In-depth Financial Reporting and Analysis of Harvey Norman Ltd

VerifiedAdded on 2023/06/09

|13

|3457

|445

Case Study

AI Summary

This report provides a detailed financial reporting analysis of Harvey Norman, focusing on its compliance with accounting standards and the quality of its financial disclosures. The analysis covers key accounting policies related to revenue recognition, expenses, intangible assets, and leases, assessing the flexibility afforded to management in each area. It explores the connection between the company's business strategies, such as its flagship store initiative, and its accounting practices, particularly concerning director remuneration and incentives. The report also examines whether there are any questionable accounting numbers and refers to financial press discussions about the company. The analysis concludes that Harvey Norman generally adheres to required accounting principles, providing transparent financial information in its annual report.

Running head: FINANCIAL REPORTING AND ANALYSIS

Financial Reporting and Analysis

Name of the Student

Name of the University

Author’s Note

Financial Reporting and Analysis

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL REPORTING AND ANALYSIS

Executive Summary

The main objective of this report is the analysis and evaluation of the latest annual report of

Harvey Norman. Different parts of the analysis show that the company has complied with the

required accounting and financial reporting principles for the purpose of their financial reporting;

and for this reason, they have disclosed all of their financial information in their annual report.

Moreover, there is a connection between the developed business strategies of the companies with

the adopted accounting principles.

Executive Summary

The main objective of this report is the analysis and evaluation of the latest annual report of

Harvey Norman. Different parts of the analysis show that the company has complied with the

required accounting and financial reporting principles for the purpose of their financial reporting;

and for this reason, they have disclosed all of their financial information in their annual report.

Moreover, there is a connection between the developed business strategies of the companies with

the adopted accounting principles.

2FINANCIAL REPORTING AND ANALYSIS

Table of Contents

Introduction......................................................................................................................................3

Summary of Activities.....................................................................................................................3

Key Accounting Policies.................................................................................................................4

Flexibility of Management..............................................................................................................4

Accounting Strategies......................................................................................................................6

Quality of Disclosures.....................................................................................................................7

Questionable Accounting Numbers.................................................................................................8

Undo Questionable Accounting Numbers.......................................................................................9

Financial Press Discussion..............................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................3

Summary of Activities.....................................................................................................................3

Key Accounting Policies.................................................................................................................4

Flexibility of Management..............................................................................................................4

Accounting Strategies......................................................................................................................6

Quality of Disclosures.....................................................................................................................7

Questionable Accounting Numbers.................................................................................................8

Undo Questionable Accounting Numbers.......................................................................................9

Financial Press Discussion..............................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL REPORTING AND ANALYSIS

Introduction

Financial Reporting is considered as a major aspect for the financial success of the

business organizations. The process of financial reporting is considered as a formal record of the

financial activities as well as financial position of the businesses (Nobes 2014). While preparing

and presenting financial statements, the companies are needed to comply with all the required

financial rules and regulations of the available accounting conceptual framework. It implies that

the companies are needed to follow all the accounting policies for the development of effective

accounting strategies to achieve the financial objectives (Beatty, Liao and Yu 2013). In the

process of financial reporting, the annual report of the companies play a crucial part as the

companies are required to provide all the financial information along with the adopted financial

policies in them so that the investors can access them to gain understanding about the financial

position of the companies (Bentley, Omer and Sharp 2013). The main aim of the report is to

conduct an analysis and evaluation on the financial reporting process of one of the Australian

companies; and Harvey Norman is taken into consideration for this report. Different parts of

this report analyze different aspects of the financial reporting process of Harvey Norman.

Summary of Activities

Harvey Norman is a large Australia based multinational organization. The company was

established in the year of 1982 and it is headquartered at Homebush West, New South Wales,

Australia. Accordant to the latest annual report of Harvey Norman that is the 2017 Annual

Report, the principal activities of the company can be seen in the areas of integrated retail,

franchise, property and digital system. More specifically, the main activities of the company can

be seen in the selling of different products like furniture, computers, bedding, communication

and consumer electrical products (static1.squarespace.com 2018). Apart from this, the

involvement of the company can also be seen in the fields of franchisor, investment in property,

lease of different premises, media placement, provision of consumer finance and many others.

