Financial Reporting for Ernst & Young: Analysis and Purpose

VerifiedAdded on 2021/02/19

|24

|8273

|46

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, addressing its context within the regulatory framework, including GAAP, IASB, and IFRS. It explores the purpose of financial reporting in achieving organizational objectives, such as strategic formulation, stakeholder engagement, and compliance with statutory requirements. The report evaluates the benefits for both internal and external stakeholders, including investors, creditors, and employees, within the context of Ernst & Young. It delves into the interpretation of financial statements, including profit and loss, cash flow, and balance sheets, along with the application of financial ratios for assessing organizational performance. The report also discusses the benefits of International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), assessing models of financial reporting and auditing. Finally, it examines the importance of financial reporting across various countries, considering differences in standards and practices.

FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Context of financial reporting including regulatory framework............................................1

P2. Purpose of financial reporting to attain organisational objectives, development and growth

.....................................................................................................................................................3

M1 Evaluation of benefits given to stakeholders........................................................................5

TASK 2............................................................................................................................................6

P3 Interpret profit and loss, Cash flow and Balance statements..................................................6

P4 Financial ratios for organisational performance and investment.........................................10

M2 Interpretation of financial results and ratios of M&S.........................................................12

TASK 3..........................................................................................................................................14

P5 Benefits of International Accounting Standards and International financial reporting

standards....................................................................................................................................14

P6 Assessment of models of financial reporting and Auditing..............................................17

TASK 4..........................................................................................................................................18

P7 Importance and differences of financial reporting across various countries........................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................21

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Context of financial reporting including regulatory framework............................................1

P2. Purpose of financial reporting to attain organisational objectives, development and growth

.....................................................................................................................................................3

M1 Evaluation of benefits given to stakeholders........................................................................5

TASK 2............................................................................................................................................6

P3 Interpret profit and loss, Cash flow and Balance statements..................................................6

P4 Financial ratios for organisational performance and investment.........................................10

M2 Interpretation of financial results and ratios of M&S.........................................................12

TASK 3..........................................................................................................................................14

P5 Benefits of International Accounting Standards and International financial reporting

standards....................................................................................................................................14

P6 Assessment of models of financial reporting and Auditing..............................................17

TASK 4..........................................................................................................................................18

P7 Importance and differences of financial reporting across various countries........................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................21

INTRODUCTION

Financial reporting considered as a method of executing information of financial evets,

transactions, strategies and plans to managers, executives and stakeholders of organisation. This

report annotates the concept of financial reporting with purpose and objectivity (Ayila, 2015).

This report is produced to line manager of Ernst & Young to define the background and concept

of international financial reporting. Company provides professional services as accounting,

auditing services to manufacturers, engineering and construction companies. Assessment of the

regulatory and conceptual framework of financial reporting and accounting is analysed to

evaluate the purpose and principle of business. Reason of financial reporting requirements and

characteristics of reliable financial information explain in a very terse manner. Meaning of

stakeholder of a company with their interest in organisational goals and how they get benefited

by accomplishment of organisational goals elaborated with practicality. Essentiality of financial

reporting defined in terms of fulfilment of business goals and growth perspective in this report.

With the help of understanding of IAS 1, users would be able to construct the financial

statements for a company. Interpretation of financial statements of the Marks and Spencer. The

diversity between the IAS and financial reporting standard analysed defined properly. Benefits of

IFRS in order to maintain ethicalness in the financial reporting explained in this report properly.

Degree of compliance is measured with IFRS by companies across the countries. The impact of

international financial and accounting standards upon national accounting standards with

appropriate examples are evaluated in more strategic manner.

TASK 1

P1 Context of financial reporting including regulatory framework

Sound financial coverage is a crucial component of the resilience of a corporation. It’s really is

vital to companies as well as the shareholders to be able to believe and comprehend the

economic situation of a company (Szychta and de la Rosa, 2012). False or outdated financial

statements leave a business vulnerable to failures and missed opportunities. The findings for

companies and their shareholders and borrowers could be devastating. When financial conditions

shift and enterprise difficulties and possibilities emerge, most significant instrument is prompt

and precise financial information.

Regulatory framework

1

Financial reporting considered as a method of executing information of financial evets,

transactions, strategies and plans to managers, executives and stakeholders of organisation. This

report annotates the concept of financial reporting with purpose and objectivity (Ayila, 2015).

This report is produced to line manager of Ernst & Young to define the background and concept

of international financial reporting. Company provides professional services as accounting,

auditing services to manufacturers, engineering and construction companies. Assessment of the

regulatory and conceptual framework of financial reporting and accounting is analysed to

evaluate the purpose and principle of business. Reason of financial reporting requirements and

characteristics of reliable financial information explain in a very terse manner. Meaning of

stakeholder of a company with their interest in organisational goals and how they get benefited

by accomplishment of organisational goals elaborated with practicality. Essentiality of financial

reporting defined in terms of fulfilment of business goals and growth perspective in this report.

With the help of understanding of IAS 1, users would be able to construct the financial

statements for a company. Interpretation of financial statements of the Marks and Spencer. The

diversity between the IAS and financial reporting standard analysed defined properly. Benefits of

IFRS in order to maintain ethicalness in the financial reporting explained in this report properly.

Degree of compliance is measured with IFRS by companies across the countries. The impact of

international financial and accounting standards upon national accounting standards with

appropriate examples are evaluated in more strategic manner.

