ACC518 - Financial Accounting: Issues and Development in Accounting

VerifiedAdded on 2023/06/04

|17

|3935

|108

Report

AI Summary

This report delves into current accounting issues and developments, focusing on auditing failures in large companies as highlighted in a Global Finance article. It links these issues to accounting theories, particularly measurement, normative accounting, and standard setting theories. The report examines the impact of issues like KPMG's fraud scandal, Carillion's collapse, and challenges related to fair value measurement standards. It also analyzes comments from Deloitte, IAS Plus, RSM, and KPMG on the upcoming accounting standard update 2018-13. The report concludes that while IFRS has developed accounting principles, their inconsistent application leads to fraud. Desklib provides students access to similar solved assignments and past papers for enhanced learning.

Accounting Issues 1

Current Development in Accounting

Current Development in Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Issues 2

Introduction

The main purpose of this report is to demonstrate the accounting issues in the management of

accounting system of companies which are headed under the accounting standards and

reporting system. The report is developed over an accounting issue based news article in

which the news article of Global Finance is assessed that discusses about the accounting

issues as audit failure in the large scale companies. Along with this, the determined

accounting and auditing issues are linked with the theories and explanation. Moreover, the

concluding significance of accounting is also elaborated with reference to the identified

accounting problems.

Introduction

The main purpose of this report is to demonstrate the accounting issues in the management of

accounting system of companies which are headed under the accounting standards and

reporting system. The report is developed over an accounting issue based news article in

which the news article of Global Finance is assessed that discusses about the accounting

issues as audit failure in the large scale companies. Along with this, the determined

accounting and auditing issues are linked with the theories and explanation. Moreover, the

concluding significance of accounting is also elaborated with reference to the identified

accounting problems.

