International Financial Reporting: Analysis, Evaluation, and Standards

VerifiedAdded on 2021/02/19

|16

|4741

|27

Report

AI Summary

This report provides a comprehensive analysis of international financial reporting, focusing on the regulatory frameworks, conceptual frameworks, and governance aspects. The report examines the purpose of financial reporting in meeting organizational goals, development, and growth, highlighting the needs of various stakeholders such as owners, management, creditors, and customers. It delves into the interpretation of profit & loss, cash flow, and balance sheet statements, providing an example using Godwin PLC and includes the analysis of statement of retained earnings. Furthermore, the report explores the benefits of International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS) and assesses financial reporting and auditing models. The report also evaluates the differences and importance of financial reporting in various countries, using Lloyds Banking Group as a representative example. The report provides detailed financial statements including income statement, statement of retained earnings and balance sheet for Godwin PLC, demonstrating the application of financial reporting principles. It aims to provide a clear understanding of the financial reporting landscape.

INTERNATIONAL

FINANCIAL

REPORTING

FINANCIAL

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Evaluating regulatory frameworks and governance in the context of financial reporting....1

P2. Analysis of Financial Reporting Purpose for meeting organisational goals, development

and growth...................................................................................................................................3

TASK 2............................................................................................................................................4

P3. Interpretation of Profit & Loss, Cash Flow and Balance Sheet Statements..........................4

P4. Calculation of financial ratios and their presentation............................................................7

TASK 3............................................................................................................................................8

P5. Benefits of International Accounting Standards (IAS) and International Financial

Reporting Standards (IFRS).........................................................................................................8

P6. Assessing the models of Financial Reporting and Auditing................................................10

TASK 4..........................................................................................................................................11

P7. Evaluating the differences and importance of financial reporting in various countries......11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

APPENDICES...............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Evaluating regulatory frameworks and governance in the context of financial reporting....1

P2. Analysis of Financial Reporting Purpose for meeting organisational goals, development

and growth...................................................................................................................................3

TASK 2............................................................................................................................................4

P3. Interpretation of Profit & Loss, Cash Flow and Balance Sheet Statements..........................4

P4. Calculation of financial ratios and their presentation............................................................7

TASK 3............................................................................................................................................8

P5. Benefits of International Accounting Standards (IAS) and International Financial

Reporting Standards (IFRS).........................................................................................................8

P6. Assessing the models of Financial Reporting and Auditing................................................10

TASK 4..........................................................................................................................................11

P7. Evaluating the differences and importance of financial reporting in various countries......11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

APPENDICES...............................................................................................................................14

INTRODUCTION

Every business enterprise has a set of book-keeping records for each accounting period that

are inclusive of important financial transactions which the organisation undertakes over the

course of its life. It is mandatory for the companies to disclose such information to both internal

as well as external shareholders. In order to ensure consistency and promote comparability,

financial reporting is mandated to be followed using certain formats and principles all around the

world. These are popularly known as International Financial Reporting Standards (IFRS) and

International Accounting Standards (IAS).

This project report aims to outline the context and purpose of financial reporting,

provides benefits and methods of ensuring compliance and accountability as well as evaluate key

principles. Also, different countries have been evaluated to account for deviations in Financial

Reporting Practices. For this purpose, Grant Thornton Accountancy Firm's client Lloyds

Banking Group has been taken into account which is an FTSE 100 retail banking company

headquartered in UK (Representative Client List of Grant Thornton, 2019). It provides banking

as well as financial services to its client on a global scale.

TASK 1

P1. Evaluating regulatory frameworks and governance in the context of financial reporting

The term 'Financial Reporting' can be defined as the presentation as well as

communication of financial records to the relevant key stakeholders. Usually financial reports

are issued in the form of Income Statements, Balance Sheet and Cash Flow Statements among

others, based on the policies and nature of business. Thus, there issuance may differ from

organisation to organisation. Every organisation including Lloyd's Banking Group is required to

comply with the conceptual as well as regulatory frameworks of financial reporting. These have

been discussed as under:

Conceptual framework:

These aim to define the objectives of financial reporting along with acting as a practical

tool that helps in formulation of various Standards (Abeysekera, 2013). Hence, this framework is

required to enables Lloyd's management to develop a strong theoretical foundation so that they

are able to easily measure, present and communicate the various financial transactions

undertaken by them to their key stakeholders. In the context of Financial Reporting, a conceptual

1

Every business enterprise has a set of book-keeping records for each accounting period that

are inclusive of important financial transactions which the organisation undertakes over the

course of its life. It is mandatory for the companies to disclose such information to both internal

as well as external shareholders. In order to ensure consistency and promote comparability,

financial reporting is mandated to be followed using certain formats and principles all around the

world. These are popularly known as International Financial Reporting Standards (IFRS) and

International Accounting Standards (IAS).

This project report aims to outline the context and purpose of financial reporting,

provides benefits and methods of ensuring compliance and accountability as well as evaluate key

principles. Also, different countries have been evaluated to account for deviations in Financial

Reporting Practices. For this purpose, Grant Thornton Accountancy Firm's client Lloyds

Banking Group has been taken into account which is an FTSE 100 retail banking company

headquartered in UK (Representative Client List of Grant Thornton, 2019). It provides banking

as well as financial services to its client on a global scale.

TASK 1

P1. Evaluating regulatory frameworks and governance in the context of financial reporting

The term 'Financial Reporting' can be defined as the presentation as well as

communication of financial records to the relevant key stakeholders. Usually financial reports

are issued in the form of Income Statements, Balance Sheet and Cash Flow Statements among

others, based on the policies and nature of business. Thus, there issuance may differ from

organisation to organisation. Every organisation including Lloyd's Banking Group is required to

comply with the conceptual as well as regulatory frameworks of financial reporting. These have

been discussed as under:

Conceptual framework:

These aim to define the objectives of financial reporting along with acting as a practical

tool that helps in formulation of various Standards (Abeysekera, 2013). Hence, this framework is

required to enables Lloyd's management to develop a strong theoretical foundation so that they

are able to easily measure, present and communicate the various financial transactions

undertaken by them to their key stakeholders. In the context of Financial Reporting, a conceptual

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

framework can be mainly observed as a statement of Generally Accepted Accounting Principles

(GAAP). These principles act as a measuring yardstick as well as point of references in order to

compare and improvise current accounting practices of a company. Lack of such a framework

can lead to a substantial increase in proliferation as well as number of accounting scandals

through misappropriation of profits. Thus, conceptual framework assists in:

Development of future standards;

Promoting coherence between accounting regulations as well as standards;

Preparation and Communication of Financial Statements to the identified key

stakeholders.

