Financial Reporting: M&S Financial Performance, IFRS, and Stakeholders

VerifiedAdded on 2020/10/23

|12

|3378

|200

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, focusing on Marks & Spencer (M&S). It begins by defining financial reporting's context and purpose, emphasizing its role in communicating financial information to stakeholders, including investors, creditors, and management. The report then delves into the regulatory and conceptual framework, highlighting the importance of key principles and qualitative characteristics in ensuring reliable financial information. It identifies M&S's main stakeholders and the benefits they derive from financial reporting, such as informed decision-making and performance evaluation. The report explores how financial reporting contributes to organizational growth and objectives, emphasizing its role in attracting investment and guiding strategic planning. It includes interpretations of financial statements, including the statement of profit or loss, statement of changes in equity, and statement of financial position. Furthermore, the report analyzes M&S's financial performance over two years using financial ratios. It also differentiates between IFRS and IAS, highlighting the benefits of IFRS and the degree of compliance across the world. Finally, the report concludes by summarizing the key findings and implications of financial reporting for M&S.

FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Context and purpose of financial reporting.............................................................................1

2. Analysis of regulatory and conceptual framework and key principles and qualitative

characteristics makes the financial information more reliable....................................................2

3.Main stakeholders of Marks & Spencer and benefits from financial information...................3

4. Value of financial reporting for meeting organisational growth and objectives.....................4

5. Interpretation of Financial statements as per IAS...................................................................4

6. Interpretation of last two years financial statement of the company for financial

performance.................................................................................................................................5

7. Differences Between IFRS and IAS.......................................................................................6

8. Benefits of IFRS......................................................................................................................7

9. Degree of compliance with IFRS by organisation across the world and the factors in a

nation...........................................................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Context and purpose of financial reporting.............................................................................1

2. Analysis of regulatory and conceptual framework and key principles and qualitative

characteristics makes the financial information more reliable....................................................2

3.Main stakeholders of Marks & Spencer and benefits from financial information...................3

4. Value of financial reporting for meeting organisational growth and objectives.....................4

5. Interpretation of Financial statements as per IAS...................................................................4

6. Interpretation of last two years financial statement of the company for financial

performance.................................................................................................................................5

7. Differences Between IFRS and IAS.......................................................................................6

8. Benefits of IFRS......................................................................................................................7

9. Degree of compliance with IFRS by organisation across the world and the factors in a

nation...........................................................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial reporting is the procedure of producing statements that bring out an

organization's financial information to the several stakeholders about the financial performance

and financial position of the company over a specified period of time. Companies stakeholders

are creditors, investors, debt providers and government (Hope, Thomas and Vyas, 2013). In this

report taken company marks & Spencer, it is a retail sector industry that selling of clothing,

home products and luxury food products. In this report consist of context and purpose of

financial reporting for meeting organisational objectives, development and growth. Interpret

financial statements and evaluate financial reporting standards and concepts. Identify difference

between IAS and IFRS.

MAIN BODY

1. Context and purpose of financial reporting

Financial Reporting

It is a framework that involves to discover all financial information to management and

the public about the company related to particular accounting period for showing how company

perform business activities. Financial reports are prepare on the basis of quarterly and annual

basis for for identify activities according to situations. In financial report consist of profit and

loss account, balance sheet and cash flow statements. On the basis of these reports management

are taking effective decisions and public ready to invest in the company.

It is commonly considered as end product of accounting because it is mainly prepared by

professional accountants in the end of year as well as quarter. The objective of provide accurate

and reliable information that shows financial performance, position and changes of the

organisation that is helpful to a broad range of users in making economic decisions (Fu, R., Kraft

and Zhang, 2012). For preparing these reports using International accounting standards that are

identify to reasons for taking different items according to financial position.

Purpose of Financial reporting

The main purpose of financial reporting is to presenting financial information to the

stakeholders and lenders of the business. According to FTES financial reporting have many

purposes are as following -

1

Financial reporting is the procedure of producing statements that bring out an

organization's financial information to the several stakeholders about the financial performance

and financial position of the company over a specified period of time. Companies stakeholders

are creditors, investors, debt providers and government (Hope, Thomas and Vyas, 2013). In this

report taken company marks & Spencer, it is a retail sector industry that selling of clothing,

home products and luxury food products. In this report consist of context and purpose of

financial reporting for meeting organisational objectives, development and growth. Interpret

financial statements and evaluate financial reporting standards and concepts. Identify difference

between IAS and IFRS.

MAIN BODY

1. Context and purpose of financial reporting

Financial Reporting

It is a framework that involves to discover all financial information to management and

the public about the company related to particular accounting period for showing how company

perform business activities. Financial reports are prepare on the basis of quarterly and annual

basis for for identify activities according to situations. In financial report consist of profit and

loss account, balance sheet and cash flow statements. On the basis of these reports management

are taking effective decisions and public ready to invest in the company.

