Financial Reporting Updates and Analysis of Blake Ltd. Statements

VerifiedAdded on 2023/06/15

|12

|1884

|264

Report

AI Summary

This report provides a summary of recent changes in financial reporting, focusing on updates relevant to preparers of general-purpose financial reports for large ASX companies. It covers news, changes, and developments, including technical and political issues. The second part of the report analyzes financial statements prepared for Blake Ltd. by a trainee, highlighting corrections and recommendations based on AASB 101 regulations, which require minimum line items on the balance sheet and profit and loss account, with additional details in the notes. The revised statements and explanations for required changes are provided, addressing aspects such as asset and liability categorization, equity presentation, gross profit and cost of sales display, dividend treatment, and property, plant, and equipment schedules.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 07 March 2018.

1 | P a g e

By student name

Professor

University

Date: 07 March 2018.

1 | P a g e

2

Executive Summary

In the given report, a brief summary of the changes introduced in the financial reporting arean in the

last 4 months needs to be prepared to to enlighten the preparers of general purpose financial reports of

the large companies oin ASX. This will include anys news/changes/deveopments in reporting and their

impact and can include technical as well as political issue. In the 2nd part of the assignment the financial

reports have been prepared by one of the trainees for Blake Ltd., however as per the regulations given

in AASB 101, the directors of the company require minimum line items on the face of both the balance

sheet as well as profit and loss account and the rest to be reported in Notes on accounts. The

corrections, suggestions, recommendations and the revised statements have be prepared and discussed.

2 | P a g e

Executive Summary

In the given report, a brief summary of the changes introduced in the financial reporting arean in the

last 4 months needs to be prepared to to enlighten the preparers of general purpose financial reports of

the large companies oin ASX. This will include anys news/changes/deveopments in reporting and their

impact and can include technical as well as political issue. In the 2nd part of the assignment the financial

reports have been prepared by one of the trainees for Blake Ltd., however as per the regulations given

in AASB 101, the directors of the company require minimum line items on the face of both the balance

sheet as well as profit and loss account and the rest to be reported in Notes on accounts. The

corrections, suggestions, recommendations and the revised statements have be prepared and discussed.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Question No. 1: Regulatory environment and financial reporting...............................................................4

Introduction.............................................................................................................................................4

Exposure draft for changes in the accounting policies............................................................................4

New Australian accounting standard introduced....................................................................................4

Amendments to the existing Australian accounting standards...............................................................5

Making materiality judgements...............................................................................................................5

Other highlights of changes.....................................................................................................................6

Question No. 2: Financial Statement Presentation......................................................................................7

References.................................................................................................................................................11

3 | P a g e

Contents

Question No. 1: Regulatory environment and financial reporting...............................................................4

Introduction.............................................................................................................................................4

Exposure draft for changes in the accounting policies............................................................................4

New Australian accounting standard introduced....................................................................................4

Amendments to the existing Australian accounting standards...............................................................5

Making materiality judgements...............................................................................................................5

Other highlights of changes.....................................................................................................................6

Question No. 2: Financial Statement Presentation......................................................................................7

References.................................................................................................................................................11

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Question No. 1: Regulatory environment and financial reporting

Introduction

There have been many accounting changes in the accounting arena in the last 4 months including the

reduction in the tax rates and the structure for the small entities, calculation of the defereed tax for the

intangible assets having indefinite life, recognition of the deferred tax assets for unrealised losses of the

entity, increase in the cash flow disclosures, financiual reporting relief for whilly owned entity but the

changes which have took place in the financial reporting include release of the exposure draft for

changes in the accounting policies, introduction of new Australian accounting standard on employee

benefits, amendments to the existing Australian accounting standards, Australian financial reporting for

Charities, etc. some of which are explained below in details (Belton, 2017).

Exposure draft for changes in the accounting policies

This would bring about a change in AASB 108, Accounting policies, changes in the accounting estimates

and errors. This would simplify the procedure a bit and there would a voluntary change in the

accounting policy as a result of decision of the IFRS implementation committee (Alexander, 2016).

