Financial Accounting: Compliance Analysis of Wesfarmers and Rio Tinto

VerifiedAdded on 2023/04/04

|25

|4388

|295

Report

AI Summary

This report assesses the financial reporting compliance of Wesfarmers Ltd and Rio Tinto Ltd, two companies from different industries listed on the ASX. It examines their adherence to Australian Financial Reporting Standards, focusing on key areas such as the concept of a reporting entity, disclosures related to liabilities and intangible assets, and income tax disclosures. The report highlights the importance of following accounting standards to ensure transparency and accountability in financial reporting. It analyzes the qualitative characteristics of financial information, including relevance, faithful representation, comparability, verifiability, timeliness, and understandability, as demonstrated in the companies' annual reports. Specific examples from Wesfarmers and Rio Tinto are used to illustrate compliance with accounting standards related to provisions, interest-bearing securities, trade payables and other liabilities. Desklib offers a wealth of similar solved assignments and resources for students.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Concept of Reporting Entity........................................................................................................2

Disclosures of Liabilities.............................................................................................................6

Disclosures Relating to Intangible Assets.................................................................................10

Disclosure Relating to Income Tax Expenses...........................................................................15

Conclusion.....................................................................................................................................18

Reference.......................................................................................................................................20

FINANCIAL ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Concept of Reporting Entity........................................................................................................2

Disclosures of Liabilities.............................................................................................................6

Disclosures Relating to Intangible Assets.................................................................................10

Disclosure Relating to Income Tax Expenses...........................................................................15

Conclusion.....................................................................................................................................18

Reference.......................................................................................................................................20

2

FINANCIAL ACCOUNTING

Introduction

The main purpose of the assessment is to analyse reporting framework which is followed

by two entities which belong to different industries. The assessment analyses the reporting

framework of two different companies of different industries is to identify the compliance

requirements which each of the businesses follow as per the accounting standards introduced.

The companies which are considered for this assessment are Wesfarmers ltd which is engaged in

retail and consumer goods and Rio Tinto ltd which is engaged in the business of mining and

extraction of minerals (Riotinto.com. 2019). The report would be discussing the concept of

reporting entity for both the businesses and how the same is important from the perspective of

providing appropriate disclosures relating to the operations of the business. The assessment

would also deal with the disclosures which is provided by the business relating to liabilities and

intangibles assets of the business. In addition to this, the assessment would also be discussing

regarding the income tax disclosures which are provided by the management of the respective

companies in the annual reports which is prepared. The report would be focusing on the

application of relevant accounting standards which are applied by businesses in order to enhance

the quality of reports which is formulated by the businesses.

Discussion

Concept of Reporting Entity

The concept of reporting entity is important which deals with how the businesses needs to

report financial information so that the potential users of the financial statements can consider

the information and take decisions regarding the same appropriately. The concept of reporting

entity relates with the reasonableness that there exist users who are dependent on the disclosures

FINANCIAL ACCOUNTING

Introduction

The main purpose of the assessment is to analyse reporting framework which is followed

by two entities which belong to different industries. The assessment analyses the reporting

framework of two different companies of different industries is to identify the compliance

requirements which each of the businesses follow as per the accounting standards introduced.

The companies which are considered for this assessment are Wesfarmers ltd which is engaged in

retail and consumer goods and Rio Tinto ltd which is engaged in the business of mining and

extraction of minerals (Riotinto.com. 2019). The report would be discussing the concept of

reporting entity for both the businesses and how the same is important from the perspective of

providing appropriate disclosures relating to the operations of the business. The assessment

would also deal with the disclosures which is provided by the business relating to liabilities and

intangibles assets of the business. In addition to this, the assessment would also be discussing

regarding the income tax disclosures which are provided by the management of the respective

companies in the annual reports which is prepared. The report would be focusing on the

application of relevant accounting standards which are applied by businesses in order to enhance

the quality of reports which is formulated by the businesses.

Discussion

Concept of Reporting Entity

The concept of reporting entity is important which deals with how the businesses needs to

report financial information so that the potential users of the financial statements can consider

the information and take decisions regarding the same appropriately. The concept of reporting

entity relates with the reasonableness that there exist users who are dependent on the disclosures

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL ACCOUNTING

provided in the financial statements for taking important decisions regarding investments

(Fasb.org. 2019). The concept requires all businesses to incorporate relevant and useful financial

information in the annual reports so that the same can be used by the users for taking appropriate

decisions.

It is the responsibility of those charged with governance of the company to identify

primarily if the entity is a reporting concern or a non-reporting concern (Pkf.com.au. 2019). If

the former is the case, then the management of the company needs to prepare a general purpose

financial report. This also signifies that the entity needs to follow all relevant accounting

standards while formulating the general purpose financial report.

