Financial Reporting: Conceptual Framework, Stakeholders, and Analysis

VerifiedAdded on 2021/02/20

|16

|4689

|26

Report

AI Summary

This report provides a comprehensive overview of financial reporting, beginning with its fundamental concepts and purpose. It explores the roles of various stakeholders, including internal (employees, managers) and external (customers, suppliers, shareholders) parties, and how they benefit from financial information. The report then delves into the conceptual and regulatory frameworks that guide financial reporting, emphasizing the importance of qualitative characteristics such as relevance, reliability, understandability, and comparability. A key component of the report is an analysis of financial statements, using Golwin Plc as a case study, including a profit and loss account, balance sheet, and statements of changes in equity. Furthermore, the report examines ratio analysis to assess financial performance and liquidity, and it concludes by comparing and contrasting the International Financial Reporting Standards (IFRS) and International Accounting Standards (IAS), discussing their benefits and the varying degrees of compliance across the globe. The report aims to provide a clear understanding of financial reporting and its practical applications.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO1..................................................................................................................................................1

P1 Financial reporting concept and purpose................................................................................1

P2 Conceptual and regulatory framework and the qualitative characteristics of financial

information...................................................................................................................................2

P3 Key Stakeholders or users of Tesco and how they take benefits from financial information

......................................................................................................................................................3

P4 Value of Financial Reporting:................................................................................................4

LO2..................................................................................................................................................5

P5 financial statements of Golwin plc. Company........................................................................5

P6 Ratio Analysis.........................................................................................................................7

LO3..................................................................................................................................................9

P7 Difference between IAS and IFRS.........................................................................................9

P8 Benefits of IFRS...................................................................................................................11

LO 4...............................................................................................................................................12

P9 Varying degree of compliance of IFRS across the world.....................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO1..................................................................................................................................................1

P1 Financial reporting concept and purpose................................................................................1

P2 Conceptual and regulatory framework and the qualitative characteristics of financial

information...................................................................................................................................2

P3 Key Stakeholders or users of Tesco and how they take benefits from financial information

......................................................................................................................................................3

P4 Value of Financial Reporting:................................................................................................4

LO2..................................................................................................................................................5

P5 financial statements of Golwin plc. Company........................................................................5

P6 Ratio Analysis.........................................................................................................................7

LO3..................................................................................................................................................9

P7 Difference between IAS and IFRS.........................................................................................9

P8 Benefits of IFRS...................................................................................................................11

LO 4...............................................................................................................................................12

P9 Varying degree of compliance of IFRS across the world.....................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial reporting is the process of presenting financial statements to the variety of

stakeholders and directors to take the useful decision regarding the company. As a junior

accountant of Grant Thornton, which is a large accountancy firm; various issues and component

of financial reporting are identified such as the regulatory and conceptual framework, internal

and external stakeholders etc. Tesco is a British multinational company whose headquarters are

in England, UK. The financial reporting helps Tesco to regulate the financial transaction and

statements. The report highlights the concept and purpose of financial reporting and the different

stakeholders who use this information. It explains various regulatory and conceptual framework

to provide guideline for the presentation of financial reports. Report also explains the usage of

financial reporting obligating companies aims and objectives. It presents the financial

information of Godwin Plc. Company by income statements and balance sheet. It also highlights

the usage of various accounting standard such as IFRS and IAS and their benefits to the

company.

MAIN BODY

LO1

P1 Financial reporting concept and purpose

Financial reporting: The presentation of financial data and information to the different

stakeholders such as customer, creditors, suppliers, shareholders, employees etc. is known as

financial reporting. It helps to take useful decision regarding the improvement in financial

performance of company. Different stakeholders and investors use the financial reporting data to

take decision regarding the investment.

Purpose of financial reporting

Provide financial information: The main purpose of financial reporting is to provide the

information regarding the financial statements to the different stakeholders and help them to take

the decision that whether they have to invest in the company or not (Clatworthy and Peel, 2016).

The financial statements content the information regarding the growth of the company, profit,

sales, cash flow etc. in particular accounting period.

Track cash flow: The aim of financial reporting is to track the cash flow of particular

accounting period and identify that whether the company is capable to accomplish the aim and

1

Financial reporting is the process of presenting financial statements to the variety of

stakeholders and directors to take the useful decision regarding the company. As a junior

accountant of Grant Thornton, which is a large accountancy firm; various issues and component

of financial reporting are identified such as the regulatory and conceptual framework, internal

and external stakeholders etc. Tesco is a British multinational company whose headquarters are

in England, UK. The financial reporting helps Tesco to regulate the financial transaction and

statements. The report highlights the concept and purpose of financial reporting and the different

stakeholders who use this information. It explains various regulatory and conceptual framework

to provide guideline for the presentation of financial reports. Report also explains the usage of

financial reporting obligating companies aims and objectives. It presents the financial

information of Godwin Plc. Company by income statements and balance sheet. It also highlights

the usage of various accounting standard such as IFRS and IAS and their benefits to the

company.

MAIN BODY

LO1

P1 Financial reporting concept and purpose

Financial reporting: The presentation of financial data and information to the different

stakeholders such as customer, creditors, suppliers, shareholders, employees etc. is known as

financial reporting. It helps to take useful decision regarding the improvement in financial

performance of company. Different stakeholders and investors use the financial reporting data to

take decision regarding the investment.

Purpose of financial reporting

Provide financial information: The main purpose of financial reporting is to provide the

information regarding the financial statements to the different stakeholders and help them to take

the decision that whether they have to invest in the company or not (Clatworthy and Peel, 2016).

The financial statements content the information regarding the growth of the company, profit,

sales, cash flow etc. in particular accounting period.

Track cash flow: The aim of financial reporting is to track the cash flow of particular

accounting period and identify that whether the company is capable to accomplish the aim and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

objective or not. It also used to pay the current debt and day to day expenses of the organization

on the given time. It helps to track the cash inflow and outflow of the Tesco company.