It is commonly considered as end product of accounting because it is mainly prepared by

professional accountants in the end of year as well as quarter. The objective of provide accurate

and reliable information that shows financial performance, position and changes of the

organisation that is helpful to a broad range of users in making economic decisions (Fu, R., Kraft

and Zhang, 2012). For preparing these reports using International accounting standards that are

identify to reasons for taking different items according to financial position.

Purpose of Financial reporting

The main purpose of financial reporting is to presenting financial information to the

stakeholders and lenders of the business. According to FTES financial reporting have many

purposes are as following -

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a) Financial reporting are provide information to management for taking effective decision to

achieve organisations objectives ad goals. And it is helping to know strength and weakness of the

company.

b) It is helping to company for preparing strategies according to overall performance.

c) Financial reporting giving crucial information that are related to financial health and activities

of the company to its stakeholders as well as shareholders, government regulators and

consumers.

d) It is providing information that how to company operating & using various resources.

e) To provide essential data to the management of the organization to show how an association is

utilizing and obtaining diverse assets.

2. Analysis of regulatory and conceptual framework and key principles and qualitative

characteristics makes the financial information more reliable

Regulatory and conceptual framework

The conceptual and regulatory framework of financial reporting elaborate of objectives

and concepts. It will using as technical tool to help it develop standards and make abstracted

discrimination and organize opinions. In different words this structure incorporates the

requirements of financial related attributes and valuable financial data for substantial limits. With

the help of regulatory framework defined set of regulations while preparing of financial reporting

and provide financial information. Marks & Spencer adopted regulatory and conceptual

framework to follow rules and regulations and also principles to properly execute business

activities without government interference (Skaife, Veenman and Wangerin, D., 2013).

Purpose

1. The primary purpose of regulatory and conceptual framework is to guide company to

prepare their financial statements in suitable manner because it is present transparent

image of the company can be presented in front of shareholders.

2. Other purpose of these framework is to help companies to attract foreign investors so that

business can be operated in more effective manner.

All the above rules and standards are required to be followed by Marks and Spencer as they may

help to attain organisational objectives.

Principles

2

achieve organisations objectives ad goals. And it is helping to know strength and weakness of the

company.

b) It is helping to company for preparing strategies according to overall performance.

c) Financial reporting giving crucial information that are related to financial health and activities

of the company to its stakeholders as well as shareholders, government regulators and

consumers.

d) It is providing information that how to company operating & using various resources.

e) To provide essential data to the management of the organization to show how an association is

utilizing and obtaining diverse assets.

2. Analysis of regulatory and conceptual framework and key principles and qualitative

characteristics makes the financial information more reliable

Regulatory and conceptual framework

The conceptual and regulatory framework of financial reporting elaborate of objectives

and concepts. It will using as technical tool to help it develop standards and make abstracted

discrimination and organize opinions. In different words this structure incorporates the

requirements of financial related attributes and valuable financial data for substantial limits. With

the help of regulatory framework defined set of regulations while preparing of financial reporting

and provide financial information. Marks & Spencer adopted regulatory and conceptual

framework to follow rules and regulations and also principles to properly execute business

activities without government interference (Skaife, Veenman and Wangerin, D., 2013).

Purpose

1. The primary purpose of regulatory and conceptual framework is to guide company to

prepare their financial statements in suitable manner because it is present transparent

image of the company can be presented in front of shareholders.

2. Other purpose of these framework is to help companies to attract foreign investors so that

business can be operated in more effective manner.

All the above rules and standards are required to be followed by Marks and Spencer as they may

help to attain organisational objectives.

Principles

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The principle of framework related to income and expenses and according to that it was

categorised according to statement of profit and loss.

Income and expenses according to principle consist of other comprehensive income in the

head of recycling to describe that one period are recycled to the statement of profit and

loss

The qualitative characteristics

Faithful Representation – Financial reports are present in right way because it will helping to

enhance trust of shareholders and investors. If company time to time provide reliable information

so it will helping to achieve trust from management side.

Relevance – In this characteristics provide relevant information that are effected to management

decision and helping to know predict vale of actual vale (Botzem, 2012). These information

making difference to making decision according to situation.

Understandability – When recording transaction in financial statements that are understanding

by management easily, not create any misunderstanding.

3.Main stakeholders of Marks & Spencer and benefits from financial information

Stakeholders

These are important part of any organisation because with the help of them organisation

are operate in effective way. After analysing performance of the company they are taking

strategic decisions. In every organisation have two types stakeholders are as follows -

Internal stakeholders – All the internal stakeholders are that persons who analysis organisational

situation and decisions according to sales and profit. In this including internal stakeholders are

shareholders that are provide funds to company and helping to execute business activities,

managers are those persons who mainly connected to decision making processes and keep an eye

on daily transactions (Cohen and et. al, 2013).

