University Financial Reporting: CPI Limited Case Study Analysis

VerifiedAdded on 2023/03/20

|12

|1913

|35

Report

AI Summary

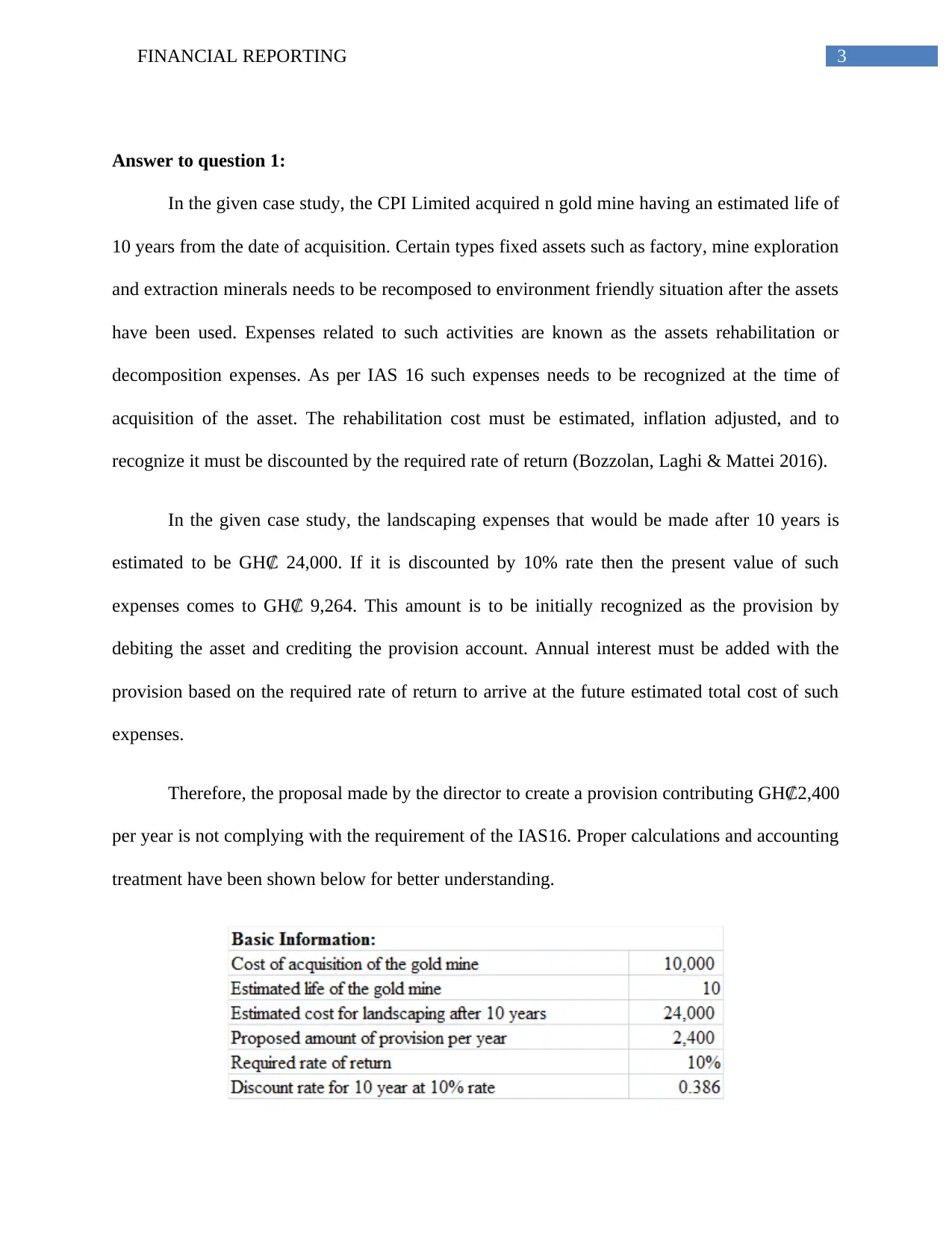

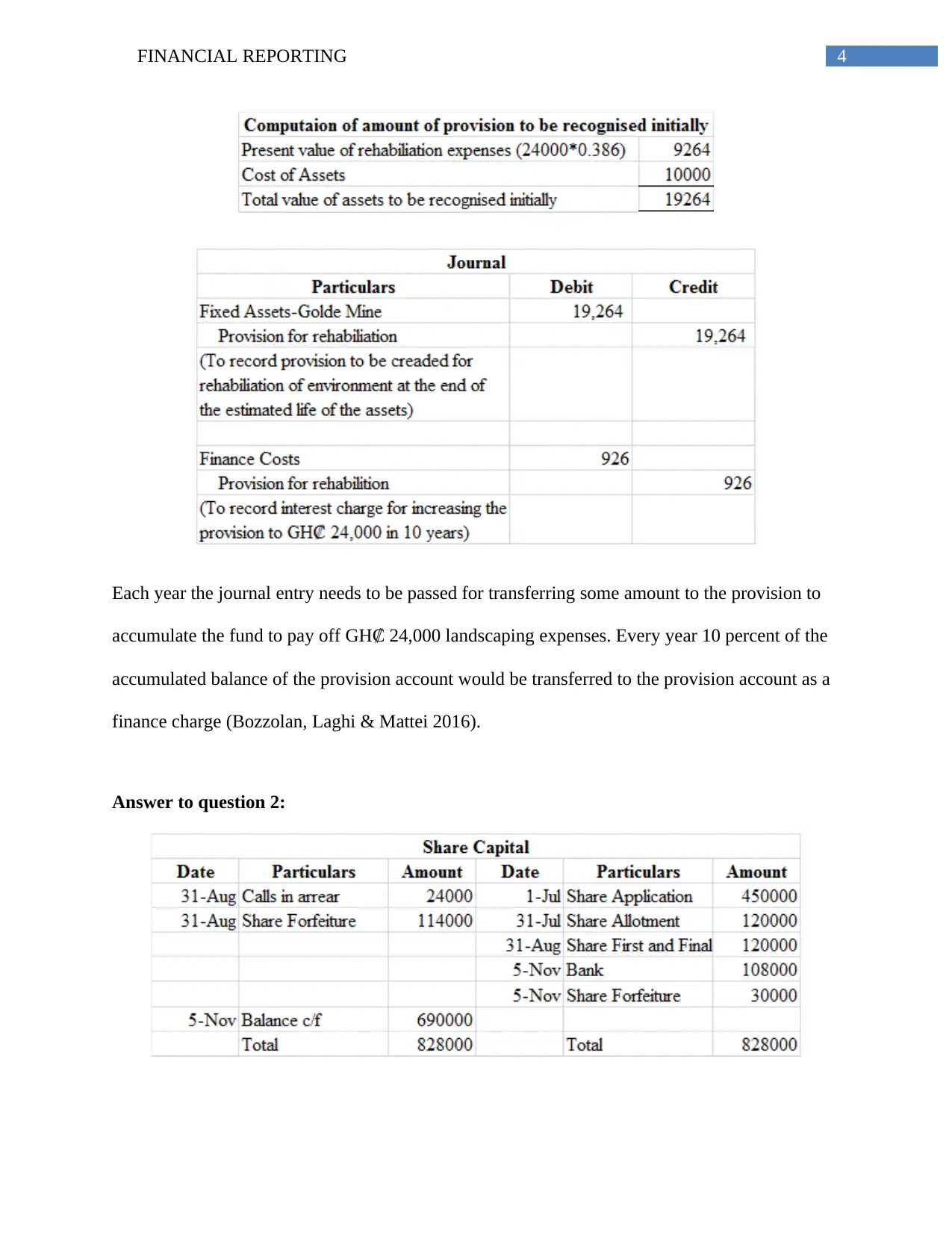

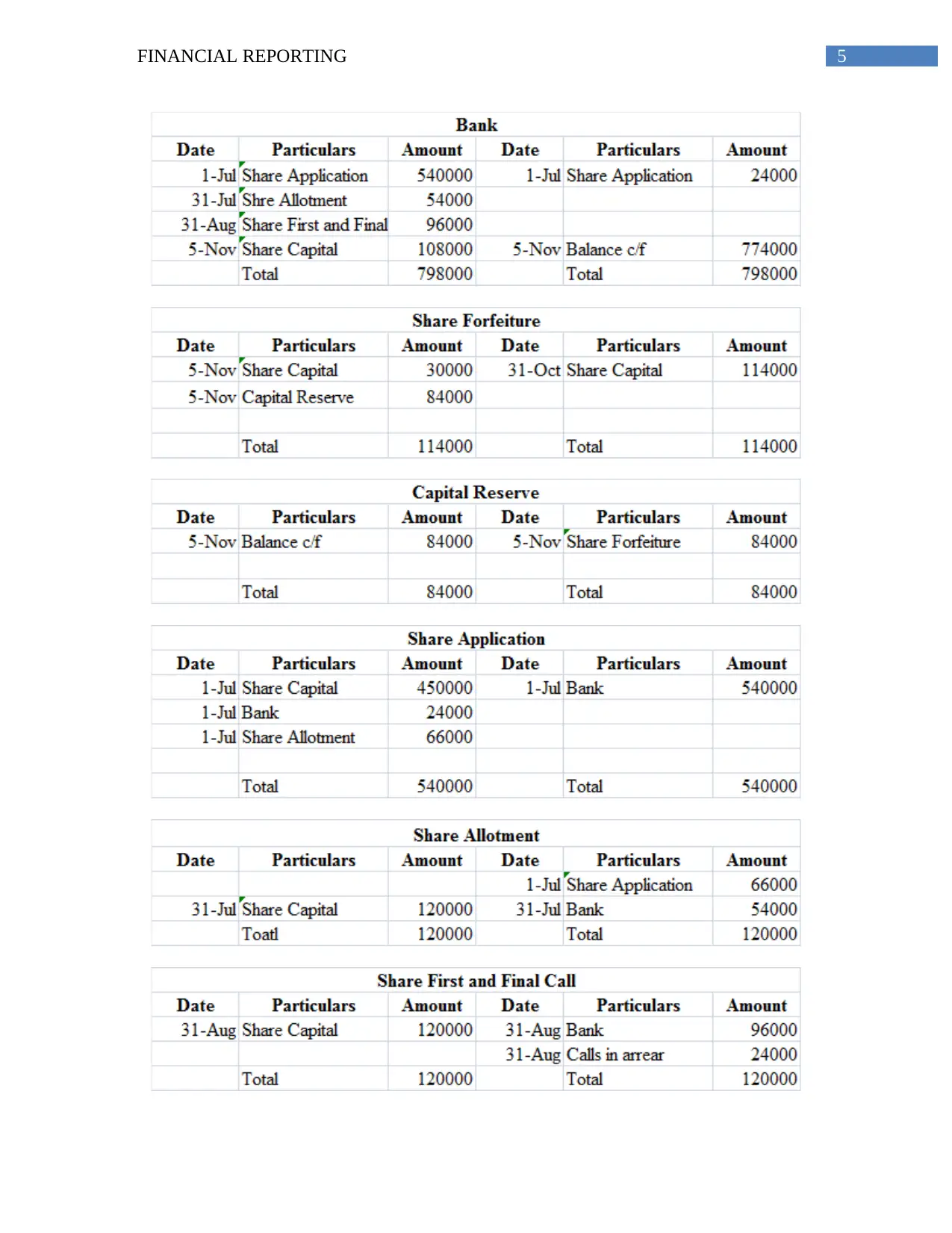

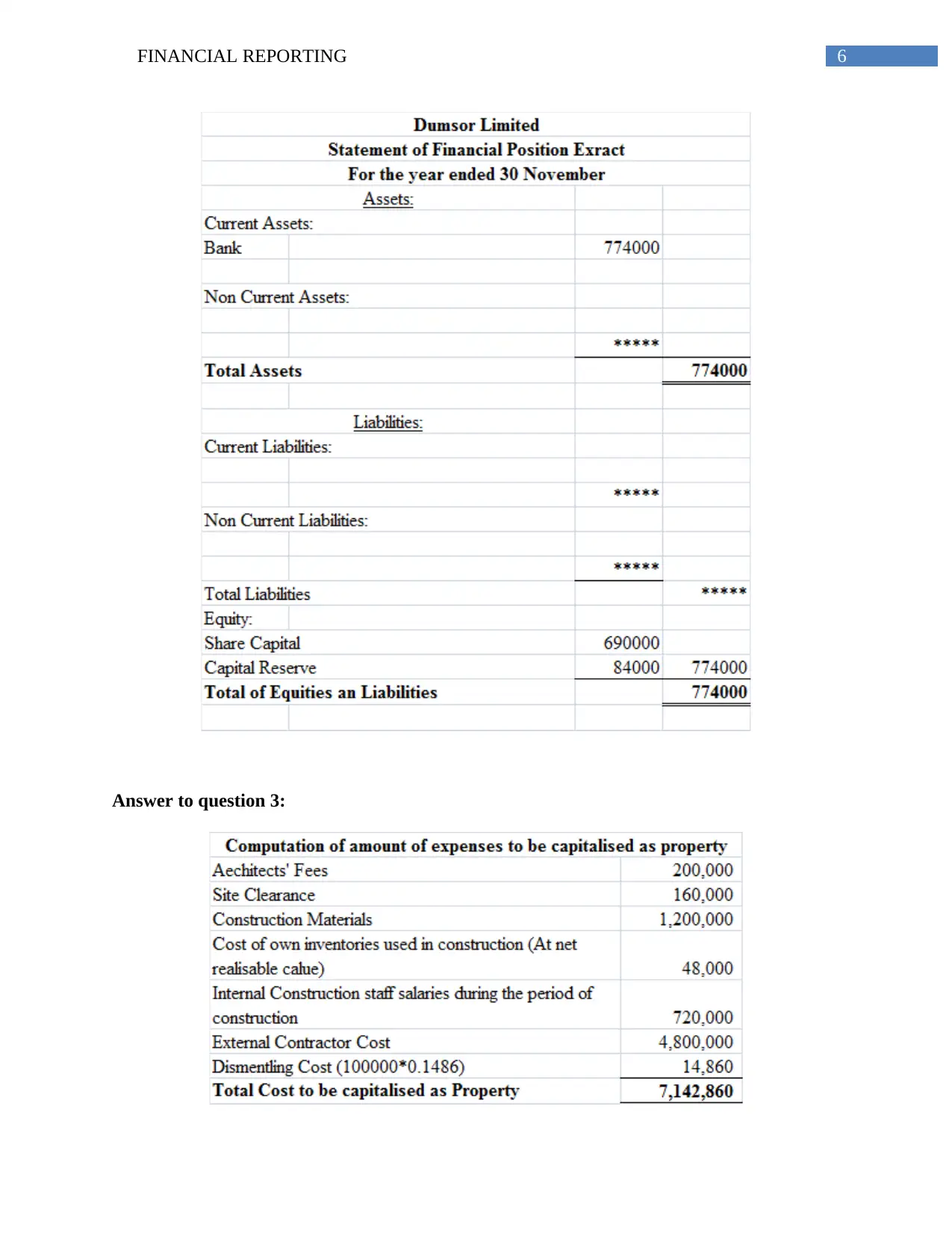