As per paragraph 10 of SAC 1 Definition of The Reporting Entity, the management of

the companies need to consider themselves as reporting entities and be identified by reference to

the existence of users who are dependent on general purpose financial reports for information for

making and evaluating resource allocation decisions (Aasb.gov.au. 2019). The provisions which

are stated in the SAC 1 clearly shows the application of reporting entity of the business and

classifies the different aspects which are considered similar to reporting entity concepts such

legal entity concept. The financial statements which are prepared by the management of the

company are done so that full disclosures are provided by businesses regarding every aspect of

the business and how the same can improve the transparency and accountability of the business.

It is a known fact that most of the businesses follow conceptual framework of accounting

which is followed across the global in order to ensure that there is consistency and accountability

in the information which is presented in the financial statements of the business. Such a

framework includes accounting standards, principles, conventions and rules on the basis of

which an entity prepares its financial statements. The annual reports which are prepared by the

FINANCIAL ACCOUNTING

provided in the financial statements for taking important decisions regarding investments

(Fasb.org. 2019). The concept requires all businesses to incorporate relevant and useful financial

information in the annual reports so that the same can be used by the users for taking appropriate

decisions.

It is the responsibility of those charged with governance of the company to identify

primarily if the entity is a reporting concern or a non-reporting concern (Pkf.com.au. 2019). If

the former is the case, then the management of the company needs to prepare a general purpose

financial report. This also signifies that the entity needs to follow all relevant accounting

standards while formulating the general purpose financial report.

As per paragraph 10 of SAC 1 Definition of The Reporting Entity, the management of

the companies need to consider themselves as reporting entities and be identified by reference to

the existence of users who are dependent on general purpose financial reports for information for

making and evaluating resource allocation decisions (Aasb.gov.au. 2019). The provisions which

are stated in the SAC 1 clearly shows the application of reporting entity of the business and

classifies the different aspects which are considered similar to reporting entity concepts such

legal entity concept. The financial statements which are prepared by the management of the

company are done so that full disclosures are provided by businesses regarding every aspect of

the business and how the same can improve the transparency and accountability of the business.

It is a known fact that most of the businesses follow conceptual framework of accounting

which is followed across the global in order to ensure that there is consistency and accountability

in the information which is presented in the financial statements of the business. Such a

framework includes accounting standards, principles, conventions and rules on the basis of

which an entity prepares its financial statements. The annual reports which are prepared by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL ACCOUNTING

management of the company should have relevant information along with proper disclosures for

all the treatments which is shown in the financial statements of the business. In addition to this,

the financial statement should also be prepared according to the qualitative characteristic of the

financial statements (Christensen and Nikolaev 2013). The annual report of both Wesfarmers ltd

and Rio Tinto ltd shows that the management of the company has effectively followed relevant

accounting standards and has been consistent with the reporting of different items which are

presented in the annual reports of the business. The disclosures which are provided in the annual

reports confirm with the policies which are followed by most of the businesses following the

reporting framework in the business (Edmonds et al. 2016). In order to enhance the quality of the

financial statements, the information which are included in the annual report should contain the

following qualitative characteristic of the generally accepted financial reports.

Fundamental Qualitative Characteristics

Relevance: The financial information which are included in the annual report of the

business should be relevant to requirements of the users so that appropriate decisions can

be provided on the basis of the information which are shown in the annual report of the

business (Barth 2013). The information and disclosures are considered to be relevant if

proper accounting standards are followed by the business. The annual reports of both

Wesfarmers ltd and Rio Tinto ltd shows that the business has disclosed all relevant

standards which are used by the management for preparing the financial statements of the

business.

Faithful Representation: The information which are shown in the annual reports should

be appropriate and free from any material misstatement. The concept of reporting entity

states that the information would be considered by the users for taking important

FINANCIAL ACCOUNTING

management of the company should have relevant information along with proper disclosures for

all the treatments which is shown in the financial statements of the business. In addition to this,

the financial statement should also be prepared according to the qualitative characteristic of the

financial statements (Christensen and Nikolaev 2013). The annual report of both Wesfarmers ltd

and Rio Tinto ltd shows that the management of the company has effectively followed relevant

accounting standards and has been consistent with the reporting of different items which are

presented in the annual reports of the business. The disclosures which are provided in the annual

reports confirm with the policies which are followed by most of the businesses following the

reporting framework in the business (Edmonds et al. 2016). In order to enhance the quality of the

financial statements, the information which are included in the annual report should contain the

following qualitative characteristic of the generally accepted financial reports.

Fundamental Qualitative Characteristics

Relevance: The financial information which are included in the annual report of the

business should be relevant to requirements of the users so that appropriate decisions can

be provided on the basis of the information which are shown in the annual report of the

business (Barth 2013). The information and disclosures are considered to be relevant if

proper accounting standards are followed by the business. The annual reports of both

Wesfarmers ltd and Rio Tinto ltd shows that the business has disclosed all relevant

standards which are used by the management for preparing the financial statements of the

business.

