In-depth Financial Reporting and Analysis of Hikma Pharmaceuticals Plc

VerifiedAdded on 2023/06/15

|14

|3886

|148

Report

AI Summary

This report provides a financial analysis of Hikma Pharmaceuticals Plc, a British multinational pharmaceutical company. It critically discusses the importance of financial statements such as the statement of cash flows, statement of financial position, and income statement for financial reporting. The report evaluates Hikma Plc's financial performance based on profitability and investment ratios, including gross profit ratio, net profit ratio, return on capital employed, earning per share, and debt-to-equity ratio, comparing the company's performance in 2020 and 2019. Furthermore, it includes future expectations of Hikma Plc's performance based on current and past trends and analyzes the advantages and disadvantages of historical cost accounting. The analysis suggests areas for improvement in cost management and investment strategies to enhance the company's overall financial health. Desklib offers a range of solved assignments and resources for students.

FINANCIAL REPORTING

AND ANALYSIS -

ASSESSMENT 2 REPORT

AND ANALYSIS -

ASSESSMENT 2 REPORT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Background of Hikma Pharmaceuticals Plc................................................................................3

Critical discussion of importance of different financial statements meant for financial

reporting......................................................................................................................................4

Critical evaluation of Hikma Plc financial performance based on profitability and investment

ratios............................................................................................................................................6

Future expectations of the Hikma Plc performance based on its current and past performance 8

Critical analysis of the advantage and disadvantage of historical cost accounting...................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Background of Hikma Pharmaceuticals Plc................................................................................3

Critical discussion of importance of different financial statements meant for financial

reporting......................................................................................................................................4

Critical evaluation of Hikma Plc financial performance based on profitability and investment

ratios............................................................................................................................................6

Future expectations of the Hikma Plc performance based on its current and past performance 8

Critical analysis of the advantage and disadvantage of historical cost accounting...................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial reporting is considered to be an important part of financial analysis which

indicates financial health of the company and helps in enhancing financial resources along with

its efficient management within the business (Osadchy and et.al., 2018). For the purpose of

financial reporting, various financial statements are prepared such as balance sheet, income

statement and cash flow statement. The present report is based on Hikma Pharmaceutical Plc

which is headquartered in London, United Kingdom. The report includes critical discussion of

various financial statements, company's financial performance on the basis of investment and

profitability ratios, future expected performance of the company with regard to past and current

trends and at last, critical discussion of historical accounting will be done by stating its

advantages and disadvantages.

MAIN BODY

Background of Hikma Pharmaceuticals Plc

Hikma Pharmaceuticals Plc is basically a British multinational organization located in

London, UK founded in the year 1978 having the experience of 44 years in pharmaceuticals

industry. The company manufactures non-branded generic and in-licensed pharmaceuticals

products.

Key Features of Hikma Plc:

The company have broad global portfolio across diverse market which involve more than

650 compound dosage forms which make them leader in the market.

Hikma also have extensive and well-established manufacture footprints with high quality

along with its operations in more that 11 countries including Europe, MENA, US etc.

Another feature of the company is such that they have specialized team of research and

development which involve in the dosage forms and delivery system development.

Beside this, the company also have experience leadership team along with the strong

financial position (Kolsi, Ananzeh and Awawdeh, 2021).

In the year 2020, Hikma earns revenue and net profit of $2341 million and $430 million

respectively.

Presently, the company have around more than 780 products with 7 R&D centres and 31

manufacturing plants in 11 countries.

Financial reporting is considered to be an important part of financial analysis which

indicates financial health of the company and helps in enhancing financial resources along with

its efficient management within the business (Osadchy and et.al., 2018). For the purpose of

financial reporting, various financial statements are prepared such as balance sheet, income

statement and cash flow statement. The present report is based on Hikma Pharmaceutical Plc

which is headquartered in London, United Kingdom. The report includes critical discussion of

various financial statements, company's financial performance on the basis of investment and

profitability ratios, future expected performance of the company with regard to past and current

trends and at last, critical discussion of historical accounting will be done by stating its

advantages and disadvantages.

MAIN BODY

Background of Hikma Pharmaceuticals Plc

Hikma Pharmaceuticals Plc is basically a British multinational organization located in

London, UK founded in the year 1978 having the experience of 44 years in pharmaceuticals

industry. The company manufactures non-branded generic and in-licensed pharmaceuticals

products.

Key Features of Hikma Plc:

The company have broad global portfolio across diverse market which involve more than

650 compound dosage forms which make them leader in the market.

Hikma also have extensive and well-established manufacture footprints with high quality

along with its operations in more that 11 countries including Europe, MENA, US etc.

Another feature of the company is such that they have specialized team of research and

development which involve in the dosage forms and delivery system development.

Beside this, the company also have experience leadership team along with the strong

financial position (Kolsi, Ananzeh and Awawdeh, 2021).

In the year 2020, Hikma earns revenue and net profit of $2341 million and $430 million

respectively.

Presently, the company have around more than 780 products with 7 R&D centres and 31

manufacturing plants in 11 countries.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The total number of employees work with the Hikma Plc is around 8600 as per the

Hikma 2020 annual report.

