Financial Reporting Report: Conceptual Framework, Analysis, and IFRS

VerifiedAdded on 2021/02/19

|18

|5635

|211

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, encompassing its context, purpose, and benefits to stakeholders. It delves into the conceptual and regulatory frameworks, including key principles and qualitative characteristics, while also examining the main financial statements such as the profit and loss statement and the statement of changes in equity. The report explores the value of financial reporting in meeting organizational objectives and driving growth, with a focus on interpretation and communication of financial performance. It also highlights the differences between IAS and IFRS, the advantages of the international financial reporting system, and the degree of compliance with IFRS standards. The report includes detailed financial statements, providing practical examples and insights into financial analysis and reporting practices, specifically referencing the practices of KPMG.

Financial

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Context and purpose of financial reporting.............................................................................1

2. Conceptual, regulatory framework, key principle and qualitative characteristics..................2

3. Main Stakeholder and benefit to financial information..........................................................3

4. Value of financial reporting to meet objective and growth.....................................................5

5. Main Financial Statements......................................................................................................5

6. Interpretation and communication of financial performance..................................................8

7. Differences between IAS and IFRS........................................................................................9

8. Advantages of International financial reporting system.......................................................10

9. Degree of compliance with IFRS..........................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Context and purpose of financial reporting.............................................................................1

2. Conceptual, regulatory framework, key principle and qualitative characteristics..................2

3. Main Stakeholder and benefit to financial information..........................................................3

4. Value of financial reporting to meet objective and growth.....................................................5

5. Main Financial Statements......................................................................................................5

6. Interpretation and communication of financial performance..................................................8

7. Differences between IAS and IFRS........................................................................................9

8. Advantages of International financial reporting system.......................................................10

9. Degree of compliance with IFRS..........................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

In the present time, every type of business has different departments to conduct business

activities and present daily operational activities in a successful way. It helps to achieve

organizational goals and objectives (Bennett, James and Klinkers, 2017) . The functioning of

these sections are based on other departments but mainly connected with accounting and finance

section which are provided useful resources to present different types of business activities. The

main concept of financial reporting is connected with the disclosure of meaningful financial

information which presents in front of stakeholders. On the basis of this information, they can

analyse overall performance and present situation of company in a particular period of time. At

the end of accounting process present some typical factors of financial reporting like financial

statements, annual reports, catalogue, and management analysis and decision. To better

understand concept of financial reporting KPMG one of the largest financial accounting

organization which provide several financial services.

In the report consist of purpose, benefits to stakeholder, conceptual and regulatory

frameworks and value of financial reporting for a company is discussed. Apart from the report,

differences between IAS and IFRS, an advantage of IFRS and degree of compliances are

discussed respectively. Additionally, prepare different types of financial statements such as

balance sheet, statement of equity and income statements using financial information.

TASK 1

1. Context and purpose of financial reporting

In current times, financial reporting plays a significant role in the world economy and it

will provide authentic and reliable financial information to owner of company. This financial

information present through financial statements like balance sheet, income statement, and

statement of changes in equity. On the basis of these statements they analysis of overall

performance then take effective decisions to improve profit margin. These statements are

prepared on an annual basis and summarise the real performance of several operations and staff

members. Financial reporting consists of disclosure of financial information to top management

which is defined about the performance of an organization in a specific period of time (Chen,

Zhang and Zhou, 2018) .

1

In the present time, every type of business has different departments to conduct business

activities and present daily operational activities in a successful way. It helps to achieve

organizational goals and objectives (Bennett, James and Klinkers, 2017) . The functioning of

these sections are based on other departments but mainly connected with accounting and finance

section which are provided useful resources to present different types of business activities. The

main concept of financial reporting is connected with the disclosure of meaningful financial

information which presents in front of stakeholders. On the basis of this information, they can

analyse overall performance and present situation of company in a particular period of time. At

the end of accounting process present some typical factors of financial reporting like financial

statements, annual reports, catalogue, and management analysis and decision. To better

understand concept of financial reporting KPMG one of the largest financial accounting

organization which provide several financial services.

In the report consist of purpose, benefits to stakeholder, conceptual and regulatory

frameworks and value of financial reporting for a company is discussed. Apart from the report,

differences between IAS and IFRS, an advantage of IFRS and degree of compliances are

discussed respectively. Additionally, prepare different types of financial statements such as

balance sheet, statement of equity and income statements using financial information.

TASK 1

1. Context and purpose of financial reporting

In current times, financial reporting plays a significant role in the world economy and it

will provide authentic and reliable financial information to owner of company. This financial

information present through financial statements like balance sheet, income statement, and

statement of changes in equity. On the basis of these statements they analysis of overall

performance then take effective decisions to improve profit margin. These statements are

prepared on an annual basis and summarise the real performance of several operations and staff

members. Financial reporting consists of disclosure of financial information to top management

which is defined about the performance of an organization in a specific period of time (Chen,

Zhang and Zhou, 2018) .

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps in further investments and generates profit through various operations. It is getting that

financial statements important for KPMG to meet the necessity then apply with an appropriate

accounting system. It enables to provide the right information that is important to make a future

investment decision. There are defined purpose of financial reporting, that are as follows:

The main purpose of financial reporting management connect with effective decision

making and concerning the objective of business as well as overall strategies.