Accounting Issues 3

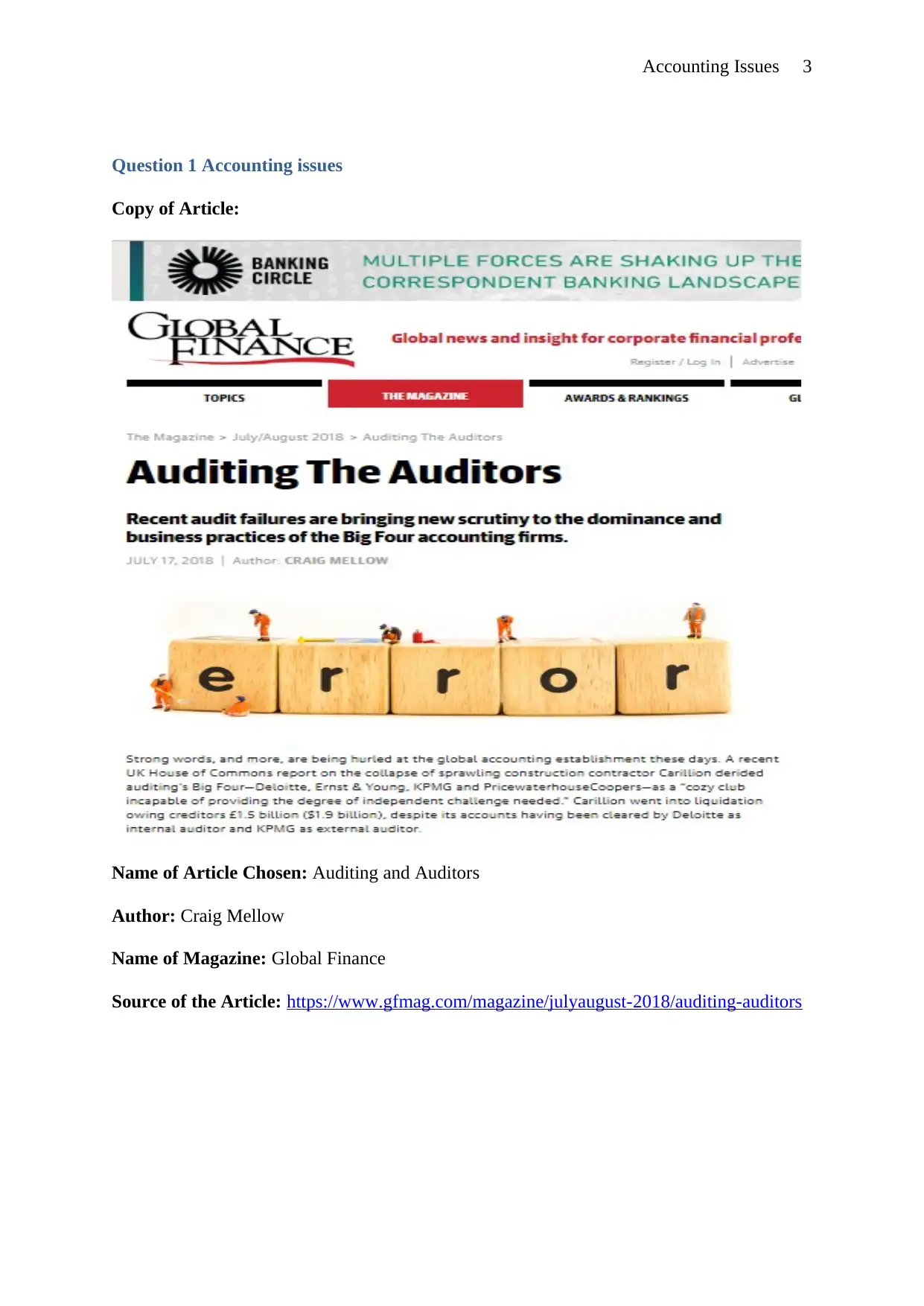

Question 1 Accounting issues

Copy of Article:

Name of Article Chosen: Auditing and Auditors

Author: Craig Mellow

Name of Magazine: Global Finance

Source of the Article: https://www.gfmag.com/magazine/julyaugust-2018/auditing-auditors

Question 1 Accounting issues

Copy of Article:

Name of Article Chosen: Auditing and Auditors

Author: Craig Mellow

Name of Magazine: Global Finance

Source of the Article: https://www.gfmag.com/magazine/julyaugust-2018/auditing-auditors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Issues 4

Discussion about the article:

The Global Finance has published the news about the auditing and accounting failure which

has resulted into the new scrutiny of business practices for big accounting firms. Craig

Mellow has presented the information about the falsification of accounting and auditing.

From the review of article, it is determined that the UK house presented a report on the

collapse of Carillion which has got into the wind up of its business practices. The main

reason behind the liquidity was due to the creditors as the creditors own the amount as £1.5

billion ($1.9 billion) from the accounting operations. In this article, the issue of auditors for

company to retain the accounting for a century as General Insurance Company and the results

obtained as $15billion charge (MELLOW, 2018).

In addition to this, the issue of eliciting the confidential information from the six partners of

KPMG plc is also came into the light. In a report, the partners of KPMG were founded a

fraud for detecting the confidential information so the issue for KPMG has also up shored

and shareholders do not want to keep the KPMG as auditor for the Company. Moreover, the

PWC plc has also face the issue of detecting the fraud of $2.3 billion in Alabama-based bank

but it was not successful so the Pwc plc bears the loss due to the damage. The whole

insurance reserves for the company have created a problem about reporting the information.

Apart from this, the KPMG has also face the issue of having relationship with the Gupta

family of South Africa and the family was also close to the president of Jacob Zuma.

Moreover, the author has also described the frauds and scam and related provisions in the

accounting and auditing. In relation to the discretion about the KPMG Company, it is also

assessed that the company has also employed the junior auditor so the accounting firm can

face the challenges from its typical competitor (Basak, Chiglinskyand and Clough, 2018). In

addition to this, the author has also levied from 2002 Sarbanes-Oxley law which was brought

Discussion about the article:

The Global Finance has published the news about the auditing and accounting failure which

has resulted into the new scrutiny of business practices for big accounting firms. Craig

Mellow has presented the information about the falsification of accounting and auditing.