Reliability and accuracy: The purpose of financial reporting is to regulate the reliability

and accuracy of the data and identified that all the practices used by Tesco to prepare financial

information are legal. It helps to build up the trust of the investor that the presented information

in the annual report or published source are accurate and free from manipulation.

P2 Conceptual and regulatory framework and the qualitative characteristics of financial

information

Conceptual framework: It refers to the guideline or framework which provide the basic

details regarding the financial information and statements to develop the understanding of the

users. It is developed by international accounting standard Boards to measure and regulate the

uniformity of accounting methods across the borders.

Requirement of conceptual framework

They are required to provide a set of guideline to prepare and present the accounting

information.

It helps the user to compare and interpret the data to take useful decisions.

It is required to regulate the accounting methods at international level.

The conceptual framework principles say that the use of general accepted accounting

principles and accounting standard are useful for the company to accomplish aims and

objectives.

Regulatory framework: It helps to regulate the financial information, practices and

methods. Regulatory framework is used to ensure that company follow the accounting standard

in prescribed rules and regulation.

Requirement of regulatory framework

It helps to identify that the need and requirement of financial users are fulfilled by the

financial statements or not.

Regulatory framework is required to regulate the behaviour of companies and their

directors towards in the various investors (The regulatory framework, 2012).

Regulatory framework is used to ensure that the information is reliable, comparable and

consistent. It helps to gain the global investment from the market.

2

on the given time. It helps to track the cash inflow and outflow of the Tesco company.

Reliability and accuracy: The purpose of financial reporting is to regulate the reliability

and accuracy of the data and identified that all the practices used by Tesco to prepare financial

information are legal. It helps to build up the trust of the investor that the presented information

in the annual report or published source are accurate and free from manipulation.

P2 Conceptual and regulatory framework and the qualitative characteristics of financial

information

Conceptual framework: It refers to the guideline or framework which provide the basic

details regarding the financial information and statements to develop the understanding of the

users. It is developed by international accounting standard Boards to measure and regulate the

uniformity of accounting methods across the borders.

Requirement of conceptual framework

They are required to provide a set of guideline to prepare and present the accounting

information.

It helps the user to compare and interpret the data to take useful decisions.

It is required to regulate the accounting methods at international level.

The conceptual framework principles say that the use of general accepted accounting

principles and accounting standard are useful for the company to accomplish aims and

objectives.

Regulatory framework: It helps to regulate the financial information, practices and

methods. Regulatory framework is used to ensure that company follow the accounting standard

in prescribed rules and regulation.

Requirement of regulatory framework

It helps to identify that the need and requirement of financial users are fulfilled by the

financial statements or not.

Regulatory framework is required to regulate the behaviour of companies and their

directors towards in the various investors (The regulatory framework, 2012).

Regulatory framework is used to ensure that the information is reliable, comparable and

consistent. It helps to gain the global investment from the market.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The principle of regulatory framework state the different accounting standard such as IFRS,

IAS helps to monitor the performance of the company.

Qualitative characteristics

Relevance: It helps to ensure that all the information provided to the investor or

stakeholders is relevant and helps to take the financial decisions. The provided information

should be in prescribed and accurate format which help to understand and interpret the

information.

Reliability: It refers that the presented data are accurate and valid. It helps the

stakeholders to relay on the data that the data are free from the error, manipulation and any other

illegal practices (Flower and Ebbers, 2018). The reliability characteristics helps attract large

number of investor toward the Tesco.

Understandability: It refers that the presented data and information is in prescribed

format and easily understandable. It helps the users to understand the data and interpret the

financial information for effective and efficient decision-making. It helps Tesco to gain

international customer from the global market.

Comparability: It helps the decision maker or stakeholders to compare the financial

information of different accounting year or to the other companies from the same industry or

other industry (Michelon, Pilonato and Ricceri, 2015). The comparability characteristics helps to

identified that the information are in same format with same methods. It makes the data more

understandable and comparable for Tesco stakeholders.

P3 Key Stakeholders or users of Tesco and how they take benefits from financial information

Stakeholders are those who have an interest in the growth and success of the organization

and they play an important role in Tesco also. The key stakeholders of Tesco are described as

below:

Internal Stakeholders:

Employees: Employees influence Tesco by working efficiently and they always want

that it should succeed as if Tesco will perform effectively it will generate more profits because of

which employees are likely to get more chances of promotion, better salaries and they will also

get a secured job (Maynard., 2017). The financial information is also helpful for employees as

they get knowledge regarding the profits of Tesco because more profits may lead to extra bonus

to them.

3

IAS helps to monitor the performance of the company.

Qualitative characteristics

Relevance: It helps to ensure that all the information provided to the investor or

stakeholders is relevant and helps to take the financial decisions. The provided information

should be in prescribed and accurate format which help to understand and interpret the

information.

Reliability: It refers that the presented data are accurate and valid. It helps the

stakeholders to relay on the data that the data are free from the error, manipulation and any other

illegal practices (Flower and Ebbers, 2018). The reliability characteristics helps attract large

number of investor toward the Tesco.

Understandability: It refers that the presented data and information is in prescribed

format and easily understandable. It helps the users to understand the data and interpret the

financial information for effective and efficient decision-making. It helps Tesco to gain

international customer from the global market.

Comparability: It helps the decision maker or stakeholders to compare the financial

information of different accounting year or to the other companies from the same industry or

other industry (Michelon, Pilonato and Ricceri, 2015). The comparability characteristics helps to

identified that the information are in same format with same methods. It makes the data more

understandable and comparable for Tesco stakeholders.

P3 Key Stakeholders or users of Tesco and how they take benefits from financial information

Stakeholders are those who have an interest in the growth and success of the organization

and they play an important role in Tesco also. The key stakeholders of Tesco are described as

below:

Internal Stakeholders:

Employees: Employees influence Tesco by working efficiently and they always want

that it should succeed as if Tesco will perform effectively it will generate more profits because of

which employees are likely to get more chances of promotion, better salaries and they will also

get a secured job (Maynard., 2017). The financial information is also helpful for employees as

they get knowledge regarding the profits of Tesco because more profits may lead to extra bonus

to them.

