Evaluating Financial Reporting Systems and Costing Methodologies

VerifiedAdded on 2023/06/18

|16

|3825

|463

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on financial reporting systems and costing methodologies. It discusses various financial reporting systems, including cost accounting, inventory management, and price optimization, highlighting their critical applications in enhancing profitability, performance evaluation, and managerial influence. The report also examines different financial reporting systems used in creating reports such as income statements, financial declarations, and summaries of financial positions. Furthermore, it delves into various costing methodologies like marginal costing and absorption costing, comparing their features and applications. The analysis includes examples of income statement formulations using marginal costing. Finally, the report touches on the benefits and drawbacks of using planning techniques in the budgeting process and addresses various financial problems and measures to mitigate them, using Nero Ltd. as a case study. Desklib offers this student-contributed assignment and many more resources to aid students in their studies.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

P1: Financial reporting systems of varying sorts and their critical applications....................3

P2: Different financial reporting systems that are being used in various sorts of reports......5

P3: Various costing methodologies and income statement formulation................................7

SECTION 2....................................................................................................................................12

PART A.........................................................................................................................................12

P4: The benefits and drawbacks of utilising planning techniques in budgeting process.....12

PART B..........................................................................................................................................13

P5: Different financial problems and measures to address them.........................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

P1: Financial reporting systems of varying sorts and their critical applications....................3

P2: Different financial reporting systems that are being used in various sorts of reports......5

P3: Various costing methodologies and income statement formulation................................7

SECTION 2....................................................................................................................................12

PART A.........................................................................................................................................12

P4: The benefits and drawbacks of utilising planning techniques in budgeting process.....12

PART B..........................................................................................................................................13

P5: Different financial problems and measures to address them.........................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial bookkeeping is much more helpful in defining, measuring, analysing, and

evaluate budgets financial reporting records that also aids in providing essential information and

developing appropriate proposals for the improvement of an institution (Eisenberg, 2016).

Financial reporting leaders are accountable for recording all financial and non-financial transfers

that occur on an everyday ground that also aids in recognising financially viable ways a

corporation achieves attractive returns. Accounting statements must be needed of companies on a

yearly ground in order to form the corporation's monetary stance to their interested parties. Nero

Ltd. is the basis for the current guidance document. All other facets are described in the light of

this document. The endeavour proposal discusses various bookkeeping structures and providing

information that help leadership develop and implement decisions and planning processes for

development and prosperity. This document also discusses various management strategies been

using to regulate the cash flow.

SECTION 1

P1: Financial reporting systems of varying sorts and their critical applications

There are numerous activities that occur on a routine criterion in company processes that

should be documented and maintained in finance statements like profits and losses, income

statements, cash flow statements, and so forth. Those very plans are published with the intention

of discovering the firm's current monetary situation, so that organisation is better ready to take

corrective measures if some inaccuracies or discrepancies are discovered in the accounting

records. This compels organisation to implement a variety of financial accounting, such as cost

accounting processes, stock managerial structures, price optimization structures, and so on. Prior

to actually implementing of those kind financial structures inside an institution, supervisors must

initially recognise their critical issues that are mentioned underneath:

Increased profitability: This would aid in determining the effectiveness areas of industry

operations by remedying inconsistencies or variations that could prevents individuals from

performing to their full potential.

Performance evaluation: Various accounting technologies aid in evaluating worker

productivity by contrasting real to conventional productivity. This would aid in determining any

deviations of the kind that managers would be able to settle as soon as feasible.

Managerial bookkeeping is much more helpful in defining, measuring, analysing, and

evaluate budgets financial reporting records that also aids in providing essential information and

developing appropriate proposals for the improvement of an institution (Eisenberg, 2016).

Financial reporting leaders are accountable for recording all financial and non-financial transfers

that occur on an everyday ground that also aids in recognising financially viable ways a

corporation achieves attractive returns. Accounting statements must be needed of companies on a

yearly ground in order to form the corporation's monetary stance to their interested parties. Nero

Ltd. is the basis for the current guidance document. All other facets are described in the light of

this document. The endeavour proposal discusses various bookkeeping structures and providing

information that help leadership develop and implement decisions and planning processes for

development and prosperity. This document also discusses various management strategies been

using to regulate the cash flow.

