Financial Reporting: Principles, Statements, GSK Analysis, and IFRS

VerifiedAdded on 2020/06/06

|13

|3085

|50

Report

AI Summary

This report delves into the core aspects of financial reporting, commencing with an introduction to its fundamental role in organizations and its objectives, such as aiding decision-making and providing economic information. It then explores the frameworks and key principles underpinning financial reporting, including expense, cost, and revenue principles, alongside qualitative and quantitative considerations. The report identifies key stakeholders, like managers, employees, and investors, and examines the benefits they derive from financial information. It emphasizes the importance of financial reporting for meeting organizational objectives and fostering growth. The report presents key financial statements, including the statement of profit and loss, statements of changes in equity, and the statement of financial position, derived from provided financial data. It also details the information involved in cash flow statements, comparing it with income statements and balance sheets. A significant portion of the report is dedicated to analyzing the financial performance of Glaxo Smith Kline (GSK) using financial ratios. The report concludes by differentiating between IAS and IFRS, highlighting the benefits of IFRS for organizations. The report provides a comprehensive overview of financial reporting, offering valuable insights into its principles, practices, and applications.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financials are one of the essential aspect for every company in which different

information involved like cost, profit, expenses, payments etc. Process in which financial

statements are framed and then published among all internal and external stakeholders is

considered as financial reporting. The current project shows about objectives of the financial

reporting along with its basis principles used for completing this specific procedure. Apart from

this, with the help of Trial balance of Rita Plc Basic financial statements are prepared for the

year ended 31st December 2016. The study reflects on the business performance of Glaxo Smith

Kline (GSK) enterprise from accounting year 2016 to 2016. Besides these, difference among IAS

and IFRS is shown along with benefits of IFRS for an organisation.

1. Context as well as objectives of financial reporting

When the company uses financial reporting in the workplace then become beneficial

different ways. Further, its several objectives are mentioned below:

Key purpose of the financial reporting is to provide those kinds of information to the

company which helps to make an effective decision.

It helps to the management and investors both in order to assess or track cash availability

within the workplace. On the basis of this, creditors and suppliers also make fruitful

decision towards the company (Objectives of financial reporting, 2015).

Information related to the economic sources of the company also provided by financial

reporting. Such information include liabilities, equity of owner etc.

Another objective of financial reporting is to provide statutory auditing information

which becomes change with facilitates audit.

For identifying various scandals and malpractices incurred within financial statements

and resolving them the financial reporting is an important aspect.

2. Evaluating different framework and its key principles

In the financial reporting various frameworks included which regulate to the whole

process and amend required changes. On the basis of this, the management able to prepare

financials and publish in the market using legal rules. Further, any of the stakeholder easily able

1

Financials are one of the essential aspect for every company in which different

information involved like cost, profit, expenses, payments etc. Process in which financial

statements are framed and then published among all internal and external stakeholders is

considered as financial reporting. The current project shows about objectives of the financial

reporting along with its basis principles used for completing this specific procedure. Apart from

this, with the help of Trial balance of Rita Plc Basic financial statements are prepared for the

year ended 31st December 2016. The study reflects on the business performance of Glaxo Smith

Kline (GSK) enterprise from accounting year 2016 to 2016. Besides these, difference among IAS

and IFRS is shown along with benefits of IFRS for an organisation.

1. Context as well as objectives of financial reporting

When the company uses financial reporting in the workplace then become beneficial

different ways. Further, its several objectives are mentioned below:

Key purpose of the financial reporting is to provide those kinds of information to the

company which helps to make an effective decision.

It helps to the management and investors both in order to assess or track cash availability

within the workplace. On the basis of this, creditors and suppliers also make fruitful

decision towards the company (Objectives of financial reporting, 2015).

Information related to the economic sources of the company also provided by financial

reporting. Such information include liabilities, equity of owner etc.

Another objective of financial reporting is to provide statutory auditing information

which becomes change with facilitates audit.

For identifying various scandals and malpractices incurred within financial statements

and resolving them the financial reporting is an important aspect.

2. Evaluating different framework and its key principles

In the financial reporting various frameworks included which regulate to the whole

process and amend required changes. On the basis of this, the management able to prepare

financials and publish in the market using legal rules. Further, any of the stakeholder easily able

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to understand and analyse the statements of financial of the company. There are various

principles associated with financial reporting which are listed out below:

Expense principle

Cost principle

Objectivity principle

Consistency principle

Matching principle

Revenue principle

Going concern principle

Separate entity assumption

Continuity principle

Unit-of-measure assumption

When looking at the qualitative aspect then it helps to make clear explanation about the

business and its performance in regarded industry. The quantitative considers only numerical

data which can be understood by only financial employees (Reheul, Van Caneghem and

Verbruggen, 2014). On the other side, qualitative supports to both kinds of the people like

financial or non-financial for assessing performance and take fruitful decisions towards the

organisation. Further, the qualitative kind of information helps to provide reliable as well as

appropriate data to the stakeholders.

3. Key stakeholders of an entity and benefits to them of financial information

Financial information of the company always used by different stakeholders in proper

way for taking better decisions. Furthermore, ways through which basic stakeholders consider

financial information are described below: Managers: One of the important internal stakeholders of an organisation are managers

who make decisions for the business using financial information (Nobes, 2014). In this,

they decide about investment making in any new project or other alternatives, produce

more products, increase salary or wages etc.

