Financial Reporting Report: Goodman Group Hedge Accounting Analysis

VerifiedAdded on 2022/11/17

|11

|2026

|141

Report

AI Summary

This report provides a comprehensive analysis of the Goodman Group's financial reporting practices, specifically focusing on hedge accounting. It examines the company's use of derivative instruments to mitigate foreign currency and interest rate risks, detailing the qualifying criteria for hedge accounting as adopted by the company. The report explores the advantages and disadvantages of hedge accounting, including its impact on financial statements, and the measurement of hedge instruments and hedged items. Furthermore, the report references relevant Australian Accounting Standards (AASB) to support its findings, providing a detailed understanding of the company's approach to managing financial risks and presenting financial information.

Student Name

UNIVERSITY NAME | AUSTRALIA

FINANCIAL

REPORTING

ACC00145 2019 S1

UNIVERSITY NAME | AUSTRALIA

FINANCIAL

REPORTING

ACC00145 2019 S1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

By student name

Professor

University

Date:

Professor

University

Date:

Executive Summary

This report is prepared on one of the listed companies which is using Hedge Accounting in the

financial statements. The company under consideration is Goodman Group of companies. It is an

Australian company. The report elucidates the concept of hedge accounting and its implementation

in the books of accounts. The report is also explaining the way the Goodman Group has adopted the

hedge and its qualifying criteria. One can also find the pros and cons of hedge accounting in this

report. It focuses on the measurement of hedge instruments and the hedged items in the company’s

books of accounts. To validate the facts shared in the report, relevant paragraphs from Australian

Accounting Standards have been cited in it.

-

Contents

This report is prepared on one of the listed companies which is using Hedge Accounting in the

financial statements. The company under consideration is Goodman Group of companies. It is an

Australian company. The report elucidates the concept of hedge accounting and its implementation

in the books of accounts. The report is also explaining the way the Goodman Group has adopted the

hedge and its qualifying criteria. One can also find the pros and cons of hedge accounting in this

report. It focuses on the measurement of hedge instruments and the hedged items in the company’s

books of accounts. To validate the facts shared in the report, relevant paragraphs from Australian

Accounting Standards have been cited in it.

-

Contents

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction...........................................................................................................................................5

Discussion and Analysis.........................................................................................................................5

Hedge Presented in Annual Report and Qualifying Criteria Adopted by the company......................5

Advantages and Disadvantages of Hedge Accounting.......................................................................9

Measurement of Hedge Instrument and the hedged item in the company......................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Discussion and Analysis.........................................................................................................................5

Hedge Presented in Annual Report and Qualifying Criteria Adopted by the company......................5

Advantages and Disadvantages of Hedge Accounting.......................................................................9

Measurement of Hedge Instrument and the hedged item in the company......................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The Goodman group, the company which has been selected for analysis is listed on the Australian

Stock Exchange (ASX), is being considered for analysis here. It is an Australian based company mainly

known as global industrial property hub. It deals in owning, developing and managing modern and

industrial real estate. It also includes warehousing and logistics facilities and business parks in

strategic locations. To meet the growing demand and supply across the world the Goodman

properties are located close to urban centres so one can easily access to large number of consumers

and ports, airports. The company carries on its business in 17 different countries (Arnott, et al.,

2017). During the current year the invested in heavily in the industrial property and investment

management as well as property development and services. It supported charities around the globe

for the health, safety and wellbeing of children. It provides physical space, helping in operations and

purchasing equipment and other services. The company has progressed over the past few years

through its subsidiaries Goodman Industrial Trust (GIT) and Goodman Logistics (HK) Limited (GLHK)

and other acquisitions.

A Hedge is the financial instrument just like taking an insurance policy to cover the risk of negative

price movements in an asset and fluctuations in the exchange rates. The companies use this

instrument of hedging to minimize or offset the risk of loss of value of asset in the future. It takes the

counteract position with respect to given security. For example if anyone takes house near seashore.