SECTION 1

P1: Financial reporting systems of varying sorts and their critical applications

There are numerous activities that occur on a routine criterion in company processes that

should be documented and maintained in finance statements like profits and losses, income

statements, cash flow statements, and so forth. Those very plans are published with the intention

of discovering the firm's current monetary situation, so that organisation is better ready to take

corrective measures if some inaccuracies or discrepancies are discovered in the accounting

records. This compels organisation to implement a variety of financial accounting, such as cost

accounting processes, stock managerial structures, price optimization structures, and so on. Prior

to actually implementing of those kind financial structures inside an institution, supervisors must

initially recognise their critical issues that are mentioned underneath:

Increased profitability: This would aid in determining the effectiveness areas of industry

operations by remedying inconsistencies or variations that could prevents individuals from

performing to their full potential.

Performance evaluation: Various accounting technologies aid in evaluating worker

productivity by contrasting real to conventional productivity. This would aid in determining any

deviations of the kind that managers would be able to settle as soon as feasible.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

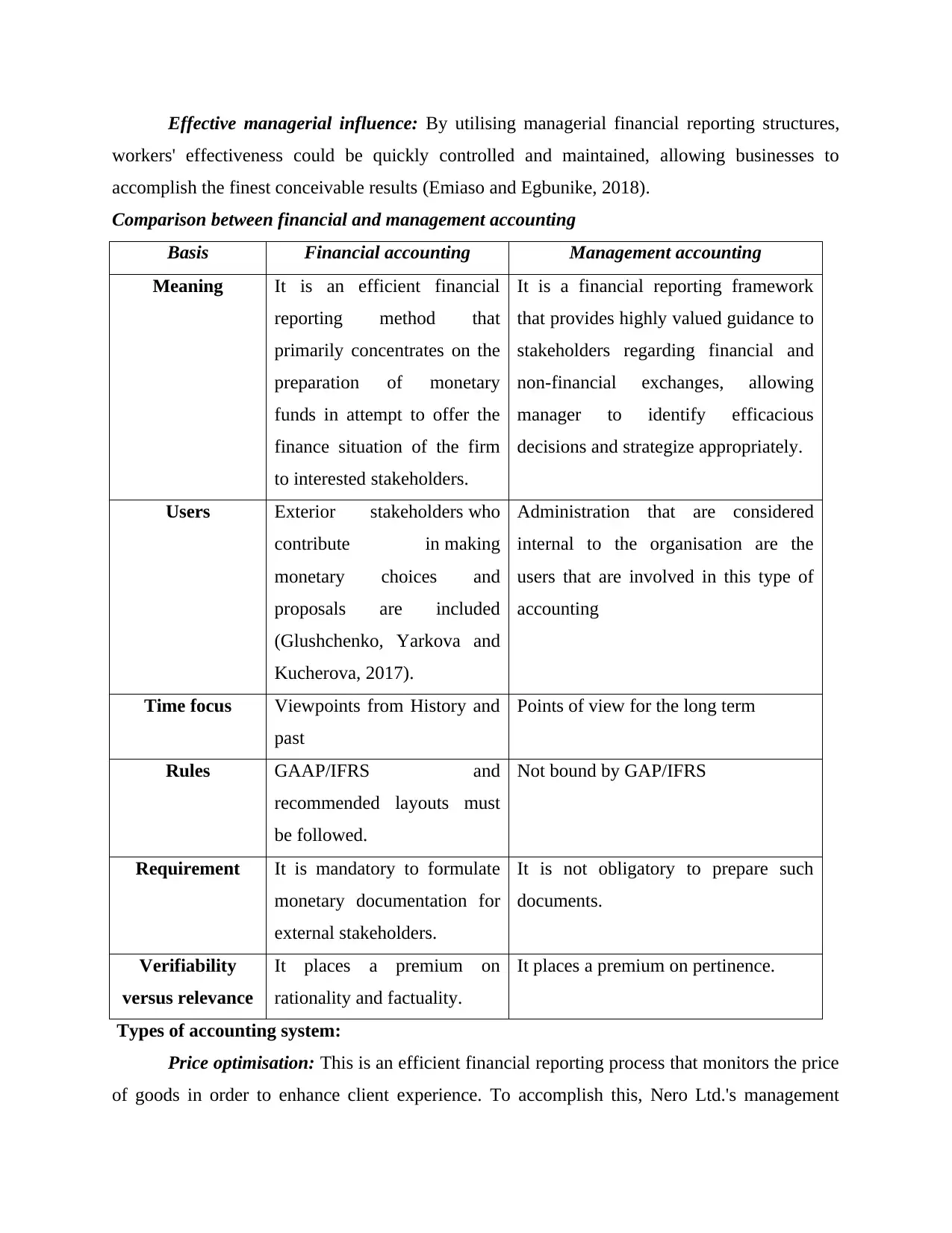

Effective managerial influence: By utilising managerial financial reporting structures,

workers' effectiveness could be quickly controlled and maintained, allowing businesses to

accomplish the finest conceivable results (Emiaso and Egbunike, 2018).

