to determine

IASBs approach to the arrangement of an accounting standards.

Regulatory framework: The existence of essential infrastructure that support direction,

control and implementation of proposed course of action and laws (Nobes, 2014). The system of

regulation is said to be uniform set of account which present operators to keep regular entries in

the books of accounts. The IASC(International accounting standard board) has issues set pattern

for recording necessary information according to the policies made by the department.

Qualitative characteristic of financial information

It will help to identify various types of data which are likely to be most effective for users

in making necessary decision for the betterment of an organisation.

2

is more effective to existing and potential investors in order take valuable decision.

It is framework developed to meet out common financial requirement for large range of

users (Rajgopal and Venkatachalam, 2011).

Financial reports are submitted to gain credit or loan from financial institutions.

Certain specific decision related with buying, selling or holding equity and debts

instrument and other way of credit.

It will help to provide necessary information about economic resources and effective

utilisation of those over a period of time.

Q2: Examination of reporting framework

It has been seen that IFRS framework is providing basic concept that underlie the

preparation of financial statement for outside users. It serves as a guide to board in developing

bright future IFRS and make efforts to resolve accounting problem that are not solved directly in

an international accounting standard (IAS). The conceptual framework is relies on the primary

concept that is used for the preparation and formation of financial statements for outside users. It

mainly deal with:

The purpose of financial reporting is related with financial data regarding reporting

activities which is helpful to existing and potential investors other parties to take

necessary decision-making.

The qualitative characteristics of valuable financial data is based on relevance and

understandability of every department.

It is more valuable to the auditors and other users to help interested parties to determine

IASBs approach to the arrangement of an accounting standards.

Regulatory framework: The existence of essential infrastructure that support direction,

control and implementation of proposed course of action and laws (Nobes, 2014). The system of

regulation is said to be uniform set of account which present operators to keep regular entries in

the books of accounts. The IASC(International accounting standard board) has issues set pattern

for recording necessary information according to the policies made by the department.

Qualitative characteristic of financial information

It will help to identify various types of data which are likely to be most effective for users

in making necessary decision for the betterment of an organisation.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It apply equally to financial data in more general purpose during preparation of financial

reports.

Financial data is crucial when, it is relevant and represent correctly the exact demanded

by the company's owner (Van Greuning, Scott and Terblanche, 2011).

Companies those are using IFRS and have their financial audited in accordance with ISA

will help them to enhance their status and goodwill for longer period of time.

The benefits of financial information is increased if it is more comparable, verifiable and

timely presented.

Q3: Identification of main stakeholders of an organisation and its benefits

Stakeholders are primary part of any business concern without them a company cannot

survive or function in well planned manner. Those individuals which are having some beneficial

interest in M&S company. An organisation's shareholders are said to be that individual or team

that impact or have certain value in the firm's decision making. They are responsible for affecting

the activities either directly or indirectly. Members of stakeholders are customers, suppliers,

local communities and regulatory bodies.

It is important that every stakeholder of a company can have vital information about the

capital invested by an organisation. Investors and creditors of a M&S is mostly relies on

financial situation and performance of the company during the year. Every party those are

invested in M&S project have the right to know about there investment and return they are

getting (Morris, 2011). It is necessary to analyse several financial statements such as profit and

loss, balance sheet that give vital information about total investment made by the firm.

Benefit to organisation:

Being an active participants in M&S company to anticipate environmental problems

those are affecting performance of an organisation.

They are responsible for making solution and eliminate risk of litigation those are arises

because of many reason and affect the profitability.

Being praised by stakeholders for commitment to sustain business action and practices to

help with employee motivation and recruiting.

Financial report of shareholders equity provide valuable information about all those

modification those are taking place in an organisation.

3

reports.

Financial data is crucial when, it is relevant and represent correctly the exact demanded

by the company's owner (Van Greuning, Scott and Terblanche, 2011).

Companies those are using IFRS and have their financial audited in accordance with ISA

will help them to enhance their status and goodwill for longer period of time.

The benefits of financial information is increased if it is more comparable, verifiable and

timely presented.

Q3: Identification of main stakeholders of an organisation and its benefits

Stakeholders are primary part of any business concern without them a company cannot

survive or function in well planned manner. Those individuals which are having some beneficial

interest in M&S company. An organisation's shareholders are said to be that individual or team

that impact or have certain value in the firm's decision making. They are responsible for affecting

the activities either directly or indirectly. Members of stakeholders are customers, suppliers,

local communities and regulatory bodies.

It is important that every stakeholder of a company can have vital information about the

capital invested by an organisation. Investors and creditors of a M&S is mostly relies on

financial situation and performance of the company during the year. Every party those are

invested in M&S project have the right to know about there investment and return they are

getting (Morris, 2011). It is necessary to analyse several financial statements such as profit and

loss, balance sheet that give vital information about total investment made by the firm.

Benefit to organisation:

Being an active participants in M&S company to anticipate environmental problems

those are affecting performance of an organisation.

They are responsible for making solution and eliminate risk of litigation those are arises

because of many reason and affect the profitability.

Being praised by stakeholders for commitment to sustain business action and practices to

help with employee motivation and recruiting.

Financial report of shareholders equity provide valuable information about all those

modification those are taking place in an organisation.

3

These report can help them to determine exact position of an organisation position

through proper guidance (Klai and Omri, 2011).

Stakeholder pursue businesses team in an equal and transparent mode and employ

informal and formal engagement planning.

They have the right to reveal crucial data like whether firm has enough capital to pay its

expenses and outstanding debts obligation those are available with the company.