The annual report of the company states that the main operating areas of the company are

Australia, New Zealand, Malaysia, Singapore, Slovenia, Ireland, Northern Ireland and Croatia. It

can be seen in the 2017 Annual Report of Harvey Norman that there has not been any significant

Introduction

Financial Reporting is considered as a major aspect for the financial success of the

business organizations. The process of financial reporting is considered as a formal record of the

financial activities as well as financial position of the businesses (Nobes 2014). While preparing

and presenting financial statements, the companies are needed to comply with all the required

financial rules and regulations of the available accounting conceptual framework. It implies that

the companies are needed to follow all the accounting policies for the development of effective

accounting strategies to achieve the financial objectives (Beatty, Liao and Yu 2013). In the

process of financial reporting, the annual report of the companies play a crucial part as the

companies are required to provide all the financial information along with the adopted financial

policies in them so that the investors can access them to gain understanding about the financial

position of the companies (Bentley, Omer and Sharp 2013). The main aim of the report is to

conduct an analysis and evaluation on the financial reporting process of one of the Australian

companies; and Harvey Norman is taken into consideration for this report. Different parts of

this report analyze different aspects of the financial reporting process of Harvey Norman.

Summary of Activities

Harvey Norman is a large Australia based multinational organization. The company was

established in the year of 1982 and it is headquartered at Homebush West, New South Wales,

Australia. Accordant to the latest annual report of Harvey Norman that is the 2017 Annual

Report, the principal activities of the company can be seen in the areas of integrated retail,

franchise, property and digital system. More specifically, the main activities of the company can

be seen in the selling of different products like furniture, computers, bedding, communication

and consumer electrical products (static1.squarespace.com 2018). Apart from this, the

involvement of the company can also be seen in the fields of franchisor, investment in property,

lease of different premises, media placement, provision of consumer finance and many others.

The annual report of the company states that the main operating areas of the company are

Australia, New Zealand, Malaysia, Singapore, Slovenia, Ireland, Northern Ireland and Croatia. It

can be seen in the 2017 Annual Report of Harvey Norman that there has not been any significant

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL REPORTING AND ANALYSIS

changes in the states of affair of the consolidated entities of Harvey Norman during the year of

2017 as per the directors of the company (static1.squarespace.com 2018).

Key Accounting Policies

According to the 2017 Annual Report, Harvey Norman has complied with the principles

and guiding regulations of AASB 10 Consolidated Financial Statements for preparing and

presenting their financial statements (static1.squarespace.com 2018).

Revenue and Expenses: It can be seen from the 2017 Annual Report of Harvey Norman that the

company follows the principles of AASB 118 Revenues for the recognition of their business

revenues. It needs to be mentioned that Harvey Norman recognizes their revenues as the income

from day-to-day business operations. It can also be observed that the management of the

company reviews all the determining factors for the determination of their revenues and expense.

It needs to be mentioned that the company is going to adopt the standards of AASB 118

Revenues from Contracts with Customers for the recognition of their revenues from July 1,

2018 (aasb.gov.au 2018).

Intangible Assets: For the recognition and the accounting policies of the intangible assets of the

business, Harvey Norman follows the principles and standards of AASB 138 Intangible Assets

as per AASB conceptual framework. Some of the important intangible assets of the business of

Harvey Norman are computer software assets, capitalized development expenditures and

licensed properties. The company recognizes their intangible assets of business in the cost value

less accumulated amortization and accumulated impairment losses (aasb.gov.au 2018).

Lease: For the accounting treatments as well as recognition of the business leases, the

management of Harvey Norman follows the principles of AASB 117 Leases. As a result of the

adoption of this lease standard, the requirement for the management of the company is to

distinguish all of their leases between operating leases and finance leases (aasb.gov.au 2018).

Flexibility of Management

Accounting Standards Flexibility Description

Revenue Recognition As per the 2017 Annual Report of Harvey Norman, it

changes in the states of affair of the consolidated entities of Harvey Norman during the year of

2017 as per the directors of the company (static1.squarespace.com 2018).

Key Accounting Policies

According to the 2017 Annual Report, Harvey Norman has complied with the principles

and guiding regulations of AASB 10 Consolidated Financial Statements for preparing and

presenting their financial statements (static1.squarespace.com 2018).

Revenue and Expenses: It can be seen from the 2017 Annual Report of Harvey Norman that the

company follows the principles of AASB 118 Revenues for the recognition of their business

revenues. It needs to be mentioned that Harvey Norman recognizes their revenues as the income

from day-to-day business operations. It can also be observed that the management of the

company reviews all the determining factors for the determination of their revenues and expense.