From the review of article, it is determined that the UK house presented a report on the

collapse of Carillion which has got into the wind up of its business practices. The main

reason behind the liquidity was due to the creditors as the creditors own the amount as £1.5

billion ($1.9 billion) from the accounting operations. In this article, the issue of auditors for

company to retain the accounting for a century as General Insurance Company and the results

obtained as $15billion charge (MELLOW, 2018).

In addition to this, the issue of eliciting the confidential information from the six partners of

KPMG plc is also came into the light. In a report, the partners of KPMG were founded a

fraud for detecting the confidential information so the issue for KPMG has also up shored

and shareholders do not want to keep the KPMG as auditor for the Company. Moreover, the

PWC plc has also face the issue of detecting the fraud of $2.3 billion in Alabama-based bank

but it was not successful so the Pwc plc bears the loss due to the damage. The whole

insurance reserves for the company have created a problem about reporting the information.

Apart from this, the KPMG has also face the issue of having relationship with the Gupta

family of South Africa and the family was also close to the president of Jacob Zuma.

Moreover, the author has also described the frauds and scam and related provisions in the

accounting and auditing. In relation to the discretion about the KPMG Company, it is also

assessed that the company has also employed the junior auditor so the accounting firm can

face the challenges from its typical competitor (Basak, Chiglinskyand and Clough, 2018). In

addition to this, the author has also levied from 2002 Sarbanes-Oxley law which was brought

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Issues 5

into the existence for the purpose of responding or taking actions towards the control of

scandals in the accounting and auditing management. At the same time, the new article also

entails about the accounting fraud of Enron and WorldCom. Over the analysis, the issue of

Brexit is also evaluated as how the company can remain the auditors after leaving the

European Union by UK. Moreover, the issue of fully disclosing the information is also raised

by the Marks and Spencer which is a corporate governance leader in the perspective market.

It is stated that the report stated that the Marks and Spencer also denoted the difference in

between disclosing the information more as compare to the annual report providers

(Tinkelman, 2015). Along with this, the issues related to the policies for goodwill and

allowance for doubtful debts is also crucial information for the company to present the

information in professional manner. Apart from this, the author has also stated that the

companies can create the environment in which the subordinates can raise the issue against

their senior management so that the business can become like the Carillion and General

Electric’s. Due to the above issues, the market position of KPMG, PWC, Deloitte, and Ernst

& Young has impacted and the share price of KPMG plc has decreased in a day so these

types of accounting issues can be challenging for firms and accounting standards (Zyla,

2012).

Linkage of issues with ACC518 theories

The accounting standards are developed for the improvement of accounting theories which is

concerned to the foundation of accounting system and procedure as per the required changes

by the regulatory framework which is focused on reporting the financial statement of entity.

In relation to the ACC518 which is related to the current development in the accounting

theories and framework.

The major accounting theories are assessed as the measurement of accounting theory and

measurement is one the crucial issue in the accounting (Weirich, Churyk and Pearson, 2012).

into the existence for the purpose of responding or taking actions towards the control of

scandals in the accounting and auditing management. At the same time, the new article also

entails about the accounting fraud of Enron and WorldCom. Over the analysis, the issue of

Brexit is also evaluated as how the company can remain the auditors after leaving the

European Union by UK. Moreover, the issue of fully disclosing the information is also raised

by the Marks and Spencer which is a corporate governance leader in the perspective market.