New Australian accounting standard introduced

This is on employee benefits named AASB 2018-2 which will be having an impact on all the entities

having defined benefit plan which are planning to change the plans. This AASB standard will give more

clarity on how to measure the defined benefit asset or liability and other such related amounts like past

4 | P a g e

Question No. 1: Regulatory environment and financial reporting

Introduction

There have been many accounting changes in the accounting arena in the last 4 months including the

reduction in the tax rates and the structure for the small entities, calculation of the defereed tax for the

intangible assets having indefinite life, recognition of the deferred tax assets for unrealised losses of the

entity, increase in the cash flow disclosures, financiual reporting relief for whilly owned entity but the

changes which have took place in the financial reporting include release of the exposure draft for

changes in the accounting policies, introduction of new Australian accounting standard on employee

benefits, amendments to the existing Australian accounting standards, Australian financial reporting for

Charities, etc. some of which are explained below in details (Belton, 2017).

Exposure draft for changes in the accounting policies

This would bring about a change in AASB 108, Accounting policies, changes in the accounting estimates

and errors. This would simplify the procedure a bit and there would a voluntary change in the

accounting policy as a result of decision of the IFRS implementation committee (Alexander, 2016).

New Australian accounting standard introduced

This is on employee benefits named AASB 2018-2 which will be having an impact on all the entities

having defined benefit plan which are planning to change the plans. This AASB standard will give more

clarity on how to measure the defined benefit asset or liability and other such related amounts like past

4 | P a g e

5

cost, current service cost, when will the modification has to be done during the reporting period. The

meeting was being held on 23rd March, 2018 and the changes will be effective from 01st Jan, 2019

(Boccia & Leonardi, 2016).

Amendments to the existing Australian accounting standards

Another major change was AASB 3 on Business combinations and AASB 11 on Joint Arrangements with

res[ect to the interest previously being held in the joint operations, implication on the income payment

on the payment of the financial instruments (AASB 112 on income taxes) and computation of the

borrowing cost eligible for capitalisation as per AASB 123 borrowing costs (Das, 2017).

Making materiality judgements

Materiality is judgemental and based on the estimates and opinion of the top management of the

company. Directors, trustees and other responsible stakeholders are the one who make continuous

judgements on the scope of materiality during the preparation and presentation of the financial

statements. AASB practice statement 2 gives a brief and the outline of how the materiality can be

determined and gives practical examples for public sector and non for profit entities. It gives examples

which may help while discussion with the auditors and othe regulators.

5 | P a g e

cost, current service cost, when will the modification has to be done during the reporting period. The

meeting was being held on 23rd March, 2018 and the changes will be effective from 01st Jan, 2019

(Boccia & Leonardi, 2016).

Amendments to the existing Australian accounting standards

Another major change was AASB 3 on Business combinations and AASB 11 on Joint Arrangements with

res[ect to the interest previously being held in the joint operations, implication on the income payment

on the payment of the financial instruments (AASB 112 on income taxes) and computation of the

borrowing cost eligible for capitalisation as per AASB 123 borrowing costs (Das, 2017).

Making materiality judgements

Materiality is judgemental and based on the estimates and opinion of the top management of the

company. Directors, trustees and other responsible stakeholders are the one who make continuous

judgements on the scope of materiality during the preparation and presentation of the financial

statements. AASB practice statement 2 gives a brief and the outline of how the materiality can be

determined and gives practical examples for public sector and non for profit entities. It gives examples

which may help while discussion with the auditors and othe regulators.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Other highlights of changes

The AASB also clarified that the calculation of depreciation based on the revenue streams or the

cash flow of the entity is not acceptable and is not appropriate (Dumay & Baard, 2017).

The amendments also allows the companies to use the equity method while measuring the

investments in the joint ventures, the subsidiaries and the associates while preparing the

separate financial statements.

The IFRS implementation committee also clarified in one of the recent accouncements that

entities should not presume that the intangible asset having the indefinite life can be recovered

through sale if it has not been amortized (Dichev, 2017).

With respect to additional disclosures in the statement of cash flows, it clarified via an

amendment that entities should make a disclosure that enables the users to identify the

changes in the liabilities due to the financing activities (Gooley, 2016). The amendment basically

requires disclosures of changes resulting cash flows such as repayment of borrowings and also

the non cash changes like acquisitions, disposals and exchanges gain or losses that have

remained unrealised.

