Financial Reporting: HSBC, Regulatory Framework, and Standards

VerifiedAdded on 2023/01/11

|20

|4904

|1

Report

AI Summary

This report provides an in-depth analysis of financial reporting, focusing on regulatory frameworks, governance, and the purpose of financial reporting within organizations, using HSBC Holdings plc as a case study. The report examines the regulatory frameworks of financial accounting, including IFRS and GAAP, and their importance for transparency and stakeholder trust. It also delves into the purpose of financial reporting in meeting organizational objectives, development, and growth, highlighting the role of financial statements in decision-making and internal control. Furthermore, the report discusses the interpretation of financial statements, including profit & loss, balance sheets, and cash flows, as well as the use of financial ratios for organizational performance and investment analysis. The benefits of International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS) are also explored, along with models of financial reporting and auditing. The report concludes with an evaluation of the differences and importance of financial reporting across different countries, providing a comprehensive overview of the subject matter.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

TASK 1.......................................................................................................................................................3

P1 Regulatory frameworks and governance of financial accounting:......................................................3

P2 Purpose of financial reporting for meeting organizational objectives, development and growth:.......6

TASK 2.......................................................................................................................................................7

P3 Interpretation of profit & loss, balance sheet and cash flows..............................................................7

P4 Financial ratios for organisational performance and investment........................................................8

TASK 3.......................................................................................................................................................9

P5 Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS).....................................................................................................................................9

P6 Models of financial reporting and auditing:......................................................................................10

P7 Evaluate the differences and importance of financial reporting across different countries:..............11

CONCLUSION.........................................................................................................................................12

REFERENCES..........................................................................................................................................13

INTRODUCTION.......................................................................................................................................3

TASK 1.......................................................................................................................................................3

P1 Regulatory frameworks and governance of financial accounting:......................................................3

P2 Purpose of financial reporting for meeting organizational objectives, development and growth:.......6

TASK 2.......................................................................................................................................................7

P3 Interpretation of profit & loss, balance sheet and cash flows..............................................................7

P4 Financial ratios for organisational performance and investment........................................................8

TASK 3.......................................................................................................................................................9

P5 Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS).....................................................................................................................................9

P6 Models of financial reporting and auditing:......................................................................................10

P7 Evaluate the differences and importance of financial reporting across different countries:..............11

CONCLUSION.........................................................................................................................................12

REFERENCES..........................................................................................................................................13

INTRODUCTION

Financial reporting define to the standard accuracy of the financial or administrative

reports as well as other associated documents to top management and various customers such as

clients, innovators, legislation, etc. on corporate performance for a specified period of time.

Details are compiled by administrators on a monthly or quarterly basis according to financial

statements. Financial statements consist of income statement planning, income statement,

changes in security solution, and statement of financial position. Financial reporting is the

representation of the organizations' financial statements in information stated (Abeysekera,

2013). Financial reporting generally indicates more about company's financial results for a

specified time frame as well as it is important for a company to file the financial statements not

just for their own function but mostly for interested entities. This report presents analyzes of

financial reporting alongside rights recognized and corporate finance policy making, assessment

of accounting principles, key assumptions and approaches, and assessment of worldwide changes

in rates accounting in the perspective of HSBC Holdings plc, UK's banking and investment

banking standing strong. This report also describes the function of financial reporting to achieve

organizational goals and objectives, development and innovation. Moreover, analysis the

advantages of international accounting standard and international financial reporting.

TASK 1

P1 Regulatory frameworks and governance of financial accounting:

Financial reporting is a planned method of preparing the financial statements such as

balance sheets, profit and loss accounts, cash flow statements etc. which explains the main

economic condition of large companies to externally and internally parties such as shareholders,

ruling party, governance etc. It helps to provide financial data and information to upper

executives within a corporate organization that is being used by managers in various strategic

practices such as research, preparing, decision-making and performance analysis. The key

purpose of financial accounting is to provide data in regard different areas of business operation

for lenders, investors and a broad public audience. It also helps to examine how different tasks

are being used and procured by large companies. It also maintains conformity with applicable

Financial reporting define to the standard accuracy of the financial or administrative

reports as well as other associated documents to top management and various customers such as

clients, innovators, legislation, etc. on corporate performance for a specified period of time.

Details are compiled by administrators on a monthly or quarterly basis according to financial

statements. Financial statements consist of income statement planning, income statement,

changes in security solution, and statement of financial position. Financial reporting is the

representation of the organizations' financial statements in information stated (Abeysekera,

2013). Financial reporting generally indicates more about company's financial results for a

specified time frame as well as it is important for a company to file the financial statements not

just for their own function but mostly for interested entities. This report presents analyzes of

financial reporting alongside rights recognized and corporate finance policy making, assessment

of accounting principles, key assumptions and approaches, and assessment of worldwide changes

in rates accounting in the perspective of HSBC Holdings plc, UK's banking and investment

banking standing strong. This report also describes the function of financial reporting to achieve

organizational goals and objectives, development and innovation. Moreover, analysis the

advantages of international accounting standard and international financial reporting.