That person has to take insurance policy to cover the loss in case of flood or tsunami as he cannot

control or stop the natural calamity (Bromwich & Scapens, 2016). The act he has done is popularly

known as hedging. Hedging helps the investors and money managers in reducing the risk. The

examples of hedging instruments are options and swaps, forward and future contracts, interest rate

swaps, derivative contracts and money market operations. The same is directed in AASB 7, AASB 9,

AASB 101, AASB 132 and AASB 139 among the Australian accounting standards.

Discussion and Analysis

Hedge Presented in Annual Report and Qualifying Criteria Adopted by the

company

The group has foreign currency risk as it provides services to many countries which are to be

received in foreign currency. The group has derivative financial instruments to minimise the risk of

earning less due to exchange rate fluctuations. As per company’s policy, whenever the Group makes

an investment in the foreign assets, it either goes for borrowing in that currency or enters into

derivative instruments so that a corresponding liability is being created. In this process, the company

is able to reduce its net assets and risk or exposure to the respective foreign currencies (Glaum &

Klocker, 2011). The unrealised portion of the fair value movement on account of the derivative

financial instruments is charged to the profit and loss account whereas the translation on account of

the hedged net investment is reflected in the reserves in the balance sheet. As per the practice of

the company, it hedges approximately 65% to 90% of the foreign assets balance and operations.

The Goodman group, the company which has been selected for analysis is listed on the Australian

Stock Exchange (ASX), is being considered for analysis here. It is an Australian based company mainly

known as global industrial property hub. It deals in owning, developing and managing modern and

industrial real estate. It also includes warehousing and logistics facilities and business parks in

strategic locations. To meet the growing demand and supply across the world the Goodman

properties are located close to urban centres so one can easily access to large number of consumers

and ports, airports. The company carries on its business in 17 different countries (Arnott, et al.,

2017). During the current year the invested in heavily in the industrial property and investment

management as well as property development and services. It supported charities around the globe

for the health, safety and wellbeing of children. It provides physical space, helping in operations and

purchasing equipment and other services. The company has progressed over the past few years

through its subsidiaries Goodman Industrial Trust (GIT) and Goodman Logistics (HK) Limited (GLHK)

and other acquisitions.

A Hedge is the financial instrument just like taking an insurance policy to cover the risk of negative

price movements in an asset and fluctuations in the exchange rates. The companies use this

instrument of hedging to minimize or offset the risk of loss of value of asset in the future. It takes the

counteract position with respect to given security. For example if anyone takes house near seashore.

That person has to take insurance policy to cover the loss in case of flood or tsunami as he cannot

control or stop the natural calamity (Bromwich & Scapens, 2016). The act he has done is popularly

known as hedging. Hedging helps the investors and money managers in reducing the risk. The

examples of hedging instruments are options and swaps, forward and future contracts, interest rate

swaps, derivative contracts and money market operations. The same is directed in AASB 7, AASB 9,

AASB 101, AASB 132 and AASB 139 among the Australian accounting standards.

Discussion and Analysis

Hedge Presented in Annual Report and Qualifying Criteria Adopted by the

company

The group has foreign currency risk as it provides services to many countries which are to be

received in foreign currency. The group has derivative financial instruments to minimise the risk of

earning less due to exchange rate fluctuations. As per company’s policy, whenever the Group makes

an investment in the foreign assets, it either goes for borrowing in that currency or enters into

derivative instruments so that a corresponding liability is being created. In this process, the company

is able to reduce its net assets and risk or exposure to the respective foreign currencies (Glaum &

Klocker, 2011). The unrealised portion of the fair value movement on account of the derivative

financial instruments is charged to the profit and loss account whereas the translation on account of

the hedged net investment is reflected in the reserves in the balance sheet. As per the practice of

the company, it hedges approximately 65% to 90% of the foreign assets balance and operations.