Faithful Representation: The information which are shown in the annual reports should

be appropriate and free from any material misstatement. The concept of reporting entity

states that the information would be considered by the users for taking important

5

FINANCIAL ACCOUNTING

decisions. It is therefore a requirement that the information which is presented in the

financial statement should be free from any omission or material misstatement. If a

financial statement is audited than the risks of material misstatement is significantly

lowered as the same is shown the case with Wesfarmers ltd and Rio Tinto ltd.

Enhancing Qualitative Characteristics

Comparability: The information which is shown in the annual reports of the business

should be comparable with performance of the business in next financial year (Chen et al.

2014). The users would be comparing the performance of the business with that of

previous years in order to take major decisions regarding investments.

Verifiability: The information which is presented in the annual report should be

verifiable by the users of the financial statements. This principle states that the treatments

which are shown in the annual reports for different items must be verifiable by the users

by assessing the disclosures which is provided in the notes to account section of the

annual report of the business (Henderson et al. 2015).

Timeliness: The information which are to be recorded in the financial statement should

be presented to the users in a timely manner so that the same can assist the users to take

major decisions regarding the business (Stice and Stice 2013). The timing of providing of

the financial statements are normally at the end of the financial year of the company. The

provisions of Para 36 of AASB 101 states that an entity shall present a complete set of

financial statements (including comparative information) at least annually (Aasb.gov.au.

2019). This shows that the management of the company needs to formulate the

accounting standards at least annually depending on the reporting period which is

followed by the management of the company.

FINANCIAL ACCOUNTING

decisions. It is therefore a requirement that the information which is presented in the

financial statement should be free from any omission or material misstatement. If a

financial statement is audited than the risks of material misstatement is significantly

lowered as the same is shown the case with Wesfarmers ltd and Rio Tinto ltd.

Enhancing Qualitative Characteristics

Comparability: The information which is shown in the annual reports of the business

should be comparable with performance of the business in next financial year (Chen et al.

2014). The users would be comparing the performance of the business with that of

previous years in order to take major decisions regarding investments.

Verifiability: The information which is presented in the annual report should be

verifiable by the users of the financial statements. This principle states that the treatments

which are shown in the annual reports for different items must be verifiable by the users

by assessing the disclosures which is provided in the notes to account section of the

annual report of the business (Henderson et al. 2015).

Timeliness: The information which are to be recorded in the financial statement should

be presented to the users in a timely manner so that the same can assist the users to take

major decisions regarding the business (Stice and Stice 2013). The timing of providing of

the financial statements are normally at the end of the financial year of the company. The

provisions of Para 36 of AASB 101 states that an entity shall present a complete set of

financial statements (including comparative information) at least annually (Aasb.gov.au.

2019). This shows that the management of the company needs to formulate the

accounting standards at least annually depending on the reporting period which is

followed by the management of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL ACCOUNTING

Understandability: The financial statement should be such that it can be easily be

understood by everyone (Stent and Dowler 2015). It is stated that the application of more

numeric and percentages figures would help the users to understand the information

which is covered in the annual reports of the business.

The above guidelines help the management of the company to make improvements in the

reporting framework and thereby also enhances the quality of financial reports which are

presented to the users of the financial statements. The financial information which is shown in

the annual report of both Wesfarmers and Rio Tinto ltd needs to adhere to the principles which is

stated in the above paragraph. However, the management of both the companies can still

improve the reporting framework which is followed by adding more disclosures and notes so that

the users are easily able to interpret the performance of the business.

Disclosures of Liabilities

The annual reports of the business also show the liabilities which are incurred by the

business during the period. As per the analysis of the financial statements of both Wesfarmers

and Rio Tinto ltd, the management of the respective companies has appropriately shown the

liabilities which are associated with the business. The presentation of the information in the

financial statement should be fair and free from any material misstatement as per the

requirements of AASB 101 (Aasb.gov.au. 2019). The disclosure regarding the liabilities which is

presented in the annual report of Wesfarmers ltd and Rio Tinto ltd are appropriately discussed

bellowed.

Wesfarmers ltd

FINANCIAL ACCOUNTING

Understandability: The financial statement should be such that it can be easily be

understood by everyone (Stent and Dowler 2015). It is stated that the application of more

numeric and percentages figures would help the users to understand the information

which is covered in the annual reports of the business.

The above guidelines help the management of the company to make improvements in the

reporting framework and thereby also enhances the quality of financial reports which are

presented to the users of the financial statements. The financial information which is shown in

the annual report of both Wesfarmers and Rio Tinto ltd needs to adhere to the principles which is

stated in the above paragraph. However, the management of both the companies can still

improve the reporting framework which is followed by adding more disclosures and notes so that

the users are easily able to interpret the performance of the business.