External stakeholders – All external stakeholders are seeing business activities in different

manner. In this including Creditors, investors, governments and customers.

Benefits from Financial information to stakeholders

Stakeholders obtain a set of financial statements as a right and are the only stakeholders

take benefits from that, they are as following -

Providing Information

3

categorised according to statement of profit and loss.

Income and expenses according to principle consist of other comprehensive income in the

head of recycling to describe that one period are recycled to the statement of profit and

loss

The qualitative characteristics

Faithful Representation – Financial reports are present in right way because it will helping to

enhance trust of shareholders and investors. If company time to time provide reliable information

so it will helping to achieve trust from management side.

Relevance – In this characteristics provide relevant information that are effected to management

decision and helping to know predict vale of actual vale (Botzem, 2012). These information

making difference to making decision according to situation.

Understandability – When recording transaction in financial statements that are understanding

by management easily, not create any misunderstanding.

3.Main stakeholders of Marks & Spencer and benefits from financial information

Stakeholders

These are important part of any organisation because with the help of them organisation

are operate in effective way. After analysing performance of the company they are taking

strategic decisions. In every organisation have two types stakeholders are as follows -

Internal stakeholders – All the internal stakeholders are that persons who analysis organisational

situation and decisions according to sales and profit. In this including internal stakeholders are

shareholders that are provide funds to company and helping to execute business activities,

managers are those persons who mainly connected to decision making processes and keep an eye

on daily transactions (Cohen and et. al, 2013).

External stakeholders – All external stakeholders are seeing business activities in different

manner. In this including Creditors, investors, governments and customers.

Benefits from Financial information to stakeholders

Stakeholders obtain a set of financial statements as a right and are the only stakeholders

take benefits from that, they are as following -

Providing Information

3

It will helping to provide needful information that are using by management for effective

decisions. In these information including of ratios, net profit, investments and business activities

according to the situation.

Measure of performance

With the help of this companies are measures performance of the company by financial

report as well as employees performance. After measuring where need to improve so apply

strategies.

Decision making

On the basis of financial statements management of the company taking decision and also

helping to predict cost for future time period.

4. Value of financial reporting for meeting organisational growth and objectives

Financial reporting help to accomplish organisational goals but it is possible when

company record all transactions in appropriate manner. Marks & Spencer is a large retail sector

company in UK that retail of luxury products, clothes (Gomariz and Ballesta, 2014). For

organisation growth Marks & Spencer decided various goals to attract foreign investments,

investors, satisfy of customers and increasing sales. There are some points are helping to

organisation to accomplish growth and objectives -

1. With the help of financial reporting know actual financial position of the company that

are helping to the management for taking effective and appropriate decisions.

2. It is helping to attract foreign investment as well as large number of investors.

3. On the basis of these reports preparing strategies and policies for Marks & Spencer for

achieve objectives.

4. It is using as technical tool to improve efficiency of the company as well as employees.

5. It helps to Marks & Spencer to raise capital both domestic and overseas and serve as an

accounting database for future deferences (Benefits of IFRS, 2018).

5. Interpretation of Financial statements as per IAS

a) Statement of profit or loss and other comprehensive income

Statement of Profit & Loss and comprehensive income

For the year ended 31.12.2017 (in £000)

Particulars Amount

Sales 385100

4

decisions. In these information including of ratios, net profit, investments and business activities

according to the situation.

Measure of performance

With the help of this companies are measures performance of the company by financial

report as well as employees performance. After measuring where need to improve so apply

strategies.

Decision making

On the basis of financial statements management of the company taking decision and also

helping to predict cost for future time period.

4. Value of financial reporting for meeting organisational growth and objectives

Financial reporting help to accomplish organisational goals but it is possible when

company record all transactions in appropriate manner. Marks & Spencer is a large retail sector

company in UK that retail of luxury products, clothes (Gomariz and Ballesta, 2014). For

organisation growth Marks & Spencer decided various goals to attract foreign investments,

investors, satisfy of customers and increasing sales. There are some points are helping to

organisation to accomplish growth and objectives -

1. With the help of financial reporting know actual financial position of the company that

are helping to the management for taking effective and appropriate decisions.

2. It is helping to attract foreign investment as well as large number of investors.

3. On the basis of these reports preparing strategies and policies for Marks & Spencer for

achieve objectives.

4. It is using as technical tool to improve efficiency of the company as well as employees.

5. It helps to Marks & Spencer to raise capital both domestic and overseas and serve as an

accounting database for future deferences (Benefits of IFRS, 2018).