2

principles associated with financial reporting which are listed out below:

Expense principle

Cost principle

Objectivity principle

Consistency principle

Matching principle

Revenue principle

Going concern principle

Separate entity assumption

Continuity principle

Unit-of-measure assumption

When looking at the qualitative aspect then it helps to make clear explanation about the

business and its performance in regarded industry. The quantitative considers only numerical

data which can be understood by only financial employees (Reheul, Van Caneghem and

Verbruggen, 2014). On the other side, qualitative supports to both kinds of the people like

financial or non-financial for assessing performance and take fruitful decisions towards the

organisation. Further, the qualitative kind of information helps to provide reliable as well as

appropriate data to the stakeholders.

3. Key stakeholders of an entity and benefits to them of financial information

Financial information of the company always used by different stakeholders in proper

way for taking better decisions. Furthermore, ways through which basic stakeholders consider

financial information are described below: Managers: One of the important internal stakeholders of an organisation are managers

who make decisions for the business using financial information (Nobes, 2014). In this,

they decide about investment making in any new project or other alternatives, produce

more products, increase salary or wages etc.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Employees: These are internal stakeholder of the company which makes assumptions

related to the salary, wages, bonuses, allowances and other monetary benefits on the basis

of financial information. For instance: if the enterprise generates more profit, then will

attract more for doing job and sustaining and vice-versa.

Shareholders or investors: These kinds of external stakeholders always seeks towards

the higher dividend and return on investment (Flower, 2016). During analysis of the

financial information if the firm generates higher level of profit on consistent basis then

will expect more dividend amount. Furthermore, to take investment decisions these

stakeholders use financial information.

Apart from the above stakeholders, customers, creditors, government, suppliers etc. also

use the financial information of an organisation to take respect decisions towards business.

4. Importance of financial reporting for meeting objectives and growth of the firm

The financial reporting is supportive for assessing business performance in proper way

where management can determine level of profits. Apart from this, using auditing process

malpractice associated while preparing financial statements can be identified. In accordance to

these all, if it has been ascertained that objectives of sales or profit increasing, cost decreasing

and any other are achieved or not (Wagenhofer, 2014). Moreover, during making the accounting

treatments in the financial statements if any issue found then eliminated by taking corrective

actions. Therefore, it can be stated that, with the help of financial reporting the company easily

able to meet the agreed purposes and grow in positive way ion respective market.