Comparison between financial and management accounting

Basis Financial accounting Management accounting

Meaning It is an efficient financial

reporting method that

primarily concentrates on the

preparation of monetary

funds in attempt to offer the

finance situation of the firm

to interested stakeholders.

It is a financial reporting framework

that provides highly valued guidance to

stakeholders regarding financial and

non-financial exchanges, allowing

manager to identify efficacious

decisions and strategize appropriately.

Users Exterior stakeholders who

contribute in making

monetary choices and

proposals are included

(Glushchenko, Yarkova and

Kucherova, 2017).

Administration that are considered

internal to the organisation are the

users that are involved in this type of

accounting

Time focus Viewpoints from History and

past

Points of view for the long term

Rules GAAP/IFRS and

recommended layouts must

be followed.

Not bound by GAP/IFRS

Requirement It is mandatory to formulate

monetary documentation for

external stakeholders.

It is not obligatory to prepare such

documents.

Verifiability

versus relevance

It places a premium on

rationality and factuality.

It places a premium on pertinence.

Types of accounting system:

Price optimisation: This is an efficient financial reporting process that monitors the price

of goods in order to enhance client experience. To accomplish this, Nero Ltd.'s management

workers' effectiveness could be quickly controlled and maintained, allowing businesses to

accomplish the finest conceivable results (Emiaso and Egbunike, 2018).

Comparison between financial and management accounting

Basis Financial accounting Management accounting

Meaning It is an efficient financial

reporting method that

primarily concentrates on the

preparation of monetary

funds in attempt to offer the

finance situation of the firm

to interested stakeholders.

It is a financial reporting framework

that provides highly valued guidance to

stakeholders regarding financial and

non-financial exchanges, allowing

manager to identify efficacious

decisions and strategize appropriately.

Users Exterior stakeholders who

contribute in making

monetary choices and

proposals are included

(Glushchenko, Yarkova and

Kucherova, 2017).

Administration that are considered

internal to the organisation are the

users that are involved in this type of

accounting

Time focus Viewpoints from History and

past

Points of view for the long term

Rules GAAP/IFRS and

recommended layouts must

be followed.

Not bound by GAP/IFRS

Requirement It is mandatory to formulate

monetary documentation for

external stakeholders.

It is not obligatory to prepare such

documents.

Verifiability

versus relevance

It places a premium on

rationality and factuality.

It places a premium on pertinence.

Types of accounting system:

Price optimisation: This is an efficient financial reporting process that monitors the price

of goods in order to enhance client experience. To accomplish this, Nero Ltd.'s management

accountant must employ an investigator to undertake investigations on their behalf and assist

them in evaluating the exact attitudes of consumers toward the prices indicted by the firm on

their goods and offerings. Operational expenses, inventory, and ancient significance are all

specifics utilised in price optimization. Thereby, after understanding the relative amount of client

contentment, the supervisor of Nero is ready to establish an optimal rate that also boosts

consumer purchasing behaviour and attitude and also the corporation's financial gains.

Cost accounting system: Such a financial reporting method is helpful to use in attempt to

calculate the overall expense or costs accrued in the manufacturing procedure in sequence to

produce durability goods, which enables the business to established its percentage on every item.

To accomplish this, the supervisor of Nero Ltd. must intend to concentrate on expense reduction

by enlightening its staff to operate on technological advances that also allows them to produce

top notch goods at the lowest possible price, thereby increasing the firm's financial performance

(Hyndman, 2016).

Inventory management system: It is a method of management that establishes and

monitors non-capital investments and inventory merchandise. It is beneficial to utilise such a

method that enables the businesses to manage how much inventory is accessible at any given

period. This would allow the team of Nero Ltd. to make purchases of stock from providers in

sequence to accomplish an optimal quantity of stock at storage facilities, ensuring that the

manufacturing framework is not disrupted in any way and that clients ’ requirements are met in a

brief span of time.

Job costing system: Such a financial reporting framework is much more beneficial to the

management team of Nero Ltd. in allocating costs to create a particular item or a group of goods

of the highest performance. This could motivate the employee to consider how and when to

lower the expense of operational activities and identify sectors where even the price of inventing

more must be needed and can prove beneficial for the company in the long run. This could assist

managers in determining a spending plan for reaching employment action based on its

production period and financially viable results obtained in the long term.