3

Managers: Managers are also the main stakeholders of Tesco as they are the persons

who conduct the operation of the organization efficiently. If Managers will make better strategies

and execute them effectively then it will lead to growth of Tesco which might also result in

increasing their part of profits and salaries. They are able to make better plans with the help of

financial information.

External Stakeholders:

Customers: Customers are often considered as key stakeholders who keep major interest

in the Tesco as when they buy a product they always expect it to be of good quality and to

represent appropriate value for their money (Williams and Dobelman, 2017). Financial reporting

helps the customer to identify the position of company in market and compare their performance

with the competitors to take the decision of purchasing products.

Suppliers/Creditors: Suppliers are the persons from whom Tesco purchases products or

services. They keep interest in the performance of the company because they wanted to know

that whether Tesco is able to pay its debts or not (Lang and Stice-Lawrence., 2015). From the

financial information, the lenders or creditors come to know about the financial position of Tesco

as they are always concerned about their debts that they have provided to the company.

Shareholders: Shareholders are also known as key stakeholders of Tesco as they are the

one who invest in the company and get affected from the decisions of management. From

financial information the shareholders also get benefits like they come to know that whether the

profit rate of Tesco is increasing or not as if this rate will increase they will get more dividend.

P4 Value of Financial Reporting:

The financial reporting is very important and valuable for an organization. The financial

Reports are needed by each and every user or stakeholder who keeps interest in Tesco for their

own respective benefits and purposes (Kraft., Vashishtha and Venkatachalam., 2017). So the

preparation and presentation of financial reports should be made properly and efficiently.

However, there are various points that highlights the importance of financial reporting in which

are explained below:

It helps Tesco to comply with various regulatory and statutory requirements as Tesco

is needed to file financial reports to government agencies and ROC. Even Tesco is

required to file its annual as well as quarterly results to stock exchanges and get them

published.

4

who conduct the operation of the organization efficiently. If Managers will make better strategies

and execute them effectively then it will lead to growth of Tesco which might also result in

increasing their part of profits and salaries. They are able to make better plans with the help of

financial information.

External Stakeholders:

Customers: Customers are often considered as key stakeholders who keep major interest

in the Tesco as when they buy a product they always expect it to be of good quality and to

represent appropriate value for their money (Williams and Dobelman, 2017). Financial reporting

helps the customer to identify the position of company in market and compare their performance

with the competitors to take the decision of purchasing products.

Suppliers/Creditors: Suppliers are the persons from whom Tesco purchases products or

services. They keep interest in the performance of the company because they wanted to know

that whether Tesco is able to pay its debts or not (Lang and Stice-Lawrence., 2015). From the

financial information, the lenders or creditors come to know about the financial position of Tesco

as they are always concerned about their debts that they have provided to the company.

Shareholders: Shareholders are also known as key stakeholders of Tesco as they are the

one who invest in the company and get affected from the decisions of management. From

financial information the shareholders also get benefits like they come to know that whether the

profit rate of Tesco is increasing or not as if this rate will increase they will get more dividend.

P4 Value of Financial Reporting:

The financial reporting is very important and valuable for an organization. The financial

Reports are needed by each and every user or stakeholder who keeps interest in Tesco for their

own respective benefits and purposes (Kraft., Vashishtha and Venkatachalam., 2017). So the

preparation and presentation of financial reports should be made properly and efficiently.

However, there are various points that highlights the importance of financial reporting in which

are explained below:

It helps Tesco to comply with various regulatory and statutory requirements as Tesco

is needed to file financial reports to government agencies and ROC. Even Tesco is

required to file its annual as well as quarterly results to stock exchanges and get them

published.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial reporting also facilitates statutory audit as statutory auditors of Tesco are

needed to audit its financial reports or statements to express their views and opinions

(Schroeder., Clark and Cathey, 2019).

Financial Reporting is also considered as the backbone of financial analysis,

planning, decision-making and benchmarking (Progunova and et.al., 2018). On the

basis of financial reports, the top management makes various plans and strategies of

Tesco on the basis of which all the operations and activities are performed. If these

financial reports will be accurate it will help in making better plans which will

ultimately lead to growth and success of Tesco. Financial reporting will help Tesco

in proper decision-making through which it can become easier for Tesco to meets its

organizational goal and objectives.

The another benefit of financial reporting is that it helps in fulfilling the purpose of

labour contract, government supplies and bidding as Tesco is required to furnish all

these purposes in its financial reports and statements.

Financial reporting is valuable and important for Tesco as it helps it to increase

capital both domestic and overseas. As it provides necessary information about

shareholders which might help Tesco to manage its current business operations by

improving interest of investors in investment process.

With the help of financial-reporting the managers can also analyse the performance

of Tesco and if they find any variations between standards and actual performance

then corrective measures are taken for improving the performance (Li., Sougiannis

and Wang., 2017). And actions taken to enhance the performance will ultimately lead

to the accomplishment of its objectives and growth of Tesco.