It will help to provide reliable and appropriate information to those stakeholders who are

connected with company and help in decision-making process.

This support in several appearances like information connected to credit to a customer,

lend of the borrower and either to invest in a particular business or move to another

alternative.

The financial reports of a company provide important information which is connected

with net inflows and outflows of cash within an organization. There are including

appropriate time and unprofitable activities that will determine of liquidity of a company.

The financial data help to management recognize strengths and weaknesses of company

and also about overall financial health.

In case if there are a number of subdivision or partner working within main organization

then financial reporting must act as main part of a crucial agreement in between various

sections which make easy for stakeholders and investor to have enough knowledge

regarding money (Cohen, 2017) .

2. Conceptual, regulatory framework, key principle and qualitative characteristics

Conceptual and Regulatory framework:

The concept of financial reporting is connected with financial reports which define about

the different financial types of statements that help in decision making process for future

improvement. There are various stakeholders who is directly connected with annual financial

position as well as position of business, they are investors, creditors, financial institutions and

general public who wants to become part of business sharing. A regulatory framework of

business beneficial due to valuable predication for improving efficiency of financial standards

and principles. It will provide support to control financial activities in efficient manner. The

selected company follow the procedure and principle of IFRS which is as follows:

2

financial statements important for KPMG to meet the necessity then apply with an appropriate

accounting system. It enables to provide the right information that is important to make a future

investment decision. There are defined purpose of financial reporting, that are as follows:

The main purpose of financial reporting management connect with effective decision

making and concerning the objective of business as well as overall strategies.

It will help to provide reliable and appropriate information to those stakeholders who are

connected with company and help in decision-making process.

This support in several appearances like information connected to credit to a customer,

lend of the borrower and either to invest in a particular business or move to another

alternative.

The financial reports of a company provide important information which is connected

with net inflows and outflows of cash within an organization. There are including

appropriate time and unprofitable activities that will determine of liquidity of a company.

The financial data help to management recognize strengths and weaknesses of company

and also about overall financial health.

In case if there are a number of subdivision or partner working within main organization

then financial reporting must act as main part of a crucial agreement in between various

sections which make easy for stakeholders and investor to have enough knowledge

regarding money (Cohen, 2017) .

2. Conceptual, regulatory framework, key principle and qualitative characteristics

Conceptual and Regulatory framework:

The concept of financial reporting is connected with financial reports which define about

the different financial types of statements that help in decision making process for future

improvement. There are various stakeholders who is directly connected with annual financial

position as well as position of business, they are investors, creditors, financial institutions and

general public who wants to become part of business sharing. A regulatory framework of

business beneficial due to valuable predication for improving efficiency of financial standards

and principles. It will provide support to control financial activities in efficient manner. The

selected company follow the procedure and principle of IFRS which is as follows:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The particular reports provides valuable ideas that can support for determine the necessity

of total amount which is essential to survive business operations in successful way.

It is advantageous for creating and managing the financial information as per the

requirement of accounting standards.

These are supporting for develop good image of company with the help of increase

growth and grab opportunities (Hanlon, 2018).

Qualitative Characteristics of financial reporting

It is understand that financial reporting must have different types of qualitative

characteristics that will support to management to make decision. It will depend on the financial

reports which is reliable and more faithful. Some of these are discussed below: Relevance – It support to make effectual differences within the decision make by user

and it is defined about the corroborative and predictive amount. Faithful Representation – According to this it is defined after completed of report and

can not find any error then present in front of those stakeholders who is related with

company. Timeliness – It is essential for company to provide reliable and accurate information to

stakeholders. These are preparing in particular period of time such as quarterly, monthly

and annually basis.

Understandability – The provided information must be clear, classified and concisely

which is easily under stable by end user.

3. Main Stakeholder and benefit to financial information

Stakeholders are important part of any business who can invest to run business. They are

influenced to business growth and performance in direct and indirect manner. There are included

creditors, suppliers, government, customers, investors or the society. These are connected with

company with different interest as per the involvement groups. These are categorised into

internal and external entity. KPMG has different interest groups which kind of a consortium of

stakeholders for it (Indrawati, 2017) .

There are two types of stakeholders in a business unit -

Internal stakeholders

These are considering as internal members of an organisation who is connected with

internal activities and influenced by any results of the business actions.

3

of total amount which is essential to survive business operations in successful way.

It is advantageous for creating and managing the financial information as per the

requirement of accounting standards.

These are supporting for develop good image of company with the help of increase

growth and grab opportunities (Hanlon, 2018).

Qualitative Characteristics of financial reporting

It is understand that financial reporting must have different types of qualitative

characteristics that will support to management to make decision. It will depend on the financial

reports which is reliable and more faithful. Some of these are discussed below: Relevance – It support to make effectual differences within the decision make by user

and it is defined about the corroborative and predictive amount. Faithful Representation – According to this it is defined after completed of report and

can not find any error then present in front of those stakeholders who is related with

company. Timeliness – It is essential for company to provide reliable and accurate information to

stakeholders. These are preparing in particular period of time such as quarterly, monthly

and annually basis.