P2: Different financial reporting systems that are being used in various sorts of reports

In a sequence to make sound choices and relevant cost, the management accountant must

possess crucial data about the monetary standing of the firm and current assets so that long term

enterprise operations could be carried out more effectively. As a result, each trade association,

them in evaluating the exact attitudes of consumers toward the prices indicted by the firm on

their goods and offerings. Operational expenses, inventory, and ancient significance are all

specifics utilised in price optimization. Thereby, after understanding the relative amount of client

contentment, the supervisor of Nero is ready to establish an optimal rate that also boosts

consumer purchasing behaviour and attitude and also the corporation's financial gains.

Cost accounting system: Such a financial reporting method is helpful to use in attempt to

calculate the overall expense or costs accrued in the manufacturing procedure in sequence to

produce durability goods, which enables the business to established its percentage on every item.

To accomplish this, the supervisor of Nero Ltd. must intend to concentrate on expense reduction

by enlightening its staff to operate on technological advances that also allows them to produce

top notch goods at the lowest possible price, thereby increasing the firm's financial performance

(Hyndman, 2016).

Inventory management system: It is a method of management that establishes and

monitors non-capital investments and inventory merchandise. It is beneficial to utilise such a

method that enables the businesses to manage how much inventory is accessible at any given

period. This would allow the team of Nero Ltd. to make purchases of stock from providers in

sequence to accomplish an optimal quantity of stock at storage facilities, ensuring that the

manufacturing framework is not disrupted in any way and that clients ’ requirements are met in a

brief span of time.

Job costing system: Such a financial reporting framework is much more beneficial to the

management team of Nero Ltd. in allocating costs to create a particular item or a group of goods

of the highest performance. This could motivate the employee to consider how and when to

lower the expense of operational activities and identify sectors where even the price of inventing

more must be needed and can prove beneficial for the company in the long run. This could assist

managers in determining a spending plan for reaching employment action based on its

production period and financially viable results obtained in the long term.

P2: Different financial reporting systems that are being used in various sorts of reports

In a sequence to make sound choices and relevant cost, the management accountant must

possess crucial data about the monetary standing of the firm and current assets so that long term

enterprise operations could be carried out more effectively. As a result, each trade association,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

like Nero Ltd., should start preparing various reports on a continual ground in order to obtain

details whenever it is needed. Income statements, financial declarations, summary of financial

position, and other financial statements provide critical guidance to stakeholders. These reports

aid in determining as to if a corporation has the opportunity to interfere with both short and long-

term liabilities in the coming years. All long term decisions made by supervisors must be

designed to take into account the data given via those very reports, so that factors which are

affecting the business success can be conveniently detected (Jermias, Gani and Juliana, 2018).

These reports are much more beneficial when some changes are made in response to

volatility in industry circumstances. These reports, on either side, could not be produced without

the cooperation of various divisions. As a result, sufficient assistance from them is mandated,

allowing the firms to manage the requisites of every division in the implementation of specific

industry operations. As a result, managers need to use different reporting systems to assist people

in investigating their monetary exchanges. This would aid in determining the corporation's

accurate and reasonable monetary stance. This type of reporting framework consists of the

following components:

Performance report: These reports are kept up by companies with the goal of assessing

the productivity of workers and also an institution, assisting people in tackling problems and

discrepancies that could occur in the context of carrying out corporate operations in a much more

efficient way. These reports involve details about asset utilization and prospective possibilities

for expansion for third party companies. This could assist in understanding the relative condition

of the company and, as a result, putting forth best initiatives in optimising its effectiveness

level by eliminating all obstacles and divergences.

Account receivable ageing report: It includes information about the firm's

uncompensated borrowers and instructs managers to take certain objectives and proposals to

regain the liabilities as well as with interest. It aids the organisation in developing sensible

measures for eradicating those very situations in the coming years. As a result, it is critical to

create these reports that would offer additional costumer specifics associated with debt payroll

methods.

Inventory management report: It is far more challenging for warehouse manger to

regulate amount of inventory at the highest tier, which could be addressed by utilising a suitable

inventory platform that could assist in evaluating an organization's stock levels. Economic order

details whenever it is needed. Income statements, financial declarations, summary of financial

position, and other financial statements provide critical guidance to stakeholders. These reports

aid in determining as to if a corporation has the opportunity to interfere with both short and long-

term liabilities in the coming years. All long term decisions made by supervisors must be

designed to take into account the data given via those very reports, so that factors which are

affecting the business success can be conveniently detected (Jermias, Gani and Juliana, 2018).