It needs to be mentioned that the company is going to adopt the standards of AASB 118

Revenues from Contracts with Customers for the recognition of their revenues from July 1,

2018 (aasb.gov.au 2018).

Intangible Assets: For the recognition and the accounting policies of the intangible assets of the

business, Harvey Norman follows the principles and standards of AASB 138 Intangible Assets

as per AASB conceptual framework. Some of the important intangible assets of the business of

Harvey Norman are computer software assets, capitalized development expenditures and

licensed properties. The company recognizes their intangible assets of business in the cost value

less accumulated amortization and accumulated impairment losses (aasb.gov.au 2018).

Lease: For the accounting treatments as well as recognition of the business leases, the

management of Harvey Norman follows the principles of AASB 117 Leases. As a result of the

adoption of this lease standard, the requirement for the management of the company is to

distinguish all of their leases between operating leases and finance leases (aasb.gov.au 2018).

Flexibility of Management

Accounting Standards Flexibility Description

Revenue Recognition As per the 2017 Annual Report of Harvey Norman, it

5FINANCIAL REPORTING AND ANALYSIS

(AASB 118)

High

can be seen that the majority potion of the revenue of

the company comes from the sale of goods. As per

AASB 118, the companies are needed to recognize

revenue from three major sources like sale of goods,

rendering of services and interest dividends and

royalties. Thus, it can be said that the company has

recognized their business revenue as per the

guidelines of AASB 15 and it provides the

management of the company with high flexibility.

Expenses (AASB 15

Paragraph 132 (a) and

(b))

Medium

It can be seen from the 2017 Annual Report of

Harvey Norman that Employee benefits expenses are

one major portion of the total expenses of the

company. As per the principles of this standard, the

company is needed to recognize their expenses at the

time of the outflow of future economic benefits.

Thus, due to the specific requirements of these

standards, the management of the company does not

have much flexibility in this as they do not have the

option to apply their own judgment while recognizing

the expenses.

Intangible Assets

(AASB 138)

High

Three major intangible assets of Harvey Norman are

computer software assets, capitalized development

expenditures and licensed properties; and the

company recognizes them on the cost value basis less

amortization and impairment. The company has the

obligation to test their intangible assets for

impairment in the presence of any indication of

impairment either individually or at the level of cash

generating units. In addition, the company determines

the useful lives on annual basis. This aspect indicates

towards the fact that the management of the company

(AASB 118)

High

can be seen that the majority potion of the revenue of

the company comes from the sale of goods. As per

AASB 118, the companies are needed to recognize

revenue from three major sources like sale of goods,

rendering of services and interest dividends and

royalties. Thus, it can be said that the company has

recognized their business revenue as per the

guidelines of AASB 15 and it provides the

management of the company with high flexibility.

Expenses (AASB 15

Paragraph 132 (a) and

(b))

Medium

It can be seen from the 2017 Annual Report of

Harvey Norman that Employee benefits expenses are

one major portion of the total expenses of the

company. As per the principles of this standard, the

company is needed to recognize their expenses at the

time of the outflow of future economic benefits.

Thus, due to the specific requirements of these

standards, the management of the company does not

have much flexibility in this as they do not have the

option to apply their own judgment while recognizing

the expenses.

Intangible Assets

(AASB 138)

High

Three major intangible assets of Harvey Norman are

computer software assets, capitalized development

expenditures and licensed properties; and the

company recognizes them on the cost value basis less

amortization and impairment. The company has the

obligation to test their intangible assets for

impairment in the presence of any indication of

impairment either individually or at the level of cash

generating units. In addition, the company determines

the useful lives on annual basis. This aspect indicates

towards the fact that the management of the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL REPORTING AND ANALYSIS

has scope to apply their own judgment or

assumptions at the time of the determination of the

presence of impairment of the intangible assets. Thus,

it can be said that the management of Harvey Norman

has the flexibility in the accounting of intangible

assets (Komninos and Cameron 2017)

Lease

(AASB 117)

High

This standard puts the obligating on the companies

not to distinguish between finance and operating

lease. It is visible from the annual report of Harvey

Norman that the company has distinguished between

the operating and finance leases for their business. As

per the annual report, the company has reported

$6432000 in 2017 and $10430000 in 2016 as total

finance lease receivable. In addition, the company has

reported $643597000 in 2017 and $593601000 in

2016 as total operating lease commitments. Thus, it

can be said that the management has flexibility in the

lease accounting.