6 | P a g e

Other highlights of changes

The AASB also clarified that the calculation of depreciation based on the revenue streams or the

cash flow of the entity is not acceptable and is not appropriate (Dumay & Baard, 2017).

The amendments also allows the companies to use the equity method while measuring the

investments in the joint ventures, the subsidiaries and the associates while preparing the

separate financial statements.

The IFRS implementation committee also clarified in one of the recent accouncements that

entities should not presume that the intangible asset having the indefinite life can be recovered

through sale if it has not been amortized (Dichev, 2017).

With respect to additional disclosures in the statement of cash flows, it clarified via an

amendment that entities should make a disclosure that enables the users to identify the

changes in the liabilities due to the financing activities (Gooley, 2016). The amendment basically

requires disclosures of changes resulting cash flows such as repayment of borrowings and also

the non cash changes like acquisitions, disposals and exchanges gain or losses that have

remained unrealised.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

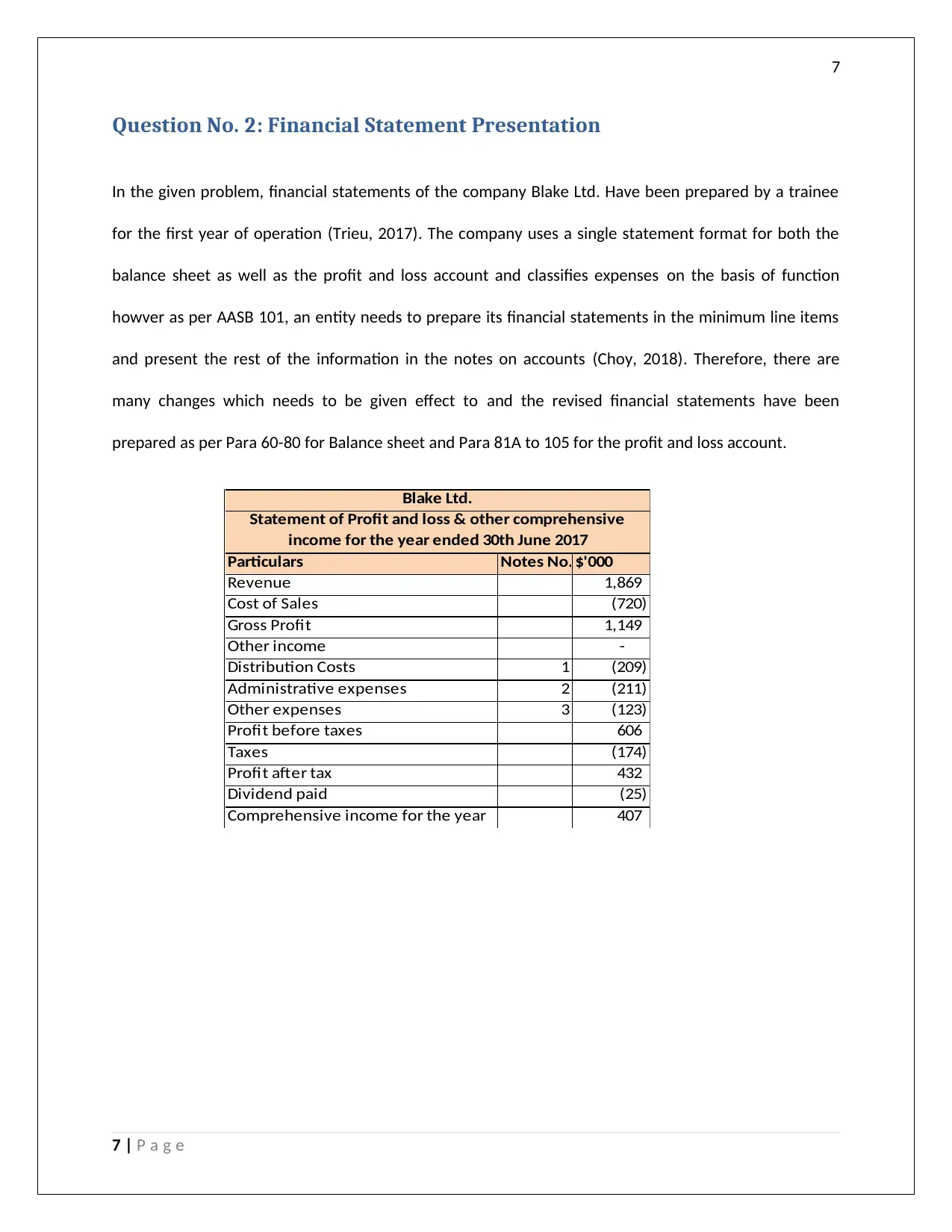

Question No. 2: Financial Statement Presentation

In the given problem, financial statements of the company Blake Ltd. Have been prepared by a trainee