These reports are much more beneficial when some changes are made in response to

volatility in industry circumstances. These reports, on either side, could not be produced without

the cooperation of various divisions. As a result, sufficient assistance from them is mandated,

allowing the firms to manage the requisites of every division in the implementation of specific

industry operations. As a result, managers need to use different reporting systems to assist people

in investigating their monetary exchanges. This would aid in determining the corporation's

accurate and reasonable monetary stance. This type of reporting framework consists of the

following components:

Performance report: These reports are kept up by companies with the goal of assessing

the productivity of workers and also an institution, assisting people in tackling problems and

discrepancies that could occur in the context of carrying out corporate operations in a much more

efficient way. These reports involve details about asset utilization and prospective possibilities

for expansion for third party companies. This could assist in understanding the relative condition

of the company and, as a result, putting forth best initiatives in optimising its effectiveness

level by eliminating all obstacles and divergences.

Account receivable ageing report: It includes information about the firm's

uncompensated borrowers and instructs managers to take certain objectives and proposals to

regain the liabilities as well as with interest. It aids the organisation in developing sensible

measures for eradicating those very situations in the coming years. As a result, it is critical to

create these reports that would offer additional costumer specifics associated with debt payroll

methods.

Inventory management report: It is far more challenging for warehouse manger to

regulate amount of inventory at the highest tier, which could be addressed by utilising a suitable

inventory platform that could assist in evaluating an organization's stock levels. Economic order

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

quantity, activity based costing, and stock control proportions are examples of these kind of

techniques. As a result, these reports given ample knowledge regarding the existing quantity of

stock, directing supervisors to determine whether to choose or not to in relation with the relevant

orders with the prospective providers that are prevailing in the market.

Job cost report: These reports assist managers in tracking overall costs sustained during

the manufacturing procedure, allowing them to conveniently identify the price of generating each

item. This could assist managers in establishing item rates after conducting a thorough

assessment of expenses and their financially viable results. It is much more useful in assigning

operation costs in terms of dealing with monetary quality and effectiveness over period (Kuurila,

2016).

P3: Various costing methodologies and income statement formulation

Cost: It relates to the quantity of money financed in the procedure of carrying out various

company operations in order to accomplish lucrative results in the coming years. Advertising

campaigns, operational processes, and so on are examples of these operations. Expenses

involved in carrying out manufacturing operations, for instance, involve employment costs, cost

of raw materials, and operating expenses.

As a result, it is critical for Nero Ltd's leadership to employ various valuation techniques

in necessarily to prepare rates for its goods and offerings that optimise client fulfilment while

also increasing the firm’s productivity. There seem to be various methodologies of costing that

can assist in tackling a corporation's additional costs. These costing techniques involve:

Marginal costing: It relates to the price of generating an extra component of volume in

order to cater the requisites and demands of the client. It's also much more efficacious in stock

pricing because the inventory worth is underpriced when changeable costs are considered. As a

result, these costing systems exclude permanent expenses and only take into account varying

costs.

Absorption costing: These costing techniques compromise all expenditures inflicted

during the production procedure, implying that both permanent and changeable costs must be

considered when valuing goods and facilities. It includes everything that has an immediate

repercussion on the goods. Worker costs, production costs, and operational expenditure are

examples of these costs.

Comparison between Marginal and Absorption costing

techniques. As a result, these reports given ample knowledge regarding the existing quantity of

stock, directing supervisors to determine whether to choose or not to in relation with the relevant

orders with the prospective providers that are prevailing in the market.

Job cost report: These reports assist managers in tracking overall costs sustained during

the manufacturing procedure, allowing them to conveniently identify the price of generating each

item. This could assist managers in establishing item rates after conducting a thorough

assessment of expenses and their financially viable results. It is much more useful in assigning

operation costs in terms of dealing with monetary quality and effectiveness over period (Kuurila,

2016).

P3: Various costing methodologies and income statement formulation

Cost: It relates to the quantity of money financed in the procedure of carrying out various

company operations in order to accomplish lucrative results in the coming years. Advertising

campaigns, operational processes, and so on are examples of these operations. Expenses

involved in carrying out manufacturing operations, for instance, involve employment costs, cost

of raw materials, and operating expenses.

As a result, it is critical for Nero Ltd's leadership to employ various valuation techniques

in necessarily to prepare rates for its goods and offerings that optimise client fulfilment while

also increasing the firm’s productivity. There seem to be various methodologies of costing that

can assist in tackling a corporation's additional costs. These costing techniques involve:

Marginal costing: It relates to the price of generating an extra component of volume in

order to cater the requisites and demands of the client. It's also much more efficacious in stock

pricing because the inventory worth is underpriced when changeable costs are considered. As a

result, these costing systems exclude permanent expenses and only take into account varying

costs.

Absorption costing: These costing techniques compromise all expenditures inflicted

during the production procedure, implying that both permanent and changeable costs must be

considered when valuing goods and facilities. It includes everything that has an immediate

repercussion on the goods. Worker costs, production costs, and operational expenditure are

examples of these costs.

