Financial Reporting Analysis: Objectives, Standards, and Statements

VerifiedAdded on 2021/02/20

|15

|4303

|39

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, beginning with its context and purpose, and then delving into the conceptual and regulatory frameworks, principles, and qualitative characteristics. It examines various stakeholders and the benefits they derive from financial information, and how financial reports are used to meet organizational growth and objectives. The report includes the presentation of financial statements, such as the profit and loss account, statement of changes in equity, and statement of financial position, along with working notes. It also covers the interpretation of financial statements of a FTSE 100 listed company, a comparison of International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), and the benefits and degree of compliance with IFRS across organizations worldwide. The report offers a detailed overview of financial reporting standards and their practical application.

FINANCIAL-

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTIONS...................................................................................................................................3

1. Context and purpose of financial reporting.............................................................................3

2. Conceptual, regulatory framework, principles and qualitative characteristics. ....................4

3. Different types of stakeholders and benefits which they get from financial information.......5

4. Financial reports for meeting organisational growth and objectives......................................6

5. Presentation of financial statements........................................................................................7

6. Interpretation of financial statements of a company which is listed in FTSE 100.................9

7. Comparison of international accounting standard (IAS) and international financial

reporting standard (IFRS).........................................................................................................11

8. Benefits of IFRS....................................................................................................................12

9. Degree of compliance with IFRS by organisation across the world.....................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

QUESTIONS...................................................................................................................................3

1. Context and purpose of financial reporting.............................................................................3

2. Conceptual, regulatory framework, principles and qualitative characteristics. ....................4

3. Different types of stakeholders and benefits which they get from financial information.......5

4. Financial reports for meeting organisational growth and objectives......................................6

5. Presentation of financial statements........................................................................................7

6. Interpretation of financial statements of a company which is listed in FTSE 100.................9

7. Comparison of international accounting standard (IAS) and international financial

reporting standard (IFRS).........................................................................................................11

8. Benefits of IFRS....................................................................................................................12

9. Degree of compliance with IFRS by organisation across the world.....................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

The financial reporting can be defined as a process of disclosure of financial results and

other information to the all stakeholders so that they may know about performance of company

(Perera and Chand, 2015). Basically, presentation of financial reports is very important because

there are wide range of financial activities in the businesses. In the absence of presentation of

financial reports it can be difficult for the organisations to analyse the actual financial condition.

As well as these financial reports are presented in the end of a particular time period which is

known as accounting period. Herein, the project report a large accountancy firm is selected

which is Price water coopers (PWC) company is selected. Its headquarter is in London, UK and

company deals in providing accountancy, tax and regulatory services.

In the project report, term financial-reporting is mentioned along with its purpose as well

as financial statements are prepared as per given information. Apart from it, financial-reporting

standards, models and concepts are described. In the end, difference and importance of financial-

reports is also mentioned.

QUESTIONS

1. Context and purpose of financial reporting.

Financial reporting- The term financial-reporting can be defined as a method of presenting the

financial information of company in the form of financial statements. The key objective of

producing the financial reports is to informing the stakeholders about financial position of

company. Eventually, these reports are prepared with the help of financial statements such as

profit & loss account, balance sheet, cash flow etc. Companies who prepare the financial reports

on time, helps them in building strong reputation in the external environment. The financial

reports are needed to be prepared at the end of an accounting period (Krishnan and Zhang,

2014). For example the PWC company prepares the financial reports on time so that their

external stakeholders can aware about their financial position. Along with they advice to their

other client companies to prepare the financial reports timely and as per the standards.

Objectives of financial reporting: The financial reports are very important for all who are linked

with the company's operations and activities. Herein, below some objectives are mentioned

below:

The financial reporting can be defined as a process of disclosure of financial results and

other information to the all stakeholders so that they may know about performance of company

(Perera and Chand, 2015). Basically, presentation of financial reports is very important because

there are wide range of financial activities in the businesses. In the absence of presentation of

financial reports it can be difficult for the organisations to analyse the actual financial condition.

As well as these financial reports are presented in the end of a particular time period which is

known as accounting period. Herein, the project report a large accountancy firm is selected

which is Price water coopers (PWC) company is selected. Its headquarter is in London, UK and

company deals in providing accountancy, tax and regulatory services.

In the project report, term financial-reporting is mentioned along with its purpose as well

as financial statements are prepared as per given information. Apart from it, financial-reporting

standards, models and concepts are described. In the end, difference and importance of financial-

reports is also mentioned.

QUESTIONS

1. Context and purpose of financial reporting.

Financial reporting- The term financial-reporting can be defined as a method of presenting the

financial information of company in the form of financial statements. The key objective of

producing the financial reports is to informing the stakeholders about financial position of

company. Eventually, these reports are prepared with the help of financial statements such as

profit & loss account, balance sheet, cash flow etc. Companies who prepare the financial reports

on time, helps them in building strong reputation in the external environment. The financial

reports are needed to be prepared at the end of an accounting period (Krishnan and Zhang,

2014). For example the PWC company prepares the financial reports on time so that their

external stakeholders can aware about their financial position. Along with they advice to their

other client companies to prepare the financial reports timely and as per the standards.

Objectives of financial reporting: The financial reports are very important for all who are linked

with the company's operations and activities. Herein, below some objectives are mentioned

below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

One of the key objective of financial-reports is to helping in taking important decisions

for future. This is why because financial-reports include a wide range of financial

information about company that become a basis for decision-making. Like the above

company takes the advantage of reports for futuristic decisions.

