Financial Reporting Disclosures in Australian Corporate Sector Report

VerifiedAdded on 2020/03/16

|12

|2119

|33

Report

AI Summary

This report provides a detailed analysis of financial reporting disclosures within the Australian corporate sector, focusing on the application of AASB 116 and the identification of relevant qualitative characteristics as per the Conceptual Framework for Financial Reporting. The report examines the financial statements of Monash Ivf Group Limited, assessing their compliance with accounting standards, particularly regarding depreciation methods and the treatment of agricultural bearer plants. It identifies relevance and understandability as key qualitative characteristics and evaluates how the company meets these criteria through its disclosures. The report also discusses areas for improvement, such as incorporating materiality aspects and enhancing comparability. The analysis includes an overview of the primary users of General Purpose Financial Reporting (GPFR) and the rationale behind it, providing a comprehensive view of the financial reporting landscape in Australia.

Running head: FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN

CORPORATE SECTOR

Financial Reporting Disclosures in the Australian Corporate Sector

Name of Student:

Name of University:

Author’s Note:

CORPORATE SECTOR

Financial Reporting Disclosures in the Australian Corporate Sector

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................3

Body.................................................................................................................................................3

Answer to Part A.........................................................................................................................3

Answer to Part B..........................................................................................................................4

Answer to Part C..........................................................................................................................5

Answer to Part D.........................................................................................................................6

Conclusion.......................................................................................................................................7

Reference list...................................................................................................................................8

List of Appendix..............................................................................................................................9

Appendix 1...................................................................................................................................9

Appendix 2...................................................................................................................................9

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................3

Body.................................................................................................................................................3

Answer to Part A.........................................................................................................................3

Answer to Part B..........................................................................................................................4

Answer to Part C..........................................................................................................................5

Answer to Part D.........................................................................................................................6

Conclusion.......................................................................................................................................7

Reference list...................................................................................................................................8

List of Appendix..............................................................................................................................9

Appendix 1...................................................................................................................................9

Appendix 2...................................................................................................................................9

2

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Executive summary

The report is intended to state on the qualitative characteristics mentioned as per “General

Purpose Financial Reporting (GPFR)”. In order to perform the analysis, Monash Ivf Group

Limited has been selected. Based on QC-1 to QC-39 some of the fundamental qualitative

characteristics as for the conceptual framework has been identified in terms of relevance,

materiality, faithful representation, verifiability, timeliness, understandability and consideration

of cost constraint. “Monash Ivf Group Limited” published in the year 2016, it has been discerned

that the clarification for the acceptable method of depreciation and amortisation are done based

on “Amendments to AASB 116 and AASB 138”. Another important application of

“Amendments to AASB 116 and AASB 141” has been evident with agricultural bearer plants.

Among the several types of “qualitative characteristics” useful for financial information as per

conceptual framework for financial reporting, “relevance” and “understandability” has been

identified as the two main “qualitative characteristics for “Monash Ivf Group Limited”. The

company has been able to recognise the PPE values in the balance sheet with utmost “relevance”

to the prescribed guidelines. It has been further able to identify the percentage change in property

expenses for both present and previous financial year. The “understandability” factor has been

covered with concisely segregating the PPE values for the present and previous year in the

annual report. The “understandability” aspect has been duly maintained by clearly stating about

the contractual commitment for the acquisition of PPE.The company needs to take several

improvements which are associated to improve the financial reporting by including the scope

base types of materiality aspects in the financial report.

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Executive summary

The report is intended to state on the qualitative characteristics mentioned as per “General

Purpose Financial Reporting (GPFR)”. In order to perform the analysis, Monash Ivf Group

Limited has been selected. Based on QC-1 to QC-39 some of the fundamental qualitative

characteristics as for the conceptual framework has been identified in terms of relevance,

materiality, faithful representation, verifiability, timeliness, understandability and consideration

of cost constraint. “Monash Ivf Group Limited” published in the year 2016, it has been discerned

that the clarification for the acceptable method of depreciation and amortisation are done based

on “Amendments to AASB 116 and AASB 138”. Another important application of

“Amendments to AASB 116 and AASB 141” has been evident with agricultural bearer plants.