Comparison between Marginal and Absorption costing

Marginal costing Absorption costing

When valuing goods and facilities, it really

only considers changeable costs and ignores

fixed costs.

At the moment of market value, it includes

both permanent and changeable costs.

Revenues increases when utilising this

technique because earnings are collected

from each independent selling (Maalouf and

El-Fadel, 2019).

A profit margin appears to be at a bare lower

limit while using this technique.

In an institution, this technique is helpful for

creating quick choices.

A technique like this is helpful for creating

long-term choices.

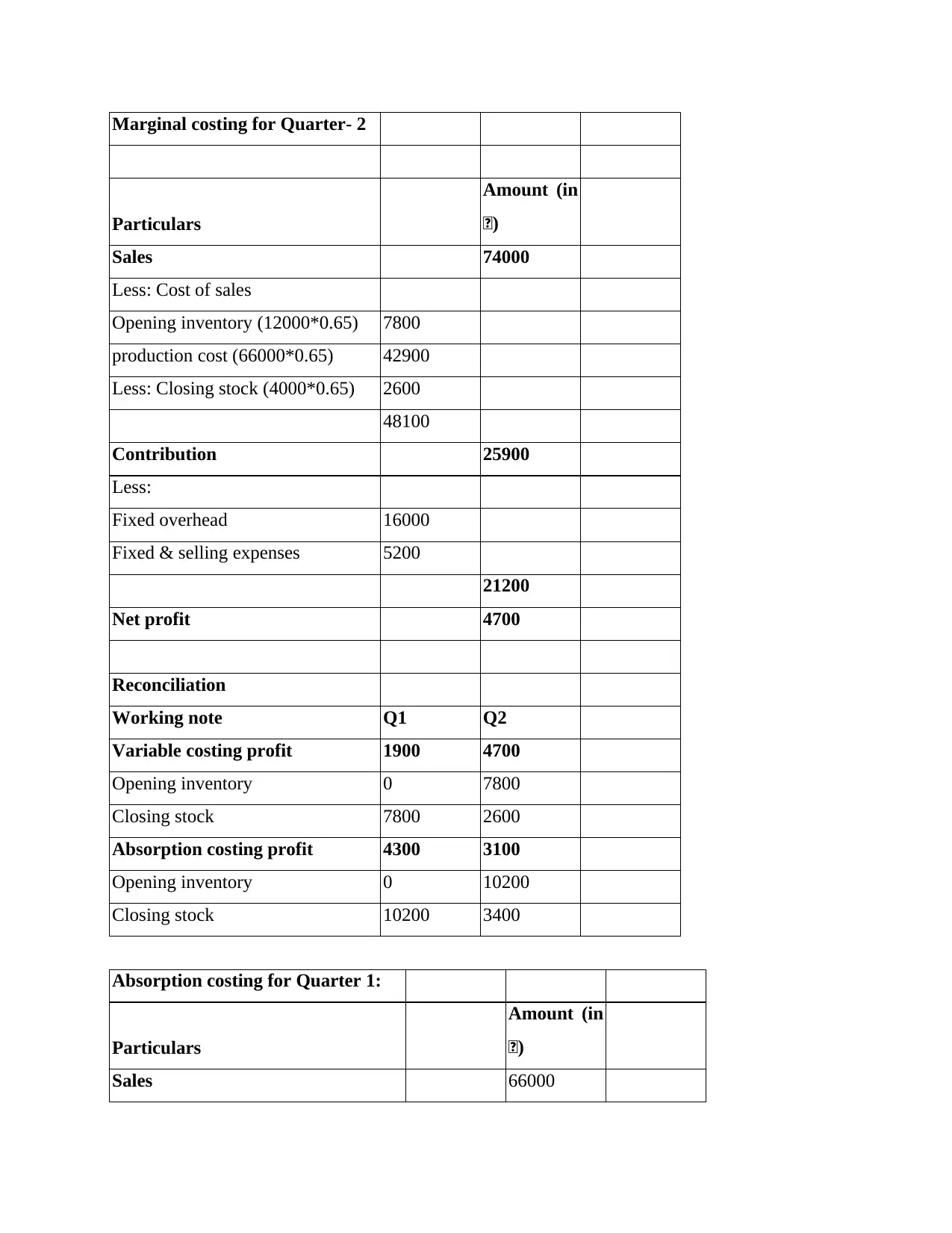

Marginal costing for Quarter 1

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

When valuing goods and facilities, it really

only considers changeable costs and ignores

fixed costs.

At the moment of market value, it includes

both permanent and changeable costs.