Q4: Value of financial reporting for meeting organisation goals

Reporting is more useful in attain organisation aims and objectives. It mainly consists of

balance sheet, cash flow and other statements that are affecting profitability of an administration.

By the help of this, M&S can evaluate its financial position by comparing its standard with other

business activities of other company's. From this, business organisation can compare to make

valuable modification in its present position. At present, this will be more easy to financial

reporting that does not provide firm to attain its group objectives.

But with supportive efforts planning can be made in order to gain future sustainability. It

is made by using necessary data from concern financial statement during the time. The role of

regulatory bodies are more crucial while posting the entries into the books of accounts. It will be

helpful in gaining organisational transparency. IAS are the main financial bodies that set out the

standards for formulating proper accounting in every sector so that more effective outcomes can

be generated in a year. Every department needed to follow proper rules and regulation according

to the set standard made by organisations (Beatty, Liao and Yu, 2013). The main objectives of

financial reporting is to guide the firm for making existing and potential investors and outside

parties to take vital decision for the sake of M&S. There main components of financial reporting

are as mentioned underneath:

Income statement: It is financial record that help a company's to determine its financial

performance over a particular period of time. It is mainly assess by providing a complete detail

of business revenue and expenses through operating and non-operating activities.

Balance sheet: A company performance is mainly decided through analysis its balance

sheets which is prepare by collecting necessary information from various sources. It will

represent total assets and liabilities that are available with the company.

4

through proper guidance (Klai and Omri, 2011).

Stakeholder pursue businesses team in an equal and transparent mode and employ

informal and formal engagement planning.

They have the right to reveal crucial data like whether firm has enough capital to pay its

expenses and outstanding debts obligation those are available with the company.

Q4: Value of financial reporting for meeting organisation goals

Reporting is more useful in attain organisation aims and objectives. It mainly consists of

balance sheet, cash flow and other statements that are affecting profitability of an administration.

By the help of this, M&S can evaluate its financial position by comparing its standard with other

business activities of other company's. From this, business organisation can compare to make

valuable modification in its present position. At present, this will be more easy to financial

reporting that does not provide firm to attain its group objectives.

But with supportive efforts planning can be made in order to gain future sustainability. It

is made by using necessary data from concern financial statement during the time. The role of

regulatory bodies are more crucial while posting the entries into the books of accounts. It will be

helpful in gaining organisational transparency. IAS are the main financial bodies that set out the

standards for formulating proper accounting in every sector so that more effective outcomes can

be generated in a year. Every department needed to follow proper rules and regulation according

to the set standard made by organisations (Beatty, Liao and Yu, 2013). The main objectives of

financial reporting is to guide the firm for making existing and potential investors and outside

parties to take vital decision for the sake of M&S. There main components of financial reporting

are as mentioned underneath:

Income statement: It is financial record that help a company's to determine its financial

performance over a particular period of time. It is mainly assess by providing a complete detail

of business revenue and expenses through operating and non-operating activities.

Balance sheet: A company performance is mainly decided through analysis its balance

sheets which is prepare by collecting necessary information from various sources. It will

represent total assets and liabilities that are available with the company.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash flow: It is one of the crucial statement that is used to detect total amount of cash

inflow and outflow incur by company from its various activities. Such as operating, investing

and financing (Maffett, 2012).