TASK 1

P1 Context of financial reporting including regulatory framework

Sound financial coverage is a crucial component of the resilience of a corporation. It’s really is

vital to companies as well as the shareholders to be able to believe and comprehend the

economic situation of a company (Szychta and de la Rosa, 2012). False or outdated financial

statements leave a business vulnerable to failures and missed opportunities. The findings for

companies and their shareholders and borrowers could be devastating. When financial conditions

shift and enterprise difficulties and possibilities emerge, most significant instrument is prompt

and precise financial information.

Regulatory framework

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

GAAP is the authentic regulatory reform that regulates the laws and legislations at

national and international level with identification of particular jurisdiction. In Ireland and the

UK various parts of regulations are combined and constituted with regulatory reforms (Wayne

Gould, 2012). The structure is determined format. Professional regulation subject to international

and national financial reporting standards others financial reporting standards with the

professional and accounting bodies are treated in specific transactions. It also contains the

company law requirements and directives. The Stock exchange and regulations subject to listing

and ruling the parties among various sections considered in more strategic confined manner.

Regulations are considered more strategic with the specific accounting aspects.

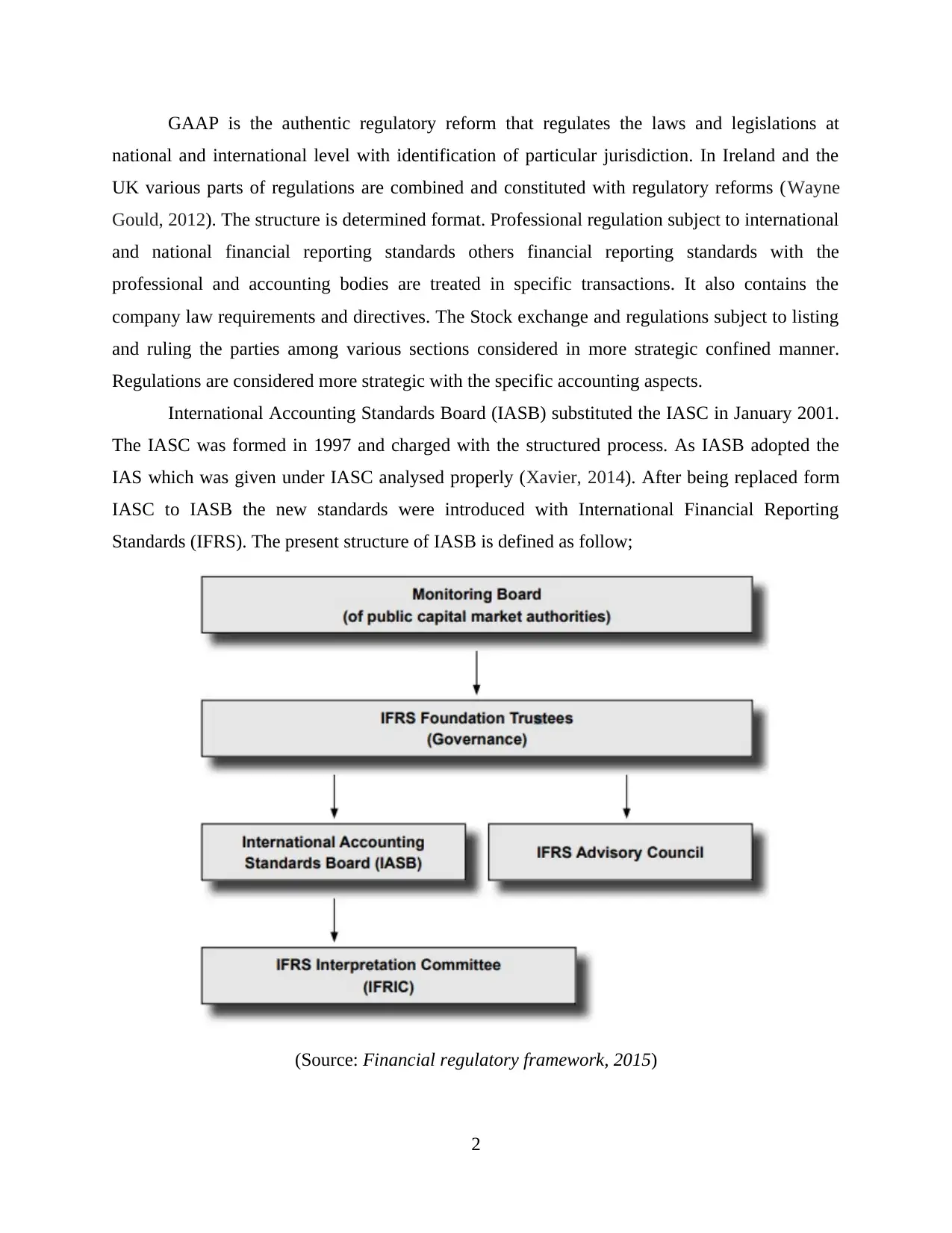

International Accounting Standards Board (IASB) substituted the IASC in January 2001.