Among the several types of “qualitative characteristics” useful for financial information as per

conceptual framework for financial reporting, “relevance” and “understandability” has been

identified as the two main “qualitative characteristics for “Monash Ivf Group Limited”. The

company has been able to recognise the PPE values in the balance sheet with utmost “relevance”

to the prescribed guidelines. It has been further able to identify the percentage change in property

expenses for both present and previous financial year. The “understandability” factor has been

covered with concisely segregating the PPE values for the present and previous year in the

annual report. The “understandability” aspect has been duly maintained by clearly stating about

the contractual commitment for the acquisition of PPE.The company needs to take several

improvements which are associated to improve the financial reporting by including the scope

base types of materiality aspects in the financial report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Introduction

The report is aimed to highlight on the main users of “General Purpose Financial

Reporting (GPFR)” along with the rationale for the same. It also defines the qualitative

characteristics mentioned as per the standard. The next section of the report has anyone related to

what extent the latest and will report for a company listed under ASX 300 Index has been able to

meet the criteria for disclosure requirement for “AASB 116”. It has been particularly ensured

that the company is having 30th June as the year-end. In order to perform the analysis, Monash

Ivf Group Limited has been selected. Based on the analysis on the disclosures compliance the

report has been able to suggest on two qualitative enhancing characteristics for the selected

company. The latter part of the report has been able to critically discuss on the disclosures on

meeting the PPE criteria for the primary users.

Body

Answer to Part A

Citizens of a country are identified as the primary users of GPFRs. The legislature or a

alike body along with Parliament member or alike representatives are also considered as an

important user for GPFR. Citizens are regarded as primary users of GPFR as they receive and

provide service at the same time to the government and other public sector entities, henceforth

they need to rely on GPFRs for the necessary information which aides in decision-making

purposes and accountability (Cnc.min-financas.pt. 2017).

As per OB 5 to OB 10, the “qualitative characteristics” of functional information as per

the “Conceptual Framework for Financial Reporting” states that several existing potential

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Introduction

The report is aimed to highlight on the main users of “General Purpose Financial

Reporting (GPFR)” along with the rationale for the same. It also defines the qualitative

characteristics mentioned as per the standard. The next section of the report has anyone related to

what extent the latest and will report for a company listed under ASX 300 Index has been able to

meet the criteria for disclosure requirement for “AASB 116”. It has been particularly ensured

that the company is having 30th June as the year-end. In order to perform the analysis, Monash

Ivf Group Limited has been selected. Based on the analysis on the disclosures compliance the

report has been able to suggest on two qualitative enhancing characteristics for the selected

company. The latter part of the report has been able to critically discuss on the disclosures on

meeting the PPE criteria for the primary users.

Body

Answer to Part A

Citizens of a country are identified as the primary users of GPFRs. The legislature or a

alike body along with Parliament member or alike representatives are also considered as an

important user for GPFR. Citizens are regarded as primary users of GPFR as they receive and

provide service at the same time to the government and other public sector entities, henceforth

they need to rely on GPFRs for the necessary information which aides in decision-making

purposes and accountability (Cnc.min-financas.pt. 2017).

As per OB 5 to OB 10, the “qualitative characteristics” of functional information as per

the “Conceptual Framework for Financial Reporting” states that several existing potential

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

investors and lenders along with additional creditors cannot require the reporting entities for

providing information directly to them and should consistently rely on the requirements for