Understandability – The provided information must be clear, classified and concisely

which is easily under stable by end user.

3. Main Stakeholder and benefit to financial information

Stakeholders are important part of any business who can invest to run business. They are

influenced to business growth and performance in direct and indirect manner. There are included

creditors, suppliers, government, customers, investors or the society. These are connected with

company with different interest as per the involvement groups. These are categorised into

internal and external entity. KPMG has different interest groups which kind of a consortium of

stakeholders for it (Indrawati, 2017) .

There are two types of stakeholders in a business unit -

Internal stakeholders

These are considering as internal members of an organisation who is connected with

internal activities and influenced by any results of the business actions.

3

Board of Directors – These types of stakeholders afraid about the administration of the

company. These members are taking strategic decision regarding to functioning of the

business entity. If organisational performance goes down so they will influenced by

corporate position. In KPMG, Board of directors consider as first line of defence. The

assure about employee appointment, agreements, regulatory norms and preparation of

policies.

Employees – They are part of internal stakeholders and afraid about those business

activities which is directly related to employment security, monetary benefits and non

monetary benefits. Staff members of KPMG are connected on different levels thus have

various types of associate with clients (Kaspersen and Johansen, 2016) .

External stakeholders

These types of stakeholders have no interest with the daily activities of the business but

in a way or another duly influenced by the activity which is taken by an organisation. The

selected company KPMG, it is composed broad lodge of external stakeholders including majorly

of governments, investors and creditors. Investors – These types of investors are investing their money in the business and include

of debt holders and share holders. On their investing money expect good rate of return. It

is mainly depended on the market value of a company. The investors of KPMG in

proportionate ratio of debt to equity. To satisfy of their customers KPMG has performed

in effective manner. Creditors – They are providing loans, goods, services and other advantages to a business.

The creditors of a company expect to timely return of the debt along with the interest. So

they wants to good financial position and survive for long time in market because they

totally depended on profit of a company.

Government – It is a part of external stakeholder of any business due to collect corporate

taxes, payroll taxes and other taxes like GST. Every organisation paid tax to government

for contribute in GDP to increase growth rate and reduction of unemployment which

related with any government (Kurt, 2018).

4. Value of financial reporting to meet objective and growth

The financial statement are helpful for every organisation which can help to attain their

objectives of an organisation (Young, Cohen and Bens, 2018). Most of the companies use

4

company. These members are taking strategic decision regarding to functioning of the

business entity. If organisational performance goes down so they will influenced by

corporate position. In KPMG, Board of directors consider as first line of defence. The

assure about employee appointment, agreements, regulatory norms and preparation of

policies.

Employees – They are part of internal stakeholders and afraid about those business

activities which is directly related to employment security, monetary benefits and non

monetary benefits. Staff members of KPMG are connected on different levels thus have

various types of associate with clients (Kaspersen and Johansen, 2016) .

External stakeholders

These types of stakeholders have no interest with the daily activities of the business but

in a way or another duly influenced by the activity which is taken by an organisation. The

selected company KPMG, it is composed broad lodge of external stakeholders including majorly

of governments, investors and creditors. Investors – These types of investors are investing their money in the business and include

of debt holders and share holders. On their investing money expect good rate of return. It

is mainly depended on the market value of a company. The investors of KPMG in

proportionate ratio of debt to equity. To satisfy of their customers KPMG has performed

in effective manner. Creditors – They are providing loans, goods, services and other advantages to a business.

The creditors of a company expect to timely return of the debt along with the interest. So

they wants to good financial position and survive for long time in market because they

totally depended on profit of a company.

Government – It is a part of external stakeholder of any business due to collect corporate

taxes, payroll taxes and other taxes like GST. Every organisation paid tax to government

for contribute in GDP to increase growth rate and reduction of unemployment which

related with any government (Kurt, 2018).

4. Value of financial reporting to meet objective and growth

The financial statement are helpful for every organisation which can help to attain their

objectives of an organisation (Young, Cohen and Bens, 2018). Most of the companies use

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial reports foe analysis overall performance and actual situation in present time of

company. It helps to develop plan and strategies as per the requirement and financial reports

interprets the financial information in effective manner. Such as in the KPMG company, they

develop several type of financial statements due to accomplish their goals and objectives. With

the help of financial report a company achieve their objectives in particular period of time.

Financial Reporting and development of organisation

With the help of financial reports develop business because it reflects on the financial

position of the companies. These are helping to take effective decision for further investments.

Such as an organisation wants to spread out of their business operations. For this need to analysis

of financial documents and if there is profit then they may expand. So it is said that financial

reporting important part of any organisation and help in development of the companies. The

selected company take effective decision on the basis of development for their venture.

Additionally, in the absence of these financial reports it is difficult to understand about the

companies and take decision about the development (Menicucci and Paolucci, 2016) .

Financial reporting and growth of business

Apart from it, the financial statements are considering as important part of any

organisation which plays role in the development of the business. Through these reports present

all financial data in front of internal and external stakeholders. On the basis of these reports they

can analysis of financial performance of an organisation. If company have good market position

so investors will increase and take interest to invest in particular company. The efficiency of a

business improve after followed of financial accounting and presenting the financial statement on

time. The selected organisation KPMG limited produce financial statements that help them in

growth.