The IASC was formed in 1997 and charged with the structured process. As IASB adopted the

IAS which was given under IASC analysed properly (Xavier, 2014). After being replaced form

IASC to IASB the new standards were introduced with International Financial Reporting

Standards (IFRS). The present structure of IASB is defined as follow;

(Source: Financial regulatory framework, 2015)

2

national and international level with identification of particular jurisdiction. In Ireland and the

UK various parts of regulations are combined and constituted with regulatory reforms (Wayne

Gould, 2012). The structure is determined format. Professional regulation subject to international

and national financial reporting standards others financial reporting standards with the

professional and accounting bodies are treated in specific transactions. It also contains the

company law requirements and directives. The Stock exchange and regulations subject to listing

and ruling the parties among various sections considered in more strategic confined manner.

Regulations are considered more strategic with the specific accounting aspects.

International Accounting Standards Board (IASB) substituted the IASC in January 2001.

The IASC was formed in 1997 and charged with the structured process. As IASB adopted the

IAS which was given under IASC analysed properly (Xavier, 2014). After being replaced form

IASC to IASB the new standards were introduced with International Financial Reporting

Standards (IFRS). The present structure of IASB is defined as follow;

(Source: Financial regulatory framework, 2015)

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Monitioring board: It is operated by the trustees of the IFRS foundation. The monitoting board

was formed in Febuary 1, 2009 subject to improve the accountability of the IFRS foundation

(Crane and Livesey, 2017).

IFRS foundation: This was formed in march 2010 with 21 Trustees. The monitoring

board also consider significant operation and activities which are undertaken by IFRS

foundation. Managing the financiang arrangements.

The International Accounting Standards Boards (IASB): The IASB has complete

control over the development and establishment of self-technical strategy, the IFRS Structure

believes this ideology, but do not have the authority to determine it. The IASB had fifteen

participants taken from all over the world for centuries of reading, although in the near future

they feel compelled to extend this amount to seventeen.

IFRS interpretation Committee: There are fourten committee in it. It key opeartion is to

analyse accounting issues and challenges ascend from IFRS. It tries to resolve the issues by valid

accounting treatment and provides an effectivee and authorative guidance subject to associated

issues (Grünewald and et. al., 2012).

Governance of financial reporting

Corporate governance was structured in order to improve the ethics and key consideration

while keeping the financial records and information. Governance is recognised as a system that

manage and control the accountability of business to protect the rights of stakeholders, associated

parties and staff members of company. Safeguard the integrity and the morality of accounting

standards is the main objective of the corporate governance. It provides a valid considerations

and assurance to mangers that the financial operations are carried out properly and in effective

manner.

P2. Purpose of financial reporting to attain organisational objectives, development and growth

The scope of financial reporting has become vital in organisational context due to its

subjectivity and practicality. Relevancy of information is considering the main factor of

enhancing the scope of financial reporting with in organisation. Financial statements of company

are the key source of information that helps to analyse the actual financial performance of the

organisation. As per IAS 1, Financial statements of company are categorised in five pats as

Income statement, balance sheet, Statement of change in equity, statement of cash flow and

Notes to financial statements. Every statement gives a specific information to users as income

3

was formed in Febuary 1, 2009 subject to improve the accountability of the IFRS foundation

(Crane and Livesey, 2017).

IFRS foundation: This was formed in march 2010 with 21 Trustees. The monitoring

board also consider significant operation and activities which are undertaken by IFRS

foundation. Managing the financiang arrangements.

The International Accounting Standards Boards (IASB): The IASB has complete

control over the development and establishment of self-technical strategy, the IFRS Structure

believes this ideology, but do not have the authority to determine it. The IASB had fifteen

participants taken from all over the world for centuries of reading, although in the near future

they feel compelled to extend this amount to seventeen.

IFRS interpretation Committee: There are fourten committee in it. It key opeartion is to

analyse accounting issues and challenges ascend from IFRS. It tries to resolve the issues by valid

accounting treatment and provides an effectivee and authorative guidance subject to associated

issues (Grünewald and et. al., 2012).

Governance of financial reporting

Corporate governance was structured in order to improve the ethics and key consideration

while keeping the financial records and information. Governance is recognised as a system that

manage and control the accountability of business to protect the rights of stakeholders, associated

parties and staff members of company. Safeguard the integrity and the morality of accounting

standards is the main objective of the corporate governance. It provides a valid considerations

and assurance to mangers that the financial operations are carried out properly and in effective

manner.

P2. Purpose of financial reporting to attain organisational objectives, development and growth

The scope of financial reporting has become vital in organisational context due to its

subjectivity and practicality. Relevancy of information is considering the main factor of

enhancing the scope of financial reporting with in organisation. Financial statements of company

are the key source of information that helps to analyse the actual financial performance of the

organisation. As per IAS 1, Financial statements of company are categorised in five pats as

Income statement, balance sheet, Statement of change in equity, statement of cash flow and

Notes to financial statements. Every statement gives a specific information to users as income

3

statements states that how much profit or loss earned by company subject to a particular

accounting year, balance sheet states the amount of assets and liabilities retained by organisation

in a particular period, cash flow statements presents the information related to flow of cash and

cash equilanets in order to run business operations, Change in equity statement presents the

information related to overall equity and reserves retained by company and variation in the share

capital, Notes to financial accounts contains the subjective information of each elements

recorded in income statement and balance sheet of company (Deng, Kang and Low, 2013).

Subjectivity and purpose become vast with the increasing scope of financial reporting. The key

purpose of financial reporting is defined as follows:

Strategic formulation: Companies formulate plans, budgets and strategies for sustainable

business operation. Building a sustainable business structure remains key objective of business.