Along with the financial-reports are useful in providing information about net inflows

and outflows of cash during a particular time period. Like the above respective company

assess their liquidity position with help of financial reports.

As well as the financial reports helps in providing detailed information about total

creditors, debtors, total investment etc. With the help of it, the PWC company can track

the all financial information.

So these are the objectives of financial-reports which are helpful for all kind of companies.

2. Conceptual, regulatory framework, principles and qualitative characteristics.

Conceptual and regulatory framework: The international accounting standard board is

responsible for developing the conceptual framework (Wolfson, 2014). Basically, the concept of

financial-reporting is linked to preparation of financial reports that contains various financial

statements. As well as there are a wide range of stakeholders who are involved in the financial

activities of companies so it is essential that financial reports should be as per the accounting

standards and as per the structure.

The regulatory frameworks are useful for making forecasting for enhancing the efficiency

and effectiveness of financial statements and principles. Like in the above respective company

they implement all the frameworks in the process of financial report preparing.

Key principles: There are various kind of principles of financial reporting and some of

these are mentioned below:

Full disclosure of information- As per this principle, it is necessary for companies to

disclose all the information in the financial reports. Eventually, this is important to

include complete financial information so that stakeholders can aware about financial

position.

Consistency- As per this principle, the financial reports should be prepared continuously

year by year. This is important to prepare the financial reports on a consistence basis so

that previous financial position can be evaluated.

for future. This is why because financial-reports include a wide range of financial

information about company that become a basis for decision-making. Like the above

company takes the advantage of reports for futuristic decisions.

Along with the financial-reports are useful in providing information about net inflows

and outflows of cash during a particular time period. Like the above respective company

assess their liquidity position with help of financial reports.

As well as the financial reports helps in providing detailed information about total

creditors, debtors, total investment etc. With the help of it, the PWC company can track

the all financial information.

So these are the objectives of financial-reports which are helpful for all kind of companies.

2. Conceptual, regulatory framework, principles and qualitative characteristics.

Conceptual and regulatory framework: The international accounting standard board is

responsible for developing the conceptual framework (Wolfson, 2014). Basically, the concept of

financial-reporting is linked to preparation of financial reports that contains various financial

statements. As well as there are a wide range of stakeholders who are involved in the financial

activities of companies so it is essential that financial reports should be as per the accounting

standards and as per the structure.

The regulatory frameworks are useful for making forecasting for enhancing the efficiency

and effectiveness of financial statements and principles. Like in the above respective company

they implement all the frameworks in the process of financial report preparing.

Key principles: There are various kind of principles of financial reporting and some of

these are mentioned below:

Full disclosure of information- As per this principle, it is necessary for companies to

disclose all the information in the financial reports. Eventually, this is important to

include complete financial information so that stakeholders can aware about financial

position.

Consistency- As per this principle, the financial reports should be prepared continuously

year by year. This is important to prepare the financial reports on a consistence basis so

that previous financial position can be evaluated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

So these are the key principles of financial reports which are required to be implemented.

Qualitative features of financial reporting: Herein below some characteristics of financial reports

are mentioned below:

Relevance- This is a kind of feature of financial reports which defines that there should

be relevancy of financial reports with the business transactions (Rotimi, 2012).

Timeliness- This is mandatory that financial reports should be prepared on a timely basis

which can be yearly or quarterly.

Understandability- According to this feature, the financial reports should be

understandable for all stakeholders so that decision can be taken.

3. Different types of stakeholders and benefits which they get from financial information.

Stakeholders- In the aspect of business, the stakeholders can be government, customers,

suppliers or any other who gets effected due to the policies of an organisation (Powers,

Robinson and Stomberg, 2016). These all stakeholders can be impacted in directly and indirectly

manner. In broad sense there are two types of stakeholders which are internal and external. The

above company has various kind of stakeholders who have their interest in the company. Some

of these are mentioned below:

Internal stakeholders- These are those stakeholders who actively involve in the company's

operations and activities. Along with these stakeholders can stuck due to change in organisations'

plans and policies. Herein, some types of internal stakeholders are mentioned below:

Managers- These are the most important internal stakeholders of company. This is why

because they involve in the process of preparation of plans and policies for companies as

well as manage all the activities in an effective manner. These stakeholders get benefit

from financial reports by getting relevant and needed information for decision-making.

Employees- These stakeholders are involved in completing the given task and activities.

As well as get salary, wages and other financial benefits in return. The employees take

benefits from financial information in ensuring their monetary benefits, financial security

etc.

Qualitative features of financial reporting: Herein below some characteristics of financial reports

are mentioned below:

Relevance- This is a kind of feature of financial reports which defines that there should

be relevancy of financial reports with the business transactions (Rotimi, 2012).

Timeliness- This is mandatory that financial reports should be prepared on a timely basis

which can be yearly or quarterly.

Understandability- According to this feature, the financial reports should be

understandable for all stakeholders so that decision can be taken.

