Financial Reporting Developments Report

VerifiedAdded on 2020/03/07

|9

|1406

|86

Report

AI Summary

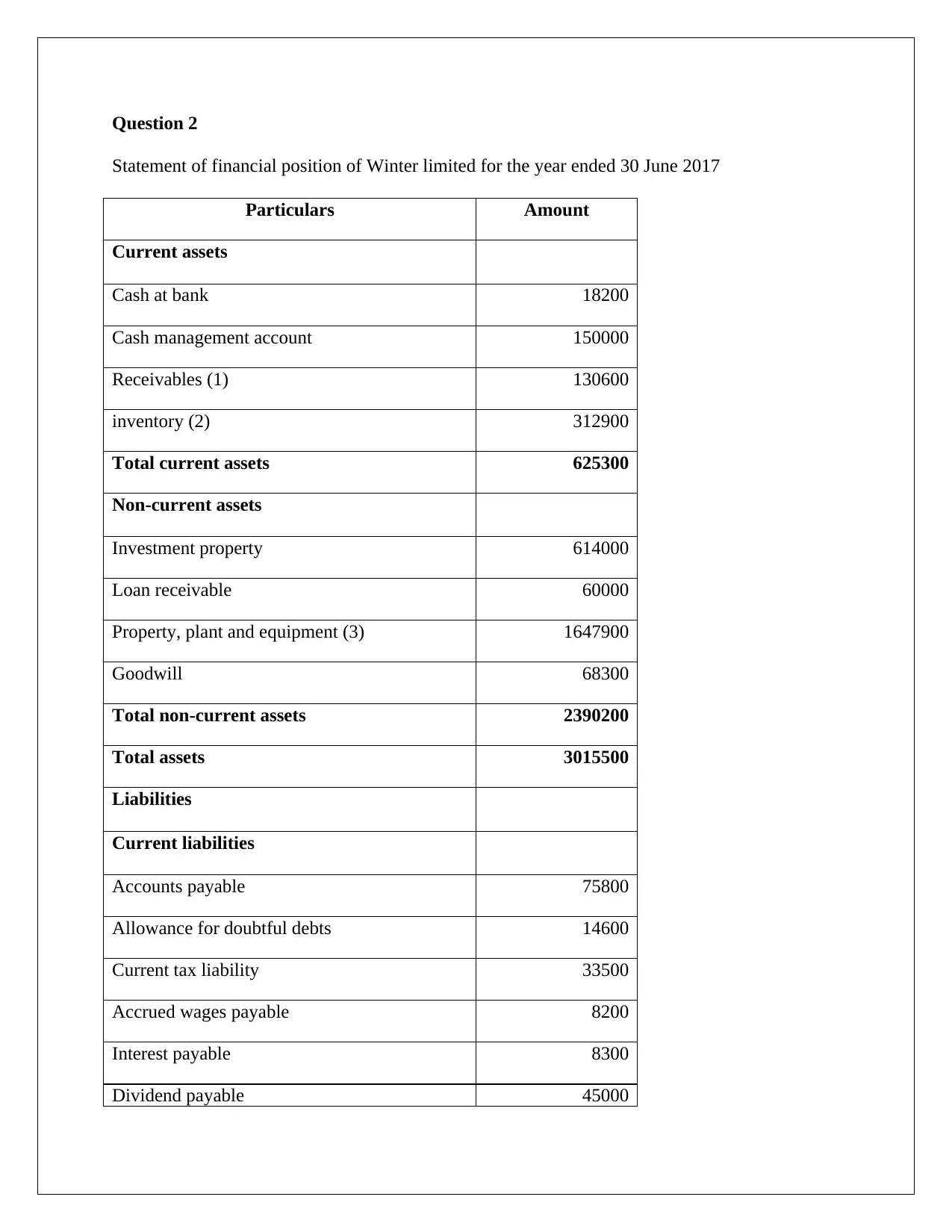

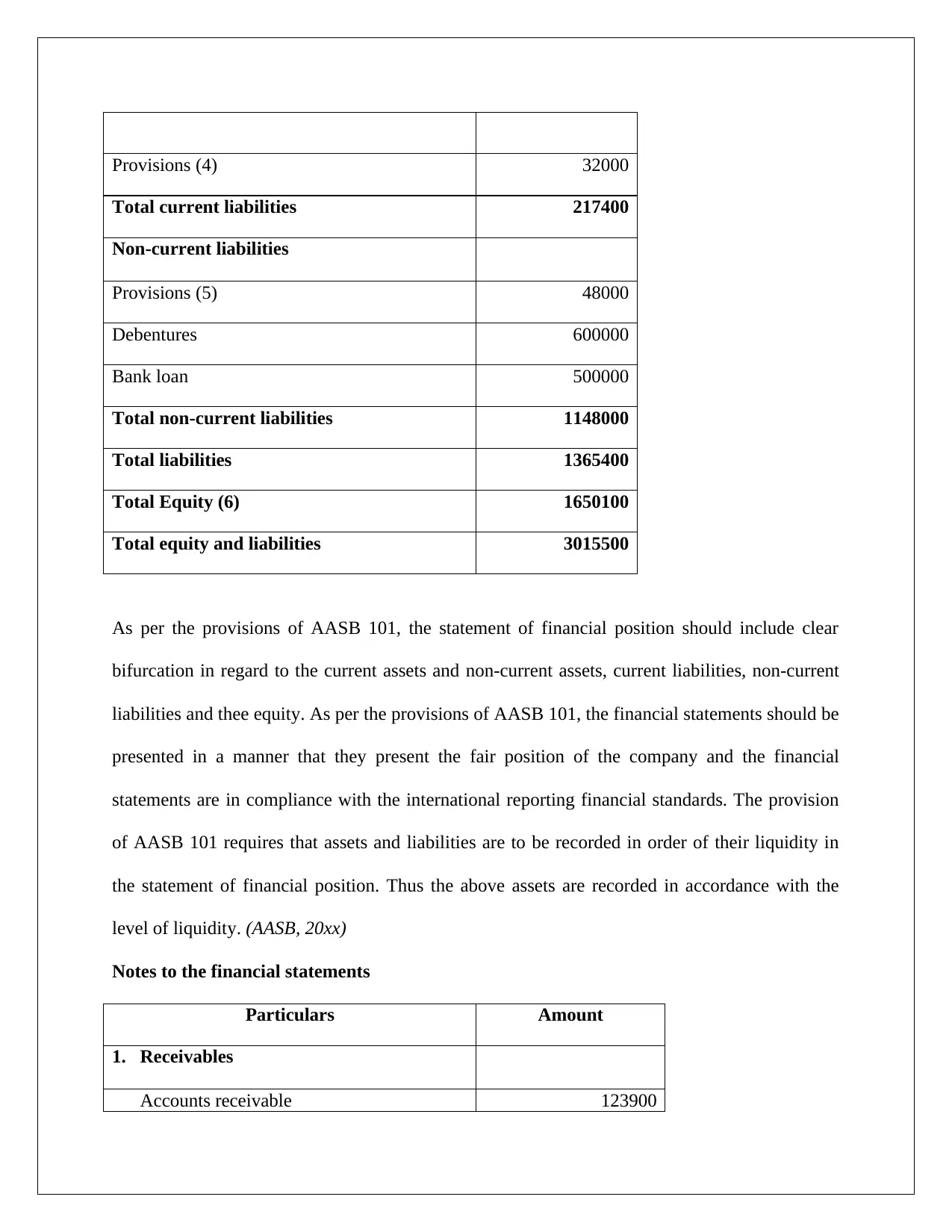

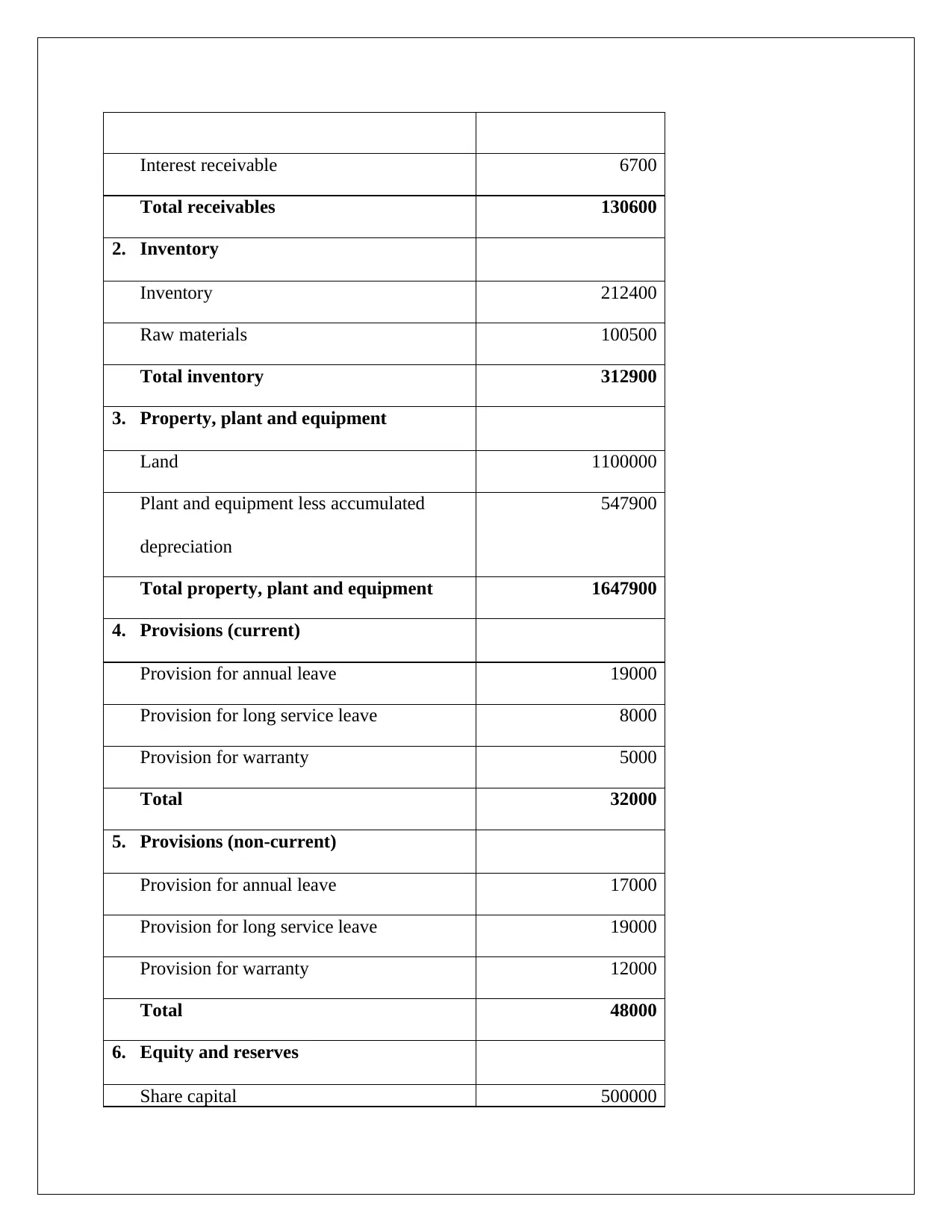

