Corporate and Financial Reporting: Equity and Debt Analysis Report

VerifiedAdded on 2023/06/05

|32

|4583

|319

Report

AI Summary

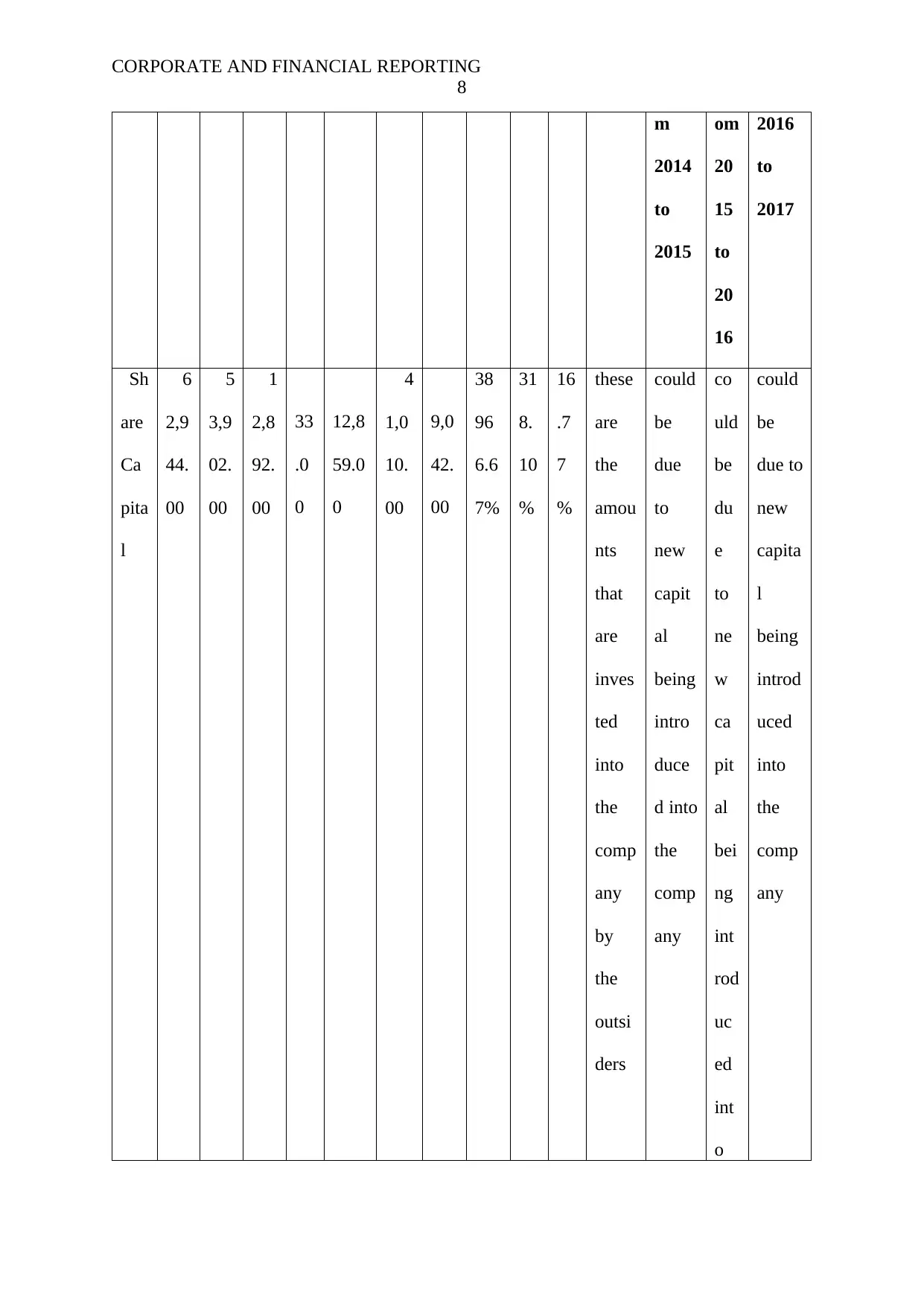

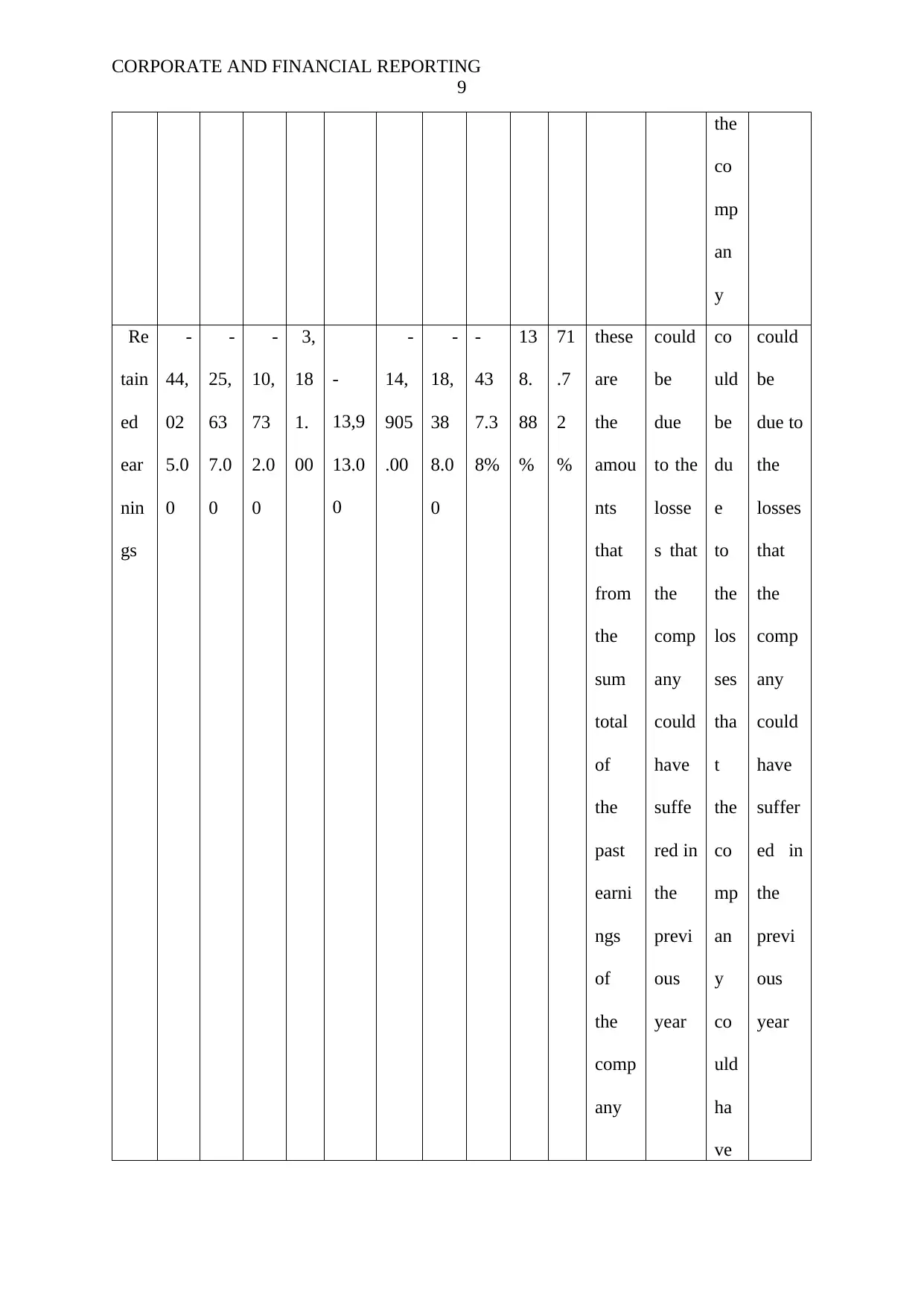

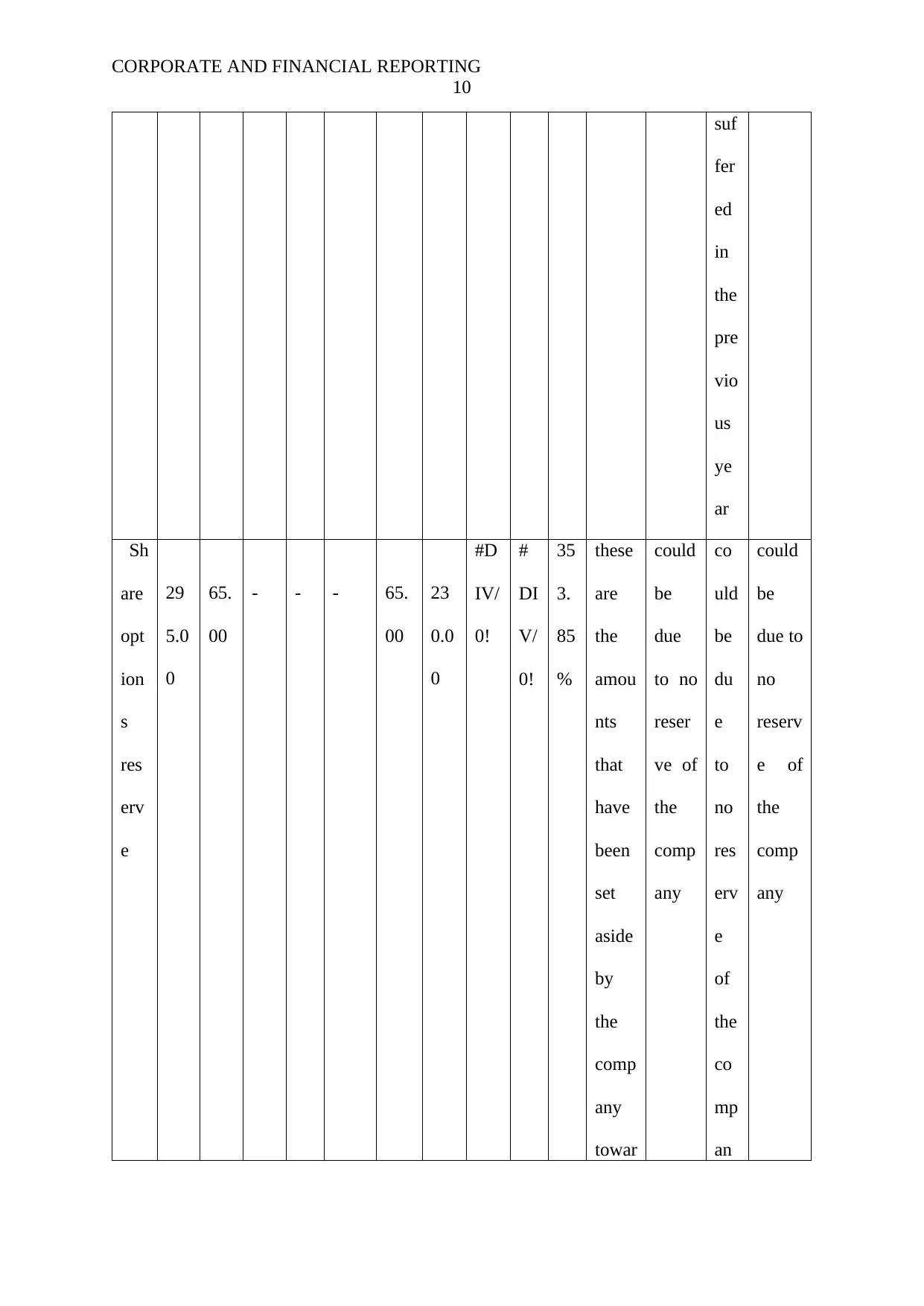

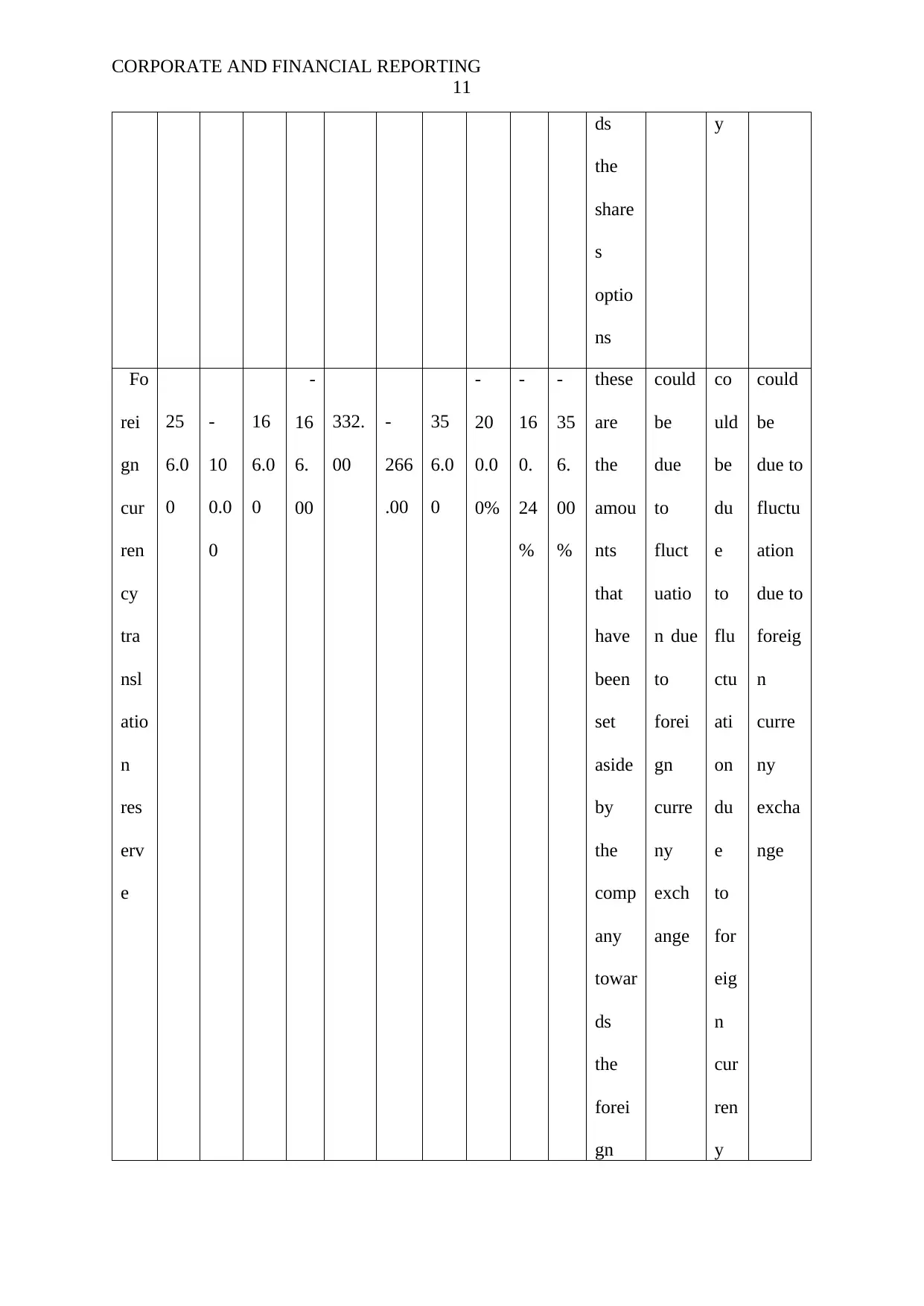