3. Different types of stakeholders and benefits which they get from financial information.

Stakeholders- In the aspect of business, the stakeholders can be government, customers,

suppliers or any other who gets effected due to the policies of an organisation (Powers,

Robinson and Stomberg, 2016). These all stakeholders can be impacted in directly and indirectly

manner. In broad sense there are two types of stakeholders which are internal and external. The

above company has various kind of stakeholders who have their interest in the company. Some

of these are mentioned below:

Internal stakeholders- These are those stakeholders who actively involve in the company's

operations and activities. Along with these stakeholders can stuck due to change in organisations'

plans and policies. Herein, some types of internal stakeholders are mentioned below:

Managers- These are the most important internal stakeholders of company. This is why

because they involve in the process of preparation of plans and policies for companies as

well as manage all the activities in an effective manner. These stakeholders get benefit

from financial reports by getting relevant and needed information for decision-making.

Employees- These stakeholders are involved in completing the given task and activities.

As well as get salary, wages and other financial benefits in return. The employees take

benefits from financial information in ensuring their monetary benefits, financial security

etc.

External stakeholder- These stakeholders are those who do not show any interest in the

company's daily operations and activities. They show interest only in financial position of

companies. Some types of external stakeholders are as follows:

Creditors- These external stakeholders provide financial assistance and other services on

credit to the companies (Dhole, Lobo, Mishra and Pal, 2015). As well as they show they

take benefit from the financial information in assessing the financial conditions to make

credit transaction.

Government- The government is a kind of stakeholder who charges taxes such as goods

service tax, payroll tax etc. which helps in economic growth of countries. They show

their interest in the financial information to assess total tax payable amount on the basis

of income.

4. Financial reports for meeting organisational growth and objectives.

The financial reports are important for meeting the organisational growth and objectives,

this why because of following reasons:

Financial reports for meeting organisational growth- The financial reports are very important

for meeting the organisational growth (Aversano and Christiaens, 2014). It is so because with the

help of financial reports companies can analyse the actual financial condition and on the basis of

it they can make further decisions for growing the business entity. Like the price water coopers

company can take benefit from the financial reports for their growth.

Financial reports for meeting organisational objectives- Additionally, the financial reports play

an important role for meeting the organisational objectives. This is why because on the basis of

financial reports companies can make their plans and policies for achievement of goals and

objectives. Like the above respective company if they want to make plans and strategies about

achievement of their goals then it can be done with the help of various kind of financial

statements and reports.

Financial reports for development of organisation- Apart from these benefits of the financial

reports, this is also an another importance. Due to regular preparation of financial reports,

companies' goodwill can increase. This is why because if a company prepares the financial

reports on a regular basis then it can be spread out to all the stakeholders which may lead to the

increase in reputation. So overall, the financial reports are very important for development of

company's daily operations and activities. They show interest only in financial position of

companies. Some types of external stakeholders are as follows:

Creditors- These external stakeholders provide financial assistance and other services on

credit to the companies (Dhole, Lobo, Mishra and Pal, 2015). As well as they show they

take benefit from the financial information in assessing the financial conditions to make

credit transaction.

Government- The government is a kind of stakeholder who charges taxes such as goods

service tax, payroll tax etc. which helps in economic growth of countries. They show

their interest in the financial information to assess total tax payable amount on the basis

of income.

4. Financial reports for meeting organisational growth and objectives.

The financial reports are important for meeting the organisational growth and objectives,

this why because of following reasons:

Financial reports for meeting organisational growth- The financial reports are very important

for meeting the organisational growth (Aversano and Christiaens, 2014). It is so because with the

help of financial reports companies can analyse the actual financial condition and on the basis of

it they can make further decisions for growing the business entity. Like the price water coopers

company can take benefit from the financial reports for their growth.

Financial reports for meeting organisational objectives- Additionally, the financial reports play

an important role for meeting the organisational objectives. This is why because on the basis of

financial reports companies can make their plans and policies for achievement of goals and

objectives. Like the above respective company if they want to make plans and strategies about

achievement of their goals then it can be done with the help of various kind of financial

statements and reports.

Financial reports for development of organisation- Apart from these benefits of the financial

reports, this is also an another importance. Due to regular preparation of financial reports,

companies' goodwill can increase. This is why because if a company prepares the financial

reports on a regular basis then it can be spread out to all the stakeholders which may lead to the

increase in reputation. So overall, the financial reports are very important for development of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organisations. Such as in the price water coopers company, they enables the development of their

business by producing the financial reports timely.

So these are the importance of the financial reports in the context of organisational growth,

objectives and development.