Q5: Main financial statements

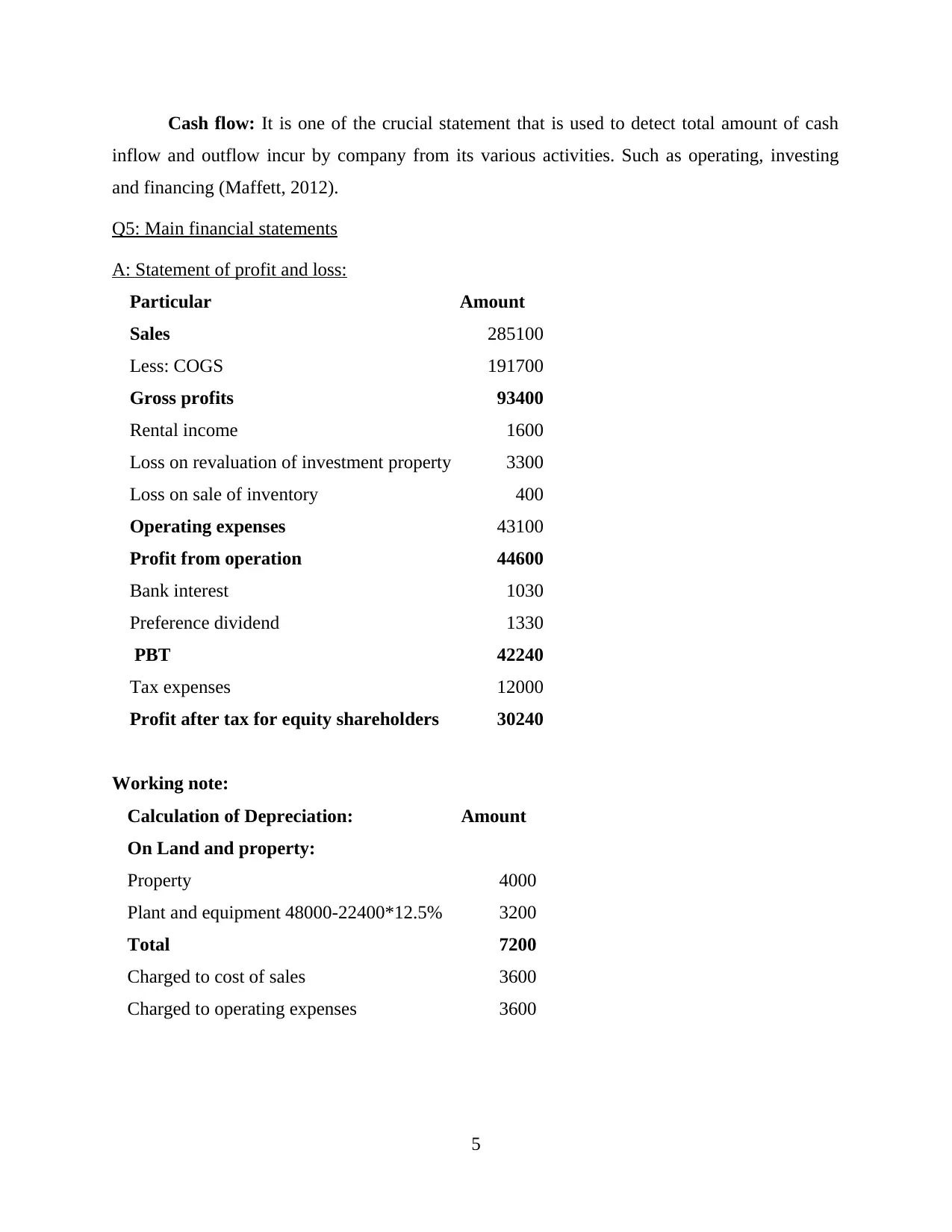

A: Statement of profit and loss:

Particular Amount

Sales 285100

Less: COGS 191700

Gross profits 93400

Rental income 1600

Loss on revaluation of investment property 3300

Loss on sale of inventory 400

Operating expenses 43100

Profit from operation 44600

Bank interest 1030

Preference dividend 1330

PBT 42240

Tax expenses 12000

Profit after tax for equity shareholders 30240

Working note:

Calculation of Depreciation: Amount

On Land and property:

Property 4000

Plant and equipment 48000-22400*12.5% 3200

Total 7200

Charged to cost of sales 3600

Charged to operating expenses 3600

5

inflow and outflow incur by company from its various activities. Such as operating, investing

and financing (Maffett, 2012).

Q5: Main financial statements

A: Statement of profit and loss:

Particular Amount

Sales 285100

Less: COGS 191700

Gross profits 93400

Rental income 1600

Loss on revaluation of investment property 3300

Loss on sale of inventory 400

Operating expenses 43100

Profit from operation 44600

Bank interest 1030

Preference dividend 1330

PBT 42240

Tax expenses 12000

Profit after tax for equity shareholders 30240

Working note:

Calculation of Depreciation: Amount

On Land and property:

Property 4000

Plant and equipment 48000-22400*12.5% 3200

Total 7200

Charged to cost of sales 3600

Charged to operating expenses 3600

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

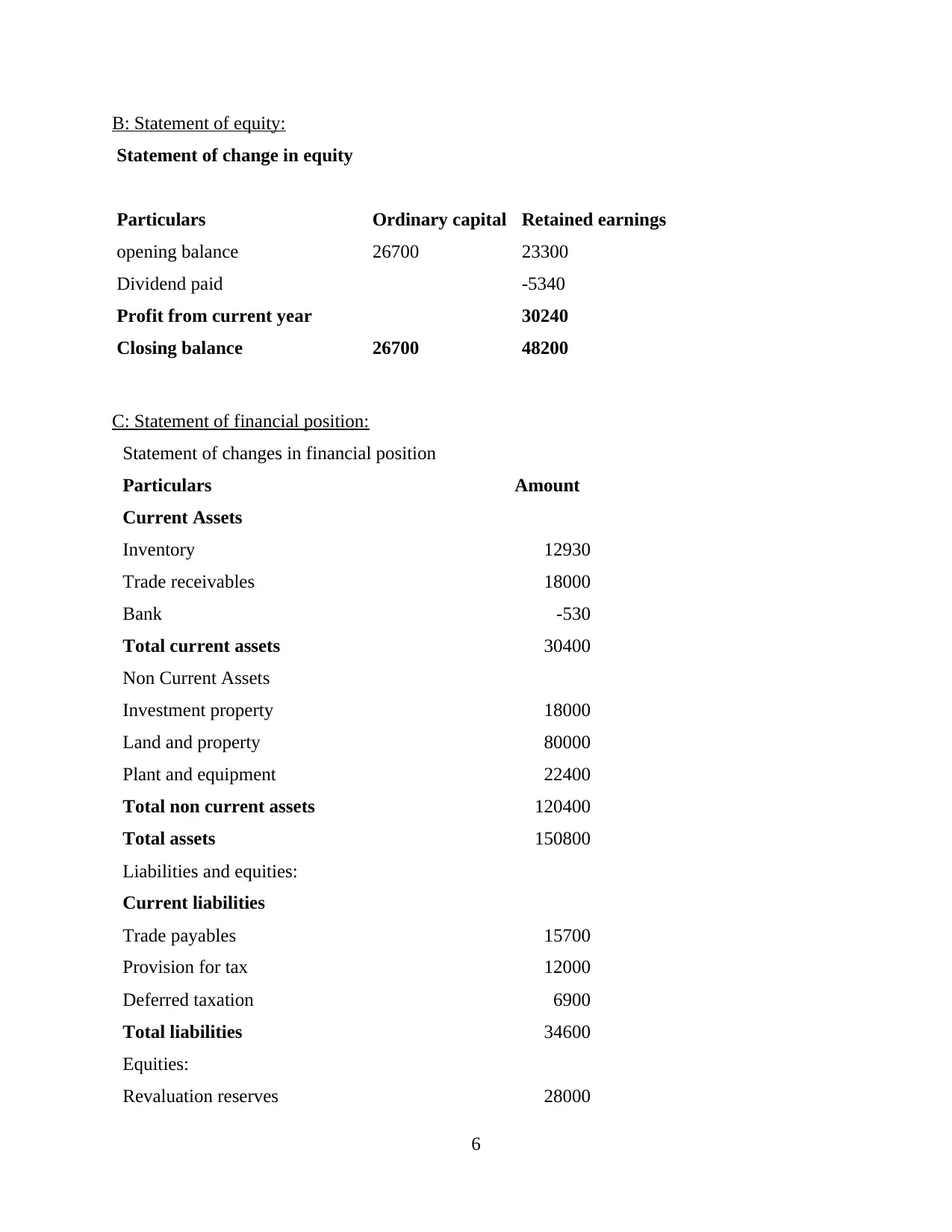

B: Statement of equity:

Statement of change in equity

Particulars Ordinary capital Retained earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

C: Statement of financial position:

Statement of changes in financial position

Particulars Amount

Current Assets

Inventory 12930

Trade receivables 18000

Bank -530

Total current assets 30400

Non Current Assets

Investment property 18000

Land and property 80000

Plant and equipment 22400

Total non current assets 120400

Total assets 150800

Liabilities and equities:

Current liabilities

Trade payables 15700

Provision for tax 12000

Deferred taxation 6900

Total liabilities 34600

Equities:

Revaluation reserves 28000

6

Statement of change in equity

Particulars Ordinary capital Retained earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

C: Statement of financial position:

Statement of changes in financial position

Particulars Amount

Current Assets

Inventory 12930

Trade receivables 18000

Bank -530

Total current assets 30400

Non Current Assets

Investment property 18000

Land and property 80000

Plant and equipment 22400

Total non current assets 120400

Total assets 150800

Liabilities and equities:

Current liabilities

Trade payables 15700

Provision for tax 12000

Deferred taxation 6900

Total liabilities 34600

Equities:

Revaluation reserves 28000

6

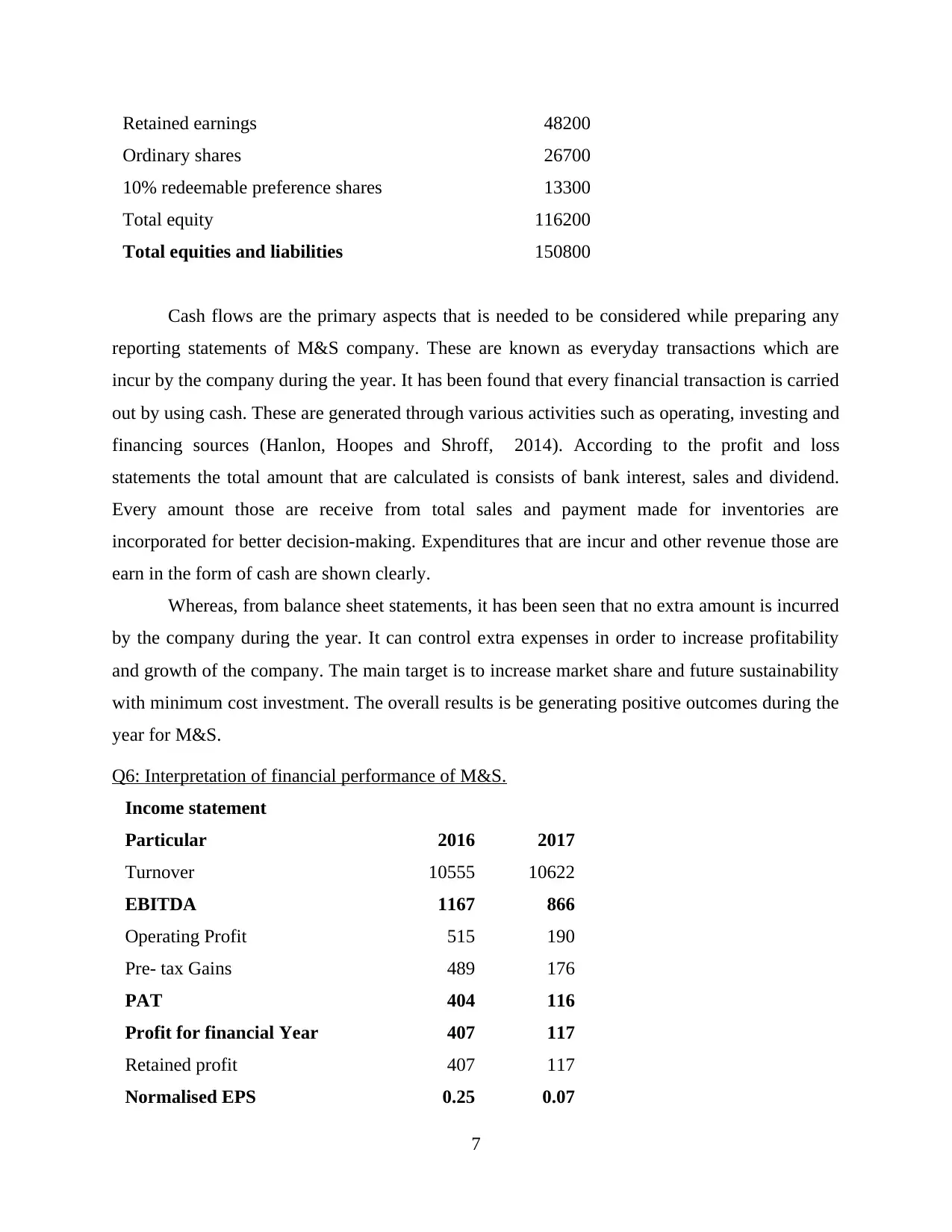

Retained earnings 48200

Ordinary shares 26700

10% redeemable preference shares 13300

Total equity 116200

Total equities and liabilities 150800

Cash flows are the primary aspects that is needed to be considered while preparing any

