Financial Reporting Analysis: Marks & Spencer, IAS 1, and IFRS

VerifiedAdded on 2020/10/05

|14

|3534

|352

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, beginning with an introduction to the concept and its significance in business decision-making. It explores the main objectives of financial reporting, emphasizing its role in investment decisions and management accountability. The report delves into the main principles and conceptual framework, highlighting the importance of regulatory frameworks like IFRS and qualitative characteristics such as relevance and faithful presentation. It identifies the key stakeholders of an organization, differentiating between internal stakeholders like employees and external stakeholders like customers and shareholders, and discusses the value of financial reporting in meeting company goals. The report includes an analysis of financial statements as per IAS 1, including profit and loss statements, statements of equity, and statements of financial position. It also touches upon the differences between IAS and IFRS, the evaluation of benefits of IFRS, and the varying degrees of compliance with IFRS. The case study uses Marks & Spencer as an example, providing real-world context to the theoretical concepts discussed. The report concludes with a discussion on the value of financial reporting to meet companies’ goals, highlighting the importance of income statements, ratio analysis, and balance sheets in achieving these goals.

Financial Reporting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.................................................................................................................................3

MAIN BODY........................................................................................................................................3

1. Main objective of financial reporting.............................................................................................3

2. Main principle and conceptual framework.....................................................................................4

3. Main stakeholder of an organisation..............................................................................................5

4. Value of financial reporting to meet companies’ goals..................................................................6

5. Financial statement as per the IAS 1:.............................................................................................7

7. Differences between IAS and IFRS.............................................................................................10

8. Evaluation of benefits of IFRS....................................................................................................11

9 Ascertaining the varying degree of compliance with IFRS...........................................................12

REFERENCES....................................................................................................................................14

INTRODUCTION.................................................................................................................................3

MAIN BODY........................................................................................................................................3

1. Main objective of financial reporting.............................................................................................3

2. Main principle and conceptual framework.....................................................................................4

3. Main stakeholder of an organisation..............................................................................................5

4. Value of financial reporting to meet companies’ goals..................................................................6

5. Financial statement as per the IAS 1:.............................................................................................7

7. Differences between IAS and IFRS.............................................................................................10

8. Evaluation of benefits of IFRS....................................................................................................11

9 Ascertaining the varying degree of compliance with IFRS...........................................................12

REFERENCES....................................................................................................................................14

INTRODUCTION

Financial reporting is the process related to analysing, gathering, posting of useful

financial information within organisation that help to make effective decision so that

performance and productivity can be increased (Financial reporting, 2018). Almost every

company make financial report at a certain time period so that help to determine the financial

strength and market position of company. With the help of report internal manager are able to

make effective decision in order to improve the profitability of company can be improved.

Financial statement is also useful to external manager as they are able to make valuable

investment decision by viewing the position of company. Company taken in this report is

Marks & Spenser which is situated in UK.

In this assignment, main objective of financial reporting, its requirement, main beliefs

of conceptual and regulatory outline, important investor of company is exposed. Assignment

also attentions on worth of statement, interpretation of last two year statements, significance

of IFRS and actual difference between IFRS and IAS is exposed.

MAIN BODY

1. Main objective of financial reporting

In accounting, all business transaction is needed to be recorded that make ease the

work of internal and external stakeholder. The process of posting accurate transaction in to

right book is known as financial reporting. These reports are prepared by the internal

department that provide the appropriate and current data related to the companies. External

stakeholder view the financial statement of companies and make valuable investment

decision in order to get the best rate of return depending upon the current financial strength

and market position of company. Manager of on organisation keep the detail information

about overall happing, so that performance of every units, employees can be measured and

improved if required. Business entity financial reporting is defined as a total communication

scheme concerning the firm as issuer, investors and creditors as main users, additional

external employers. The accounting business as procedures and accountants and the company

rule controlling establishments (Aversano and Christiaens, 2014. ). Management of Mark &

Spencer, preserve translucent and correct report or statement, which support stockholder to

collect valuable evidence connected to presentation, effectiveness throughout an accounting

Financial reporting is the process related to analysing, gathering, posting of useful

financial information within organisation that help to make effective decision so that

performance and productivity can be increased (Financial reporting, 2018). Almost every

company make financial report at a certain time period so that help to determine the financial

strength and market position of company. With the help of report internal manager are able to

make effective decision in order to improve the profitability of company can be improved.

Financial statement is also useful to external manager as they are able to make valuable

investment decision by viewing the position of company. Company taken in this report is

Marks & Spenser which is situated in UK.

In this assignment, main objective of financial reporting, its requirement, main beliefs

of conceptual and regulatory outline, important investor of company is exposed. Assignment

also attentions on worth of statement, interpretation of last two year statements, significance

of IFRS and actual difference between IFRS and IAS is exposed.

MAIN BODY

1. Main objective of financial reporting

In accounting, all business transaction is needed to be recorded that make ease the

work of internal and external stakeholder. The process of posting accurate transaction in to

right book is known as financial reporting. These reports are prepared by the internal

department that provide the appropriate and current data related to the companies. External

stakeholder view the financial statement of companies and make valuable investment

decision in order to get the best rate of return depending upon the current financial strength

and market position of company. Manager of on organisation keep the detail information

about overall happing, so that performance of every units, employees can be measured and

improved if required. Business entity financial reporting is defined as a total communication

scheme concerning the firm as issuer, investors and creditors as main users, additional

external employers. The accounting business as procedures and accountants and the company

rule controlling establishments (Aversano and Christiaens, 2014. ). Management of Mark &

Spencer, preserve translucent and correct report or statement, which support stockholder to

collect valuable evidence connected to presentation, effectiveness throughout an accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

period. This benefit to attain programmed administrative objectives that are crucial to achieve

dissimilar business task in company. There is various objective, purpose of financial

reporting that are described underneath:

Purpose of reporting.

(a) Investment Decision-Making:

The simple aim of financial writing is to deliver material convenient to stockholders and new

users in creation sound outlay decisions.

(b) Management Accountability:

The second aim of reporting is to deliver information on organization accountability to

review organization’s efficiency in using the funds and managing the operation of company.