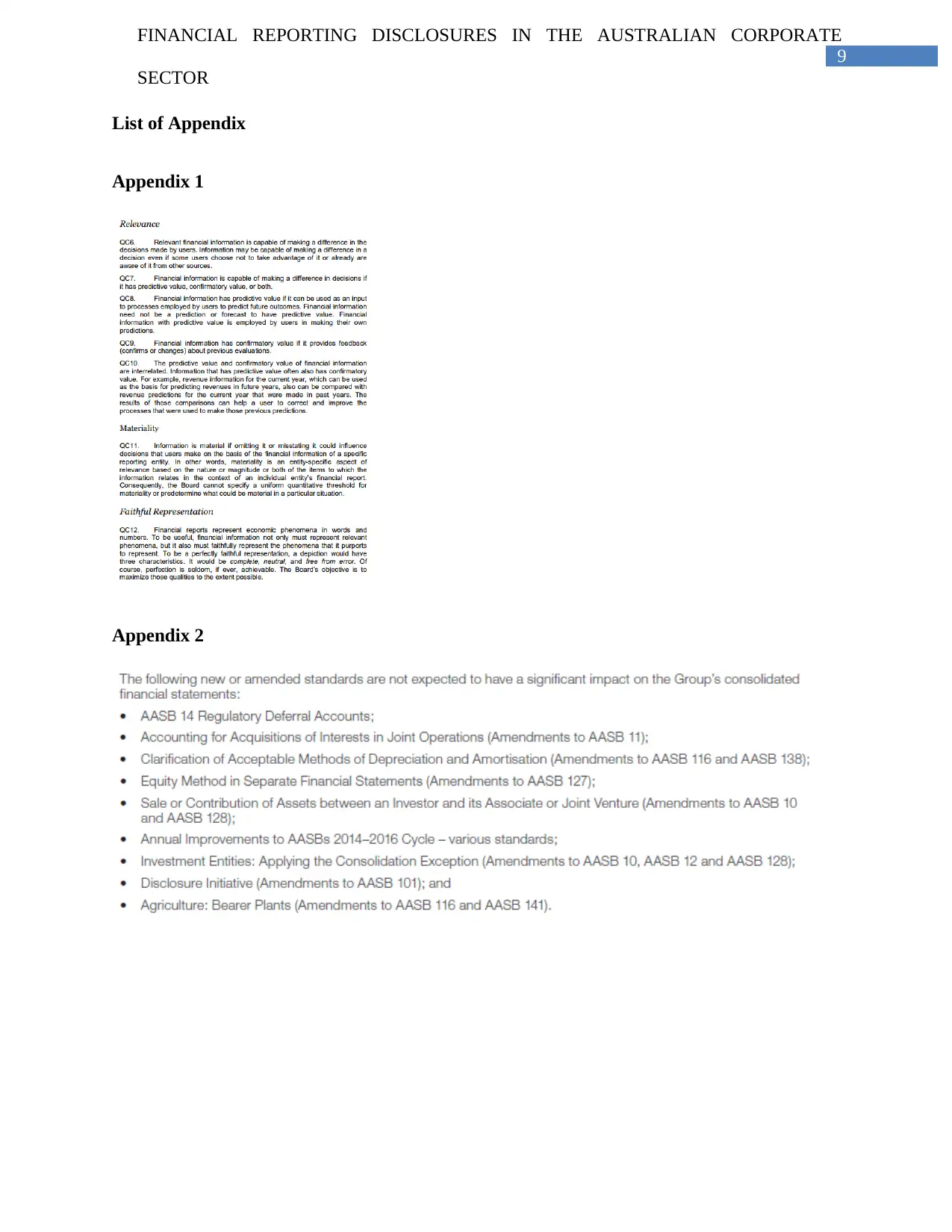

general purpose reports. Based on QC-1 to QC-39 some of the fundamental qualitative

characteristics as for the conceptual framework has been identified in terms of relevance,

materiality, faithful representation, verifiability, timeliness, understandability and consideration

of cost constraint. The same has been represented in the “Appendix 1” of the study. The faithful

representation aspect of the financial information has been identified in terms of potential to

make a difference in decisions depiction of complete, neutral and error free report. The main

objective of the board has been seen in terms of maximising the quality as much as possible

(Fasb.org. 2017).