5. Presenting key financial statements considering provided information

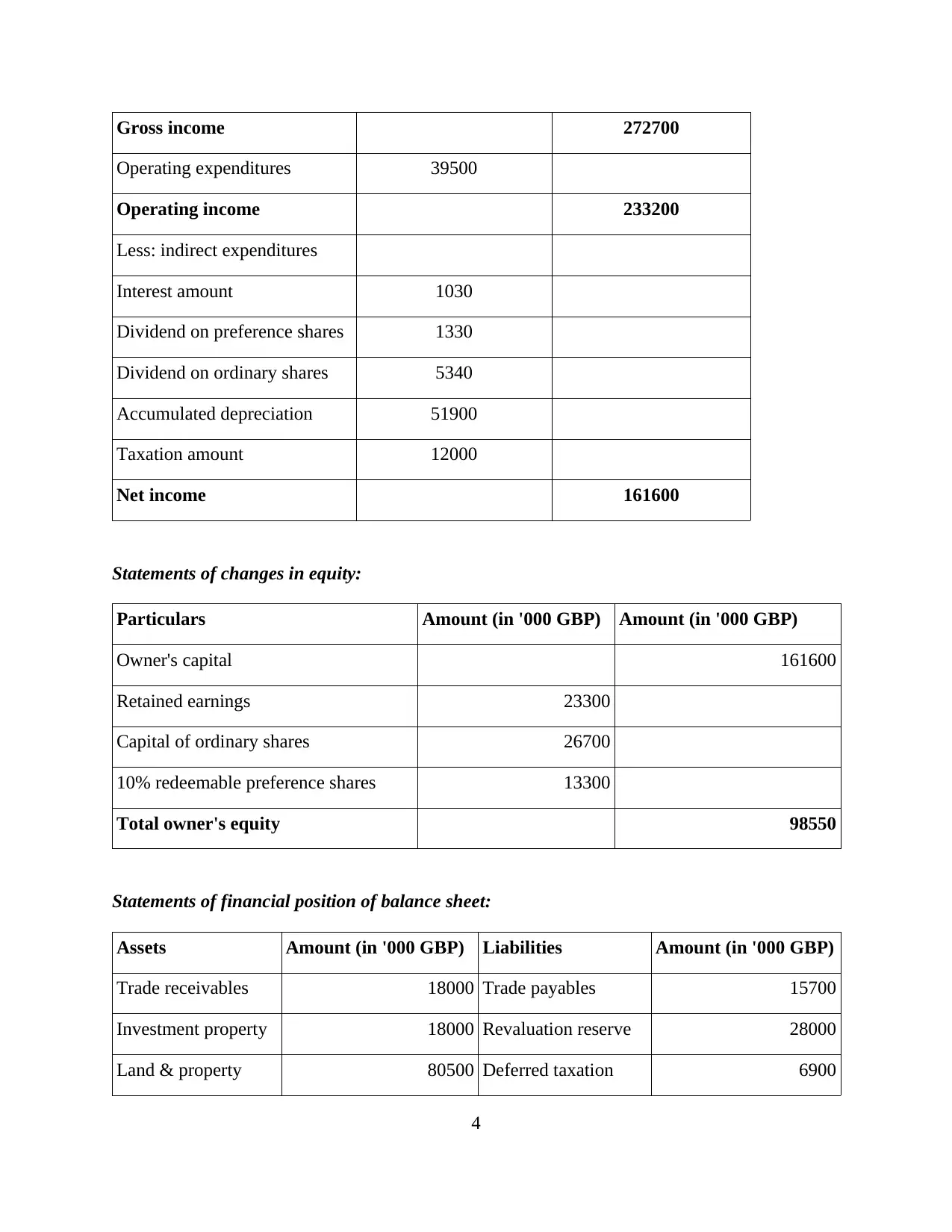

Statement of profit and loss:

Particulars Amount (in '000 GBP) Amount (in '000 GBP)

Sales revenue 285100

Less: Stock at the end of year 14000

Cost of sales 271100

Add: Rental income earned

from investment properties 1600

3

related to the salary, wages, bonuses, allowances and other monetary benefits on the basis

of financial information. For instance: if the enterprise generates more profit, then will

attract more for doing job and sustaining and vice-versa.

Shareholders or investors: These kinds of external stakeholders always seeks towards

the higher dividend and return on investment (Flower, 2016). During analysis of the

financial information if the firm generates higher level of profit on consistent basis then

will expect more dividend amount. Furthermore, to take investment decisions these

stakeholders use financial information.

Apart from the above stakeholders, customers, creditors, government, suppliers etc. also

use the financial information of an organisation to take respect decisions towards business.

4. Importance of financial reporting for meeting objectives and growth of the firm

The financial reporting is supportive for assessing business performance in proper way

where management can determine level of profits. Apart from this, using auditing process

malpractice associated while preparing financial statements can be identified. In accordance to

these all, if it has been ascertained that objectives of sales or profit increasing, cost decreasing

and any other are achieved or not (Wagenhofer, 2014). Moreover, during making the accounting

treatments in the financial statements if any issue found then eliminated by taking corrective

actions. Therefore, it can be stated that, with the help of financial reporting the company easily

able to meet the agreed purposes and grow in positive way ion respective market.

5. Presenting key financial statements considering provided information

Statement of profit and loss:

Particulars Amount (in '000 GBP) Amount (in '000 GBP)

Sales revenue 285100

Less: Stock at the end of year 14000

Cost of sales 271100

Add: Rental income earned

from investment properties 1600

3

Gross income 272700

Operating expenditures 39500

Operating income 233200

Less: indirect expenditures

Interest amount 1030

Dividend on preference shares 1330

Dividend on ordinary shares 5340

Accumulated depreciation 51900

Taxation amount 12000

Net income 161600

Statements of changes in equity:

Particulars Amount (in '000 GBP) Amount (in '000 GBP)

Owner's capital 161600

Retained earnings 23300

Capital of ordinary shares 26700

10% redeemable preference shares 13300

Total owner's equity 98550

Statements of financial position of balance sheet:

Assets Amount (in '000 GBP) Liabilities Amount (in '000 GBP)

Trade receivables 18000 Trade payables 15700

Investment property 18000 Revaluation reserve 28000

Land & property 80500 Deferred taxation 6900

4

Operating expenditures 39500

Operating income 233200

Less: indirect expenditures

Interest amount 1030

Dividend on preference shares 1330

Dividend on ordinary shares 5340

Accumulated depreciation 51900

Taxation amount 12000

Net income 161600

Statements of changes in equity:

Particulars Amount (in '000 GBP) Amount (in '000 GBP)

Owner's capital 161600

Retained earnings 23300

Capital of ordinary shares 26700

10% redeemable preference shares 13300

Total owner's equity 98550

Statements of financial position of balance sheet:

Assets Amount (in '000 GBP) Liabilities Amount (in '000 GBP)