TASK 1

P1 Regulatory frameworks and governance of financial accounting:

Financial reporting is a planned method of preparing the financial statements such as

balance sheets, profit and loss accounts, cash flow statements etc. which explains the main

economic condition of large companies to externally and internally parties such as shareholders,

ruling party, governance etc. It helps to provide financial data and information to upper

executives within a corporate organization that is being used by managers in various strategic

practices such as research, preparing, decision-making and performance analysis. The key

purpose of financial accounting is to provide data in regard different areas of business operation

for lenders, investors and a broad public audience. It also helps to examine how different tasks

are being used and procured by large companies. It also maintains conformity with applicable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

laws and legislation, in order to mitigate any potential ambiguity. Financial reporting helps

companies improve transparency. Specific annual results serve as a basis for individual choices

to be made by company organizations (Albu and Albu, 2012). There are discussed some purpose

of financial reporting in context of HSBC such as:

1. Documenting to management team that assists in HSBC organizational planning and decision-

making.

2. Increasingly providing documents and information to organizers, borrowers, lenders and other

creditors to support them in trying to take reasonable as well as reasonable choices on corporate

financing.

3. To convey to shareholders and the community at wide the real and honest image of business

enterprises.

4. To determine how businesses are using their monetary and certain company capital

effectively.

5. To provide detailed data on the success and development of the company to key parties.

6. Determining and reporting to different stakeholders on the success of measures provided by

the business organization.

7. To guarantee that HSBC complies adequately with various legislative laws and regulations.

Regulatory framework of financial reporting:

A high workload is being utilized by different business entities to cover all measures of

business monitoring in broad manner, in order to enforce procedures and investigating trying to

report revenue recognition. Inside an entity, the regulatory structure guarantees the most accurate

and appropriate financial statements. To make accounting standardized, it stresses conformity

with widely agreed reporting standards. The legal framework involves IFRS (International

Financial Reporting Standards) and GAAP (generally accepted accounting principles), which

comprises a collection of guidelines, hypotheses, theoretical frameworks to be implemented by

companies improve transparency. Specific annual results serve as a basis for individual choices

to be made by company organizations (Albu and Albu, 2012). There are discussed some purpose

of financial reporting in context of HSBC such as:

1. Documenting to management team that assists in HSBC organizational planning and decision-

making.

2. Increasingly providing documents and information to organizers, borrowers, lenders and other

creditors to support them in trying to take reasonable as well as reasonable choices on corporate

financing.

3. To convey to shareholders and the community at wide the real and honest image of business

enterprises.

4. To determine how businesses are using their monetary and certain company capital

effectively.

5. To provide detailed data on the success and development of the company to key parties.

6. Determining and reporting to different stakeholders on the success of measures provided by

the business organization.

7. To guarantee that HSBC complies adequately with various legislative laws and regulations.

Regulatory framework of financial reporting:

A high workload is being utilized by different business entities to cover all measures of

business monitoring in broad manner, in order to enforce procedures and investigating trying to

report revenue recognition. Inside an entity, the regulatory structure guarantees the most accurate

and appropriate financial statements. To make accounting standardized, it stresses conformity

with widely agreed reporting standards. The legal framework involves IFRS (International

Financial Reporting Standards) and GAAP (generally accepted accounting principles), which

comprises a collection of guidelines, hypotheses, theoretical frameworks to be implemented by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

bookkeepers even when going to report on various topics. Regulatory process is set of stages that

regulatory agencies start taking to enhance the sensitivity of different rules (Council, 2012).

Compliance with the legislative structure is important for HSBC, as it guarantees that appropriate

financial data is shared with shareholders and consumers. Making convergence in accounting

systems implemented by various entities worldwide is the key purpose of the legal framework.

IFRS is a crucial element of the legislative component, as it contains requirements which support

in the smooth surface of financial reporting. The regulatory system is drawn up by the

government bodies so conformance with the laws and restrictions is also an aim.

Financial statements prepared utilizing legal structure contribute to improved trust

building for shareholders as well as other company's financial consumers. Adherence with the

legal framework increases financial reports legitimacy. The confidence of stockholders and

public company in companies like HSBC is powerful due to normal compliance with regulatory

structure. Some rather process is established for all companies listed encouraging digital

payments in order to find potential shareholders. It also helps in dealing with different challenges

that may occur mostly at the time of financial reporting system and improves responsibility.

