AP Eagers Limited: Analysis of Conceptual Framework Compliance

VerifiedAdded on 2023/05/28

|20

|2575

|95

Report

AI Summary

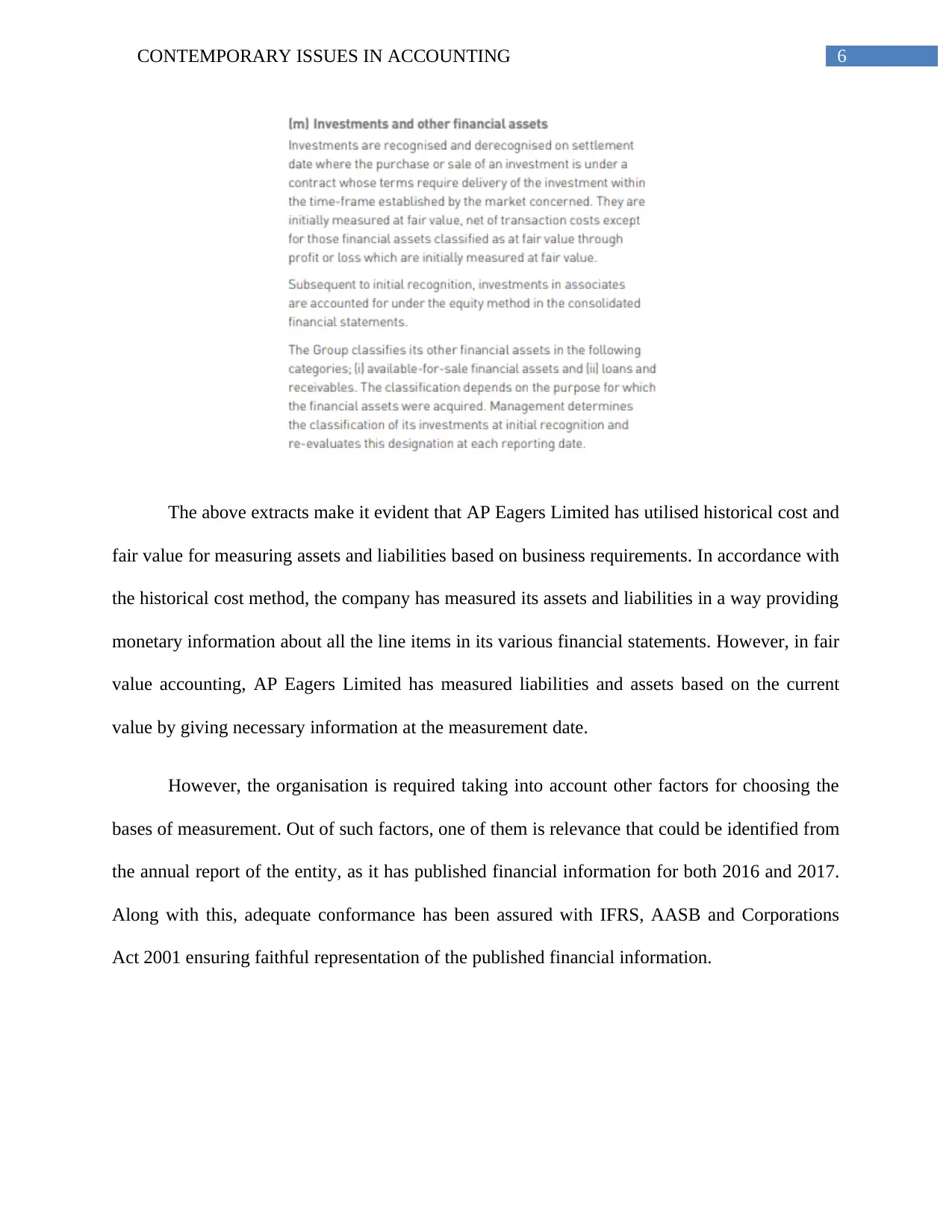

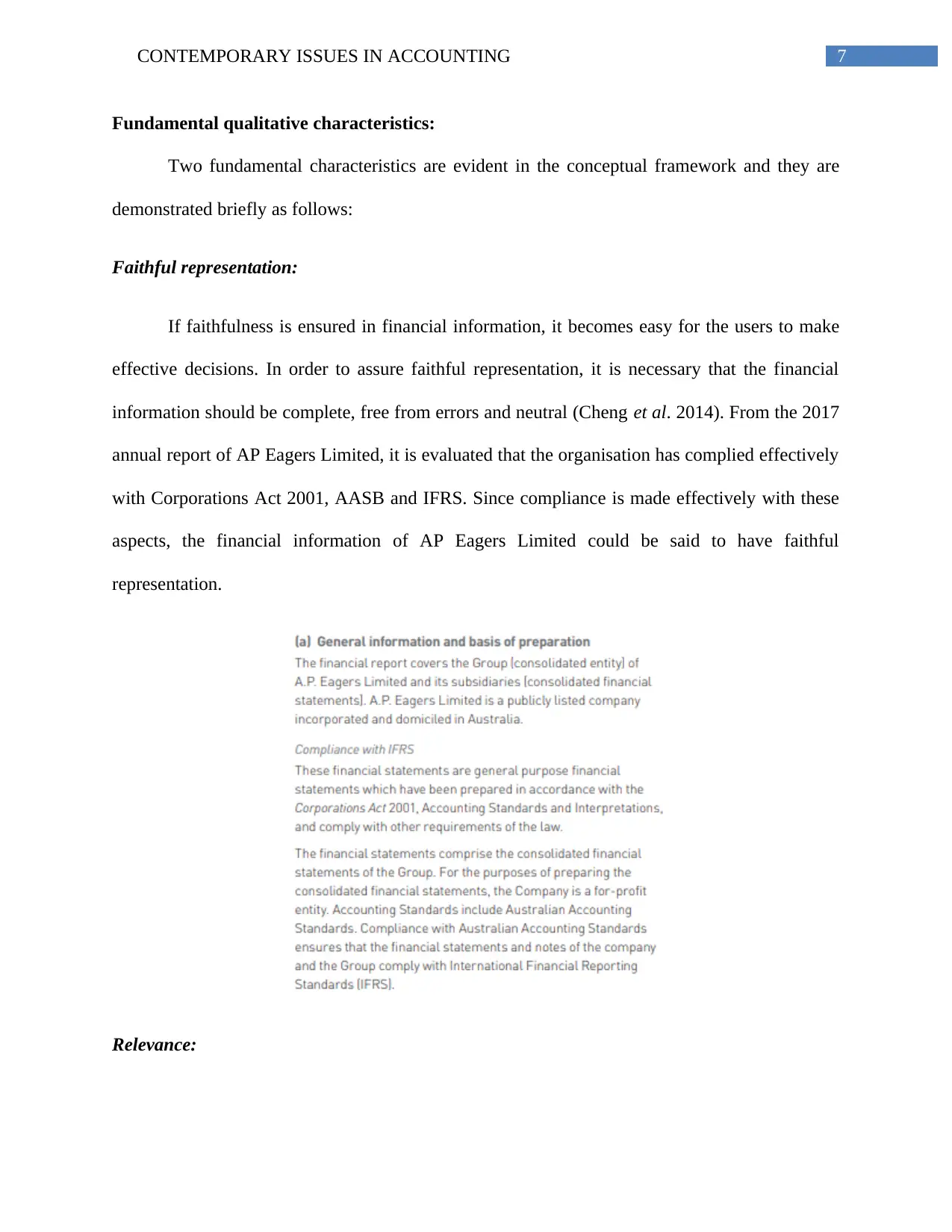

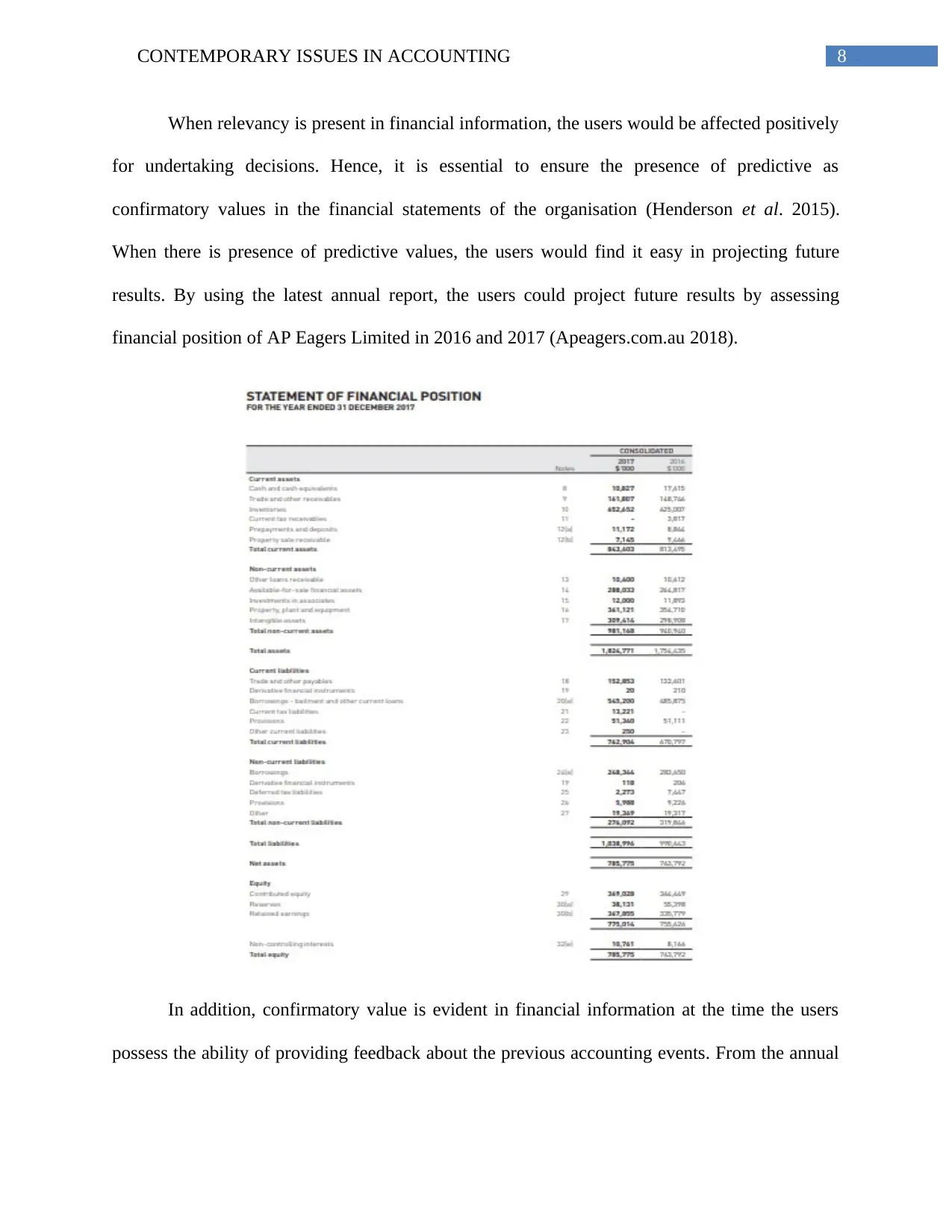

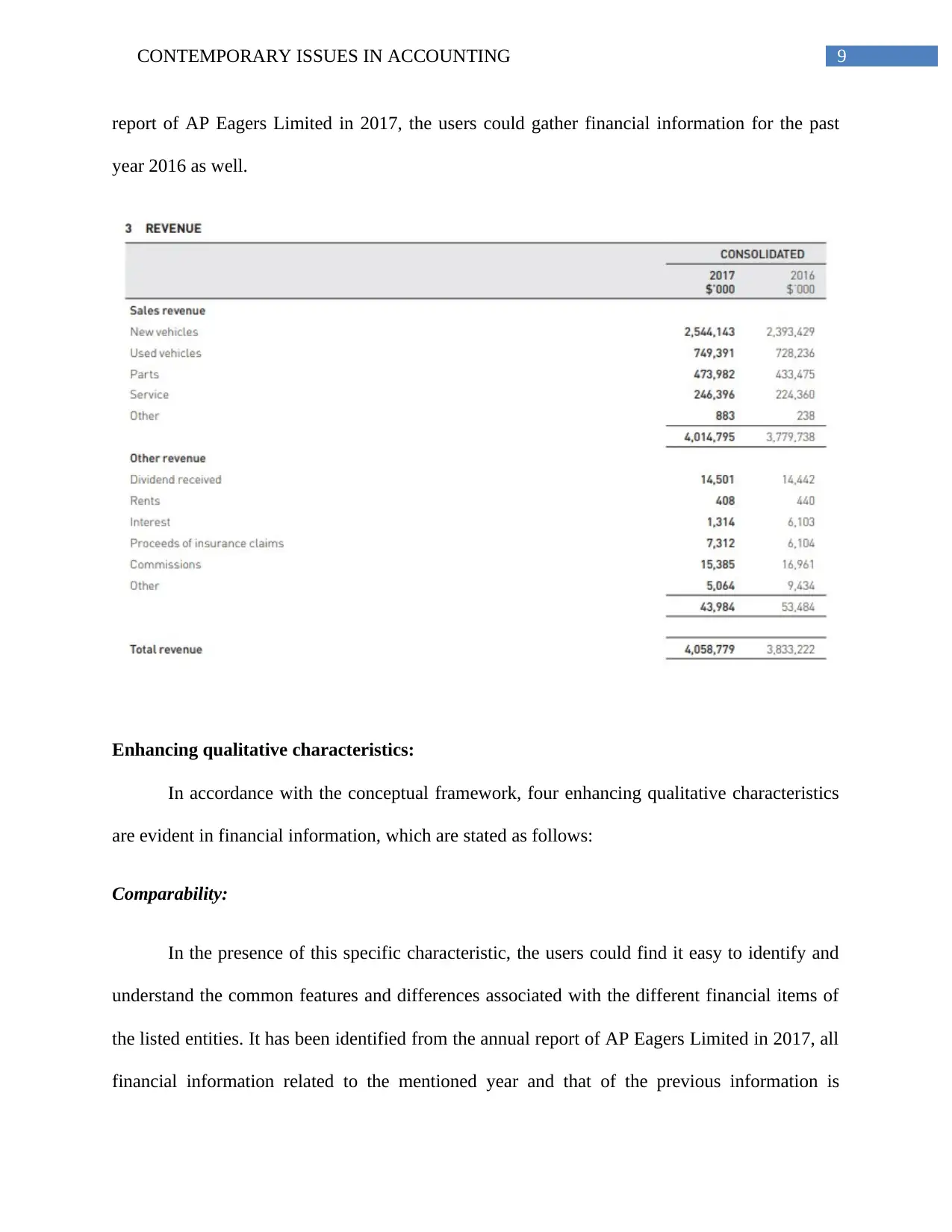

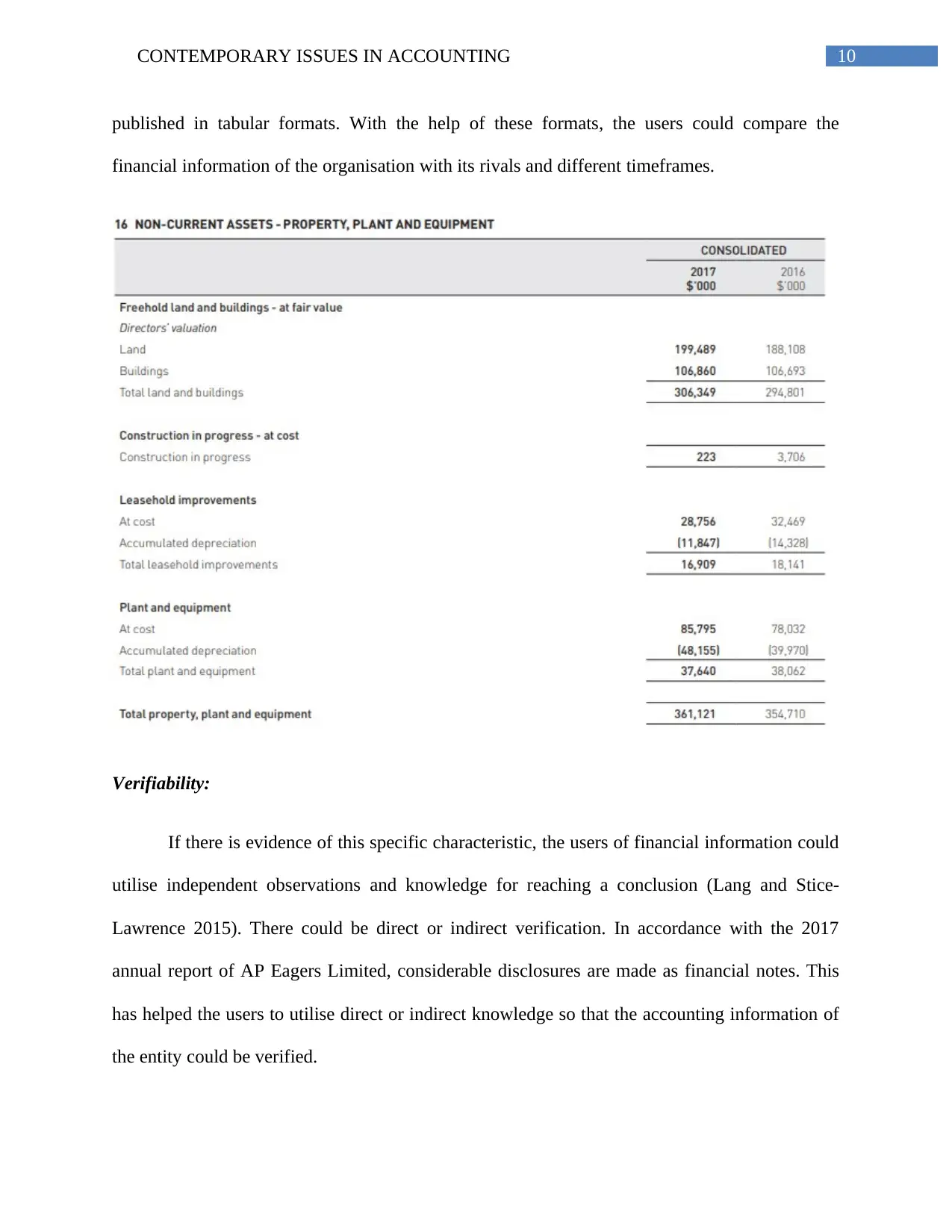

This report provides a comprehensive analysis of AP Eagers Limited's financial reporting practices in relation to the conceptual framework. It begins with an executive summary and an overview of the company's background as an ASX-listed automotive retail group. The report then delves into the measurement requirements of the conceptual framework, examining the company's use of historical cost and fair value in measuring assets and liabilities, and its adherence to relevance and faithful representation. The analysis continues with an assessment of the fundamental and enhancing qualitative characteristics of financial information, including comparability, verifiability, timeliness, and understandability. Furthermore, the report evaluates the ability of users to utilize AP Eagers Limited's financial statements for decision-making, considering the objectives of the conceptual framework, such as disclosing information about financial position, performance, and cash flows. It also addresses the knowledge needed for business analysis and the requirements for general-purpose financial reporting. The report concludes with recommendations for improving financial reporting practices, such as implementing internal audits and ensuring proper revenue recognition and disclosure of goodwill impairments.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.