LO2

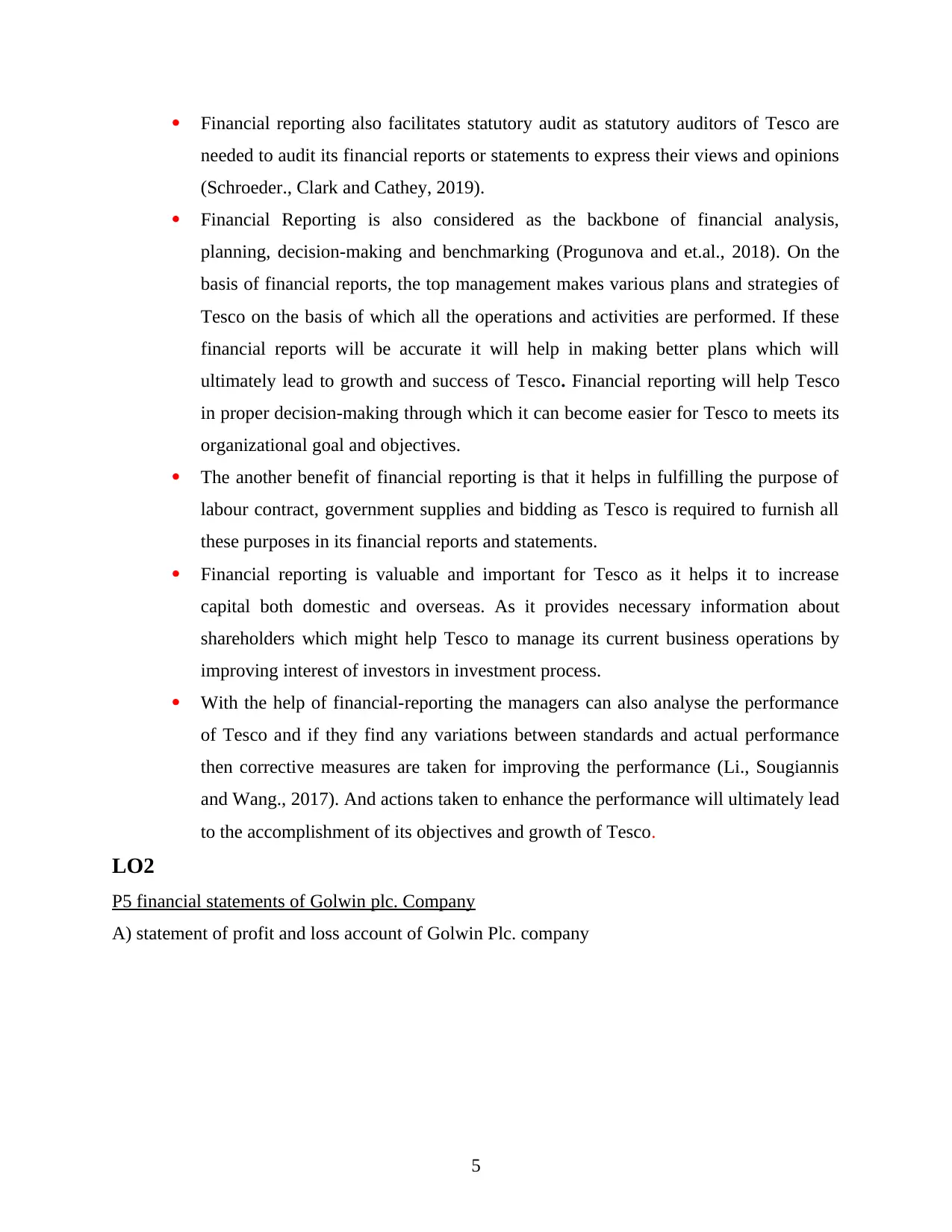

P5 financial statements of Golwin plc. Company

A) statement of profit and loss account of Golwin Plc. company

5

needed to audit its financial reports or statements to express their views and opinions

(Schroeder., Clark and Cathey, 2019).

Financial Reporting is also considered as the backbone of financial analysis,

planning, decision-making and benchmarking (Progunova and et.al., 2018). On the

basis of financial reports, the top management makes various plans and strategies of

Tesco on the basis of which all the operations and activities are performed. If these

financial reports will be accurate it will help in making better plans which will

ultimately lead to growth and success of Tesco. Financial reporting will help Tesco

in proper decision-making through which it can become easier for Tesco to meets its

organizational goal and objectives.

The another benefit of financial reporting is that it helps in fulfilling the purpose of

labour contract, government supplies and bidding as Tesco is required to furnish all

these purposes in its financial reports and statements.

Financial reporting is valuable and important for Tesco as it helps it to increase

capital both domestic and overseas. As it provides necessary information about

shareholders which might help Tesco to manage its current business operations by

improving interest of investors in investment process.

With the help of financial-reporting the managers can also analyse the performance

of Tesco and if they find any variations between standards and actual performance

then corrective measures are taken for improving the performance (Li., Sougiannis

and Wang., 2017). And actions taken to enhance the performance will ultimately lead

to the accomplishment of its objectives and growth of Tesco.