Disclosures of Liabilities

The annual reports of the business also show the liabilities which are incurred by the

business during the period. As per the analysis of the financial statements of both Wesfarmers

and Rio Tinto ltd, the management of the respective companies has appropriately shown the

liabilities which are associated with the business. The presentation of the information in the

financial statement should be fair and free from any material misstatement as per the

requirements of AASB 101 (Aasb.gov.au. 2019). The disclosure regarding the liabilities which is

presented in the annual report of Wesfarmers ltd and Rio Tinto ltd are appropriately discussed

bellowed.

Wesfarmers ltd

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL ACCOUNTING

The management of the company has covered different liabilities which have a complex

treatment in the notes to account section of the annual reports so that the users of the financial

statements can easily understand the treatment which is undertaken by the management of

Wesfarmers ltd.

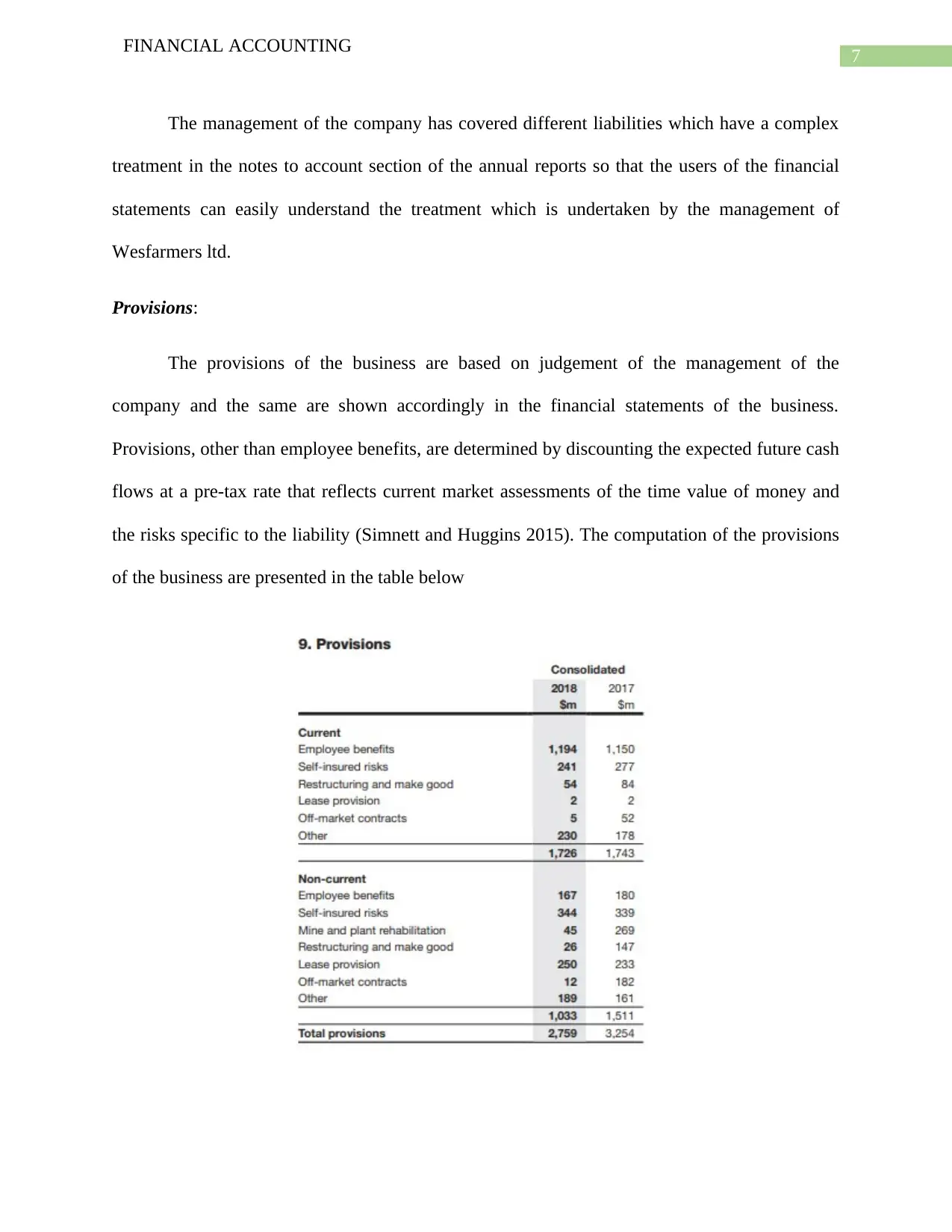

Provisions:

The provisions of the business are based on judgement of the management of the

company and the same are shown accordingly in the financial statements of the business.

Provisions, other than employee benefits, are determined by discounting the expected future cash

flows at a pre-tax rate that reflects current market assessments of the time value of money and

the risks specific to the liability (Simnett and Huggins 2015). The computation of the provisions

of the business are presented in the table below

FINANCIAL ACCOUNTING

The management of the company has covered different liabilities which have a complex

treatment in the notes to account section of the annual reports so that the users of the financial

statements can easily understand the treatment which is undertaken by the management of

Wesfarmers ltd.