There are some elements of regulatory framework of financial reporting such as:

IFRS: Financial statements of the company for the publicly traded companies are

recognized as international financial reporting standards. Those regulatory frame works are

established by the committee of standard practices in finance. These are key components of the

financial reporting legal framework. Listed businesses embrace these requirements globally for

carrying out account balances and reporting concerns. These principles serve as a common

identity for conducting company's value at national scale, so that financial reports can be readily

comprehensible to all users and comparable around the globe. These guidelines reflect both

positive and negative attributes of organization of the company.

GAAP (Generally accepted accounting principles): It indicates that business activity must be

accompanied even when financial reporting in a collection of frequently reasonable accounting

principles, policies and practices. GAAP provides a structured basis for the notification to

concerned financial statement users matters (Flower, 2016).

Governance of financial reporting

regulatory agencies start taking to enhance the sensitivity of different rules (Council, 2012).

Compliance with the legislative structure is important for HSBC, as it guarantees that appropriate

financial data is shared with shareholders and consumers. Making convergence in accounting

systems implemented by various entities worldwide is the key purpose of the legal framework.

IFRS is a crucial element of the legislative component, as it contains requirements which support

in the smooth surface of financial reporting. The regulatory system is drawn up by the

government bodies so conformance with the laws and restrictions is also an aim.

Financial statements prepared utilizing legal structure contribute to improved trust

building for shareholders as well as other company's financial consumers. Adherence with the

legal framework increases financial reports legitimacy. The confidence of stockholders and

public company in companies like HSBC is powerful due to normal compliance with regulatory

structure. Some rather process is established for all companies listed encouraging digital

payments in order to find potential shareholders. It also helps in dealing with different challenges

that may occur mostly at the time of financial reporting system and improves responsibility.

There are some elements of regulatory framework of financial reporting such as:

IFRS: Financial statements of the company for the publicly traded companies are

recognized as international financial reporting standards. Those regulatory frame works are

established by the committee of standard practices in finance. These are key components of the

financial reporting legal framework. Listed businesses embrace these requirements globally for

carrying out account balances and reporting concerns. These principles serve as a common

identity for conducting company's value at national scale, so that financial reports can be readily

comprehensible to all users and comparable around the globe. These guidelines reflect both

positive and negative attributes of organization of the company.

GAAP (Generally accepted accounting principles): It indicates that business activity must be

accompanied even when financial reporting in a collection of frequently reasonable accounting

principles, policies and practices. GAAP provides a structured basis for the notification to

concerned financial statement users matters (Flower, 2016).

Governance of financial reporting

Regulatory authorities are focusing their energies into strengthening corporate

governance system pertaining to economic statements in the current market environment, public

firms experiencing financial difficulties. Financial statement leadership is particularly concerned

with the investigator, who's still accountable for supplying a viewpoint on the company's

financial statements. According to their duties, the inspector can be an audit committee or a

legislative inspector. Audit committee can be government workers but are advisors inspectors. In

HSBC, internal as well as external or legislative accountants are important for the effective

management of financial statements. Nonetheless, compared to external auditors, inner auditors'

abilities are limited. Some governmental corpses such as IAB, ASB, etc. are also dedicated to

good leadership of revenue recognition, but these body parts problem distinct standards and

regulations for enforcing good governance. Additionally, regulatory bodies establish the laws

and duties of relevant stakeholders such as auditors. An active economic reporting regulation

offers an explicit image of the quality of the business in addition to safeguard investors interest.

Likely to follow are some basic criteria of financial reporting effective governance, as continues

to follow:

Due diligence: Accountable people such as bookkeepers, supervisors, inspectors etc. are

mandated to execute their responsibilities with proper research in order to integrate effective

corporate governance. Conformance with proper research even when achieving obligations can

generate a scamp and free economic environment which is scandalous. It merely relates to an

employee sound moral and appropriate step within the same business entity to prevent an offense

or torture.

Transparency: It relates to the way to which stakeholders typically have access to

needed or applicable company-related details such as consolidated financial statements It is

important to preserve transparency in the financial accounting strategy to produce efficient or

good management in financial reporting (Johnston and Petacchi, 2017). It refers specifically to

displaying the actual company institution's status without removing something from consumers

of income statement.

Effective internal controls: Internal control system helps guarantee of great economic

reporting policy making within such a business firm. Inner strategy is carried out at HSBC via

governance system pertaining to economic statements in the current market environment, public

firms experiencing financial difficulties. Financial statement leadership is particularly concerned

with the investigator, who's still accountable for supplying a viewpoint on the company's

financial statements. According to their duties, the inspector can be an audit committee or a

legislative inspector. Audit committee can be government workers but are advisors inspectors. In

HSBC, internal as well as external or legislative accountants are important for the effective

management of financial statements. Nonetheless, compared to external auditors, inner auditors'

abilities are limited. Some governmental corpses such as IAB, ASB, etc. are also dedicated to

good leadership of revenue recognition, but these body parts problem distinct standards and

regulations for enforcing good governance. Additionally, regulatory bodies establish the laws

and duties of relevant stakeholders such as auditors. An active economic reporting regulation

offers an explicit image of the quality of the business in addition to safeguard investors interest.