reporting statements of M&S company. These are known as everyday transactions which are

incur by the company during the year. It has been found that every financial transaction is carried

out by using cash. These are generated through various activities such as operating, investing and

financing sources (Hanlon, Hoopes and Shroff, 2014). According to the profit and loss

statements the total amount that are calculated is consists of bank interest, sales and dividend.

Every amount those are receive from total sales and payment made for inventories are

incorporated for better decision-making. Expenditures that are incur and other revenue those are

earn in the form of cash are shown clearly.

Whereas, from balance sheet statements, it has been seen that no extra amount is incurred

by the company during the year. It can control extra expenses in order to increase profitability

and growth of the company. The main target is to increase market share and future sustainability

with minimum cost investment. The overall results is be generating positive outcomes during the

year for M&S.

Q6: Interpretation of financial performance of M&S.

Income statement

Particular 2016 2017

Turnover 10555 10622

EBITDA 1167 866

Operating Profit 515 190

Pre- tax Gains 489 176

PAT 404 116

Profit for financial Year 407 117

Retained profit 407 117

Normalised EPS 0.25 0.07

7

Ordinary shares 26700

10% redeemable preference shares 13300

Total equity 116200

Total equities and liabilities 150800

Cash flows are the primary aspects that is needed to be considered while preparing any

reporting statements of M&S company. These are known as everyday transactions which are

incur by the company during the year. It has been found that every financial transaction is carried

out by using cash. These are generated through various activities such as operating, investing and

financing sources (Hanlon, Hoopes and Shroff, 2014). According to the profit and loss

statements the total amount that are calculated is consists of bank interest, sales and dividend.

Every amount those are receive from total sales and payment made for inventories are

incorporated for better decision-making. Expenditures that are incur and other revenue those are

earn in the form of cash are shown clearly.

Whereas, from balance sheet statements, it has been seen that no extra amount is incurred

by the company during the year. It can control extra expenses in order to increase profitability

and growth of the company. The main target is to increase market share and future sustainability

with minimum cost investment. The overall results is be generating positive outcomes during the

year for M&S.

Q6: Interpretation of financial performance of M&S.