Trade receivables 18000 Trade payables 15700

Investment property 18000 Revaluation reserve 28000

Land & property 80500 Deferred taxation 6900

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

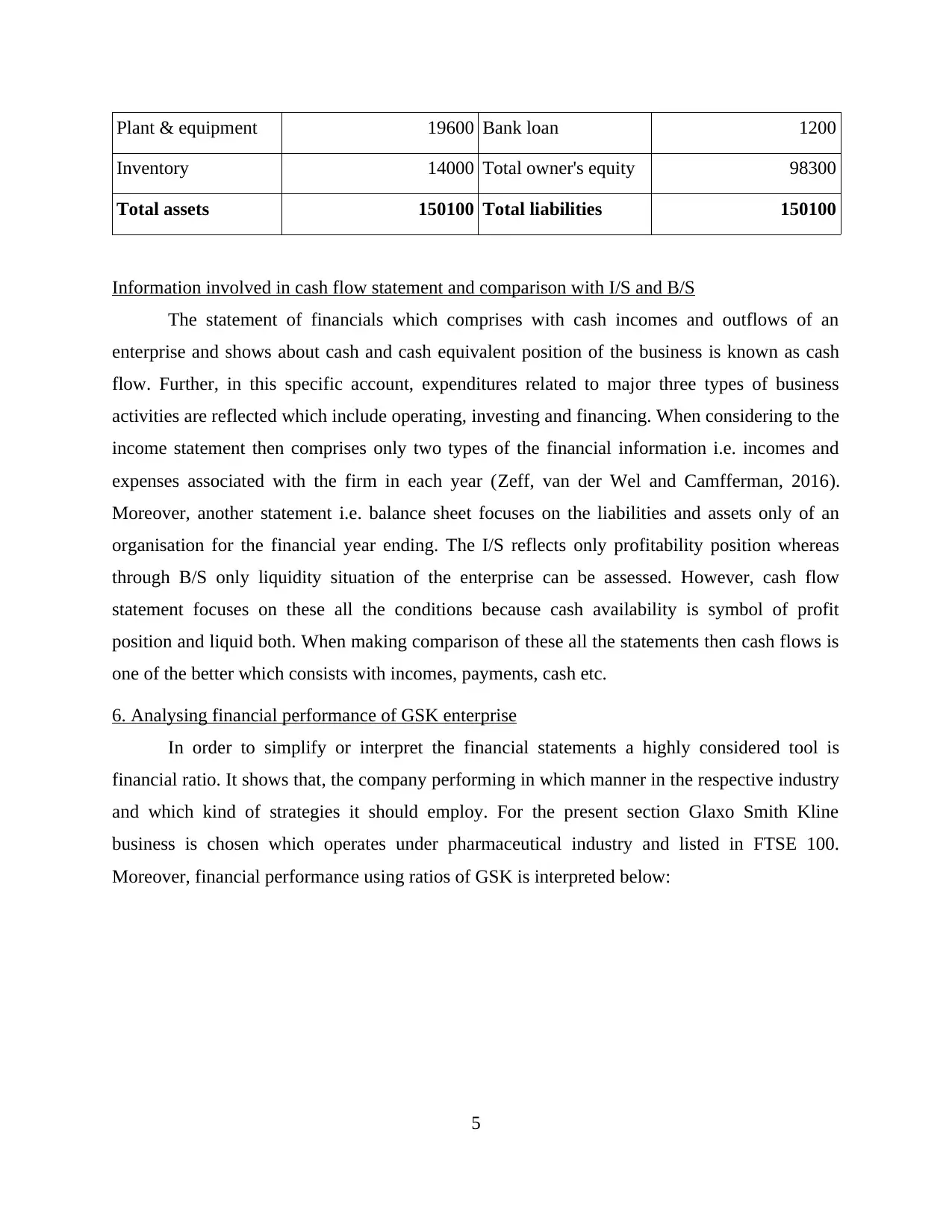

Plant & equipment 19600 Bank loan 1200

Inventory 14000 Total owner's equity 98300

Total assets 150100 Total liabilities 150100

Information involved in cash flow statement and comparison with I/S and B/S

The statement of financials which comprises with cash incomes and outflows of an

enterprise and shows about cash and cash equivalent position of the business is known as cash

flow. Further, in this specific account, expenditures related to major three types of business

activities are reflected which include operating, investing and financing. When considering to the

income statement then comprises only two types of the financial information i.e. incomes and

expenses associated with the firm in each year (Zeff, van der Wel and Camfferman, 2016).

Moreover, another statement i.e. balance sheet focuses on the liabilities and assets only of an

organisation for the financial year ending. The I/S reflects only profitability position whereas

through B/S only liquidity situation of the enterprise can be assessed. However, cash flow

statement focuses on these all the conditions because cash availability is symbol of profit

position and liquid both. When making comparison of these all the statements then cash flows is

one of the better which consists with incomes, payments, cash etc.

6. Analysing financial performance of GSK enterprise

In order to simplify or interpret the financial statements a highly considered tool is

financial ratio. It shows that, the company performing in which manner in the respective industry

and which kind of strategies it should employ. For the present section Glaxo Smith Kline

business is chosen which operates under pharmaceutical industry and listed in FTSE 100.

Moreover, financial performance using ratios of GSK is interpreted below:

5

Inventory 14000 Total owner's equity 98300

Total assets 150100 Total liabilities 150100

Information involved in cash flow statement and comparison with I/S and B/S

The statement of financials which comprises with cash incomes and outflows of an

enterprise and shows about cash and cash equivalent position of the business is known as cash

flow. Further, in this specific account, expenditures related to major three types of business

activities are reflected which include operating, investing and financing. When considering to the

income statement then comprises only two types of the financial information i.e. incomes and

expenses associated with the firm in each year (Zeff, van der Wel and Camfferman, 2016).

Moreover, another statement i.e. balance sheet focuses on the liabilities and assets only of an

organisation for the financial year ending. The I/S reflects only profitability position whereas

through B/S only liquidity situation of the enterprise can be assessed. However, cash flow

statement focuses on these all the conditions because cash availability is symbol of profit

position and liquid both. When making comparison of these all the statements then cash flows is

one of the better which consists with incomes, payments, cash etc.

6. Analysing financial performance of GSK enterprise

In order to simplify or interpret the financial statements a highly considered tool is

financial ratio. It shows that, the company performing in which manner in the respective industry

and which kind of strategies it should employ. For the present section Glaxo Smith Kline

business is chosen which operates under pharmaceutical industry and listed in FTSE 100.