Regulatory Framework:

As the name suggests, the regulatory framework determines the manner in which

reporting of financial information is carried out among organisation on a worldwide scale. For

this purpose, International Financial Reporting Standards (IFRS) is one such body which aims to

encourage collaboration, investor engagement and transparency in due process (Albu and Albu,

2012). This framework is necessary for ensuring that the communication of relevant information

to Lloyd's key stakeholders is made in such a way that their needs are fulfilled adequately. Some

of the most important IFRS are as follows:

IFRS 1: First- time Adoption of International Financial Reporting Standards

IFRS 10: Consolidated Financial Statements

IFRS 12: Disclosure of Interest in Other Entities

IFRS 13: Fair Value Measurement

The main purpose of conceptual framework is to facilitate understanding and revision of

both GAAP as well as IFRS. On the other hand, the qualitative characteristics of financial

information can be divided as:

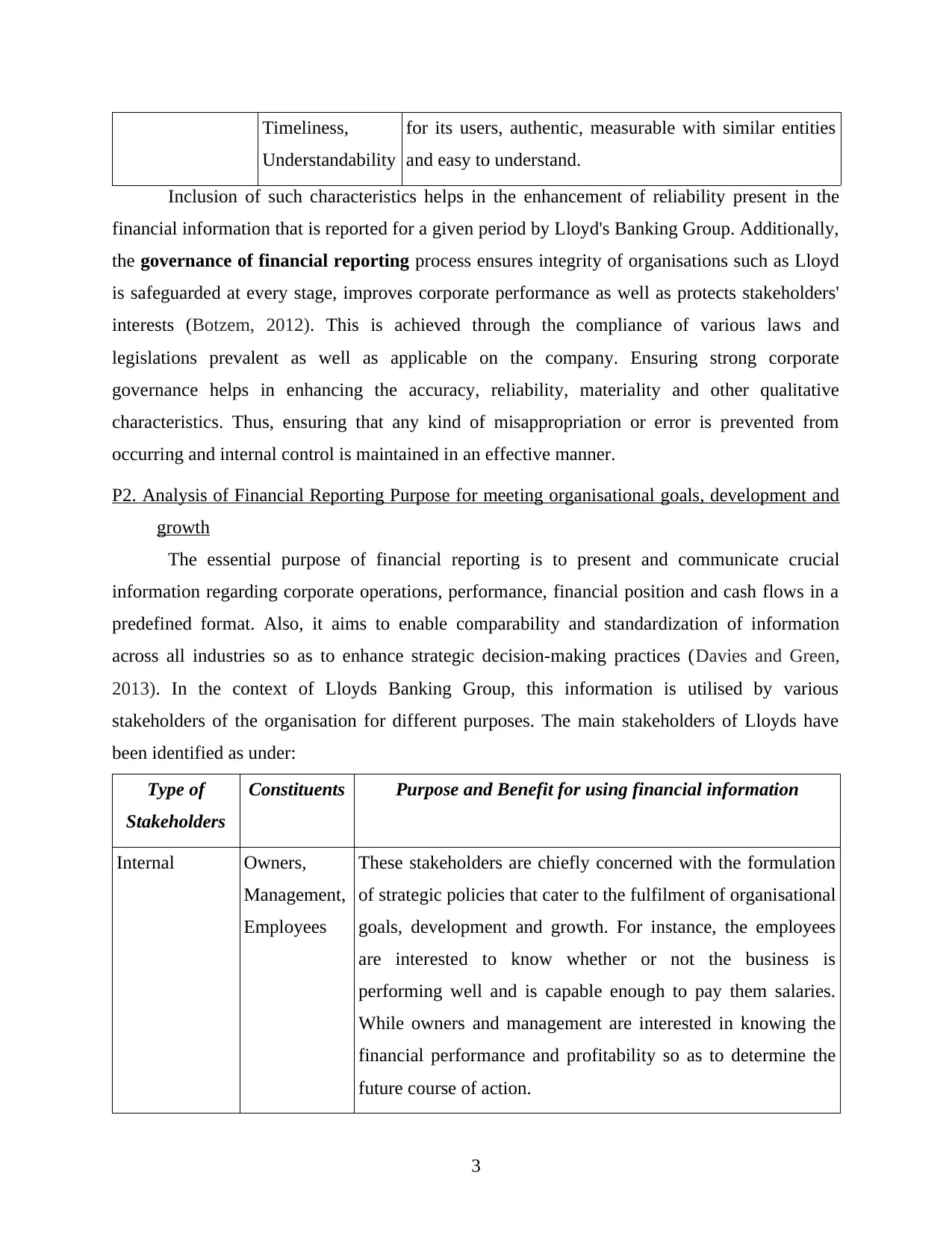

Type Components Description

Fundamental Relevance,

Faithful

representation

These characteristics imply that the financial information

is material, conforms to legal guidelines, free of errors,

complete and neutral.

Enhancing Comparability,

Verifiability,

These characteristics imply that the financial information

is capable of promoting timely decision-making practices

2

(GAAP). These principles act as a measuring yardstick as well as point of references in order to

compare and improvise current accounting practices of a company. Lack of such a framework

can lead to a substantial increase in proliferation as well as number of accounting scandals

through misappropriation of profits. Thus, conceptual framework assists in:

Development of future standards;

Promoting coherence between accounting regulations as well as standards;

Preparation and Communication of Financial Statements to the identified key

stakeholders.

Regulatory Framework:

As the name suggests, the regulatory framework determines the manner in which

reporting of financial information is carried out among organisation on a worldwide scale. For

this purpose, International Financial Reporting Standards (IFRS) is one such body which aims to

encourage collaboration, investor engagement and transparency in due process (Albu and Albu,

2012). This framework is necessary for ensuring that the communication of relevant information

to Lloyd's key stakeholders is made in such a way that their needs are fulfilled adequately. Some

of the most important IFRS are as follows:

IFRS 1: First- time Adoption of International Financial Reporting Standards

IFRS 10: Consolidated Financial Statements

IFRS 12: Disclosure of Interest in Other Entities

IFRS 13: Fair Value Measurement

The main purpose of conceptual framework is to facilitate understanding and revision of

both GAAP as well as IFRS. On the other hand, the qualitative characteristics of financial

information can be divided as:

Type Components Description

Fundamental Relevance,

Faithful

representation

These characteristics imply that the financial information

is material, conforms to legal guidelines, free of errors,

complete and neutral.

Enhancing Comparability,

Verifiability,

These characteristics imply that the financial information

is capable of promoting timely decision-making practices

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Timeliness,

Understandability

for its users, authentic, measurable with similar entities

and easy to understand.

Inclusion of such characteristics helps in the enhancement of reliability present in the

financial information that is reported for a given period by Lloyd's Banking Group. Additionally,

the governance of financial reporting process ensures integrity of organisations such as Lloyd

is safeguarded at every stage, improves corporate performance as well as protects stakeholders'

interests (Botzem, 2012). This is achieved through the compliance of various laws and

legislations prevalent as well as applicable on the company. Ensuring strong corporate

governance helps in enhancing the accuracy, reliability, materiality and other qualitative

characteristics. Thus, ensuring that any kind of misappropriation or error is prevented from

occurring and internal control is maintained in an effective manner.