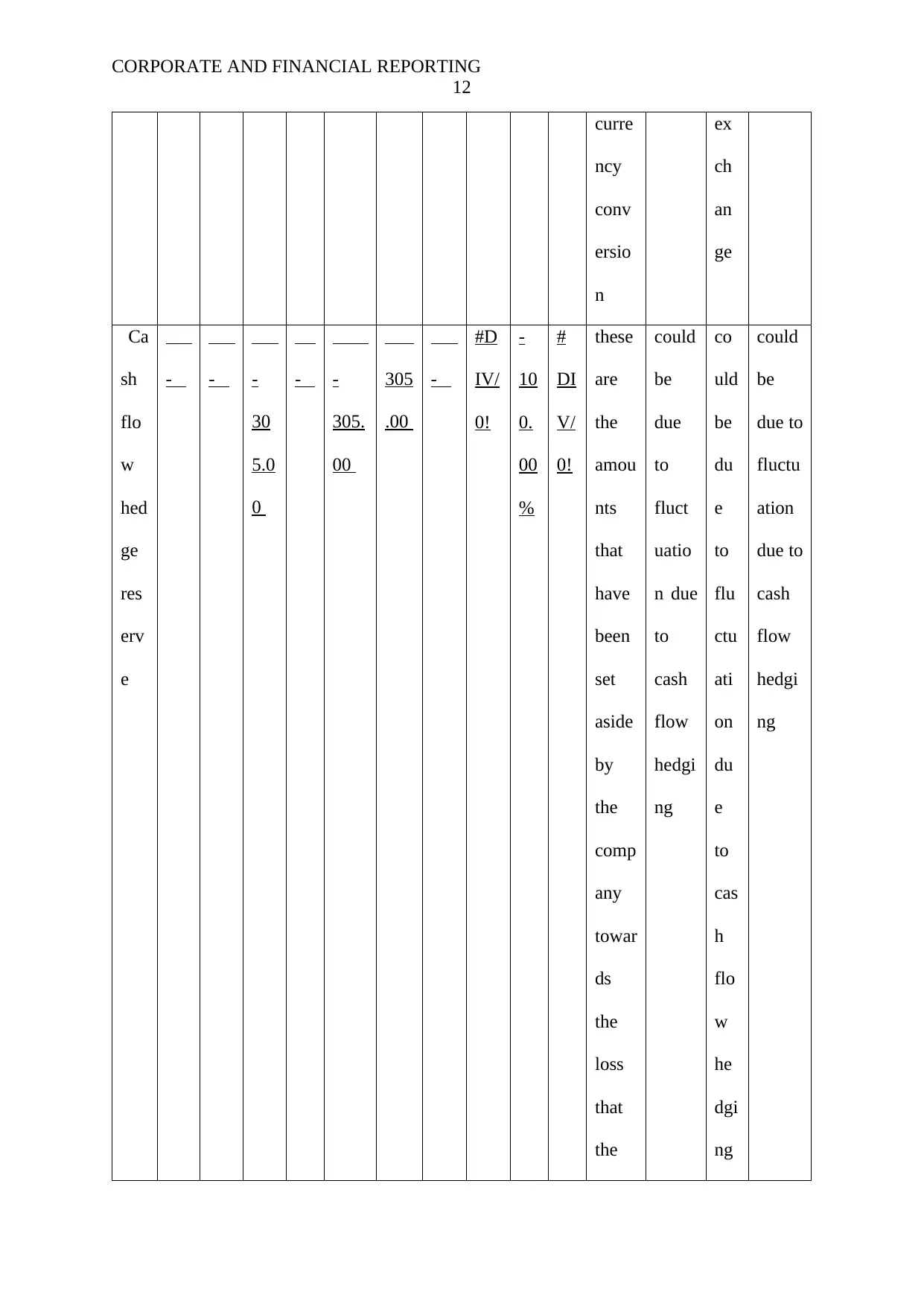

This report provides an executive summary discussing the significance of financial reporting and the role of the Australian Accounting Standards Board (AASB) in establishing accounting standards. The report examines the debt-to-equity ratios of four companies and presents a breakdown of their equity statements. It begins with an introduction to financial accounting and its importance, followed by an explanation of the AASB and its functions. The core of the report includes an analysis of owner's equity components and a comparative analysis of debt-to-equity ratios across the selected companies. The report also highlights the importance of financial reporting for stakeholders and the need for regulation to ensure uniformity and transparency. Finally, the report provides tables with detailed equity analyses for AFT Pharmaceuticals and Alchemia Limited, detailing changes in equity items over several years, with explanations for the changes. The report concludes with a summary of the key findings.

1 out of 32

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.