Provisions:

The provisions of the business are based on judgement of the management of the

company and the same are shown accordingly in the financial statements of the business.

Provisions, other than employee benefits, are determined by discounting the expected future cash

flows at a pre-tax rate that reflects current market assessments of the time value of money and

the risks specific to the liability (Simnett and Huggins 2015). The computation of the provisions

of the business are presented in the table below

8

FINANCIAL ACCOUNTING

The above table represent that the different items on which provisions are created for the

current years and the total of the same are represented in the annual reports of the business. The

provisions of the business appropriately represent the losses which is anticipated by the

management of the company for the future period (Wesfarmers.com.au. 2019).

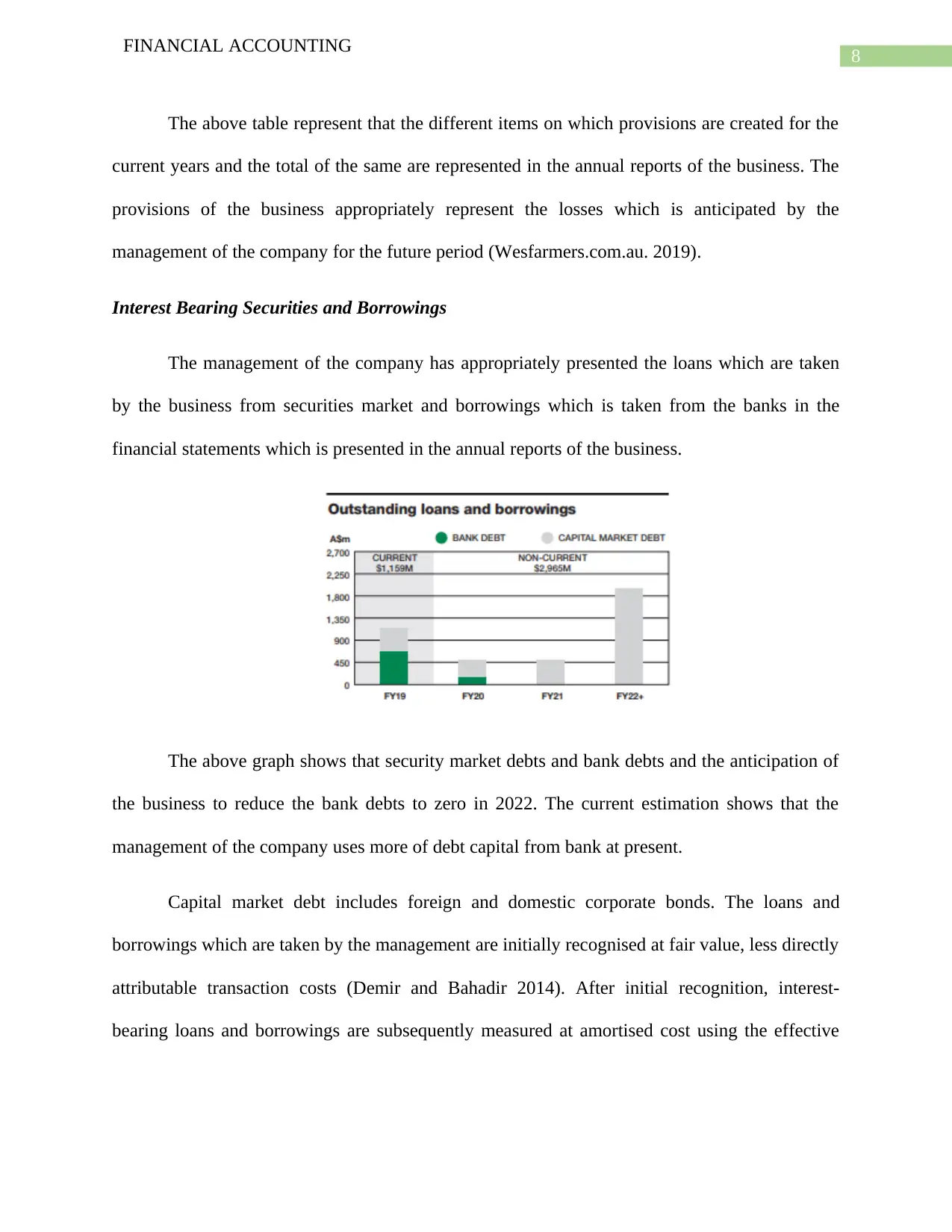

Interest Bearing Securities and Borrowings

The management of the company has appropriately presented the loans which are taken

by the business from securities market and borrowings which is taken from the banks in the

financial statements which is presented in the annual reports of the business.

The above graph shows that security market debts and bank debts and the anticipation of

the business to reduce the bank debts to zero in 2022. The current estimation shows that the

management of the company uses more of debt capital from bank at present.