P2. Analysis of Financial Reporting Purpose for meeting organisational goals, development and

growth

The essential purpose of financial reporting is to present and communicate crucial

information regarding corporate operations, performance, financial position and cash flows in a

predefined format. Also, it aims to enable comparability and standardization of information

across all industries so as to enhance strategic decision-making practices (Davies and Green,

2013). In the context of Lloyds Banking Group, this information is utilised by various

stakeholders of the organisation for different purposes. The main stakeholders of Lloyds have

been identified as under:

Type of

Stakeholders

Constituents Purpose and Benefit for using financial information

Internal Owners,

Management,

Employees

These stakeholders are chiefly concerned with the formulation

of strategic policies that cater to the fulfilment of organisational

goals, development and growth. For instance, the employees

are interested to know whether or not the business is

performing well and is capable enough to pay them salaries.

While owners and management are interested in knowing the

financial performance and profitability so as to determine the

future course of action.

3

Understandability

for its users, authentic, measurable with similar entities

and easy to understand.

Inclusion of such characteristics helps in the enhancement of reliability present in the

financial information that is reported for a given period by Lloyd's Banking Group. Additionally,

the governance of financial reporting process ensures integrity of organisations such as Lloyd

is safeguarded at every stage, improves corporate performance as well as protects stakeholders'

interests (Botzem, 2012). This is achieved through the compliance of various laws and

legislations prevalent as well as applicable on the company. Ensuring strong corporate

governance helps in enhancing the accuracy, reliability, materiality and other qualitative

characteristics. Thus, ensuring that any kind of misappropriation or error is prevented from

occurring and internal control is maintained in an effective manner.

P2. Analysis of Financial Reporting Purpose for meeting organisational goals, development and

growth

The essential purpose of financial reporting is to present and communicate crucial

information regarding corporate operations, performance, financial position and cash flows in a

predefined format. Also, it aims to enable comparability and standardization of information

across all industries so as to enhance strategic decision-making practices (Davies and Green,

2013). In the context of Lloyds Banking Group, this information is utilised by various

stakeholders of the organisation for different purposes. The main stakeholders of Lloyds have

been identified as under:

Type of

Stakeholders

Constituents Purpose and Benefit for using financial information

Internal Owners,

Management,

Employees

These stakeholders are chiefly concerned with the formulation

of strategic policies that cater to the fulfilment of organisational

goals, development and growth. For instance, the employees

are interested to know whether or not the business is

performing well and is capable enough to pay them salaries.

While owners and management are interested in knowing the

financial performance and profitability so as to determine the

future course of action.

3

External Government,

Creditors &

Suppliers,

Competitors,

Customers

These users of financial information are interested in knowing

whether or not Lloyds Bank is:

Complying with legal guidelines in its operations

(Government);

Capable enough to repay its liabilities within the

stipulated time (Creditors & Suppliers);

Analyse the strategies and future plans of the bank so as

to compete effectively (Competitors);

Profitable enough to give higher return in form of

interest to the account holders (Customers).

In order to ensure that such needs are met in full, Lloyds need to take care of all

stakeholder requirements while preparing the financial reports. Additionally, the bank also needs

to keep in mind that the communication of information is done with due diligence and

transparently as it will enable them to seek investment or funding, formulate future plans or goals

and achieve their vision in an organised manner.

TASK 2

P3. Interpretation of Profit & Loss, Cash Flow and Balance Sheet Statements

(a) Income Statement:

GODWIN PLC.

Statement of Profit and Loss for the year ended December 31, 2018

Particulars £'000

Revenue 585100

Rental Income from Investment Properties 9600

Total Revenue 594700

Less: Cost of Sales(WN2) 403638.75

Earnings before interest and tax 191061.25

Less: Operating Expenses(WN3) 92138.75

4

Creditors &

Suppliers,

Competitors,

Customers

These users of financial information are interested in knowing

whether or not Lloyds Bank is:

Complying with legal guidelines in its operations

(Government);

Capable enough to repay its liabilities within the

stipulated time (Creditors & Suppliers);

Analyse the strategies and future plans of the bank so as

to compete effectively (Competitors);

Profitable enough to give higher return in form of

interest to the account holders (Customers).

In order to ensure that such needs are met in full, Lloyds need to take care of all

stakeholder requirements while preparing the financial reports. Additionally, the bank also needs

to keep in mind that the communication of information is done with due diligence and

transparently as it will enable them to seek investment or funding, formulate future plans or goals

and achieve their vision in an organised manner.

TASK 2

P3. Interpretation of Profit & Loss, Cash Flow and Balance Sheet Statements

(a) Income Statement:

GODWIN PLC.