Moreover, financial performance using ratios of GSK is interpreted below:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

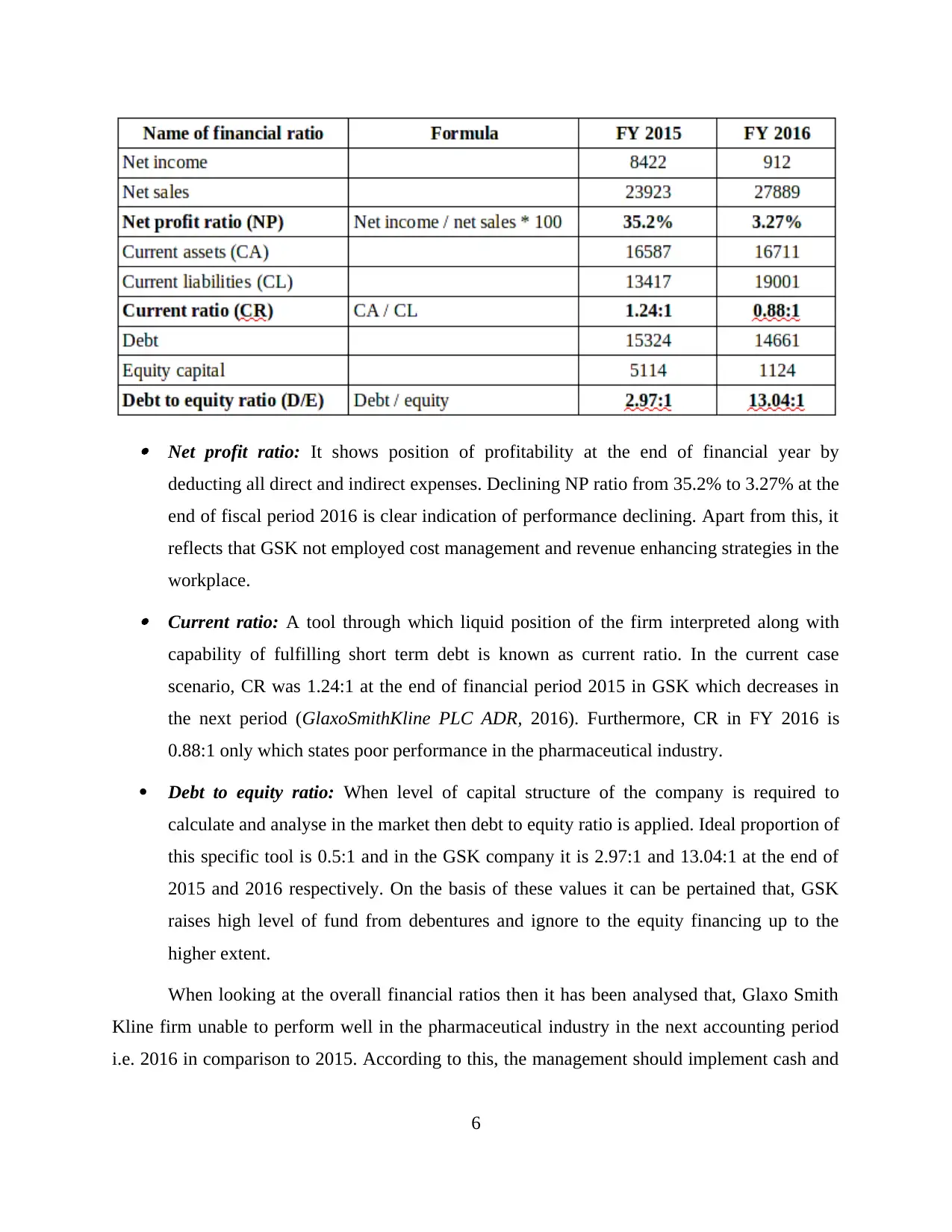

Net profit ratio: It shows position of profitability at the end of financial year by

deducting all direct and indirect expenses. Declining NP ratio from 35.2% to 3.27% at the

end of fiscal period 2016 is clear indication of performance declining. Apart from this, it

reflects that GSK not employed cost management and revenue enhancing strategies in the

workplace. Current ratio: A tool through which liquid position of the firm interpreted along with

capability of fulfilling short term debt is known as current ratio. In the current case

scenario, CR was 1.24:1 at the end of financial period 2015 in GSK which decreases in

the next period (GlaxoSmithKline PLC ADR, 2016). Furthermore, CR in FY 2016 is

0.88:1 only which states poor performance in the pharmaceutical industry.

Debt to equity ratio: When level of capital structure of the company is required to

calculate and analyse in the market then debt to equity ratio is applied. Ideal proportion of

this specific tool is 0.5:1 and in the GSK company it is 2.97:1 and 13.04:1 at the end of

2015 and 2016 respectively. On the basis of these values it can be pertained that, GSK

raises high level of fund from debentures and ignore to the equity financing up to the

higher extent.

When looking at the overall financial ratios then it has been analysed that, Glaxo Smith

Kline firm unable to perform well in the pharmaceutical industry in the next accounting period

i.e. 2016 in comparison to 2015. According to this, the management should implement cash and

6

deducting all direct and indirect expenses. Declining NP ratio from 35.2% to 3.27% at the

end of fiscal period 2016 is clear indication of performance declining. Apart from this, it

reflects that GSK not employed cost management and revenue enhancing strategies in the

workplace. Current ratio: A tool through which liquid position of the firm interpreted along with

capability of fulfilling short term debt is known as current ratio. In the current case

scenario, CR was 1.24:1 at the end of financial period 2015 in GSK which decreases in

the next period (GlaxoSmithKline PLC ADR, 2016). Furthermore, CR in FY 2016 is

0.88:1 only which states poor performance in the pharmaceutical industry.