Optimum use of financial resources is the key solution to attain the financial goals. Financial

reporting helps the entity to analyse the strength and capacity whether the sustainable business

structure can be formed. For this purpose, team of accountants and executives put their efforts to

track the financial transactions and events to attain the business objectives in best possible

manner. Organisation’s revenue and profits are monitored on periodic basis and proper reporting

done in order to control excessive or misuse of financial resources. By utilizing information at

required areas helps entity to grab opportunities on the right time that is considered great sign of

growth and development of business.

Correlating objectives of business to stakeholders: Gaining the stakeholder interest and faith

is also considered prime objective of companies. Communicating goals and objectives of

business to suppliers, customers, investors, owners, financial institutions, shareholders is also

main objective of organisation and communicating the valuable information is become the

purpose for organisation. Investors invest their amount in the business and expect higher return

in consideration. If organisation be successful to meet the expectations of stakeholders than the

changes of having less funding facility in future. This maintain the regular flow of financial

resources with in the operation through which organisation be able to accomplish the goals of

business in more effective manner (Hörisch, Freeman and Schaltegger, 2014).

Keeping the employees well informed: Effective employee engagement leads entity

towards targets. For the purpose of connecting employees with the financial position of

organisation, a periodic reporting is carried out by management. This boost up the confidence

4

accounting year, balance sheet states the amount of assets and liabilities retained by organisation

in a particular period, cash flow statements presents the information related to flow of cash and

cash equilanets in order to run business operations, Change in equity statement presents the

information related to overall equity and reserves retained by company and variation in the share

capital, Notes to financial accounts contains the subjective information of each elements

recorded in income statement and balance sheet of company (Deng, Kang and Low, 2013).

Subjectivity and purpose become vast with the increasing scope of financial reporting. The key

purpose of financial reporting is defined as follows:

Strategic formulation: Companies formulate plans, budgets and strategies for sustainable

business operation. Building a sustainable business structure remains key objective of business.

Optimum use of financial resources is the key solution to attain the financial goals. Financial

reporting helps the entity to analyse the strength and capacity whether the sustainable business

structure can be formed. For this purpose, team of accountants and executives put their efforts to

track the financial transactions and events to attain the business objectives in best possible

manner. Organisation’s revenue and profits are monitored on periodic basis and proper reporting

done in order to control excessive or misuse of financial resources. By utilizing information at

required areas helps entity to grab opportunities on the right time that is considered great sign of

growth and development of business.

Correlating objectives of business to stakeholders: Gaining the stakeholder interest and faith

is also considered prime objective of companies. Communicating goals and objectives of

business to suppliers, customers, investors, owners, financial institutions, shareholders is also

main objective of organisation and communicating the valuable information is become the

purpose for organisation. Investors invest their amount in the business and expect higher return

in consideration. If organisation be successful to meet the expectations of stakeholders than the

changes of having less funding facility in future. This maintain the regular flow of financial

resources with in the operation through which organisation be able to accomplish the goals of

business in more effective manner (Hörisch, Freeman and Schaltegger, 2014).

Keeping the employees well informed: Effective employee engagement leads entity

towards targets. For the purpose of connecting employees with the financial position of

organisation, a periodic reporting is carried out by management. This boost up the confidence

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

level of employees and staff members in order to work more efficiently. Future plans are also

communicated with employees that also keep engaging them for long term period.

To Comply the statutory requirements: Organisations are required to comply the international

rules and regulations to file reports to different parties as governments, stock exchange and

registrar of companies (Nour and Mouakket, 2013). Financial reporting is useful for this purpose

also. It remains essential to circulate new agreements and renew existing agreements under the

legal law and legislations. Image of organisation become clear if all the statutory requirements

are fulfilled by entity. This helps to grow the business by building strong loyal.

M1 Evaluation of benefits given to stakeholders

Stakeholders are considered as a most essential element of the organisation because efforts of the

stakeholders helps the administrators to run the organisation effectively. There is a reciprocal

relation found between the organisation and the stakeholders of the organisation. As the

organisation gets better results as the stakeholders also gets benefited with the growth of the

business (Fox and et. al., 2013). Ernst & Young has both the internal and external stakeholders

that keep seeking the essential information produced by organisation. How the stakeholders of

E&Y get benefited are defined below:

External stakeholders

These kinds of participants have no stake in the companies ' everyday operations but are

duly affected in one manner by an organization's operation (Iyoha and Owolabi, 2012). The

chosen business EARNST & YOUNG consists of a wide range of stakeholders as external

investors, financial institutions, banks and suppliers.

Government It is component of any company ' internal participant by collecting corporate tax

rates, income taxes as well as further taxes such as GST and TDS. Each organization give

government tax for contributing to GDP in order to improve the rate of development as well as

reduce the inflation associated with any region (Liapis and Thalassinos, 2013).

Investors – Such kinds of investors, including bond holders but also stakeholders, spend

their capital in the company. Reasonable return rates are expected on the investment capital. It

depends primarily on organisation's market value. E&Y stakeholders have a commensurate

mortgage-to-equity percentage. EARNST & YOUNG has performed the best business practices

to gain the interest of investors and building the brand image in more effective manner.

5

communicated with employees that also keep engaging them for long term period.