Statement of Profit and Loss for the year ended December 31, 2018

Particulars £'000

Revenue 585100

Rental Income from Investment Properties 9600

Total Revenue 594700

Less: Cost of Sales(WN2) 403638.75

Earnings before interest and tax 191061.25

Less: Operating Expenses(WN3) 92138.75

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

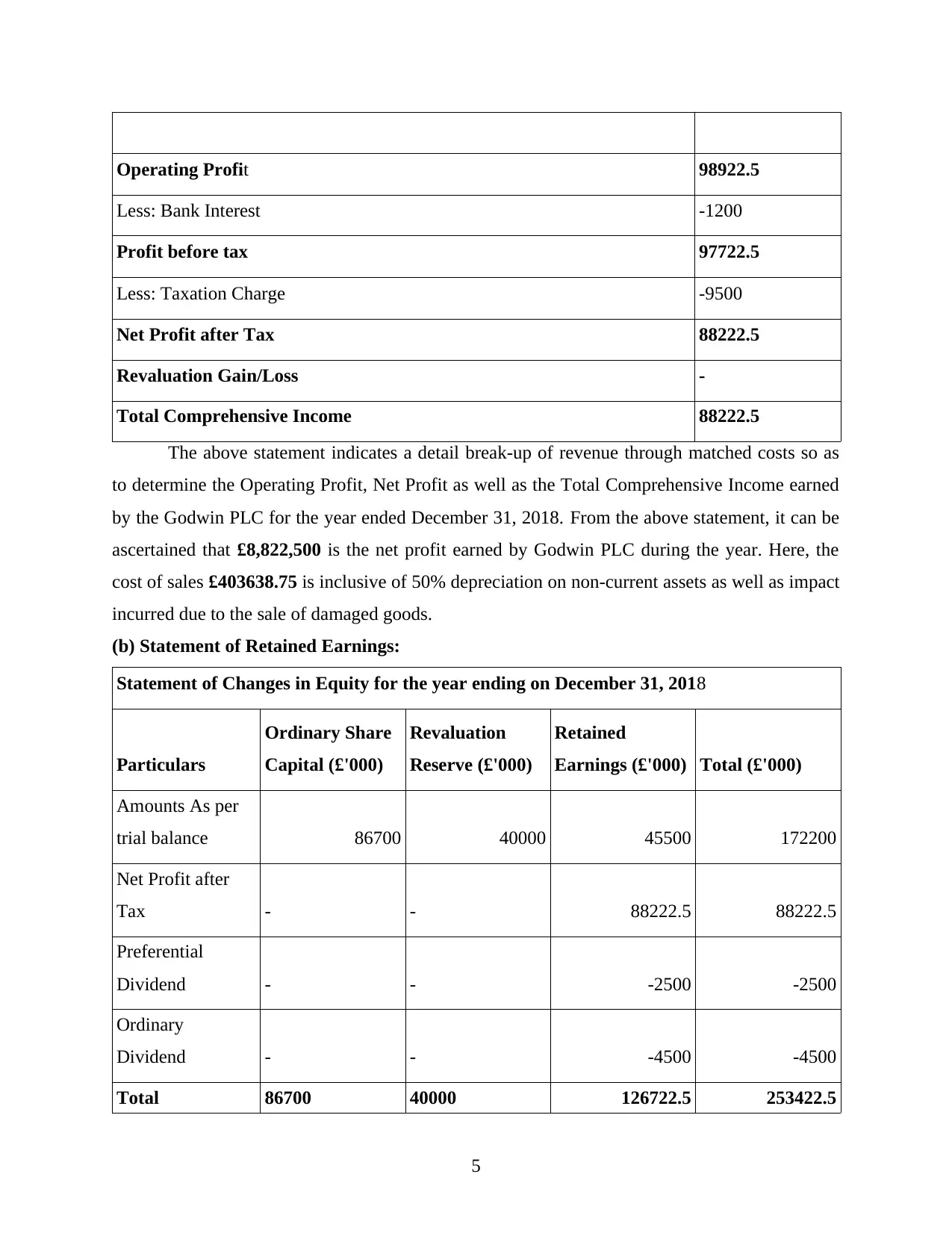

Operating Profit 98922.5

Less: Bank Interest -1200

Profit before tax 97722.5

Less: Taxation Charge -9500

Net Profit after Tax 88222.5

Revaluation Gain/Loss -

Total Comprehensive Income 88222.5

The above statement indicates a detail break-up of revenue through matched costs so as

to determine the Operating Profit, Net Profit as well as the Total Comprehensive Income earned

by the Godwin PLC for the year ended December 31, 2018. From the above statement, it can be

ascertained that £8,822,500 is the net profit earned by Godwin PLC during the year. Here, the

cost of sales £403638.75 is inclusive of 50% depreciation on non-current assets as well as impact

incurred due to the sale of damaged goods.

(b) Statement of Retained Earnings:

Statement of Changes in Equity for the year ending on December 31, 2018

Particulars

Ordinary Share

Capital (£'000)

Revaluation

Reserve (£'000)

Retained

Earnings (£'000) Total (£'000)

Amounts As per

trial balance 86700 40000 45500 172200

Net Profit after

Tax - - 88222.5 88222.5

Preferential

Dividend - - -2500 -2500

Ordinary

Dividend - - -4500 -4500

Total 86700 40000 126722.5 253422.5

5

Less: Bank Interest -1200

Profit before tax 97722.5

Less: Taxation Charge -9500

Net Profit after Tax 88222.5

Revaluation Gain/Loss -

Total Comprehensive Income 88222.5

The above statement indicates a detail break-up of revenue through matched costs so as

to determine the Operating Profit, Net Profit as well as the Total Comprehensive Income earned

by the Godwin PLC for the year ended December 31, 2018. From the above statement, it can be

ascertained that £8,822,500 is the net profit earned by Godwin PLC during the year. Here, the

cost of sales £403638.75 is inclusive of 50% depreciation on non-current assets as well as impact

incurred due to the sale of damaged goods.

(b) Statement of Retained Earnings:

Statement of Changes in Equity for the year ending on December 31, 2018

Particulars

Ordinary Share

Capital (£'000)

Revaluation

Reserve (£'000)

Retained

Earnings (£'000) Total (£'000)