LO2

P5 financial statements of Golwin plc. Company

A) statement of profit and loss account of Golwin Plc. company

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

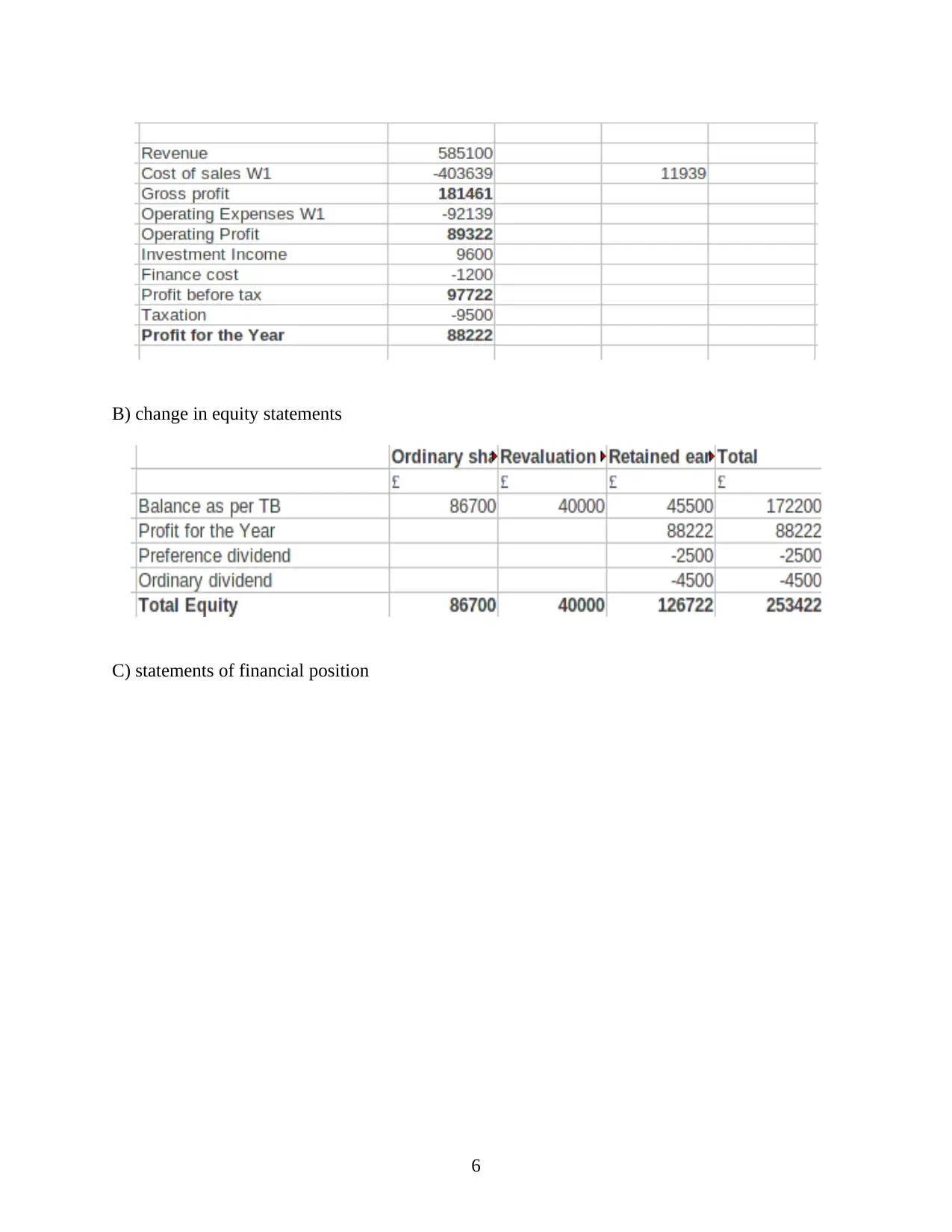

B) change in equity statements

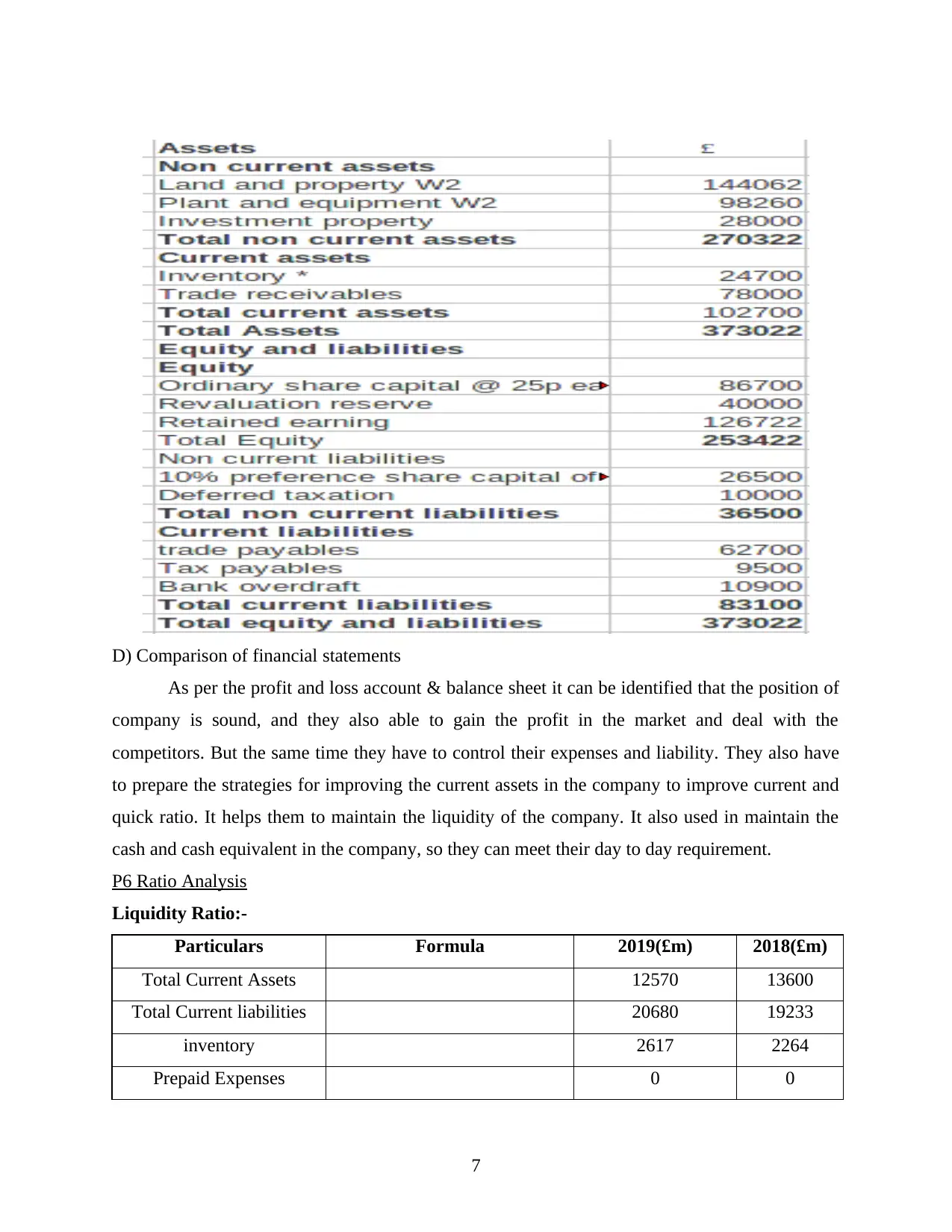

C) statements of financial position

6

C) statements of financial position

6

D) Comparison of financial statements

As per the profit and loss account & balance sheet it can be identified that the position of

company is sound, and they also able to gain the profit in the market and deal with the

competitors. But the same time they have to control their expenses and liability. They also have

to prepare the strategies for improving the current assets in the company to improve current and

quick ratio. It helps them to maintain the liquidity of the company. It also used in maintain the

cash and cash equivalent in the company, so they can meet their day to day requirement.