To Comply the statutory requirements: Organisations are required to comply the international

rules and regulations to file reports to different parties as governments, stock exchange and

registrar of companies (Nour and Mouakket, 2013). Financial reporting is useful for this purpose

also. It remains essential to circulate new agreements and renew existing agreements under the

legal law and legislations. Image of organisation become clear if all the statutory requirements

are fulfilled by entity. This helps to grow the business by building strong loyal.

M1 Evaluation of benefits given to stakeholders

Stakeholders are considered as a most essential element of the organisation because efforts of the

stakeholders helps the administrators to run the organisation effectively. There is a reciprocal

relation found between the organisation and the stakeholders of the organisation. As the

organisation gets better results as the stakeholders also gets benefited with the growth of the

business (Fox and et. al., 2013). Ernst & Young has both the internal and external stakeholders

that keep seeking the essential information produced by organisation. How the stakeholders of

E&Y get benefited are defined below:

External stakeholders

These kinds of participants have no stake in the companies ' everyday operations but are

duly affected in one manner by an organization's operation (Iyoha and Owolabi, 2012). The

chosen business EARNST & YOUNG consists of a wide range of stakeholders as external

investors, financial institutions, banks and suppliers.

Government It is component of any company ' internal participant by collecting corporate tax

rates, income taxes as well as further taxes such as GST and TDS. Each organization give

government tax for contributing to GDP in order to improve the rate of development as well as

reduce the inflation associated with any region (Liapis and Thalassinos, 2013).

Investors – Such kinds of investors, including bond holders but also stakeholders, spend

their capital in the company. Reasonable return rates are expected on the investment capital. It

depends primarily on organisation's market value. E&Y stakeholders have a commensurate

mortgage-to-equity percentage. EARNST & YOUNG has performed the best business practices

to gain the interest of investors and building the brand image in more effective manner.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Creditors – Company uses a formal protocol to keep the interest of creditors. Crashaw

Group Plc, Crawshaw Butchers Limited (‘Butchers’) East Yorkshire Beef Limited (‘EYB’)

Gabbotts Farm (Retail) Limited (‘GFRL’) are the creditors to paid for further. A letter to these

creditors was sent due to non-payment with proper reason and misconduct. This procedure helps

to maintain the trust among creditors even after delaying in payments.

Internal stakeholders

The stakeholder that retain a particular share in the entity are pointed as internal

stakeholders of the organisation. E&Y understand the responsibility of keeping the interest of

internal stakeholders for better accomplishments of set targets and aims.

Board of Directors – The members who take the valuable decisions, making policies and

provide change policies are considered as board of directors (Jindrichovska and Kubickova,

2014). These members are recognised as key internal stakeholders because major decisions of

strategic planning and control are taken by these members. Future existence of organisation

depends upon the strategies and decision of the board members. Being a valuable stakeholder of

organisation they also answerable to further stakeholders too. Board members of Ernst and

Young remain committee to their deliverables and keep stable with their plans and strategies for

better results.

Employees – Professional and skilled staffs is delivering great services to the E&Y and company

also keep record of every employee working in it (Miková, 2014). Each members of EARNST &

YOUNG are associated with the growth and development of business. Company offers

opportunities of high pay scales, fringe benefits and award them for their best results. These type

of considerations emerge the confidence and motivates the staff. Staff get the full support form

senior authorities in terms of valuable information and sources.

TASK 2

P3 Interpret profit and loss, Cash flow and Balance statements

IAS 1 provides the rules and regulations related to presenting financial statements to

stakeholders to understand the financial performance of company (Susanti and Daryanto, 2017).

Financial statements as per the IAS 1 are defined as follows:

6

Group Plc, Crawshaw Butchers Limited (‘Butchers’) East Yorkshire Beef Limited (‘EYB’)

Gabbotts Farm (Retail) Limited (‘GFRL’) are the creditors to paid for further. A letter to these

creditors was sent due to non-payment with proper reason and misconduct. This procedure helps

to maintain the trust among creditors even after delaying in payments.

Internal stakeholders

The stakeholder that retain a particular share in the entity are pointed as internal

stakeholders of the organisation. E&Y understand the responsibility of keeping the interest of

internal stakeholders for better accomplishments of set targets and aims.

Board of Directors – The members who take the valuable decisions, making policies and

provide change policies are considered as board of directors (Jindrichovska and Kubickova,

2014). These members are recognised as key internal stakeholders because major decisions of

strategic planning and control are taken by these members. Future existence of organisation

depends upon the strategies and decision of the board members. Being a valuable stakeholder of

organisation they also answerable to further stakeholders too. Board members of Ernst and

Young remain committee to their deliverables and keep stable with their plans and strategies for

better results.

Employees – Professional and skilled staffs is delivering great services to the E&Y and company

also keep record of every employee working in it (Miková, 2014). Each members of EARNST &

YOUNG are associated with the growth and development of business. Company offers

opportunities of high pay scales, fringe benefits and award them for their best results. These type

of considerations emerge the confidence and motivates the staff. Staff get the full support form

senior authorities in terms of valuable information and sources.

TASK 2

P3 Interpret profit and loss, Cash flow and Balance statements

IAS 1 provides the rules and regulations related to presenting financial statements to

stakeholders to understand the financial performance of company (Susanti and Daryanto, 2017).