Accounting Strategies

It can be observed from the 2017 Annual Report of Harvey Norman that the company has

adopted different strategies and the connection of these strategies can be seen with the

accounting policies of the company. The main aim of the adoption of the accounting policies of

Harvey Norman is the maximization of business as well as profitability (static1.squarespace.com

2018). Alignment of this policy can be seen with the strategy of the company to identify and

develop unique Flagship stores or a Franchised Flasgship complex in each of the operational

countries of the company. Major progress can be seen in this strategy for the financial year of

2017. Another major strategy of the company is the retail strategy in order to get steady as well

as reliable income throughout the financial year. According to the 2017 Annual Report, the

has scope to apply their own judgment or

assumptions at the time of the determination of the

presence of impairment of the intangible assets. Thus,

it can be said that the management of Harvey Norman

has the flexibility in the accounting of intangible

assets (Komninos and Cameron 2017)

Lease

(AASB 117)

High

This standard puts the obligating on the companies

not to distinguish between finance and operating

lease. It is visible from the annual report of Harvey

Norman that the company has distinguished between

the operating and finance leases for their business. As

per the annual report, the company has reported

$6432000 in 2017 and $10430000 in 2016 as total

finance lease receivable. In addition, the company has

reported $643597000 in 2017 and $593601000 in

2016 as total operating lease commitments. Thus, it

can be said that the management has flexibility in the

lease accounting.

Accounting Strategies

It can be observed from the 2017 Annual Report of Harvey Norman that the company has

adopted different strategies and the connection of these strategies can be seen with the

accounting policies of the company. The main aim of the adoption of the accounting policies of

Harvey Norman is the maximization of business as well as profitability (static1.squarespace.com

2018). Alignment of this policy can be seen with the strategy of the company to identify and

develop unique Flagship stores or a Franchised Flasgship complex in each of the operational

countries of the company. Major progress can be seen in this strategy for the financial year of

2017. Another major strategy of the company is the retail strategy in order to get steady as well

as reliable income throughout the financial year. According to the 2017 Annual Report, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL REPORTING AND ANALYSIS

Flagship strategy of Harvey Norman leads to a 30.8% rise in the profit before tax of the company

from $77.09 million to $100.68 million (static1.squarespace.com 2018).

In this context, it needs to be mentioned that the remuneration of the directors of Harvey

Norman largely depends on the achievement of financial strategies of the company along with

the incentives. The 2017 Annual Report of Harvey Norman states that the Short-Term Incentives

(STI) and Long-Term Incentives (LTI) re largely dependent on the outcome of the financial

performance of the company (static1.squarespace.com 2018). For example, the payment of the

LTIs for the directors of Harvey Norman large depends on the achievement of the objectives that

are utilization of the net assets of the company and the generation of wealth of the shareholders.

On the other hand, he payment of the STIs of the directors depends on the achievement of

desired profit level, Return on Investment and others (Bender 2013). This particular aspect

provides the directors of Harvey Norman with the intention to distort the financial information of

the company so that they can show higher amount of return on profit for gaining higher amount

of incentives. However, it needs to be mentioned that there is not any instances of such distortion

in the financial reporting of Harvey Norman (static1.squarespace.com 2018).

Quality of Disclosures

Disclosure of all the required financial information of the companies is considered as a

major pillar for the financial reporting success of the organizations (Lawrence 2013). According

to the 2017 Annual Report of Harvey Norman, the general purpose financial reports of the

organizations have been prepared by complying with the requirements of Corporations Act 2001,

Australian Accounting Standards and related pronouncements. It can also be seen from the 2017

Annual Report that the company has made compliance with the Australian Accounting Standard

Board (AASB), International Financial Reporting Standards (IFRS) and International

Accounting Standards Board (IASB) for the purpose of financial reporting.

Flagship strategy of Harvey Norman leads to a 30.8% rise in the profit before tax of the company

from $77.09 million to $100.68 million (static1.squarespace.com 2018).