Likely to follow are some basic criteria of financial reporting effective governance, as continues

to follow:

Due diligence: Accountable people such as bookkeepers, supervisors, inspectors etc. are

mandated to execute their responsibilities with proper research in order to integrate effective

corporate governance. Conformance with proper research even when achieving obligations can

generate a scamp and free economic environment which is scandalous. It merely relates to an

employee sound moral and appropriate step within the same business entity to prevent an offense

or torture.

Transparency: It relates to the way to which stakeholders typically have access to

needed or applicable company-related details such as consolidated financial statements It is

important to preserve transparency in the financial accounting strategy to produce efficient or

good management in financial reporting (Johnston and Petacchi, 2017). It refers specifically to

displaying the actual company institution's status without removing something from consumers

of income statement.

Effective internal controls: Internal control system helps guarantee of great economic

reporting policy making within such a business firm. Inner strategy is carried out at HSBC via

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

inbuilt rules and practices. It also includes ensuring that procedures, revenue recognition task, are

running effectively.

P2 Purpose of financial reporting for meeting organizational objectives, development and

growth:

Financial reports give a true image of business success by financial statements such as

report of sales and financial position. Financial reporting is important to a corporate

organization, as it guarantees long-term success and development. In HSBC, cash transactions

are compiled by executives underneath the financial reporting framework financial statements,

income statement, in order to demonstrate their real effects over a specified timeframe. Likely to

follow are some significant financial reporting advantages, mentioned elsewhere here:

• Assistance in decision-making: Administration in large-scale organizations such as HSBC,

taking important corporate strategic decisions through the use of financial statements. Financial

reporting offers extensive data on the transactions and financial functions of the business that

support managers in HSBC decision-making.

• Assist in the impact of the external variables: the revenue recognition system helps to recognize

various environment or elements that that impact the overall performance of an entity in negative

manner. In HSBC, management determines the influence of environmental variables such as

inflation, modifications in public sector policies, alteration in economics etc. on corporate

efficiency by using analysis as well as assessment of financial information (K. Johl,

Subramaniam and Cooper, 2013).

• Internal management regulate: financial statement assists in the implementation of strategies

corporate governance by supplying sensible, precise insights for the category. Every other staff

members requirements are corrected by planning in financial statements which provides system

of internal control across all processes and tasks.

• Helps to manage effectively: accounting information seeks to strengthen appropriate individual

governance. Within HSBC, protective behavior financial statements with the aid of careful

planning and controlling, which eventually lead to the successful leadership.

running effectively.

P2 Purpose of financial reporting for meeting organizational objectives, development and

growth:

Financial reports give a true image of business success by financial statements such as

report of sales and financial position. Financial reporting is important to a corporate

organization, as it guarantees long-term success and development. In HSBC, cash transactions

are compiled by executives underneath the financial reporting framework financial statements,

income statement, in order to demonstrate their real effects over a specified timeframe. Likely to

follow are some significant financial reporting advantages, mentioned elsewhere here:

• Assistance in decision-making: Administration in large-scale organizations such as HSBC,

taking important corporate strategic decisions through the use of financial statements. Financial

reporting offers extensive data on the transactions and financial functions of the business that

support managers in HSBC decision-making.

• Assist in the impact of the external variables: the revenue recognition system helps to recognize

various environment or elements that that impact the overall performance of an entity in negative

manner. In HSBC, management determines the influence of environmental variables such as

inflation, modifications in public sector policies, alteration in economics etc. on corporate

efficiency by using analysis as well as assessment of financial information (K. Johl,

Subramaniam and Cooper, 2013).

• Internal management regulate: financial statement assists in the implementation of strategies

corporate governance by supplying sensible, precise insights for the category. Every other staff

members requirements are corrected by planning in financial statements which provides system

of internal control across all processes and tasks.

• Helps to manage effectively: accounting information seeks to strengthen appropriate individual

governance. Within HSBC, protective behavior financial statements with the aid of careful

planning and controlling, which eventually lead to the successful leadership.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Investors are people or businesses involved in organization's environment and influence

the overall enterprise organizational effectiveness. Interested parties are the ultimate recipient of

the financial statements submitted underneath the framework of financial reporting. They should

use financial results to make policy about banking and finance. Within HSBC, financial

reporting is conducted by managers as well as other responsible staff, thus taking into account

the key interests and expectations of diverse participants. Investors are categorized as different

stakeholders, internal users are company participants and interested parties are non-business

stakeholders. Mentioned business offers an accurate measure of their results by financial

statements. Financial reporting addresses participant needs and preferences, mentioned

following:

Customers: Customers are important corporate stakeholders, as their choice and expectations

determine the success of the business. Consumers receive only the brand equity, commitment

and availability of the corporation's product offerings. Through financial reporting organization

interacts their business success and market capital.

