ACC204 Financial Accounting: Depreciation, Impairment Loss Analysis

VerifiedAdded on 2023/06/12

|8

|1318

|341

Report

AI Summary

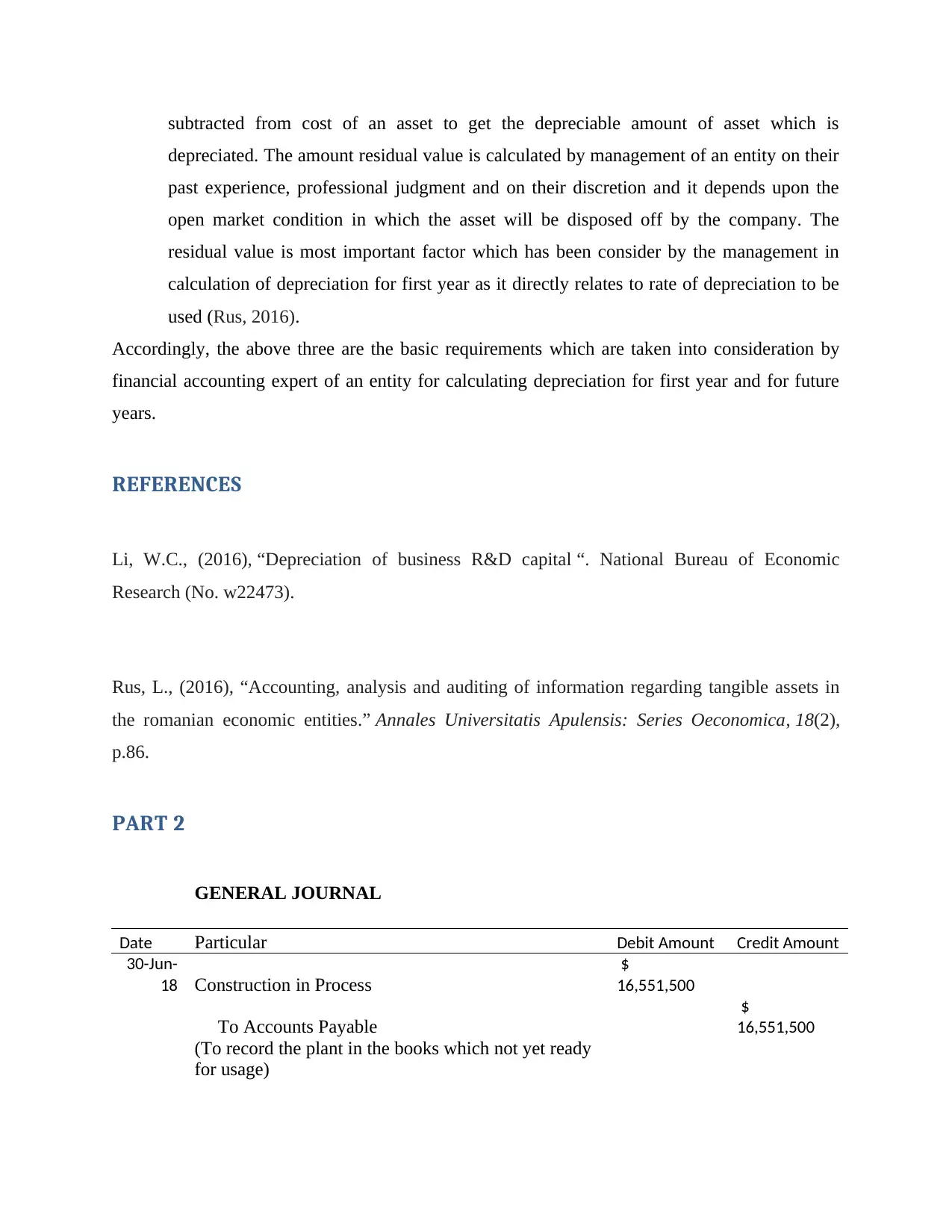