In this context, it needs to be mentioned that the remuneration of the directors of Harvey

Norman largely depends on the achievement of financial strategies of the company along with

the incentives. The 2017 Annual Report of Harvey Norman states that the Short-Term Incentives

(STI) and Long-Term Incentives (LTI) re largely dependent on the outcome of the financial

performance of the company (static1.squarespace.com 2018). For example, the payment of the

LTIs for the directors of Harvey Norman large depends on the achievement of the objectives that

are utilization of the net assets of the company and the generation of wealth of the shareholders.

On the other hand, he payment of the STIs of the directors depends on the achievement of

desired profit level, Return on Investment and others (Bender 2013). This particular aspect

provides the directors of Harvey Norman with the intention to distort the financial information of

the company so that they can show higher amount of return on profit for gaining higher amount

of incentives. However, it needs to be mentioned that there is not any instances of such distortion

in the financial reporting of Harvey Norman (static1.squarespace.com 2018).

Quality of Disclosures

Disclosure of all the required financial information of the companies is considered as a

major pillar for the financial reporting success of the organizations (Lawrence 2013). According

to the 2017 Annual Report of Harvey Norman, the general purpose financial reports of the

organizations have been prepared by complying with the requirements of Corporations Act 2001,

Australian Accounting Standards and related pronouncements. It can also be seen from the 2017

Annual Report that the company has made compliance with the Australian Accounting Standard

Board (AASB), International Financial Reporting Standards (IFRS) and International

Accounting Standards Board (IASB) for the purpose of financial reporting.

8FINANCIAL REPORTING AND ANALYSIS

(Source: static1.squarespace.com 2018)

Apart from this, as per analysis of the annual report of Harvey Norman, it can be seen

that the company has released all the financial information for their investors and other users

with the help of the required financial statements such as Statement of Financial Position,

Income Statement, Statement of Comprehensive Income, Statement of Change in Equity and

Statement of Cash Flows (Quayes and Hasan 2014). Investors and other users can gain

underatsding about the financial position of the company from assessing these financial

statements. Most importantly, the company provides all the information related to the change in

the disclosure of the financial information in the annual reports so that the investors and users

can know about this. Thus, based on the above discussion, the company has made all the

required disclosures about the financial accounts of their business (static1.squarespace.com

2018).

Questionable Accounting Numbers

It needs to be mentioned that Harvey Norman has compiled with the guidelines of AASB

117 Leases for the purpose of lease accounting for the financial year of 2017. Under this lease

standard, Harvey Norman is needed to classify their business leases wither financial lease or

operating lease (Dakis 2016). Thus, the company is not needed to show the leases in the

statement of financial position if they are classified as operating lease; and thus, they are needed

to show in the profit or loss account as expenses in the profit or loss. However, it needs to be

mentioned that there are some leases that re non-cancellable and for this reason, the companies

are needed to consider them as liability and need to show them in the liability side of the

statement of financial position (Wong and Joshi 2015). In the absence of disclosure in the

statement of financial position, companies get the chance or scope to hide them from the balance

sheet; and this process is highly illegal and manipulative.

(Source: static1.squarespace.com 2018)

Apart from this, as per analysis of the annual report of Harvey Norman, it can be seen

that the company has released all the financial information for their investors and other users

with the help of the required financial statements such as Statement of Financial Position,

Income Statement, Statement of Comprehensive Income, Statement of Change in Equity and

Statement of Cash Flows (Quayes and Hasan 2014). Investors and other users can gain

underatsding about the financial position of the company from assessing these financial

statements. Most importantly, the company provides all the information related to the change in

the disclosure of the financial information in the annual reports so that the investors and users

can know about this. Thus, based on the above discussion, the company has made all the

required disclosures about the financial accounts of their business (static1.squarespace.com

2018).

Questionable Accounting Numbers

It needs to be mentioned that Harvey Norman has compiled with the guidelines of AASB

117 Leases for the purpose of lease accounting for the financial year of 2017. Under this lease

standard, Harvey Norman is needed to classify their business leases wither financial lease or

operating lease (Dakis 2016). Thus, the company is not needed to show the leases in the

statement of financial position if they are classified as operating lease; and thus, they are needed

to show in the profit or loss account as expenses in the profit or loss. However, it needs to be

mentioned that there are some leases that re non-cancellable and for this reason, the companies

are needed to consider them as liability and need to show them in the liability side of the

statement of financial position (Wong and Joshi 2015). In the absence of disclosure in the

statement of financial position, companies get the chance or scope to hide them from the balance

sheet; and this process is highly illegal and manipulative.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL REPORTING AND ANALYSIS