P6 Ratio Analysis

Liquidity Ratio:-

Particulars Formula 2019(£m) 2018(£m)

Total Current Assets 12570 13600

Total Current liabilities 20680 19233

inventory 2617 2264

Prepaid Expenses 0 0

7

As per the profit and loss account & balance sheet it can be identified that the position of

company is sound, and they also able to gain the profit in the market and deal with the

competitors. But the same time they have to control their expenses and liability. They also have

to prepare the strategies for improving the current assets in the company to improve current and

quick ratio. It helps them to maintain the liquidity of the company. It also used in maintain the

cash and cash equivalent in the company, so they can meet their day to day requirement.

P6 Ratio Analysis

Liquidity Ratio:-

Particulars Formula 2019(£m) 2018(£m)

Total Current Assets 12570 13600

Total Current liabilities 20680 19233

inventory 2617 2264

Prepaid Expenses 0 0

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick Assets Total current Assets-

(inventory+ Prepaid Expenses)

10916 12907

Current Ratio Total current

Assets / Total

Current Liabilities

0.61 0.71

Quick Ratio Quick Assets / Total

Current Liabilities

0.53 0.67

Interpretation: From the above table it is interpreted that the Current Ratio of Tesco is

0.61 in 2018 and 0.71 in 2019. However, it is showing an increase in current ratio but still it is

far from ideal current ratio. The ideal current ratio is considered as 2:1 which depicts the

organization's ability to remain solvent. Apart from that the quick ratio is 0.53 in 2018 and 0.67

in 2019 which is stating a minor increase but it is also less than ideal quick ratio. Generally, the

ideal quick ratio is taken as 1:1 which depicts the liquidity position of the company. Since the

current and quick is less than 1 which means that the liquidity position of Tesco is not sound and

efficient.

Profitability Ratio:

Particulars Formula 2019(£m) 2018(£m)

Sales 63911 57493

Gross Profit 4144 3352

Net Profit 1674 1300

Gross Profit Ratio(%) Gross Profit

/ Sales

6.48 5.83

Net Profit Ratio(%) Net Profit

/ Sales

2.62 2.26

Interpretation: The above table interprets that the Gross profit ratio of Tesco was 5.83%

in 2018 and 6.48% in 2019 Which is showing a minor increase but still it is not considered as the

ideal GP ratio. The ideal GP ratio depicts the gross profits of company after deducting the cost of

goods sold. Apart from that the Net Profit Ratio was 2.26 in 2018 and 2.62 in 2019 and this is

also stating a minor increase in the profit rates. So the net profit rates of Tesco is not taken as

8

(inventory+ Prepaid Expenses)

10916 12907

Current Ratio Total current

Assets / Total

Current Liabilities

0.61 0.71

Quick Ratio Quick Assets / Total

Current Liabilities

0.53 0.67

Interpretation: From the above table it is interpreted that the Current Ratio of Tesco is

0.61 in 2018 and 0.71 in 2019. However, it is showing an increase in current ratio but still it is

far from ideal current ratio. The ideal current ratio is considered as 2:1 which depicts the

organization's ability to remain solvent. Apart from that the quick ratio is 0.53 in 2018 and 0.67

in 2019 which is stating a minor increase but it is also less than ideal quick ratio. Generally, the

ideal quick ratio is taken as 1:1 which depicts the liquidity position of the company. Since the

current and quick is less than 1 which means that the liquidity position of Tesco is not sound and

efficient.

Profitability Ratio:

Particulars Formula 2019(£m) 2018(£m)

Sales 63911 57493

Gross Profit 4144 3352

Net Profit 1674 1300

Gross Profit Ratio(%) Gross Profit

/ Sales

6.48 5.83

Net Profit Ratio(%) Net Profit

/ Sales

2.62 2.26

Interpretation: The above table interprets that the Gross profit ratio of Tesco was 5.83%

in 2018 and 6.48% in 2019 Which is showing a minor increase but still it is not considered as the

ideal GP ratio. The ideal GP ratio depicts the gross profits of company after deducting the cost of

goods sold. Apart from that the Net Profit Ratio was 2.26 in 2018 and 2.62 in 2019 and this is

also stating a minor increase in the profit rates. So the net profit rates of Tesco is not taken as

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ideal net profit ratio. Since the rate of gross and net profit ratio is not indicating the ideal ratio so

it means that Tesco is not using its resources efficiently.