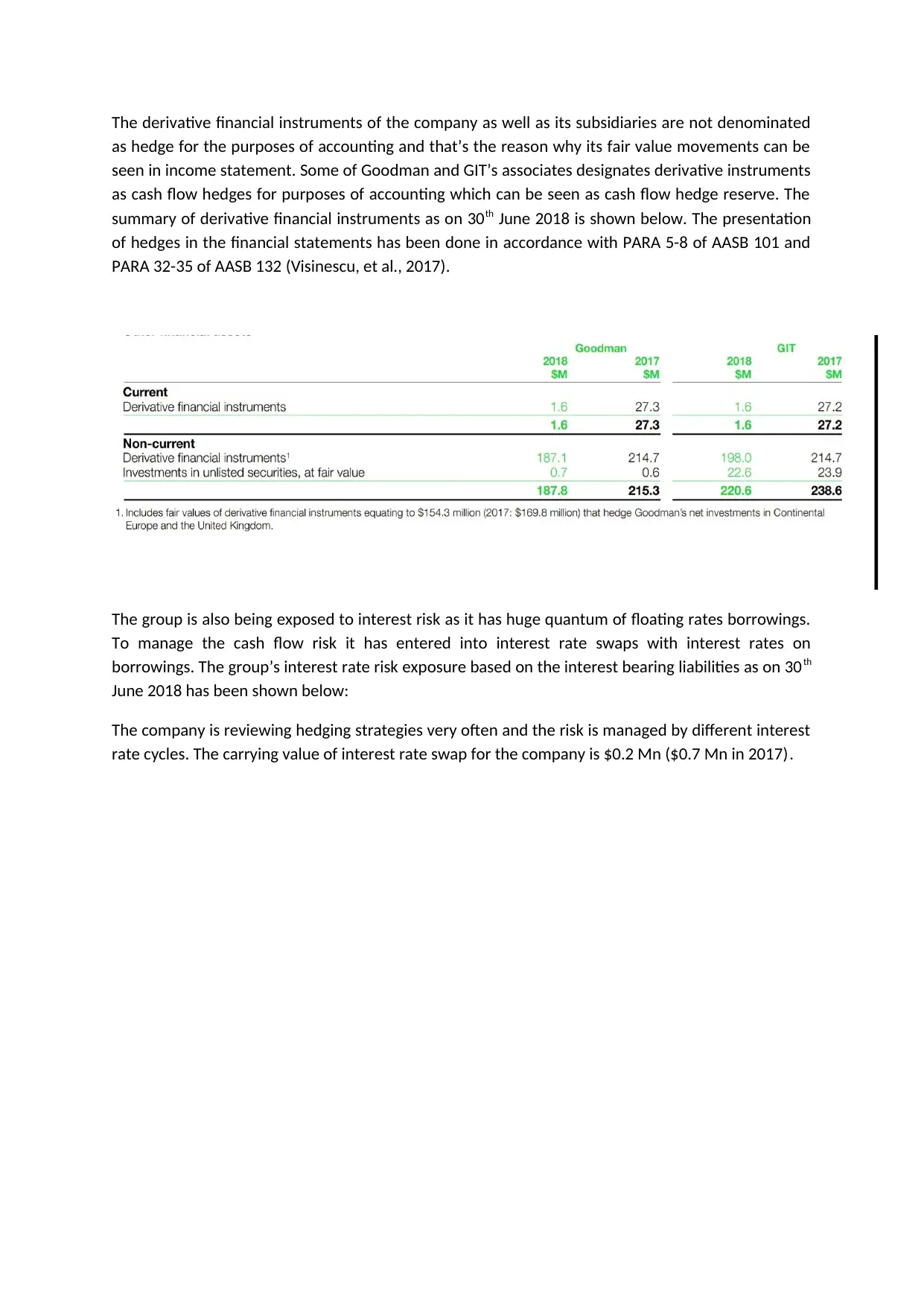

The derivative financial instruments of the company as well as its subsidiaries are not denominated

as hedge for the purposes of accounting and that’s the reason why its fair value movements can be

seen in income statement. Some of Goodman and GIT’s associates designates derivative instruments

as cash flow hedges for purposes of accounting which can be seen as cash flow hedge reserve. The

summary of derivative financial instruments as on 30th June 2018 is shown below. The presentation

of hedges in the financial statements has been done in accordance with PARA 5-8 of AASB 101 and

PARA 32-35 of AASB 132 (Visinescu, et al., 2017).