for the first year of operation (Trieu, 2017). The company uses a single statement format for both the

balance sheet as well as the profit and loss account and classifies expenses on the basis of function

howver as per AASB 101, an entity needs to prepare its financial statements in the minimum line items

and present the rest of the information in the notes on accounts (Choy, 2018). Therefore, there are

many changes which needs to be given effect to and the revised financial statements have been

prepared as per Para 60-80 for Balance sheet and Para 81A to 105 for the profit and loss account.

Particulars Notes No. $'000

Revenue 1,869

Cost of Sales (720)

Gross Profit 1,149

Other income -

Distribution Costs 1 (209)

Administrative expenses 2 (211)

Other expenses 3 (123)

Profit before taxes 606

Taxes (174)

Profit after tax 432

Dividend paid (25)

Comprehensive income for the year 407

Blake Ltd.

Statement of Profit and loss & other comprehensive

income for the year ended 30th June 2017

7 | P a g e

Question No. 2: Financial Statement Presentation

In the given problem, financial statements of the company Blake Ltd. Have been prepared by a trainee

for the first year of operation (Trieu, 2017). The company uses a single statement format for both the

balance sheet as well as the profit and loss account and classifies expenses on the basis of function

howver as per AASB 101, an entity needs to prepare its financial statements in the minimum line items

and present the rest of the information in the notes on accounts (Choy, 2018). Therefore, there are

many changes which needs to be given effect to and the revised financial statements have been

prepared as per Para 60-80 for Balance sheet and Para 81A to 105 for the profit and loss account.

Particulars Notes No. $'000

Revenue 1,869

Cost of Sales (720)

Gross Profit 1,149

Other income -

Distribution Costs 1 (209)

Administrative expenses 2 (211)

Other expenses 3 (123)

Profit before taxes 606

Taxes (174)

Profit after tax 432

Dividend paid (25)

Comprehensive income for the year 407

Blake Ltd.