Financial statements as per the IAS 1 are defined as follows:

6

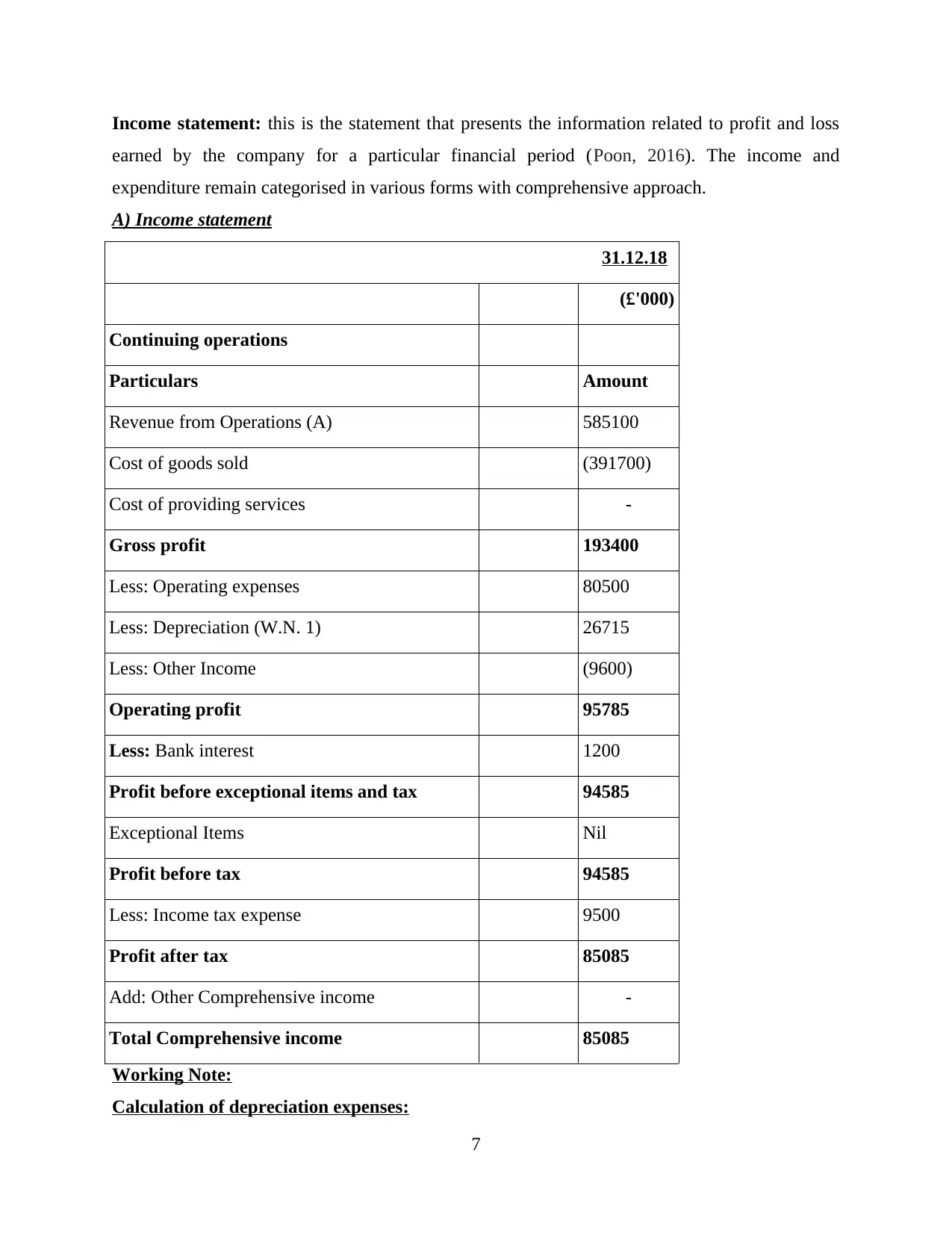

Income statement: this is the statement that presents the information related to profit and loss

earned by the company for a particular financial period (Poon, 2016). The income and

expenditure remain categorised in various forms with comprehensive approach.

A) Income statement

31.12.18

(£'000)

Continuing operations

Particulars Amount

Revenue from Operations (A) 585100

Cost of goods sold (391700)

Cost of providing services -

Gross profit 193400

Less: Operating expenses 80500

Less: Depreciation (W.N. 1) 26715

Less: Other Income (9600)

Operating profit 95785

Less: Bank interest 1200

Profit before exceptional items and tax 94585

Exceptional Items Nil

Profit before tax 94585

Less: Income tax expense 9500

Profit after tax 85085

Add: Other Comprehensive income -

Total Comprehensive income 85085

Working Note:

Calculation of depreciation expenses:

7

earned by the company for a particular financial period (Poon, 2016). The income and

expenditure remain categorised in various forms with comprehensive approach.

A) Income statement

31.12.18

(£'000)

Continuing operations

Particulars Amount

Revenue from Operations (A) 585100

Cost of goods sold (391700)

Cost of providing services -

Gross profit 193400

Less: Operating expenses 80500

Less: Depreciation (W.N. 1) 26715

Less: Other Income (9600)

Operating profit 95785

Less: Bank interest 1200

Profit before exceptional items and tax 94585

Exceptional Items Nil

Profit before tax 94585

Less: Income tax expense 9500

Profit after tax 85085

Add: Other Comprehensive income -

Total Comprehensive income 85085

Working Note:

Calculation of depreciation expenses:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Land and machinery: 150000/16 = £9375

Plant and equipment: 148000-32400 = £115600

115600*15/100 = £17340

Total depreciation = 9375+17340 = £26715

Financial position statement: This statement mainly helps in identifying the total assets

acquired or hold for sale and total liabilities including current and non-current liabilities in an

accounting period (Mahoney, 2012). The use of financial information through financial position

statement helps investors to understand the actual returns to be earned by stakeholders.