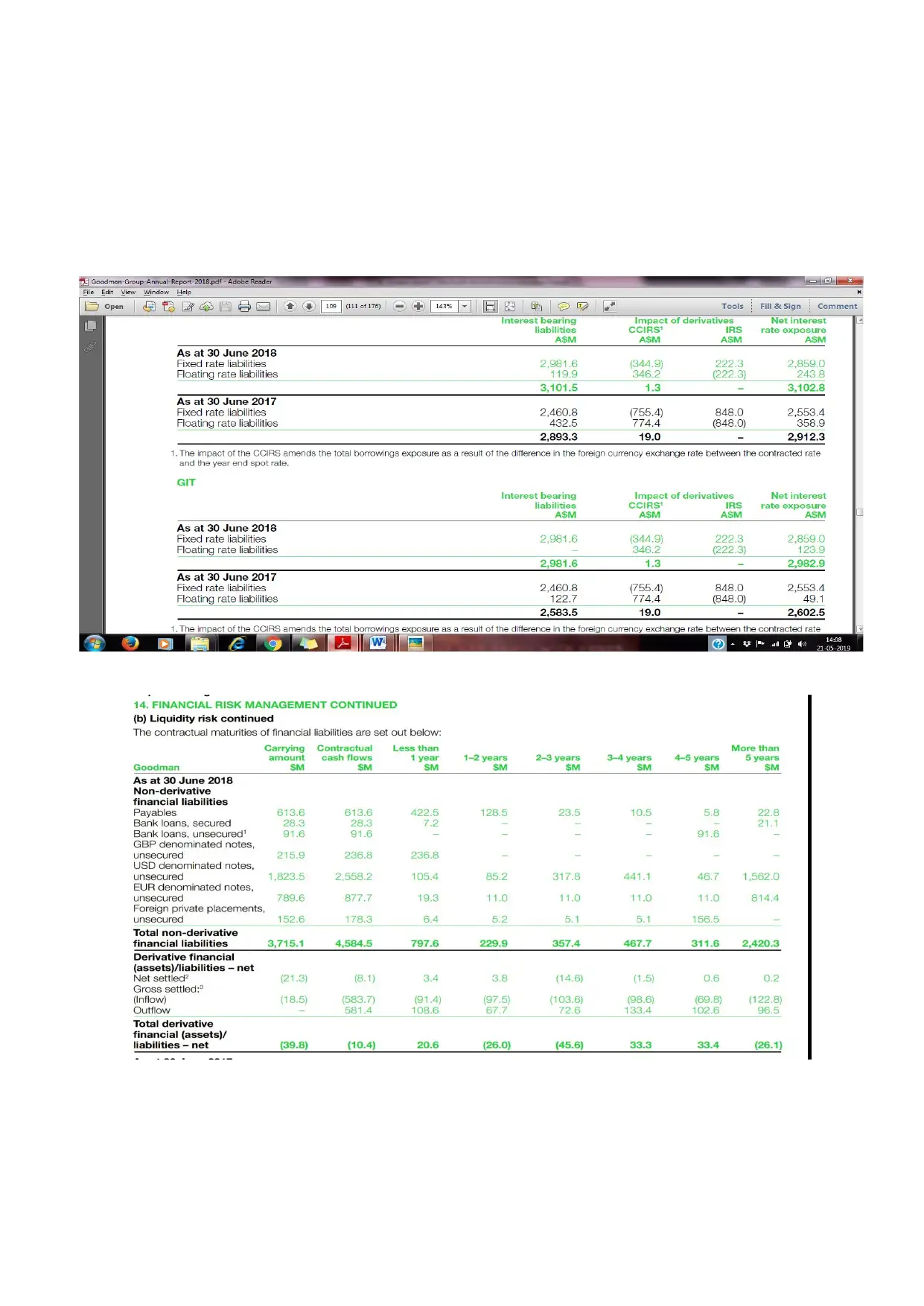

The group is also being exposed to interest risk as it has huge quantum of floating rates borrowings.