Revenues increases when utilising this

technique because earnings are collected

from each independent selling (Maalouf and

El-Fadel, 2019).

A profit margin appears to be at a bare lower

limit while using this technique.

In an institution, this technique is helpful for

creating quick choices.

A technique like this is helpful for creating

long-term choices.

Marginal costing for Quarter 1

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marginal costing for Quarter- 2

Particulars

Amount (in

£)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

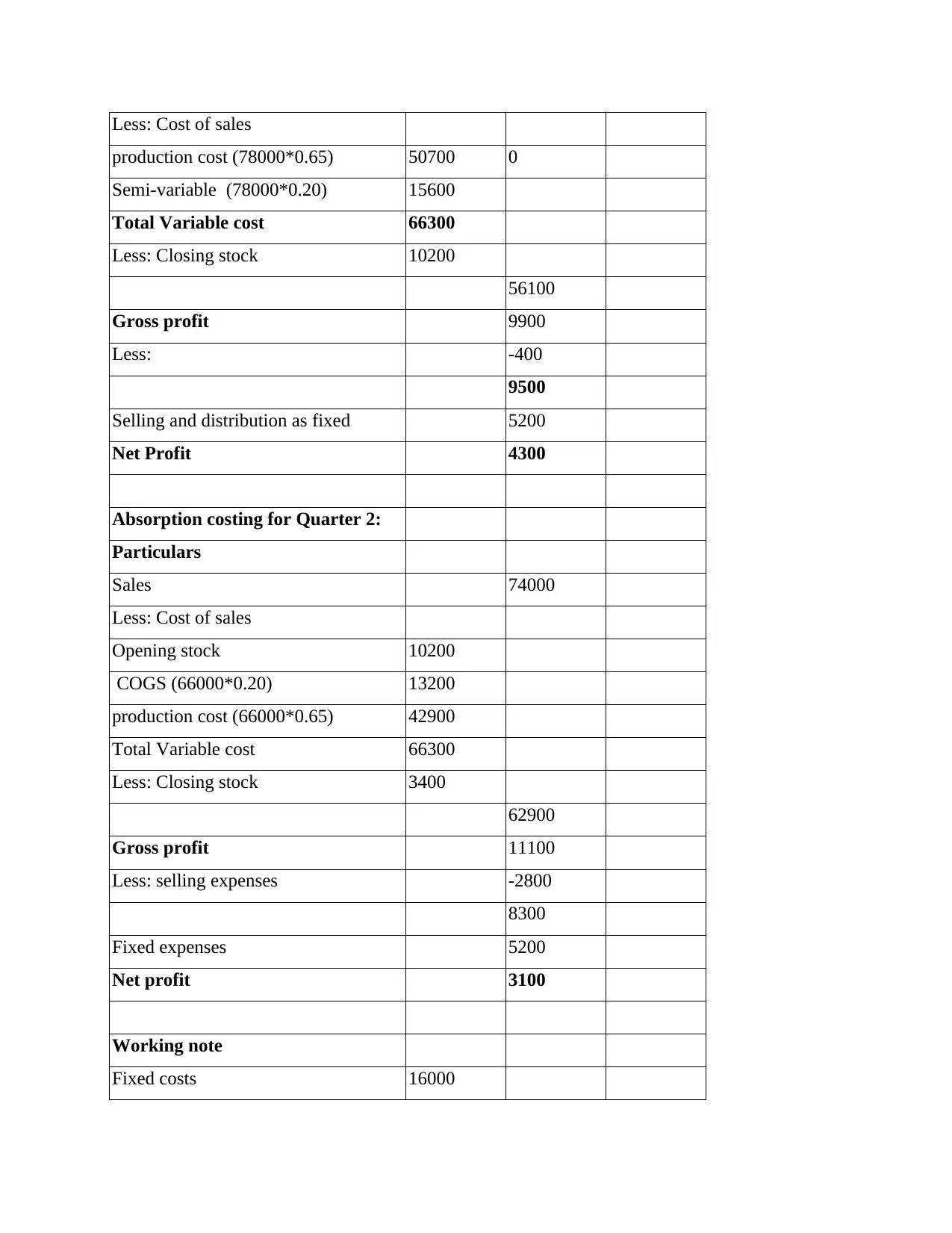

Absorption costing for Quarter 1:

Particulars

Amount (in

£)

Sales 66000

Particulars

Amount (in

£)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for Quarter 1:

Particulars

Amount (in

£)

