Analysis of Financial Reporting Framework: ACCT20074 Report, Term 1

VerifiedAdded on 2022/11/13

|22

|4828

|331

Report

AI Summary

This report provides a comprehensive analysis of the conceptual framework of financial reporting, tracing its historical development in the USA, UK, and Australia, and addressing concerns about its adoption. It applies the IASB/IFRS framework, examining its practical application through the financial statements of Ingenia Communities Group, an ASX-listed entity, focusing on recognition principles, measurement bases, and qualitative characteristics. The report also investigates sustainability and integrated reporting, comparing GRI with integrated reporting, discussing the application of accounting theories, and evaluating NEPI RockCastle (South African Company). Finally, it compares the reporting practices of the selected Australian company with those of the South African company to identify differences in sustainability disclosures. The report concludes with a summary of key findings and insights.

ACCT20074 Contemporary Accounting Theory

Term 1 Assessment 3: Practical report (Major assignment)

1

Term 1 Assessment 3: Practical report (Major assignment)

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report has undertaken an evaluation of the conceptual framework of financial

reporting by analyzing its history of development; concerns related to its adoption and also

demonstrated its application with the selection of financial reports of an ASX listed entity. In

addition to this, it also presented an examination of sustainability or integrated reporting

framework of businesses. It includes comparison of GRI with integrated reporting, discussion of

CF for sustainability reporting, application of theories for developing content of sustainability

reporting and examined the various components of integrated reporting systems in reference to a

South African company. Also, the comparisons of the components are done with the selected

Australian company to identify the differences between the types of disclosures in relation to

sustainability by the two companies.

2

This report has undertaken an evaluation of the conceptual framework of financial

reporting by analyzing its history of development; concerns related to its adoption and also

demonstrated its application with the selection of financial reports of an ASX listed entity. In

addition to this, it also presented an examination of sustainability or integrated reporting

framework of businesses. It includes comparison of GRI with integrated reporting, discussion of

CF for sustainability reporting, application of theories for developing content of sustainability

reporting and examined the various components of integrated reporting systems in reference to a

South African company. Also, the comparisons of the components are done with the selected

Australian company to identify the differences between the types of disclosures in relation to

sustainability by the two companies.

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................5

Part A: Conceptual Framework.......................................................................................................6

A: Review of Literature Regarding History and Development of Conceptual Framework for

Financial Reporting in the USA, UK, Australia..........................................................................6

B: Application of the IASB/IFRS Conceptual Framework for Financial Reporting...................7

C: Quality Concerns of the Conceptual Framework of Reporting...............................................8

D: Application of conceptual framework by Ingenia Communities Group.................................8

D(i): Financial Statements and their components........................................................................8

D (ii): Recognition principles and measurement basis used to present revenue, assets and

liabilities by Ingenia Communities Group...................................................................................9

D (iii): Qualitative characteristics of financial information used in financial report of Ingenia

Communities Group...................................................................................................................10

Part B: Integrated and sustainability reporting..............................................................................13

A: Comparison of GRI (Global Reporting Initiative) with International Integrated Reporting

Framework.................................................................................................................................13

B: Strengths and Limitations of the Conventional Accounting.................................................13

C: Applicability of Theories to Explain Content of Sustainability and Integrated Reporting...14

D: Evaluation of NEPI RockCastle (South African Company) on the grounds of different

components of integrated reporting through use of index (Table or check list)........................15

E: Comparison of reporting practice of selected Australian Company with the index and

reporting practices of selected South African company............................................................17

Conclusion.....................................................................................................................................19

Reference.......................................................................................................................................20

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................5

Part A: Conceptual Framework.......................................................................................................6

A: Review of Literature Regarding History and Development of Conceptual Framework for

Financial Reporting in the USA, UK, Australia..........................................................................6

B: Application of the IASB/IFRS Conceptual Framework for Financial Reporting...................7

C: Quality Concerns of the Conceptual Framework of Reporting...............................................8

D: Application of conceptual framework by Ingenia Communities Group.................................8

D(i): Financial Statements and their components........................................................................8

D (ii): Recognition principles and measurement basis used to present revenue, assets and

liabilities by Ingenia Communities Group...................................................................................9

D (iii): Qualitative characteristics of financial information used in financial report of Ingenia

Communities Group...................................................................................................................10