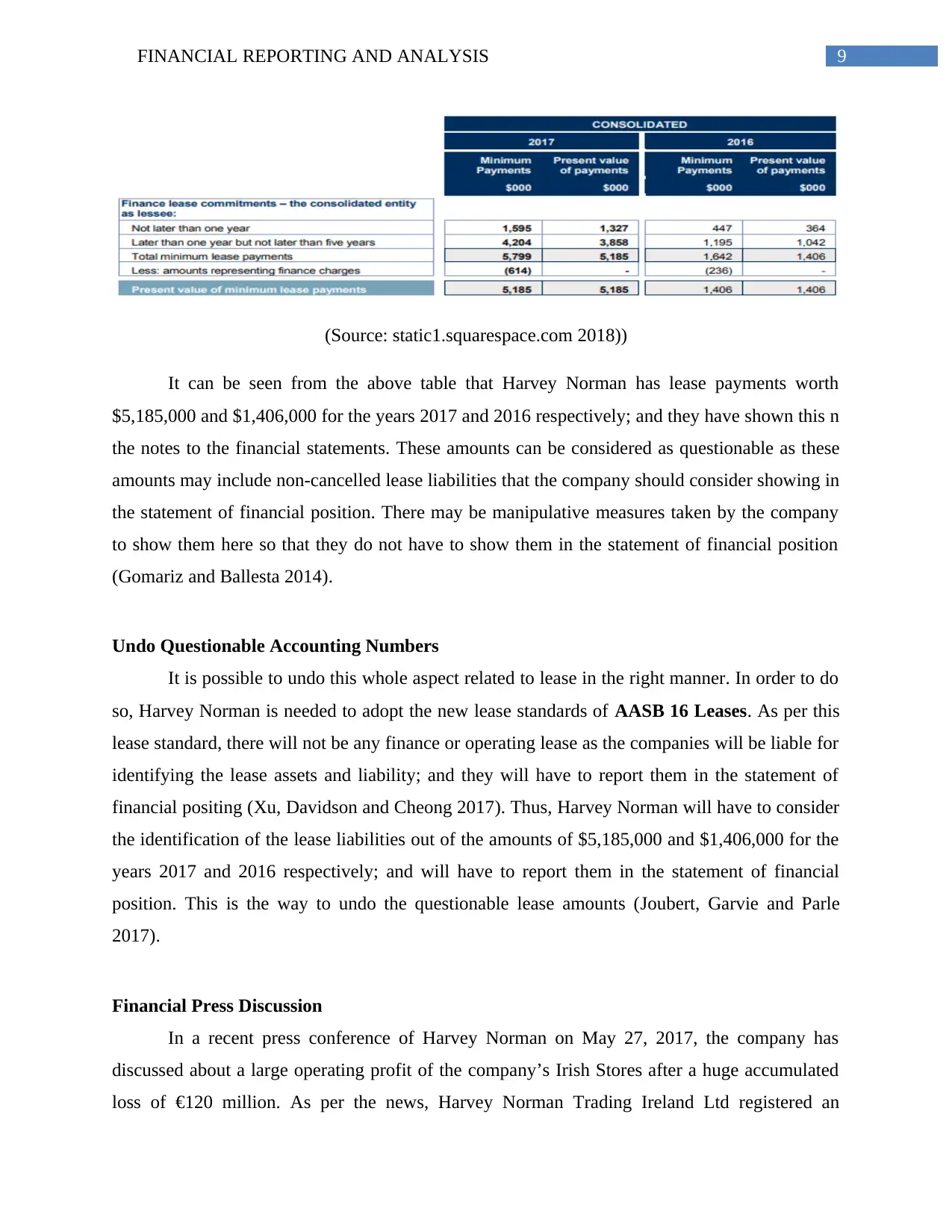

(Source: static1.squarespace.com 2018))

It can be seen from the above table that Harvey Norman has lease payments worth

$5,185,000 and $1,406,000 for the years 2017 and 2016 respectively; and they have shown this n

the notes to the financial statements. These amounts can be considered as questionable as these

amounts may include non-cancelled lease liabilities that the company should consider showing in

the statement of financial position. There may be manipulative measures taken by the company

to show them here so that they do not have to show them in the statement of financial position

(Gomariz and Ballesta 2014).