To manage the cash flow risk it has entered into interest rate swaps with interest rates on

borrowings. The group’s interest rate risk exposure based on the interest bearing liabilities as on 30th

June 2018 has been shown below:

The company is reviewing hedging strategies very often and the risk is managed by different interest

rate cycles. The carrying value of interest rate swap for the company is $0.2 Mn ($0.7 Mn in 2017).

as hedge for the purposes of accounting and that’s the reason why its fair value movements can be

seen in income statement. Some of Goodman and GIT’s associates designates derivative instruments

as cash flow hedges for purposes of accounting which can be seen as cash flow hedge reserve. The

summary of derivative financial instruments as on 30th June 2018 is shown below. The presentation

of hedges in the financial statements has been done in accordance with PARA 5-8 of AASB 101 and

PARA 32-35 of AASB 132 (Visinescu, et al., 2017).

The group is also being exposed to interest risk as it has huge quantum of floating rates borrowings.

To manage the cash flow risk it has entered into interest rate swaps with interest rates on

borrowings. The group’s interest rate risk exposure based on the interest bearing liabilities as on 30th

June 2018 has been shown below:

The company is reviewing hedging strategies very often and the risk is managed by different interest

rate cycles. The carrying value of interest rate swap for the company is $0.2 Mn ($0.7 Mn in 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