Part B: Integrated and sustainability reporting..............................................................................13

A: Comparison of GRI (Global Reporting Initiative) with International Integrated Reporting

Framework.................................................................................................................................13

B: Strengths and Limitations of the Conventional Accounting.................................................13

C: Applicability of Theories to Explain Content of Sustainability and Integrated Reporting...14

D: Evaluation of NEPI RockCastle (South African Company) on the grounds of different

components of integrated reporting through use of index (Table or check list)........................15

E: Comparison of reporting practice of selected Australian Company with the index and

reporting practices of selected South African company............................................................17

Conclusion.....................................................................................................................................19

Reference.......................................................................................................................................20

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The conceptual framework has been developed as per the normative theory of accounting

that has been developed for providing recommendations to the policy makers such as IASB

(International Accounting Standards Board) regarding the development of accounting policies on

the basis of theoretical principles. On the other hand, the term ‘Corporate Social Responsibility

Reporting’ or ‘sustainability reporting’ implies to satisfying information against social, economic

and environmental indicators of an organization. It requires business to provide adequate

disclosures about the ways in which their different operational activities are impacting the

abilities of future generations for meeting their varying needs. As such, this report has discussed

and analyzed various aspects related to conceptual framework and sustainability reporting with

including `examples from a selected Australian and South African entity.

5

The conceptual framework has been developed as per the normative theory of accounting

that has been developed for providing recommendations to the policy makers such as IASB

(International Accounting Standards Board) regarding the development of accounting policies on

the basis of theoretical principles. On the other hand, the term ‘Corporate Social Responsibility

Reporting’ or ‘sustainability reporting’ implies to satisfying information against social, economic

and environmental indicators of an organization. It requires business to provide adequate

disclosures about the ways in which their different operational activities are impacting the

abilities of future generations for meeting their varying needs. As such, this report has discussed

and analyzed various aspects related to conceptual framework and sustainability reporting with

including `examples from a selected Australian and South African entity.

5

Part A: Conceptual Framework

A: Review of Literature Regarding History and Development of Conceptual Framework

for Financial Reporting in the USA, UK, Australia

The Conceptual Framework (CF) has been applied by business entities across the world

complying with IASB or FASB for development of their financial reports. The development of

the conceptual framework in the USA can be traced back to early 1960s by the development of

Accounting Principles Board (APB). However, the accounting framework of the country has

received criticism on account of lack of an appropriate framework. As such, there has been the

development of Trueblood Committee in the year 1971 that produced Trueblood Report which

has outlined the accounting objectives and the required qualitative features to be present within

financial information. However, these initiatives undertaken have not led in improving the

quality of financial reporting system which leads to the replacement of APB by FASB. FASB

has then introduced CF into the financial reporting system of the US business entities by working

in co-operation with IASB and developing a revised conceptual framework in the year 2005

(Barth, 2008).

Similarly, in the UK there has been development of the Corporate Report in the year

1976 that has placed emphasis on meeting the rights of the users by providing them access to the

accurate financial information. However, the content provided by it is not accepted by the

accounting professionals. ASB in the UK has replaced by IASC (International Accounting

Standards Committee’s) but it was regarded as inconsistent with the US framework and thereby

finally replaced by the IASB framework and as such lead to the adoption of the CF (Macías and

Muiño, 2011).

The development of a coherent system of financial reporting was rather very slow in

Australia and here has been presence of only four accounting statement concepts that are,

defining reporting entity, stating the objectives of purpose of developing financial reports,

qualitative features of financial reports and recognition of varying elements of financial

statements (Chua, Chee and Cheong, 2012). The deficiencies in the reporting framework of

Australia have lead to the adoption of IASB CF as per the Financial Reporting Council decision

(Dean and Clarke, 2003). The IASB and FASB are working together in co-operation for

6

A: Review of Literature Regarding History and Development of Conceptual Framework

for Financial Reporting in the USA, UK, Australia

The Conceptual Framework (CF) has been applied by business entities across the world

complying with IASB or FASB for development of their financial reports. The development of

the conceptual framework in the USA can be traced back to early 1960s by the development of

Accounting Principles Board (APB). However, the accounting framework of the country has

received criticism on account of lack of an appropriate framework. As such, there has been the

development of Trueblood Committee in the year 1971 that produced Trueblood Report which

has outlined the accounting objectives and the required qualitative features to be present within

financial information. However, these initiatives undertaken have not led in improving the

quality of financial reporting system which leads to the replacement of APB by FASB. FASB

has then introduced CF into the financial reporting system of the US business entities by working

in co-operation with IASB and developing a revised conceptual framework in the year 2005

(Barth, 2008).