Undo Questionable Accounting Numbers

It is possible to undo this whole aspect related to lease in the right manner. In order to do

so, Harvey Norman is needed to adopt the new lease standards of AASB 16 Leases. As per this

lease standard, there will not be any finance or operating lease as the companies will be liable for

identifying the lease assets and liability; and they will have to report them in the statement of

financial positing (Xu, Davidson and Cheong 2017). Thus, Harvey Norman will have to consider

the identification of the lease liabilities out of the amounts of $5,185,000 and $1,406,000 for the

years 2017 and 2016 respectively; and will have to report them in the statement of financial

position. This is the way to undo the questionable lease amounts (Joubert, Garvie and Parle

2017).

Financial Press Discussion

In a recent press conference of Harvey Norman on May 27, 2017, the company has

discussed about a large operating profit of the company’s Irish Stores after a huge accumulated

loss of €120 million. As per the news, Harvey Norman Trading Ireland Ltd registered an

(Source: static1.squarespace.com 2018))

It can be seen from the above table that Harvey Norman has lease payments worth

$5,185,000 and $1,406,000 for the years 2017 and 2016 respectively; and they have shown this n

the notes to the financial statements. These amounts can be considered as questionable as these

amounts may include non-cancelled lease liabilities that the company should consider showing in

the statement of financial position. There may be manipulative measures taken by the company

to show them here so that they do not have to show them in the statement of financial position

(Gomariz and Ballesta 2014).

Undo Questionable Accounting Numbers

It is possible to undo this whole aspect related to lease in the right manner. In order to do

so, Harvey Norman is needed to adopt the new lease standards of AASB 16 Leases. As per this

lease standard, there will not be any finance or operating lease as the companies will be liable for

identifying the lease assets and liability; and they will have to report them in the statement of

financial positing (Xu, Davidson and Cheong 2017). Thus, Harvey Norman will have to consider

the identification of the lease liabilities out of the amounts of $5,185,000 and $1,406,000 for the

years 2017 and 2016 respectively; and will have to report them in the statement of financial

position. This is the way to undo the questionable lease amounts (Joubert, Garvie and Parle

2017).

Financial Press Discussion

In a recent press conference of Harvey Norman on May 27, 2017, the company has

discussed about a large operating profit of the company’s Irish Stores after a huge accumulated

loss of €120 million. As per the news, Harvey Norman Trading Ireland Ltd registered an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL REPORTING AND ANALYSIS

operating profit of €203,799 after the 12 months to the end of June 2016. This profit was majorly

boosted by a 13% increase in revenue from €158 million to €178 million. However, in the

presence of an interest amount of €1.4 million, there was a pre-tax loss of €1.2 million. However,

the profit after tax was a major relief for the management of the company

(harveynormanholdings.com.au 2018).

Conclusion

From the above discussion, it can be observed that Harvey Norman is a major Australian

company involves in different types of businesses like retail and others. The above discussion

sheds light on the fact that the company has adhered to the standards and principles of AASB 10

Consolidated Financial Statements for the preparation of their general purpose financial reports.

At the same time, compliance of the company can be seen with Corporations Act 2001, AASB,

IFRS and IASB. The management of Harvey Norman has huge flexibility in making accounting

judgments and estimates as they have stated in the financial statements that there may be

difference in the financial reporting results with the judgments and assumptions. After that, it can

be seen that the company has developed their business strategies with accordance to their

adopted financial and accenting policies; and the STIs and LTIs of the directors largely depend

on the financial performance of the company. Harvey Norman has disclosed all the required

financial information by complying with the required standards. Due to the not adoption of

AASB 16 Leases, there can be questions in the reported operating lease payments of the

company.

operating profit of €203,799 after the 12 months to the end of June 2016. This profit was majorly

boosted by a 13% increase in revenue from €158 million to €178 million. However, in the

presence of an interest amount of €1.4 million, there was a pre-tax loss of €1.2 million. However,

the profit after tax was a major relief for the management of the company

(harveynormanholdings.com.au 2018).

Conclusion

From the above discussion, it can be observed that Harvey Norman is a major Australian

company involves in different types of businesses like retail and others. The above discussion

sheds light on the fact that the company has adhered to the standards and principles of AASB 10

Consolidated Financial Statements for the preparation of their general purpose financial reports.