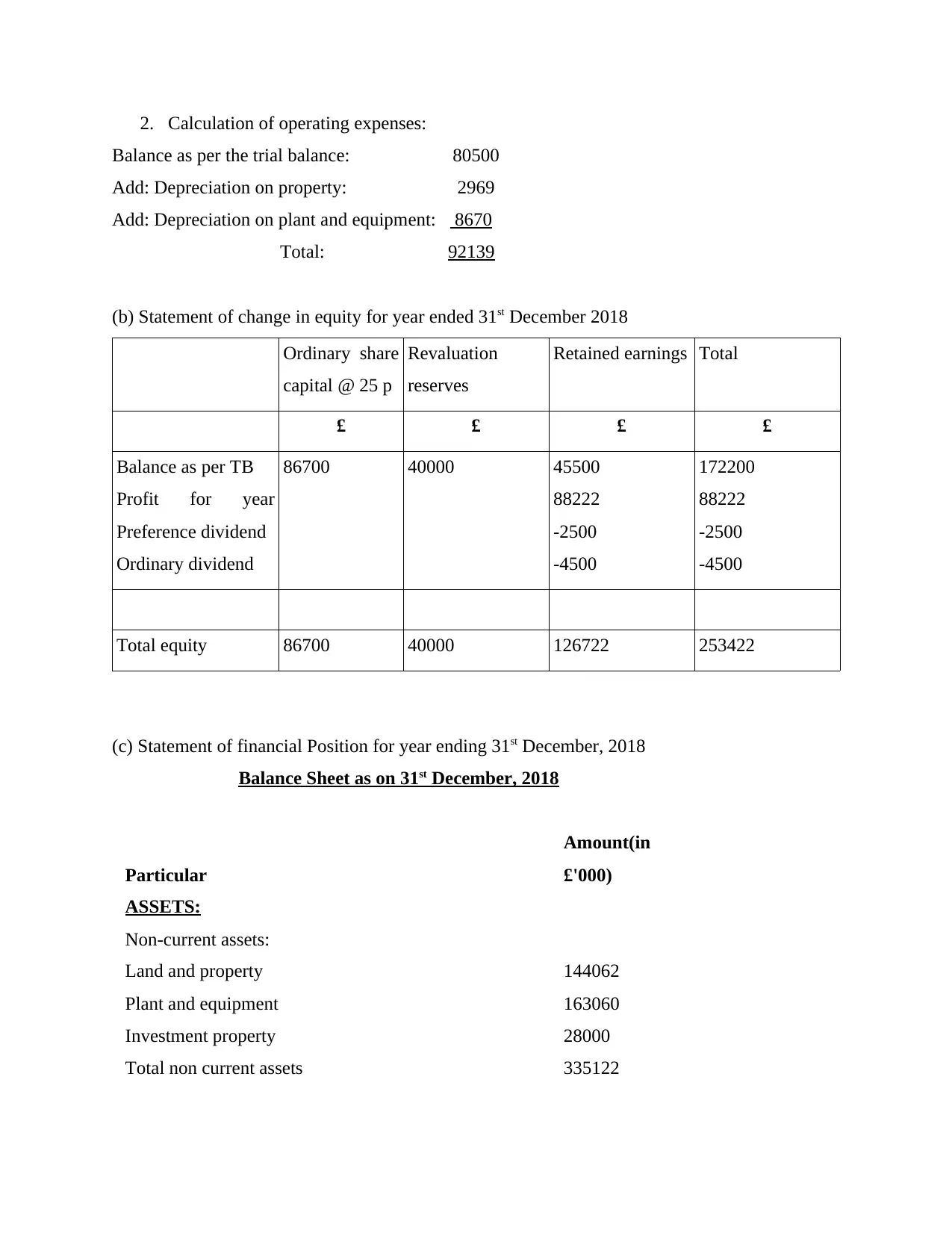

5. Presentation of financial statements.

(a) Profit and loss account for year ending 31st December, 2018

Particular Amount(in £'000)

Revenue from Operations (A) 585100

Cost of sales w1 (403639)

-

Gross profit 181461

Less: Operating expense w1 (92139)

Less: Depreciation (W.N. 1) 26715

Operating profits 89322

Add: Investment income 9600

Less: Finance cost (1200)

Profit before tax 97722

Less: Taxation (9500)

Profit of the year 88222

Working Note:

1. Calculation of cost of sales:

Balance as per the trial balance: 391700

Add: Adjustment as per closing stock: 300

Add: Depreciation on property: 2969

Add: Depreciation on plant and equipment: 8670

Total: 403639

business by producing the financial reports timely.

So these are the importance of the financial reports in the context of organisational growth,

objectives and development.

5. Presentation of financial statements.

(a) Profit and loss account for year ending 31st December, 2018

Particular Amount(in £'000)

Revenue from Operations (A) 585100

Cost of sales w1 (403639)

-

Gross profit 181461

Less: Operating expense w1 (92139)

Less: Depreciation (W.N. 1) 26715

Operating profits 89322

Add: Investment income 9600

Less: Finance cost (1200)

Profit before tax 97722

Less: Taxation (9500)

Profit of the year 88222

Working Note:

1. Calculation of cost of sales:

Balance as per the trial balance: 391700

Add: Adjustment as per closing stock: 300

Add: Depreciation on property: 2969

Add: Depreciation on plant and equipment: 8670

Total: 403639

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Calculation of operating expenses:

Balance as per the trial balance: 80500

Add: Depreciation on property: 2969

Add: Depreciation on plant and equipment: 8670

Total: 92139

(b) Statement of change in equity for year ended 31st December 2018

Ordinary share

capital @ 25 p

Revaluation

reserves

Retained earnings Total

£ £ £ £

Balance as per TB

Profit for year

Preference dividend

Ordinary dividend

86700 40000 45500

88222

-2500

-4500

172200

88222

-2500

-4500

Total equity 86700 40000 126722 253422

(c) Statement of financial Position for year ending 31st December, 2018

Balance Sheet as on 31st December, 2018

Particular

Amount(in

£'000)

ASSETS:

Non-current assets:

Land and property 144062

Plant and equipment 163060

Investment property 28000

Total non current assets 335122

Balance as per the trial balance: 80500

Add: Depreciation on property: 2969

Add: Depreciation on plant and equipment: 8670

Total: 92139

(b) Statement of change in equity for year ended 31st December 2018

Ordinary share

capital @ 25 p

Revaluation

reserves

Retained earnings Total

£ £ £ £

Balance as per TB

Profit for year

Preference dividend

Ordinary dividend

86700 40000 45500

88222

-2500

-4500

172200

88222

-2500

-4500

Total equity 86700 40000 126722 253422

(c) Statement of financial Position for year ending 31st December, 2018

Balance Sheet as on 31st December, 2018

Particular

Amount(in

£'000)

ASSETS:

Non-current assets:

Land and property 144062

Plant and equipment 163060

Investment property 28000

Total non current assets 335122

Current assets:

Inventories 24700

Trade receivables 78000

Total current assets 102700

Total assets 437822

EQUITY AND LIABILITIES:

1. Equity:

Ordinary share capital 86700

Revaluation reserve 40000

Retained earnings 126722

Total equity 253422

Non current liabilities:

10% preference share capital 26500

Deferred taxation 10000

Total non current liabilities 36500

Current liabilities:

Trade payables 62700

Tax payables 9500

Bank overdraft 10900

Total current liabilities 83100

Total equity and liabilities 373022

Working Note:

1. Land and property:

Cost: 150000

Less: Current depreciation: 5938

Total: 144062

2.

Inventories 24700

Trade receivables 78000

Total current assets 102700

Total assets 437822

EQUITY AND LIABILITIES:

1. Equity:

Ordinary share capital 86700

Revaluation reserve 40000

Retained earnings 126722

Total equity 253422

Non current liabilities:

10% preference share capital 26500

Deferred taxation 10000

Total non current liabilities 36500

Current liabilities:

Trade payables 62700

Tax payables 9500

Bank overdraft 10900

Total current liabilities 83100

Total equity and liabilities 373022

Working Note:

1. Land and property:

Cost: 150000

Less: Current depreciation: 5938

Total: 144062

2.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

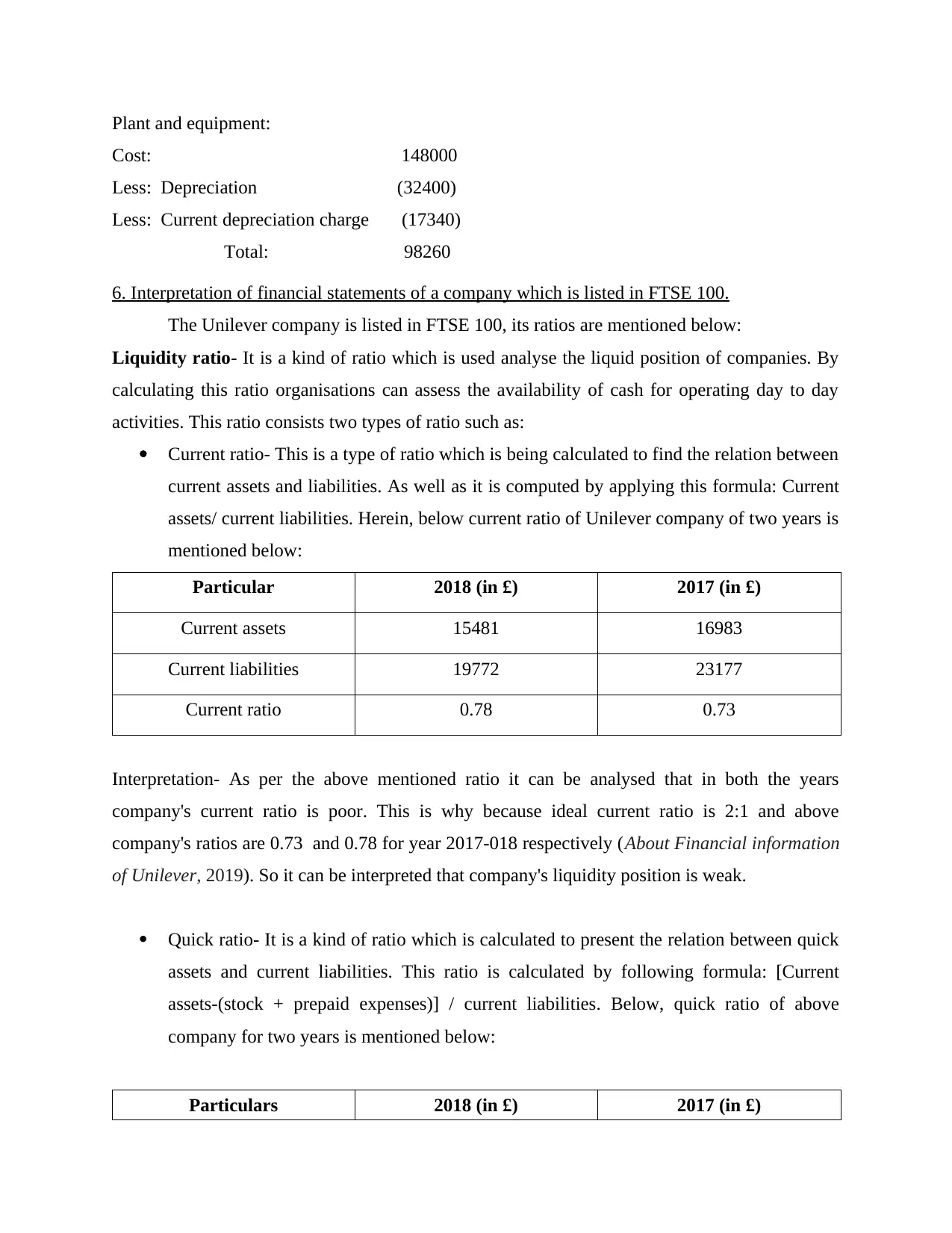

Plant and equipment:

Cost: 148000

Less: Depreciation (32400)

Less: Current depreciation charge (17340)

Total: 98260

6. Interpretation of financial statements of a company which is listed in FTSE 100.

The Unilever company is listed in FTSE 100, its ratios are mentioned below:

Liquidity ratio- It is a kind of ratio which is used analyse the liquid position of companies. By

calculating this ratio organisations can assess the availability of cash for operating day to day

activities. This ratio consists two types of ratio such as:

Current ratio- This is a type of ratio which is being calculated to find the relation between

current assets and liabilities. As well as it is computed by applying this formula: Current

assets/ current liabilities. Herein, below current ratio of Unilever company of two years is

mentioned below:

Particular 2018 (in £) 2017 (in £)

Current assets 15481 16983

Current liabilities 19772 23177

Current ratio 0.78 0.73

Interpretation- As per the above mentioned ratio it can be analysed that in both the years

company's current ratio is poor. This is why because ideal current ratio is 2:1 and above

company's ratios are 0.73 and 0.78 for year 2017-018 respectively (About Financial information

of Unilever, 2019). So it can be interpreted that company's liquidity position is weak.

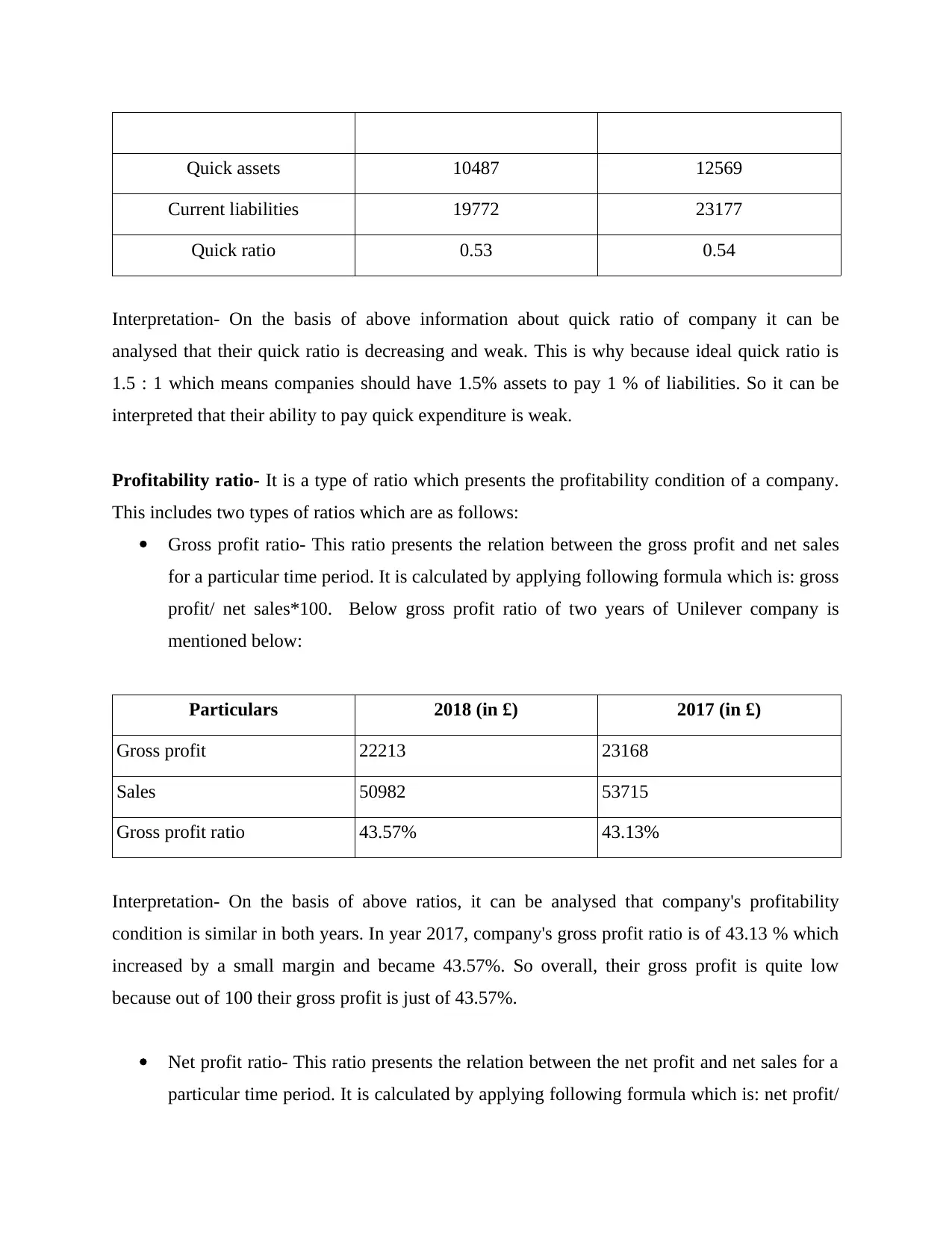

Quick ratio- It is a kind of ratio which is calculated to present the relation between quick

assets and current liabilities. This ratio is calculated by following formula: [Current

assets-(stock + prepaid expenses)] / current liabilities. Below, quick ratio of above

company for two years is mentioned below:

Particulars 2018 (in £) 2017 (in £)

Cost: 148000

Less: Depreciation (32400)

Less: Current depreciation charge (17340)

Total: 98260

6. Interpretation of financial statements of a company which is listed in FTSE 100.

The Unilever company is listed in FTSE 100, its ratios are mentioned below:

Liquidity ratio- It is a kind of ratio which is used analyse the liquid position of companies. By

calculating this ratio organisations can assess the availability of cash for operating day to day

activities. This ratio consists two types of ratio such as:

Current ratio- This is a type of ratio which is being calculated to find the relation between

current assets and liabilities. As well as it is computed by applying this formula: Current

assets/ current liabilities. Herein, below current ratio of Unilever company of two years is

mentioned below:

Particular 2018 (in £) 2017 (in £)

Current assets 15481 16983

Current liabilities 19772 23177

Current ratio 0.78 0.73

Interpretation- As per the above mentioned ratio it can be analysed that in both the years

company's current ratio is poor. This is why because ideal current ratio is 2:1 and above

company's ratios are 0.73 and 0.78 for year 2017-018 respectively (About Financial information

of Unilever, 2019). So it can be interpreted that company's liquidity position is weak.

Quick ratio- It is a kind of ratio which is calculated to present the relation between quick

assets and current liabilities. This ratio is calculated by following formula: [Current

assets-(stock + prepaid expenses)] / current liabilities. Below, quick ratio of above

company for two years is mentioned below:

Particulars 2018 (in £) 2017 (in £)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Quick assets 10487 12569

Current liabilities 19772 23177

Quick ratio 0.53 0.54

Interpretation- On the basis of above information about quick ratio of company it can be

analysed that their quick ratio is decreasing and weak. This is why because ideal quick ratio is

1.5 : 1 which means companies should have 1.5% assets to pay 1 % of liabilities. So it can be

interpreted that their ability to pay quick expenditure is weak.

Profitability ratio- It is a type of ratio which presents the profitability condition of a company.

This includes two types of ratios which are as follows:

Gross profit ratio- This ratio presents the relation between the gross profit and net sales

for a particular time period. It is calculated by applying following formula which is: gross

profit/ net sales*100. Below gross profit ratio of two years of Unilever company is

mentioned below:

Particulars 2018 (in £) 2017 (in £)

Gross profit 22213 23168

Sales 50982 53715

Gross profit ratio 43.57% 43.13%

Interpretation- On the basis of above ratios, it can be analysed that company's profitability

condition is similar in both years. In year 2017, company's gross profit ratio is of 43.13 % which

increased by a small margin and became 43.57%. So overall, their gross profit is quite low

because out of 100 their gross profit is just of 43.57%.