5. Interpretation of Financial statements as per IAS

a) Statement of profit or loss and other comprehensive income

Statement of Profit & Loss and comprehensive income

For the year ended 31.12.2017 (in £000)

Particulars Amount

Sales 385100

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of goods sold (before damage) 297560

Gross profit 87538

Less – Operating Expenses -83443

Total 3875

Other income

Add – Rental Income 5600

Less - Loss in value of investment property 2300

Net profit 7175

Less - Bank interest 830

Profit before tax 6345

Taxation 1500

Profit for the year 4845

b) Statement of change in equity

Date Particular

Opening

share

capital

Revised

reserve

Retained

earnings Total

01/01/17 Balance B/f 86700 32100 118800

01/01/17 Revaluation 40700 40700

01/01/17 Ordinary dividend paid -4340 -4340

Profit for the year for share of equity

holders 2515 2515

31/12/17 Balance C/d 86700 40700 30275 157675

c) Statement of financial position

Particular Amount (£)

Investment in Boland LTD Asso. co. 165000

Sundry Assets 759000

Total 924000

Share capital 240000

5

Gross profit 87538

Less – Operating Expenses -83443

Total 3875

Other income

Add – Rental Income 5600

Less - Loss in value of investment property 2300

Net profit 7175

Less - Bank interest 830

Profit before tax 6345

Taxation 1500

Profit for the year 4845

b) Statement of change in equity

Date Particular

Opening

share

capital

Revised

reserve

Retained

earnings Total

01/01/17 Balance B/f 86700 32100 118800

01/01/17 Revaluation 40700 40700

01/01/17 Ordinary dividend paid -4340 -4340

Profit for the year for share of equity

holders 2515 2515

31/12/17 Balance C/d 86700 40700 30275 157675

c) Statement of financial position

Particular Amount (£)

Investment in Boland LTD Asso. co. 165000

Sundry Assets 759000

Total 924000

Share capital 240000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Retained earnings at 1st April 2008 600000