Importance of report.

In Mark & Spenser manger make analysis of performance of staff member and

business operation with the help of detail information.

Financial reporting is vital for the businesses that support to stakeholder to examine

the financial performance throughout an accounting period.

It is cooperative for investor to investigate that weather their money will give better

result or not.

2. Main principle and conceptual framework.

In business world every company requires to follow a certain guidelines or a set of

regulation to perform their business operation or record these business transactions into

books. So, basically the regulatory framework or standard are defined as the set of rules that

has to be implemented by every company to record with business transaction. In UK,

government have formulated different kind of rules for small and large company that guide

manager to make transparent record. Similarly, the conceptual framework is defined as the

kind of analytical tool that has variable quantity and textual matter. With the support of this

tool organisation are able to collected information and compare performance of different

business activities and employees working in company. It also used to make intellectual

differences and arrange business ideas so that valuable plans are made to improve the actual

differences. In M&S it has been noticed that principle that are formulated by IASB are

followed that support in formation of appropriate and transparent statements. These are

dissimilar business task in company. There is various objective, purpose of financial

reporting that are described underneath:

Purpose of reporting.

(a) Investment Decision-Making:

The simple aim of financial writing is to deliver material convenient to stockholders and new

users in creation sound outlay decisions.

(b) Management Accountability:

The second aim of reporting is to deliver information on organization accountability to

review organization’s efficiency in using the funds and managing the operation of company.

Importance of report.

In Mark & Spenser manger make analysis of performance of staff member and

business operation with the help of detail information.

Financial reporting is vital for the businesses that support to stakeholder to examine

the financial performance throughout an accounting period.

It is cooperative for investor to investigate that weather their money will give better

result or not.

2. Main principle and conceptual framework.

In business world every company requires to follow a certain guidelines or a set of

regulation to perform their business operation or record these business transactions into

books. So, basically the regulatory framework or standard are defined as the set of rules that

has to be implemented by every company to record with business transaction. In UK,

government have formulated different kind of rules for small and large company that guide

manager to make transparent record. Similarly, the conceptual framework is defined as the

kind of analytical tool that has variable quantity and textual matter. With the support of this

tool organisation are able to collected information and compare performance of different

business activities and employees working in company. It also used to make intellectual

differences and arrange business ideas so that valuable plans are made to improve the actual

differences. In M&S it has been noticed that principle that are formulated by IASB are

followed that support in formation of appropriate and transparent statements. These are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

imposed in the form of IFRS (Dyreng, Mayew and Williams, 2012). International financial

reporting standard are recognized by IASB that are monitored by businesses and are usually

called ethics of regulatory and conceptual frameworks. Some of these are described below:

IFRS 1: It is connected to the principle that firms accept at very first time. These

established of IFRS guides the manager of Mark & Spenser to frame financial

statements precisely and efficiently.

IFRS 3: Conferring to this technique the acquisitions recognizable assets and

liabilities necessity be measured and noted at their definite values on the date of

purchase.

Qualitative characteristic

Relevance: So that it creates a variance to the conclusions about a company made by users of

the declarations. Thus, In M&S different investor come across to male investment depending

on the financial reports.

Faithful presentation: Financial statements are complete and free from bias and error. So In

M&S manager are able to make effective budget for upcoming period.

3. Main stakeholder of an organisation.

Stakeholder are individual or group of people those are willing to investment within company

in order to get a return on investment are a predefined rate of interest. These stakeholders are

categorising according to their interest and involvement in company. These are divided in

external and internal according to their impact on business performance. Some of the main

stakeholders are creditor, director, employees, shareholder, employees, suppliers and the

society from which company uses different resources (Flower, 2016. ). These are describing

below:

Internal stakeholder: These types of investor have direct impact on the business

performance and they directly participate in business operation. Such as

Employees: these are the group of people those are working in Mar & Spenser. They

help to run business activities effectively in order to maximise profit and attain predefined

goals and objectives.

Financial reporting has different advantages to the internal stakeholder that are discussed

below:

reporting standard are recognized by IASB that are monitored by businesses and are usually

called ethics of regulatory and conceptual frameworks. Some of these are described below:

IFRS 1: It is connected to the principle that firms accept at very first time. These

established of IFRS guides the manager of Mark & Spenser to frame financial

statements precisely and efficiently.

IFRS 3: Conferring to this technique the acquisitions recognizable assets and

liabilities necessity be measured and noted at their definite values on the date of

purchase.

Qualitative characteristic

Relevance: So that it creates a variance to the conclusions about a company made by users of

the declarations. Thus, In M&S different investor come across to male investment depending

on the financial reports.

Faithful presentation: Financial statements are complete and free from bias and error. So In

M&S manager are able to make effective budget for upcoming period.

3. Main stakeholder of an organisation.

Stakeholder are individual or group of people those are willing to investment within company

in order to get a return on investment are a predefined rate of interest. These stakeholders are

categorising according to their interest and involvement in company. These are divided in

external and internal according to their impact on business performance. Some of the main

stakeholders are creditor, director, employees, shareholder, employees, suppliers and the

society from which company uses different resources (Flower, 2016. ). These are describing

below:

Internal stakeholder: These types of investor have direct impact on the business

performance and they directly participate in business operation. Such as

Employees: these are the group of people those are working in Mar & Spenser. They

help to run business activities effectively in order to maximise profit and attain predefined

goals and objectives.

Financial reporting has different advantages to the internal stakeholder that are discussed

below:

To create dividend judgement.

To determine that security must be traded, holder or carry more stake of the

corporation.

Likewise aids to regulate the constancy and efficiency of managers and other

employees.

External stakeholder: These people or investor is also important for companies as they

make investment decision deepening upon the actual position and financial strength. Such as

Customer: They are consider to be the backbone for company, as if there are more

number of customer then company will be going to earn more profit. So M&S produces best

goods that satisfy customer.

Shareholder: These groups of individual wants to invest in company in reference to

get the best result that will double their money (Lee and Parker, 2014. ).

Financial reporting has its advantages to the external stakeholder like:

To ensure that disbursement of provisions are cleared on agreed date

This also assistances government to collect tax and related sum from business

entity on a particular date.

