Financial Reporting Analysis: Differential Reporting in Australia

VerifiedAdded on 2020/03/01

|10

|1802

|45

Report

AI Summary

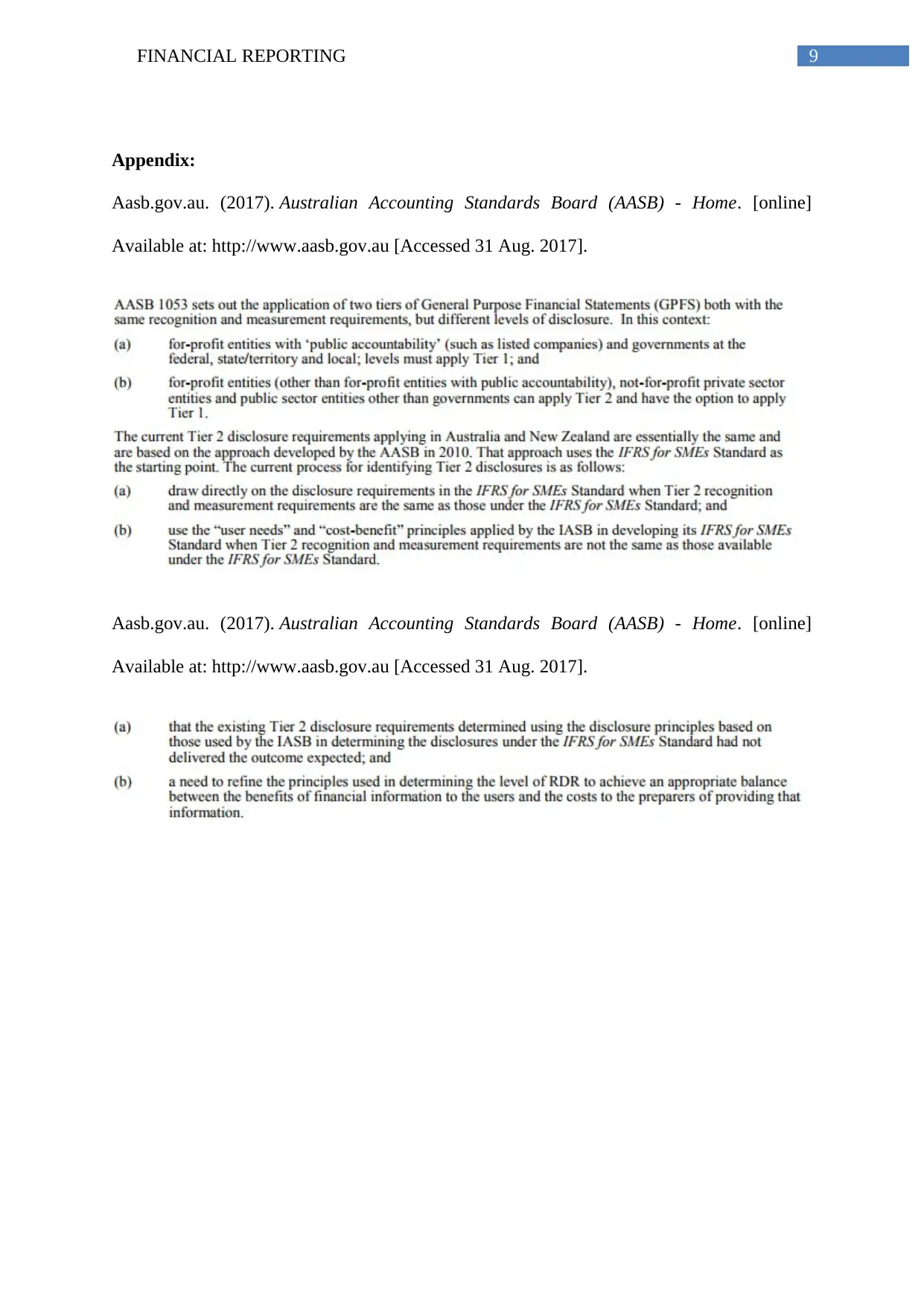

This report examines financial reporting in Australia, specifically focusing on the Australian Accounting Standards Board (AASB) and its differential reporting framework, which has evolved since 1990. It delves into the shift from the 'Reporting Entity' concept to a more regulatory model, as well as the introduction of a two-tier reporting system (Tier 1 and Tier 2) for General Purpose Financial Reports (GPFR). The report discusses the reduced disclosure requirements (RDR) for Tier 2 entities, the implications of AASB 1053 and AASB 2010-2, and the potential impact on companies, including the elimination of special purpose financial reports. It highlights the importance of compliance with AASB standards, particularly for directors and committee members, and the opportunity for entities to move from special-purpose financial reporting to GPFR. The report also references key sources like AASB publications and academic research on the topic.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.