Earnings 2008/09 (38400+9600) 48000

Earnings 2009/10 (21600 + 14400) 36000

Total 924000

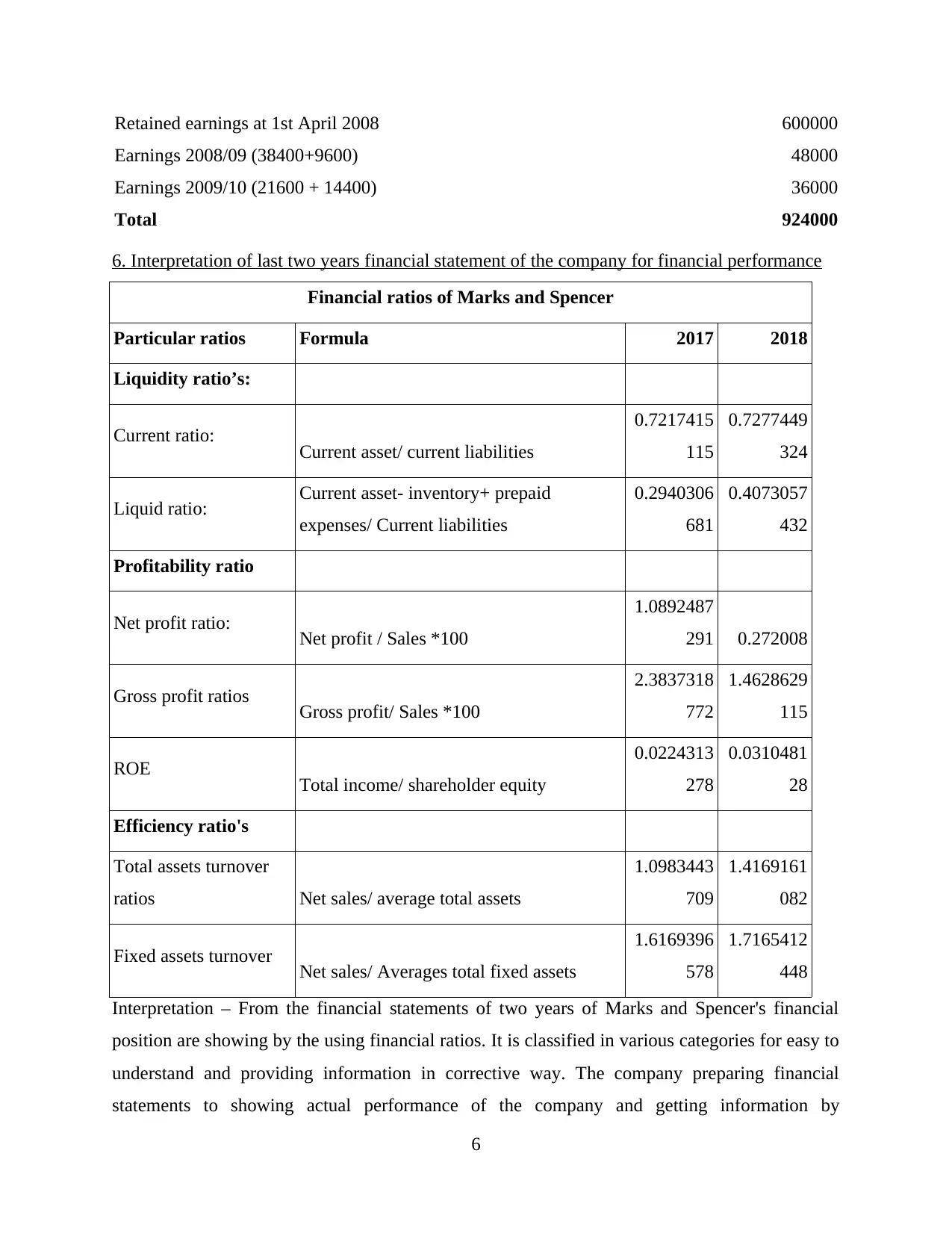

6. Interpretation of last two years financial statement of the company for financial performance

Financial ratios of Marks and Spencer

Particular ratios Formula 2017 2018

Liquidity ratio’s:

Current ratio: Current asset/ current liabilities

0.7217415

115

0.7277449

324

Liquid ratio: Current asset- inventory+ prepaid

expenses/ Current liabilities

0.2940306

681

0.4073057

432

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.0892487

291 0.272008

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.0983443

709

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets

1.6169396

578

1.7165412

448

Interpretation – From the financial statements of two years of Marks and Spencer's financial

position are showing by the using financial ratios. It is classified in various categories for easy to

understand and providing information in corrective way. The company preparing financial

statements to showing actual performance of the company and getting information by

6

Earnings 2008/09 (38400+9600) 48000

Earnings 2009/10 (21600 + 14400) 36000

Total 924000

6. Interpretation of last two years financial statement of the company for financial performance

Financial ratios of Marks and Spencer

Particular ratios Formula 2017 2018

Liquidity ratio’s:

Current ratio: Current asset/ current liabilities

0.7217415

115

0.7277449

324

Liquid ratio: Current asset- inventory+ prepaid

expenses/ Current liabilities

0.2940306

681

0.4073057

432

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.0892487

291 0.272008

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.0983443

709

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets

1.6169396

578

1.7165412

448

Interpretation – From the financial statements of two years of Marks and Spencer's financial

position are showing by the using financial ratios. It is classified in various categories for easy to

understand and providing information in corrective way. The company preparing financial

statements to showing actual performance of the company and getting information by

6

consolidates incomes of their organisation along with their subsidiary organisations. For present

financial situation of the company prepare consolidated income statement, there are present

profit in 2017 was (426.4) and in 2018 is 455.5. Income statement and comprehensive income

statement are individually equipped in order to find out their realisable value. Along with

equilibrium and cash flow statement, this company also prepares their changes in equity.

From the above table of ratios, it has been identified in 2018 company have more than

liquidity to compare 2017. Profitability ratio in 2018 not much more increases compare to 2017

but determine efficiency ratio increasing from 2017 to 2018.