Answer to Part B

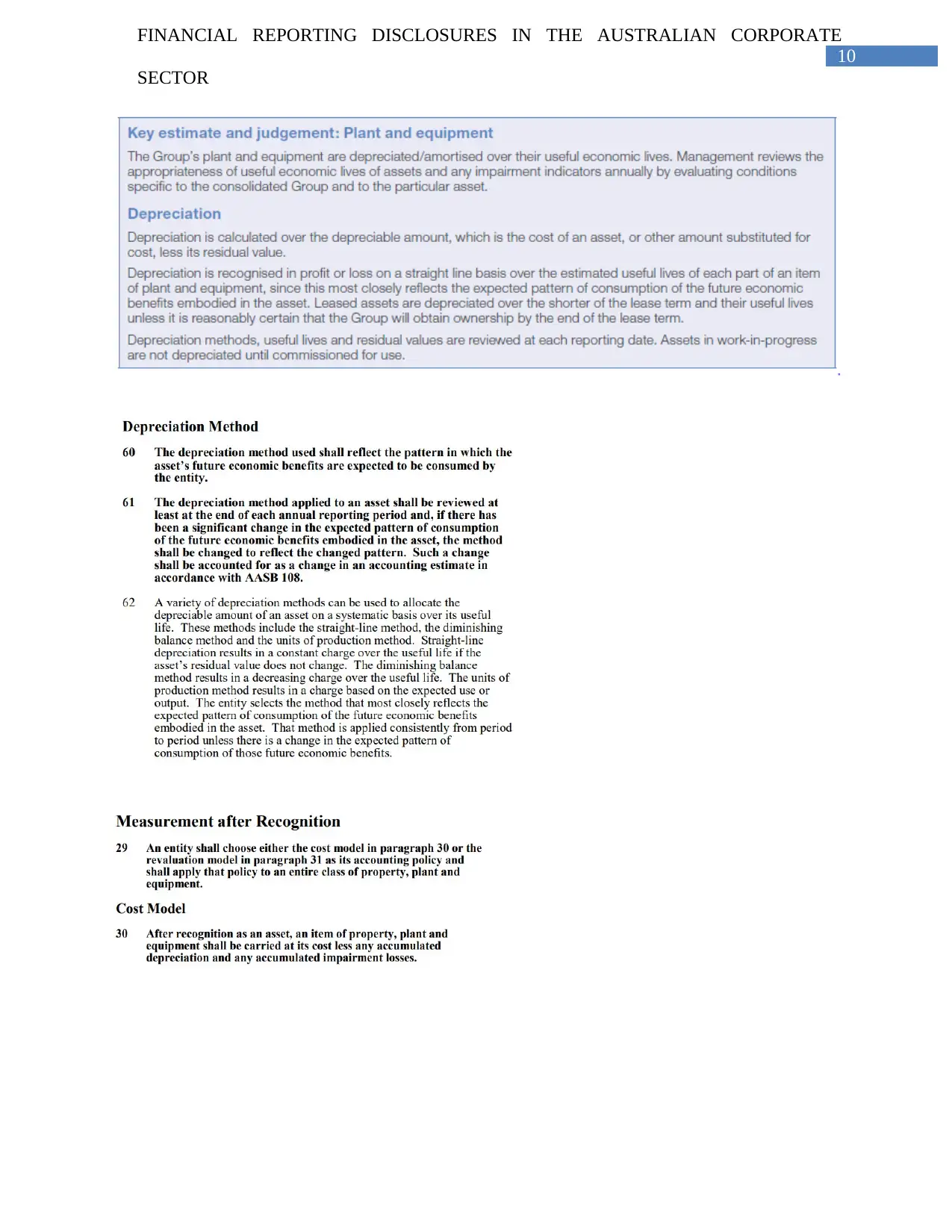

Based on the depiction of annual report of “Monash Ivf Group Limited” published in the

year 2016, it has been discerned that the clarification for the acceptable method of depreciation

and amortisation are done based on “Amendments to AASB 116 and AASB 138”. Another

important application of “Amendments to AASB 116 and AASB 141” has been evident with

agricultural bearer plants.