Debt to equity ratio: When level of capital structure of the company is required to

calculate and analyse in the market then debt to equity ratio is applied. Ideal proportion of

this specific tool is 0.5:1 and in the GSK company it is 2.97:1 and 13.04:1 at the end of

2015 and 2016 respectively. On the basis of these values it can be pertained that, GSK

raises high level of fund from debentures and ignore to the equity financing up to the

higher extent.

When looking at the overall financial ratios then it has been analysed that, Glaxo Smith

Kline firm unable to perform well in the pharmaceutical industry in the next accounting period

i.e. 2016 in comparison to 2015. According to this, the management should implement cash and

6

cost reducing tactics in the workplace. Along with this, it must train to employees for utilising

resources in highly optimum direction.

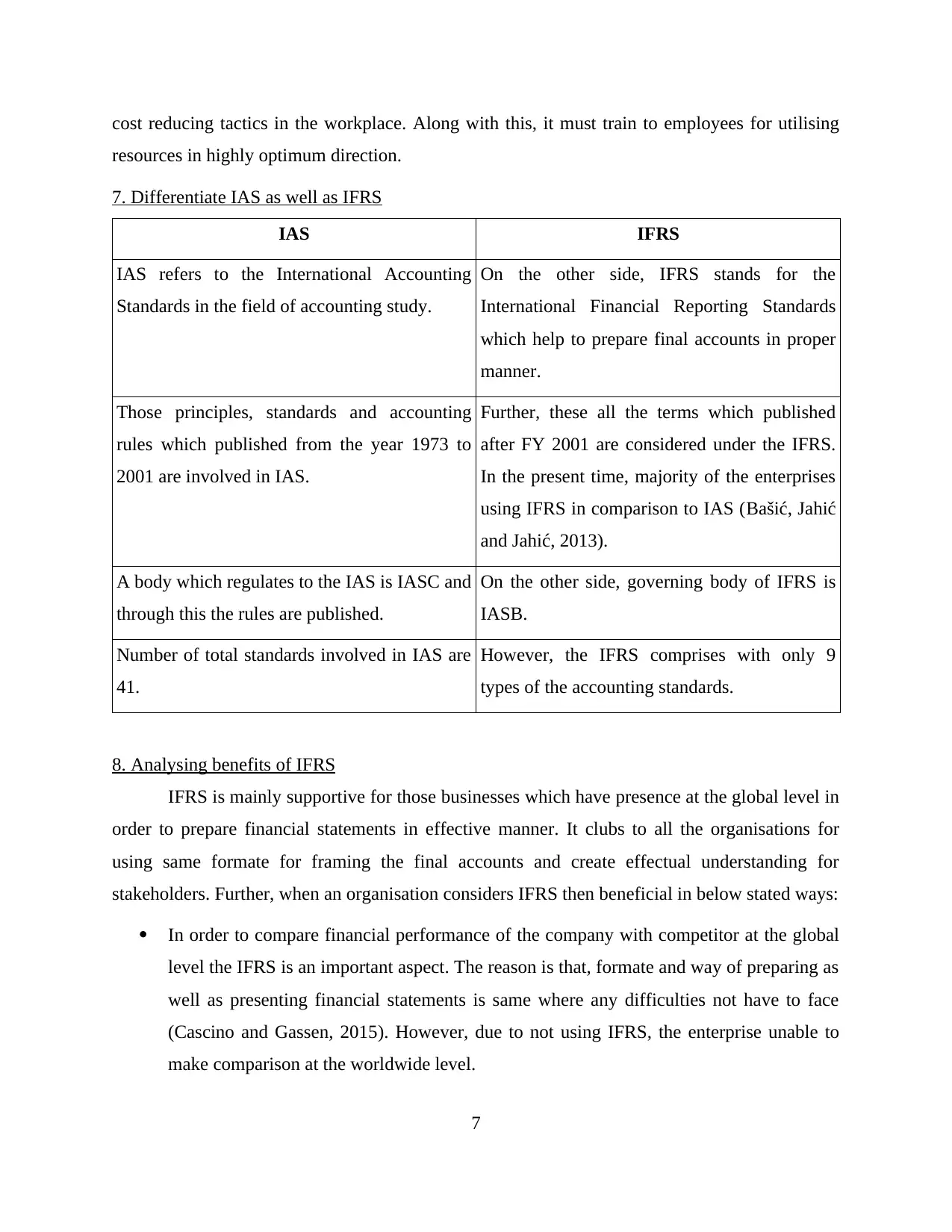

7. Differentiate IAS as well as IFRS

IAS IFRS

IAS refers to the International Accounting

Standards in the field of accounting study.

On the other side, IFRS stands for the

International Financial Reporting Standards

which help to prepare final accounts in proper

manner.

Those principles, standards and accounting

rules which published from the year 1973 to

2001 are involved in IAS.

Further, these all the terms which published

after FY 2001 are considered under the IFRS.