4. Value of financial reporting to meet companies’ goals.

For companies it is very important to have a predefined goals and objective that help

them to perform well in the market to ascertain those goals. Thus manager of Mark and

Spenser focuses to develop transparent and accurate financial reports and statement at the end

of every quarter so that effective plans are formulated. As discussed above the process of

recording finance related information in right books is known as financial reporting. In

general, reporting aids in formulation of crucial financial statement, balance sheet and cash

flow statement during an accounting year. From the M&S point of view the main impartial of

these yearly reports is to deliver beneficial statistics to the current and probable stockholders

so, they make effective decision to various investments.

It is observed that there are basically three types of financial statements that support

management of firm to determine either the goals are attain or they require some more effort

to attain those goals. With the aid of these annual report manager also comes to know about

the financial position and outstanding debts for a complete year. Generally, three statements

To determine that security must be traded, holder or carry more stake of the

corporation.

Likewise aids to regulate the constancy and efficiency of managers and other

employees.

External stakeholder: These people or investor is also important for companies as they

make investment decision deepening upon the actual position and financial strength. Such as

Customer: They are consider to be the backbone for company, as if there are more

number of customer then company will be going to earn more profit. So M&S produces best

goods that satisfy customer.

Shareholder: These groups of individual wants to invest in company in reference to

get the best result that will double their money (Lee and Parker, 2014. ).

Financial reporting has its advantages to the external stakeholder like:

To ensure that disbursement of provisions are cleared on agreed date

This also assistances government to collect tax and related sum from business

entity on a particular date.

4. Value of financial reporting to meet companies’ goals.

For companies it is very important to have a predefined goals and objective that help

them to perform well in the market to ascertain those goals. Thus manager of Mark and

Spenser focuses to develop transparent and accurate financial reports and statement at the end

of every quarter so that effective plans are formulated. As discussed above the process of

recording finance related information in right books is known as financial reporting. In

general, reporting aids in formulation of crucial financial statement, balance sheet and cash

flow statement during an accounting year. From the M&S point of view the main impartial of

these yearly reports is to deliver beneficial statistics to the current and probable stockholders

so, they make effective decision to various investments.

It is observed that there are basically three types of financial statements that support

management of firm to determine either the goals are attain or they require some more effort

to attain those goals. With the aid of these annual report manager also comes to know about

the financial position and outstanding debts for a complete year. Generally, three statements

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

benefit manager of Mark and Spenser to recognize better almost the business process so that

they might reach the company goals. These are discussed below:

Income statement: It is also identified as the profit and loss report or statement of

revenue and expenditure, the income statement principally emphases on business’s incomes

and expenditures throughout a time frame. The income statement, attentions on the basic four

main items such as expenses, gains, revenue and losses.

Ratio analysis: It is one of the most popular financial analysis tool that manger of

M&S to make evaluate, measure the performance, liquidity during an accounting year.

Balance sheet: The systematic record of assets and liabilities of company that help to

calculate the actual financial position of Mark & Spenser in known as balance sheet. This

also help manager to determine the capability of numerous project that aid to produce cash

flows that benefit to attain the desired goals.

