University Financial Reporting and Analysis I Assignment Solution

VerifiedAdded on 2022/12/09

|7

|1137

|492

Homework Assignment

AI Summary

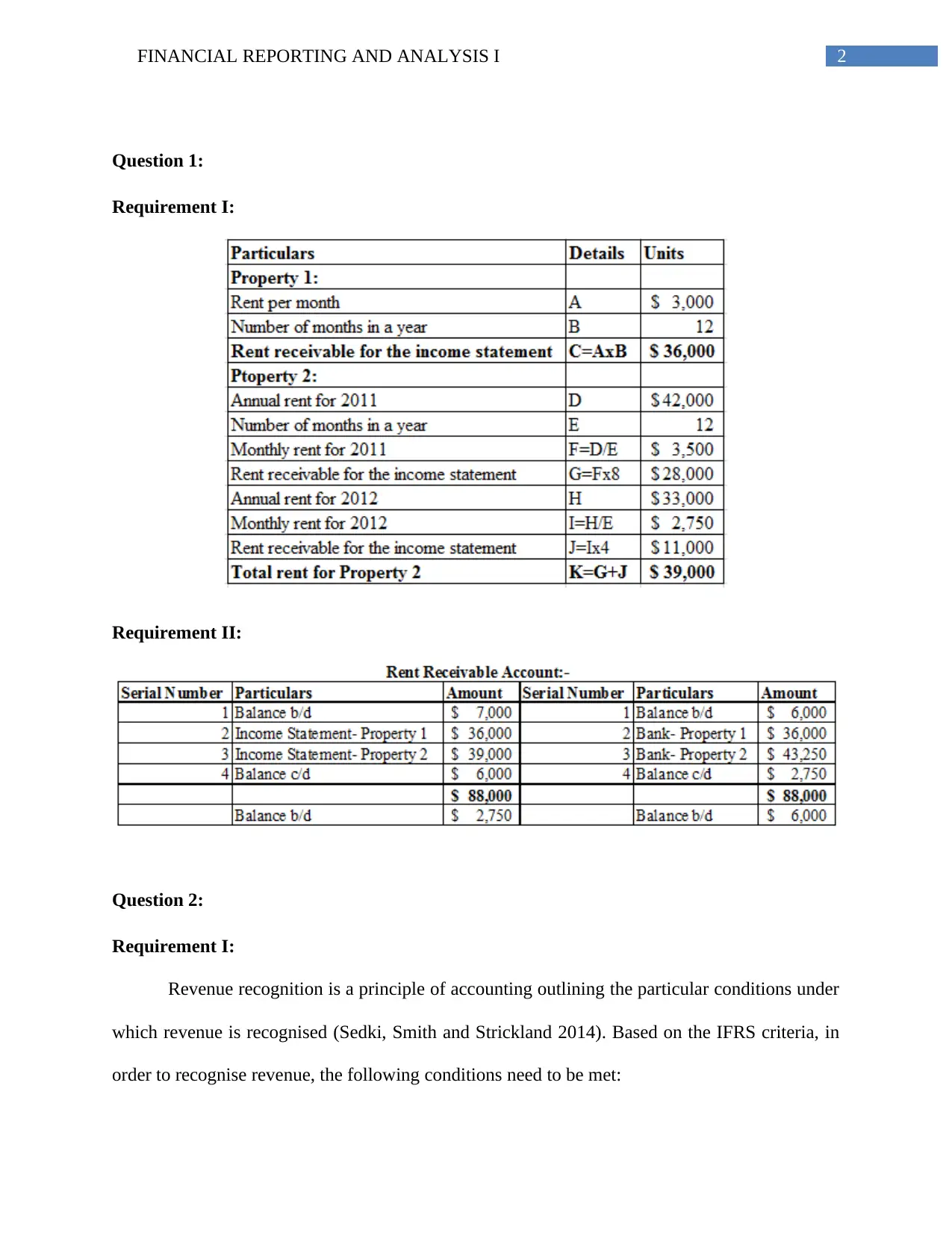

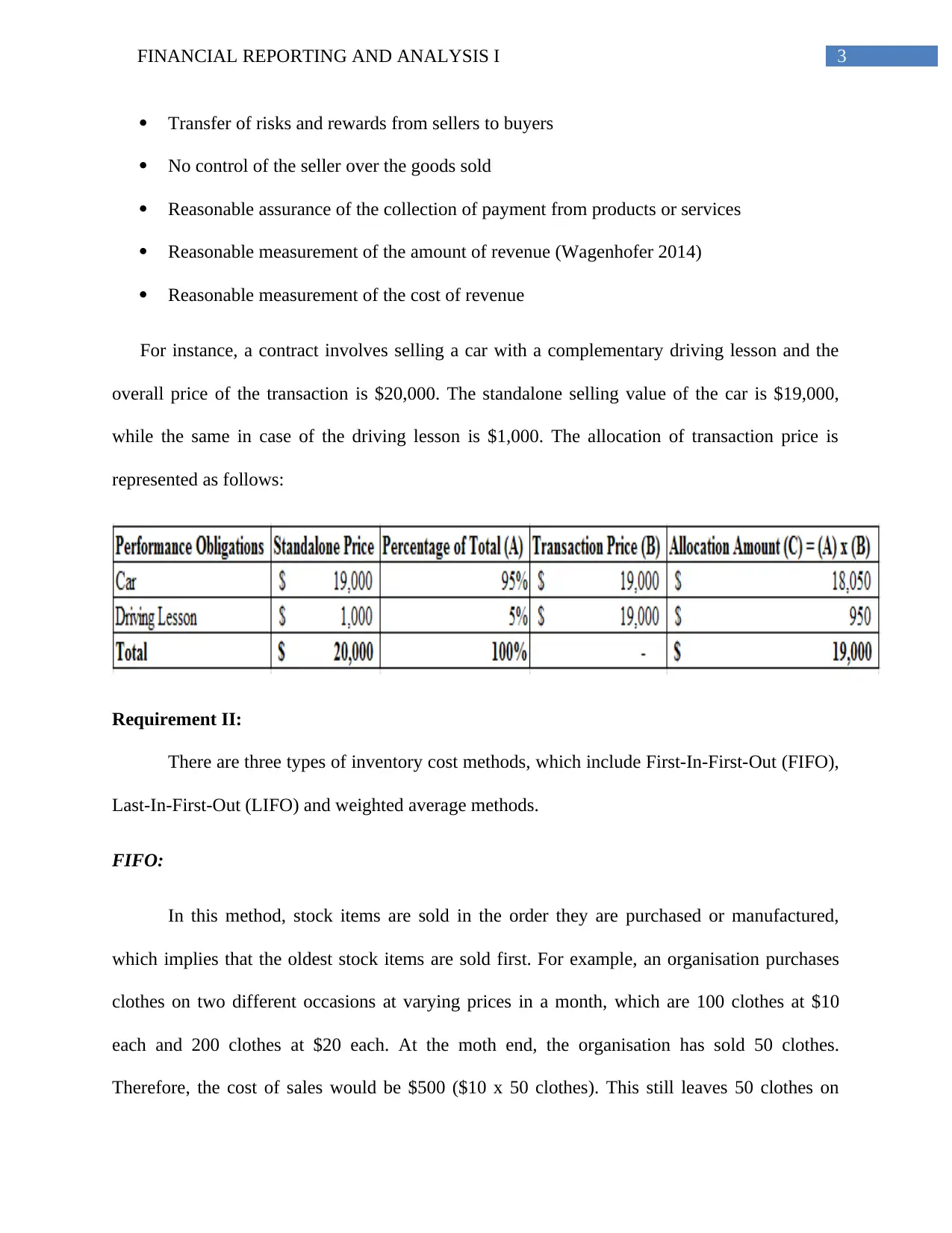

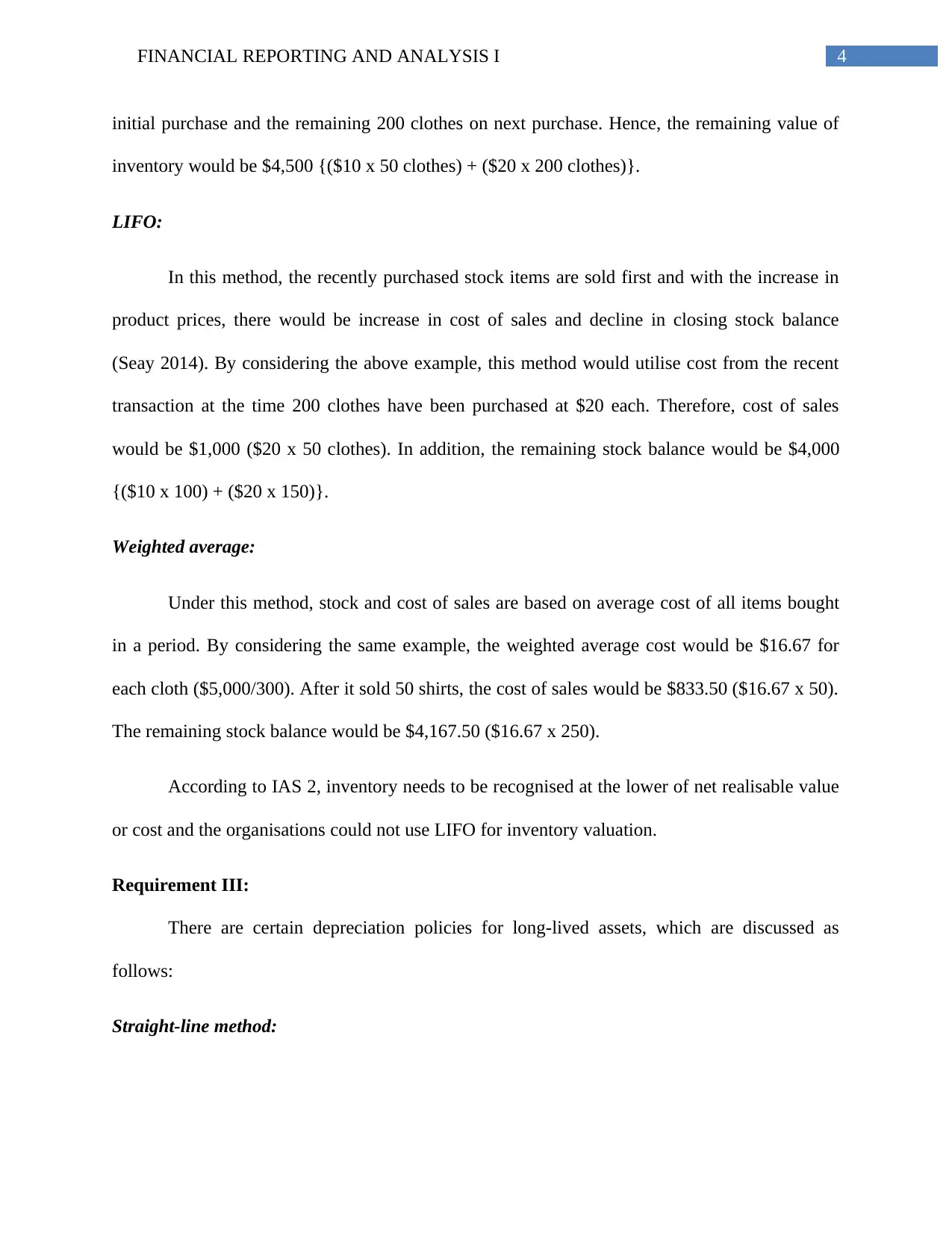

This assignment solution for Financial Reporting and Analysis I addresses key accounting concepts. It begins with an explanation of revenue recognition, outlining the conditions under which revenue is recognized according to IFRS, and provides an example of transaction price allocation. The solution then delves into inventory cost methods, including First-In-First-Out (FIFO), Last-In-First-Out (LIFO), and weighted average methods, with examples illustrating their application. Finally, the assignment explores depreciation policies for long-lived assets, covering the straight-line method, accelerated depreciation, and the declining balance method, providing examples for each. The assignment is well-structured, providing a clear understanding of the concepts discussed. The solution is well-researched and supported by relevant references.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.