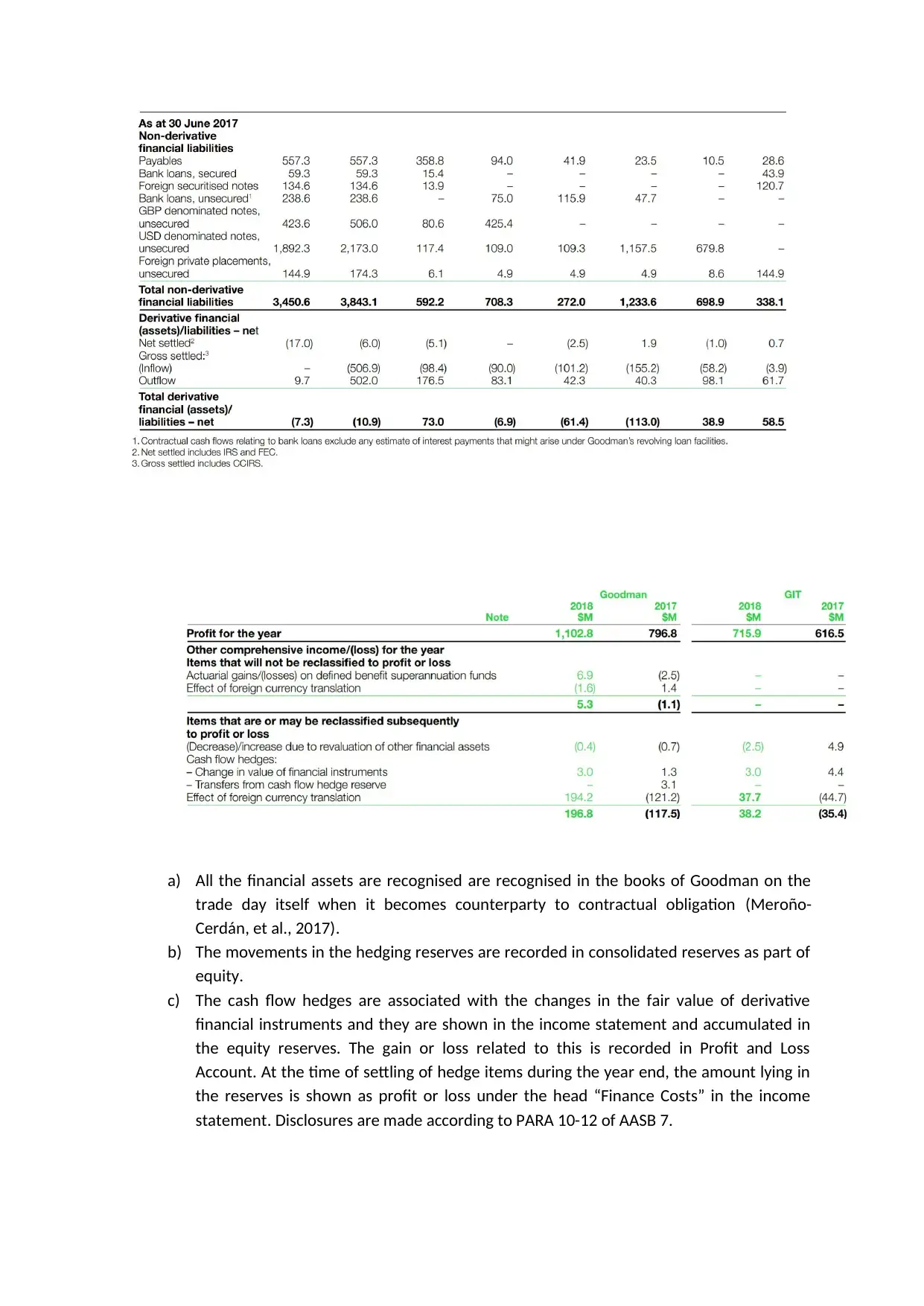

a) All the financial assets are recognised are recognised in the books of Goodman on the

trade day itself when it becomes counterparty to contractual obligation (Meroño-

Cerdán, et al., 2017).

b) The movements in the hedging reserves are recorded in consolidated reserves as part of

equity.

c) The cash flow hedges are associated with the changes in the fair value of derivative

financial instruments and they are shown in the income statement and accumulated in

the equity reserves. The gain or loss related to this is recorded in Profit and Loss

Account. At the time of settling of hedge items during the year end, the amount lying in

the reserves is shown as profit or loss under the head “Finance Costs” in the income

statement. Disclosures are made according to PARA 10-12 of AASB 7.

trade day itself when it becomes counterparty to contractual obligation (Meroño-

Cerdán, et al., 2017).

b) The movements in the hedging reserves are recorded in consolidated reserves as part of

equity.

c) The cash flow hedges are associated with the changes in the fair value of derivative

financial instruments and they are shown in the income statement and accumulated in

the equity reserves. The gain or loss related to this is recorded in Profit and Loss

Account. At the time of settling of hedge items during the year end, the amount lying in

the reserves is shown as profit or loss under the head “Finance Costs” in the income

statement. Disclosures are made according to PARA 10-12 of AASB 7.

Advantages and Disadvantages of Hedge Accounting

The use of hedges provides multiple advantages to the company in question here. As per the policy

of the company, in order to minimise the risk of the foreign currency as well as exchange

movements, it enters into derivatives for both USD/EUR and USD/GBP – which provides the capital

hedge to the company for all those assets which are denominates in GBP or EUR. Thus, it provides

adequate security to the value of capital assets here (Das, 2017).

The company also has a policy of 60% to 100% of the interest expenses exposure due to the change

in the interest rates is on fixed rate basis and the same is also hedged to minimise the risk.

Some of the disadvantages of using the hedging instruments is that the company might also face the

opportunity loss in case the market works in the opposite direction. Furthermore the company also

has to pay a lot of hedging fees and premium considering the hedging instruments it enters into

cover all its foreign assets. It has not been mentioned if the company is using derivatives which are

traded on the exchange or which are traded on counter (Timothy, 2004). The one which is trade on

counter can be risky as there are huge chances of counterparty default. Since it needs expertise on

the subject, the company may also need to bear cost on knowledge on this niche skill. It also cuts

short the opportunity of the company to gain in the highly volatile market.