Similarly, in the UK there has been development of the Corporate Report in the year

1976 that has placed emphasis on meeting the rights of the users by providing them access to the

accurate financial information. However, the content provided by it is not accepted by the

accounting professionals. ASB in the UK has replaced by IASC (International Accounting

Standards Committee’s) but it was regarded as inconsistent with the US framework and thereby

finally replaced by the IASB framework and as such lead to the adoption of the CF (Macías and

Muiño, 2011).

The development of a coherent system of financial reporting was rather very slow in

Australia and here has been presence of only four accounting statement concepts that are,

defining reporting entity, stating the objectives of purpose of developing financial reports,

qualitative features of financial reports and recognition of varying elements of financial

statements (Chua, Chee and Cheong, 2012). The deficiencies in the reporting framework of

Australia have lead to the adoption of IASB CF as per the Financial Reporting Council decision

(Dean and Clarke, 2003). The IASB and FASB are working together in co-operation for

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

convergence of the accounting standards and developing a uniform set of accounting principles

and policies to improve comparability across the financial information. The project undertaken is

meant for global acceptance and adoption of CF by business entities worldwide (Seng, 2014).

B: Application of the IASB/IFRS Conceptual Framework for Financial Reporting

There has been increasing emphasis placed from various countries across the world for

driving improvement in the financial reporting through making it more comparable and useful in

decision-making. However, there have been various challenges faced by Australian entities to

comply with the conceptual framework of IASB are discussed as follows:

Gaining Understanding of the International Financial Reporting Practices

The main issue that is being faced in the Australian context relating to the framework of

IASB is that it involves many complexities and difficulties in the adoption phase. The

accountants need to be provided with relevant training for making them understand the ways of

implementing various accounting concepts as per the conceptual framework. It is difficult task

for the Australian businesses entities to providing understanding of IASB standards to the

accountants as it will incur higher cost and time (Wong, 2004).

Legal and Regulatory Issues

It has been stated by the Institute of Chartered Accountants in Australia (ICAA) that less

than half of the surveyed entities are able to adopt the conceptual framework of accounting. As

per the regulatory bodies such as CPA’s (Certified Public Accountants) and ICAA that

adherence to IFRS is posing difficulty among the business entities in Australia mainly due to

legal implications. The business entities have to bring major changes within their legal system in

order to comply with new legal systems and processes under the IASB standards. This may lead

to creating complications in the financial reporting system and therefore restricting business

entities to integrate IASB standards (AASB adoption of IASB standards by 2005, 2004).

Lack of Competent Accounting Professional

The limited availability of competent and experienced accounting professionals within

Australia is also posing a major challenge towards the integration of IFRS. They have to be

7

and policies to improve comparability across the financial information. The project undertaken is

meant for global acceptance and adoption of CF by business entities worldwide (Seng, 2014).

B: Application of the IASB/IFRS Conceptual Framework for Financial Reporting

There has been increasing emphasis placed from various countries across the world for

driving improvement in the financial reporting through making it more comparable and useful in

decision-making. However, there have been various challenges faced by Australian entities to

comply with the conceptual framework of IASB are discussed as follows:

Gaining Understanding of the International Financial Reporting Practices

The main issue that is being faced in the Australian context relating to the framework of

IASB is that it involves many complexities and difficulties in the adoption phase. The

accountants need to be provided with relevant training for making them understand the ways of

implementing various accounting concepts as per the conceptual framework. It is difficult task

for the Australian businesses entities to providing understanding of IASB standards to the

accountants as it will incur higher cost and time (Wong, 2004).

Legal and Regulatory Issues

It has been stated by the Institute of Chartered Accountants in Australia (ICAA) that less

than half of the surveyed entities are able to adopt the conceptual framework of accounting. As

per the regulatory bodies such as CPA’s (Certified Public Accountants) and ICAA that

adherence to IFRS is posing difficulty among the business entities in Australia mainly due to

legal implications. The business entities have to bring major changes within their legal system in

order to comply with new legal systems and processes under the IASB standards. This may lead

to creating complications in the financial reporting system and therefore restricting business

entities to integrate IASB standards (AASB adoption of IASB standards by 2005, 2004).