Key Objectives of Hikma Plc:

The objective of Hikma company is provide high quality pharmaceuticals products to the

worldwide consumers in the most inclusive and affordable price.

With the help of their unique and established strategies, the aim of the company is to

offer clear proposition to investors.

Another objective of the company involve emphasizing accessibility, with the help of

which their products can benefit people around the world and further contribute towards

the sustainable development (Al-Jedaiah, 2021).

Also, the company purpose is to measure its progress using the key performance

indicators (KPI) such as return on capital invested etc.

Critical discussion of importance of different financial statements meant for financial reporting

There are various financial statements such as statement of cash flow, statement of financial

position and income statement that are being prepared for the purpose of reporting financial

results obtained at the end of each financial year to the external users of company's financial

information. These statements are of great importance for the purpose of providing financial

information to the external users of the company but also there are various limitations of these

financial statements that has been evaluated in the following section of this report.

Statement of cash flows

Cash flow statement provides important information pertaining to entity's liquidity

position by listing all the events related to movement of money from and into the company. With

the help of this statement, shareholders and investors are able to make out how much money a

concern is spending and making (Chen and et.al., 2019). Also, company's long term cash

planning can be done to ensure future growth where management undertakes vital changes in the

company to prioritize crucial business activities for better financial positioning. Furthermore,

optimal cash balance that is required to be maintained by company can be easily ascertained

because it is necessary to determine whether company has idle or shortage of funds. Working

capital management is one of the most important task of company's financial management as it

Hikma 2020 annual report.

Key Objectives of Hikma Plc:

The objective of Hikma company is provide high quality pharmaceuticals products to the

worldwide consumers in the most inclusive and affordable price.

With the help of their unique and established strategies, the aim of the company is to

offer clear proposition to investors.

Another objective of the company involve emphasizing accessibility, with the help of

which their products can benefit people around the world and further contribute towards

the sustainable development (Al-Jedaiah, 2021).

Also, the company purpose is to measure its progress using the key performance

indicators (KPI) such as return on capital invested etc.

Critical discussion of importance of different financial statements meant for financial reporting

There are various financial statements such as statement of cash flow, statement of financial

position and income statement that are being prepared for the purpose of reporting financial

results obtained at the end of each financial year to the external users of company's financial

information. These statements are of great importance for the purpose of providing financial

information to the external users of the company but also there are various limitations of these

financial statements that has been evaluated in the following section of this report.

Statement of cash flows

Cash flow statement provides important information pertaining to entity's liquidity

position by listing all the events related to movement of money from and into the company. With

the help of this statement, shareholders and investors are able to make out how much money a

concern is spending and making (Chen and et.al., 2019). Also, company's long term cash

planning can be done to ensure future growth where management undertakes vital changes in the

company to prioritize crucial business activities for better financial positioning. Furthermore,

optimal cash balance that is required to be maintained by company can be easily ascertained

because it is necessary to determine whether company has idle or shortage of funds. Working

capital management is one of the most important task of company's financial management as it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can have great influence over the business operations and cash flow statement provides useful

insights into how working capital is moving from and into the business.

However, statement of cash flow is affected from certain limitations as well like, it does

not indicate net income of the business due to not considering non-cash items. Also, just by

looking at the cash flow position of the business at the year doesn't seem to be sufficient for

ascertaining solvency and liquidity position. Furthermore, cash flow from operations depicted in

statement of cash flow is not sufficient for assessing firm's profitability as it never considers

revenues and cost of the business (Palepu and et.al., 2020). At last, cash flow statement does not

aid financial management team in predicting future cash flows of the company as it is prepared

on the basis of historical business transaction and just indicate how cash has move in and out of

the business during the given period what is still remains with the business at the end of this

period.

Statement of financial position

The basic purpose for which balance sheet or statement of financial position is being prepared is

to reflect upon the assets, equity and liabilities of the business. It is meant for revealing

company's financial position at a particular date (Hasanaj and Kuqi, 2019). The debt and equity

amount mentioned in this financial statement is helpful in determining long term solvency of the

company along with identifying how much capital does the owner have invested of their own

and how much has been borrowed from external lenders. This information is very important for

both internal management and investors of the company as it determines future performance and

position of a concern. Also, this financial statement indicates how financial activity has changed

during the period at the end of which statement has been prepared and in the absence of

information provided in it management may make poor financial decisions which might have

negative repercussions on business's financial standing.

On the other hand, there are various limitations of statement of financial position such as

the financial information contained in this statement is based on historical cost where no

consideration is being given to changes taking place pertaining to prices of its different elements

(Faccia and Mosco, 2019). Hence, balance sheet is not meant for conveying fruitful information

to make effective decisions. Also, those assets which cannot be measured in terms of money are

not included in balance sheet.

Income statement

insights into how working capital is moving from and into the business.

However, statement of cash flow is affected from certain limitations as well like, it does

not indicate net income of the business due to not considering non-cash items. Also, just by

looking at the cash flow position of the business at the year doesn't seem to be sufficient for

ascertaining solvency and liquidity position. Furthermore, cash flow from operations depicted in

statement of cash flow is not sufficient for assessing firm's profitability as it never considers

revenues and cost of the business (Palepu and et.al., 2020). At last, cash flow statement does not

aid financial management team in predicting future cash flows of the company as it is prepared

on the basis of historical business transaction and just indicate how cash has move in and out of

the business during the given period what is still remains with the business at the end of this

period.

