Semester 2 Financial Reporting for Management BMP6015 Exam Solution

VerifiedAdded on 2023/06/11

|21

|3467

|58

Report

AI Summary

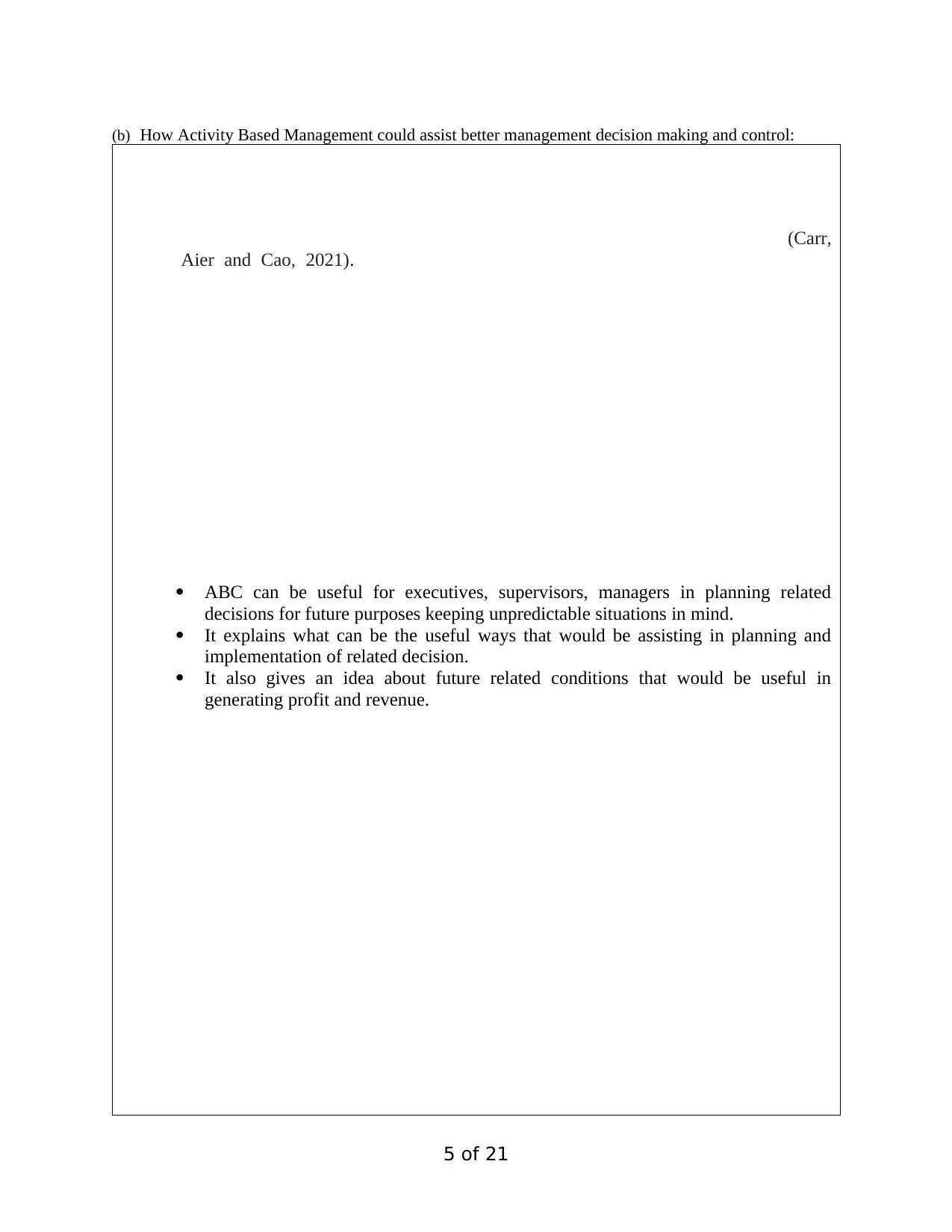