Investors: Shareholders are actual business shareholders as they spend the shares in the business

that allows companies to work in markets efficiently and satisfies the investment goals of the

firm. They make a reasonable return on investment or assets from the business that they invest.

Business publishes their shareholder financial statements to guarantee their purchase position is

correct and also gain new customers (Klassen and Laplante, 2012).

Employees: Employees are the organization's corporate participant, since they keep position in

the context of their salaries and development or promotion of jobs. They expect strong success

and development for the organization in the future. So company supporting its quarterly earnings

by publishing to dedicate its resources to the potential expansion of the industry.

Owners or management: Such shareholders are significantly affected by the development and

success of the organisation. Manager and executives create a major investment in a company or

keep large sums or volumes of stock holdings and they expect strong financial results and

business profits. They evaluate actual firm productivity through revenue recognition.

the overall enterprise organizational effectiveness. Interested parties are the ultimate recipient of

the financial statements submitted underneath the framework of financial reporting. They should

use financial results to make policy about banking and finance. Within HSBC, financial

reporting is conducted by managers as well as other responsible staff, thus taking into account

the key interests and expectations of diverse participants. Investors are categorized as different

stakeholders, internal users are company participants and interested parties are non-business

stakeholders. Mentioned business offers an accurate measure of their results by financial

statements. Financial reporting addresses participant needs and preferences, mentioned

following:

Customers: Customers are important corporate stakeholders, as their choice and expectations

determine the success of the business. Consumers receive only the brand equity, commitment

and availability of the corporation's product offerings. Through financial reporting organization

interacts their business success and market capital.

Investors: Shareholders are actual business shareholders as they spend the shares in the business

that allows companies to work in markets efficiently and satisfies the investment goals of the

firm. They make a reasonable return on investment or assets from the business that they invest.

Business publishes their shareholder financial statements to guarantee their purchase position is

correct and also gain new customers (Klassen and Laplante, 2012).

Employees: Employees are the organization's corporate participant, since they keep position in

the context of their salaries and development or promotion of jobs. They expect strong success

and development for the organization in the future. So company supporting its quarterly earnings

by publishing to dedicate its resources to the potential expansion of the industry.

Owners or management: Such shareholders are significantly affected by the development and

success of the organisation. Manager and executives create a major investment in a company or

keep large sums or volumes of stock holdings and they expect strong financial results and

business profits. They evaluate actual firm productivity through revenue recognition.

TASK 2

P3 Interpretation of profit & loss, balance sheet and cash flows

Profit & loss account interpretation: A company institution's revenue statement of

income pay defines the profit margins. According to HSBC's income statement, the company

made a net profit of $150,25 million in 2018 and $11,879 million in 2017, indicating that the

profit margin status of the country is enhanced. In 2018, the company reported $30489 million in

investment earnings, and $4865 million in tax expenses. HSBC's total revenue growth pattern is

concept toward slightly up. While the net income of the company decreased leading to financial

impact in 2016, the company had grown strongly in 2017 and 2018 by $11648 million.

Balance sheet interpretation: Balance sheet is a snapshot that shows company's current results

by presenting actual representation of financial assets as well as liabilities business organisation.

HSBC has announced its total assets amounting $204,115 million and $159,884 million

throughout the year 2018 and 2017 separately. As a whole assets of the company are expanded

throughout the year, indicating an improvement in the productivity of the corporation in asset

generation (HSBC Holdings plc Annual Report and Accounts. 2018). Where even the current

expenses as a corporation are meaning of the new 2,363,875 million and 2,323,900 million over

the years 2018 and 2017. Current liabilities are confirmed to have small reduction. Where as

shareholder's equity is $186,253 million and $190,250 million in year 2018 and year 2017

respectively.

Cash flow statement interpretation: Cash balance statements offer an overview of cash

movement within a corporate organization. In 2018 and 2017, HSBC meaning of the new

consolidated revenue cash flow from operations of $6469 million and $10478, showed that the

company has enhanced its productivity in generating operating income. The cash equivalents of

the company are receptive at 301082 million and 337412 million in the year 2018 and 2017. The

general volatility situation of the company was actually dead related to the speed of inflation.

P4 Financial ratios for organisational performance and investment.