Amounts As per

trial balance 86700 40000 45500 172200

Net Profit after

Tax - - 88222.5 88222.5

Preferential

Dividend - - -2500 -2500

Ordinary

Dividend - - -4500 -4500

Total 86700 40000 126722.5 253422.5

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

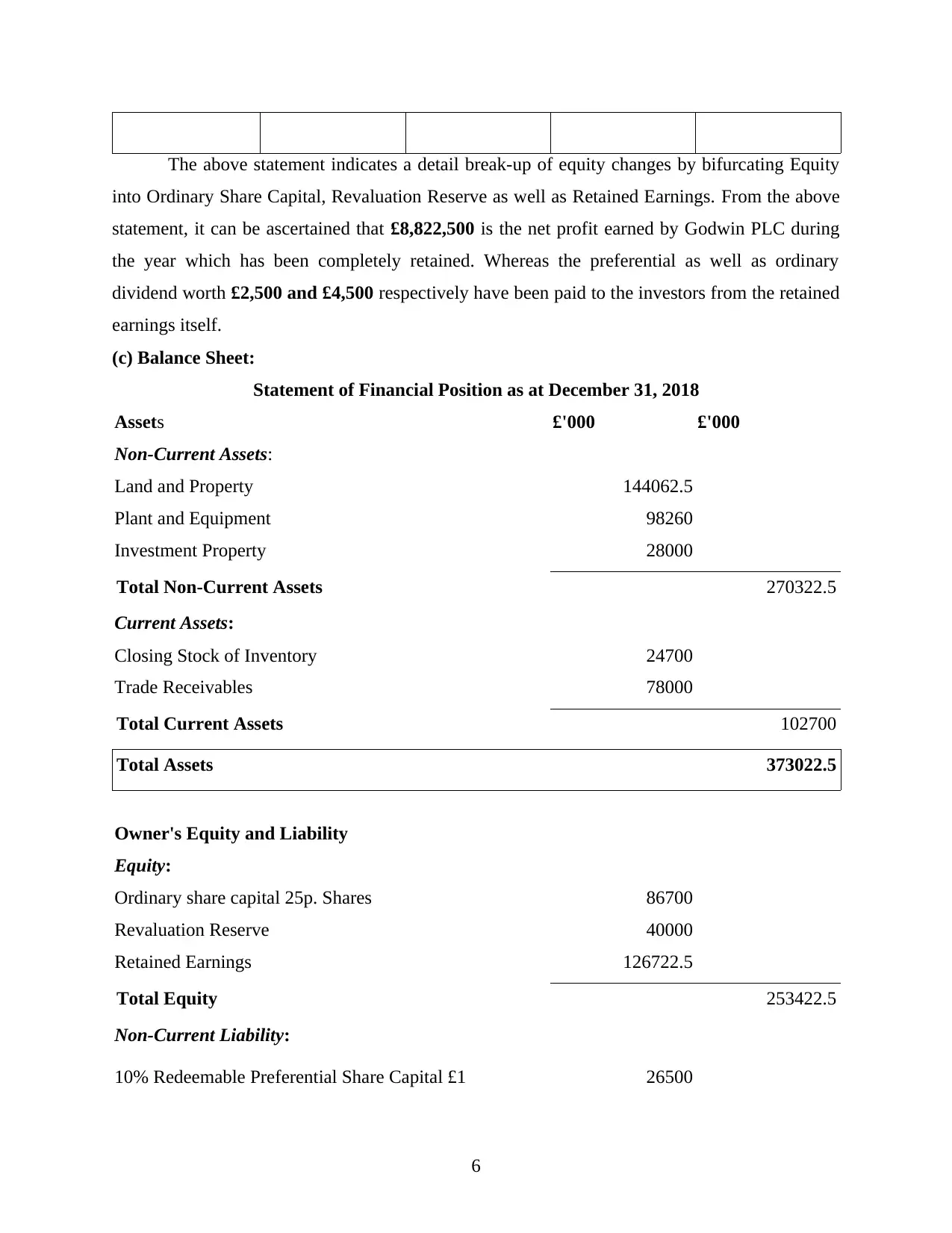

The above statement indicates a detail break-up of equity changes by bifurcating Equity

into Ordinary Share Capital, Revaluation Reserve as well as Retained Earnings. From the above

statement, it can be ascertained that £8,822,500 is the net profit earned by Godwin PLC during

the year which has been completely retained. Whereas the preferential as well as ordinary

dividend worth £2,500 and £4,500 respectively have been paid to the investors from the retained

earnings itself.

(c) Balance Sheet:

Statement of Financial Position as at December 31, 2018

Assets £'000 £'000

Non-Current Assets:

Land and Property 144062.5

Plant and Equipment 98260

Investment Property 28000

Total Non-Current Assets 270322.5

Current Assets:

Closing Stock of Inventory 24700

Trade Receivables 78000

Total Current Assets 102700

Total Assets 373022.5

Owner's Equity and Liability

Equity:

Ordinary share capital 25p. Shares 86700

Revaluation Reserve 40000

Retained Earnings 126722.5

Total Equity 253422.5

Non-Current Liability:

10% Redeemable Preferential Share Capital £1 26500

6

into Ordinary Share Capital, Revaluation Reserve as well as Retained Earnings. From the above

statement, it can be ascertained that £8,822,500 is the net profit earned by Godwin PLC during

the year which has been completely retained. Whereas the preferential as well as ordinary

dividend worth £2,500 and £4,500 respectively have been paid to the investors from the retained

earnings itself.

(c) Balance Sheet:

Statement of Financial Position as at December 31, 2018

Assets £'000 £'000

Non-Current Assets:

Land and Property 144062.5

Plant and Equipment 98260

Investment Property 28000

Total Non-Current Assets 270322.5

Current Assets:

Closing Stock of Inventory 24700

Trade Receivables 78000

Total Current Assets 102700

Total Assets 373022.5

Owner's Equity and Liability

Equity:

Ordinary share capital 25p. Shares 86700

Revaluation Reserve 40000

Retained Earnings 126722.5

Total Equity 253422.5

Non-Current Liability:

10% Redeemable Preferential Share Capital £1 26500

6

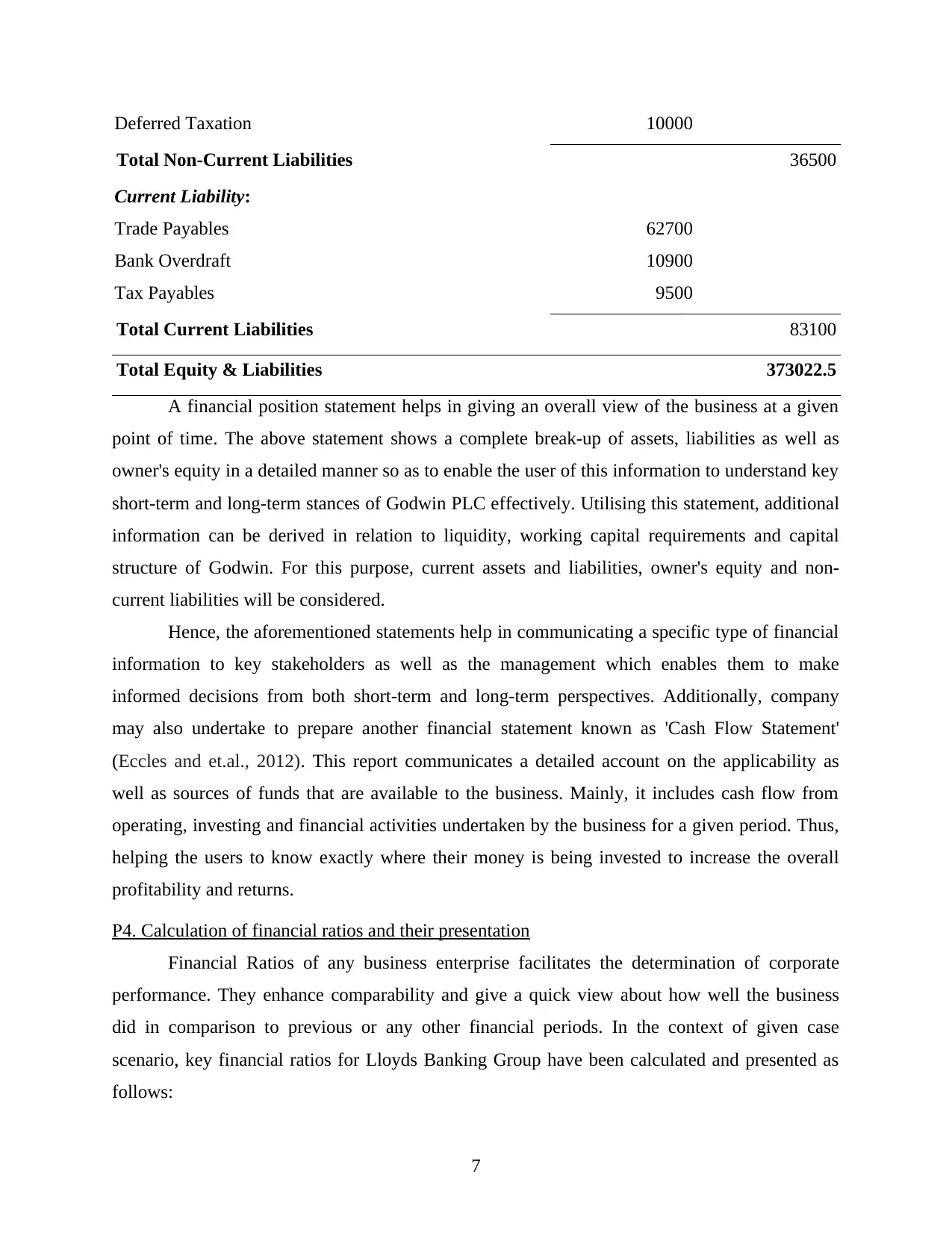

Deferred Taxation 10000

Total Non-Current Liabilities 36500

Current Liability:

Trade Payables 62700

Bank Overdraft 10900

Tax Payables 9500

Total Current Liabilities 83100

Total Equity & Liabilities 373022.5

A financial position statement helps in giving an overall view of the business at a given

point of time. The above statement shows a complete break-up of assets, liabilities as well as

owner's equity in a detailed manner so as to enable the user of this information to understand key

short-term and long-term stances of Godwin PLC effectively. Utilising this statement, additional

information can be derived in relation to liquidity, working capital requirements and capital

structure of Godwin. For this purpose, current assets and liabilities, owner's equity and non-

current liabilities will be considered.