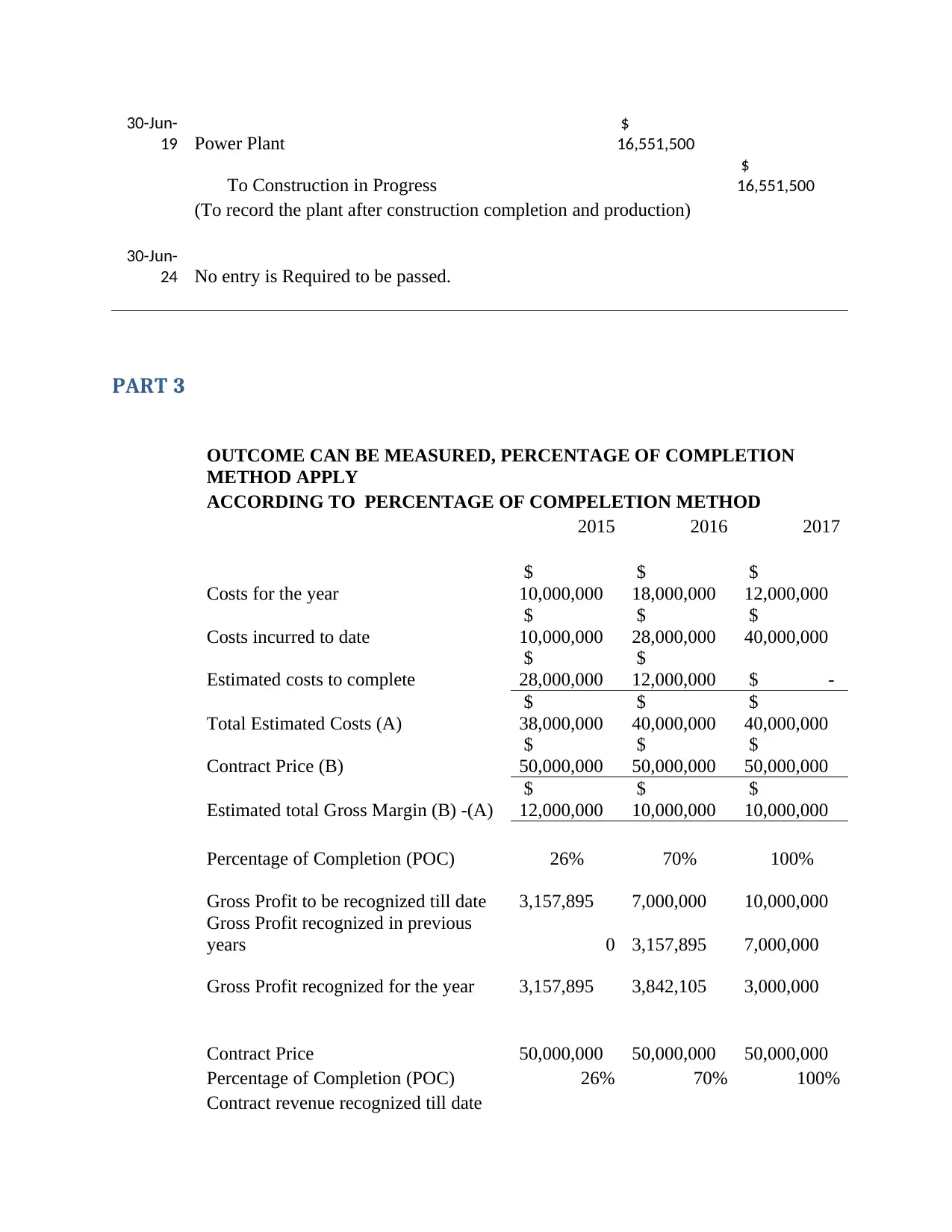

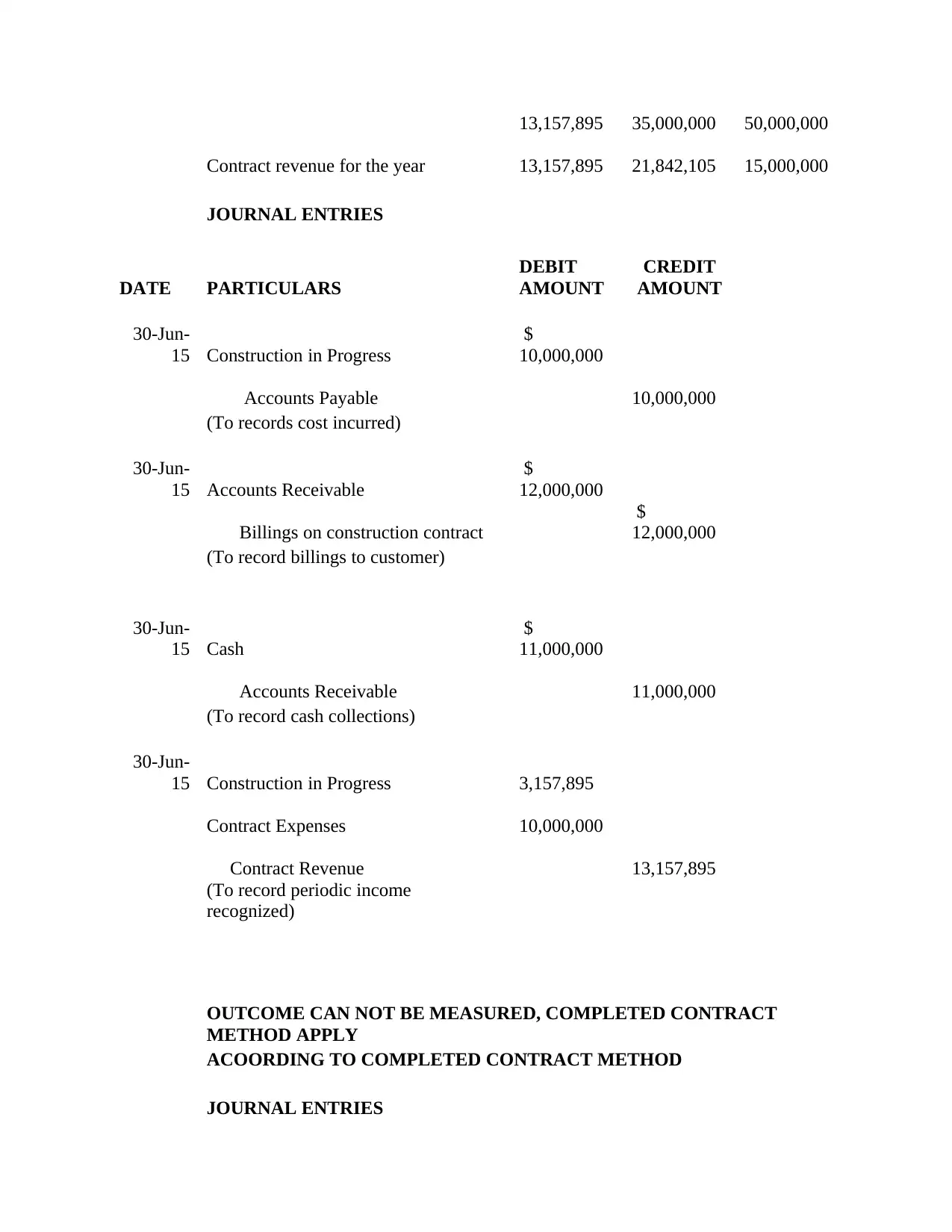

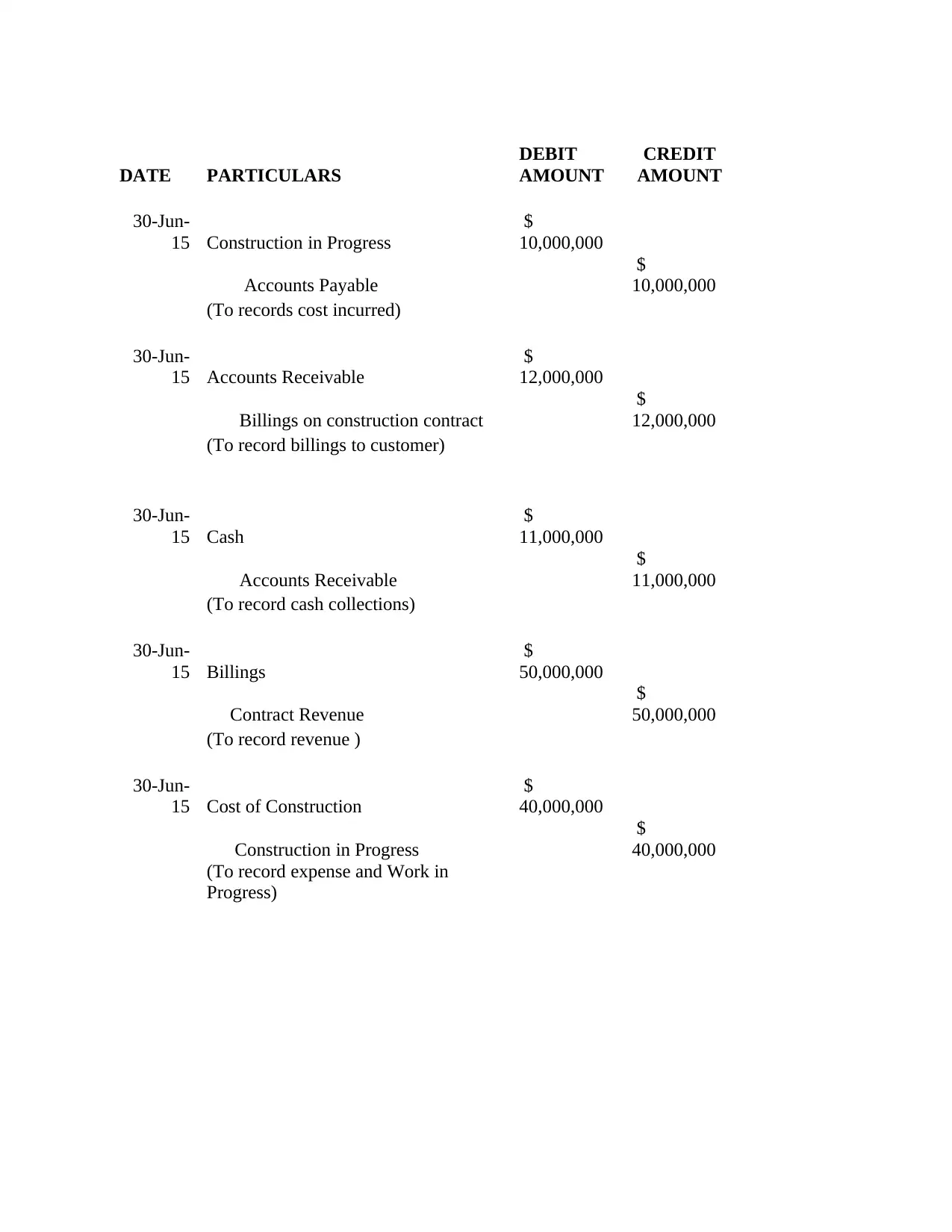

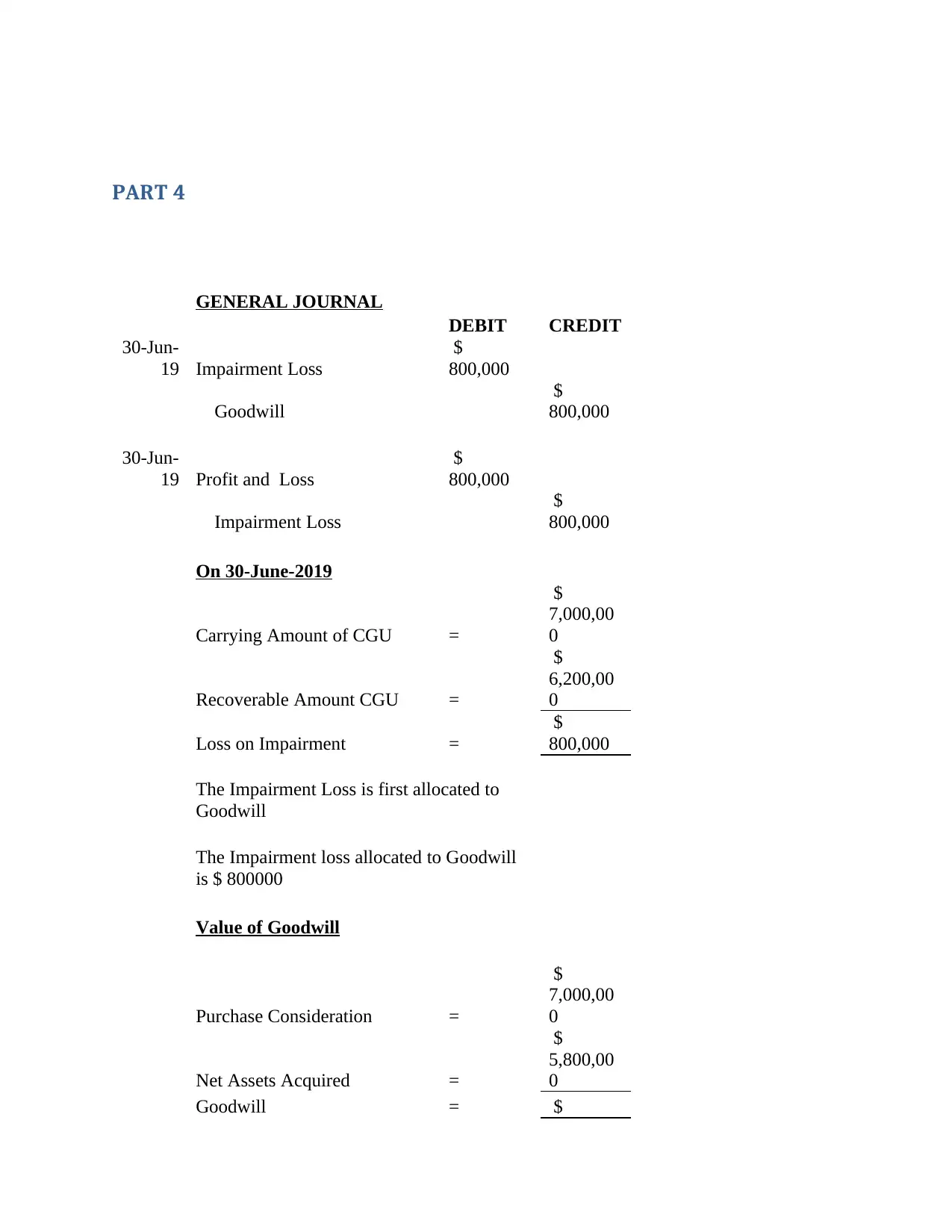