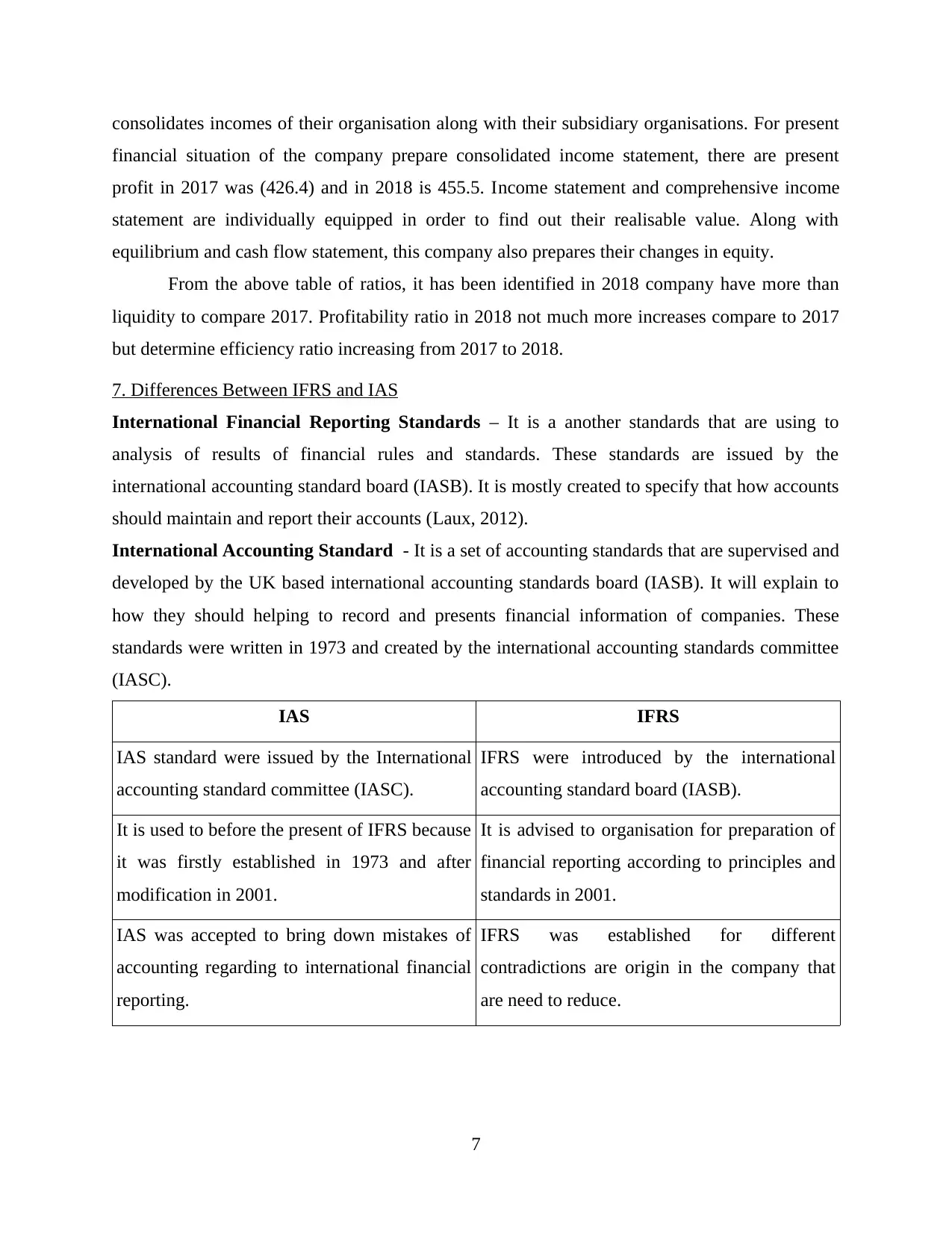

7. Differences Between IFRS and IAS

International Financial Reporting Standards – It is a another standards that are using to

analysis of results of financial rules and standards. These standards are issued by the

international accounting standard board (IASB). It is mostly created to specify that how accounts

should maintain and report their accounts (Laux, 2012).

International Accounting Standard - It is a set of accounting standards that are supervised and

developed by the UK based international accounting standards board (IASB). It will explain to

how they should helping to record and presents financial information of companies. These

standards were written in 1973 and created by the international accounting standards committee

(IASC).

IAS IFRS

IAS standard were issued by the International

accounting standard committee (IASC).

IFRS were introduced by the international

accounting standard board (IASB).

It is used to before the present of IFRS because

it was firstly established in 1973 and after

modification in 2001.

It is advised to organisation for preparation of

financial reporting according to principles and

standards in 2001.

IAS was accepted to bring down mistakes of

accounting regarding to international financial

reporting.

IFRS was established for different

contradictions are origin in the company that

are need to reduce.

7

financial situation of the company prepare consolidated income statement, there are present

profit in 2017 was (426.4) and in 2018 is 455.5. Income statement and comprehensive income

statement are individually equipped in order to find out their realisable value. Along with

equilibrium and cash flow statement, this company also prepares their changes in equity.

From the above table of ratios, it has been identified in 2018 company have more than

liquidity to compare 2017. Profitability ratio in 2018 not much more increases compare to 2017

but determine efficiency ratio increasing from 2017 to 2018.

7. Differences Between IFRS and IAS

International Financial Reporting Standards – It is a another standards that are using to

analysis of results of financial rules and standards. These standards are issued by the

international accounting standard board (IASB). It is mostly created to specify that how accounts

should maintain and report their accounts (Laux, 2012).

International Accounting Standard - It is a set of accounting standards that are supervised and

developed by the UK based international accounting standards board (IASB). It will explain to

how they should helping to record and presents financial information of companies. These

standards were written in 1973 and created by the international accounting standards committee

(IASC).

IAS IFRS

IAS standard were issued by the International

accounting standard committee (IASC).

IFRS were introduced by the international

accounting standard board (IASB).

It is used to before the present of IFRS because

it was firstly established in 1973 and after

modification in 2001.

It is advised to organisation for preparation of

financial reporting according to principles and

standards in 2001.

IAS was accepted to bring down mistakes of

accounting regarding to international financial

reporting.

IFRS was established for different

contradictions are origin in the company that

are need to reduce.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is mainly connected with managing the

international accounting standards and

estimations.

It will helping to present the international

financial reporting standards and the

provisions.

8. Benefits of IFRS

IFRS plays crucial role in the international accounting and financial rules and regulations.