Hence, the aforementioned statements help in communicating a specific type of financial

information to key stakeholders as well as the management which enables them to make

informed decisions from both short-term and long-term perspectives. Additionally, company

may also undertake to prepare another financial statement known as 'Cash Flow Statement'

(Eccles and et.al., 2012). This report communicates a detailed account on the applicability as

well as sources of funds that are available to the business. Mainly, it includes cash flow from

operating, investing and financial activities undertaken by the business for a given period. Thus,

helping the users to know exactly where their money is being invested to increase the overall

profitability and returns.

P4. Calculation of financial ratios and their presentation

Financial Ratios of any business enterprise facilitates the determination of corporate

performance. They enhance comparability and give a quick view about how well the business

did in comparison to previous or any other financial periods. In the context of given case

scenario, key financial ratios for Lloyds Banking Group have been calculated and presented as

follows:

7

Total Non-Current Liabilities 36500

Current Liability:

Trade Payables 62700

Bank Overdraft 10900

Tax Payables 9500

Total Current Liabilities 83100

Total Equity & Liabilities 373022.5

A financial position statement helps in giving an overall view of the business at a given

point of time. The above statement shows a complete break-up of assets, liabilities as well as

owner's equity in a detailed manner so as to enable the user of this information to understand key

short-term and long-term stances of Godwin PLC effectively. Utilising this statement, additional

information can be derived in relation to liquidity, working capital requirements and capital

structure of Godwin. For this purpose, current assets and liabilities, owner's equity and non-

current liabilities will be considered.

Hence, the aforementioned statements help in communicating a specific type of financial

information to key stakeholders as well as the management which enables them to make

informed decisions from both short-term and long-term perspectives. Additionally, company

may also undertake to prepare another financial statement known as 'Cash Flow Statement'

(Eccles and et.al., 2012). This report communicates a detailed account on the applicability as

well as sources of funds that are available to the business. Mainly, it includes cash flow from

operating, investing and financial activities undertaken by the business for a given period. Thus,

helping the users to know exactly where their money is being invested to increase the overall

profitability and returns.

P4. Calculation of financial ratios and their presentation

Financial Ratios of any business enterprise facilitates the determination of corporate

performance. They enhance comparability and give a quick view about how well the business

did in comparison to previous or any other financial periods. In the context of given case

scenario, key financial ratios for Lloyds Banking Group have been calculated and presented as

follows:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

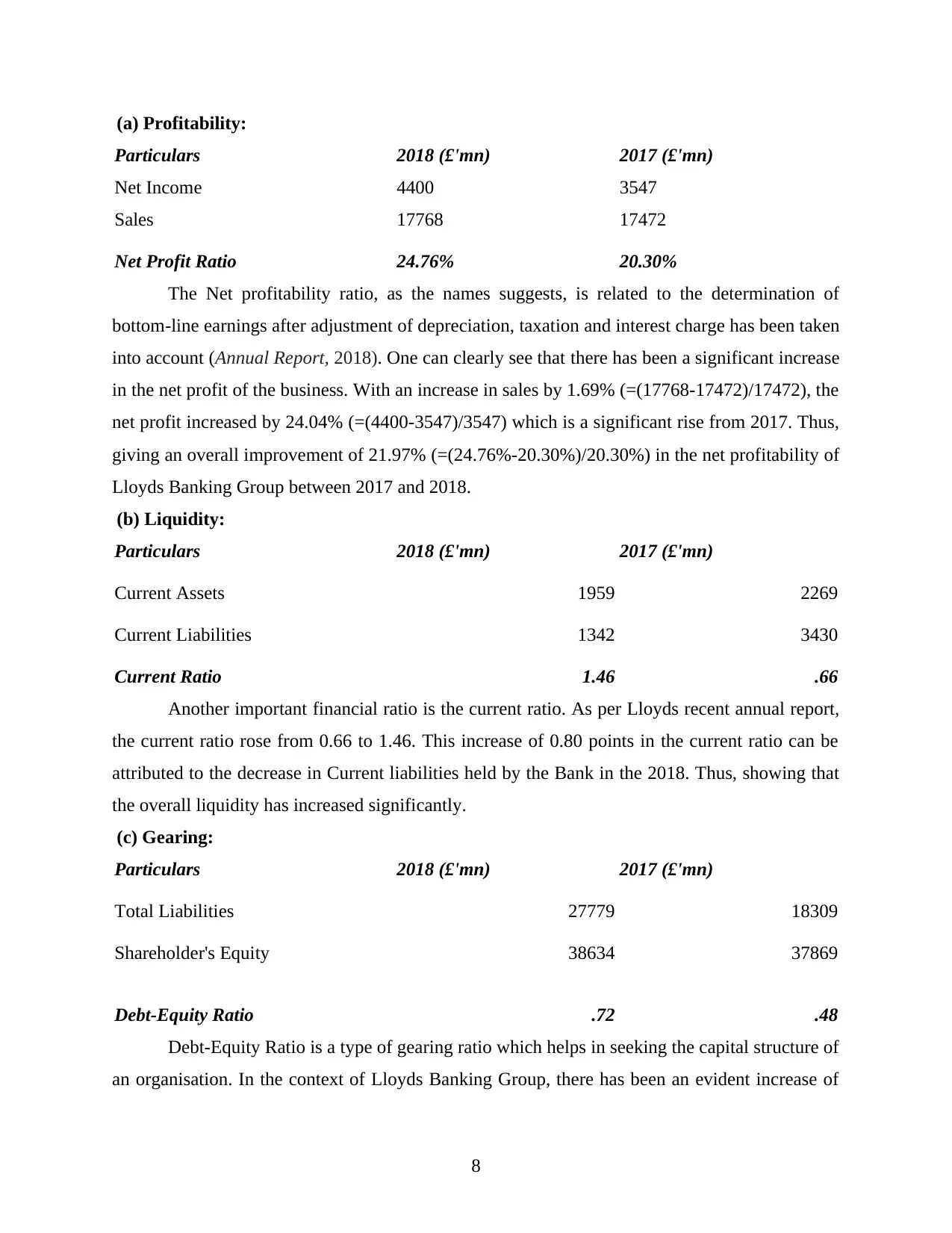

(a) Profitability:

Particulars 2018 (£'mn) 2017 (£'mn)

Net Income 4400 3547

Sales 17768 17472

Net Profit Ratio 24.76% 20.30%

The Net profitability ratio, as the names suggests, is related to the determination of

bottom-line earnings after adjustment of depreciation, taxation and interest charge has been taken

into account (Annual Report, 2018). One can clearly see that there has been a significant increase

in the net profit of the business. With an increase in sales by 1.69% (=(17768-17472)/17472), the

net profit increased by 24.04% (=(4400-3547)/3547) which is a significant rise from 2017. Thus,

giving an overall improvement of 21.97% (=(24.76%-20.30%)/20.30%) in the net profitability of

Lloyds Banking Group between 2017 and 2018.

(b) Liquidity:

Particulars 2018 (£'mn) 2017 (£'mn)

Current Assets 1959 2269

Current Liabilities 1342 3430

Current Ratio 1.46 .66

Another important financial ratio is the current ratio. As per Lloyds recent annual report,

the current ratio rose from 0.66 to 1.46. This increase of 0.80 points in the current ratio can be

attributed to the decrease in Current liabilities held by the Bank in the 2018. Thus, showing that

the overall liquidity has increased significantly.

(c) Gearing:

Particulars 2018 (£'mn) 2017 (£'mn)

Total Liabilities 27779 18309

Shareholder's Equity 38634 37869

Debt-Equity Ratio .72 .48

Debt-Equity Ratio is a type of gearing ratio which helps in seeking the capital structure of

an organisation. In the context of Lloyds Banking Group, there has been an evident increase of

8

Particulars 2018 (£'mn) 2017 (£'mn)

Net Income 4400 3547

Sales 17768 17472

Net Profit Ratio 24.76% 20.30%

The Net profitability ratio, as the names suggests, is related to the determination of

bottom-line earnings after adjustment of depreciation, taxation and interest charge has been taken

into account (Annual Report, 2018). One can clearly see that there has been a significant increase

in the net profit of the business. With an increase in sales by 1.69% (=(17768-17472)/17472), the

net profit increased by 24.04% (=(4400-3547)/3547) which is a significant rise from 2017. Thus,

giving an overall improvement of 21.97% (=(24.76%-20.30%)/20.30%) in the net profitability of

Lloyds Banking Group between 2017 and 2018.

(b) Liquidity:

Particulars 2018 (£'mn) 2017 (£'mn)

Current Assets 1959 2269

Current Liabilities 1342 3430

Current Ratio 1.46 .66

Another important financial ratio is the current ratio. As per Lloyds recent annual report,

the current ratio rose from 0.66 to 1.46. This increase of 0.80 points in the current ratio can be

attributed to the decrease in Current liabilities held by the Bank in the 2018. Thus, showing that

the overall liquidity has increased significantly.

(c) Gearing:

Particulars 2018 (£'mn) 2017 (£'mn)

Total Liabilities 27779 18309

Shareholder's Equity 38634 37869

Debt-Equity Ratio .72 .48

Debt-Equity Ratio is a type of gearing ratio which helps in seeking the capital structure of

an organisation. In the context of Lloyds Banking Group, there has been an evident increase of

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

51.72% (=(27779-18309)/27779) in total liabilities. Thus, improving the Debt-Equity Ratio by

0.24 points for the Bank. This indicates that the company has become more reliant on external

financing in comparison to 2017. Thus, increasing its overall financial leverage.

One can conclude that all these ratios are used to interpret and communicate financial

performance of Lloyds Banking Group by addressing specific areas such as leverage,

profitability and liquidity that are relevant in effective measurement of its overall corporate

performance (Ikpefan and Akande, 2012).

TASK 3

P5. Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS)

International Financial Reporting aims to inculcate standardization and create the

communication of important financial information as a global language that can be understood

by anyone all around the world. In this context, it is paramount to consider the Accounting

Standards (IAS) that ensure generalization of treatment regarding financial items as well as

Financial Reporting Standards (IFRS) which helps in their effective communication to various

stakeholders.

The main difference between these two components has been depicted in the following

table:

Basis of

Differentiation

International Accounting Standards

(IAS)

International Financial Reporting

Standards (IFRS)

Definition These can be defined as a set of

globally agreed standard principles

and procedures which govern how the

companies present as well as

communicate financial information to

their international clients (Leuz and

Wysocki, 2016).

Such standards are referred to those

guidelines which have been developed

to promote a common accounting

language worldwide, specifically in

relation to the presentation and

communication of company accounts

to various stakeholders.

Issuing

Authority

International Accounting Standards

Committee (IASC)

International Accounting Standards

Board (IASB)

9

0.24 points for the Bank. This indicates that the company has become more reliant on external

financing in comparison to 2017. Thus, increasing its overall financial leverage.

One can conclude that all these ratios are used to interpret and communicate financial

performance of Lloyds Banking Group by addressing specific areas such as leverage,

profitability and liquidity that are relevant in effective measurement of its overall corporate

performance (Ikpefan and Akande, 2012).

TASK 3

P5. Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS)

International Financial Reporting aims to inculcate standardization and create the

communication of important financial information as a global language that can be understood

by anyone all around the world. In this context, it is paramount to consider the Accounting

Standards (IAS) that ensure generalization of treatment regarding financial items as well as

Financial Reporting Standards (IFRS) which helps in their effective communication to various

stakeholders.

The main difference between these two components has been depicted in the following

table:

Basis of

Differentiation

International Accounting Standards

(IAS)

International Financial Reporting

Standards (IFRS)

Definition These can be defined as a set of

globally agreed standard principles

and procedures which govern how the

companies present as well as

communicate financial information to

their international clients (Leuz and

Wysocki, 2016).

Such standards are referred to those

guidelines which have been developed

to promote a common accounting

language worldwide, specifically in

relation to the presentation and

communication of company accounts

to various stakeholders.