Financial ratio is to measure the actual quality of the company enterprise alongside

efficiency, competitiveness and financial security evaluations. Below are some of HSBC's main

financial indicators, as wants to follow:

P3 Interpretation of profit & loss, balance sheet and cash flows

Profit & loss account interpretation: A company institution's revenue statement of

income pay defines the profit margins. According to HSBC's income statement, the company

made a net profit of $150,25 million in 2018 and $11,879 million in 2017, indicating that the

profit margin status of the country is enhanced. In 2018, the company reported $30489 million in

investment earnings, and $4865 million in tax expenses. HSBC's total revenue growth pattern is

concept toward slightly up. While the net income of the company decreased leading to financial

impact in 2016, the company had grown strongly in 2017 and 2018 by $11648 million.

Balance sheet interpretation: Balance sheet is a snapshot that shows company's current results

by presenting actual representation of financial assets as well as liabilities business organisation.

HSBC has announced its total assets amounting $204,115 million and $159,884 million

throughout the year 2018 and 2017 separately. As a whole assets of the company are expanded

throughout the year, indicating an improvement in the productivity of the corporation in asset

generation (HSBC Holdings plc Annual Report and Accounts. 2018). Where even the current

expenses as a corporation are meaning of the new 2,363,875 million and 2,323,900 million over

the years 2018 and 2017. Current liabilities are confirmed to have small reduction. Where as

shareholder's equity is $186,253 million and $190,250 million in year 2018 and year 2017

respectively.

Cash flow statement interpretation: Cash balance statements offer an overview of cash

movement within a corporate organization. In 2018 and 2017, HSBC meaning of the new

consolidated revenue cash flow from operations of $6469 million and $10478, showed that the

company has enhanced its productivity in generating operating income. The cash equivalents of

the company are receptive at 301082 million and 337412 million in the year 2018 and 2017. The

general volatility situation of the company was actually dead related to the speed of inflation.

P4 Financial ratios for organisational performance and investment.

Financial ratio is to measure the actual quality of the company enterprise alongside

efficiency, competitiveness and financial security evaluations. Below are some of HSBC's main

financial indicators, as wants to follow:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