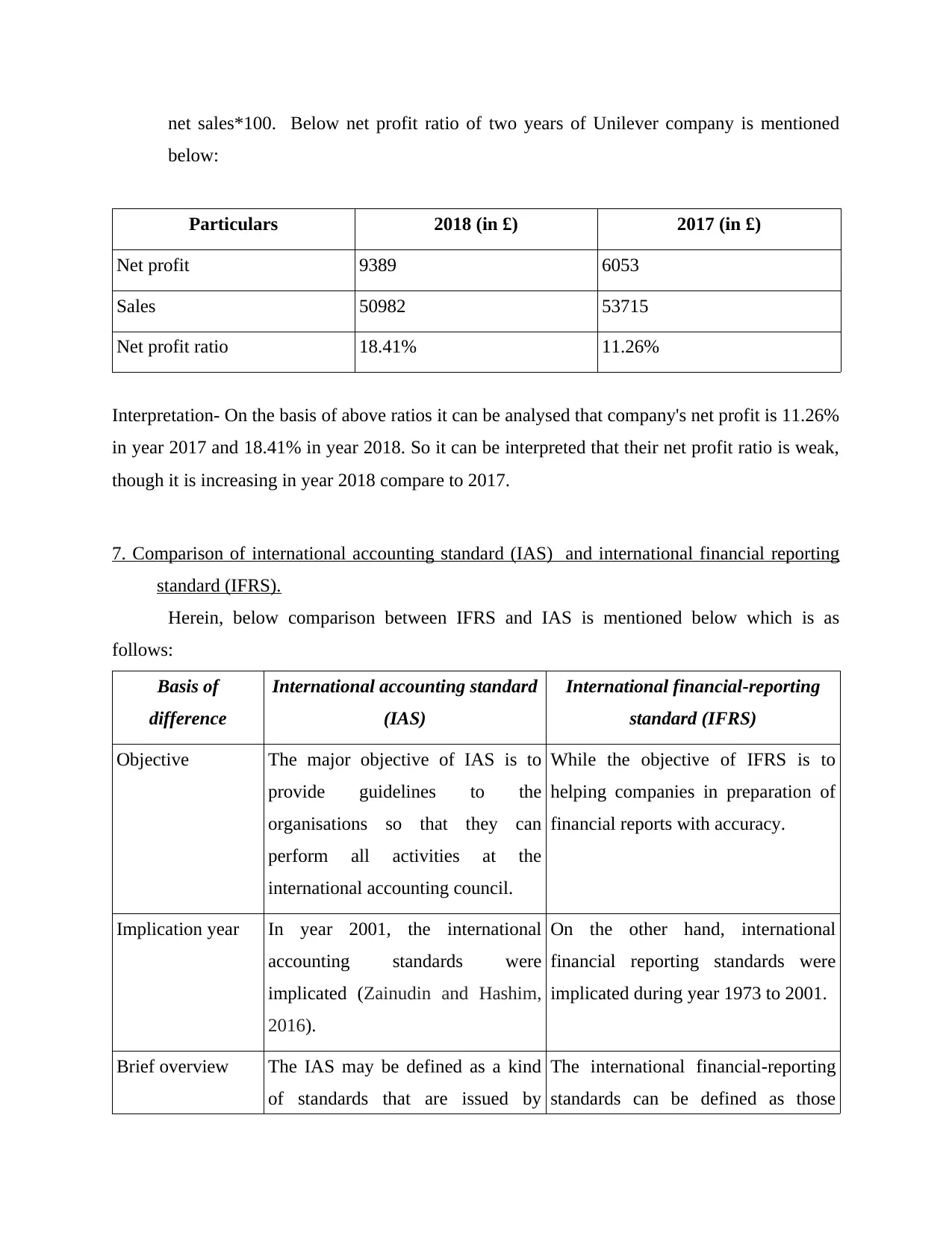

Net profit ratio- This ratio presents the relation between the net profit and net sales for a

particular time period. It is calculated by applying following formula which is: net profit/

Current liabilities 19772 23177

Quick ratio 0.53 0.54

Interpretation- On the basis of above information about quick ratio of company it can be

analysed that their quick ratio is decreasing and weak. This is why because ideal quick ratio is

1.5 : 1 which means companies should have 1.5% assets to pay 1 % of liabilities. So it can be

interpreted that their ability to pay quick expenditure is weak.

Profitability ratio- It is a type of ratio which presents the profitability condition of a company.

This includes two types of ratios which are as follows:

Gross profit ratio- This ratio presents the relation between the gross profit and net sales

for a particular time period. It is calculated by applying following formula which is: gross

profit/ net sales*100. Below gross profit ratio of two years of Unilever company is

mentioned below:

Particulars 2018 (in £) 2017 (in £)

Gross profit 22213 23168

Sales 50982 53715

Gross profit ratio 43.57% 43.13%

Interpretation- On the basis of above ratios, it can be analysed that company's profitability

condition is similar in both years. In year 2017, company's gross profit ratio is of 43.13 % which

increased by a small margin and became 43.57%. So overall, their gross profit is quite low

because out of 100 their gross profit is just of 43.57%.

Net profit ratio- This ratio presents the relation between the net profit and net sales for a

particular time period. It is calculated by applying following formula which is: net profit/

net sales*100. Below net profit ratio of two years of Unilever company is mentioned

below:

Particulars 2018 (in £) 2017 (in £)

Net profit 9389 6053

Sales 50982 53715

Net profit ratio 18.41% 11.26%

Interpretation- On the basis of above ratios it can be analysed that company's net profit is 11.26%

in year 2017 and 18.41% in year 2018. So it can be interpreted that their net profit ratio is weak,

though it is increasing in year 2018 compare to 2017.

7. Comparison of international accounting standard (IAS) and international financial reporting

standard (IFRS).

Herein, below comparison between IFRS and IAS is mentioned below which is as

follows:

Basis of

difference

International accounting standard

(IAS)

International financial-reporting

standard (IFRS)

Objective The major objective of IAS is to

provide guidelines to the

organisations so that they can

perform all activities at the

international accounting council.

While the objective of IFRS is to

helping companies in preparation of

financial reports with accuracy.

Implication year In year 2001, the international

accounting standards were

implicated (Zainudin and Hashim,

2016).

On the other hand, international

financial reporting standards were

implicated during year 1973 to 2001.

Brief overview The IAS may be defined as a kind

of standards that are issued by

The international financial-reporting

standards can be defined as those

below:

Particulars 2018 (in £) 2017 (in £)

Net profit 9389 6053

Sales 50982 53715

Net profit ratio 18.41% 11.26%

Interpretation- On the basis of above ratios it can be analysed that company's net profit is 11.26%

in year 2017 and 18.41% in year 2018. So it can be interpreted that their net profit ratio is weak,

though it is increasing in year 2018 compare to 2017.

7. Comparison of international accounting standard (IAS) and international financial reporting

standard (IFRS).

Herein, below comparison between IFRS and IAS is mentioned below which is as

follows:

Basis of

difference

International accounting standard

(IAS)

International financial-reporting

standard (IFRS)

Objective The major objective of IAS is to

provide guidelines to the

organisations so that they can

perform all activities at the

international accounting council.

While the objective of IFRS is to

helping companies in preparation of

financial reports with accuracy.

Implication year In year 2001, the international

accounting standards were

implicated (Zainudin and Hashim,

2016).

On the other hand, international

financial reporting standards were

implicated during year 1973 to 2001.

Brief overview The IAS may be defined as a kind

of standards that are issued by

The international financial-reporting

standards can be defined as those

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.