Statement of financial position

The basic purpose for which balance sheet or statement of financial position is being prepared is

to reflect upon the assets, equity and liabilities of the business. It is meant for revealing

company's financial position at a particular date (Hasanaj and Kuqi, 2019). The debt and equity

amount mentioned in this financial statement is helpful in determining long term solvency of the

company along with identifying how much capital does the owner have invested of their own

and how much has been borrowed from external lenders. This information is very important for

both internal management and investors of the company as it determines future performance and

position of a concern. Also, this financial statement indicates how financial activity has changed

during the period at the end of which statement has been prepared and in the absence of

information provided in it management may make poor financial decisions which might have

negative repercussions on business's financial standing.

On the other hand, there are various limitations of statement of financial position such as

the financial information contained in this statement is based on historical cost where no

consideration is being given to changes taking place pertaining to prices of its different elements

(Faccia and Mosco, 2019). Hence, balance sheet is not meant for conveying fruitful information

to make effective decisions. Also, those assets which cannot be measured in terms of money are

not included in balance sheet.

Income statement

Income statement is helpful for management in deciding how business profitability can be

enhanced reducing costs, increasing revenues or both. The financial results obtained from this

financial statement indicates effectiveness of business strategies made by its management at the

beginning of the financial period. Also, with the help of this statement evaluation of past budgets

and creation of future budgets becomes possible for management along with the identification of

highly expensive areas requiring immediate actions for improvement. Furthermore, on the basis

of profitability shown in this statement, investment decisions are made by investors which

increases likelihood of additional capital investment in the company (Osadchy and et.al., 2018).

In addition to this, income statement are also required to be present to bankers and lenders on the

basis of which decision are made whether to extend financial support or not by them.

However, there are many limitations of income statement as well such as it is prepared

after completion of internal auditing which gives a room for manipulation of financial data and

results accordingly when there is no existence of internal control or auditing by external auditors.

Also, it is prepared by following various accounting methods and policies where changes in

methods and policies pertaining to the treatment of business transaction makes financial results

associated with different financial year non – comparable.