Under “Section 30” of “AASB 116” (Cost model), the measurement of recognition under

the cost model states that after recognising an asset such as PPE, the total amount should be

carried as per the cost less any accumulated reduction and impairment losses. In a similar way,

“Monash Ivf Group Limited” has performed the key estimate and judgement for equipment by

depreciating/amortising over its useful economic life. In addition to this, the depreciation amount

has been substituted for cost, less its residual value. The depreciation method for the company

has been further identified with profit or loss on “straight-line basis” over the estimated useful

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

investors and lenders along with additional creditors cannot require the reporting entities for

providing information directly to them and should consistently rely on the requirements for

general purpose reports. Based on QC-1 to QC-39 some of the fundamental qualitative

characteristics as for the conceptual framework has been identified in terms of relevance,

materiality, faithful representation, verifiability, timeliness, understandability and consideration

of cost constraint. The same has been represented in the “Appendix 1” of the study. The faithful

representation aspect of the financial information has been identified in terms of potential to

make a difference in decisions depiction of complete, neutral and error free report. The main

objective of the board has been seen in terms of maximising the quality as much as possible

(Fasb.org. 2017).

Answer to Part B

Based on the depiction of annual report of “Monash Ivf Group Limited” published in the

year 2016, it has been discerned that the clarification for the acceptable method of depreciation

and amortisation are done based on “Amendments to AASB 116 and AASB 138”. Another

important application of “Amendments to AASB 116 and AASB 141” has been evident with

agricultural bearer plants.

Under “Section 30” of “AASB 116” (Cost model), the measurement of recognition under

the cost model states that after recognising an asset such as PPE, the total amount should be

carried as per the cost less any accumulated reduction and impairment losses. In a similar way,

“Monash Ivf Group Limited” has performed the key estimate and judgement for equipment by

depreciating/amortising over its useful economic life. In addition to this, the depreciation amount

has been substituted for cost, less its residual value. The depreciation method for the company

has been further identified with profit or loss on “straight-line basis” over the estimated useful

5

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

life of PPE. This is indirectly seen in terms of compliance with depreciation method stated under

“Section 62” of “AASB 116” (Annualreport2016.monashivfgroup.com.au 2017).