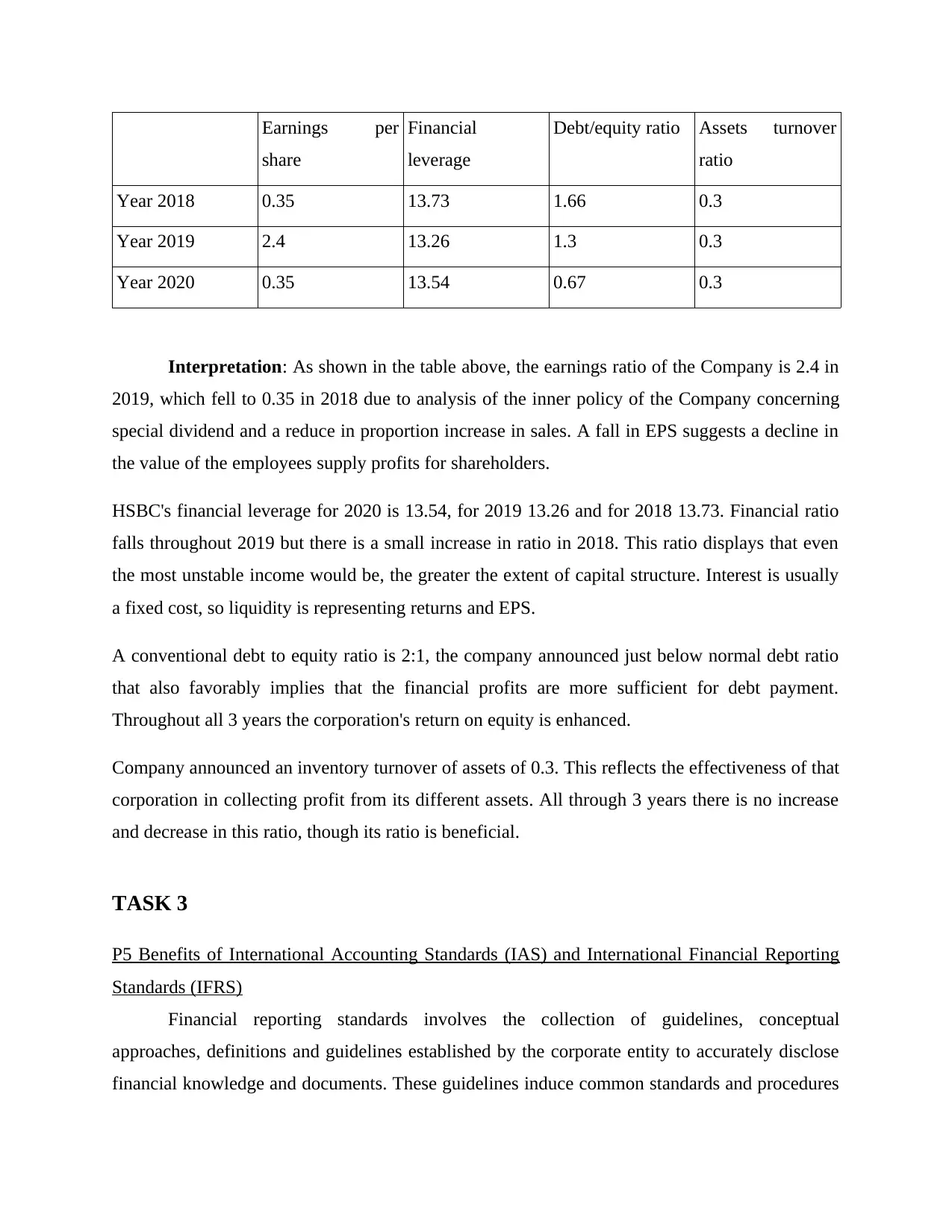

Earnings per

share

Financial

leverage

Debt/equity ratio Assets turnover

ratio

Year 2018 0.35 13.73 1.66 0.3

Year 2019 2.4 13.26 1.3 0.3

Year 2020 0.35 13.54 0.67 0.3

Interpretation: As shown in the table above, the earnings ratio of the Company is 2.4 in

2019, which fell to 0.35 in 2018 due to analysis of the inner policy of the Company concerning

special dividend and a reduce in proportion increase in sales. A fall in EPS suggests a decline in

the value of the employees supply profits for shareholders.

HSBC's financial leverage for 2020 is 13.54, for 2019 13.26 and for 2018 13.73. Financial ratio

falls throughout 2019 but there is a small increase in ratio in 2018. This ratio displays that even

the most unstable income would be, the greater the extent of capital structure. Interest is usually

a fixed cost, so liquidity is representing returns and EPS.

A conventional debt to equity ratio is 2:1, the company announced just below normal debt ratio

that also favorably implies that the financial profits are more sufficient for debt payment.

Throughout all 3 years the corporation's return on equity is enhanced.

Company announced an inventory turnover of assets of 0.3. This reflects the effectiveness of that

corporation in collecting profit from its different assets. All through 3 years there is no increase

and decrease in this ratio, though its ratio is beneficial.

TASK 3

P5 Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS)

Financial reporting standards involves the collection of guidelines, conceptual

approaches, definitions and guidelines established by the corporate entity to accurately disclose

financial knowledge and documents. These guidelines induce common standards and procedures

share

Financial

leverage

Debt/equity ratio Assets turnover

ratio

Year 2018 0.35 13.73 1.66 0.3

Year 2019 2.4 13.26 1.3 0.3

Year 2020 0.35 13.54 0.67 0.3

Interpretation: As shown in the table above, the earnings ratio of the Company is 2.4 in

2019, which fell to 0.35 in 2018 due to analysis of the inner policy of the Company concerning

special dividend and a reduce in proportion increase in sales. A fall in EPS suggests a decline in

the value of the employees supply profits for shareholders.

HSBC's financial leverage for 2020 is 13.54, for 2019 13.26 and for 2018 13.73. Financial ratio

falls throughout 2019 but there is a small increase in ratio in 2018. This ratio displays that even

the most unstable income would be, the greater the extent of capital structure. Interest is usually

a fixed cost, so liquidity is representing returns and EPS.

A conventional debt to equity ratio is 2:1, the company announced just below normal debt ratio

that also favorably implies that the financial profits are more sufficient for debt payment.

Throughout all 3 years the corporation's return on equity is enhanced.

Company announced an inventory turnover of assets of 0.3. This reflects the effectiveness of that

corporation in collecting profit from its different assets. All through 3 years there is no increase

and decrease in this ratio, though its ratio is beneficial.

TASK 3

P5 Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS)

Financial reporting standards involves the collection of guidelines, conceptual

approaches, definitions and guidelines established by the corporate entity to accurately disclose

financial knowledge and documents. These guidelines induce common standards and procedures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that different – different large companies need to implement in order to preserve consistency in

revenue recognition around the globe (Maffett, 2012). Financial document is intended or

generated by a corporate entity by implementing accounting standards that help build customer

and investor trust. HSBC implemented several important financial reporting requirements, as

follows:

International Accounting Standards (IAS): Those were International Accounting

Standards originally suggested. These standards are being substituted by global standards for

financial statements at current. The International Accounting Standards Commission (IASC)

formulates those criteria. The primary aim of these is to improve team integrity and

accountability and the results of revenue recognition. These requirements are also improving

trade and investments.

IFRS (International financial reporting standards): This applies to a specific

collection of rules used among businesses that conduct their company worldwide to file reliable,

equivalent and clear financial statements. The International Accounting Standards Board (IASB)

is recommending to IFRS. Such requirements define how businesses will have their financial

statements and activities managed and published.

Benefits of International Accounting Standards and International financial

reporting standards: Following, the therefore are some of the main advantages of international

accounting standards:

• Such criteria are valuable for mentioned multinationals such as HSBC, as they promote

compliance with ethical.