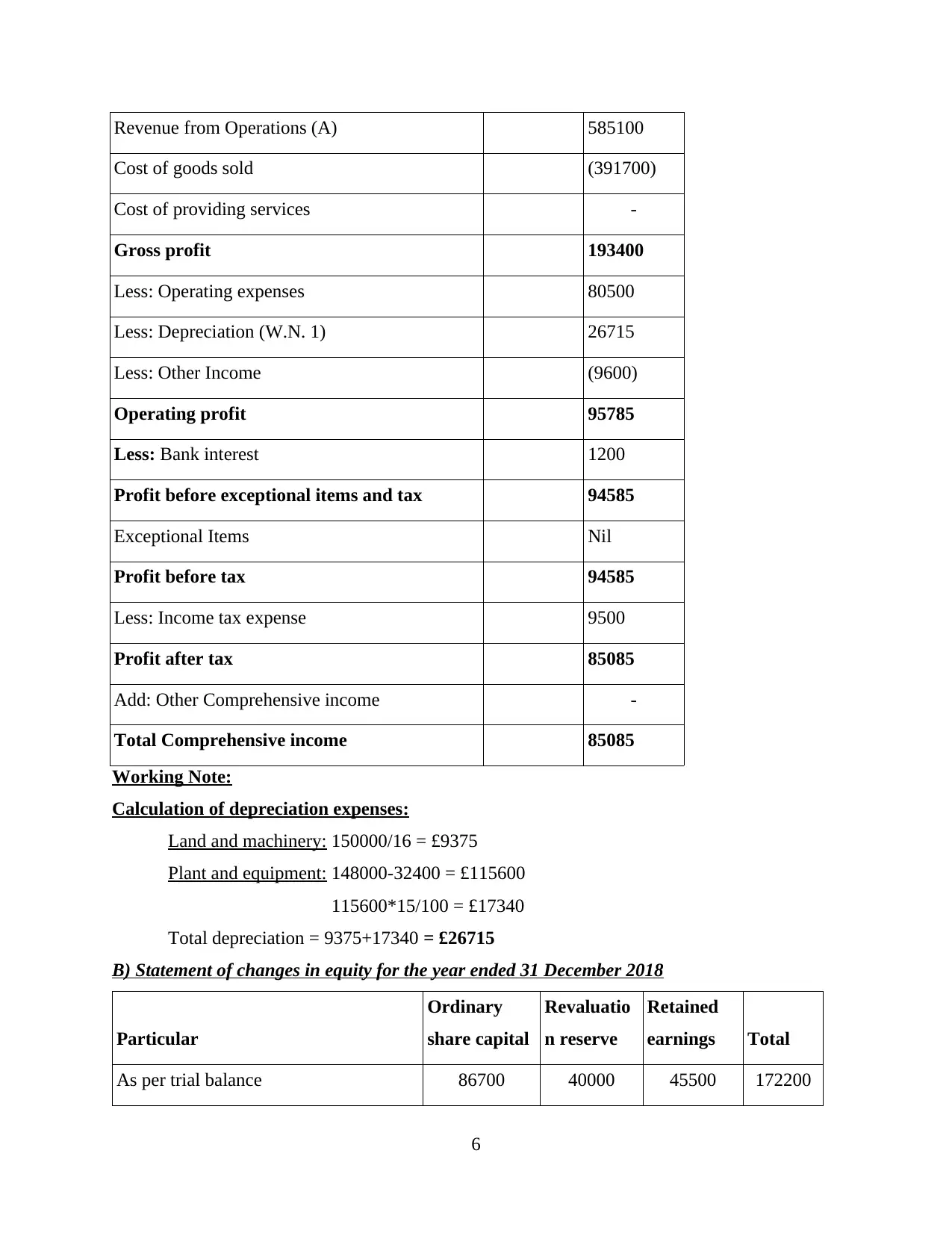

5. Main Financial Statements

A) Profit and Loss statement

31.12.18

(£'000)

Continuing operations

Particulars Amount

5

company. It helps to develop plan and strategies as per the requirement and financial reports

interprets the financial information in effective manner. Such as in the KPMG company, they

develop several type of financial statements due to accomplish their goals and objectives. With

the help of financial report a company achieve their objectives in particular period of time.

Financial Reporting and development of organisation

With the help of financial reports develop business because it reflects on the financial

position of the companies. These are helping to take effective decision for further investments.

Such as an organisation wants to spread out of their business operations. For this need to analysis

of financial documents and if there is profit then they may expand. So it is said that financial

reporting important part of any organisation and help in development of the companies. The

selected company take effective decision on the basis of development for their venture.

Additionally, in the absence of these financial reports it is difficult to understand about the

companies and take decision about the development (Menicucci and Paolucci, 2016) .

Financial reporting and growth of business

Apart from it, the financial statements are considering as important part of any

organisation which plays role in the development of the business. Through these reports present

all financial data in front of internal and external stakeholders. On the basis of these reports they

can analysis of financial performance of an organisation. If company have good market position

so investors will increase and take interest to invest in particular company. The efficiency of a

business improve after followed of financial accounting and presenting the financial statement on

time. The selected organisation KPMG limited produce financial statements that help them in

growth.