It is stated that the report stated that the Marks and Spencer also denoted the difference in

between disclosing the information more as compare to the annual report providers

(Tinkelman, 2015). Along with this, the issues related to the policies for goodwill and

allowance for doubtful debts is also crucial information for the company to present the

information in professional manner. Apart from this, the author has also stated that the

companies can create the environment in which the subordinates can raise the issue against

their senior management so that the business can become like the Carillion and General

Electric’s. Due to the above issues, the market position of KPMG, PWC, Deloitte, and Ernst

& Young has impacted and the share price of KPMG plc has decreased in a day so these

types of accounting issues can be challenging for firms and accounting standards (Zyla,

2012).

Linkage of issues with ACC518 theories

The accounting standards are developed for the improvement of accounting theories which is

concerned to the foundation of accounting system and procedure as per the required changes

by the regulatory framework which is focused on reporting the financial statement of entity.

In relation to the ACC518 which is related to the current development in the accounting

theories and framework.

The major accounting theories are assessed as the measurement of accounting theory and

measurement is one the crucial issue in the accounting (Weirich, Churyk and Pearson, 2012).

Accounting Issues 6

This theory is concerned to the measurability concept in which the transactions are included

which can be recognized in financial statement. Along with this, the normative accounting

theory is also related to the measurement principle that is related to the bases of measurement

as historical cost and fair value. On the other hand, the standard setting theory is concerned to

the accounting theory in which the security board has assigned the FASB to setting the

standards about the accounting standards (McLeay and Riccaboni, 2012). The international

accounting standards are replaced by the International financial reporting standard which is

engaged into providing the standard at global level so that the accounting language for

company can easily be compared with other companies. It is also revealed that the totally

mitigation of accounting issue are not possible because the accounting standards are

developed and initiated by the IFRS in order to manage the accounting procedure but all the

accounting activities are done according to principles of accounting with fairness.

From the assessment and link of accounting theories with the issues identified in news article

are determined as in this article, it is identified that the KPMG plc is facing the issues for

having continuous relationship with the firm to provide the accounting and auditing support

but the reviews and fraud by the partners of KPMG has resulted into the adverse impact over

the firm and the firm might not remain continue with the Carillion. In relation to this, there

are many companies which are failed due to the reason of lacking in fund management,

unethical practices but the other or partner entity might not be affected.

As per the issue of confidential information by the partners of KPMG is also not fair

according to the international standards because it might influence the creditworthiness of

firm in the perspective market and the IFRS can oblige who is subjected to spread the

confidential information. On the other hand, the issue of KPMG is also related to the standard

setting by the IFRS as if the partners of company are fraud it does not mean that the potent

entity is also fraud. With relation to this, the issue of wind up of construction contractor as

This theory is concerned to the measurability concept in which the transactions are included

which can be recognized in financial statement. Along with this, the normative accounting

theory is also related to the measurement principle that is related to the bases of measurement

as historical cost and fair value. On the other hand, the standard setting theory is concerned to

the accounting theory in which the security board has assigned the FASB to setting the

standards about the accounting standards (McLeay and Riccaboni, 2012). The international

accounting standards are replaced by the International financial reporting standard which is

engaged into providing the standard at global level so that the accounting language for

company can easily be compared with other companies. It is also revealed that the totally

mitigation of accounting issue are not possible because the accounting standards are

developed and initiated by the IFRS in order to manage the accounting procedure but all the

accounting activities are done according to principles of accounting with fairness.

From the assessment and link of accounting theories with the issues identified in news article

are determined as in this article, it is identified that the KPMG plc is facing the issues for

having continuous relationship with the firm to provide the accounting and auditing support

but the reviews and fraud by the partners of KPMG has resulted into the adverse impact over

the firm and the firm might not remain continue with the Carillion. In relation to this, there

are many companies which are failed due to the reason of lacking in fund management,

unethical practices but the other or partner entity might not be affected.