Sales 66000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

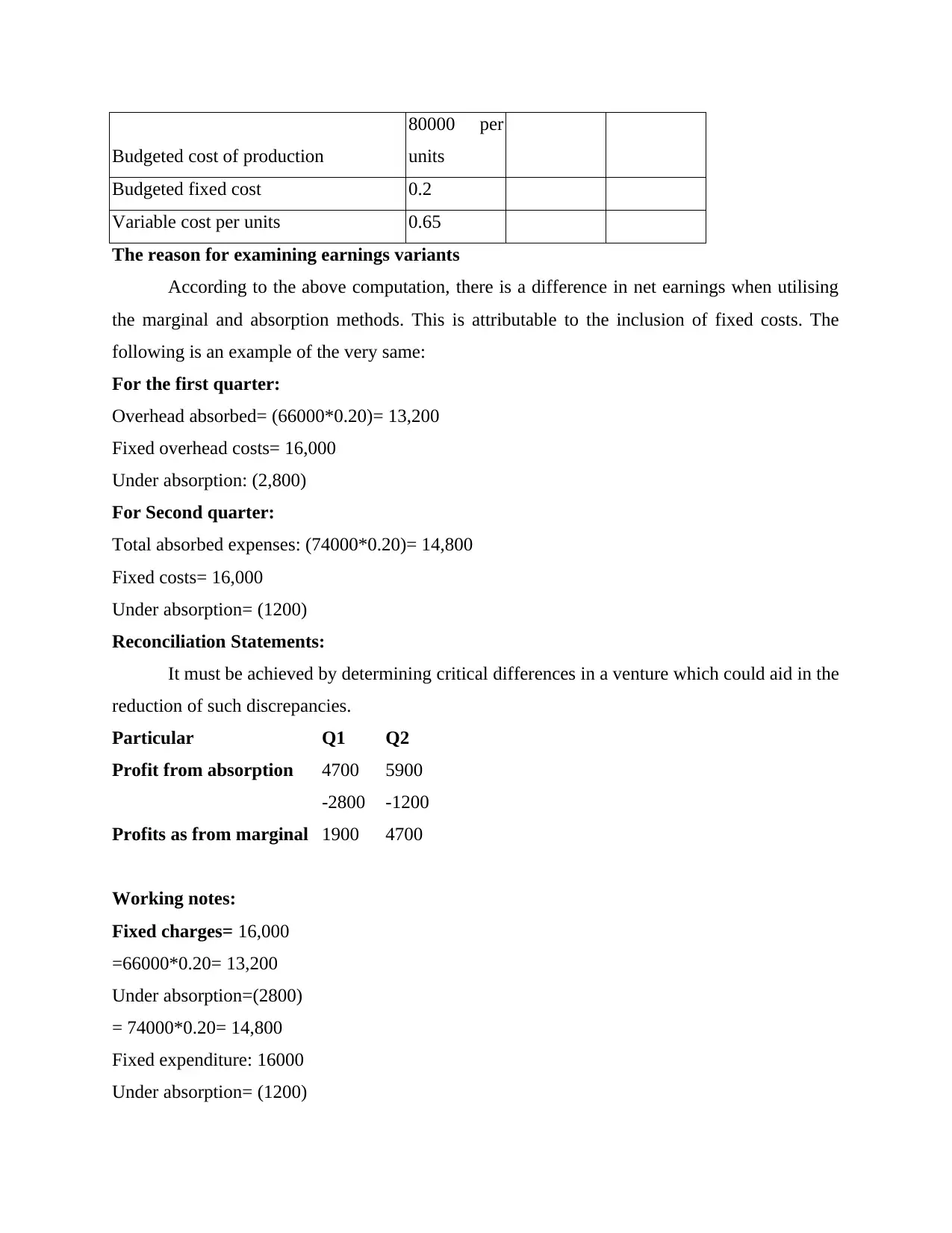

Fixed costs 16000

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

The reason for examining earnings variants

According to the above computation, there is a difference in net earnings when utilising

the marginal and absorption methods. This is attributable to the inclusion of fixed costs. The

following is an example of the very same:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

Fixed costs= 16,000

Under absorption= (1200)

Reconciliation Statements:

It must be achieved by determining critical differences in a venture which could aid in the

reduction of such discrepancies.

Particular Q1 Q2

Profit from absorption 4700 5900

-2800 -1200

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

The reason for examining earnings variants

According to the above computation, there is a difference in net earnings when utilising

the marginal and absorption methods. This is attributable to the inclusion of fixed costs. The

following is an example of the very same:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

Fixed costs= 16,000

Under absorption= (1200)

Reconciliation Statements:

It must be achieved by determining critical differences in a venture which could aid in the

reduction of such discrepancies.

Particular Q1 Q2

Profit from absorption 4700 5900

-2800 -1200

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.