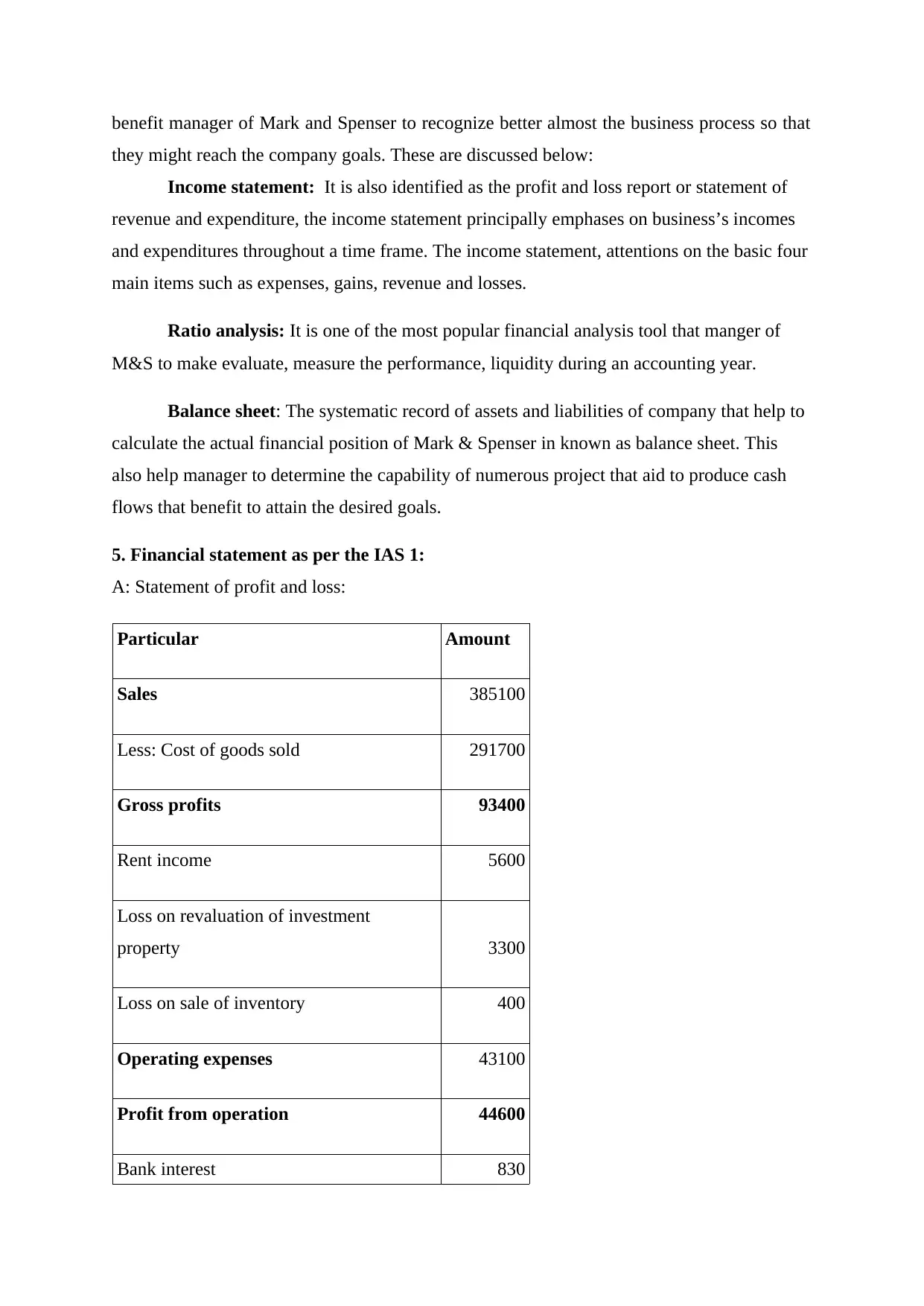

5. Financial statement as per the IAS 1:

A: Statement of profit and loss:

Particular Amount

Sales 385100

Less: Cost of goods sold 291700

Gross profits 93400

Rent income 5600

Loss on revaluation of investment

property 3300

Loss on sale of inventory 400

Operating expenses 43100

Profit from operation 44600

Bank interest 830

they might reach the company goals. These are discussed below:

Income statement: It is also identified as the profit and loss report or statement of

revenue and expenditure, the income statement principally emphases on business’s incomes

and expenditures throughout a time frame. The income statement, attentions on the basic four

main items such as expenses, gains, revenue and losses.

Ratio analysis: It is one of the most popular financial analysis tool that manger of

M&S to make evaluate, measure the performance, liquidity during an accounting year.

Balance sheet: The systematic record of assets and liabilities of company that help to

calculate the actual financial position of Mark & Spenser in known as balance sheet. This

also help manager to determine the capability of numerous project that aid to produce cash

flows that benefit to attain the desired goals.

5. Financial statement as per the IAS 1:

A: Statement of profit and loss:

Particular Amount

Sales 385100

Less: Cost of goods sold 291700

Gross profits 93400

Rent income 5600

Loss on revaluation of investment

property 3300

Loss on sale of inventory 400

Operating expenses 43100

Profit from operation 44600

Bank interest 830

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

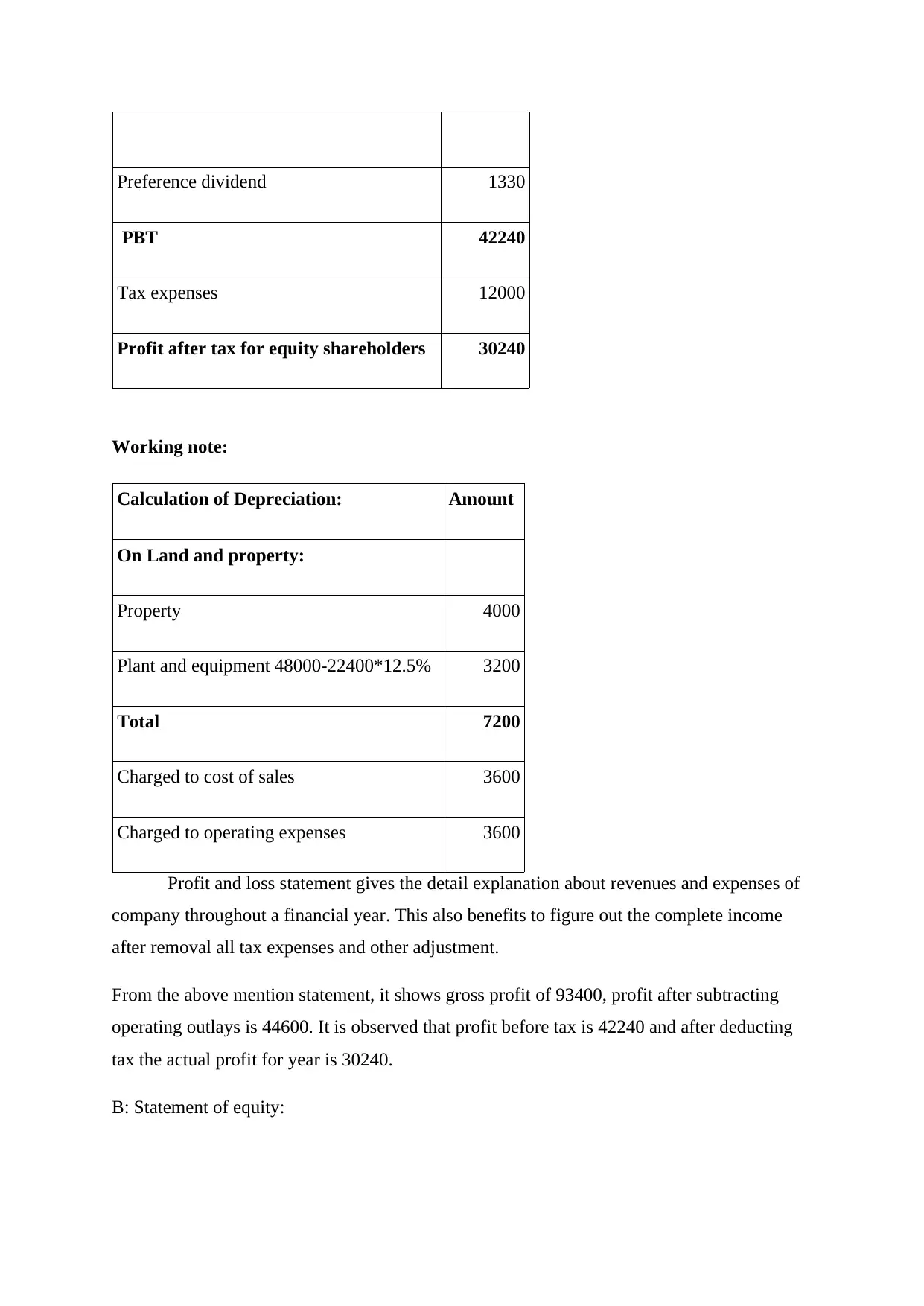

Preference dividend 1330

PBT 42240

Tax expenses 12000

Profit after tax for equity shareholders 30240

Working note:

Calculation of Depreciation: Amount

On Land and property:

Property 4000

Plant and equipment 48000-22400*12.5% 3200

Total 7200

Charged to cost of sales 3600

Charged to operating expenses 3600

Profit and loss statement gives the detail explanation about revenues and expenses of

company throughout a financial year. This also benefits to figure out the complete income

after removal all tax expenses and other adjustment.