5. Main Financial Statements

A) Profit and Loss statement

31.12.18

(£'000)

Continuing operations

Particulars Amount

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue from Operations (A) 585100

Cost of goods sold (391700)

Cost of providing services -

Gross profit 193400

Less: Operating expenses 80500

Less: Depreciation (W.N. 1) 26715

Less: Other Income (9600)

Operating profit 95785

Less: Bank interest 1200

Profit before exceptional items and tax 94585

Exceptional Items Nil

Profit before tax 94585

Less: Income tax expense 9500

Profit after tax 85085

Add: Other Comprehensive income -

Total Comprehensive income 85085

Working Note:

Calculation of depreciation expenses:

Land and machinery: 150000/16 = £9375

Plant and equipment: 148000-32400 = £115600

115600*15/100 = £17340

Total depreciation = 9375+17340 = £26715

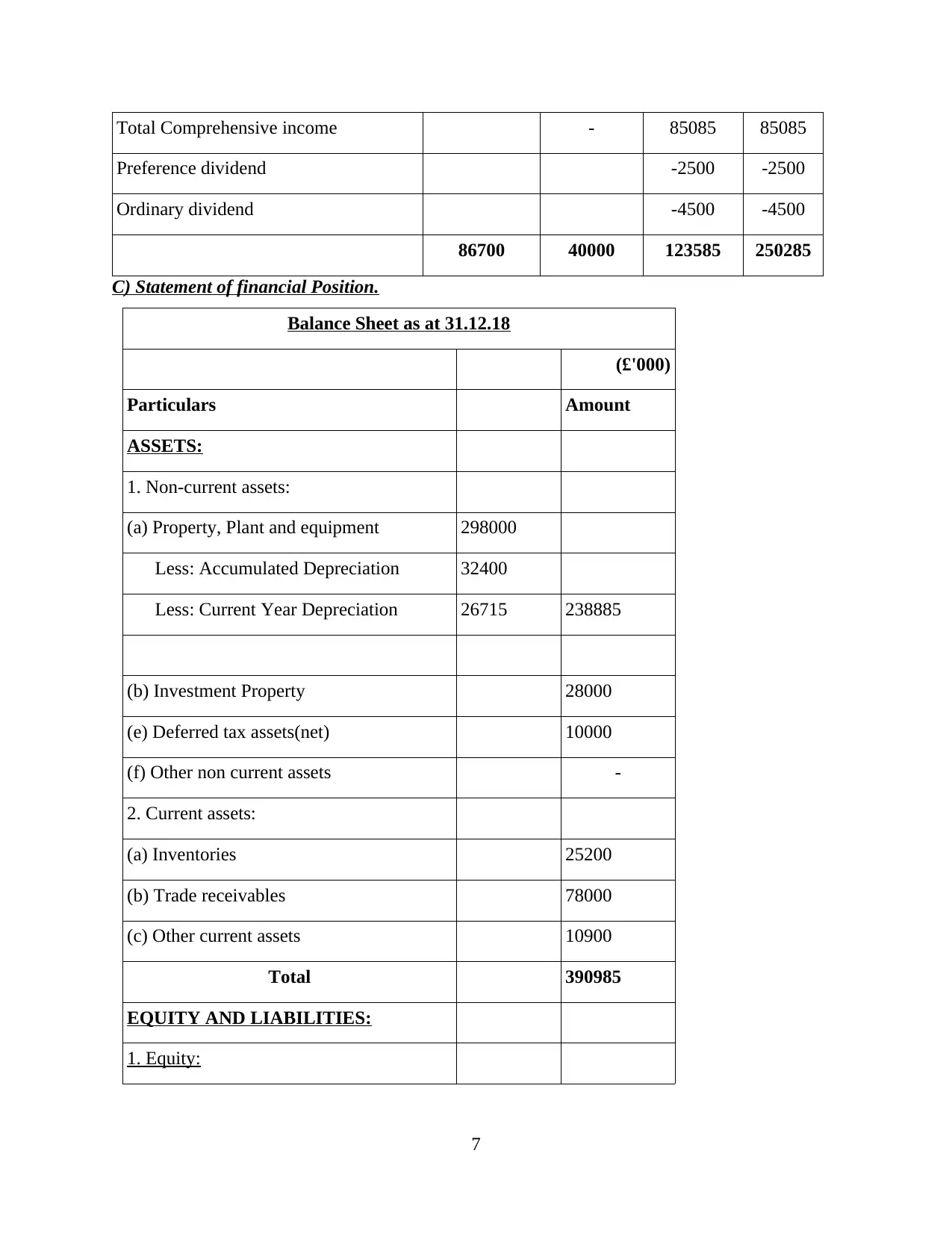

B) Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluatio

n reserve

Retained

earnings Total

As per trial balance 86700 40000 45500 172200

6

Cost of goods sold (391700)

Cost of providing services -

Gross profit 193400

Less: Operating expenses 80500

Less: Depreciation (W.N. 1) 26715

Less: Other Income (9600)

Operating profit 95785

Less: Bank interest 1200

Profit before exceptional items and tax 94585

Exceptional Items Nil

Profit before tax 94585

Less: Income tax expense 9500

Profit after tax 85085

Add: Other Comprehensive income -

Total Comprehensive income 85085

Working Note:

Calculation of depreciation expenses:

Land and machinery: 150000/16 = £9375

Plant and equipment: 148000-32400 = £115600

115600*15/100 = £17340

Total depreciation = 9375+17340 = £26715

B) Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluatio

n reserve

Retained

earnings Total

As per trial balance 86700 40000 45500 172200

6

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

C) Statement of financial Position.