Lack of Competent Accounting Professional

The limited availability of competent and experienced accounting professionals within

Australia is also posing a major challenge towards the integration of IFRS. They have to be

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

provided with the knowledge of accounting policies and standards as per the IASB framework

(Lonergan, 2005).

C: Quality Concerns of the Conceptual Framework of Reporting

It can be examined by evaluation of the significant benefits and limitations associated

with the use of CF for reporting. The major benefits that are associated with its integration are

enhancing the uniformity and consistent in the financial reporting system across the world

(Silvia, 2016). It would lead in improving the international comparability of financial reporting

and also improve accountability to support the logical decision-making. As such, it would lead in

making standard-setters more accountable for the decision-making and assist them in

development right accounting policies (Fajard, 2016). The reduced need for developing a

separate framework for different countries would help in saving both time and costs for the

standard-setters. Also, its adoption would place emphasis on improving the decision-usefulness

of the financial reporting system rather than previous frameworks that placed importance on

achieving stewardship. It has also enhanced the ability of the standard-setters for regulating the

financial reporting and reduces the role of government intervention (Tschopp and Nastanski,

2014). However, the benefits can be outweighed by thee significant limitations that are

associated with its adoption. The major drawback is that is has placed importance on enhancing

economic performance as compared to social performance of entities. Also, it is highly

troublesome for small and medium-sized entities to comply adequately with all the reporting

requirements due to constraints of financial resources. Therefore, it is essential to compared both

benefits and costs associated with the CF before its implementation (Pacter, 2013).

D: Application of conceptual framework by Ingenia Communities Group

D (i): Financial Statements and their components

According to conceptual framework, entities are required to provide information about

five major elements and they are assets, liabilities, income, expenses and equity. In addition to

this entities are required to provide information in equity balance has been increased or decrease

during the year. So following financial statements have been prepared by Ingenia Communities

Group:

8

(Lonergan, 2005).

C: Quality Concerns of the Conceptual Framework of Reporting

It can be examined by evaluation of the significant benefits and limitations associated

with the use of CF for reporting. The major benefits that are associated with its integration are

enhancing the uniformity and consistent in the financial reporting system across the world

(Silvia, 2016). It would lead in improving the international comparability of financial reporting

and also improve accountability to support the logical decision-making. As such, it would lead in

making standard-setters more accountable for the decision-making and assist them in

development right accounting policies (Fajard, 2016). The reduced need for developing a

separate framework for different countries would help in saving both time and costs for the

standard-setters. Also, its adoption would place emphasis on improving the decision-usefulness

of the financial reporting system rather than previous frameworks that placed importance on

achieving stewardship. It has also enhanced the ability of the standard-setters for regulating the

financial reporting and reduces the role of government intervention (Tschopp and Nastanski,

2014). However, the benefits can be outweighed by thee significant limitations that are

associated with its adoption. The major drawback is that is has placed importance on enhancing

economic performance as compared to social performance of entities. Also, it is highly

troublesome for small and medium-sized entities to comply adequately with all the reporting

requirements due to constraints of financial resources. Therefore, it is essential to compared both

benefits and costs associated with the CF before its implementation (Pacter, 2013).

D: Application of conceptual framework by Ingenia Communities Group

D (i): Financial Statements and their components

According to conceptual framework, entities are required to provide information about

five major elements and they are assets, liabilities, income, expenses and equity. In addition to

this entities are required to provide information in equity balance has been increased or decrease

during the year. So following financial statements have been prepared by Ingenia Communities

Group:

8

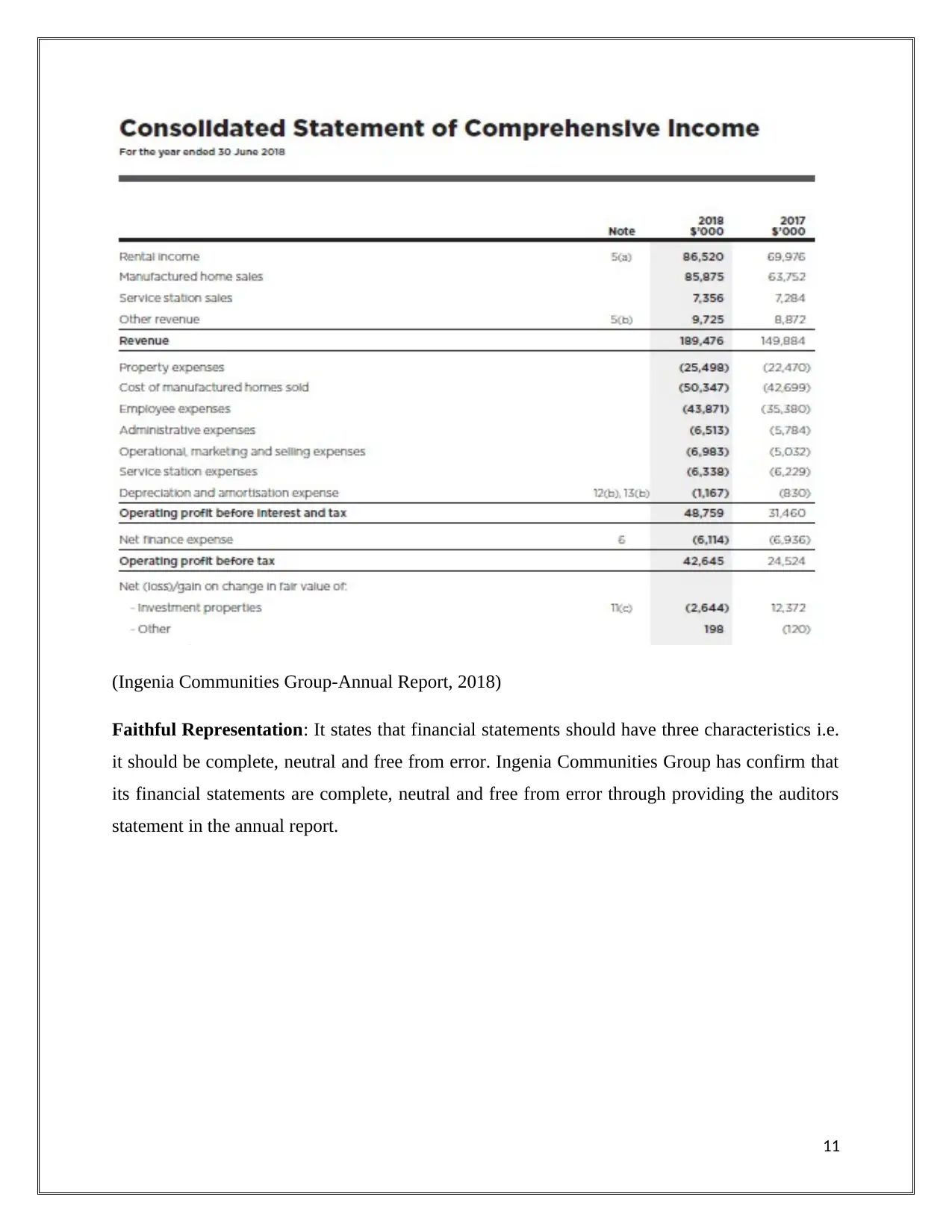

Consolidated Income statement (Statement of financial performance): This statement is

prepared to provide the details of income and expenses of the parent company as well as

its entire subsidiaries.

Consolidated Balance Sheet (Statement of financial Position): This statement provides all

the details of recognised assets and liabilities. Notes to financial statements provide

information on how they are recognised and estimated.

Consolidated cash flow statement: This statement provides information on cash flows

during the years from the operations, investment and financing activities.

Consolidated statement of change in Equity: This statement provides information on all

the contributions made by the holders of equity shares and any distribution to them.

The major components that have been included in the financial statements prepared by

Ingenia Communities Group are assets, liabilities, equity, income and expenses. Assets include

current assets and non-current liabilities, liabilities include current and non-current liabilities

(Ingenia Communities Group-Annual Report, 2018).