Income statement

Particular 2016 2017

Turnover 10555 10622

EBITDA 1167 866

Operating Profit 515 190

Pre- tax Gains 489 176

PAT 404 116

Profit for financial Year 407 117

Retained profit 407 117

Normalised EPS 0.25 0.07

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

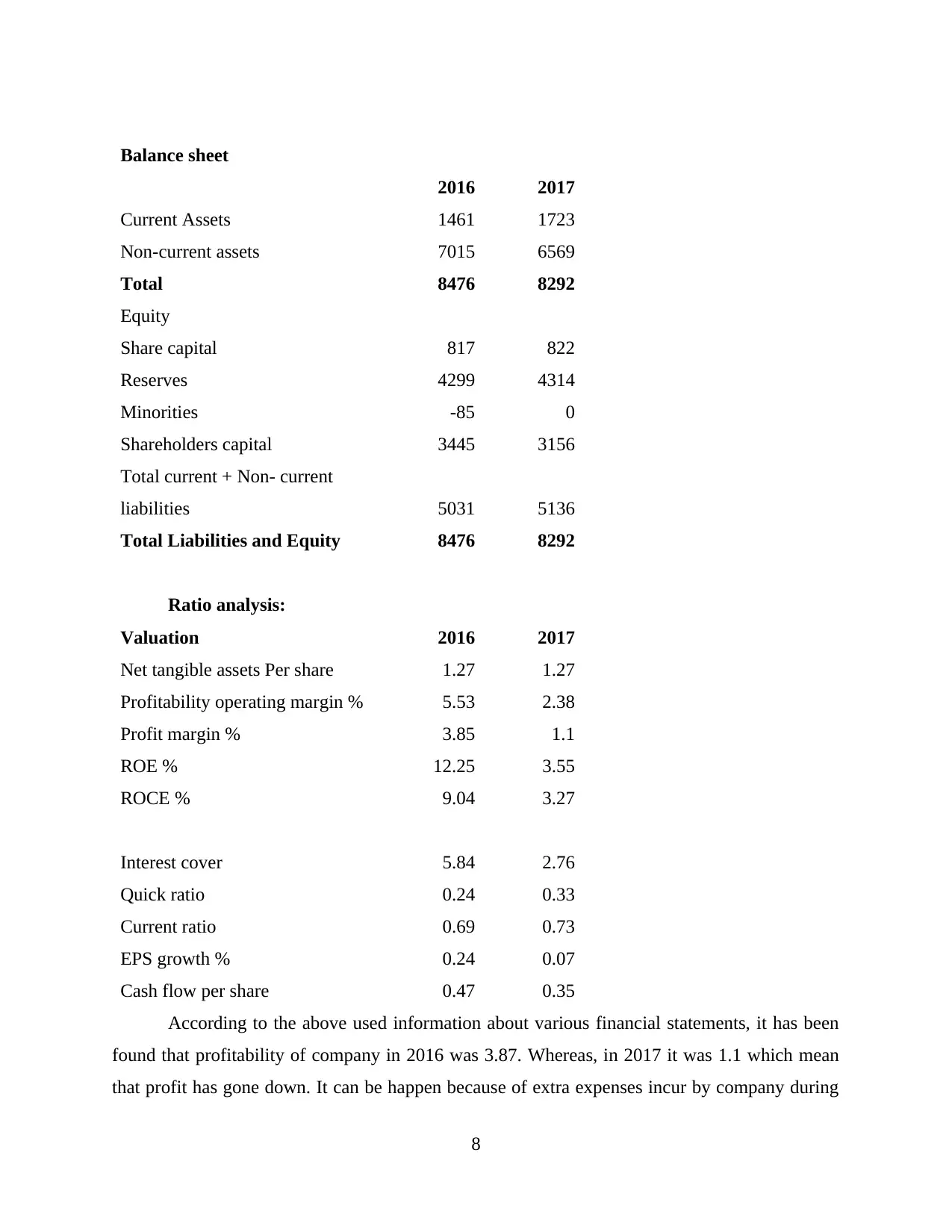

Balance sheet

2016 2017

Current Assets 1461 1723

Non-current assets 7015 6569

Total 8476 8292

Equity

Share capital 817 822

Reserves 4299 4314

Minorities -85 0

Shareholders capital 3445 3156

Total current + Non- current

liabilities 5031 5136

Total Liabilities and Equity 8476 8292

Ratio analysis:

Valuation 2016 2017

Net tangible assets Per share 1.27 1.27

Profitability operating margin % 5.53 2.38

Profit margin % 3.85 1.1

ROE % 12.25 3.55

ROCE % 9.04 3.27

Interest cover 5.84 2.76

Quick ratio 0.24 0.33

Current ratio 0.69 0.73

EPS growth % 0.24 0.07

Cash flow per share 0.47 0.35

According to the above used information about various financial statements, it has been

found that profitability of company in 2016 was 3.87. Whereas, in 2017 it was 1.1 which mean

that profit has gone down. It can be happen because of extra expenses incur by company during

8

2016 2017

Current Assets 1461 1723

Non-current assets 7015 6569

Total 8476 8292

Equity

Share capital 817 822

Reserves 4299 4314

Minorities -85 0

Shareholders capital 3445 3156

Total current + Non- current

liabilities 5031 5136

Total Liabilities and Equity 8476 8292

Ratio analysis:

Valuation 2016 2017

Net tangible assets Per share 1.27 1.27

Profitability operating margin % 5.53 2.38

Profit margin % 3.85 1.1

ROE % 12.25 3.55

ROCE % 9.04 3.27

Interest cover 5.84 2.76

Quick ratio 0.24 0.33

Current ratio 0.69 0.73

EPS growth % 0.24 0.07

Cash flow per share 0.47 0.35

According to the above used information about various financial statements, it has been

found that profitability of company in 2016 was 3.87. Whereas, in 2017 it was 1.1 which mean

that profit has gone down. It can be happen because of extra expenses incur by company during

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the year. The firm operating margin was reduced as compare to last year. ROE of the firm was

12.25% in 2016 and 3.55 in 2017. It is shows wide downfall of 8.5% since last year. Whereas,

ROCE rate is 9.04% in 2016 and 3.27% in current year.

It is also showing negative impacts in the present year because of extra expenses is made

on the purchase of shares from the market. Thus, as compare to profitability, firm is

performances is not up the level according to the set standards. Likewise, the firms liquidity

position is more healthy as compare to previous year. It means that they are able to meet out their

short-term cash-flows requirements. The quick ratio of the company is also effective since 2016.

They are having sufficient amount of capital to cover there debts. So this can be observed as

crucial requirements in order to enhance business productivity. This can be possible only through

effective utilisation of firms resources.