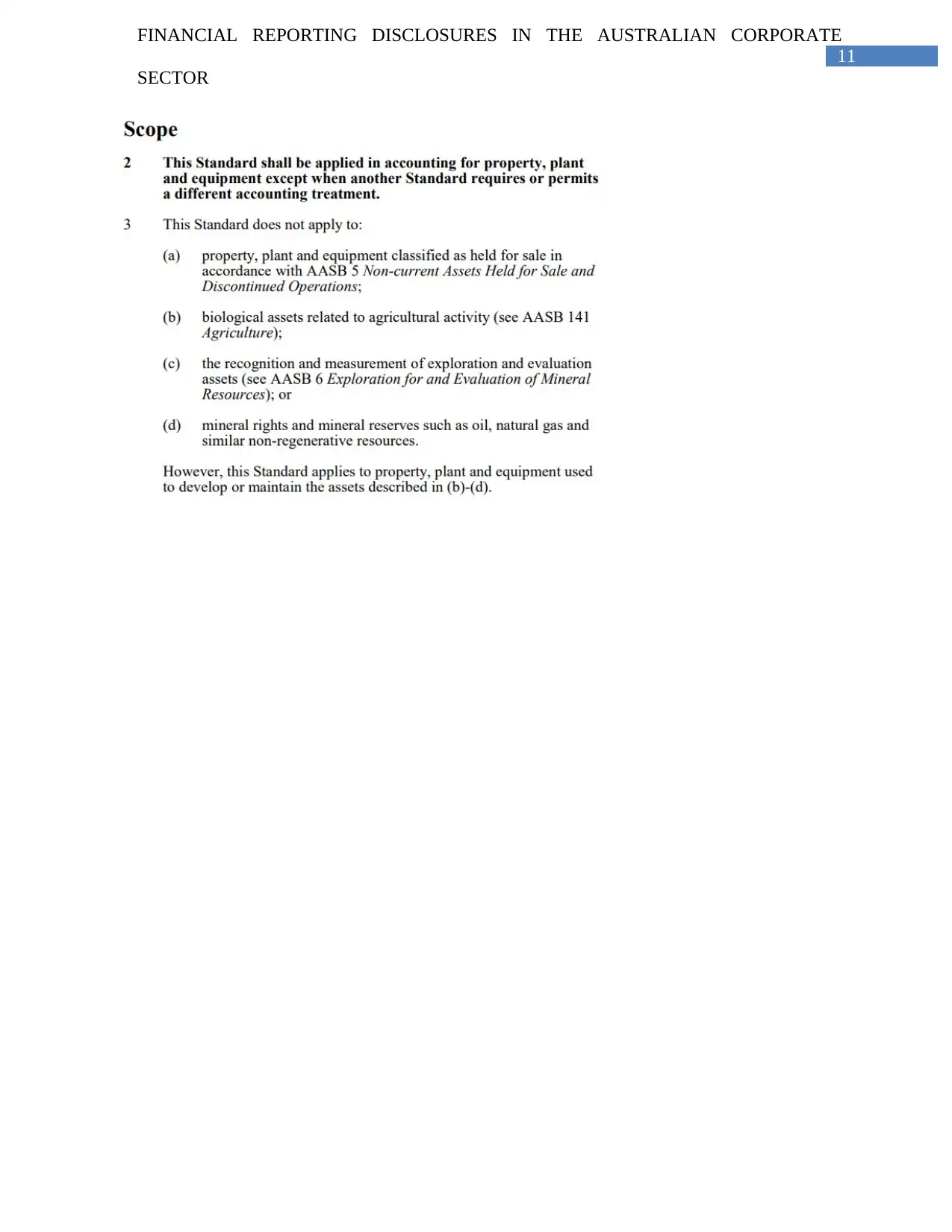

In addition to this, the company has duly complied with “Section 3b” of “AASB 116”

which is associated to biological assets linked with agricultural activity. Similarly, the company

is clearly stated that its agricultural bearer plants are in compliance with Amendments to “AASB

116” and “AASB 141”. The aforementioned findings have been clearly presented in “Appendix

2” section of the study (Deegan 2013).

Answer to Part C

Among the several types of “qualitative characteristics” useful for financial information

as per “conceptual framework for financial reporting”, “relevance” and “understandability” has

been identified as the two main qualitative characteristics for “Monash Ivf Group Limited”.

The adherence to “relevance” quality characteristics for the company has been evident in

operating segment, taxation, earnings per share and dividends. The segment EBITDA has been

able to measure the performance with most relevant results of segments in relation to the entities

which operates in the industry of healthcare. In addition to this, the segmented PBT has been

incorporated in the internal management and duly reviewed by Group’s CODM. It has been used

as a measure of performance as the management is of the notion that such information in

evaluating the financial result is relevant to their respective segments in relation to various types

of other entities which are operating in the same industry. The impairment testing for the amount

to be recovered has been estimated to be high than the usual carrying amount and responsible for

relevant assumption with reasonable possible change to the relevant inputs and such input shall

not result in any recoverable amount being lesser than the actual amount of carrying. The

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

life of PPE. This is indirectly seen in terms of compliance with depreciation method stated under

“Section 62” of “AASB 116” (Annualreport2016.monashivfgroup.com.au 2017).

In addition to this, the company has duly complied with “Section 3b” of “AASB 116”

which is associated to biological assets linked with agricultural activity. Similarly, the company

is clearly stated that its agricultural bearer plants are in compliance with Amendments to “AASB

116” and “AASB 141”. The aforementioned findings have been clearly presented in “Appendix

2” section of the study (Deegan 2013).

