Financial Reporting Assignment: Balance Sheet and Income Statement

VerifiedAdded on 2022/08/11

|10

|1209

|57

Homework Assignment

AI Summary

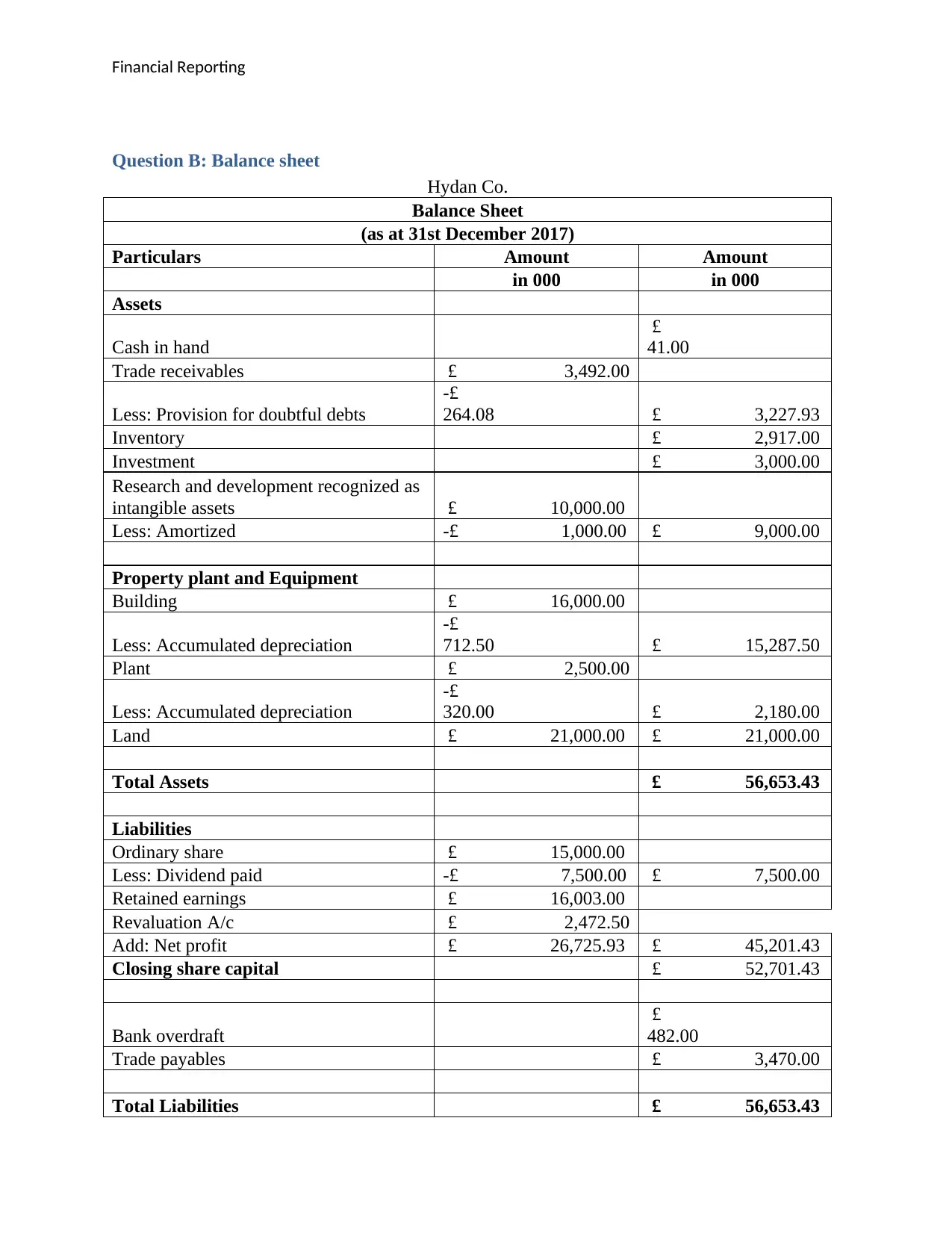

This assignment provides a comprehensive solution to a financial reporting problem. It begins with detailed journal entries, followed by a comprehensive income statement and a balance sheet. The solution then addresses the purpose of depreciation in accounting, emphasizing its role in matching costs with revenues. Finally, it contrasts the cost model and the revaluation model for measuring property, plant, and equipment, explaining their impact on financial statements. The assignment includes calculations, explanations, and references to relevant accounting standards and literature. The solution covers topics such as depreciation, amortization, revaluation gains, and the presentation of financial data, providing a solid foundation for understanding key financial reporting concepts.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.