Balance Sheet as at 31.12.18

(£'000)

Particulars Amount

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

1. Equity:

7

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

C) Statement of financial Position.

Balance Sheet as at 31.12.18

(£'000)

Particulars Amount

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

1. Equity:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(a) Ordinary share capital 86700

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

(a) Deferred Taxation -

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD -

(c) Provision for current tax 9500

Total 355985

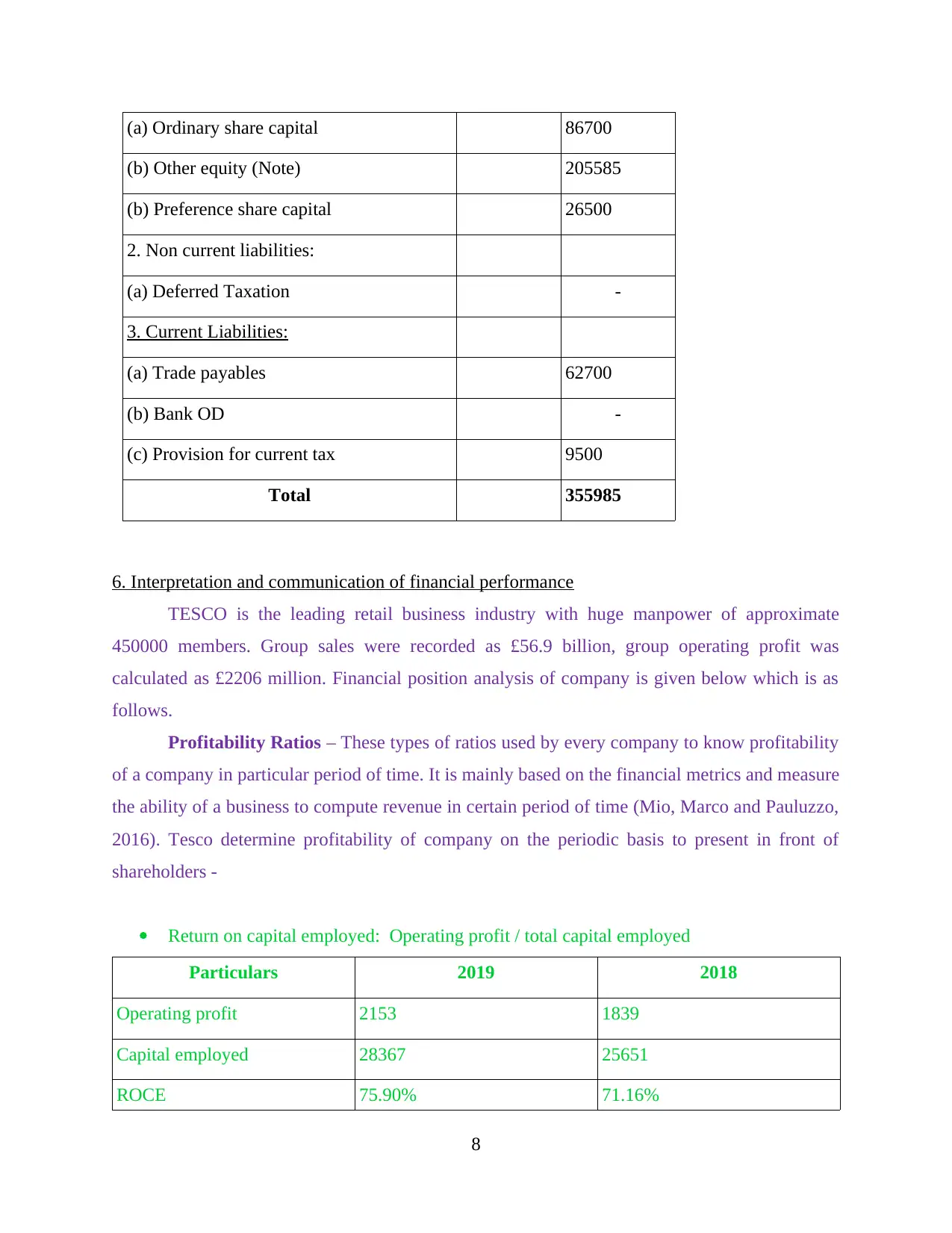

6. Interpretation and communication of financial performance

TESCO is the leading retail business industry with huge manpower of approximate

450000 members. Group sales were recorded as £56.9 billion, group operating profit was

calculated as £2206 million. Financial position analysis of company is given below which is as

follows.