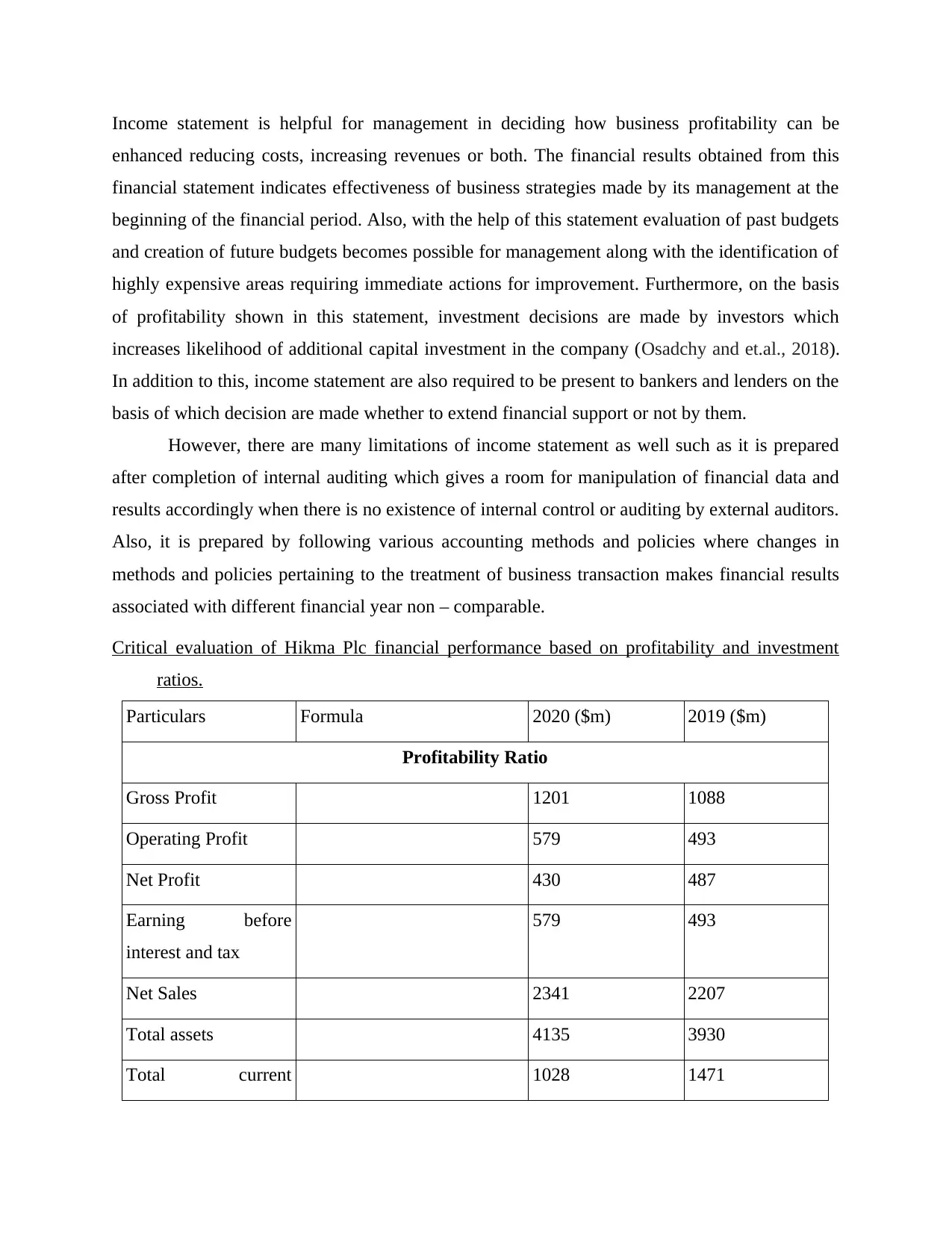

Critical evaluation of Hikma Plc financial performance based on profitability and investment

ratios.

Particulars Formula 2020 ($m) 2019 ($m)

Profitability Ratio

Gross Profit 1201 1088

Operating Profit 579 493

Net Profit 430 487

Earning before

interest and tax

579 493

Net Sales 2341 2207

Total assets 4135 3930

Total current 1028 1471

enhanced reducing costs, increasing revenues or both. The financial results obtained from this

financial statement indicates effectiveness of business strategies made by its management at the

beginning of the financial period. Also, with the help of this statement evaluation of past budgets

and creation of future budgets becomes possible for management along with the identification of

highly expensive areas requiring immediate actions for improvement. Furthermore, on the basis

of profitability shown in this statement, investment decisions are made by investors which

increases likelihood of additional capital investment in the company (Osadchy and et.al., 2018).

In addition to this, income statement are also required to be present to bankers and lenders on the

basis of which decision are made whether to extend financial support or not by them.

However, there are many limitations of income statement as well such as it is prepared

after completion of internal auditing which gives a room for manipulation of financial data and

results accordingly when there is no existence of internal control or auditing by external auditors.

Also, it is prepared by following various accounting methods and policies where changes in

methods and policies pertaining to the treatment of business transaction makes financial results

associated with different financial year non – comparable.

Critical evaluation of Hikma Plc financial performance based on profitability and investment

ratios.

Particulars Formula 2020 ($m) 2019 ($m)

