FNSACC504 Diploma of Accounting: Financial Report Assessment

VerifiedAdded on 2023/02/01

|12

|2054

|89

Homework Assignment

AI Summary

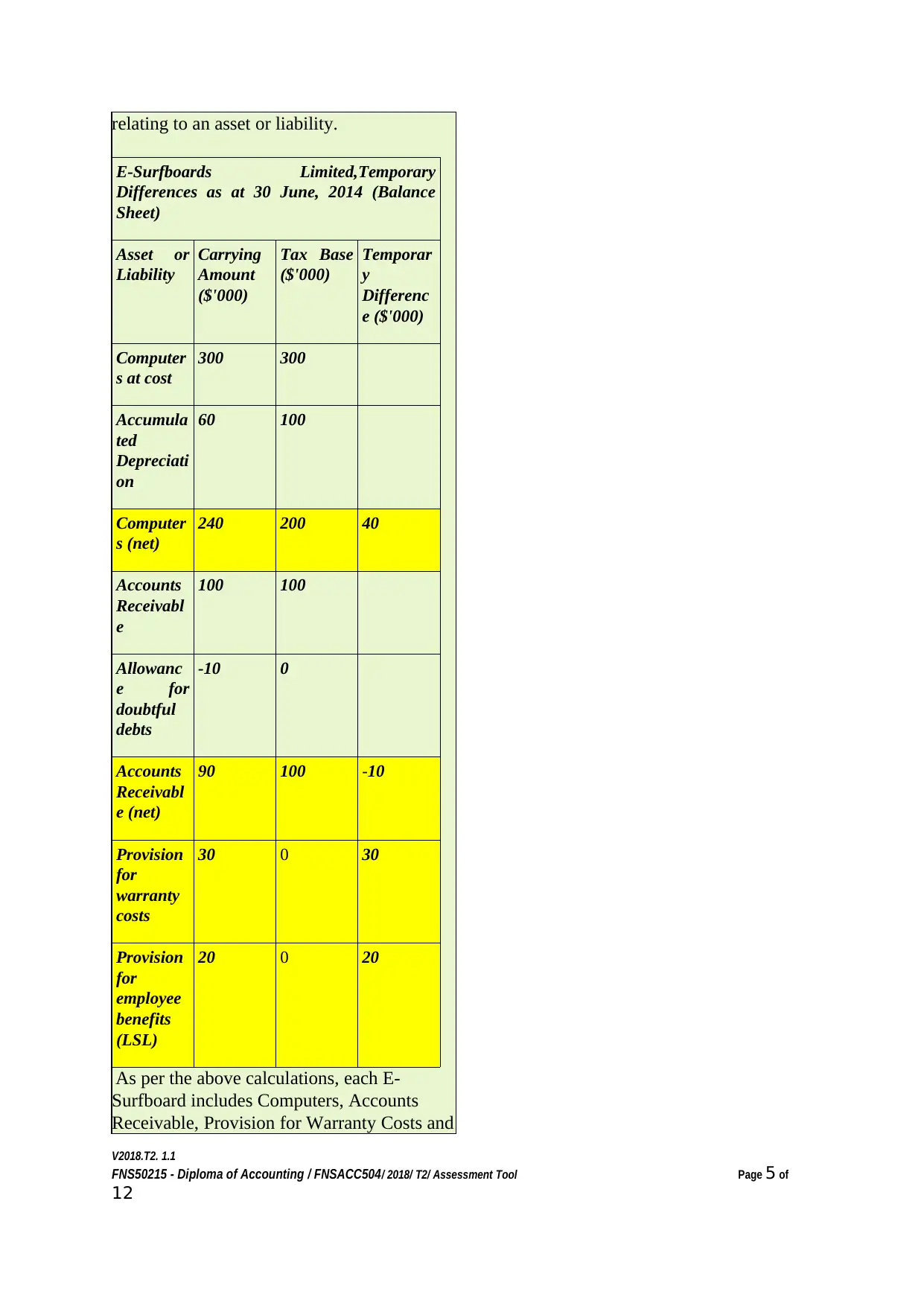

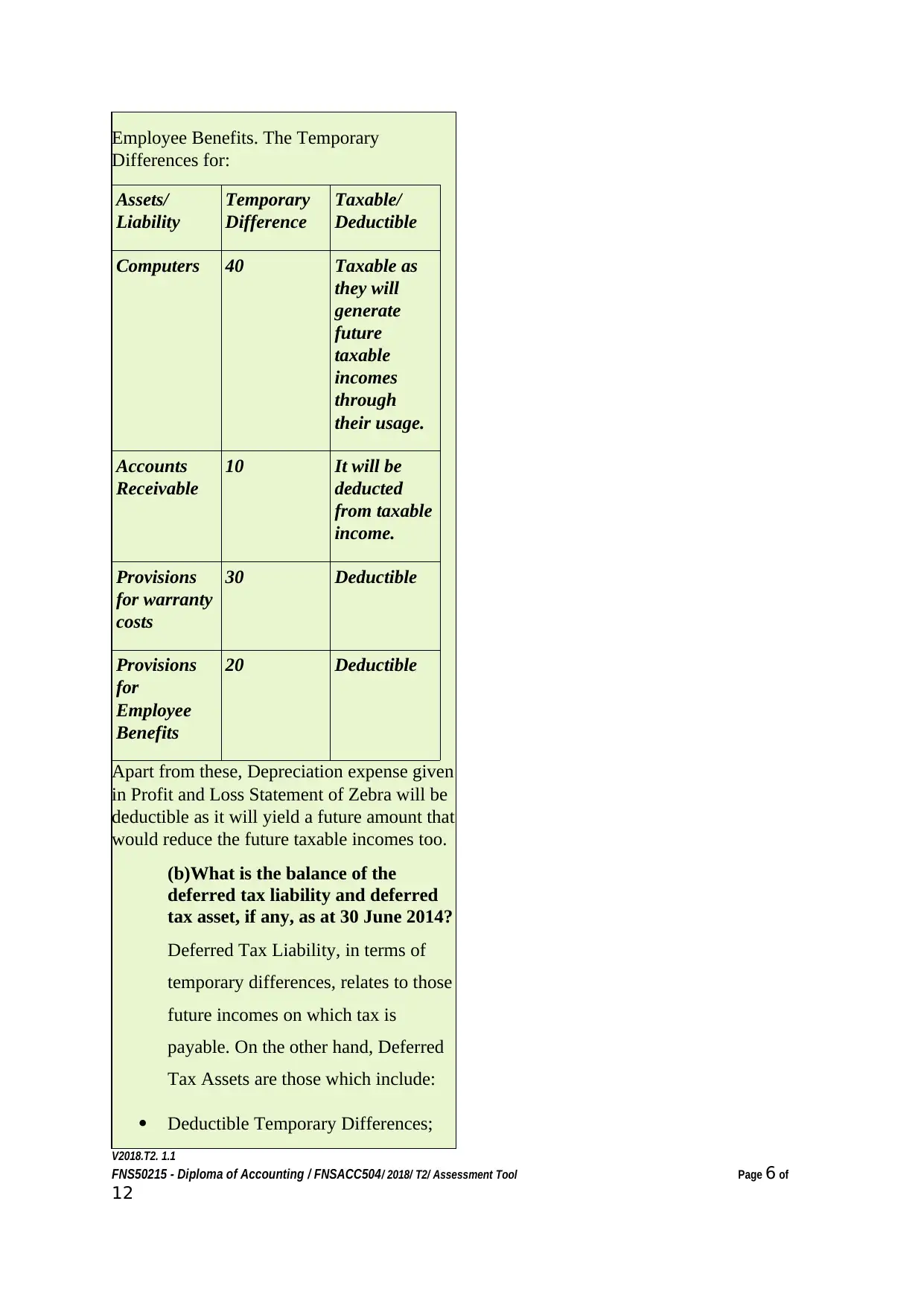

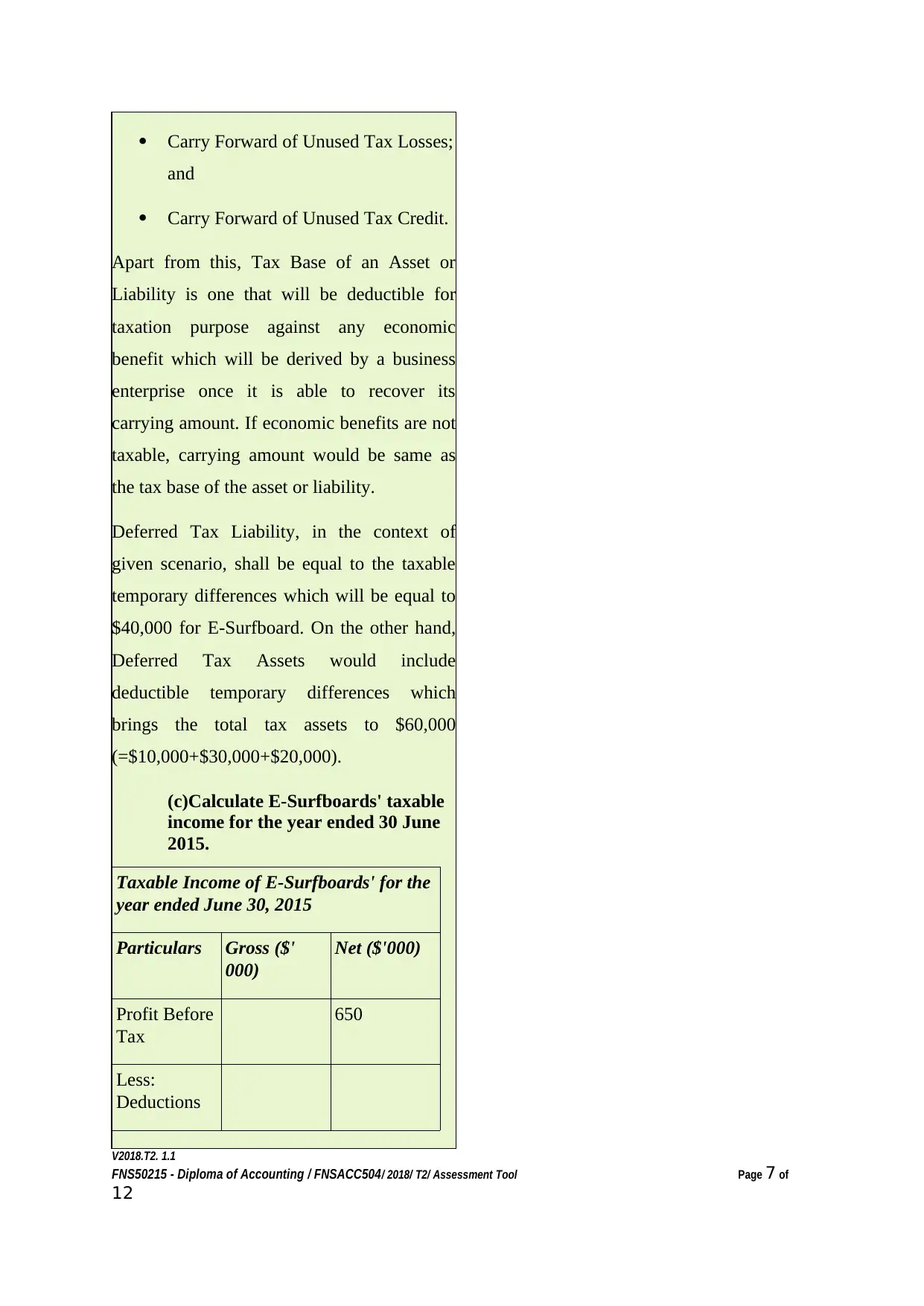

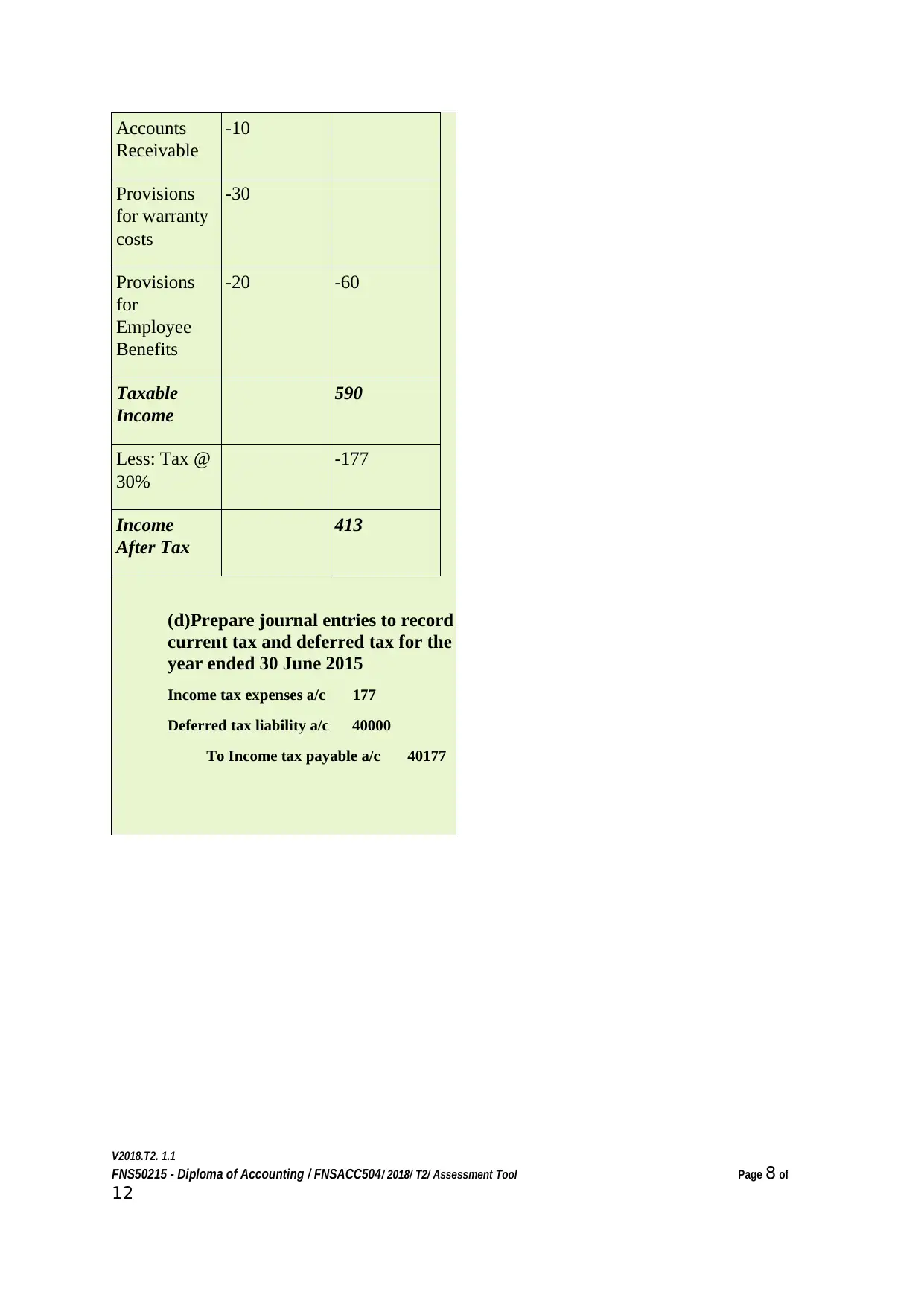

This document presents a comprehensive assessment on preparing financial reports for corporate entities, specifically focusing on the application of accounting principles and tax regulations. The assignment requires the student to analyze temporary differences, classify them as taxable or deductible, and calculate the deferred tax liability and asset. Furthermore, the student calculates the taxable income for the year ended June 30, 2015, and prepares the corresponding journal entries to record current and deferred tax. The assessment adheres to the principles of fairness, flexibility, validity, and reliability, ensuring that the student demonstrates a strong understanding of financial reporting standards and the ability to apply them in a practical scenario. The provided solution includes detailed calculations and explanations, reflecting a thorough understanding of the subject matter.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.