D (ii): Recognition principles and measurement basis used to present revenue, assets and

liabilities by Ingenia Communities Group

Revenue: The major sources of revenue for Ingenia Communities Group rent, interest

and distributions. All these revenue has been recognised to the level it is probable that the

economic benefits will flow and has already received to entity. Another criterion of

recognition is that revenue must be reliably measurable. Revenue that has not been

received till the balance sheet date is shown as accounts receivables under current assets

section. Interest income is recognised through using the effective interest rate method and

rental income is recognised through using straight line basis over the operating lease

term.

Assets: Inventory is measured at lower of cost and net realizable value. Inventory is

recognised when it is physical present with the company and it has some market value on

the date of balance sheet. Cash & cash equivalent includes cash in hand, cash at bank and

short term deposits that are readily convertible into cash in short period of time. Cash and

cash equivalent are easily measurable and have fixed value as on balance sheet date.

Company derives major part of the income from the investment properties that includes

9

prepared to provide the details of income and expenses of the parent company as well as

its entire subsidiaries.

Consolidated Balance Sheet (Statement of financial Position): This statement provides all

the details of recognised assets and liabilities. Notes to financial statements provide

information on how they are recognised and estimated.

Consolidated cash flow statement: This statement provides information on cash flows

during the years from the operations, investment and financing activities.

Consolidated statement of change in Equity: This statement provides information on all

the contributions made by the holders of equity shares and any distribution to them.

The major components that have been included in the financial statements prepared by

Ingenia Communities Group are assets, liabilities, equity, income and expenses. Assets include

current assets and non-current liabilities, liabilities include current and non-current liabilities

(Ingenia Communities Group-Annual Report, 2018).

D (ii): Recognition principles and measurement basis used to present revenue, assets and

liabilities by Ingenia Communities Group

Revenue: The major sources of revenue for Ingenia Communities Group rent, interest

and distributions. All these revenue has been recognised to the level it is probable that the

economic benefits will flow and has already received to entity. Another criterion of

recognition is that revenue must be reliably measurable. Revenue that has not been

received till the balance sheet date is shown as accounts receivables under current assets

section. Interest income is recognised through using the effective interest rate method and

rental income is recognised through using straight line basis over the operating lease

term.

Assets: Inventory is measured at lower of cost and net realizable value. Inventory is

recognised when it is physical present with the company and it has some market value on

the date of balance sheet. Cash & cash equivalent includes cash in hand, cash at bank and

short term deposits that are readily convertible into cash in short period of time. Cash and

cash equivalent are easily measurable and have fixed value as on balance sheet date.

Company derives major part of the income from the investment properties that includes

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

land & buildings, building under construction, and other amenities. Investment properties

are measured initial at cost and after that they are measured at fair value. They are

recognised when properties come into existence and their value can be determined.

Intangible assets initial recognised at total expenditures occurred for the development of

intangible assets. Subsequently they are measured at cost less accumulated depreciation.

Liabilities: Trade payables and other payable are recognised when it is probable that

economic benefits will flow out from entity and they are measured amortized cost.

Borrowings are recognised initially at fair value of amount received less any transactions

cost and after that they are measured at amortized cost (Ingenia Communities Group-

Annual Report, 2018).

D (iii): Qualitative characteristics of financial information used in financial report of

Ingenia Communities Group

Relevance: Relevance states that financial information should have capability to influence the

economic decision of users which means that it should possess predictive and confirmative

value. For example, Ingenia Communities Group has provided revenue as the financial element

that has ability to impact the decision of users regarding the past and future performance of the

company.

10

are measured initial at cost and after that they are measured at fair value. They are

recognised when properties come into existence and their value can be determined.

Intangible assets initial recognised at total expenditures occurred for the development of

intangible assets. Subsequently they are measured at cost less accumulated depreciation.

Liabilities: Trade payables and other payable are recognised when it is probable that

economic benefits will flow out from entity and they are measured amortized cost.

Borrowings are recognised initially at fair value of amount received less any transactions

cost and after that they are measured at amortized cost (Ingenia Communities Group-

Annual Report, 2018).