Profitability Ratio

Gross Profit 1201 1088

Operating Profit 579 493

Net Profit 430 487

Earning before

interest and tax

579 493

Net Sales 2341 2207

Total assets 4135 3930

Total current 1028 1471

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

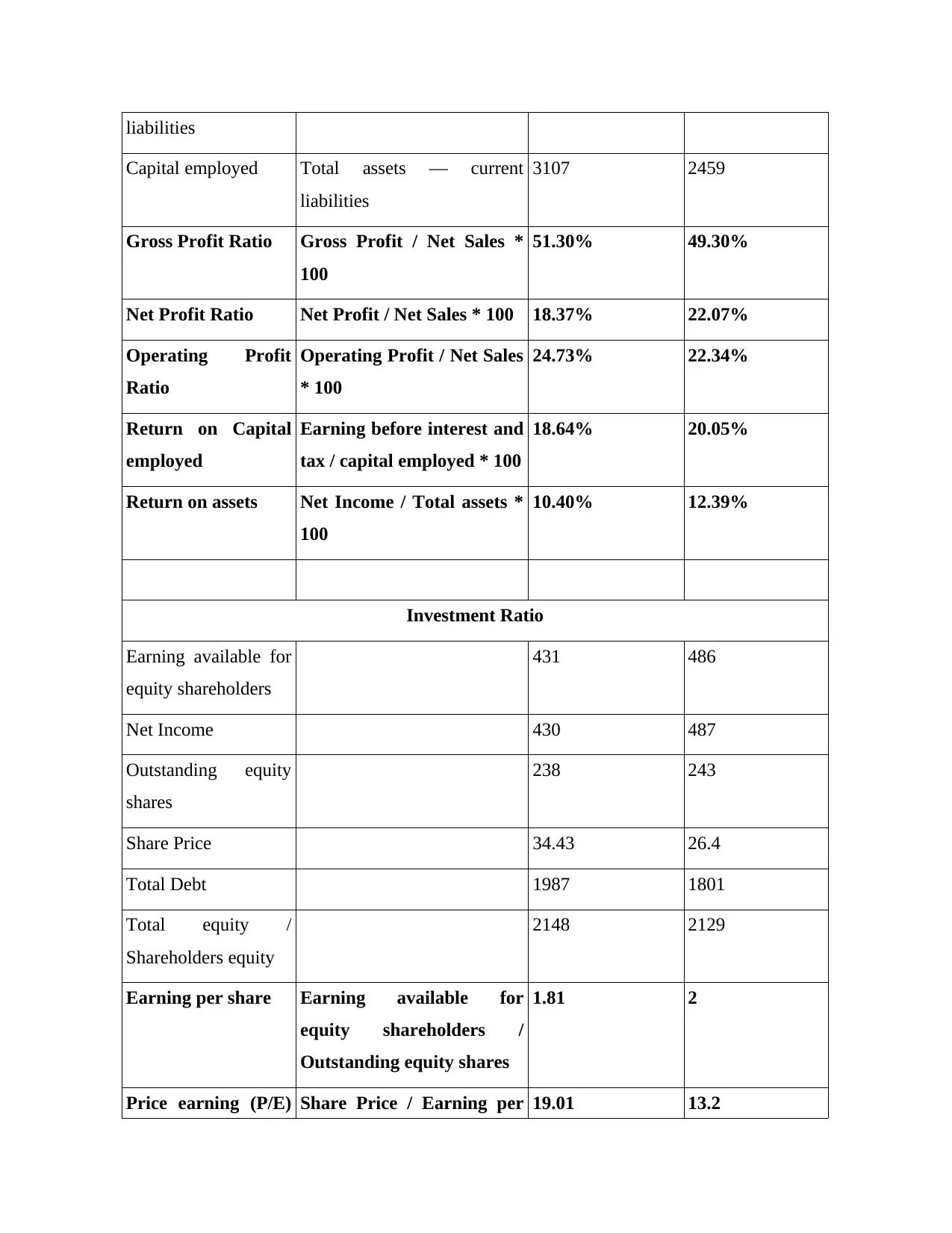

liabilities

Capital employed Total assets — current

liabilities

3107 2459

Gross Profit Ratio Gross Profit / Net Sales *

100

51.30% 49.30%

Net Profit Ratio Net Profit / Net Sales * 100 18.37% 22.07%

Operating Profit

Ratio

Operating Profit / Net Sales

* 100

24.73% 22.34%

Return on Capital

employed

Earning before interest and

tax / capital employed * 100

18.64% 20.05%

Return on assets Net Income / Total assets *

100

10.40% 12.39%

Investment Ratio

Earning available for

equity shareholders

431 486

Net Income 430 487

Outstanding equity

shares

238 243

Share Price 34.43 26.4

Total Debt 1987 1801

Total equity /

Shareholders equity

2148 2129

Earning per share Earning available for

equity shareholders /

Outstanding equity shares

1.81 2

Price earning (P/E) Share Price / Earning per 19.01 13.2

Capital employed Total assets — current

liabilities

3107 2459

Gross Profit Ratio Gross Profit / Net Sales *

100

51.30% 49.30%

Net Profit Ratio Net Profit / Net Sales * 100 18.37% 22.07%

Operating Profit

Ratio

Operating Profit / Net Sales

* 100

24.73% 22.34%

Return on Capital

employed

Earning before interest and

tax / capital employed * 100

18.64% 20.05%

Return on assets Net Income / Total assets *

100

10.40% 12.39%

Investment Ratio

Earning available for

equity shareholders

431 486

Net Income 430 487

Outstanding equity

shares

238 243

Share Price 34.43 26.4

Total Debt 1987 1801

Total equity /

Shareholders equity

2148 2129

Earning per share Earning available for

equity shareholders /

Outstanding equity shares

1.81 2

Price earning (P/E) Share Price / Earning per 19.01 13.2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