Profitability Ratios – These types of ratios used by every company to know profitability

of a company in particular period of time. It is mainly based on the financial metrics and measure

the ability of a business to compute revenue in certain period of time (Mio, Marco and Pauluzzo,

2016). Tesco determine profitability of company on the periodic basis to present in front of

shareholders -

Return on capital employed: Operating profit / total capital employed

Particulars 2019 2018

Operating profit 2153 1839

Capital employed 28367 25651

ROCE 75.90% 71.16%

8

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

(a) Deferred Taxation -

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD -

(c) Provision for current tax 9500

Total 355985

6. Interpretation and communication of financial performance

TESCO is the leading retail business industry with huge manpower of approximate

450000 members. Group sales were recorded as £56.9 billion, group operating profit was

calculated as £2206 million. Financial position analysis of company is given below which is as

follows.

Profitability Ratios – These types of ratios used by every company to know profitability

of a company in particular period of time. It is mainly based on the financial metrics and measure

the ability of a business to compute revenue in certain period of time (Mio, Marco and Pauluzzo,

2016). Tesco determine profitability of company on the periodic basis to present in front of

shareholders -

Return on capital employed: Operating profit / total capital employed

Particulars 2019 2018

Operating profit 2153 1839

Capital employed 28367 25651

ROCE 75.90% 71.16%

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation- On the basis of above calculation, this can be analysed that ROCE of tesco

company is different in both of years. Such as in year 2018, it is of 71.16% which raised in next

year and became of 75.90%.

Return on equity: Profit after interest, tax and dividend / total equity

Particulars 2019 2018

Profit after interest, tax and

dividend

1320 1210

Total equity 14834 10480

Return on equity 0.89 : 1 0.12 : 1

Interpretation- On the basis of above table, this can be analysed that in year 2018, the return for 1

equity is of 12 p. While in year return for 1 equity is of 89 p. This shows that company's position

is better in year 2019.

Net profit margin ratio: Net profit / revenue * 100

Particular 2019 2018

Net profit 2153 1839

Revenue 63911 57493

Net profit margin 2153 / 63911 * 100 = 3.39% 1839 / 57493 = 3.20%

Interpretation: From the above table it is getting that net profit ratio in 2019 good for

company rather than to 2018. Net profit margin for the year 2019 was recorded as 3.39% and

3.20% for the year 2018. This indicates that company's financial position of above company in

year 2019 as compare to year 2018.