Capital market debt includes foreign and domestic corporate bonds. The loans and

borrowings which are taken by the management are initially recognised at fair value, less directly

attributable transaction costs (Demir and Bahadir 2014). After initial recognition, interest-

bearing loans and borrowings are subsequently measured at amortised cost using the effective

FINANCIAL ACCOUNTING

The above table represent that the different items on which provisions are created for the

current years and the total of the same are represented in the annual reports of the business. The

provisions of the business appropriately represent the losses which is anticipated by the

management of the company for the future period (Wesfarmers.com.au. 2019).

Interest Bearing Securities and Borrowings

The management of the company has appropriately presented the loans which are taken

by the business from securities market and borrowings which is taken from the banks in the

financial statements which is presented in the annual reports of the business.

The above graph shows that security market debts and bank debts and the anticipation of

the business to reduce the bank debts to zero in 2022. The current estimation shows that the

management of the company uses more of debt capital from bank at present.

Capital market debt includes foreign and domestic corporate bonds. The loans and

borrowings which are taken by the management are initially recognised at fair value, less directly

attributable transaction costs (Demir and Bahadir 2014). After initial recognition, interest-

bearing loans and borrowings are subsequently measured at amortised cost using the effective

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL ACCOUNTING

interest method. The carrying value of all assets and liabilities are also considered for the

purpose of recognition of the same.

Rio Tinto Ltd

The disclosures which are provided by the management of Rio Tinto ltd in the annual

reports of the business effectively are explained below:

Trade Payables:

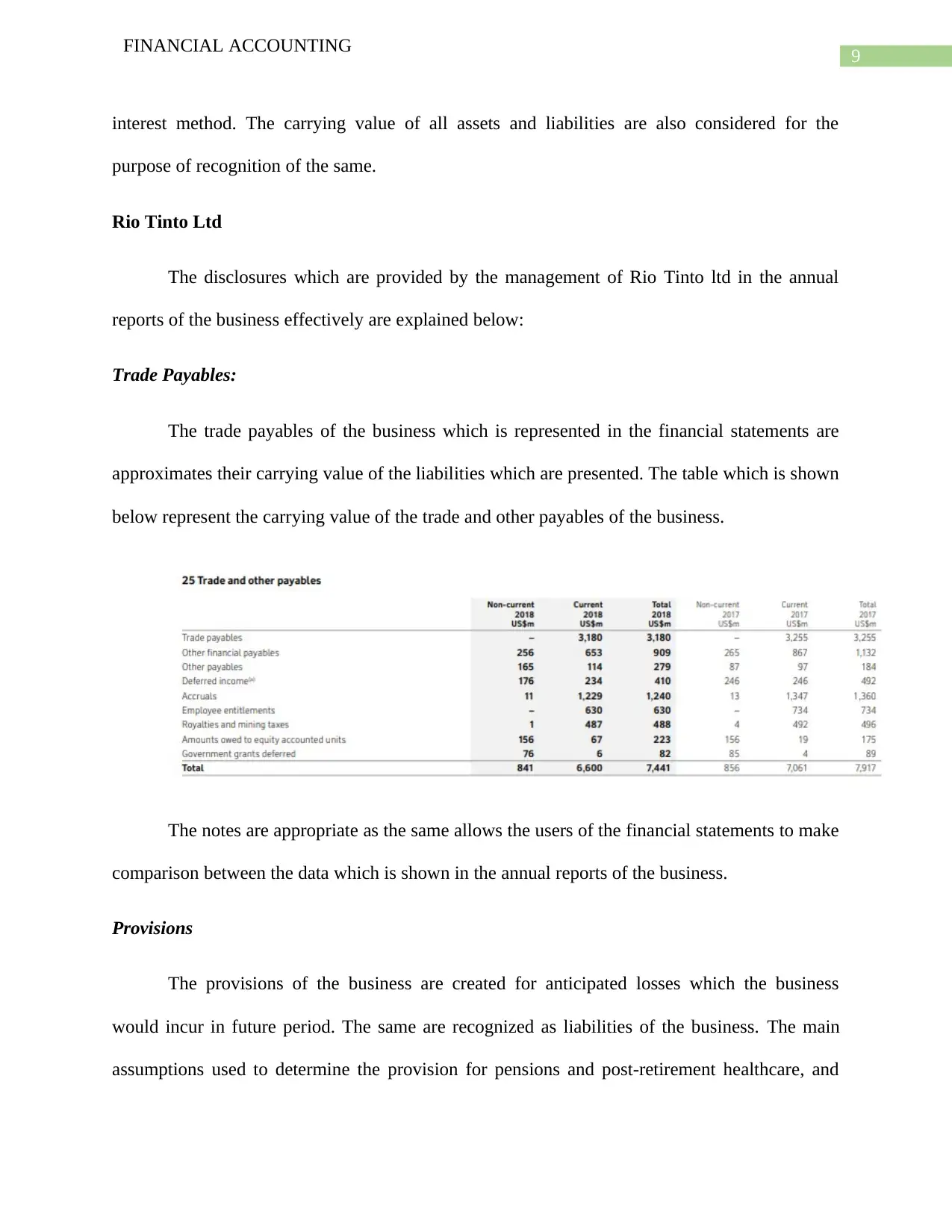

The trade payables of the business which is represented in the financial statements are

approximates their carrying value of the liabilities which are presented. The table which is shown

below represent the carrying value of the trade and other payables of the business.