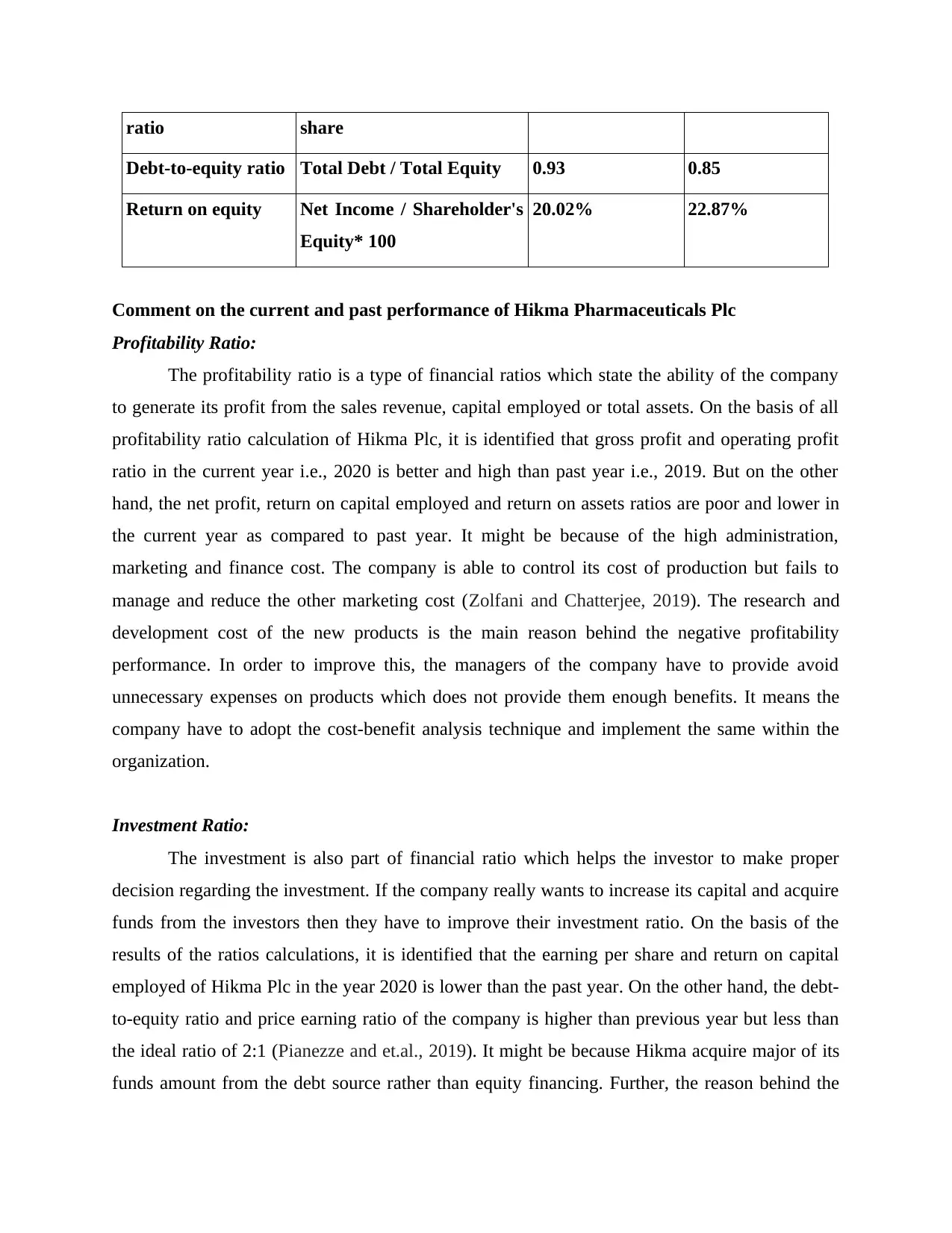

ratio share

Debt-to-equity ratio Total Debt / Total Equity 0.93 0.85

Return on equity Net Income / Shareholder's

Equity* 100

20.02% 22.87%

Comment on the current and past performance of Hikma Pharmaceuticals Plc

Profitability Ratio:

The profitability ratio is a type of financial ratios which state the ability of the company

to generate its profit from the sales revenue, capital employed or total assets. On the basis of all

profitability ratio calculation of Hikma Plc, it is identified that gross profit and operating profit

ratio in the current year i.e., 2020 is better and high than past year i.e., 2019. But on the other

hand, the net profit, return on capital employed and return on assets ratios are poor and lower in

the current year as compared to past year. It might be because of the high administration,

marketing and finance cost. The company is able to control its cost of production but fails to

manage and reduce the other marketing cost (Zolfani and Chatterjee, 2019). The research and

development cost of the new products is the main reason behind the negative profitability

performance. In order to improve this, the managers of the company have to provide avoid

unnecessary expenses on products which does not provide them enough benefits. It means the

company have to adopt the cost-benefit analysis technique and implement the same within the

organization.

Investment Ratio:

The investment is also part of financial ratio which helps the investor to make proper

decision regarding the investment. If the company really wants to increase its capital and acquire

funds from the investors then they have to improve their investment ratio. On the basis of the

results of the ratios calculations, it is identified that the earning per share and return on capital

employed of Hikma Plc in the year 2020 is lower than the past year. On the other hand, the debt-

to-equity ratio and price earning ratio of the company is higher than previous year but less than

the ideal ratio of 2:1 (Pianezze and et.al., 2019). It might be because Hikma acquire major of its

funds amount from the debt source rather than equity financing. Further, the reason behind the

Debt-to-equity ratio Total Debt / Total Equity 0.93 0.85

Return on equity Net Income / Shareholder's

Equity* 100

20.02% 22.87%

Comment on the current and past performance of Hikma Pharmaceuticals Plc

Profitability Ratio:

The profitability ratio is a type of financial ratios which state the ability of the company

to generate its profit from the sales revenue, capital employed or total assets. On the basis of all

profitability ratio calculation of Hikma Plc, it is identified that gross profit and operating profit

ratio in the current year i.e., 2020 is better and high than past year i.e., 2019. But on the other

hand, the net profit, return on capital employed and return on assets ratios are poor and lower in

the current year as compared to past year. It might be because of the high administration,

marketing and finance cost. The company is able to control its cost of production but fails to

manage and reduce the other marketing cost (Zolfani and Chatterjee, 2019). The research and

development cost of the new products is the main reason behind the negative profitability

performance. In order to improve this, the managers of the company have to provide avoid

unnecessary expenses on products which does not provide them enough benefits. It means the

company have to adopt the cost-benefit analysis technique and implement the same within the

organization.

Investment Ratio:

The investment is also part of financial ratio which helps the investor to make proper

decision regarding the investment. If the company really wants to increase its capital and acquire

funds from the investors then they have to improve their investment ratio. On the basis of the

results of the ratios calculations, it is identified that the earning per share and return on capital

employed of Hikma Plc in the year 2020 is lower than the past year. On the other hand, the debt-

to-equity ratio and price earning ratio of the company is higher than previous year but less than

the ideal ratio of 2:1 (Pianezze and et.al., 2019). It might be because Hikma acquire major of its

funds amount from the debt source rather than equity financing. Further, the reason behind the

poor performance of the company's investment ratio is such that they have low net income. Thus,

in order to improve the overall investment performance, the managers of the company need to

first start acquire funds from the debt and second increasing net income of the company.