Answer to Part C

Among the several types of “qualitative characteristics” useful for financial information

as per “conceptual framework for financial reporting”, “relevance” and “understandability” has

been identified as the two main qualitative characteristics for “Monash Ivf Group Limited”.

The adherence to “relevance” quality characteristics for the company has been evident in

operating segment, taxation, earnings per share and dividends. The segment EBITDA has been

able to measure the performance with most relevant results of segments in relation to the entities

which operates in the industry of healthcare. In addition to this, the segmented PBT has been

incorporated in the internal management and duly reviewed by Group’s CODM. It has been used

as a measure of performance as the management is of the notion that such information in

evaluating the financial result is relevant to their respective segments in relation to various types

of other entities which are operating in the same industry. The impairment testing for the amount

to be recovered has been estimated to be high than the usual carrying amount and responsible for

relevant assumption with reasonable possible change to the relevant inputs and such input shall

not result in any recoverable amount being lesser than the actual amount of carrying. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

company has been further observed to adhere to long-term obligations with relevant market

changes for the corporate bonds which are having graduated eighth approximating the terms of

obligation of the group. Therefore, it can be clearly seen that the financial information has the

capability of making a difference in decisions made by users. It has been further observed that

the information published by the company has confirmatory value and predictive value which

directly complies with “relevance” quality aspect under QC 6 to QC 10 duly stated in

“Conceptual Framework for Financial Reporting” (Cheng et al. 2014).

The “understandability” quality aspect has been duly maintained by the group through the

organising the notes to the financial statements into several sections which will help the users in

better understanding the performance of the group. In addition to this, the changes proposed by

the group has been able to provide the users with a clearer understanding for the factors which

drive the financial performance, financial position for the group thereby suggesting on better

alignment of group strategy and complying with the provisions of “Corporations Act 2001”.

Therefore, it can be said that the company is able to classify, characterise and present the

information in a clear and concise manner which makes it understandable to the user. In addition

to this the financial reports have been prepared even for users having a reasonable knowledge of

economic and business activities. Due to the aforementioned factors it can be stated that is able

to adhere to “understandability” quality as per conceptual framework (Abeysekera 2013).

Answer to Part D

The company has been able to recognise the PPE values in the balance sheet with utmost

“relevance” to the prescribed guidelines. It has been further able to identify the percentage

change in property expenses for both present and previous financial year. The relevant values for

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

company has been further observed to adhere to long-term obligations with relevant market

changes for the corporate bonds which are having graduated eighth approximating the terms of

obligation of the group. Therefore, it can be clearly seen that the financial information has the

capability of making a difference in decisions made by users. It has been further observed that

the information published by the company has confirmatory value and predictive value which

directly complies with “relevance” quality aspect under QC 6 to QC 10 duly stated in

“Conceptual Framework for Financial Reporting” (Cheng et al. 2014).

The “understandability” quality aspect has been duly maintained by the group through the

organising the notes to the financial statements into several sections which will help the users in

better understanding the performance of the group. In addition to this, the changes proposed by

the group has been able to provide the users with a clearer understanding for the factors which

drive the financial performance, financial position for the group thereby suggesting on better

alignment of group strategy and complying with the provisions of “Corporations Act 2001”.

Therefore, it can be said that the company is able to classify, characterise and present the

information in a clear and concise manner which makes it understandable to the user. In addition

to this the financial reports have been prepared even for users having a reasonable knowledge of

economic and business activities. Due to the aforementioned factors it can be stated that is able

to adhere to “understandability” quality as per conceptual framework (Abeysekera 2013).

Answer to Part D

The company has been able to recognise the PPE values in the balance sheet with utmost

“relevance” to the prescribed guidelines. It has been further able to identify the percentage

change in property expenses for both present and previous financial year. The relevant values for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

the payments for “property plant and equipment” have been duly noted in the “net cash flows

generated from the operating activities” (McNeil, Frey and Embrechts 2015).