The notes are appropriate as the same allows the users of the financial statements to make

comparison between the data which is shown in the annual reports of the business.

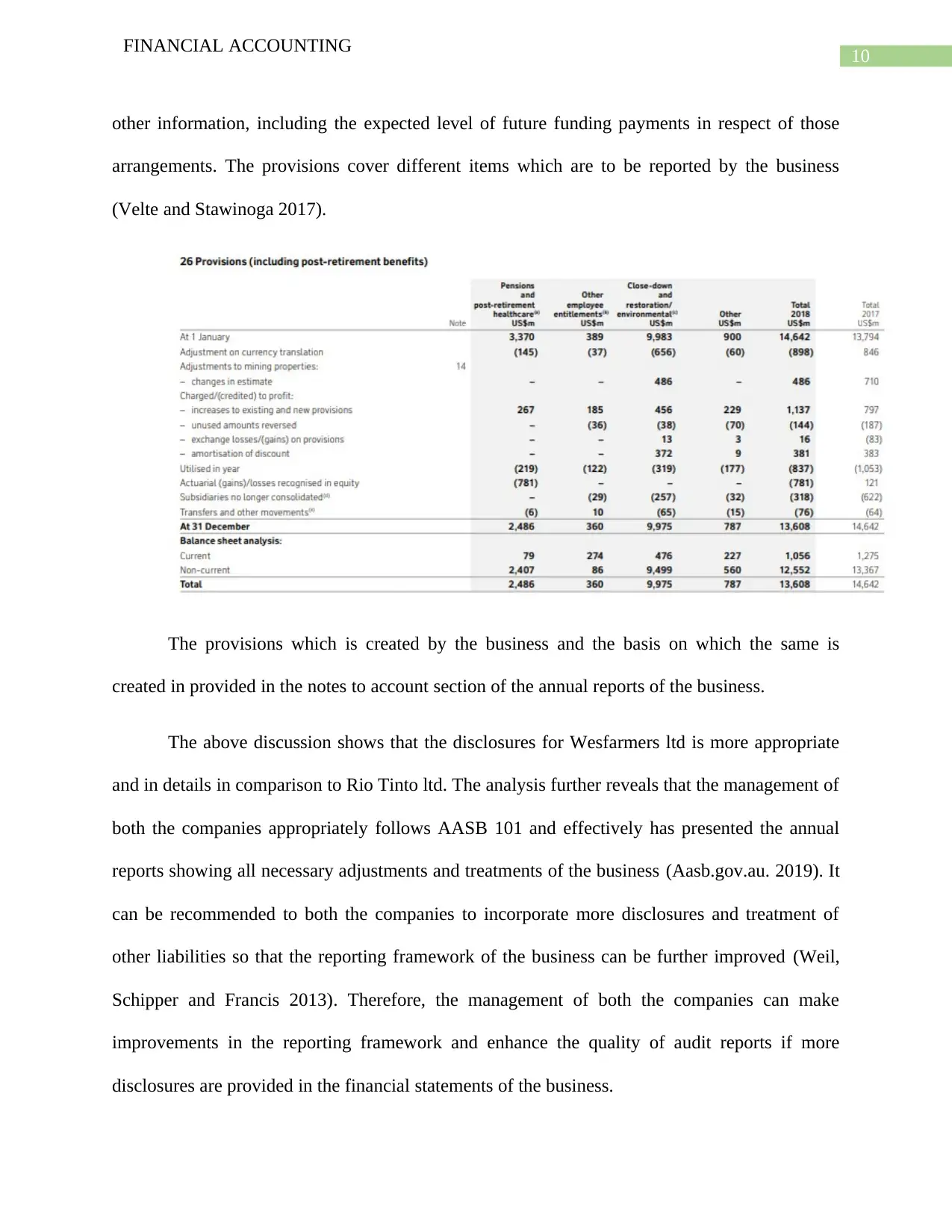

Provisions

The provisions of the business are created for anticipated losses which the business

would incur in future period. The same are recognized as liabilities of the business. The main

assumptions used to determine the provision for pensions and post-retirement healthcare, and

FINANCIAL ACCOUNTING

interest method. The carrying value of all assets and liabilities are also considered for the

purpose of recognition of the same.

Rio Tinto Ltd

The disclosures which are provided by the management of Rio Tinto ltd in the annual

reports of the business effectively are explained below:

Trade Payables:

The trade payables of the business which is represented in the financial statements are

approximates their carrying value of the liabilities which are presented. The table which is shown

below represent the carrying value of the trade and other payables of the business.