From the above mention statement, it shows gross profit of 93400, profit after subtracting

operating outlays is 44600. It is observed that profit before tax is 42240 and after deducting

tax the actual profit for year is 30240.

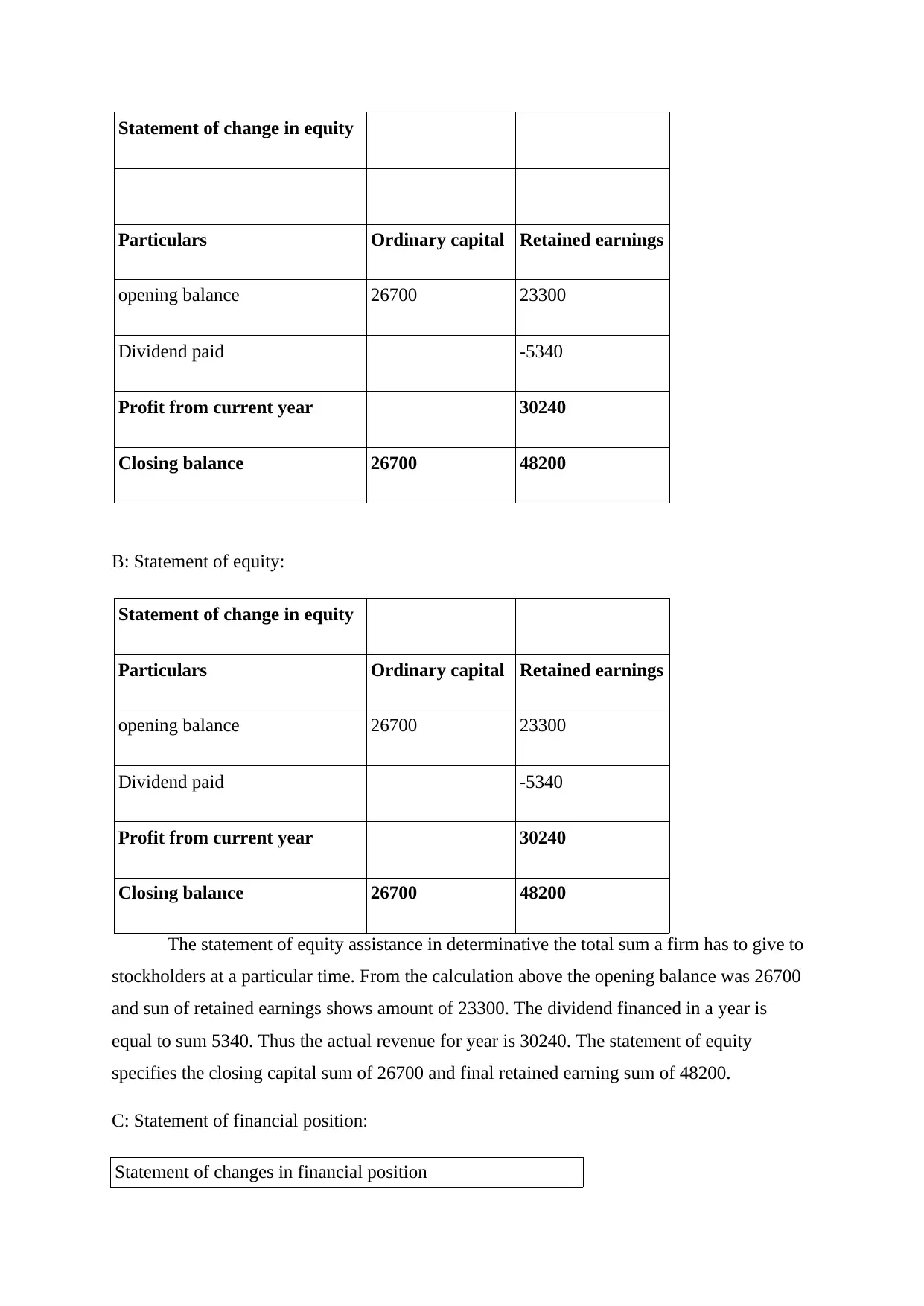

B: Statement of equity:

PBT 42240

Tax expenses 12000

Profit after tax for equity shareholders 30240

Working note:

Calculation of Depreciation: Amount

On Land and property:

Property 4000

Plant and equipment 48000-22400*12.5% 3200

Total 7200

Charged to cost of sales 3600

Charged to operating expenses 3600

Profit and loss statement gives the detail explanation about revenues and expenses of

company throughout a financial year. This also benefits to figure out the complete income

after removal all tax expenses and other adjustment.

From the above mention statement, it shows gross profit of 93400, profit after subtracting

operating outlays is 44600. It is observed that profit before tax is 42240 and after deducting

tax the actual profit for year is 30240.

B: Statement of equity:

Statement of change in equity

Particulars Ordinary capital Retained earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

B: Statement of equity:

Statement of change in equity

Particulars Ordinary capital Retained earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

The statement of equity assistance in determinative the total sum a firm has to give to

stockholders at a particular time. From the calculation above the opening balance was 26700

and sun of retained earnings shows amount of 23300. The dividend financed in a year is

equal to sum 5340. Thus the actual revenue for year is 30240. The statement of equity

specifies the closing capital sum of 26700 and final retained earning sum of 48200.

C: Statement of financial position:

Statement of changes in financial position

Particulars Ordinary capital Retained earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

B: Statement of equity:

Statement of change in equity

Particulars Ordinary capital Retained earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

The statement of equity assistance in determinative the total sum a firm has to give to

stockholders at a particular time. From the calculation above the opening balance was 26700

and sun of retained earnings shows amount of 23300. The dividend financed in a year is

equal to sum 5340. Thus the actual revenue for year is 30240. The statement of equity

specifies the closing capital sum of 26700 and final retained earning sum of 48200.