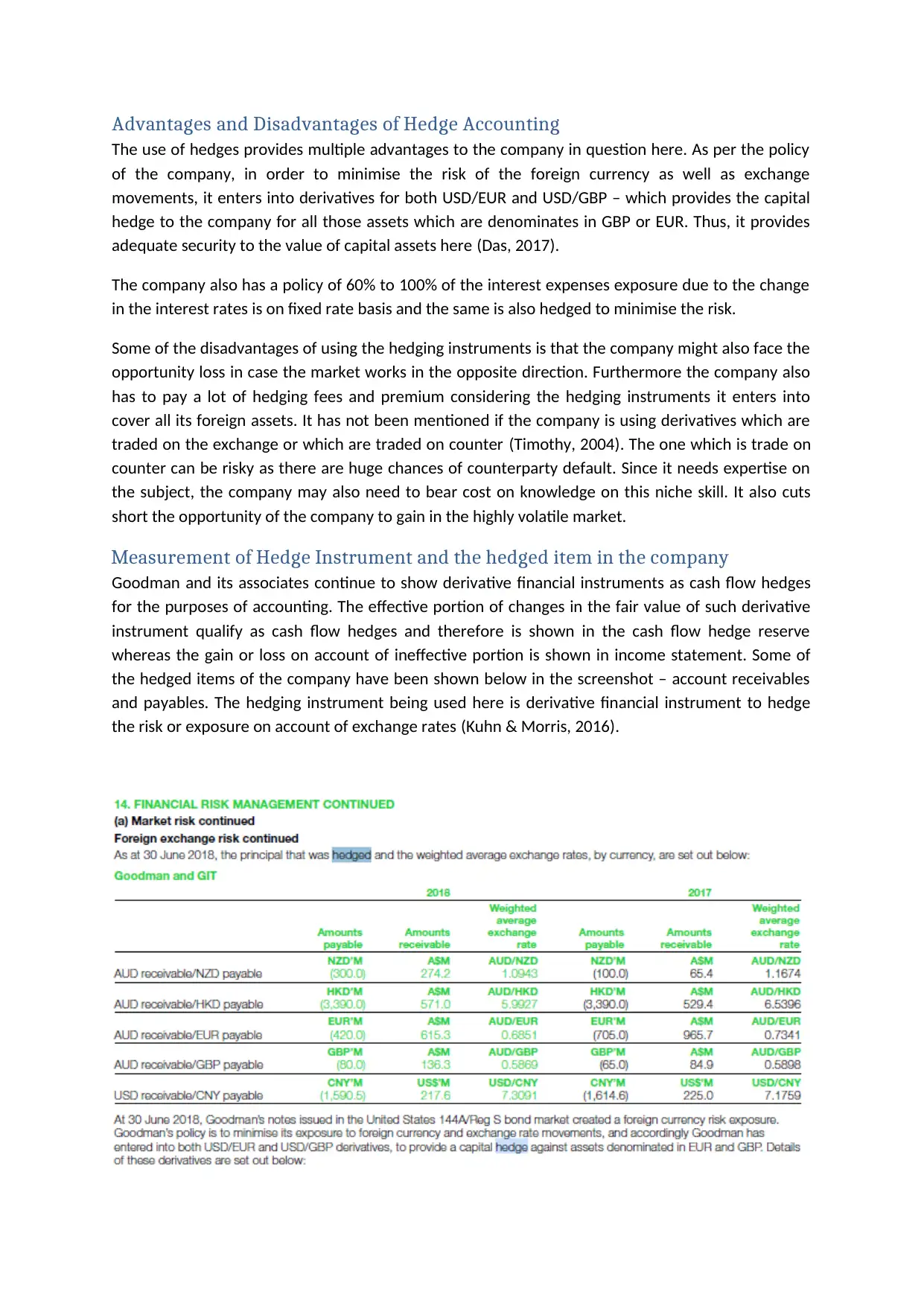

Measurement of Hedge Instrument and the hedged item in the company

Goodman and its associates continue to show derivative financial instruments as cash flow hedges

for the purposes of accounting. The effective portion of changes in the fair value of such derivative

instrument qualify as cash flow hedges and therefore is shown in the cash flow hedge reserve

whereas the gain or loss on account of ineffective portion is shown in income statement. Some of

the hedged items of the company have been shown below in the screenshot – account receivables

and payables. The hedging instrument being used here is derivative financial instrument to hedge

the risk or exposure on account of exchange rates (Kuhn & Morris, 2016).

The use of hedges provides multiple advantages to the company in question here. As per the policy

of the company, in order to minimise the risk of the foreign currency as well as exchange

movements, it enters into derivatives for both USD/EUR and USD/GBP – which provides the capital

hedge to the company for all those assets which are denominates in GBP or EUR. Thus, it provides

adequate security to the value of capital assets here (Das, 2017).

The company also has a policy of 60% to 100% of the interest expenses exposure due to the change

in the interest rates is on fixed rate basis and the same is also hedged to minimise the risk.