The notes are appropriate as the same allows the users of the financial statements to make

comparison between the data which is shown in the annual reports of the business.

Provisions

The provisions of the business are created for anticipated losses which the business

would incur in future period. The same are recognized as liabilities of the business. The main

assumptions used to determine the provision for pensions and post-retirement healthcare, and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL ACCOUNTING

other information, including the expected level of future funding payments in respect of those

arrangements. The provisions cover different items which are to be reported by the business

(Velte and Stawinoga 2017).

The provisions which is created by the business and the basis on which the same is

created in provided in the notes to account section of the annual reports of the business.

The above discussion shows that the disclosures for Wesfarmers ltd is more appropriate

and in details in comparison to Rio Tinto ltd. The analysis further reveals that the management of

both the companies appropriately follows AASB 101 and effectively has presented the annual

reports showing all necessary adjustments and treatments of the business (Aasb.gov.au. 2019). It

can be recommended to both the companies to incorporate more disclosures and treatment of

other liabilities so that the reporting framework of the business can be further improved (Weil,

Schipper and Francis 2013). Therefore, the management of both the companies can make

improvements in the reporting framework and enhance the quality of audit reports if more

disclosures are provided in the financial statements of the business.

FINANCIAL ACCOUNTING

other information, including the expected level of future funding payments in respect of those

arrangements. The provisions cover different items which are to be reported by the business

(Velte and Stawinoga 2017).

The provisions which is created by the business and the basis on which the same is

created in provided in the notes to account section of the annual reports of the business.

The above discussion shows that the disclosures for Wesfarmers ltd is more appropriate

and in details in comparison to Rio Tinto ltd. The analysis further reveals that the management of

both the companies appropriately follows AASB 101 and effectively has presented the annual

reports showing all necessary adjustments and treatments of the business (Aasb.gov.au. 2019). It

can be recommended to both the companies to incorporate more disclosures and treatment of

other liabilities so that the reporting framework of the business can be further improved (Weil,

Schipper and Francis 2013). Therefore, the management of both the companies can make

improvements in the reporting framework and enhance the quality of audit reports if more

disclosures are provided in the financial statements of the business.

11

FINANCIAL ACCOUNTING

Disclosures Relating to Intangible Assets

The accounting for intangible assets of a business is considered to be a complex process

and therefore businesses are expected to follow the provisions and guidelines which are stated

under AASB 138 Intangibles Assets. As per para 12 of AASB 138, an intangible asset is

identifiable if it is either:

Is separable which means that the management of the company can sale it, transfer it,

license it, rent it or use the same for exchange.

Arises from contractual or other legal rights, regardless of whether those rights are

transferable or separable (Aasb.gov.au. 2019).

The intangible assets are recognized in the financial statements if the same are consistent

with Para 21 of AASB 138 (Aasb.gov.au. 2019). The para states that intangible assets can be

recognized if it is probable that the expected future economic benefits that are attributable to the

asset will flow to the entity and the cost of the asset can be measured reliably. The standard

effectively guides accountants regarding the disclosures which are to be provided in the annual

reports of the business.

In addition to the recognition and measurement criteria, the standard also provides a guide as

to what is to be included in the financial statements in the notes to account section of the annual

reports of the business (K. Johl et al, 2013). The standard requires companies to disclose the

useful life of the assets and also the amortization method which is considered for disclosing the

key aspects of the report of the business. The management of the company also needs to report

gross carrying amount and any accumulated amortisation on the intangible assets which is

reported in the balance sheet of the company.

FINANCIAL ACCOUNTING

Disclosures Relating to Intangible Assets

The accounting for intangible assets of a business is considered to be a complex process

and therefore businesses are expected to follow the provisions and guidelines which are stated

under AASB 138 Intangibles Assets. As per para 12 of AASB 138, an intangible asset is

identifiable if it is either:

Is separable which means that the management of the company can sale it, transfer it,

license it, rent it or use the same for exchange.

Arises from contractual or other legal rights, regardless of whether those rights are

transferable or separable (Aasb.gov.au. 2019).

The intangible assets are recognized in the financial statements if the same are consistent

with Para 21 of AASB 138 (Aasb.gov.au. 2019). The para states that intangible assets can be

recognized if it is probable that the expected future economic benefits that are attributable to the

asset will flow to the entity and the cost of the asset can be measured reliably. The standard

effectively guides accountants regarding the disclosures which are to be provided in the annual

reports of the business.

In addition to the recognition and measurement criteria, the standard also provides a guide as

to what is to be included in the financial statements in the notes to account section of the annual

reports of the business (K. Johl et al, 2013). The standard requires companies to disclose the

useful life of the assets and also the amortization method which is considered for disclosing the

key aspects of the report of the business. The management of the company also needs to report

gross carrying amount and any accumulated amortisation on the intangible assets which is

reported in the balance sheet of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.