8

Plant and equipment: 148000-32400 = £115600

115600*15/100 = £17340

Total depreciation = 9375+17340 = £26715

Financial position statement: This statement mainly helps in identifying the total assets

acquired or hold for sale and total liabilities including current and non-current liabilities in an

accounting period (Mahoney, 2012). The use of financial information through financial position

statement helps investors to understand the actual returns to be earned by stakeholders.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

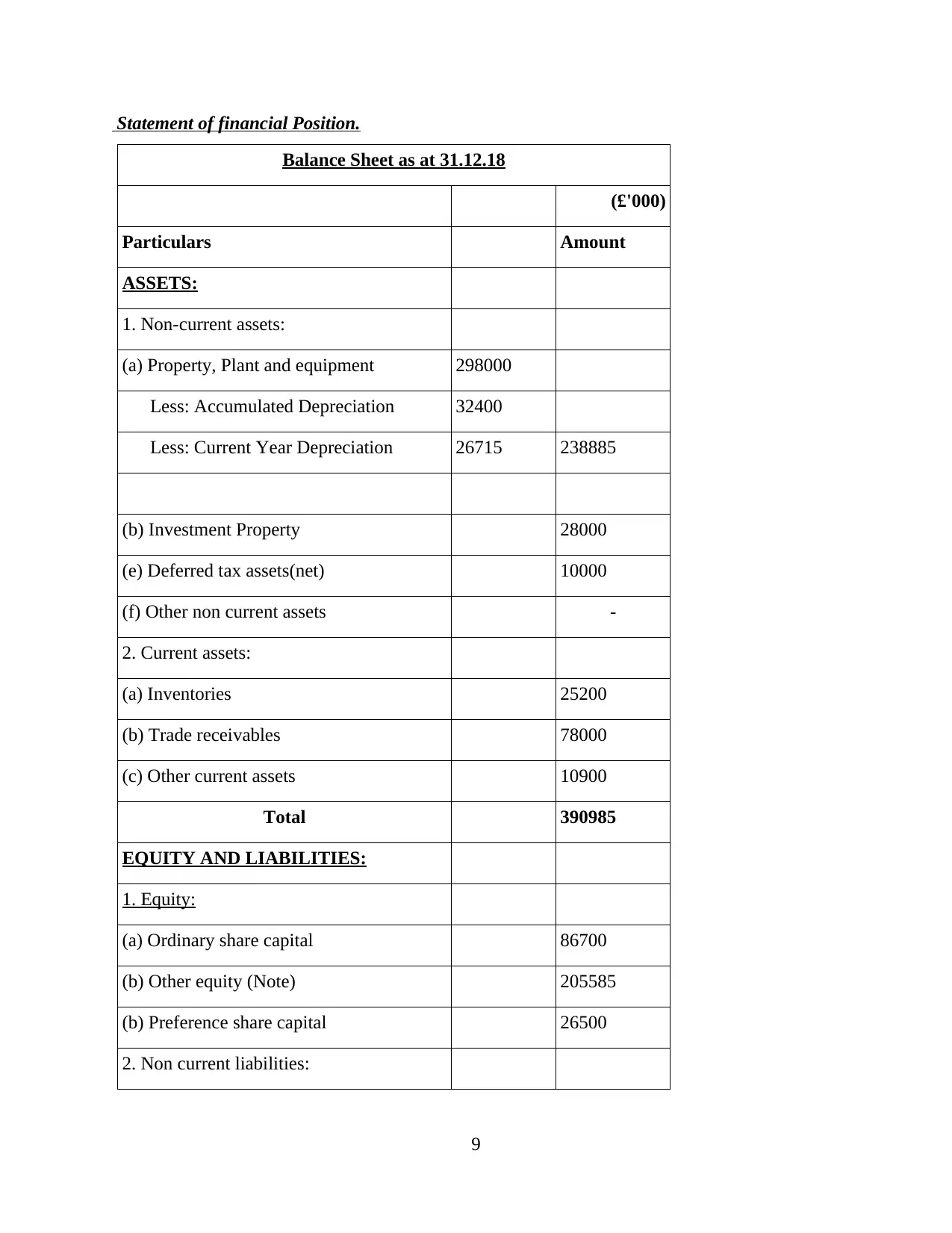

Statement of financial Position.

Balance Sheet as at 31.12.18

(£'000)

Particulars Amount

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

1. Equity:

(a) Ordinary share capital 86700

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

9

Balance Sheet as at 31.12.18

(£'000)

Particulars Amount

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

1. Equity:

(a) Ordinary share capital 86700

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

9

(a) Deferred Taxation -

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD 35000

(c) Provision for current tax 9500

Total 390985

Cash flow: Cash flow statement mainly execute the information of flow of cash form

operating, investing and financing activity (Stathopoulos, Valeri and Marcucci, 2012).