In the present time, majority of the enterprises

using IFRS in comparison to IAS (Bašić, Jahić

and Jahić, 2013).

A body which regulates to the IAS is IASC and

through this the rules are published.

On the other side, governing body of IFRS is

IASB.

Number of total standards involved in IAS are

41.

However, the IFRS comprises with only 9

types of the accounting standards.

8. Analysing benefits of IFRS

IFRS is mainly supportive for those businesses which have presence at the global level in

order to prepare financial statements in effective manner. It clubs to all the organisations for

using same formate for framing the final accounts and create effectual understanding for

stakeholders. Further, when an organisation considers IFRS then beneficial in below stated ways:

In order to compare financial performance of the company with competitor at the global

level the IFRS is an important aspect. The reason is that, formate and way of preparing as

well as presenting financial statements is same where any difficulties not have to face

(Cascino and Gassen, 2015). However, due to not using IFRS, the enterprise unable to

make comparison at the worldwide level.

7

resources in highly optimum direction.

7. Differentiate IAS as well as IFRS

IAS IFRS

IAS refers to the International Accounting

Standards in the field of accounting study.

On the other side, IFRS stands for the

International Financial Reporting Standards

which help to prepare final accounts in proper

manner.

Those principles, standards and accounting

rules which published from the year 1973 to

2001 are involved in IAS.

Further, these all the terms which published

after FY 2001 are considered under the IFRS.

In the present time, majority of the enterprises

using IFRS in comparison to IAS (Bašić, Jahić

and Jahić, 2013).

A body which regulates to the IAS is IASC and

through this the rules are published.

On the other side, governing body of IFRS is

IASB.

Number of total standards involved in IAS are

41.

However, the IFRS comprises with only 9

types of the accounting standards.

8. Analysing benefits of IFRS

IFRS is mainly supportive for those businesses which have presence at the global level in

order to prepare financial statements in effective manner. It clubs to all the organisations for

using same formate for framing the final accounts and create effectual understanding for

stakeholders. Further, when an organisation considers IFRS then beneficial in below stated ways:

In order to compare financial performance of the company with competitor at the global

level the IFRS is an important aspect. The reason is that, formate and way of preparing as

well as presenting financial statements is same where any difficulties not have to face

(Cascino and Gassen, 2015). However, due to not using IFRS, the enterprise unable to

make comparison at the worldwide level.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recognition of the financial statements in the company takes more time which hamper

efficiency and productivity of employees and firm respectively. IFRS is a method

through which time-frame of the financial recognition is to be decreased up to the higher

extent.

At the time of getting access of an organisation under foreign capital markets, wide range

of issues and obstacles are faced by it. When the management uses IFRS then accounts

are prepared at the international level which helps to take effective access to capital

markets of abroad.

When the stakeholders use financial statements then they will able to easily understand

them, if firm considered IFRS principles and standards. Moreover, it can be said that the

IFRS helps to create proper and broad level of understanding for interpreting final

accounts (Tsalavoutas, André and Dionysiou, 2014).

Besides these all, IFRS is a pivotal place for the management in order to improve

transparency related to the financial reporting. Along with this, auditing process can be

also accomplished in proper and smooth way when financials are prepared using IFRS

concept.

9. Elements create impact on compliance with IFRS

At the time of considering wide range of principles, theories and standards related to

IFRS then some factors create huge impact, which are explained below:

One of the basic element which has a higher impact on compliance with IFRS and

follow its rules in proper way is size of the company. Under this, disclosure

compliance are at the higher extent which associated with the enterprise (Terzi,

Oktem and Sen, 2013). Along with this, size of the entity has positive influence on

the workplace.

The term which indicates level of equity capital available in the workplace in

exchange to bank loan is considered as leverage. Further, it has the huge impact on

the business when it considers all compliance included with IFRS. Higher the level of

leverage has negative impact and vice-versa.

8

efficiency and productivity of employees and firm respectively. IFRS is a method

through which time-frame of the financial recognition is to be decreased up to the higher

extent.

At the time of getting access of an organisation under foreign capital markets, wide range

of issues and obstacles are faced by it. When the management uses IFRS then accounts

are prepared at the international level which helps to take effective access to capital

markets of abroad.

When the stakeholders use financial statements then they will able to easily understand

them, if firm considered IFRS principles and standards. Moreover, it can be said that the

IFRS helps to create proper and broad level of understanding for interpreting final

accounts (Tsalavoutas, André and Dionysiou, 2014).

Besides these all, IFRS is a pivotal place for the management in order to improve

transparency related to the financial reporting. Along with this, auditing process can be

also accomplished in proper and smooth way when financials are prepared using IFRS

concept.

9. Elements create impact on compliance with IFRS

At the time of considering wide range of principles, theories and standards related to

IFRS then some factors create huge impact, which are explained below:

One of the basic element which has a higher impact on compliance with IFRS and

follow its rules in proper way is size of the company. Under this, disclosure

compliance are at the higher extent which associated with the enterprise (Terzi,

Oktem and Sen, 2013). Along with this, size of the entity has positive influence on

the workplace.

The term which indicates level of equity capital available in the workplace in

exchange to bank loan is considered as leverage. Further, it has the huge impact on

the business when it considers all compliance included with IFRS. Higher the level of

leverage has negative impact and vice-versa.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Liquidity is undertaken in the workplace for deriving financial position of entity in

the industry. When this particular aspect either increase or decrease in the business

environment then affect to the compliance involved with the International Financial

Reporting Standard in same direction.