As per the issue of confidential information by the partners of KPMG is also not fair

according to the international standards because it might influence the creditworthiness of

firm in the perspective market and the IFRS can oblige who is subjected to spread the

confidential information. On the other hand, the issue of KPMG is also related to the standard

setting by the IFRS as if the partners of company are fraud it does not mean that the potent

entity is also fraud. With relation to this, the issue of wind up of construction contractor as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Issues 7

Carillion is also happened due to the creditors as $1.9 billion has credit over the company

(Conway and Byrne, 2018). In context to this, the company has also derided by the lacking of

measuring the value for its credit but the company has not measure and report about its credit

so it was not successful to manage in timely manner. Moreover, it is also detained that the

companies have not followed the ethical standards according to the IFRS that’s why the GE

is reported for charge against having the KPMG as auditor for its financial reporting

(MOHAPATRA, 2012). Further, the development of accounting theory has also resulted into

the identification of frauds and it can be controlled by the law of 2002 Sarbanes-Oxley law

which is a public company accounting reform in the accounting standards for mitigating the

frauds.

In context of assumptions of financial accounting information, it can be assumed that the

financial reporting information is useful for using the theories and implications of

international standards for improving the accounting theorem for future development. On the

other hand, it is also assumed about the in-depth understanding of accounting theories due to

the relationship of measurement, normative theory and standards setting process with the

international accounting system for its usefulness. It can also be assumed about the

possibilities of IFRS system to be followed by all the international companies in ethical

manner.

Conclusion

From the above analysis of news article, it can be stated that the theories and accounting

principles have been developed by the IFRS but it’s not following in proper manner so the

frauds in account take place. It can also be concluded that there are many issue which have

been found out as measuring the value for credit, unethical practices and eliciting the

confidential information. Moreover, it can also be summarized that the following accounting

standards are important for the companies under the standard setting process of international

Carillion is also happened due to the creditors as $1.9 billion has credit over the company

(Conway and Byrne, 2018). In context to this, the company has also derided by the lacking of

measuring the value for its credit but the company has not measure and report about its credit

so it was not successful to manage in timely manner. Moreover, it is also detained that the

companies have not followed the ethical standards according to the IFRS that’s why the GE

is reported for charge against having the KPMG as auditor for its financial reporting

(MOHAPATRA, 2012). Further, the development of accounting theory has also resulted into

the identification of frauds and it can be controlled by the law of 2002 Sarbanes-Oxley law

which is a public company accounting reform in the accounting standards for mitigating the

frauds.

In context of assumptions of financial accounting information, it can be assumed that the

financial reporting information is useful for using the theories and implications of

international standards for improving the accounting theorem for future development. On the

other hand, it is also assumed about the in-depth understanding of accounting theories due to

the relationship of measurement, normative theory and standards setting process with the

international accounting system for its usefulness. It can also be assumed about the

possibilities of IFRS system to be followed by all the international companies in ethical

manner.

Conclusion

From the above analysis of news article, it can be stated that the theories and accounting

principles have been developed by the IFRS but it’s not following in proper manner so the

frauds in account take place. It can also be concluded that there are many issue which have

been found out as measuring the value for credit, unethical practices and eliciting the

confidential information. Moreover, it can also be summarized that the following accounting

standards are important for the companies under the standard setting process of international

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Issues 8

accounting so that the ethical practices of accounting can be accomplished in efficient

manner.

accounting so that the ethical practices of accounting can be accomplished in efficient

manner.

Accounting Issues 9

Question 2

Introduction

The purpose of the report is to address the views and opinions of the different companies in

regard to an upcoming standard of accounting in Australia. The standard of accounting

chosen to fulfill the purpose of the report is 2018-13 update which is for measurement of fair

value (TOPIC 820). The update is related to the changes in requirement of disclosure for the

measurement of the fair value. In context to this, comments from four companies are

addressed and discussed in the report. The comment letters of four different companies are

named as Deloitte, IAS Plus, RSM, and KPMG.