Statement of Profit and loss & other comprehensive

income for the year ended 30th June 2017

7 | P a g e

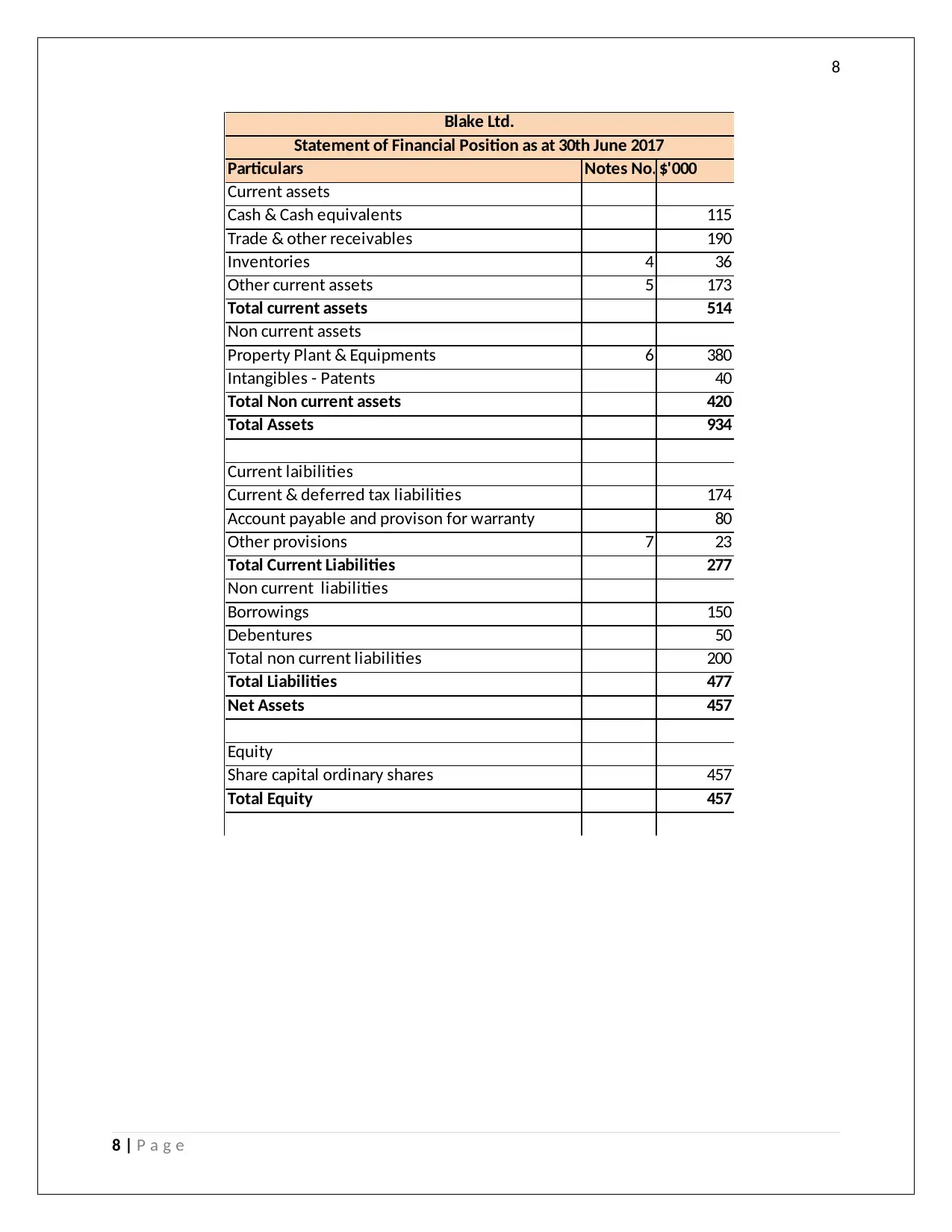

8

Particulars Notes No. $'000

Current assets

Cash & Cash equivalents 115

Trade & other receivables 190

Inventories 4 36

Other current assets 5 173

Total current assets 514

Non current assets

Property Plant & Equipments 6 380

Intangibles - Patents 40

Total Non current assets 420

Total Assets 934

Current laibilities

Current & deferred tax liabilities 174

Account payable and provison for warranty 80

Other provisions 7 23

Total Current Liabilities 277

Non current liabilities

Borrowings 150

Debentures 50

Total non current liabilities 200

Total Liabilities 477

Net Assets 457

Equity

Share capital ordinary shares 457

Total Equity 457

Blake Ltd.

Statement of Financial Position as at 30th June 2017

8 | P a g e

Particulars Notes No. $'000

Current assets

Cash & Cash equivalents 115

Trade & other receivables 190

Inventories 4 36

Other current assets 5 173

Total current assets 514

Non current assets

Property Plant & Equipments 6 380

Intangibles - Patents 40

Total Non current assets 420

Total Assets 934

Current laibilities

Current & deferred tax liabilities 174

Account payable and provison for warranty 80

Other provisions 7 23

Total Current Liabilities 277

Non current liabilities

Borrowings 150

Debentures 50

Total non current liabilities 200

Total Liabilities 477

Net Assets 457

Equity

Share capital ordinary shares 457

Total Equity 457

Blake Ltd.