Other than the above described factors, age of an enterprise, structure of business

ownership, presence whether at national or global level etc. also have huge impact

(Wild, Creighton and Simmonds, 2015). Further, when the management generates

high or low level of the incomes or profits then also effect the compliance with IFRS.

CONCLUSION

It has been analysed using the above study that, financial reporting is an essential tool

through which the company able to publish financial statements in legal direction. Further, there

are different internal and external stakeholders use financial information for making profitable

decisions towards the firm. From the financial ratios it can be concluded that, GSK business has

poor and negative performance in pharmaceutical sector at the end of 2016 compared to FY

2015. Further, International Financial Reporting Standard and International Accounting Standard

both are different up to the certain extent. Apart from these all, when an organisation uses

compliance with IFRS then wide range of aspect create wither positive or inverse influence.

9

the industry. When this particular aspect either increase or decrease in the business

environment then affect to the compliance involved with the International Financial

Reporting Standard in same direction.

Other than the above described factors, age of an enterprise, structure of business

ownership, presence whether at national or global level etc. also have huge impact

(Wild, Creighton and Simmonds, 2015). Further, when the management generates

high or low level of the incomes or profits then also effect the compliance with IFRS.

CONCLUSION

It has been analysed using the above study that, financial reporting is an essential tool

through which the company able to publish financial statements in legal direction. Further, there

are different internal and external stakeholders use financial information for making profitable

decisions towards the firm. From the financial ratios it can be concluded that, GSK business has

poor and negative performance in pharmaceutical sector at the end of 2016 compared to FY

2015. Further, International Financial Reporting Standard and International Accounting Standard

both are different up to the certain extent. Apart from these all, when an organisation uses

compliance with IFRS then wide range of aspect create wither positive or inverse influence.

9

REFERENCES

Books and Journals

Bašić, M., Jahić, H. and Jahić, L., 2013. Analysis of Causes and Effects of Applying IAS And

IFRS in Case of Mergers and Acquisitions of Banks in the Federation of Bosnia and

Herzegovina. European Journal of Sustainable Development. 2(4). pp.149-162.

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies. 20(1). pp.242-282.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Reheul, A. M., Van Caneghem, T. and Verbruggen, S., 2014. Financial reporting lags in the non-

profit sector: An empirical analysis. VOLUNTAS: International Journal of Voluntary and

Nonprofit Organizations. 25(2). pp.352-377.

Terzi, S., Oktem, R. and Sen, I. K., 2013. Impact of Adopting International Financial Reporting

Standards: Empirical Evidence from Turkey. International Business Research. 6(4). p.55.

Tsalavoutas, I., André, P. and Dionysiou, D., 2014. Worldwide application of IFRS 3, IAS 38

and IAS 36, related disclosures, and determinants of non-compliance. ACCA Research

report. 134.

Wagenhofer, A., 2014. Trading off costs and benefits of frequent financial reporting. Journal of

Accounting Research. 52(2). pp.389-401.

Wild, K., Creighton, B. and Simmonds, A., 2015. GAAP 2000: UK Financial Reporting.

Springer.

Zeff, S. A., van der Wel, F. and Camfferman, C., 2016. Company financial reporting: A

historical and comparative study of the Dutch regulatory process. Routledge.

Online

GlaxoSmithKline PLC ADR, 2016. [Online]. Available through:

<http://financials.morningstar.com/balance-sheet/bs.html?

t=GSK®ion=usa&culture=en-US> [Accessed on 24th October 2017].

10

Books and Journals

Bašić, M., Jahić, H. and Jahić, L., 2013. Analysis of Causes and Effects of Applying IAS And

IFRS in Case of Mergers and Acquisitions of Banks in the Federation of Bosnia and

Herzegovina. European Journal of Sustainable Development. 2(4). pp.149-162.

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies. 20(1). pp.242-282.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Reheul, A. M., Van Caneghem, T. and Verbruggen, S., 2014. Financial reporting lags in the non-

profit sector: An empirical analysis. VOLUNTAS: International Journal of Voluntary and

Nonprofit Organizations. 25(2). pp.352-377.

Terzi, S., Oktem, R. and Sen, I. K., 2013. Impact of Adopting International Financial Reporting

Standards: Empirical Evidence from Turkey. International Business Research. 6(4). p.55.

Tsalavoutas, I., André, P. and Dionysiou, D., 2014. Worldwide application of IFRS 3, IAS 38

and IAS 36, related disclosures, and determinants of non-compliance. ACCA Research

report. 134.

Wagenhofer, A., 2014. Trading off costs and benefits of frequent financial reporting. Journal of

Accounting Research. 52(2). pp.389-401.

Wild, K., Creighton, B. and Simmonds, A., 2015. GAAP 2000: UK Financial Reporting.

Springer.

Zeff, S. A., van der Wel, F. and Camfferman, C., 2016. Company financial reporting: A

historical and comparative study of the Dutch regulatory process. Routledge.

Online

GlaxoSmithKline PLC ADR, 2016. [Online]. Available through:

<http://financials.morningstar.com/balance-sheet/bs.html?

t=GSK®ion=usa&culture=en-US> [Accessed on 24th October 2017].

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.