It is adopted by Marks & Spencer to provide benefit to its investors, customers and other users

are relate to the company. It is helping to prepare financial reports according to accounting

standards and principles. After adopting it helping to reduce the cost of investments and

increasing the quality of providing information (Iyoha, 2012).

Greater Comparability – M&S applying IFRS and prepare according to that financial reports so

it will helping to compare with other companies who adopted different Standards for preparing

financial statements.

Improved tax planning and financial reporting – After following IFRS, company produce a

consistent and standardised set of financial and accounting reports for complying with compact

necessitate and local statutory (Hanlon, Hoopes and Shroff, 2014).

Improved day to day business activities – Marks & Spencer conduct all day to day activities

because maintaining these financial information to helping to improve financial performance.

Better managed resources – These standards are guiding to how should mange resources in

better way and M&S company capable to standardise accounting methods across the company

and helping to decrease cost of financial reports and audits.

Improved financial controls – By following these standards helping to control financial

activities of the business. It is cover all legal activities, risks, difficulties in individual countries.

Lower cost of capital – It is support to high quality Standards are related to financial activities.

After getting financial result is will provide benefit to investors and management of Marks &

Spencer.

9. Degree of compliance with IFRS by organisation across the world and the factors in a nation

IFRS are the set of standards issued by international accounting standard board to

formulated by the government and these are mainly adopted by those companies who are trading

business on international level (Zeff, van der Wel, and Camfferman, 2016). When companies

are prepare to financial statements that time follow these standards because it helping to present

8

international accounting standards and

estimations.

It will helping to present the international

financial reporting standards and the

provisions.

8. Benefits of IFRS

IFRS plays crucial role in the international accounting and financial rules and regulations.

It is adopted by Marks & Spencer to provide benefit to its investors, customers and other users

are relate to the company. It is helping to prepare financial reports according to accounting

standards and principles. After adopting it helping to reduce the cost of investments and

increasing the quality of providing information (Iyoha, 2012).

Greater Comparability – M&S applying IFRS and prepare according to that financial reports so

it will helping to compare with other companies who adopted different Standards for preparing

financial statements.

Improved tax planning and financial reporting – After following IFRS, company produce a

consistent and standardised set of financial and accounting reports for complying with compact

necessitate and local statutory (Hanlon, Hoopes and Shroff, 2014).

Improved day to day business activities – Marks & Spencer conduct all day to day activities

because maintaining these financial information to helping to improve financial performance.

Better managed resources – These standards are guiding to how should mange resources in

better way and M&S company capable to standardise accounting methods across the company

and helping to decrease cost of financial reports and audits.

Improved financial controls – By following these standards helping to control financial

activities of the business. It is cover all legal activities, risks, difficulties in individual countries.

Lower cost of capital – It is support to high quality Standards are related to financial activities.

After getting financial result is will provide benefit to investors and management of Marks &

Spencer.

9. Degree of compliance with IFRS by organisation across the world and the factors in a nation

IFRS are the set of standards issued by international accounting standard board to

formulated by the government and these are mainly adopted by those companies who are trading

business on international level (Zeff, van der Wel, and Camfferman, 2016). When companies

are prepare to financial statements that time follow these standards because it helping to present

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

transparent image of the company in front of their stakeholders. It is constituent for the company

to record reliable and appropriate data in annual report of the company. IFRS guide to businesses

how they preparing effective financial accounts that are present actual situation of the company

in appropriate manner.

For example, Marks & Spencer is operating all business activities all around the world.

The organisation prepare of the facial statements follow the accounting standards and principles

because it helping to provide those information need to organisation for showing actual

performance of the company. IFRS is good option to adopt for prepare finial reports and solve

complexities related to financial terms. It is a technique that help to organisation for accomplish

their goals and objectives (Puspitaningrum and Atmini, 2012).

CONCLUSION

From the above project report it has been concluded that financial reporting important

part of any organisation because without it business can not present financial situation. It is

essential for all the organisations to follow the standards of IFRS because it may help to achieve

objectives and goals of the company like as sales and profits. It is also provide benefits to

management, customers, stakeholders and governments. These standards are issued for those

companies are trading on international level and willing to acquire higher profit. With the help of

reports customers, investors, creditors, shareholders and other user using information for

effective decision and they are become part of business entity who have a good financial health

and market image.

9

to record reliable and appropriate data in annual report of the company. IFRS guide to businesses

how they preparing effective financial accounts that are present actual situation of the company

in appropriate manner.

For example, Marks & Spencer is operating all business activities all around the world.

The organisation prepare of the facial statements follow the accounting standards and principles

because it helping to provide those information need to organisation for showing actual

performance of the company. IFRS is good option to adopt for prepare finial reports and solve

complexities related to financial terms. It is a technique that help to organisation for accomplish

their goals and objectives (Puspitaningrum and Atmini, 2012).