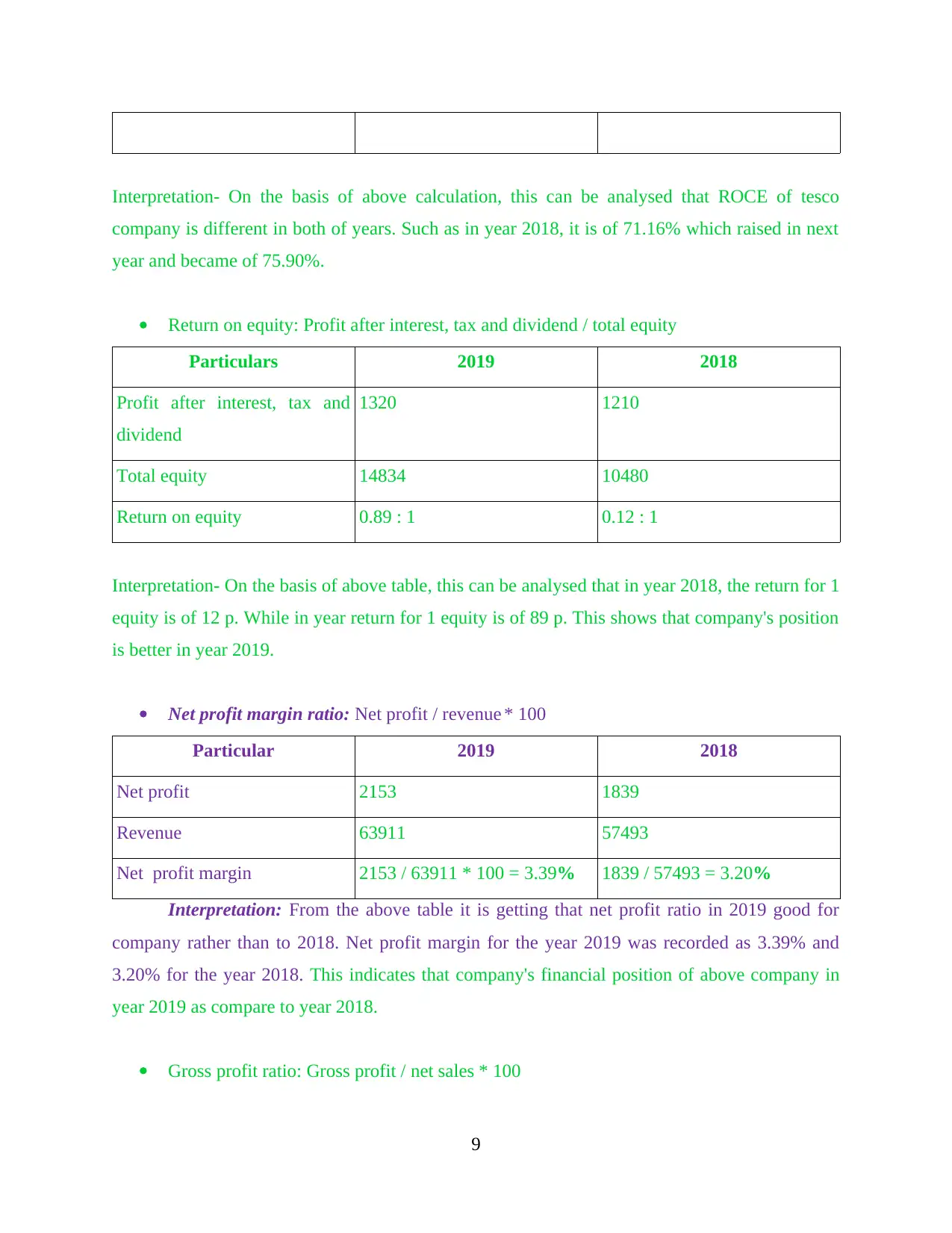

Gross profit ratio: Gross profit / net sales * 100

9

company is different in both of years. Such as in year 2018, it is of 71.16% which raised in next

year and became of 75.90%.

Return on equity: Profit after interest, tax and dividend / total equity

Particulars 2019 2018

Profit after interest, tax and

dividend

1320 1210

Total equity 14834 10480

Return on equity 0.89 : 1 0.12 : 1

Interpretation- On the basis of above table, this can be analysed that in year 2018, the return for 1

equity is of 12 p. While in year return for 1 equity is of 89 p. This shows that company's position

is better in year 2019.

Net profit margin ratio: Net profit / revenue * 100

Particular 2019 2018

Net profit 2153 1839

Revenue 63911 57493

Net profit margin 2153 / 63911 * 100 = 3.39% 1839 / 57493 = 3.20%

Interpretation: From the above table it is getting that net profit ratio in 2019 good for

company rather than to 2018. Net profit margin for the year 2019 was recorded as 3.39% and

3.20% for the year 2018. This indicates that company's financial position of above company in

year 2019 as compare to year 2018.

Gross profit ratio: Gross profit / net sales * 100

9

Particular 2019 amount in (£ million) 2018 amount in (£ million)

Gross profit 4144 3352

Revenue 63911 57493

Gross profit margin 4144 / 63911 * 100 = 6.48% 3352 / 57493 = 5.83%

Interpretation- On the basis of above table this can be analysed that company's gross

profit in year 2018 is of 5.83% that increased in next year and became of 6.48%.

Liquidity Ratio – It is considering as essential class of financial metrics applied to analysis of

ability to debtors to pay off current debt responsibility without arising external capital. It is

mainly applied to measure liquidity of a company and their margin of safety. A determination of

liquidity ratio of Tesco whether it has enough liquid funds to meet in short term.

Current Ratio - Current assets / current liabilities

Particular 2019 amount in (£ million) 2018 amount in (£ million)

Current assets 12570 13600

Current liabilities 20680 19233

Current ratio 12570 / 20680 = 0.60 13600 / 19233 = 0.70

Interpretation: From the above table it has been analysed that current ratio of the

company did not meet with ideal ratio of 2:1 and stable in both years in 2019 and 2018. The

ratio for 2019 was calculated as 0.61 times and 0.70 was calculated for the year 2018. Current

assets get decreased that may enlarge the lag in period to suppliers and creditors.

Quick Ratio: Quick assets / current liabilities

Particular 2019 amount in (£ million) 2018 amount in (£ million)

Quick assets 12570-2617 = 9953 13600-2264 =11336

Current liabilities 20680 19233

Quick ratio 0.48 times 0.58 times

Interpretation: As per the above table it is understand that in 2019 the quick ratio of the

company 0.48 times which is not near about the ideal ratio of 1:1 but in 2018 it is getting

10

Gross profit 4144 3352

Revenue 63911 57493

Gross profit margin 4144 / 63911 * 100 = 6.48% 3352 / 57493 = 5.83%

Interpretation- On the basis of above table this can be analysed that company's gross

profit in year 2018 is of 5.83% that increased in next year and became of 6.48%.

Liquidity Ratio – It is considering as essential class of financial metrics applied to analysis of

ability to debtors to pay off current debt responsibility without arising external capital. It is

mainly applied to measure liquidity of a company and their margin of safety. A determination of

liquidity ratio of Tesco whether it has enough liquid funds to meet in short term.

Current Ratio - Current assets / current liabilities

Particular 2019 amount in (£ million) 2018 amount in (£ million)

Current assets 12570 13600

Current liabilities 20680 19233

Current ratio 12570 / 20680 = 0.60 13600 / 19233 = 0.70

Interpretation: From the above table it has been analysed that current ratio of the

company did not meet with ideal ratio of 2:1 and stable in both years in 2019 and 2018. The

ratio for 2019 was calculated as 0.61 times and 0.70 was calculated for the year 2018. Current

assets get decreased that may enlarge the lag in period to suppliers and creditors.

Quick Ratio: Quick assets / current liabilities

Particular 2019 amount in (£ million) 2018 amount in (£ million)

Quick assets 12570-2617 = 9953 13600-2264 =11336

Current liabilities 20680 19233

Quick ratio 0.48 times 0.58 times

Interpretation: As per the above table it is understand that in 2019 the quick ratio of the

company 0.48 times which is not near about the ideal ratio of 1:1 but in 2018 it is getting

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.