Holmes Institute: HI6025 - IFRS Adoption and Financial Reporting

VerifiedAdded on 2023/01/13

|5

|799

|48

Report

AI Summary

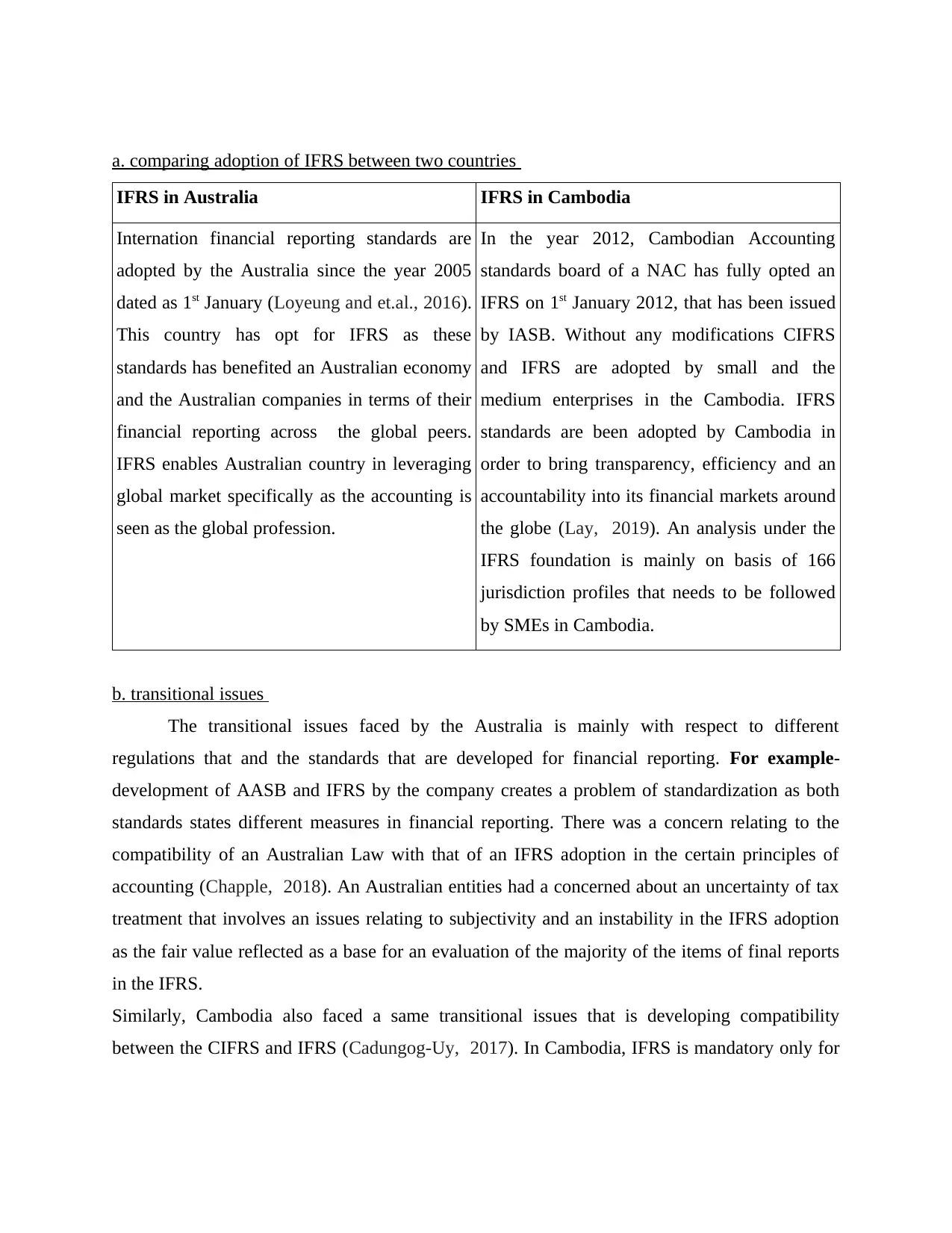

This report critically examines the adoption of International Financial Reporting Standards (IFRS) and its usefulness to Australian reporting entities. The analysis includes a comparison of IFRS adoption between Australia and Cambodia, highlighting the different approaches and impacts in each country. The report delves into the transitional issues faced by entities during IFRS implementation, such as the challenges of standardizing financial reporting and the concerns regarding compatibility with existing laws and regulations. Furthermore, it explores the challenges related to accounting concepts like materiality and going concern. The report also references relevant literature, including books and journals, to support its findings and provide a comprehensive understanding of the topic. The report is a solution to the Holmes Institute HI6025 Accounting Theory and Current Issues assignment, and it addresses the key issues of adopting IFRSs and recommends future directions to the national accounting setting bodies.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.