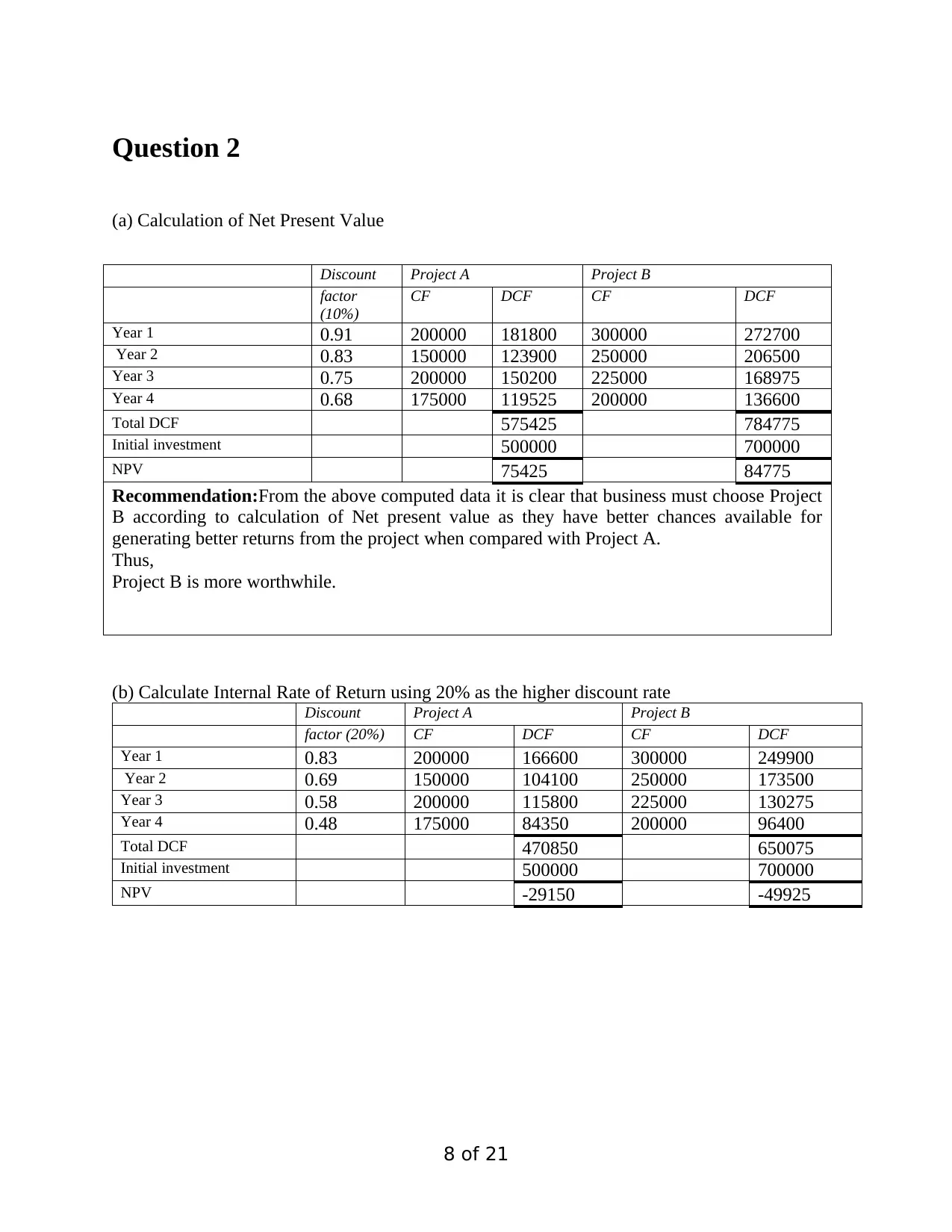

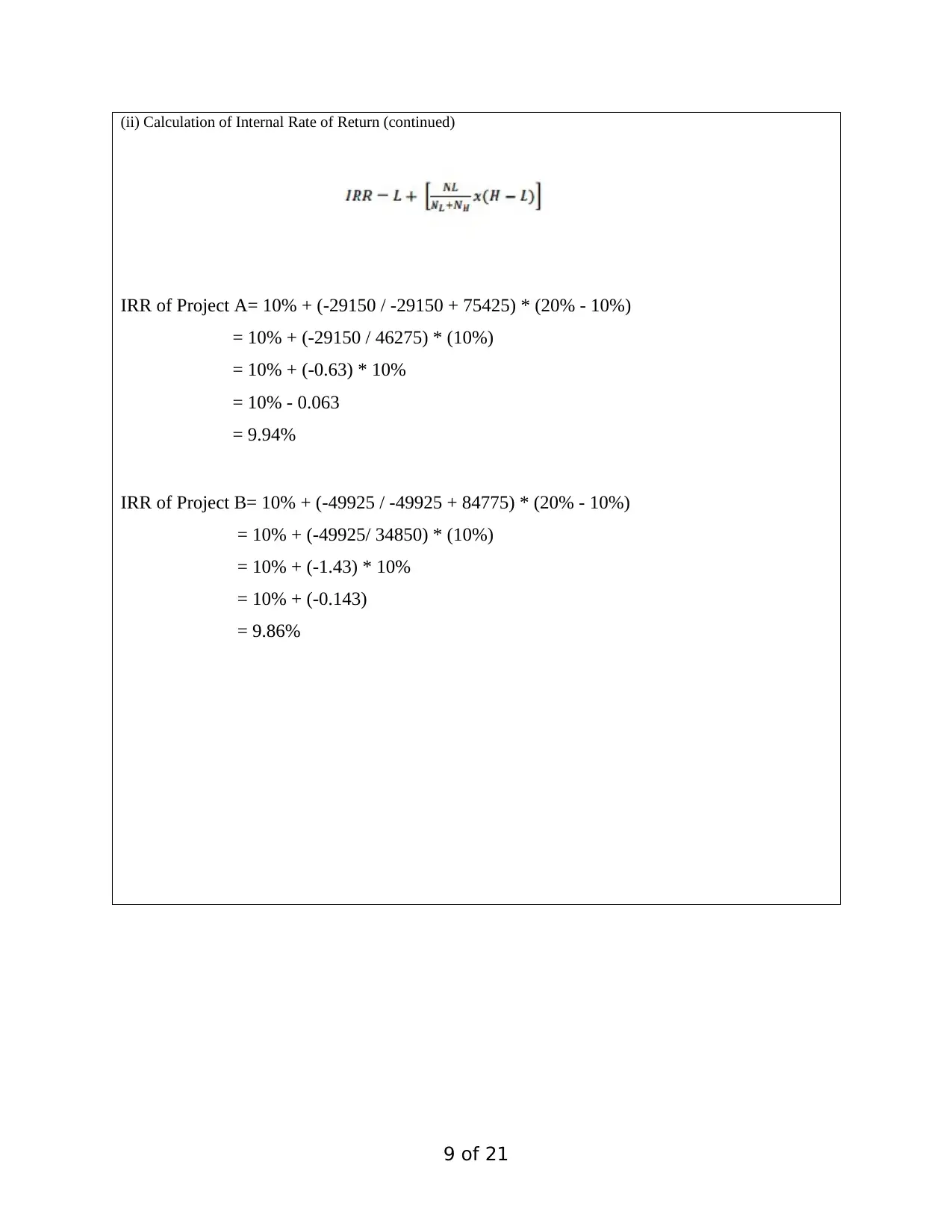

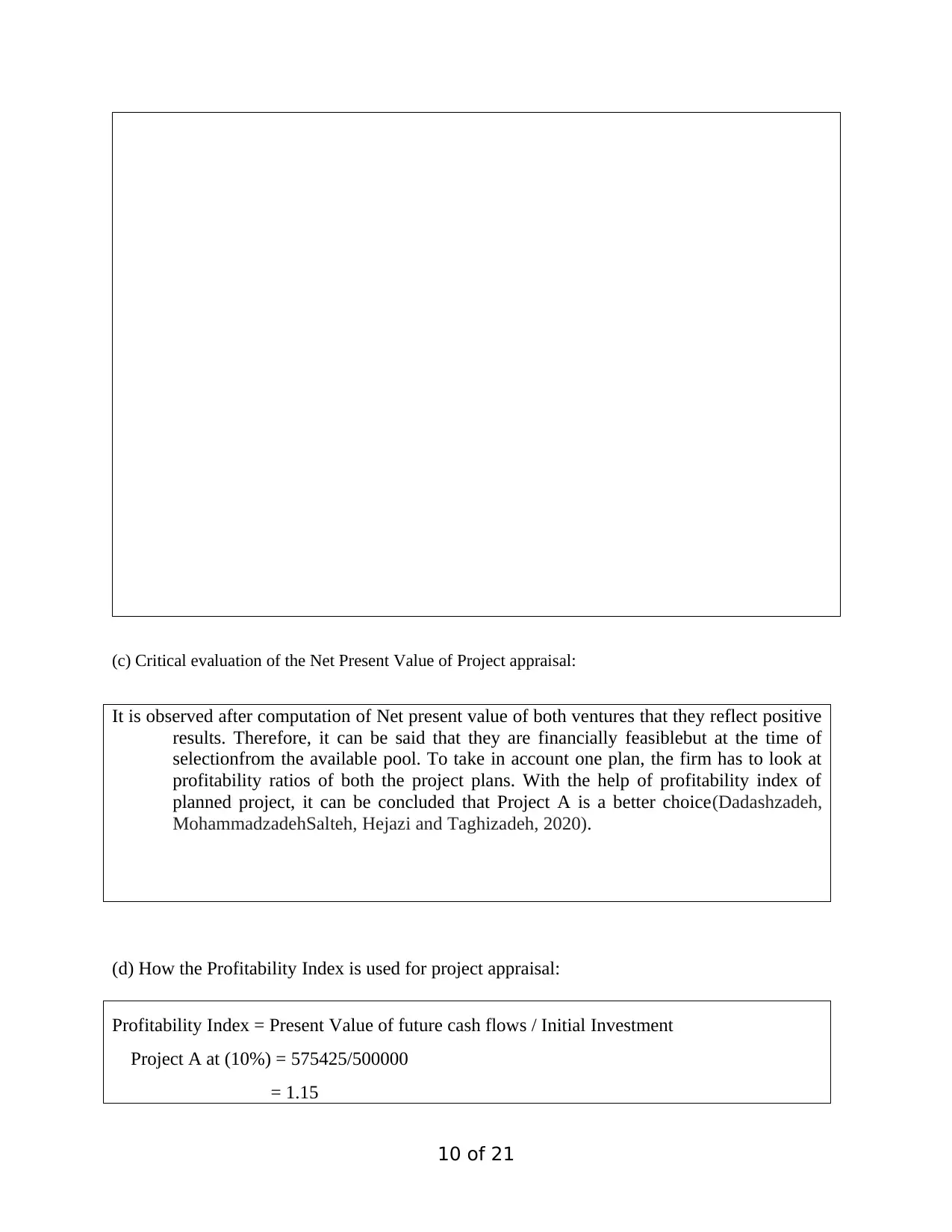

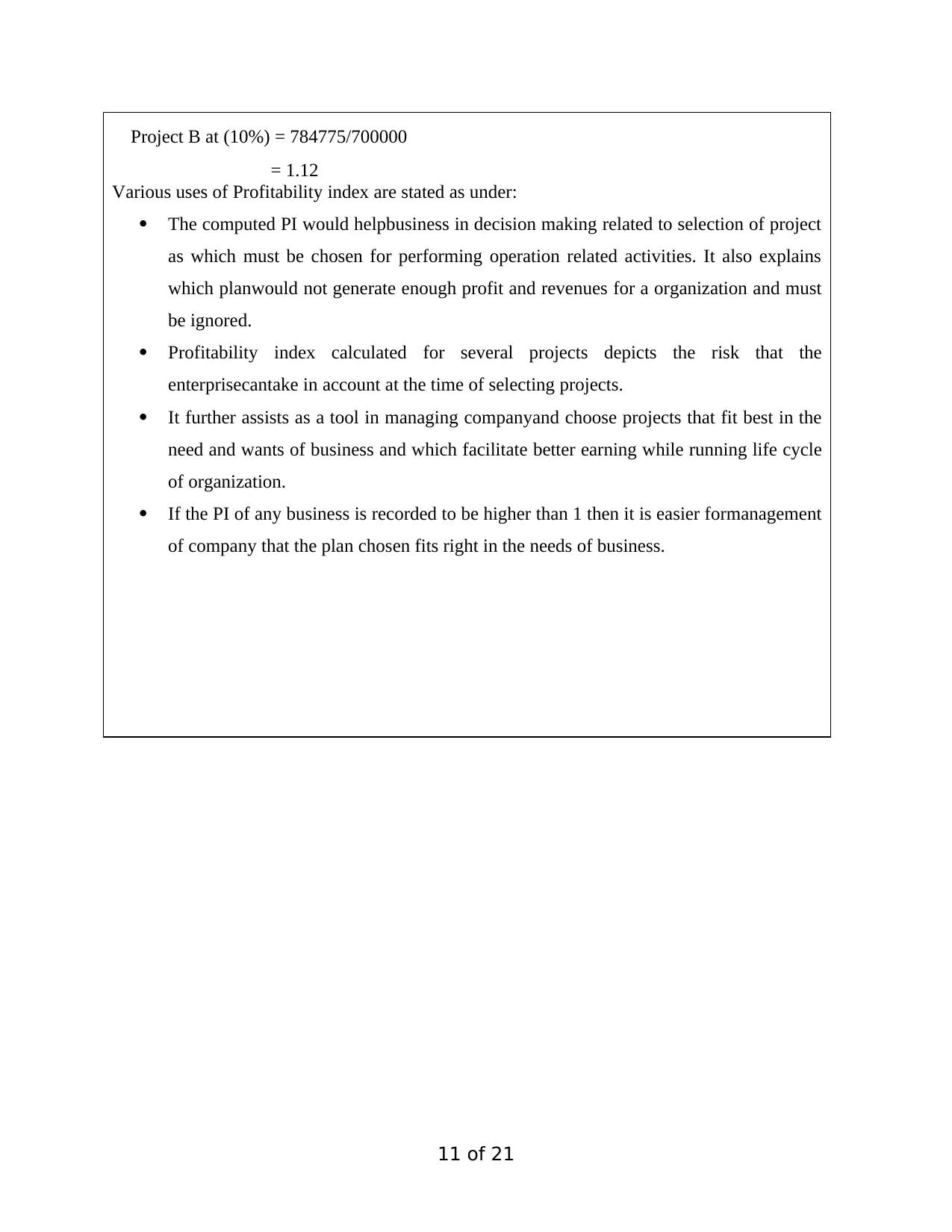

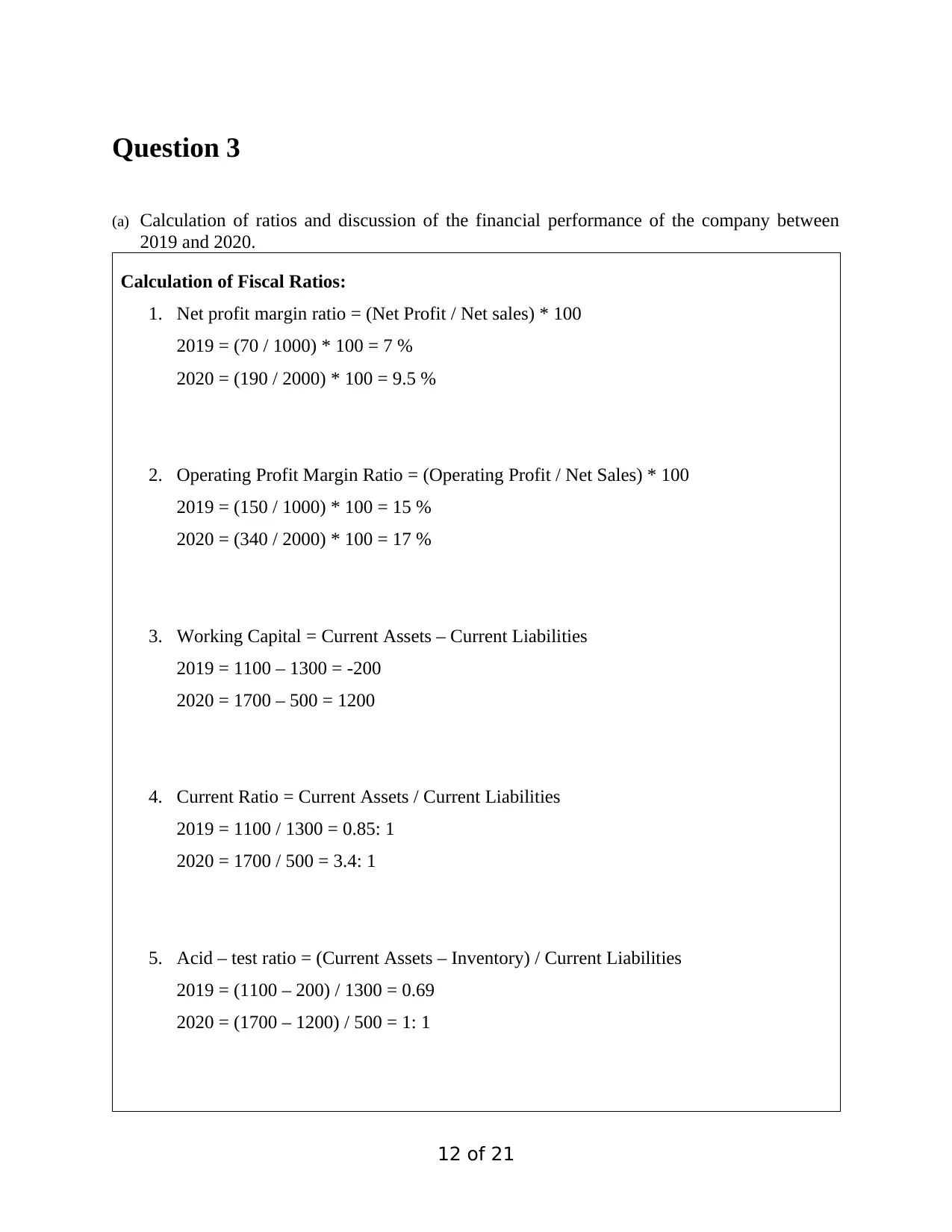

This document presents a comprehensive solution to a Financial Reporting for Management exam, covering topics such as activity-based costing (ABC), net present value (NPV), internal rate of return (IRR), profitability index, financial ratio analysis, and balanced scorecard. The solution includes detailed calculations and critical evaluations of different costing methods and project appraisal techniques. It analyzes a company's financial performance between 2019 and 2020 based on calculated ratios and discusses the balanced scorecard as a method of assessing performance. Desklib offers a platform for students to access similar solved assignments and past papers.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.