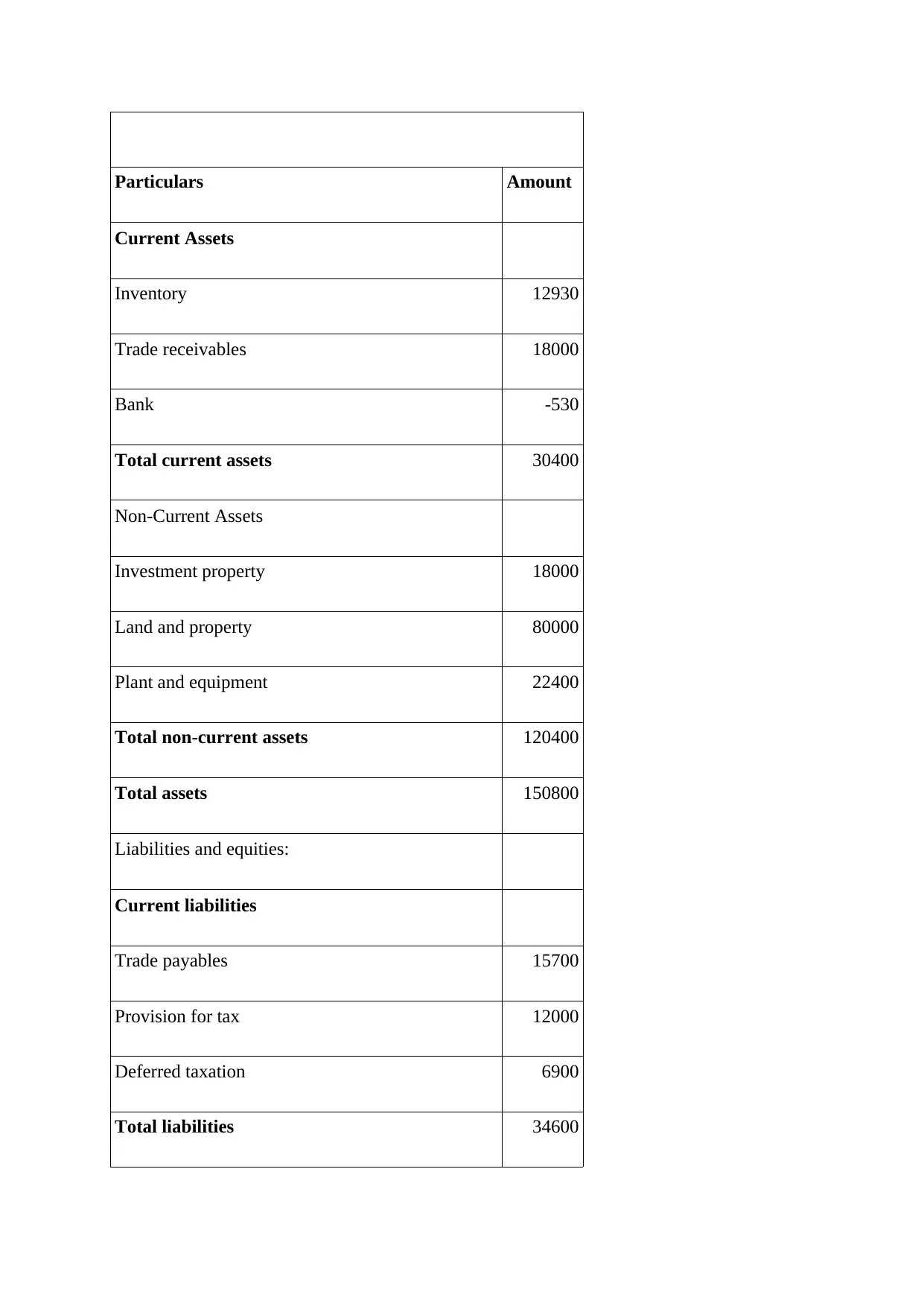

C: Statement of financial position:

Statement of changes in financial position

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Amount

Current Assets

Inventory 12930

Trade receivables 18000

Bank -530

Total current assets 30400

Non-Current Assets

Investment property 18000

Land and property 80000

Plant and equipment 22400

Total non-current assets 120400

Total assets 150800

Liabilities and equities:

Current liabilities

Trade payables 15700

Provision for tax 12000

Deferred taxation 6900

Total liabilities 34600

Current Assets

Inventory 12930

Trade receivables 18000

Bank -530

Total current assets 30400

Non-Current Assets

Investment property 18000

Land and property 80000

Plant and equipment 22400

Total non-current assets 120400

Total assets 150800

Liabilities and equities:

Current liabilities

Trade payables 15700

Provision for tax 12000

Deferred taxation 6900

Total liabilities 34600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

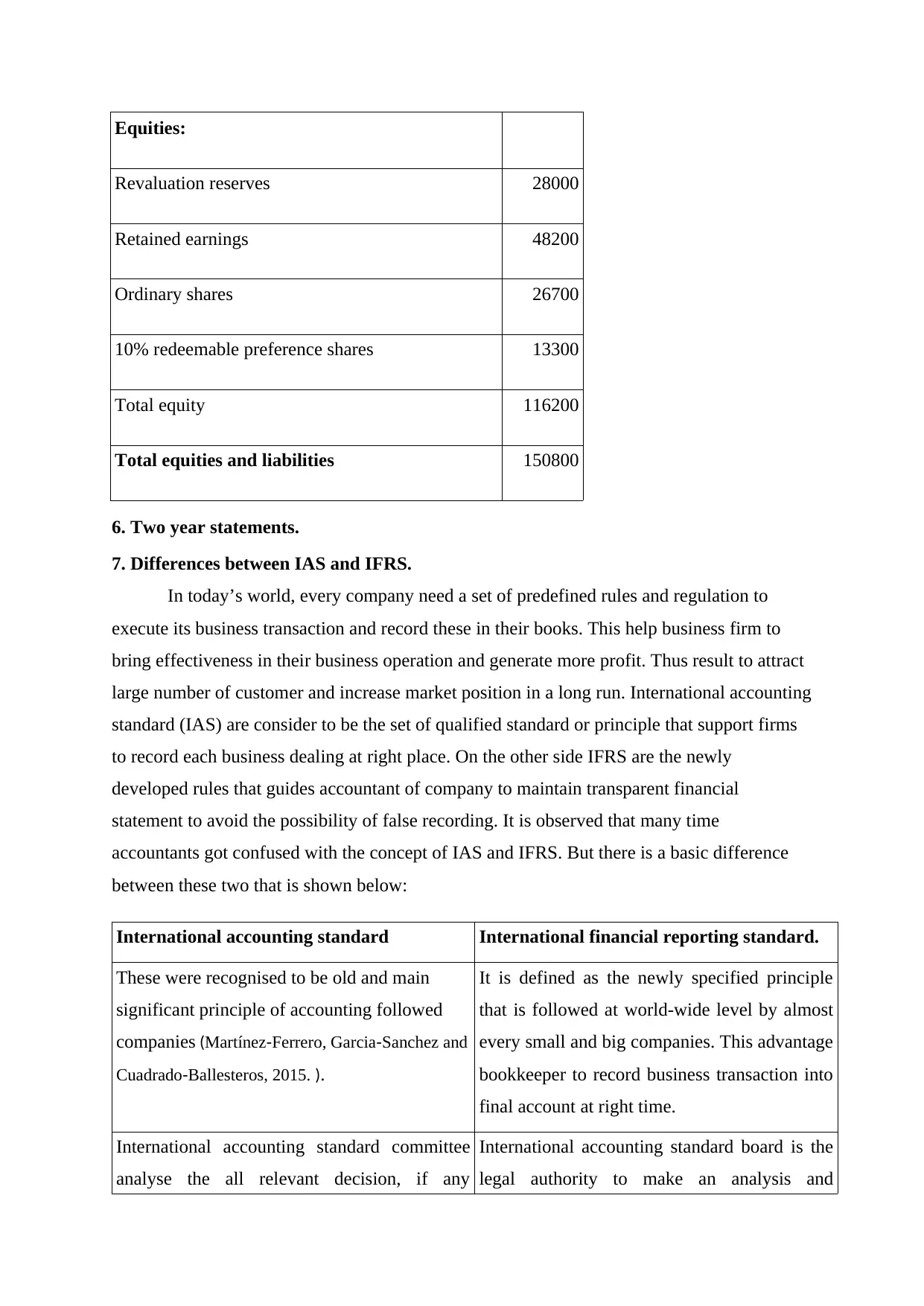

Equities:

Revaluation reserves 28000

Retained earnings 48200

Ordinary shares 26700

10% redeemable preference shares 13300

Total equity 116200

Total equities and liabilities 150800

6. Two year statements.

7. Differences between IAS and IFRS.

In today’s world, every company need a set of predefined rules and regulation to

execute its business transaction and record these in their books. This help business firm to

bring effectiveness in their business operation and generate more profit. Thus result to attract

large number of customer and increase market position in a long run. International accounting

standard (IAS) are consider to be the set of qualified standard or principle that support firms

to record each business dealing at right place. On the other side IFRS are the newly

developed rules that guides accountant of company to maintain transparent financial

statement to avoid the possibility of false recording. It is observed that many time

accountants got confused with the concept of IAS and IFRS. But there is a basic difference

between these two that is shown below:

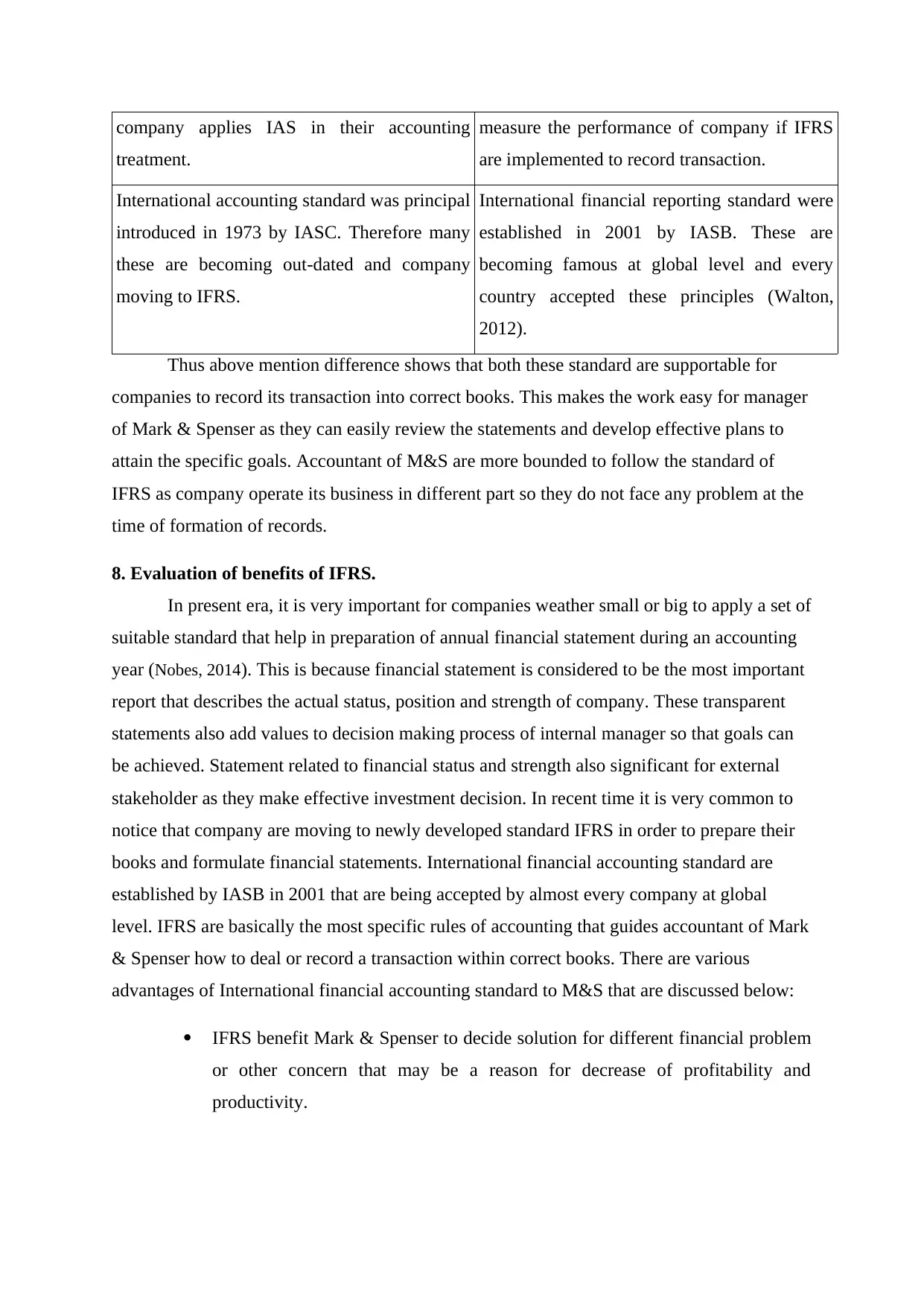

International accounting standard International financial reporting standard.

These were recognised to be old and main

significant principle of accounting followed

companies (Martínez‐Ferrero, Garcia‐Sanchez and

Cuadrado‐Ballesteros, 2015. ).

It is defined as the newly specified principle

that is followed at world-wide level by almost

every small and big companies. This advantage

bookkeeper to record business transaction into

final account at right time.

International accounting standard committee

analyse the all relevant decision, if any

International accounting standard board is the

legal authority to make an analysis and

Revaluation reserves 28000

Retained earnings 48200

Ordinary shares 26700

10% redeemable preference shares 13300

Total equity 116200

Total equities and liabilities 150800

6. Two year statements.

7. Differences between IAS and IFRS.

In today’s world, every company need a set of predefined rules and regulation to

execute its business transaction and record these in their books. This help business firm to

bring effectiveness in their business operation and generate more profit. Thus result to attract

large number of customer and increase market position in a long run. International accounting

standard (IAS) are consider to be the set of qualified standard or principle that support firms

to record each business dealing at right place. On the other side IFRS are the newly

developed rules that guides accountant of company to maintain transparent financial

statement to avoid the possibility of false recording. It is observed that many time

accountants got confused with the concept of IAS and IFRS. But there is a basic difference

between these two that is shown below:

International accounting standard International financial reporting standard.

These were recognised to be old and main

significant principle of accounting followed

companies (Martínez‐Ferrero, Garcia‐Sanchez and

Cuadrado‐Ballesteros, 2015. ).

It is defined as the newly specified principle

that is followed at world-wide level by almost

every small and big companies. This advantage

bookkeeper to record business transaction into

final account at right time.

International accounting standard committee

analyse the all relevant decision, if any

International accounting standard board is the

legal authority to make an analysis and

company applies IAS in their accounting

treatment.

measure the performance of company if IFRS

are implemented to record transaction.

International accounting standard was principal

introduced in 1973 by IASC. Therefore many

these are becoming out-dated and company

moving to IFRS.

International financial reporting standard were

established in 2001 by IASB. These are

becoming famous at global level and every

country accepted these principles (Walton,

2012).

Thus above mention difference shows that both these standard are supportable for

companies to record its transaction into correct books. This makes the work easy for manager

of Mark & Spenser as they can easily review the statements and develop effective plans to

attain the specific goals. Accountant of M&S are more bounded to follow the standard of

IFRS as company operate its business in different part so they do not face any problem at the

time of formation of records.

8. Evaluation of benefits of IFRS.

In present era, it is very important for companies weather small or big to apply a set of

suitable standard that help in preparation of annual financial statement during an accounting

year (Nobes, 2014). This is because financial statement is considered to be the most important

report that describes the actual status, position and strength of company. These transparent

statements also add values to decision making process of internal manager so that goals can

be achieved. Statement related to financial status and strength also significant for external

stakeholder as they make effective investment decision. In recent time it is very common to

notice that company are moving to newly developed standard IFRS in order to prepare their

books and formulate financial statements. International financial accounting standard are

established by IASB in 2001 that are being accepted by almost every company at global

level. IFRS are basically the most specific rules of accounting that guides accountant of Mark

& Spenser how to deal or record a transaction within correct books. There are various

advantages of International financial accounting standard to M&S that are discussed below:

IFRS benefit Mark & Spenser to decide solution for different financial problem

or other concern that may be a reason for decrease of profitability and

productivity.

treatment.

measure the performance of company if IFRS

are implemented to record transaction.

International accounting standard was principal

introduced in 1973 by IASC. Therefore many

these are becoming out-dated and company

moving to IFRS.

International financial reporting standard were

established in 2001 by IASB. These are

becoming famous at global level and every

country accepted these principles (Walton,

2012).

Thus above mention difference shows that both these standard are supportable for

companies to record its transaction into correct books. This makes the work easy for manager

of Mark & Spenser as they can easily review the statements and develop effective plans to

attain the specific goals. Accountant of M&S are more bounded to follow the standard of

IFRS as company operate its business in different part so they do not face any problem at the

time of formation of records.

8. Evaluation of benefits of IFRS.

In present era, it is very important for companies weather small or big to apply a set of

suitable standard that help in preparation of annual financial statement during an accounting

year (Nobes, 2014). This is because financial statement is considered to be the most important

report that describes the actual status, position and strength of company. These transparent

statements also add values to decision making process of internal manager so that goals can

be achieved. Statement related to financial status and strength also significant for external

stakeholder as they make effective investment decision. In recent time it is very common to

notice that company are moving to newly developed standard IFRS in order to prepare their

books and formulate financial statements. International financial accounting standard are

established by IASB in 2001 that are being accepted by almost every company at global

level. IFRS are basically the most specific rules of accounting that guides accountant of Mark

& Spenser how to deal or record a transaction within correct books. There are various

advantages of International financial accounting standard to M&S that are discussed below:

IFRS benefit Mark & Spenser to decide solution for different financial problem

or other concern that may be a reason for decrease of profitability and

productivity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.