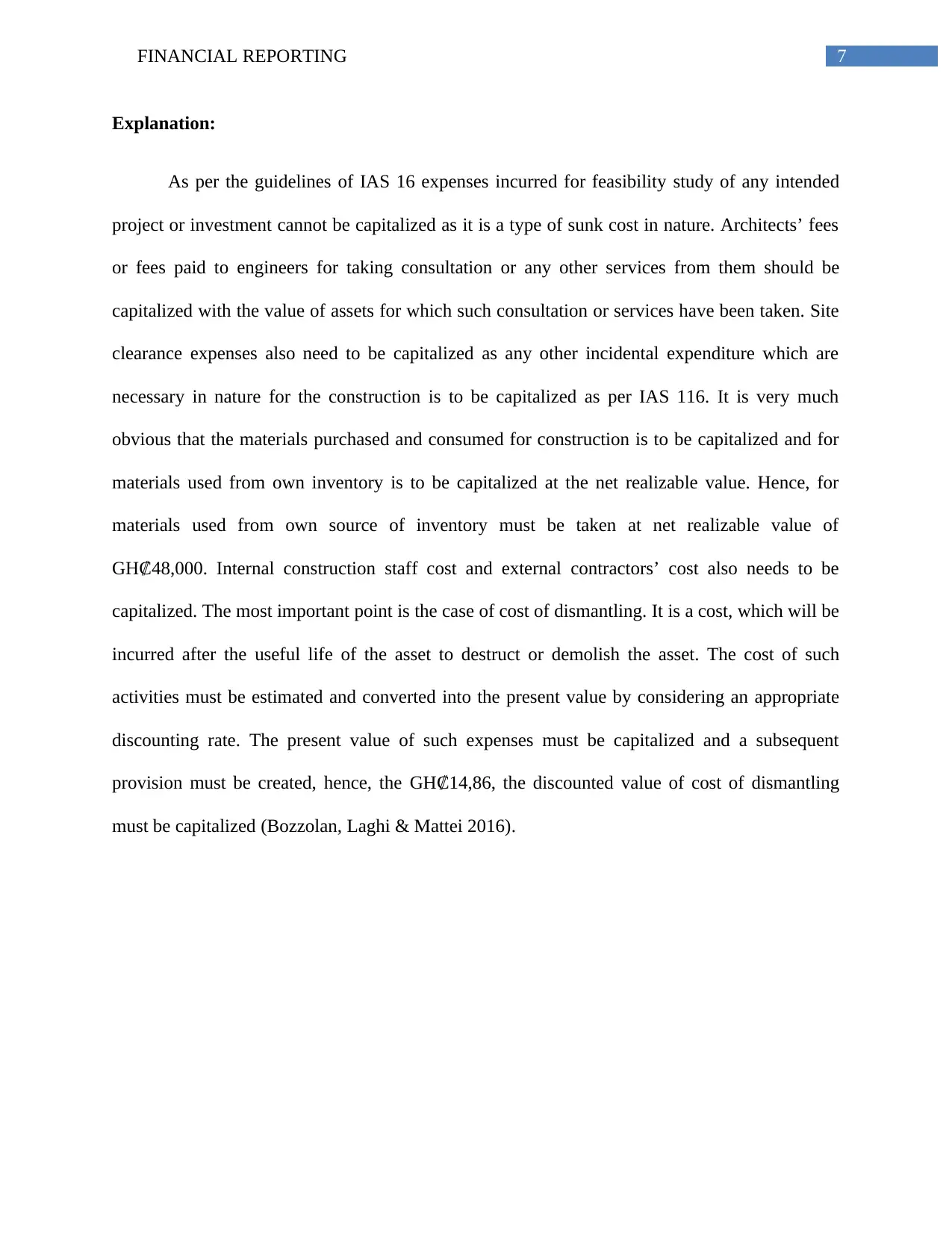

This report provides a comprehensive analysis of financial reporting, focusing on key aspects such as IAS 16 and investment property. The report begins with an examination of a case study involving CPI Limited, addressing the accounting treatment of rehabilitation expenses for a gold mine. It delves into the intricacies of recognizing these expenses, including present value calculations and the inadequacy of the director's proposed provision. The report then explores the capitalization of various costs, including feasibility studies, architect fees, site clearance expenses, and materials used in construction. The report also defines investment property under IAS 40, outlining its characteristics and the different methods of measurement, including the fair value model and the revaluation model. The report emphasizes the importance of understanding these models for accurate financial reporting and valuation. Finally, the report incorporates references to relevant academic literature and standards to support its analysis.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.