Financial Accounting Exam: IAS 2, Depreciation, and Reporting Concepts

VerifiedAdded on 2023/06/07

|8

|1515

|477

Homework Assignment

AI Summary

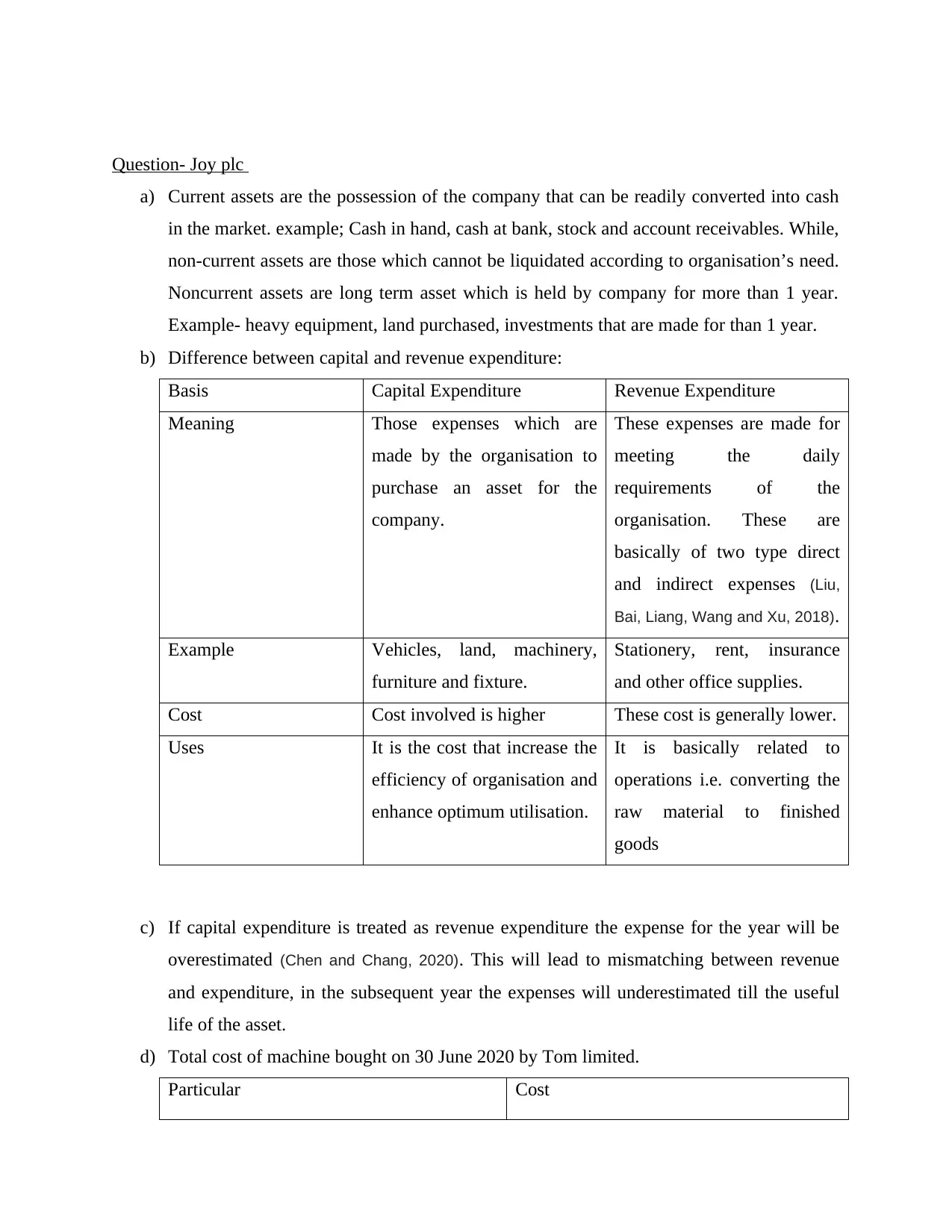

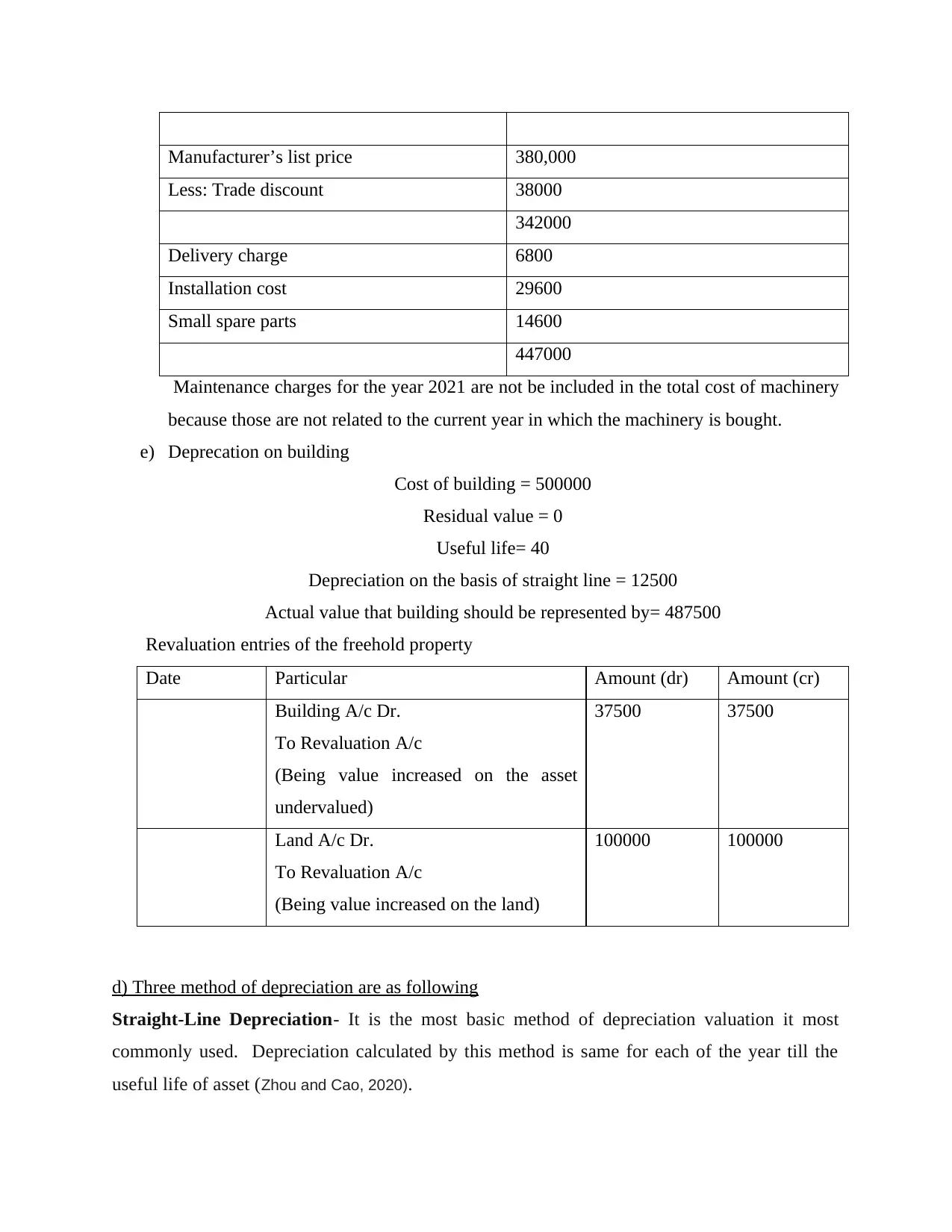

This assignment presents a comprehensive solution to an online finance exam. The document begins with an overview of the Conceptual Framework, detailing its objectives and key assumptions, followed by definitions of IAS 2 terms, including 'inventories' and 'net realisable value,' and how costs should be measured according to IAS 2. The solution then addresses specific questions related to inventory valuation, including calculations for Sean Morris Plc and Danke Linited. The document also explores the differences between current and non-current assets, capital and revenue expenditures, and depreciation methods, with examples from Joy plc and Tom limited. Finally, the assignment includes journal entries for revaluation of assets and a discussion on the differences between depreciation and amortization. The solution is supported by relevant references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.