Issuing

Authority

International Accounting Standards

Committee (IASC)

International Accounting Standards

Board (IASB)

9

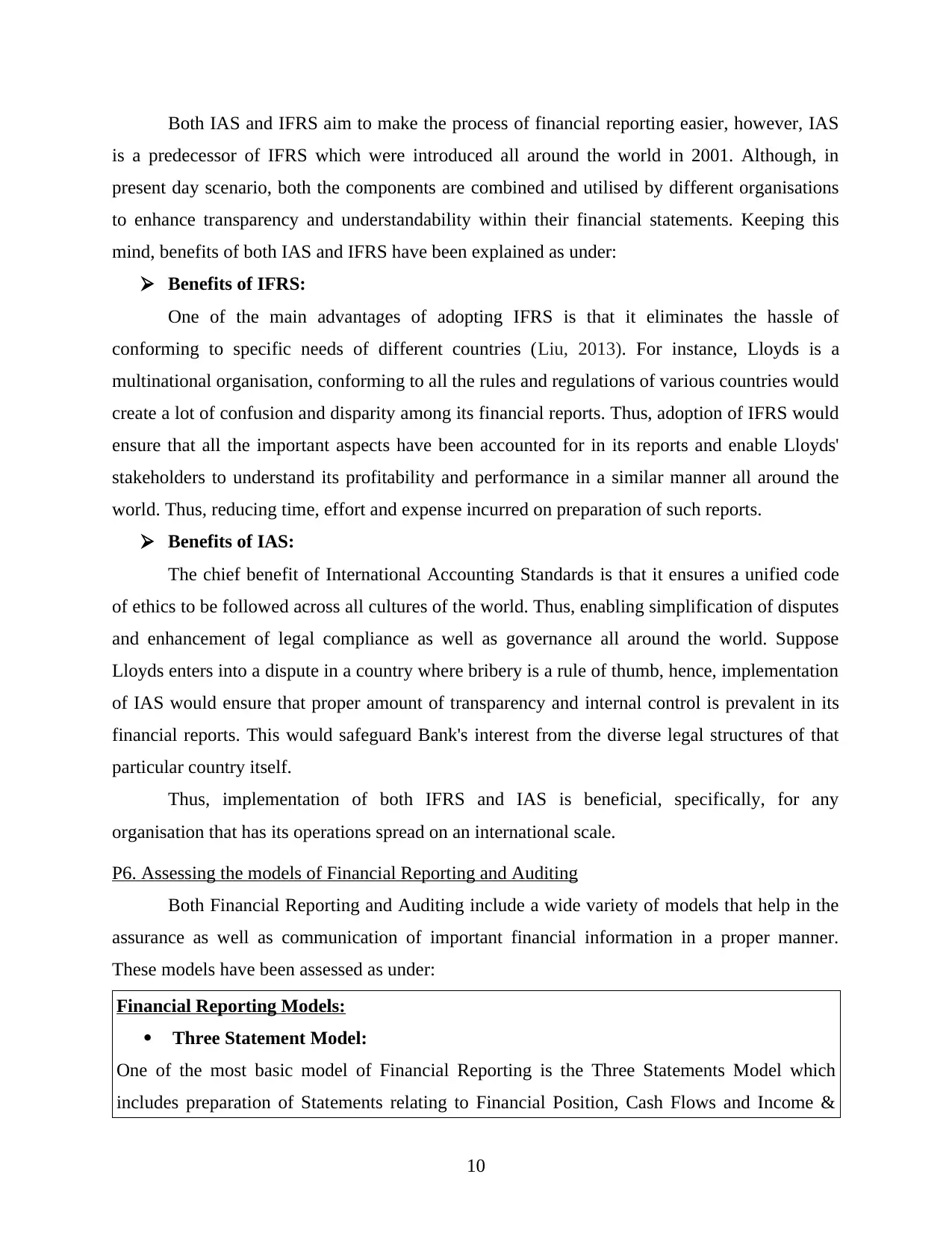

Both IAS and IFRS aim to make the process of financial reporting easier, however, IAS

is a predecessor of IFRS which were introduced all around the world in 2001. Although, in

present day scenario, both the components are combined and utilised by different organisations

to enhance transparency and understandability within their financial statements. Keeping this

mind, benefits of both IAS and IFRS have been explained as under:

Benefits of IFRS:

One of the main advantages of adopting IFRS is that it eliminates the hassle of

conforming to specific needs of different countries (Liu, 2013). For instance, Lloyds is a

multinational organisation, conforming to all the rules and regulations of various countries would

create a lot of confusion and disparity among its financial reports. Thus, adoption of IFRS would

ensure that all the important aspects have been accounted for in its reports and enable Lloyds'

stakeholders to understand its profitability and performance in a similar manner all around the

world. Thus, reducing time, effort and expense incurred on preparation of such reports.

Benefits of IAS:

The chief benefit of International Accounting Standards is that it ensures a unified code

of ethics to be followed across all cultures of the world. Thus, enabling simplification of disputes

and enhancement of legal compliance as well as governance all around the world. Suppose

Lloyds enters into a dispute in a country where bribery is a rule of thumb, hence, implementation

of IAS would ensure that proper amount of transparency and internal control is prevalent in its

financial reports. This would safeguard Bank's interest from the diverse legal structures of that

particular country itself.

Thus, implementation of both IFRS and IAS is beneficial, specifically, for any

organisation that has its operations spread on an international scale.

P6. Assessing the models of Financial Reporting and Auditing

Both Financial Reporting and Auditing include a wide variety of models that help in the

assurance as well as communication of important financial information in a proper manner.

These models have been assessed as under:

Financial Reporting Models:

Three Statement Model:

One of the most basic model of Financial Reporting is the Three Statements Model which

includes preparation of Statements relating to Financial Position, Cash Flows and Income &

10

is a predecessor of IFRS which were introduced all around the world in 2001. Although, in

present day scenario, both the components are combined and utilised by different organisations

to enhance transparency and understandability within their financial statements. Keeping this

mind, benefits of both IAS and IFRS have been explained as under:

Benefits of IFRS:

One of the main advantages of adopting IFRS is that it eliminates the hassle of

conforming to specific needs of different countries (Liu, 2013). For instance, Lloyds is a

multinational organisation, conforming to all the rules and regulations of various countries would

create a lot of confusion and disparity among its financial reports. Thus, adoption of IFRS would

ensure that all the important aspects have been accounted for in its reports and enable Lloyds'

stakeholders to understand its profitability and performance in a similar manner all around the

world. Thus, reducing time, effort and expense incurred on preparation of such reports.

Benefits of IAS:

The chief benefit of International Accounting Standards is that it ensures a unified code

of ethics to be followed across all cultures of the world. Thus, enabling simplification of disputes

and enhancement of legal compliance as well as governance all around the world. Suppose

Lloyds enters into a dispute in a country where bribery is a rule of thumb, hence, implementation

of IAS would ensure that proper amount of transparency and internal control is prevalent in its

financial reports. This would safeguard Bank's interest from the diverse legal structures of that

particular country itself.

Thus, implementation of both IFRS and IAS is beneficial, specifically, for any

organisation that has its operations spread on an international scale.

P6. Assessing the models of Financial Reporting and Auditing

Both Financial Reporting and Auditing include a wide variety of models that help in the

assurance as well as communication of important financial information in a proper manner.

These models have been assessed as under:

Financial Reporting Models:

Three Statement Model:

One of the most basic model of Financial Reporting is the Three Statements Model which

includes preparation of Statements relating to Financial Position, Cash Flows and Income &

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.