The important “understandability” factor has been covered with concisely segregating the

PPE values for the present and previous year in the annual report. The “understandability” aspect

has been duly maintained by clearly stating about the contractual commitment for the acquisition

of PPE. In 30 June 2016, the parent entity of Monash Group was not seen to have any capital

commitment associated to acquisition of PPE (Wahlen, Baginski and Bradshaw 2014).

Conclusion

The company needs to take several improvements which are associated to improve the

financial reporting by including the scope base types of materiality aspects in the financial

report. There is also no cost constraint on useful financial reporting which has been provided in

the financial report. It has been further seen that that there has been several drawbacks associated

to comparability aspect of the financial reporting which should have been shown with the

changes adopted along with eye of IFRS.

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

the payments for “property plant and equipment” have been duly noted in the “net cash flows

generated from the operating activities” (McNeil, Frey and Embrechts 2015).

The important “understandability” factor has been covered with concisely segregating the

PPE values for the present and previous year in the annual report. The “understandability” aspect

has been duly maintained by clearly stating about the contractual commitment for the acquisition

of PPE. In 30 June 2016, the parent entity of Monash Group was not seen to have any capital

commitment associated to acquisition of PPE (Wahlen, Baginski and Bradshaw 2014).

Conclusion

The company needs to take several improvements which are associated to improve the

financial reporting by including the scope base types of materiality aspects in the financial

report. There is also no cost constraint on useful financial reporting which has been provided in

the financial report. It has been further seen that that there has been several drawbacks associated

to comparability aspect of the financial reporting which should have been shown with the

changes adopted along with eye of IFRS.

8

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Reference list

Abeysekera, I., 2013. A template for integrated reporting. Journal of Intellectual Capital, 14(2),

pp.227-245.

Annualreport2016.monashivfgroup.com.au. (2017). AnnualReport. [online] Available at:

http://annualreport2016.monashivfgroup.com.au/ [Accessed 30 Sep. 2017].

Cheng, M., Green, W., Conradie, P., Konishi, N. and Romi, A., 2014. The international

integrated reporting framework: key issues and future research opportunities. Journal of

International Financial Management & Accounting, 25(1), pp.90-119.

Cnc.min-financas.pt. (2017). [online] Available at:

http://www.cnc.min-financas.pt/pdf/IPSAS_Janeiro_2013.pdf [Accessed 30 Sep. 2017].

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Fasb.org. (2017). [online] Available at: http://www.fasb.org/resources/ccurl/515/412/Concepts

%20Statement%20No%208.pdf [Accessed 30 Sep. 2017].

McNeil, A.J., Frey, R. and Embrechts, P., 2015. Quantitative risk management: Concepts,

techniques and tools. Princeton university press.

Wahlen, J., Baginski, S. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Reference list

Abeysekera, I., 2013. A template for integrated reporting. Journal of Intellectual Capital, 14(2),

pp.227-245.

Annualreport2016.monashivfgroup.com.au. (2017). AnnualReport. [online] Available at:

http://annualreport2016.monashivfgroup.com.au/ [Accessed 30 Sep. 2017].

Cheng, M., Green, W., Conradie, P., Konishi, N. and Romi, A., 2014. The international

integrated reporting framework: key issues and future research opportunities. Journal of

International Financial Management & Accounting, 25(1), pp.90-119.

Cnc.min-financas.pt. (2017). [online] Available at:

http://www.cnc.min-financas.pt/pdf/IPSAS_Janeiro_2013.pdf [Accessed 30 Sep. 2017].

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Fasb.org. (2017). [online] Available at: http://www.fasb.org/resources/ccurl/515/412/Concepts

%20Statement%20No%208.pdf [Accessed 30 Sep. 2017].

McNeil, A.J., Frey, R. and Embrechts, P., 2015. Quantitative risk management: Concepts,

techniques and tools. Princeton university press.

Wahlen, J., Baginski, S. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

List of Appendix

Appendix 1

Appendix 2

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

List of Appendix

Appendix 1

Appendix 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

11

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.