Upcoming standard of accounting

The proposed update for the standard of accounting: “Fair Value Measurement (TOPIC 820)”

It is the duty of FASB to launch drafts in order to create exposure for the proposal prior to the

implementation of any new standard of accounting in Australia (Watts and ZUO, 2016). The

organization’s major purpose is to identify the comments provided by the industry experts for

the common public for an overview in order to identify the shortcomings and accordingly

improve the IFRS for better disclosures and accounting. The draft report of FASB is in

relation with Fair Value Measurement (Topic 820). The exposure is important for the FASB

and the entities which are operating under the International Accounting Standards in fair

manner. On the other hand, the fair value measurement can also be supportive for reducing

the accounting issues and standards are also followed in positive manner.

The prime reason for making the updates in the policy of accounting is to enhance the

effectiveness in disclosure in the process of devising the financial statements and dispensing

notes for the same (Pijper, 2016). Clarity in communication about the relevant information is

facilitated through accounting policy in accordance with the GAAP. A framework for

Question 2

Introduction

The purpose of the report is to address the views and opinions of the different companies in

regard to an upcoming standard of accounting in Australia. The standard of accounting

chosen to fulfill the purpose of the report is 2018-13 update which is for measurement of fair

value (TOPIC 820). The update is related to the changes in requirement of disclosure for the

measurement of the fair value. In context to this, comments from four companies are

addressed and discussed in the report. The comment letters of four different companies are

named as Deloitte, IAS Plus, RSM, and KPMG.

Upcoming standard of accounting

The proposed update for the standard of accounting: “Fair Value Measurement (TOPIC 820)”

It is the duty of FASB to launch drafts in order to create exposure for the proposal prior to the

implementation of any new standard of accounting in Australia (Watts and ZUO, 2016). The

organization’s major purpose is to identify the comments provided by the industry experts for

the common public for an overview in order to identify the shortcomings and accordingly

improve the IFRS for better disclosures and accounting. The draft report of FASB is in

relation with Fair Value Measurement (Topic 820). The exposure is important for the FASB

and the entities which are operating under the International Accounting Standards in fair

manner. On the other hand, the fair value measurement can also be supportive for reducing

the accounting issues and standards are also followed in positive manner.

The prime reason for making the updates in the policy of accounting is to enhance the

effectiveness in disclosure in the process of devising the financial statements and dispensing

notes for the same (Pijper, 2016). Clarity in communication about the relevant information is

facilitated through accounting policy in accordance with the GAAP. A framework for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Issues 10

development is included in it for promoting and maintaining the consistency in decisions

related to disclosures according to the requirement of the board. Secondly, the reporting

exercise shall appropriately exercise the carefulness. The changes in the accounting standards

are important in relation to the enhancing the reliability and transparency for using the

standards according to the international operations.

Various changes are lead by the framework for disclosure along with the amendments. The

entities enlisted under the GAAP are affected due to these changes and the disclosures are

required to be followed in relation to the non-recurring and recurring measurement of fair

value. It is not necessary for the non-public entities to implement and follow some of the

changes. Benefits and cost consideration are the vital changes which lead to the requirement

of disclosure removal. The amount in stage 1 and 2 as well as the reasons for the same were

removed from the command of fair value chain. The transfer policy between levels and

process of valuation under third level for carrying out the measurement of fair value is also

removed (Iselin and Nicoletti, 2017). Lastly, some of the requirements for non-public entities

were also removed which includes alterations in the gains and losses which are unrealized for

the included time in income in context of third stage measurement of fair value remained at

the period end.

The amendment encloses modifications which are a replacement for the FVM stage 3 which

is rolled forward. A non-public entity is required to disclose the transfer in context of the fair

value chain’s level 3. Moreover, the issue and purchase of the liabilities and assets also

requires same treatment. Likewise, the disclosure of net value of the assets is required by

some entities when the investee’s assets are liquidated and investment is concerned (Martins

and Taborda, 2017). The liquidating assets at the time of restriction from preservation may be

lowered if the timing is communicated by the investee publicly. The last amendment for the

development is included in it for promoting and maintaining the consistency in decisions

related to disclosures according to the requirement of the board. Secondly, the reporting

exercise shall appropriately exercise the carefulness. The changes in the accounting standards

are important in relation to the enhancing the reliability and transparency for using the

standards according to the international operations.