• Business financial information provided by implementing these criteria allows businesses to

draw deliberate expenditure (Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros,

2015)

• These guidelines offer versatility to address for any unforeseen or anticipated development in

the world economic environment, since they are predicated on general guidelines.

• These standards help multinationals centralize financial examines the different businesses

across the globe.

revenue recognition around the globe (Maffett, 2012). Financial document is intended or

generated by a corporate entity by implementing accounting standards that help build customer

and investor trust. HSBC implemented several important financial reporting requirements, as

follows:

International Accounting Standards (IAS): Those were International Accounting

Standards originally suggested. These standards are being substituted by global standards for

financial statements at current. The International Accounting Standards Commission (IASC)

formulates those criteria. The primary aim of these is to improve team integrity and

accountability and the results of revenue recognition. These requirements are also improving

trade and investments.

IFRS (International financial reporting standards): This applies to a specific

collection of rules used among businesses that conduct their company worldwide to file reliable,

equivalent and clear financial statements. The International Accounting Standards Board (IASB)

is recommending to IFRS. Such requirements define how businesses will have their financial

statements and activities managed and published.

Benefits of International Accounting Standards and International financial

reporting standards: Following, the therefore are some of the main advantages of international

accounting standards:

• Such criteria are valuable for mentioned multinationals such as HSBC, as they promote

compliance with ethical.

• Business financial information provided by implementing these criteria allows businesses to

draw deliberate expenditure (Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros,

2015)

• These guidelines offer versatility to address for any unforeseen or anticipated development in

the world economic environment, since they are predicated on general guidelines.

• These standards help multinationals centralize financial examines the different businesses

across the globe.

• Use of these principles to support the key stakeholders in building trust and faith.

• Such requirements decrease the difficulty of inter-national company's financial planning.

• Implementation of these standards contributes to economic growth by boosting global trade.

• It provides expert opportunities for employment everywhere in the globe.

• Industry has benefited from these standards in maximizing their wealth with reasonable

expense in the international economy.

P6 Models of financial reporting and auditing:

At international level, corporations carry out financial statements when contemplating

various forms of financial management and auditing. Such approaches are frequently adopted by

various groups around the globe to make financial statements standardized. These simulations

also aid in overcoming a few other problems in measurement and auditing. Auditors, regulators,

and other experts apply these templates to meet their internal accounting objectives. Below are a

few significant implication of sustainable business practice, as follows:

Three statement model: This model of financial and other information demonstrates that

three most important declarations must be prepared: financial statement, statement of income and

statement of cash flow. This model also offers theories, format and process of making these main

points. Designed to operate companies must adopt three models of financial reporting statements.

Within this method, accountants are expected to remark on these following parts and to express

their views.

Consolidation model: According to this model, the consolidation of their transactions is

mandated for companies that operate their company changes in specific nations or have affiliates.

This method is fundamental to good transaction monitoring. This model is important for auditing

purposes because it assists the auditor in offering feedback or suggestions on the aggregate

performance of the firm of company (Rensburg and Botha, 2014).

Merger model: This model focuses primarily on a common framework for business

mergers around the world. This framework offers some various methodology of takeover, such

as PE ratio, operating cash flow, analytic approach of substitute, method of market price, etc.

• Such requirements decrease the difficulty of inter-national company's financial planning.

• Implementation of these standards contributes to economic growth by boosting global trade.

• It provides expert opportunities for employment everywhere in the globe.

• Industry has benefited from these standards in maximizing their wealth with reasonable

expense in the international economy.

P6 Models of financial reporting and auditing:

At international level, corporations carry out financial statements when contemplating

various forms of financial management and auditing. Such approaches are frequently adopted by

various groups around the globe to make financial statements standardized. These simulations

also aid in overcoming a few other problems in measurement and auditing. Auditors, regulators,

and other experts apply these templates to meet their internal accounting objectives. Below are a

few significant implication of sustainable business practice, as follows:

Three statement model: This model of financial and other information demonstrates that

three most important declarations must be prepared: financial statement, statement of income and

statement of cash flow. This model also offers theories, format and process of making these main

points. Designed to operate companies must adopt three models of financial reporting statements.

Within this method, accountants are expected to remark on these following parts and to express

their views.

Consolidation model: According to this model, the consolidation of their transactions is

mandated for companies that operate their company changes in specific nations or have affiliates.

This method is fundamental to good transaction monitoring. This model is important for auditing

purposes because it assists the auditor in offering feedback or suggestions on the aggregate

performance of the firm of company (Rensburg and Botha, 2014).

Merger model: This model focuses primarily on a common framework for business

mergers around the world. This framework offers some various methodology of takeover, such

as PE ratio, operating cash flow, analytic approach of substitute, method of market price, etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.