CONCLUSION

From the above project report it has been concluded that financial reporting important

part of any organisation because without it business can not present financial situation. It is

essential for all the organisations to follow the standards of IFRS because it may help to achieve

objectives and goals of the company like as sales and profits. It is also provide benefits to

management, customers, stakeholders and governments. These standards are issued for those

companies are trading on international level and willing to acquire higher profit. With the help of

reports customers, investors, creditors, shareholders and other user using information for

effective decision and they are become part of business entity who have a good financial health

and market image.

9

REFERENCES

Books and Journals

Hope, O. K., Thomas, W. B. and Vyas, D., 2013. Financial reporting quality of US private and

public firms. The Accounting Review. 88(5). pp.1715-1742.

Fu, R., Kraft, A. and Zhang, H., 2012. Financial reporting frequency, information asymmetry,

and the cost of equity. Journal of Accounting and Economics. 54(2-3). pp.132-149.

Skaife, H. A., Veenman, D. and Wangerin, D., 2013. Internal control over financial reporting

and managerial rent extraction: Evidence from the profitability of insider

trading. Journal of Accounting and Economics. 55(1). pp.91-110.

Botzem, S., 2012. The politics of accounting regulation: Organizing transnational standard

setting in financial reporting. Edward Elgar Publishing.

Cohen, J. R., Hoitash, U., Krishnamoorthy, G. and Wright, A.M., 2013. The effect of audit

committee industry expertise on monitoring the financial reporting process. The

Accounting Review. 89(1). pp.243-273.

Gomariz, M. F. C. and Ballesta, J. P. S., 2014. Financial reporting quality, debt maturity and

investment efficiency. Journal of Banking & Finance. 40. pp.494-506.

Laux, C., 2012. Financial instruments, financial reporting, and financial stability. Accounting

and business research. 42(3). pp.239-260.

Iyoha, F. O., 2012. Company attributes and the timeliness of financial reporting in Nigeria.

Business Intelligence Journal. 5(1).

Hanlon, M., Hoopes, J.L. and Shroff, N., 2014. The effect of tax authority monitoring and

enforcement on financial reporting quality. The Journal of the American Taxation

Association. 36(2). pp.137-170.

Zeff, S. A., van der Wel, F. and Camfferman, C., 2016. Company financial reporting: A

historical and comparative study of the Dutch regulatory process. Routledge.

Puspitaningrum, D. and Atmini, S., 2012. Corporate governance mechanism and the level of

internet financial reporting: Evidence from Indonesian companies. Procedia Economics

and Finance. 2. pp.157-166.

Online

Benefits of IFRS, 2018. [Online]. Available through: <https://www.morganmckinley.ie/article/5-

benefits-ifrs>

10

Books and Journals

Hope, O. K., Thomas, W. B. and Vyas, D., 2013. Financial reporting quality of US private and

public firms. The Accounting Review. 88(5). pp.1715-1742.

Fu, R., Kraft, A. and Zhang, H., 2012. Financial reporting frequency, information asymmetry,

and the cost of equity. Journal of Accounting and Economics. 54(2-3). pp.132-149.

Skaife, H. A., Veenman, D. and Wangerin, D., 2013. Internal control over financial reporting

and managerial rent extraction: Evidence from the profitability of insider

trading. Journal of Accounting and Economics. 55(1). pp.91-110.

Botzem, S., 2012. The politics of accounting regulation: Organizing transnational standard

setting in financial reporting. Edward Elgar Publishing.

Cohen, J. R., Hoitash, U., Krishnamoorthy, G. and Wright, A.M., 2013. The effect of audit

committee industry expertise on monitoring the financial reporting process. The

Accounting Review. 89(1). pp.243-273.

Gomariz, M. F. C. and Ballesta, J. P. S., 2014. Financial reporting quality, debt maturity and

investment efficiency. Journal of Banking & Finance. 40. pp.494-506.

Laux, C., 2012. Financial instruments, financial reporting, and financial stability. Accounting

and business research. 42(3). pp.239-260.

Iyoha, F. O., 2012. Company attributes and the timeliness of financial reporting in Nigeria.

Business Intelligence Journal. 5(1).

Hanlon, M., Hoopes, J.L. and Shroff, N., 2014. The effect of tax authority monitoring and

enforcement on financial reporting quality. The Journal of the American Taxation

Association. 36(2). pp.137-170.

Zeff, S. A., van der Wel, F. and Camfferman, C., 2016. Company financial reporting: A

historical and comparative study of the Dutch regulatory process. Routledge.

Puspitaningrum, D. and Atmini, S., 2012. Corporate governance mechanism and the level of

internet financial reporting: Evidence from Indonesian companies. Procedia Economics

and Finance. 2. pp.157-166.

Online

Benefits of IFRS, 2018. [Online]. Available through: <https://www.morganmckinley.ie/article/5-

benefits-ifrs>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.