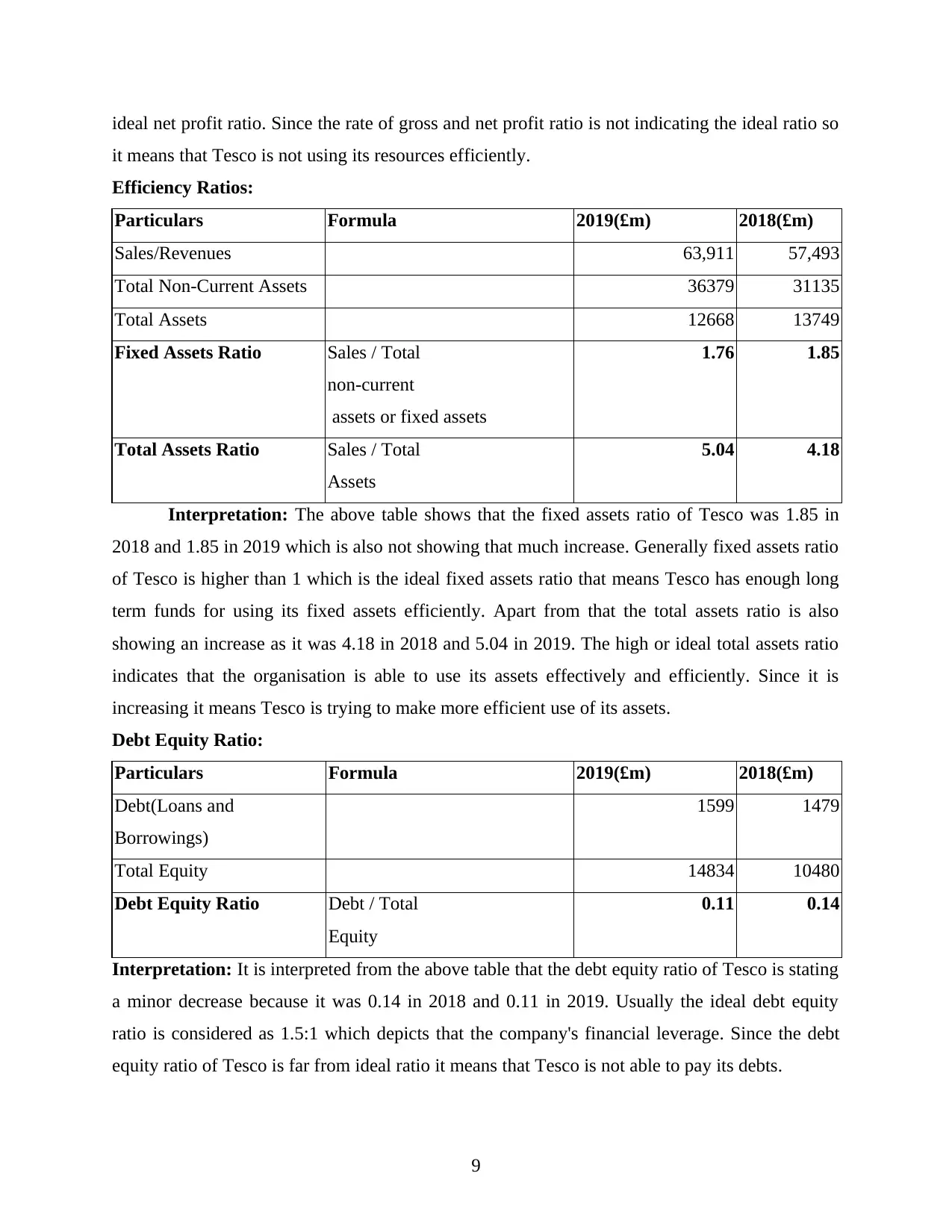

Efficiency Ratios:

Particulars Formula 2019(£m) 2018(£m)

Sales/Revenues 63,911 57,493

Total Non-Current Assets 36379 31135

Total Assets 12668 13749

Fixed Assets Ratio Sales / Total

non-current

assets or fixed assets

1.76 1.85

Total Assets Ratio Sales / Total

Assets

5.04 4.18

Interpretation: The above table shows that the fixed assets ratio of Tesco was 1.85 in

2018 and 1.85 in 2019 which is also not showing that much increase. Generally fixed assets ratio

of Tesco is higher than 1 which is the ideal fixed assets ratio that means Tesco has enough long

term funds for using its fixed assets efficiently. Apart from that the total assets ratio is also

showing an increase as it was 4.18 in 2018 and 5.04 in 2019. The high or ideal total assets ratio

indicates that the organisation is able to use its assets effectively and efficiently. Since it is

increasing it means Tesco is trying to make more efficient use of its assets.

Debt Equity Ratio:

Particulars Formula 2019(£m) 2018(£m)

Debt(Loans and

Borrowings)

1599 1479

Total Equity 14834 10480

Debt Equity Ratio Debt / Total

Equity

0.11 0.14

Interpretation: It is interpreted from the above table that the debt equity ratio of Tesco is stating

a minor decrease because it was 0.14 in 2018 and 0.11 in 2019. Usually the ideal debt equity

ratio is considered as 1.5:1 which depicts that the company's financial leverage. Since the debt

equity ratio of Tesco is far from ideal ratio it means that Tesco is not able to pay its debts.

9

it means that Tesco is not using its resources efficiently.

Efficiency Ratios:

Particulars Formula 2019(£m) 2018(£m)

Sales/Revenues 63,911 57,493

Total Non-Current Assets 36379 31135

Total Assets 12668 13749

Fixed Assets Ratio Sales / Total

non-current

assets or fixed assets

1.76 1.85

Total Assets Ratio Sales / Total

Assets

5.04 4.18

Interpretation: The above table shows that the fixed assets ratio of Tesco was 1.85 in

2018 and 1.85 in 2019 which is also not showing that much increase. Generally fixed assets ratio

of Tesco is higher than 1 which is the ideal fixed assets ratio that means Tesco has enough long

term funds for using its fixed assets efficiently. Apart from that the total assets ratio is also

showing an increase as it was 4.18 in 2018 and 5.04 in 2019. The high or ideal total assets ratio

indicates that the organisation is able to use its assets effectively and efficiently. Since it is

increasing it means Tesco is trying to make more efficient use of its assets.

Debt Equity Ratio:

Particulars Formula 2019(£m) 2018(£m)

Debt(Loans and

Borrowings)

1599 1479

Total Equity 14834 10480

Debt Equity Ratio Debt / Total

Equity

0.11 0.14

Interpretation: It is interpreted from the above table that the debt equity ratio of Tesco is stating

a minor decrease because it was 0.14 in 2018 and 0.11 in 2019. Usually the ideal debt equity

ratio is considered as 1.5:1 which depicts that the company's financial leverage. Since the debt

equity ratio of Tesco is far from ideal ratio it means that Tesco is not able to pay its debts.