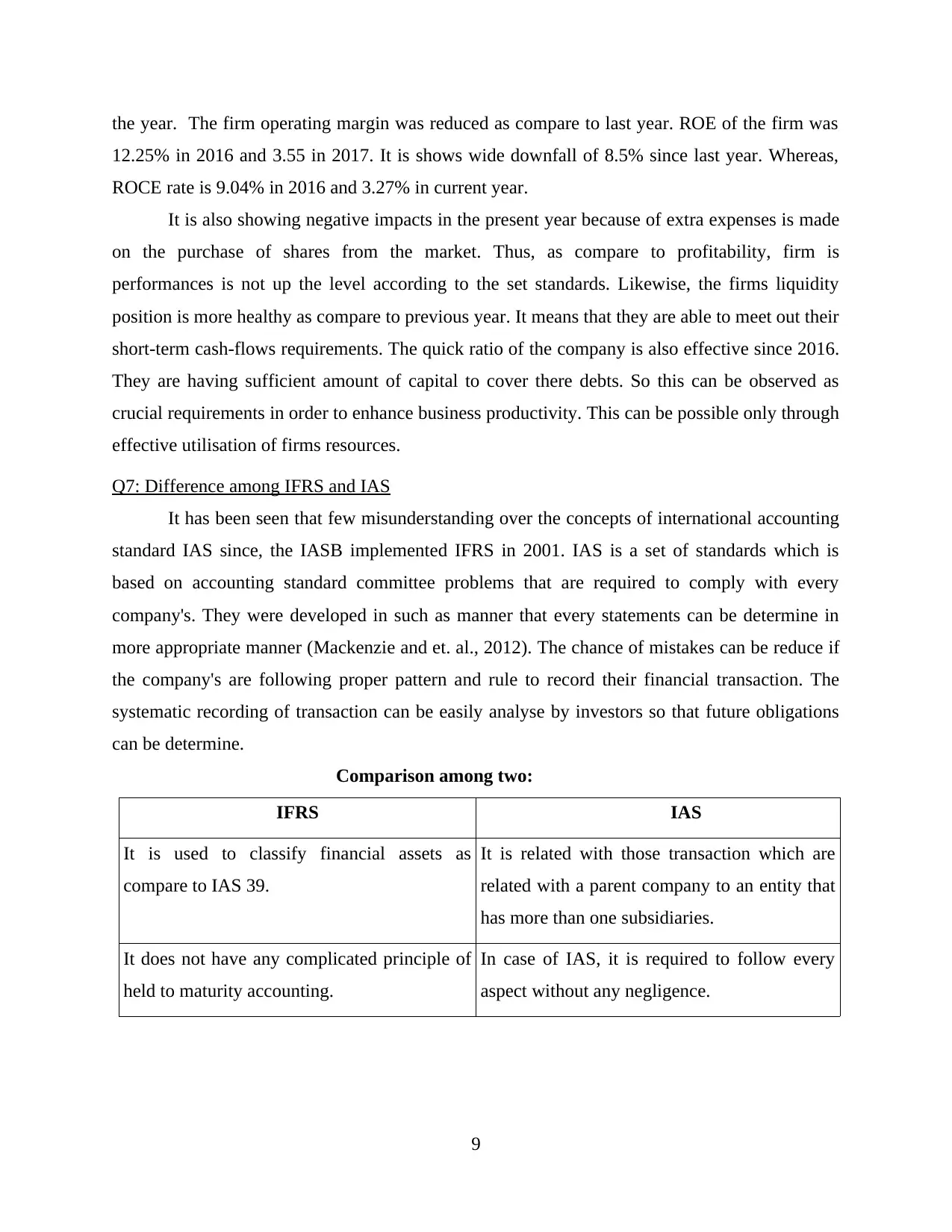

Q7: Difference among IFRS and IAS

It has been seen that few misunderstanding over the concepts of international accounting

standard IAS since, the IASB implemented IFRS in 2001. IAS is a set of standards which is

based on accounting standard committee problems that are required to comply with every

company's. They were developed in such as manner that every statements can be determine in

more appropriate manner (Mackenzie and et. al., 2012). The chance of mistakes can be reduce if

the company's are following proper pattern and rule to record their financial transaction. The

systematic recording of transaction can be easily analyse by investors so that future obligations

can be determine.

Comparison among two:

IFRS IAS

It is used to classify financial assets as

compare to IAS 39.

It is related with those transaction which are

related with a parent company to an entity that

has more than one subsidiaries.

It does not have any complicated principle of

held to maturity accounting.

In case of IAS, it is required to follow every

aspect without any negligence.

9

12.25% in 2016 and 3.55 in 2017. It is shows wide downfall of 8.5% since last year. Whereas,

ROCE rate is 9.04% in 2016 and 3.27% in current year.

It is also showing negative impacts in the present year because of extra expenses is made

on the purchase of shares from the market. Thus, as compare to profitability, firm is

performances is not up the level according to the set standards. Likewise, the firms liquidity

position is more healthy as compare to previous year. It means that they are able to meet out their

short-term cash-flows requirements. The quick ratio of the company is also effective since 2016.

They are having sufficient amount of capital to cover there debts. So this can be observed as

crucial requirements in order to enhance business productivity. This can be possible only through

effective utilisation of firms resources.

Q7: Difference among IFRS and IAS

It has been seen that few misunderstanding over the concepts of international accounting

standard IAS since, the IASB implemented IFRS in 2001. IAS is a set of standards which is

based on accounting standard committee problems that are required to comply with every

company's. They were developed in such as manner that every statements can be determine in

more appropriate manner (Mackenzie and et. al., 2012). The chance of mistakes can be reduce if

the company's are following proper pattern and rule to record their financial transaction. The

systematic recording of transaction can be easily analyse by investors so that future obligations

can be determine.

Comparison among two:

IFRS IAS

It is used to classify financial assets as

compare to IAS 39.

It is related with those transaction which are

related with a parent company to an entity that

has more than one subsidiaries.

It does not have any complicated principle of

held to maturity accounting.

In case of IAS, it is required to follow every

aspect without any negligence.