Future expectations of the Hikma Plc performance based on its current and past performance

Based on the current and past performance of Hikma Plc in the market, it is identified

that in the current year the overall performance of the company is poor as compared to the

previous one. That's why the following improvement measures in expected from the company in

the future: Issuance of more equity rather than debt: It is expected from Hikma company that they

should acquire more funds from the debt rather than equity. It is because this helps them

in improving the EPS and debt-to-equity ratio of the company. Further, it will also help

the company in increasing the net income of the business. It is because more debts helps

the company in reducing the tax expenses as debt provides tax saving benefits to the

companies. Focus on driving sales up: Another think that is expected from the pharmaceuticals

company name Hikma in the upcoming year is adoption of various ways to increase

sales. Because of the Covid-19, the company has faces lots of decrements in their sales.

So, in order to improve this it is expected from the company that they will adopt cross

selling and up selling rules. Here, managers of Hikma need to train its staff regarding

how they can influence and suggest customers about their prescription and non-

prescription products (Dunlop and et.al., 2018). Sales of outdated assets: The company have to sales its assets which are outdated and are

of no use. It is because this helps them in arranging the space for other equipments along

with generating cash. Thus, it is also expected from the Hikam Pharmaceuticals Plc that

they will also sale its all outdated assets such as plant and equipments in the market

which are of no use. Technologies shaping the future: It is also expected from the Hikma company that they

should opt for the digital methods in order to improve the performance of the company. It

means the company have to incorporate the digital service to its customer in which the

online doorstep delivery of pharmaceuticals products to the consumers are involved

in order to improve the overall investment performance, the managers of the company need to

first start acquire funds from the debt and second increasing net income of the company.

Future expectations of the Hikma Plc performance based on its current and past performance

Based on the current and past performance of Hikma Plc in the market, it is identified

that in the current year the overall performance of the company is poor as compared to the

previous one. That's why the following improvement measures in expected from the company in

the future: Issuance of more equity rather than debt: It is expected from Hikma company that they

should acquire more funds from the debt rather than equity. It is because this helps them

in improving the EPS and debt-to-equity ratio of the company. Further, it will also help

the company in increasing the net income of the business. It is because more debts helps

the company in reducing the tax expenses as debt provides tax saving benefits to the

companies. Focus on driving sales up: Another think that is expected from the pharmaceuticals

company name Hikma in the upcoming year is adoption of various ways to increase

sales. Because of the Covid-19, the company has faces lots of decrements in their sales.

So, in order to improve this it is expected from the company that they will adopt cross

selling and up selling rules. Here, managers of Hikma need to train its staff regarding

how they can influence and suggest customers about their prescription and non-

prescription products (Dunlop and et.al., 2018). Sales of outdated assets: The company have to sales its assets which are outdated and are

of no use. It is because this helps them in arranging the space for other equipments along

with generating cash. Thus, it is also expected from the Hikam Pharmaceuticals Plc that

they will also sale its all outdated assets such as plant and equipments in the market

which are of no use. Technologies shaping the future: It is also expected from the Hikma company that they

should opt for the digital methods in order to improve the performance of the company. It

means the company have to incorporate the digital service to its customer in which the

online doorstep delivery of pharmaceuticals products to the consumers are involved

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Shibata and Suzuki, 2018). Further, it can also be expected from the company that they

will start giving online prescription to the patients so that they need not come to their

stores. Artificial Intelligence: This is another and most crucial way which will help Hikma

Pharmaceuticals company in improving its performance in the upcoming years after the

pandemic. Here, the company basically need to incorporate AI in the medical decision-

making. In this, the company can select processes for clinical trials which further helps in

quickly analysing and identifying the best candidates for the trial purpose. In addition,

Hikma can also use AI in medicine which means the use of the same for the diagnosis

and treatment of the patients that requires special care for their special diseases.

3D Printing: Based on the current and past performance, it is also analysed that the

profitability and investment performance of Hikma is poor in current year. So, in order to

improve the same, it is expected from the company that they must go with the trends and

one of the most demanding trend is present time. Here, the company will be able to

commercialize printing tablets. In simple term, the 3D printing provides opportunity to

the pharmaceuticals business in producing the tablets and drugs with more than one

active substance which is basically characterized by the different properties and profiles.

Thus, it is also expected from Hikma that they will also implement and improve the same

within their business (Struble and et.al., 2020).