9

LO3

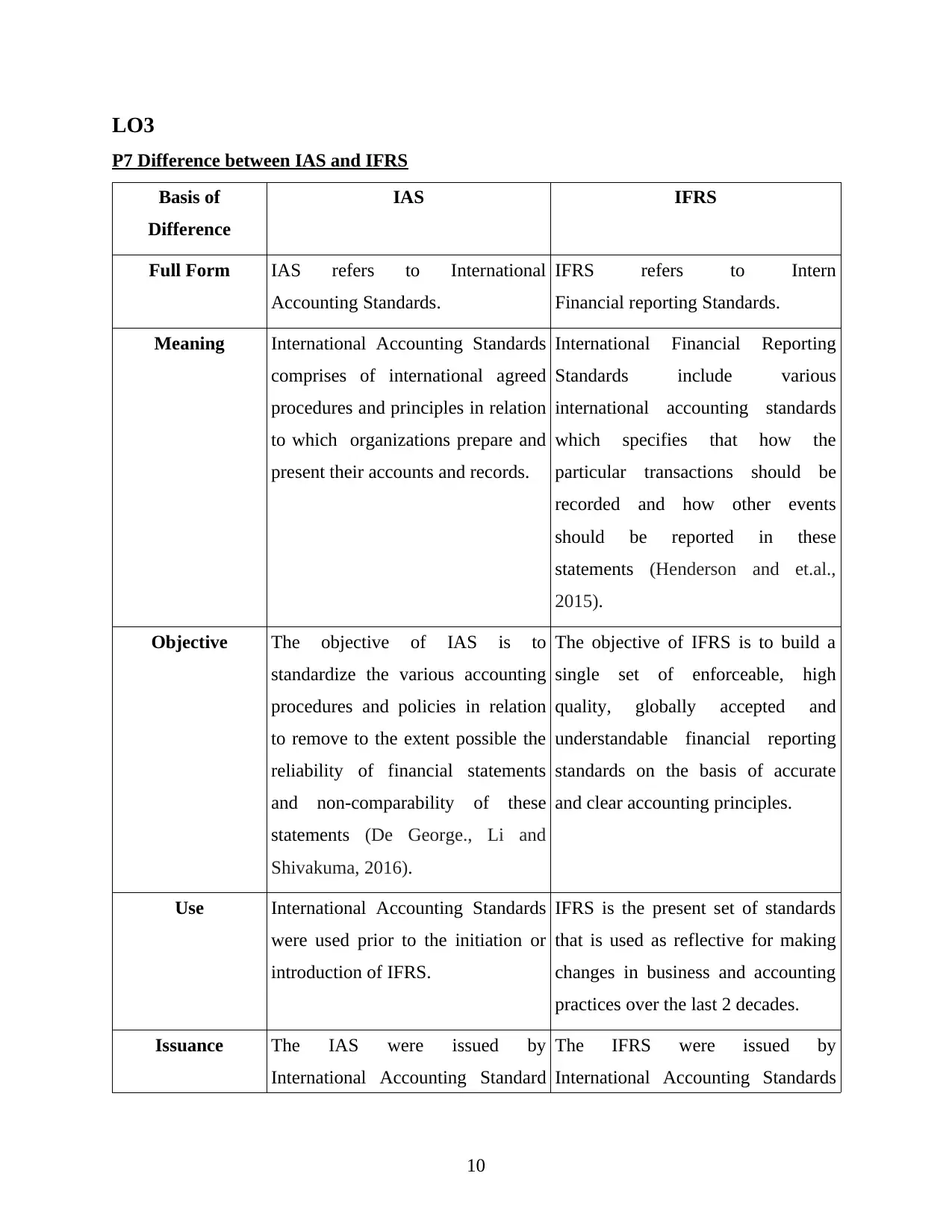

P7 Difference between IAS and IFRS

Basis of

Difference

IAS IFRS

Full Form IAS refers to International

Accounting Standards.

IFRS refers to Intern

Financial reporting Standards.

Meaning International Accounting Standards

comprises of international agreed

procedures and principles in relation

to which organizations prepare and

present their accounts and records.

International Financial Reporting

Standards include various

international accounting standards

which specifies that how the

particular transactions should be

recorded and how other events

should be reported in these

statements (Henderson and et.al.,

2015).

Objective The objective of IAS is to

standardize the various accounting

procedures and policies in relation

to remove to the extent possible the

reliability of financial statements

and non-comparability of these

statements (De George., Li and

Shivakuma, 2016).

The objective of IFRS is to build a

single set of enforceable, high

quality, globally accepted and

understandable financial reporting

standards on the basis of accurate

and clear accounting principles.

Use International Accounting Standards

were used prior to the initiation or

introduction of IFRS.

IFRS is the present set of standards

that is used as reflective for making

changes in business and accounting

practices over the last 2 decades.

Issuance The IAS were issued by

International Accounting Standard

The IFRS were issued by

International Accounting Standards

10

P7 Difference between IAS and IFRS

Basis of

Difference

IAS IFRS

Full Form IAS refers to International

Accounting Standards.

IFRS refers to Intern

Financial reporting Standards.

Meaning International Accounting Standards

comprises of international agreed

procedures and principles in relation

to which organizations prepare and

present their accounts and records.

International Financial Reporting

Standards include various

international accounting standards

which specifies that how the

particular transactions should be

recorded and how other events

should be reported in these

statements (Henderson and et.al.,

2015).

Objective The objective of IAS is to

standardize the various accounting

procedures and policies in relation

to remove to the extent possible the

reliability of financial statements

and non-comparability of these

statements (De George., Li and

Shivakuma, 2016).

The objective of IFRS is to build a

single set of enforceable, high

quality, globally accepted and

understandable financial reporting

standards on the basis of accurate

and clear accounting principles.

Use International Accounting Standards

were used prior to the initiation or

introduction of IFRS.

IFRS is the present set of standards

that is used as reflective for making

changes in business and accounting

practices over the last 2 decades.

Issuance The IAS were issued by

International Accounting Standard

The IFRS were issued by

International Accounting Standards

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.