9

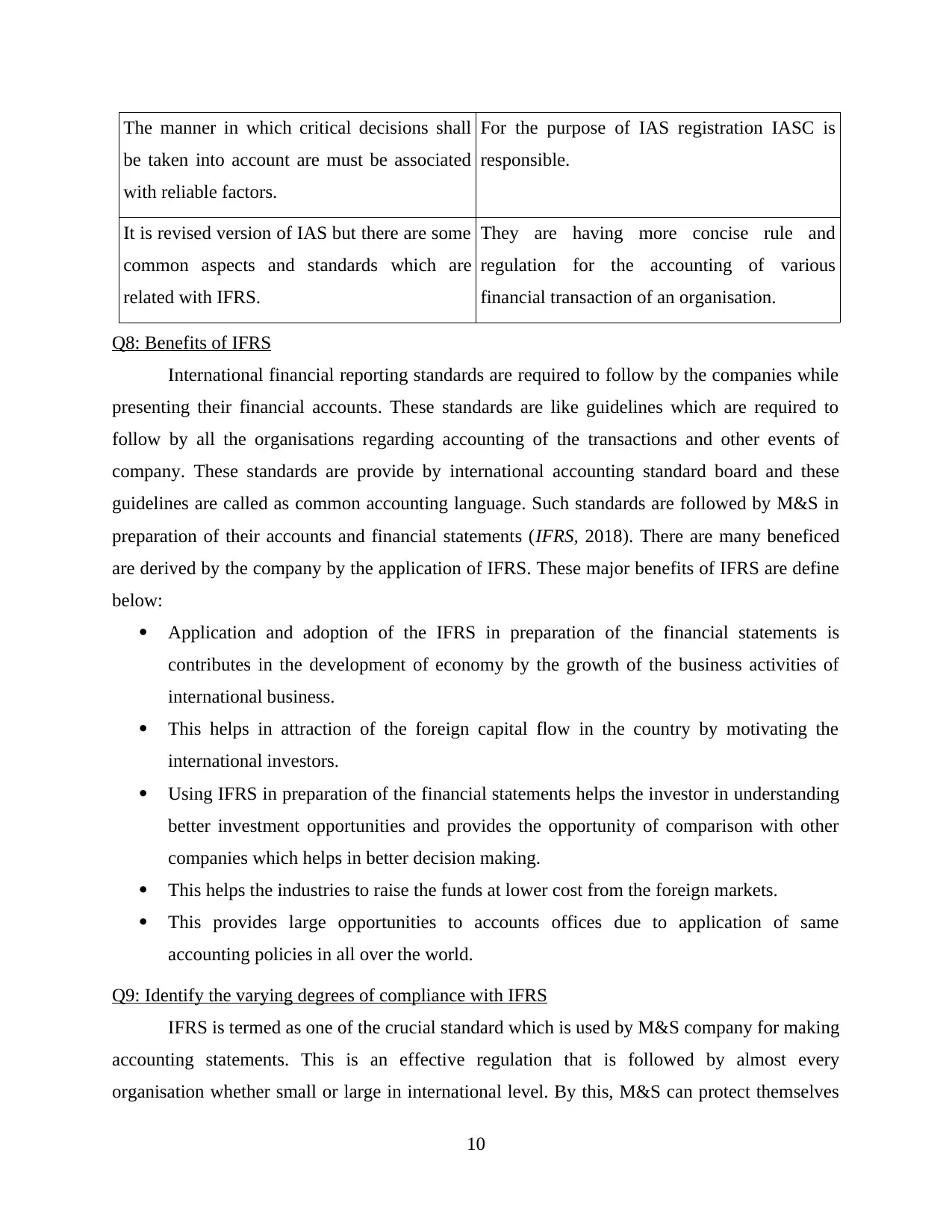

The manner in which critical decisions shall

be taken into account are must be associated

with reliable factors.

For the purpose of IAS registration IASC is

responsible.

It is revised version of IAS but there are some

common aspects and standards which are

related with IFRS.

They are having more concise rule and

regulation for the accounting of various

financial transaction of an organisation.

Q8: Benefits of IFRS

International financial reporting standards are required to follow by the companies while

presenting their financial accounts. These standards are like guidelines which are required to

follow by all the organisations regarding accounting of the transactions and other events of

company. These standards are provide by international accounting standard board and these

guidelines are called as common accounting language. Such standards are followed by M&S in

preparation of their accounts and financial statements (IFRS, 2018). There are many beneficed

are derived by the company by the application of IFRS. These major benefits of IFRS are define

below:

Application and adoption of the IFRS in preparation of the financial statements is

contributes in the development of economy by the growth of the business activities of

international business.

This helps in attraction of the foreign capital flow in the country by motivating the

international investors.

Using IFRS in preparation of the financial statements helps the investor in understanding

better investment opportunities and provides the opportunity of comparison with other

companies which helps in better decision making.

This helps the industries to raise the funds at lower cost from the foreign markets.

This provides large opportunities to accounts offices due to application of same

accounting policies in all over the world.

Q9: Identify the varying degrees of compliance with IFRS

IFRS is termed as one of the crucial standard which is used by M&S company for making

accounting statements. This is an effective regulation that is followed by almost every

organisation whether small or large in international level. By this, M&S can protect themselves

10

be taken into account are must be associated

with reliable factors.

For the purpose of IAS registration IASC is

responsible.

It is revised version of IAS but there are some

common aspects and standards which are

related with IFRS.

They are having more concise rule and

regulation for the accounting of various

financial transaction of an organisation.

Q8: Benefits of IFRS

International financial reporting standards are required to follow by the companies while

presenting their financial accounts. These standards are like guidelines which are required to

follow by all the organisations regarding accounting of the transactions and other events of

company. These standards are provide by international accounting standard board and these

guidelines are called as common accounting language. Such standards are followed by M&S in

preparation of their accounts and financial statements (IFRS, 2018). There are many beneficed

are derived by the company by the application of IFRS. These major benefits of IFRS are define

below:

Application and adoption of the IFRS in preparation of the financial statements is

contributes in the development of economy by the growth of the business activities of

international business.

This helps in attraction of the foreign capital flow in the country by motivating the

international investors.

Using IFRS in preparation of the financial statements helps the investor in understanding

better investment opportunities and provides the opportunity of comparison with other

companies which helps in better decision making.

This helps the industries to raise the funds at lower cost from the foreign markets.

This provides large opportunities to accounts offices due to application of same

accounting policies in all over the world.

Q9: Identify the varying degrees of compliance with IFRS

IFRS is termed as one of the crucial standard which is used by M&S company for making

accounting statements. This is an effective regulation that is followed by almost every

organisation whether small or large in international level. By this, M&S can protect themselves

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.