D (iii): Qualitative characteristics of financial information used in financial report of

Ingenia Communities Group

Relevance: Relevance states that financial information should have capability to influence the

economic decision of users which means that it should possess predictive and confirmative

value. For example, Ingenia Communities Group has provided revenue as the financial element

that has ability to impact the decision of users regarding the past and future performance of the

company.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

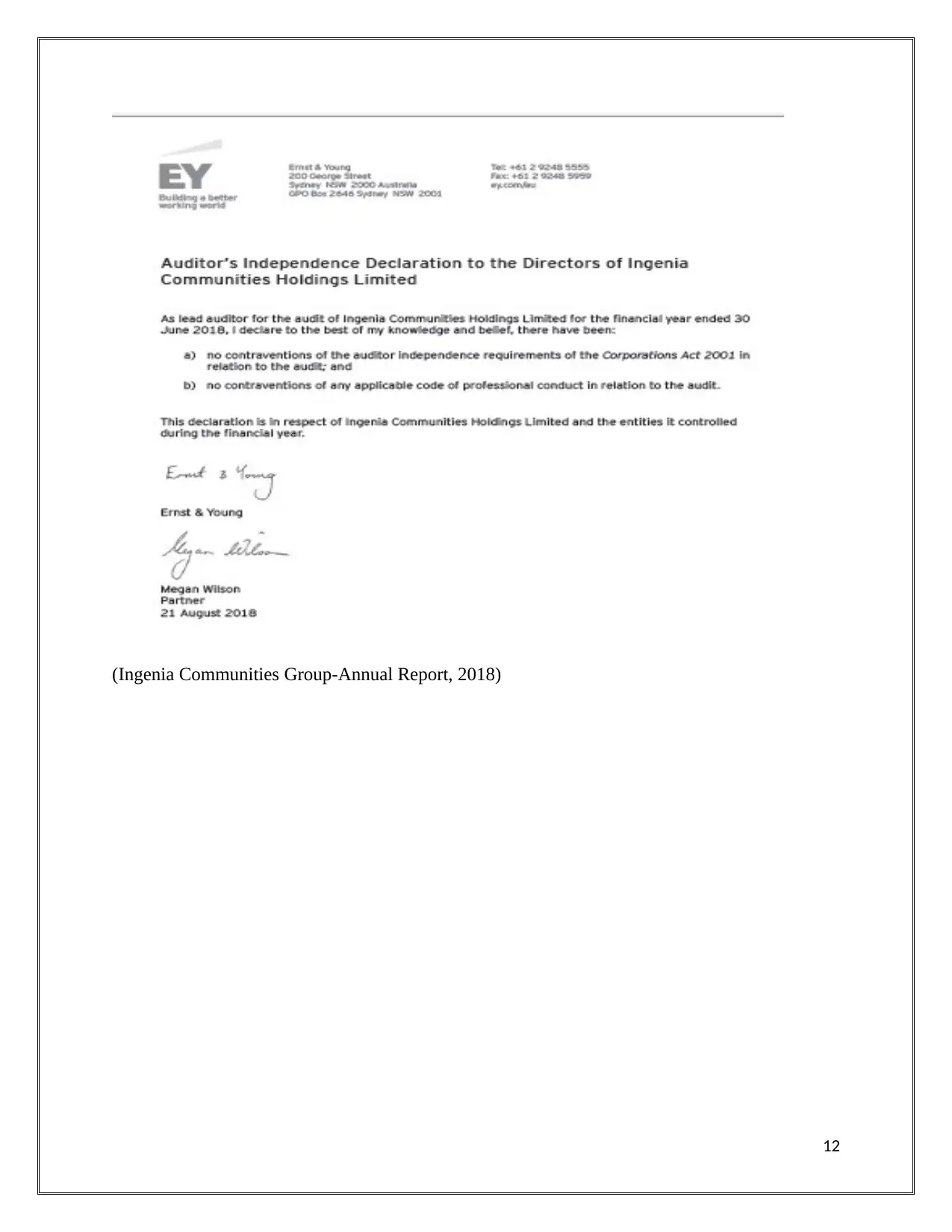

(Ingenia Communities Group-Annual Report, 2018)

Faithful Representation: It states that financial statements should have three characteristics i.e.

it should be complete, neutral and free from error. Ingenia Communities Group has confirm that

its financial statements are complete, neutral and free from error through providing the auditors

statement in the annual report.

11

Faithful Representation: It states that financial statements should have three characteristics i.e.

it should be complete, neutral and free from error. Ingenia Communities Group has confirm that

its financial statements are complete, neutral and free from error through providing the auditors

statement in the annual report.

11

(Ingenia Communities Group-Annual Report, 2018)

12

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.