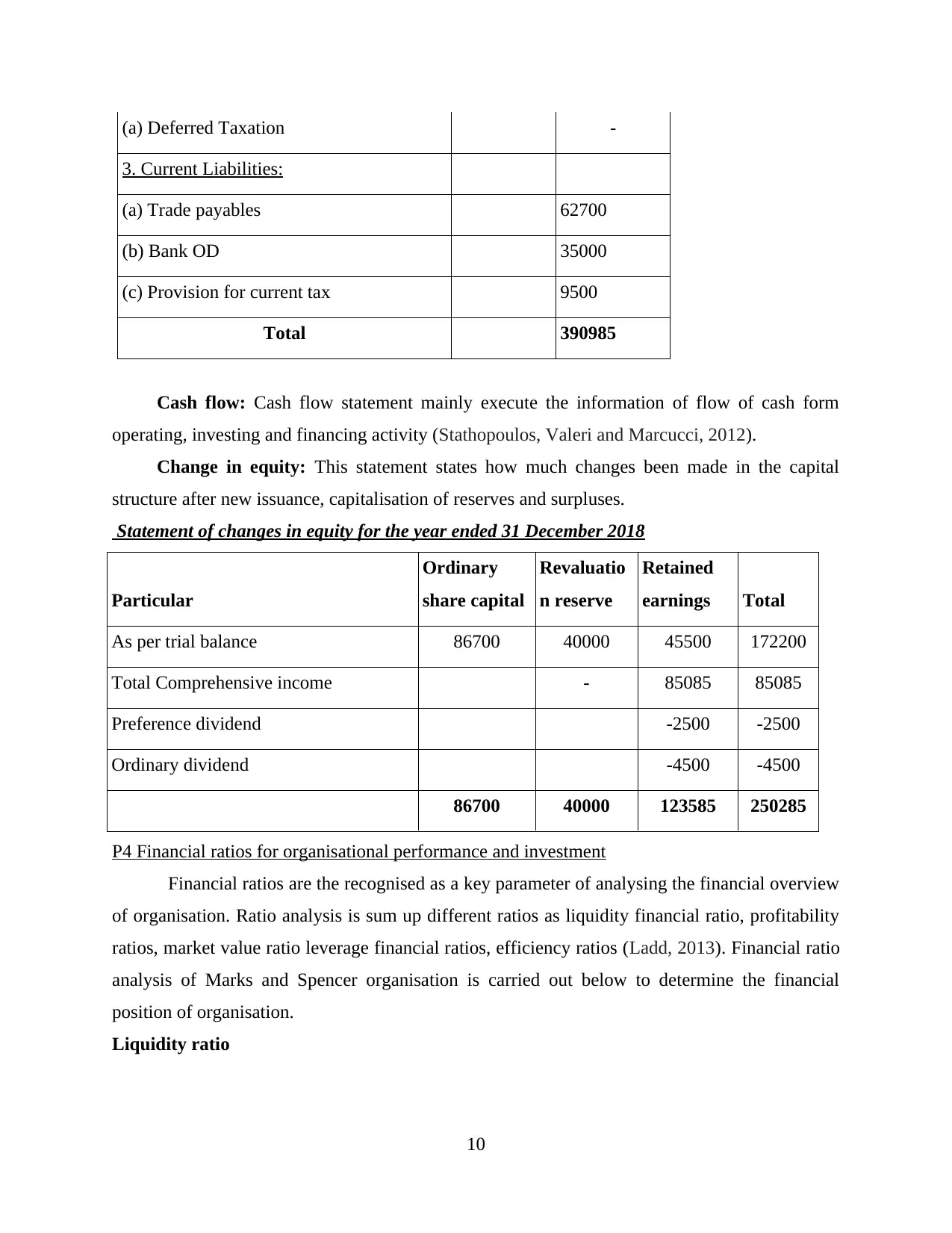

Change in equity: This statement states how much changes been made in the capital

structure after new issuance, capitalisation of reserves and surpluses.

Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluatio

n reserve

Retained

earnings Total

As per trial balance 86700 40000 45500 172200

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

P4 Financial ratios for organisational performance and investment

Financial ratios are the recognised as a key parameter of analysing the financial overview

of organisation. Ratio analysis is sum up different ratios as liquidity financial ratio, profitability

ratios, market value ratio leverage financial ratios, efficiency ratios (Ladd, 2013). Financial ratio

analysis of Marks and Spencer organisation is carried out below to determine the financial

position of organisation.

Liquidity ratio

10

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD 35000

(c) Provision for current tax 9500

Total 390985

Cash flow: Cash flow statement mainly execute the information of flow of cash form

operating, investing and financing activity (Stathopoulos, Valeri and Marcucci, 2012).

Change in equity: This statement states how much changes been made in the capital

structure after new issuance, capitalisation of reserves and surpluses.

Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluatio

n reserve

Retained

earnings Total

As per trial balance 86700 40000 45500 172200

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

P4 Financial ratios for organisational performance and investment

Financial ratios are the recognised as a key parameter of analysing the financial overview

of organisation. Ratio analysis is sum up different ratios as liquidity financial ratio, profitability

ratios, market value ratio leverage financial ratios, efficiency ratios (Ladd, 2013). Financial ratio

analysis of Marks and Spencer organisation is carried out below to determine the financial

position of organisation.

Liquidity ratio

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.