Principles of Accounting: Financial Reporting Homework Assignment

VerifiedAdded on 2023/05/30

|7

|1367

|422

Homework Assignment

AI Summary

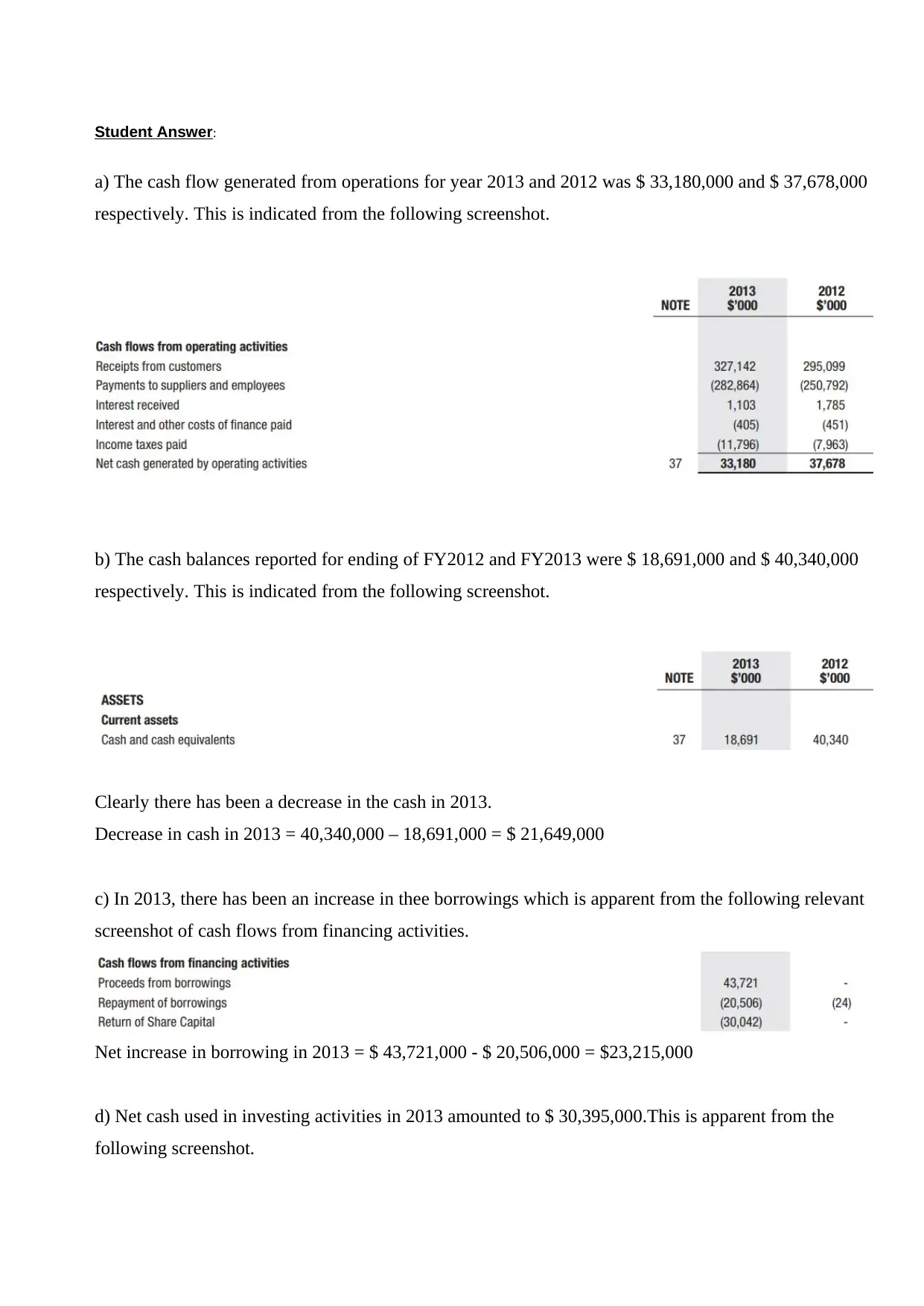

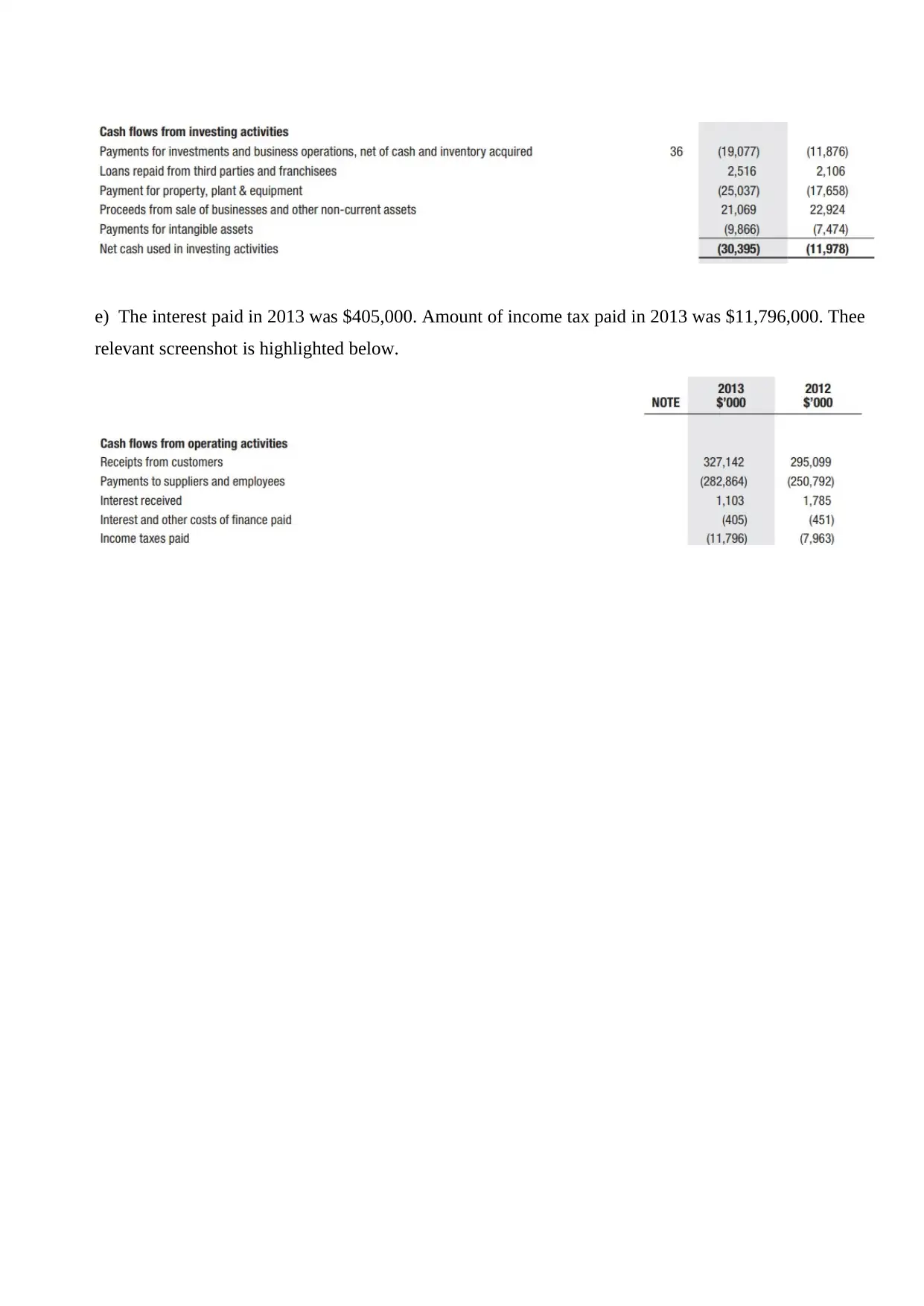

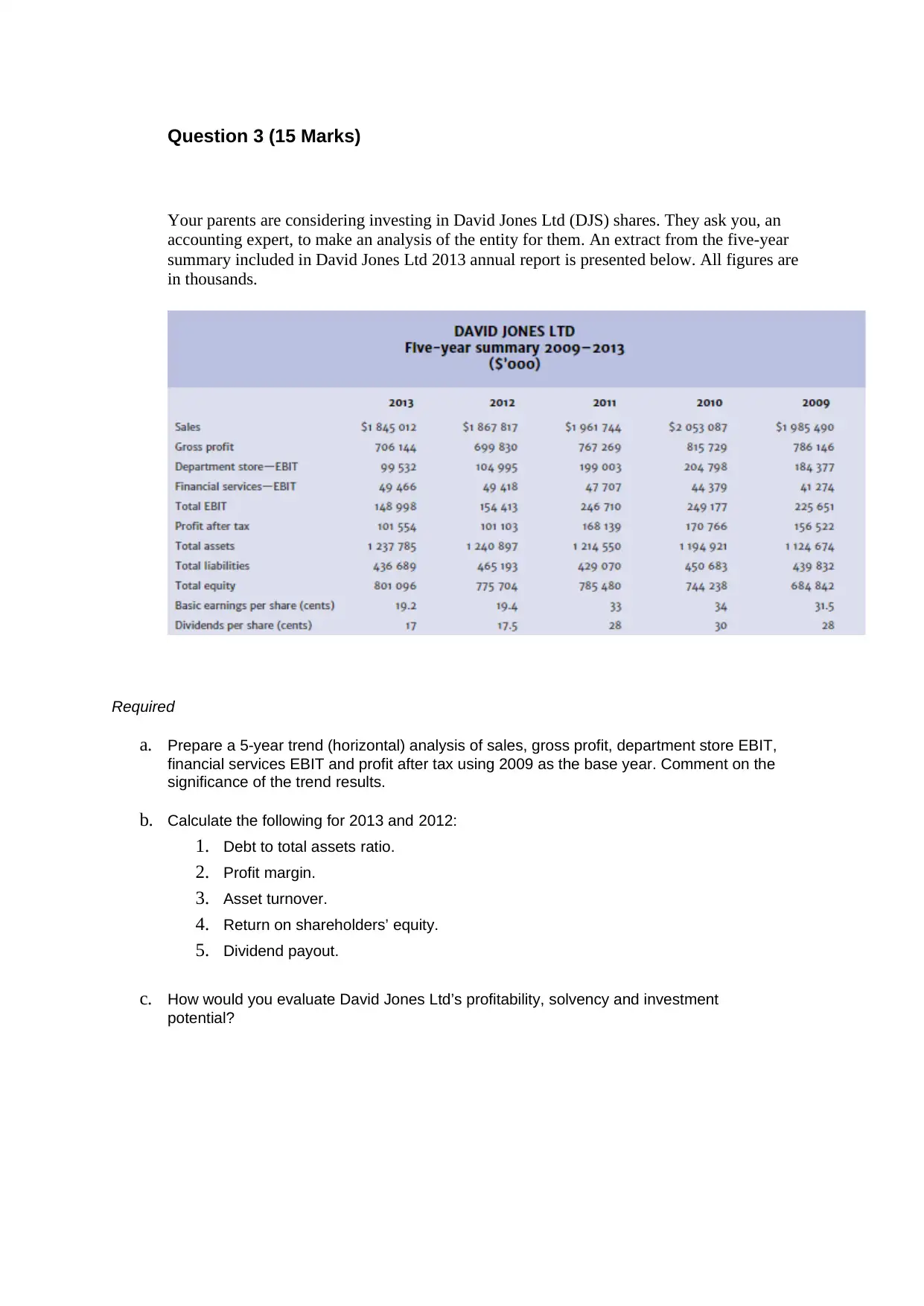

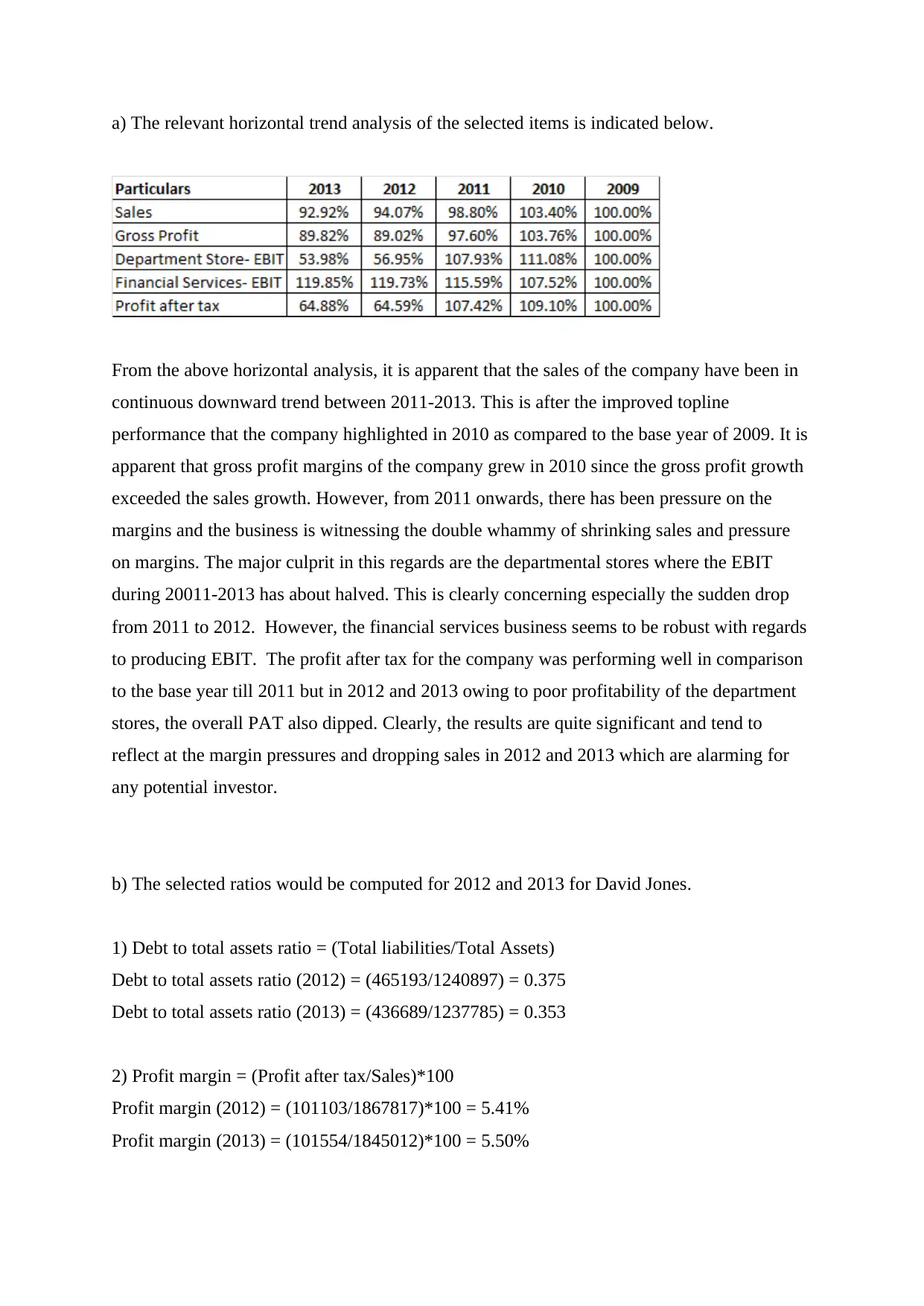

This homework assignment analyzes the financial statements of Domino's Pizza Enterprises Ltd and David Jones Ltd. The first part focuses on Domino's, requiring the calculation of net cash flow from operating activities, changes in cash, changes in borrowings, cash used for investing activities, and interest and income tax paid, based on the 2013 and 2012 financial statements. The second part involves a five-year trend analysis of David Jones' sales, gross profit, EBIT, and profit after tax, followed by the calculation of key financial ratios such as debt to total assets, profit margin, asset turnover, return on equity, and dividend payout. The assignment concludes with an evaluation of David Jones' profitability, solvency, and investment potential, providing insights for potential investors. The solution provides detailed calculations and interpretations of the financial data.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.