Various changes are lead by the framework for disclosure along with the amendments. The

entities enlisted under the GAAP are affected due to these changes and the disclosures are

required to be followed in relation to the non-recurring and recurring measurement of fair

value. It is not necessary for the non-public entities to implement and follow some of the

changes. Benefits and cost consideration are the vital changes which lead to the requirement

of disclosure removal. The amount in stage 1 and 2 as well as the reasons for the same were

removed from the command of fair value chain. The transfer policy between levels and

process of valuation under third level for carrying out the measurement of fair value is also

removed (Iselin and Nicoletti, 2017). Lastly, some of the requirements for non-public entities

were also removed which includes alterations in the gains and losses which are unrealized for

the included time in income in context of third stage measurement of fair value remained at

the period end.

The amendment encloses modifications which are a replacement for the FVM stage 3 which

is rolled forward. A non-public entity is required to disclose the transfer in context of the fair

value chain’s level 3. Moreover, the issue and purchase of the liabilities and assets also

requires same treatment. Likewise, the disclosure of net value of the assets is required by

some entities when the investee’s assets are liquidated and investment is concerned (Martins

and Taborda, 2017). The liquidating assets at the time of restriction from preservation may be

lowered if the timing is communicated by the investee publicly. The last amendment for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Issues 11

standard includes valuation of disclosure’s uncertainty so that the information related to

measurable uncertainty can be communicated at the date of reporting.

Certain addition is also there in the requirement of disclosure which the non-public entities

are not required to follow. The addition includes alterations in the losses and gains which are

unrealized and included in the level 3 income which is comprehensible. The weighted

average and range of the inputs which cannot be observed are required to be disclosed to a

certain level (DiMasi, Grabowski, and Hansen, 2016). With effect from 2020 the amendment

will become effective and shall be followed by all the entities. The application of approach

for valuation is categorized in three ways. The first is the market approach under which the

valuation is done in accordance with the price quoted in the market. Second is the income

approach under which the value is done for the amounts which will incur in future such as

income generated at present value and cash flows on the measurement date. The last is the

cost approach under which the valuation is done on certain amount which is required to be

replaced asset’s service capacity (Preiser, White, and Rabinowitz, 2015). The approach is

based on the fact that in order to purchase a substitute, an investor will never pay more than

its cost.

Comments from four different companies

Screenshots of comments from different companies

1. Deloitte

standard includes valuation of disclosure’s uncertainty so that the information related to

measurable uncertainty can be communicated at the date of reporting.

Certain addition is also there in the requirement of disclosure which the non-public entities

are not required to follow. The addition includes alterations in the losses and gains which are

unrealized and included in the level 3 income which is comprehensible. The weighted

average and range of the inputs which cannot be observed are required to be disclosed to a

certain level (DiMasi, Grabowski, and Hansen, 2016). With effect from 2020 the amendment

will become effective and shall be followed by all the entities. The application of approach

for valuation is categorized in three ways. The first is the market approach under which the

valuation is done in accordance with the price quoted in the market. Second is the income

approach under which the value is done for the amounts which will incur in future such as

income generated at present value and cash flows on the measurement date. The last is the

cost approach under which the valuation is done on certain amount which is required to be

replaced asset’s service capacity (Preiser, White, and Rabinowitz, 2015). The approach is

based on the fact that in order to purchase a substitute, an investor will never pay more than

its cost.

Comments from four different companies

Screenshots of comments from different companies

1. Deloitte

Accounting Issues 12

2. KMPG

3. RSM

2. KMPG

3. RSM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.