Critical analysis of the advantage and disadvantage of historical cost accounting

Historical Cost accounting: This is a method of accounting in which the company have

to record its assets at original value. For example, Hikma Plc will record its assets at cost and

ignores the revaluation of the assets when they opt for the historical cost accounting. The various

advantage and disadvantages of historical cost accounting which need to be understood by the

managers of the Hikma Pharmaceuticals Plc are as follows:

Advantages: Objectivity and reliability of accounting concept: The benefit of this accounting method

is that it does not consider and included the increase and decrease in the value of the

assets in the financial statement. For example, Hikma Plc can verify the accuracy of the

reported amount with the source documents such as invoices, official receipts.

will start giving online prescription to the patients so that they need not come to their

stores. Artificial Intelligence: This is another and most crucial way which will help Hikma

Pharmaceuticals company in improving its performance in the upcoming years after the

pandemic. Here, the company basically need to incorporate AI in the medical decision-

making. In this, the company can select processes for clinical trials which further helps in

quickly analysing and identifying the best candidates for the trial purpose. In addition,

Hikma can also use AI in medicine which means the use of the same for the diagnosis

and treatment of the patients that requires special care for their special diseases.

3D Printing: Based on the current and past performance, it is also analysed that the

profitability and investment performance of Hikma is poor in current year. So, in order to

improve the same, it is expected from the company that they must go with the trends and

one of the most demanding trend is present time. Here, the company will be able to

commercialize printing tablets. In simple term, the 3D printing provides opportunity to

the pharmaceuticals business in producing the tablets and drugs with more than one

active substance which is basically characterized by the different properties and profiles.

Thus, it is also expected from Hikma that they will also implement and improve the same

within their business (Struble and et.al., 2020).

Critical analysis of the advantage and disadvantage of historical cost accounting

Historical Cost accounting: This is a method of accounting in which the company have

to record its assets at original value. For example, Hikma Plc will record its assets at cost and

ignores the revaluation of the assets when they opt for the historical cost accounting. The various

advantage and disadvantages of historical cost accounting which need to be understood by the

managers of the Hikma Pharmaceuticals Plc are as follows:

Advantages: Objectivity and reliability of accounting concept: The benefit of this accounting method

is that it does not consider and included the increase and decrease in the value of the

assets in the financial statement. For example, Hikma Plc can verify the accuracy of the

reported amount with the source documents such as invoices, official receipts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Simplicity and Convenience: This concept of accounting is quite simple and convenient

for the company in which they need not the make changes in the financial statement as

per the change in the value of assets. For example, in case if Hikma Plc really wants to

avoid the additional cost such as hiring of appraisers relating to assets revaluation than

they have to adopt this method of accounting within the business.

Consistency and Comparability of financial statement: This method is also helpful for

comparing the intra and inter financial statements of the company. For example, with the

help of historical cost accounting method Hikma company can assess whether the

financial performance and cash flows and improving or decreasing over the span of time

(Yusuf and Idris, 2021).

Disadvantages: Do not consider actual value of assets: The historical accounting does not consider the

actual value of assets and focuses only on the cost distribution. So, in case if Hikma

company adopt the investors will not able to get enough information regarding the

current value of assets. Ignores inflation: This is also one of the significant cons of method that it does not

consider the inflation factors in recording assets in financial statement. The impact of

which the chance of making poor and wrong decision such as purchase and sales of assets

is taken by Hikma.

Loss to company: As this method does not consider revaluation principle, which might

cause heavy loss to the company. It is because of recording the assets at more value while

in market the value of such assets is low. The high cost and low sales value leads to loss

to company (Cristea, 2018).

CONCLUSION

The report has critically concluded the importance of statement of cash flow, financial

position and income statement for the external users of Hikma Pharmaceuticals Plc. Further, the

report has also calculated the profitability and investment ratio. On the basis of which, it is

concluded that the performance of Hikma in the current year is poor as compared to previous

year. Further, the report has suggested some ways which is expected from Hikma that they

for the company in which they need not the make changes in the financial statement as

per the change in the value of assets. For example, in case if Hikma Plc really wants to

avoid the additional cost such as hiring of appraisers relating to assets revaluation than

they have to adopt this method of accounting within the business.

Consistency and Comparability of financial statement: This method is also helpful for

comparing the intra and inter financial statements of the company. For example, with the

help of historical cost accounting method Hikma company can assess whether the

financial performance and cash flows and improving or decreasing over the span of time

(Yusuf and Idris, 2021).

Disadvantages: Do not consider actual value of assets: The historical accounting does not consider the

actual value of assets and focuses only on the cost distribution. So, in case if Hikma

company adopt the investors will not able to get enough information regarding the

current value of assets. Ignores inflation: This is also one of the significant cons of method that it does not

consider the inflation factors in recording assets in financial statement. The impact of

which the chance of making poor and wrong decision such as purchase and sales of assets

is taken by Hikma.

Loss to company: As this method does not consider revaluation principle, which might

cause heavy loss to the company. It is because of recording the assets at more value while

in market the value of such assets is low. The high cost and low sales value leads to loss

to company (Cristea, 2018).

CONCLUSION

The report has critically concluded the importance of statement of cash flow, financial

position and income statement for the external users of Hikma Pharmaceuticals Plc. Further, the

report has also calculated the profitability and investment ratio. On the basis of which, it is

concluded that the performance of Hikma in the current year is poor as compared to previous

year. Further, the report has suggested some ways which is expected from Hikma that they

should implement the same within their business for improvement of business in the future.

Lastly, the report has concluded the advantage and disadvantage of historical cost accounting to

Hikam company management.

Lastly, the report has concluded the advantage and disadvantage of historical cost accounting to

Hikam company management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.