At the same time, compliance of the company can be seen with Corporations Act 2001, AASB,

IFRS and IASB. The management of Harvey Norman has huge flexibility in making accounting

judgments and estimates as they have stated in the financial statements that there may be

difference in the financial reporting results with the judgments and assumptions. After that, it can

be seen that the company has developed their business strategies with accordance to their

adopted financial and accenting policies; and the STIs and LTIs of the directors largely depend

on the financial performance of the company. Harvey Norman has disclosed all the required

financial information by complying with the required standards. Due to the not adoption of

AASB 16 Leases, there can be questions in the reported operating lease payments of the

company.

11FINANCIAL REPORTING AND ANALYSIS

References

Aasb.gov.au. (2018). [online] Available at:

http://www.aasb.gov.au/admin/file/content102/c3/SAC4_3-95.pdf [Accessed 17 Aug. 2018].

Beatty, A., Liao, S. and Yu, J.J., 2013. The spillover effect of fraudulent financial reporting on

peer firms' investments. Journal of Accounting and Economics, 55(2-3), pp.183-205.

Bender, R., 2013. Corporate financial strategy. Routledge.

Bentley, K.A., Omer, T.C. and Sharp, N.Y., 2013. Business strategy, financial reporting

irregularities, and audit effort. Contemporary Accounting Research, 30(2), pp.780-817.

Bisogno, M., Santis, S. and Tommasetti, A., 2015. Public-Sector consolidated financial

statements: An analysis of the comment letters on IPSASB’s exposure draft no. 49. International

Journal of Public Administration, 38(4), pp.311-324.

Dakis, G.S., 2016. Upcoming changes to contributions and leasing standards. Governance

Directions, 68(2), p.99.

Gomariz, M.F.C. and Ballesta, J.P.S., 2014. Financial reporting quality, debt maturity and

investment efficiency. Journal of Banking & Finance, 40, pp.494-506.

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. Journal

of New Business Ideas & Trends, 15(2).

Kim, J.B. and Zhang, L., 2014. Financial reporting opacity and expected crash risk: Evidence

from implied volatility smirks. Contemporary Accounting Research, 31(3), pp.851-875.

Komninos, J. and Cameron, R.B., 2017. IMPACTS OF REVENUE RECOGNITION

CHANGES IN THE CONSTRUCTION INDUSTRY.

Lawrence, A., 2013. Individual investors and financial disclosure. Journal of Accounting and

Economics, 56(1), pp.130-147.

Nobes, C., 2014. International classification of financial reporting. Routledge.

References

Aasb.gov.au. (2018). [online] Available at:

http://www.aasb.gov.au/admin/file/content102/c3/SAC4_3-95.pdf [Accessed 17 Aug. 2018].

Beatty, A., Liao, S. and Yu, J.J., 2013. The spillover effect of fraudulent financial reporting on

peer firms' investments. Journal of Accounting and Economics, 55(2-3), pp.183-205.

Bender, R., 2013. Corporate financial strategy. Routledge.

Bentley, K.A., Omer, T.C. and Sharp, N.Y., 2013. Business strategy, financial reporting

irregularities, and audit effort. Contemporary Accounting Research, 30(2), pp.780-817.

Bisogno, M., Santis, S. and Tommasetti, A., 2015. Public-Sector consolidated financial

statements: An analysis of the comment letters on IPSASB’s exposure draft no. 49. International

Journal of Public Administration, 38(4), pp.311-324.

Dakis, G.S., 2016. Upcoming changes to contributions and leasing standards. Governance

Directions, 68(2), p.99.

Gomariz, M.F.C. and Ballesta, J.P.S., 2014. Financial reporting quality, debt maturity and

investment efficiency. Journal of Banking & Finance, 40, pp.494-506.

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. Journal

of New Business Ideas & Trends, 15(2).

Kim, J.B. and Zhang, L., 2014. Financial reporting opacity and expected crash risk: Evidence

from implied volatility smirks. Contemporary Accounting Research, 31(3), pp.851-875.

Komninos, J. and Cameron, R.B., 2017. IMPACTS OF REVENUE RECOGNITION

CHANGES IN THE CONSTRUCTION INDUSTRY.

Lawrence, A., 2013. Individual investors and financial disclosure. Journal of Accounting and

Economics, 56(1), pp.130-147.

Nobes, C., 2014. International classification of financial reporting. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.