Statement of Financial Position as at 30th June 2017

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

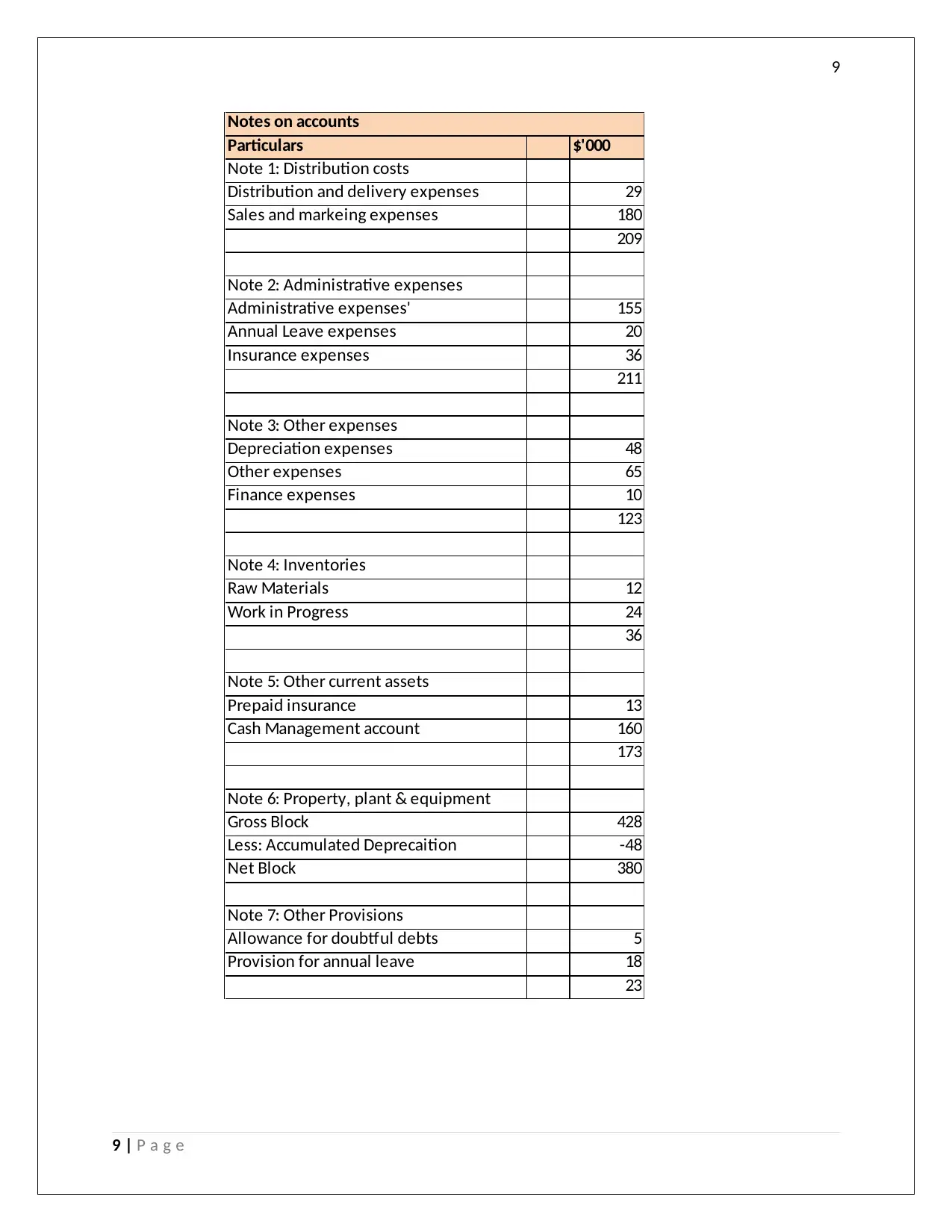

Particulars $'000

Note 1: Distribution costs

Distribution and delivery expenses 29

Sales and markeing expenses 180

209

Note 2: Administrative expenses

Administrative expenses' 155

Annual Leave expenses 20

Insurance expenses 36

211

Note 3: Other expenses

Depreciation expenses 48

Other expenses 65

Finance expenses 10

123

Note 4: Inventories

Raw Materials 12

Work in Progress 24

36

Note 5: Other current assets

Prepaid insurance 13

Cash Management account 160

173

Note 6: Property, plant & equipment

Gross Block 428

Less: Accumulated Deprecaition -48

Net Block 380

Note 7: Other Provisions

Allowance for doubtful debts 5

Provision for annual leave 18

23

Notes on accounts

9 | P a g e

Particulars $'000

Note 1: Distribution costs

Distribution and delivery expenses 29

Sales and markeing expenses 180

209

Note 2: Administrative expenses

Administrative expenses' 155

Annual Leave expenses 20

Insurance expenses 36

211

Note 3: Other expenses

Depreciation expenses 48

Other expenses 65

Finance expenses 10

123

Note 4: Inventories

Raw Materials 12

Work in Progress 24

36

Note 5: Other current assets

Prepaid insurance 13

Cash Management account 160

173

Note 6: Property, plant & equipment

Gross Block 428

Less: Accumulated Deprecaition -48

Net Block 380

Note 7: Other Provisions

Allowance for doubtful debts 5

Provision for annual leave 18

23

Notes on accounts

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Explanation for the change / changes that will be required in the financial statements prepared by the

trainee are mentioned below:

1. Assets have been categorised into current and non current assets,

2. Liabilities have been categorised into current and non current liabilities

3. Equity has been shown separately

4. The notes of accounts have been shown wherever considered necessary (Félix, 2017)

5. The trainee has not shown the gross profit and the cost of sales separately which has now been

shown separately.

6. The dividends being paid has been shown as above the line item whereas the same is below the

line items and has to be shown post the profits after tax.

7. Schedules have been prepared for property, plant and equipment has the net figure needs to be

shown on the assets side.

8. The revised financial statements do confirm to the requiremenst of the AASB 101.

10 | P a g e

Explanation for the change / changes that will be required in the financial statements prepared by the

trainee are mentioned below:

1. Assets have been categorised into current and non current assets,

2. Liabilities have been categorised into current and non current liabilities

3. Equity has been shown separately

4. The notes of accounts have been shown wherever considered necessary (Félix, 2017)

5. The trainee has not shown the gross profit and the cost of sales separately which has now been

shown separately.

6. The dividends being paid has been shown as above the line item whereas the same is below the

line items and has to be shown post the profits after tax.

7. Schedules have been prepared for property, plant and equipment has the net figure needs to be

shown on the assets side.

8. The revised financial statements do confirm to the requiremenst of the AASB 101.

10 | P a g e

11

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd. Retrieved from https://www.routledge.com/Competitive-Strategy-Creating-

and-Sustaining-Superior-Performance/Belton/p/book/9781912128808

Boccia, F., & Leonardi, R. (2016). The Challenge of the Digital Economy: Markets, Taxation and

Appropriate Economic Models. Springer.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Das, P. (2017). Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), 10-17.

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. Retrieved from https://doi.org/10.1080/00014788.2017.1299620

Dumay, J., & Baard, V. (2017). An introduction to interventionist research in accounting. The Routledge

Companion to Qualitative Accounting Research Methods, 265. Retrieved from

https://books.google.co.in/books?

hl=en&lr=&id=PzQlDwAAQBAJ&oi=fnd&pg=PA265&dq=Dumay,+J.,+%26+Baard,+V.+(2017).

+An+introduction+to+interventionist+research+in+accounting.

+The+Routledge+Companion+to+Qualitative+Accounting+Research+Methods,

+265.&ots=ta1isTHB

Félix, M. (2017). A study on the expected impact of IFRS 17 on the transparency of financial statements

of insurance companies. MASTER THESIS, 1-69.

Gooley, J. (2016). Principles of Australian Contract Law. Australia: Lexis Nexis.

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

11 | P a g e

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd. Retrieved from https://www.routledge.com/Competitive-Strategy-Creating-

and-Sustaining-Superior-Performance/Belton/p/book/9781912128808

Boccia, F., & Leonardi, R. (2016). The Challenge of the Digital Economy: Markets, Taxation and

Appropriate Economic Models. Springer.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Das, P. (2017). Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), 10-17.

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. Retrieved from https://doi.org/10.1080/00014788.2017.1299620

Dumay, J., & Baard, V. (2017). An introduction to interventionist research in accounting. The Routledge

Companion to Qualitative Accounting Research Methods, 265. Retrieved from

https://books.google.co.in/books?

hl=en&lr=&id=PzQlDwAAQBAJ&oi=fnd&pg=PA265&dq=Dumay,+J.,+%26+Baard,+V.+(2017).

+An+introduction+to+interventionist+research+in+accounting.

+The+Routledge+Companion+to+Qualitative+Accounting+Research+Methods,

+265.&ots=ta1isTHB

Félix, M. (2017). A study on the expected impact of IFRS 17 on the transparency of financial statements

of insurance companies. MASTER THESIS, 1-69.

Gooley, J. (2016). Principles of Australian Contract Law. Australia: Lexis Nexis.

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.