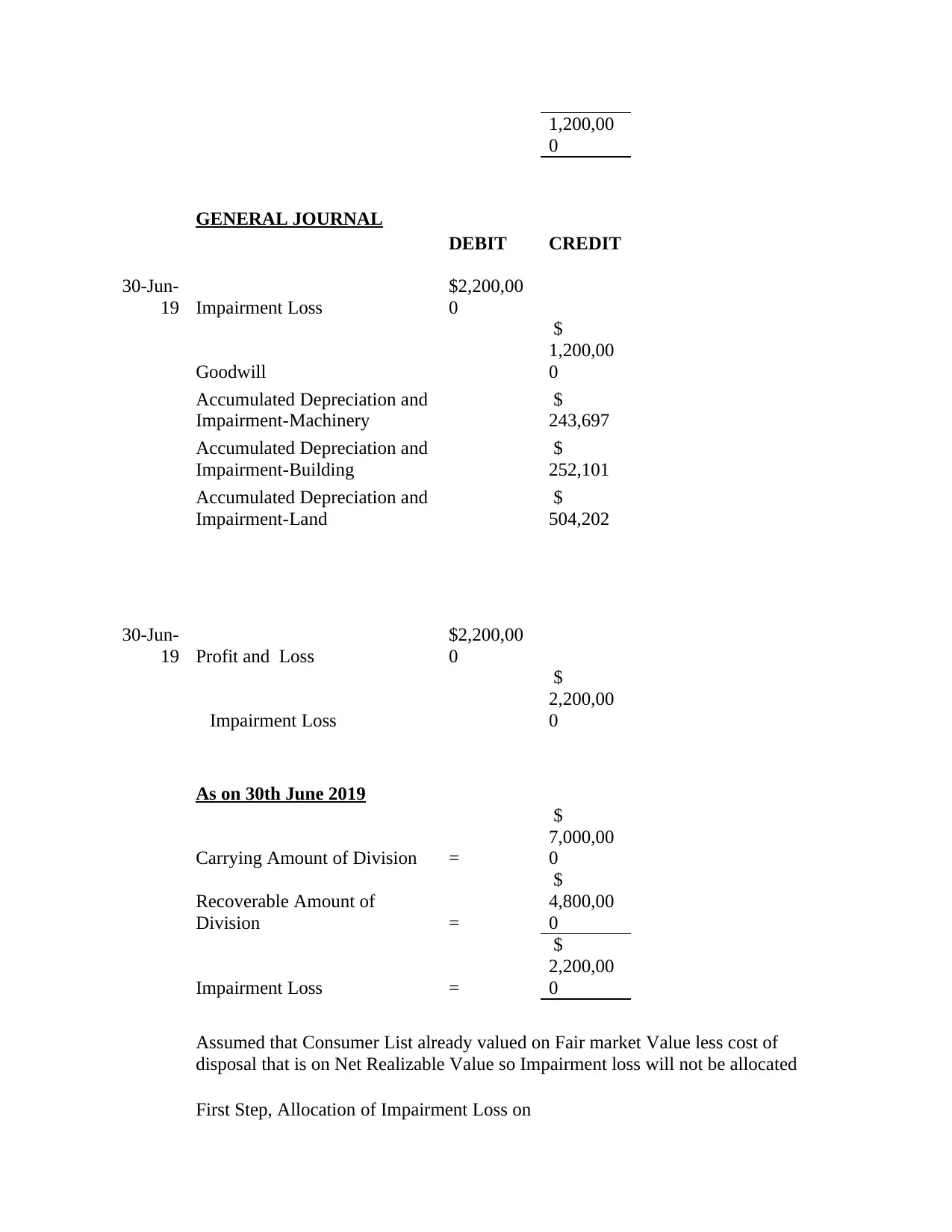

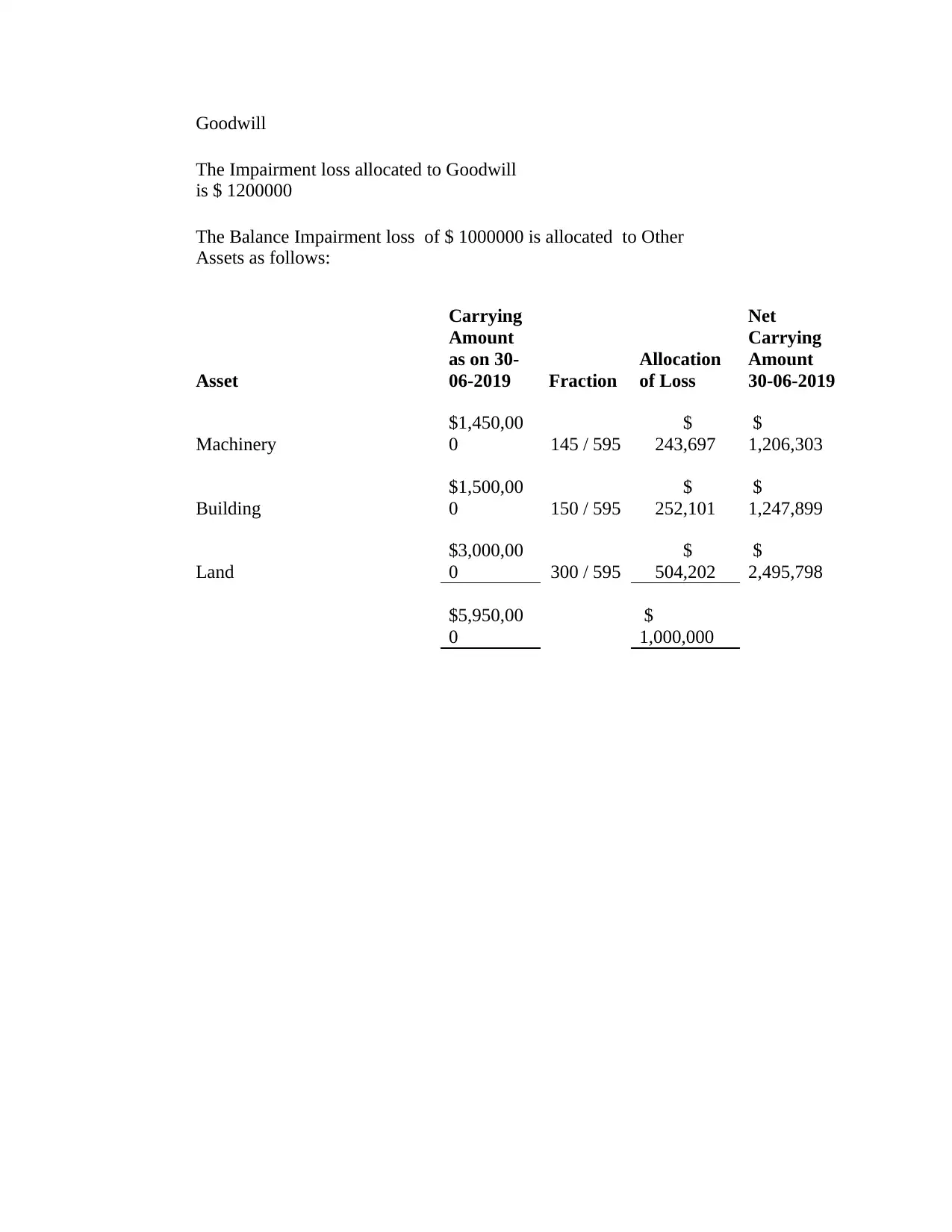

This assignment solution covers key aspects of financial accounting, including depreciation calculation, journal entries, and impairment loss analysis. Part 1 discusses the information needed to determine depreciation for the first year of an asset's life, referencing AASB 116. Part 2 provides general journal entries related to the construction of a power plant. Part 3 applies both the percentage of completion and completed contract methods for revenue recognition in construction contracts, including journal entries for each method. Finally, Part 4 addresses impairment loss on goodwill and other assets, demonstrating the allocation of impairment losses and providing relevant journal entries. The assignment uses specific examples and calculations to illustrate these concepts.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.