Some of the disadvantages of using the hedging instruments is that the company might also face the

opportunity loss in case the market works in the opposite direction. Furthermore the company also

has to pay a lot of hedging fees and premium considering the hedging instruments it enters into

cover all its foreign assets. It has not been mentioned if the company is using derivatives which are

traded on the exchange or which are traded on counter (Timothy, 2004). The one which is trade on

counter can be risky as there are huge chances of counterparty default. Since it needs expertise on

the subject, the company may also need to bear cost on knowledge on this niche skill. It also cuts

short the opportunity of the company to gain in the highly volatile market.

Measurement of Hedge Instrument and the hedged item in the company

Goodman and its associates continue to show derivative financial instruments as cash flow hedges

for the purposes of accounting. The effective portion of changes in the fair value of such derivative

instrument qualify as cash flow hedges and therefore is shown in the cash flow hedge reserve

whereas the gain or loss on account of ineffective portion is shown in income statement. Some of

the hedged items of the company have been shown below in the screenshot – account receivables

and payables. The hedging instrument being used here is derivative financial instrument to hedge

the risk or exposure on account of exchange rates (Kuhn & Morris, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Another hedged item here is the interest bearing liabilities of the company which is done using the

interest rate swaps and it helps in reducing the interest rate risk or exposure on the floating rate

debt. The company follows HKAS 39 for the recognition and measurement of the financial

instruments as of now which will be replaced by HKFRS 9 from financial statements prepared on 30 th

June 2019 (Oberoi, 2018).

Conclusion

The company has been following the accounting standards and the conceptual framework while

accounting and reporting for hedges in the financial instruments – with respect to presentation of

financial instruments, its recognition and measurement and the disclosures on account of the same.

It can also be said that the policy of the company to hedge the exposure for foreign currency,

interest rates and foreign assets has been beneficial to the company.

References

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in organizations.

Decision Support Systems, Volume 97, pp. 58-68.

Bromwich, M. & Scapens, R., 2016. Management Accounting Research: 25 years on. Management

Accounting Research, 31(1), pp. 1-9.

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social

Science Studies, 2(2), pp. 10-17.

Glaum, M. & Klocker, A., 2011. Hedge accounting and its influence on financial hedging: when the

tail wags the dog. Accounting and Business Research, 41(5), pp. 459-489.

Kuhn, J. & Morris, B., 2016. IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

Oberoi, J., 2018. Interest rate risk management and the mix of fixed and floating rate debt. Journal of

Banking and Finance, 86(3), pp. 70-86.

interest rate swaps and it helps in reducing the interest rate risk or exposure on the floating rate

debt. The company follows HKAS 39 for the recognition and measurement of the financial

instruments as of now which will be replaced by HKFRS 9 from financial statements prepared on 30 th

June 2019 (Oberoi, 2018).

Conclusion

The company has been following the accounting standards and the conceptual framework while

accounting and reporting for hedges in the financial instruments – with respect to presentation of

financial instruments, its recognition and measurement and the disclosures on account of the same.

It can also be said that the policy of the company to hedge the exposure for foreign currency,

interest rates and foreign assets has been beneficial to the company.

References

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in organizations.

Decision Support Systems, Volume 97, pp. 58-68.

Bromwich, M. & Scapens, R., 2016. Management Accounting Research: 25 years on. Management

Accounting Research, 31(1), pp. 1-9.

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social

Science Studies, 2(2), pp. 10-17.

Glaum, M. & Klocker, A., 2011. Hedge accounting and its influence on financial hedging: when the

tail wags the dog. Accounting and Business Research, 41(5), pp. 459-489.

Kuhn, J. & Morris, B., 2016. IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

Oberoi, J., 2018. Interest rate risk management and the mix of fixed and floating rate debt. Journal of

Banking and Finance, 86(3), pp. 70-86.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Timothy, G., 2004. Managing interest rate risk in a rising rate environment. RMA Journal, Risk

Management Association (RMA), 3(1), pp. 29-41.

Visinescu, L., Jones, M. & Sidorova, A., 2017. Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), pp. 58-66.

Management Association (RMA), 3(1), pp. 29-41.

Visinescu, L., Jones, M. & Sidorova, A., 2017. Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), pp. 58-66.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.