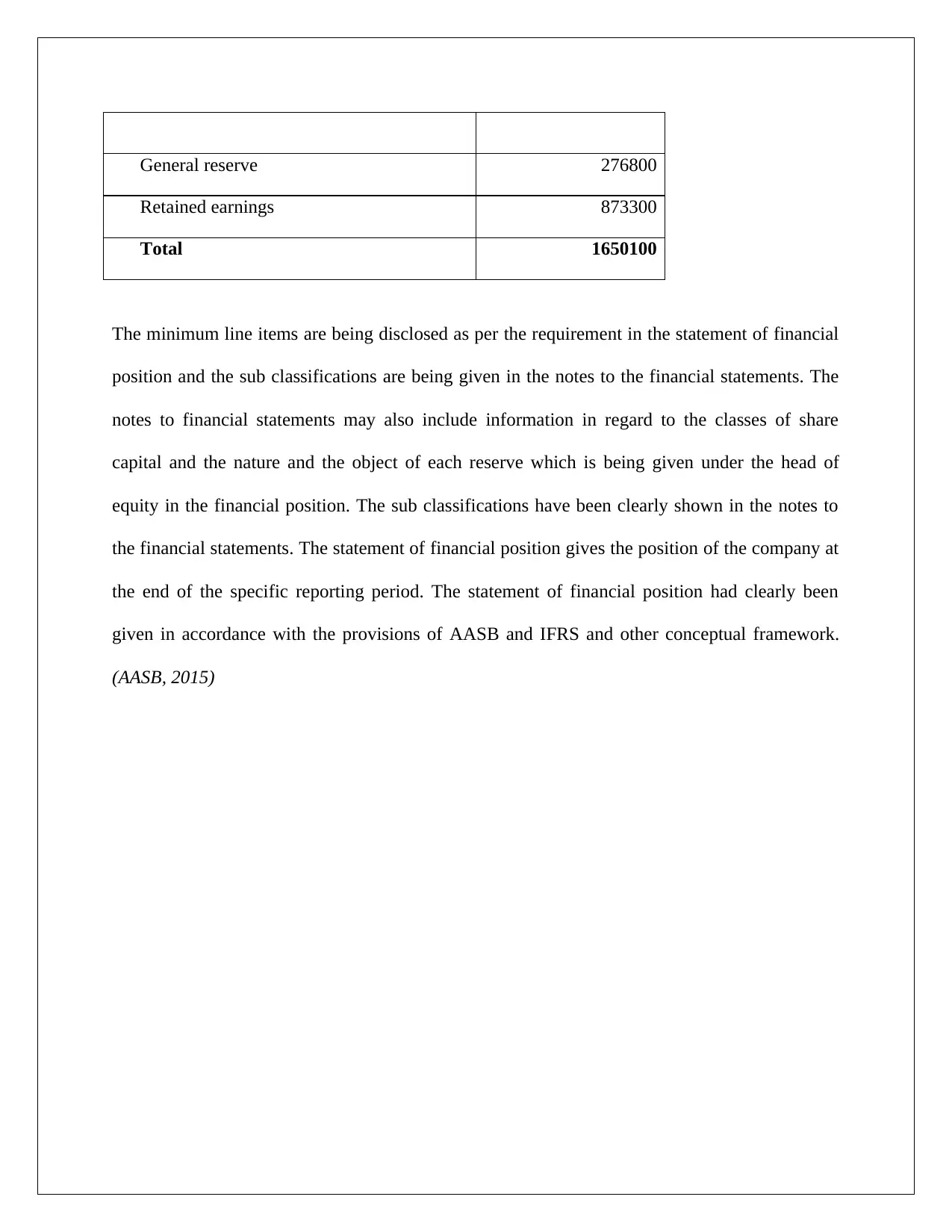

This report outlines significant changes and developments in the financial reporting environment from May to August 2017. It covers updates from various accounting standards boards, including IFRS 13, IAS 16, and AASB interpretations. The report emphasizes the importance of compliance with international financial reporting standards and highlights the ongoing convergence efforts between IASB and FASB. Additionally, it includes a detailed statement of financial position for Winter Limited, showcasing current and non-current assets, liabilities, and equity, along with notes that provide further clarification on financial items.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.