Financial Reporting and Analysis: Marks and Spencer Performance Report

VerifiedAdded on 2020/12/29

|14

|2951

|137

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, encompassing the conceptual and regulatory framework, qualitative characteristics, and the role of financial information for various stakeholders. It explores the value of financial reporting in achieving organizational objectives and examines financial statements as per IAS 1. The report includes a detailed analysis of Marks and Spencer's financial performance, utilizing key financial ratios such as liquidity, profitability, solvency, and efficiency ratios for 2017 and 2018, with an interpretation of the results. Furthermore, the report differentiates between International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), highlighting their benefits and key differences. This analysis is crucial for understanding how financial reporting supports decision-making and organizational growth.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financial reporting is preparation of various statements and reports for disclosing

financial information which assist in identifying the performance and position of the organization

for a period. Marks and Spencer will be included in this assignment for interpreting the financial

performance on the basis of financial statements. This study will include the conceptual and

regulatory framework and qualitative characteristics required for making the financial

information more reliable. Furthermore, it will include main stakeholders of the organization

which are provided with financial reports. Moreover, this assignment will examine the value of

financial reporting for achieving the organizational objectives. Also, this study will provide with

financial statements which are required as per IAS 1. It will include financial ratios for

organization performance and investment. This study will assist in differentiating between

International accounting standards and international financial reporting standards.

MAIN BODY

1. Context and purpose of financial reporting

Financial reporting is related to presentation of various reports and statements for the

purpose of providing financial information to the stakeholders of the organization. Financial

reporting shows the performance of the enterprise and its position. Financial reporting are

prepared for mainly two purpose which include providing information to the management for

effective decision – making to improve the enterprise performance (Kaya and Koch, 2015).

Another purpose of preparing financial reporting is to provide information to the external

stakeholders to provide them understanding of company's liquidity position.

Financial reporting helps ion providing information to customers, investors, suppliers,

government etc (Rajgopal, 2015). Financial reporting include profit and loss account, balance

sheet and cash flow statement. Profit and loss statement helps the firm in identify its performance

for the period by identifying the net profit or loss. Profit and loss statement include expenses and

income for a period. Balance sheet helps in identifying the position of company on the basis of

assets and liabilities. Cash flow statement under financial reporting helps in finding out cash

inflows and outflows for the period.

This reporting is necessary for the organization for disclosure of its financial information

to have record of its various transaction to pay the tax to the government (Leuz and Wysocki,

1

Financial reporting is preparation of various statements and reports for disclosing

financial information which assist in identifying the performance and position of the organization

for a period. Marks and Spencer will be included in this assignment for interpreting the financial

performance on the basis of financial statements. This study will include the conceptual and

regulatory framework and qualitative characteristics required for making the financial

information more reliable. Furthermore, it will include main stakeholders of the organization

which are provided with financial reports. Moreover, this assignment will examine the value of

financial reporting for achieving the organizational objectives. Also, this study will provide with

financial statements which are required as per IAS 1. It will include financial ratios for

organization performance and investment. This study will assist in differentiating between

International accounting standards and international financial reporting standards.

MAIN BODY

1. Context and purpose of financial reporting

Financial reporting is related to presentation of various reports and statements for the

purpose of providing financial information to the stakeholders of the organization. Financial

reporting shows the performance of the enterprise and its position. Financial reporting are

prepared for mainly two purpose which include providing information to the management for

effective decision – making to improve the enterprise performance (Kaya and Koch, 2015).

Another purpose of preparing financial reporting is to provide information to the external

stakeholders to provide them understanding of company's liquidity position.

Financial reporting helps ion providing information to customers, investors, suppliers,

government etc (Rajgopal, 2015). Financial reporting include profit and loss account, balance

sheet and cash flow statement. Profit and loss statement helps the firm in identify its performance

for the period by identifying the net profit or loss. Profit and loss statement include expenses and

income for a period. Balance sheet helps in identifying the position of company on the basis of

assets and liabilities. Cash flow statement under financial reporting helps in finding out cash

inflows and outflows for the period.

This reporting is necessary for the organization for disclosure of its financial information

to have record of its various transaction to pay the tax to the government (Leuz and Wysocki,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

016). Financial reporting is mandatory for the company to prepare to provide information to

government for paying tax.

2. Conceptual and regulatory framework and qualitative characteristics that makes the financial

information reliable

The conceptual and regulatory framework of financial reporting defines various laws and

standards on the basis of which financial statements are prepared(Francis and et.al., 2015).

Financial reporting is governed by standards of regulatory framework such as IAS and IFRS.

Financial reporting is prepared by the framework provided by international accounting standard

board(IAS) in which standards were issued by IAS committee (Holland, 2015). International

financial reporting standards which provide framework for preparing financial statements on the

basis of standards set by International financial reporting standards board.

Qualitative characteristics which makes the financial information reliable consist of :

Relevance : It involves that the accounting information contained in the financial

statements must pertain to specific time period and also provide relevant information of

the financial transaction which assist in decision – making (Frias‐Aceituno, Rodríguez‐

Ariza and Garcia‐Sánchez, 2014).

Reliability : The financial information must be reliable in order to provide understanding

for decision making and the information contained must be reliable and based on facts

(Ge and et.al., 2018). It provides that information provide in financial report must assist

users in decision making on the basis of those reports to identify financial position of

business.

Comparability : The information disclosed in the financial statements must be

comparable with other company's to make choices which will helps in improving

performance and also asst in identifying company's performance by comparing it with

other organization (Robson, Young and Power, 2017).

Consistency : The financial information to be more reliable must be presented

consistently from year to year.

3. The main stakeholders of an organization and benefits to them of financial information

The main stakeholders of the company consist of internal and external . The following

are the various stakeholders which are provided with the financial reports to provide them

various financial information.

2

government for paying tax.

2. Conceptual and regulatory framework and qualitative characteristics that makes the financial

information reliable

The conceptual and regulatory framework of financial reporting defines various laws and

standards on the basis of which financial statements are prepared(Francis and et.al., 2015).

Financial reporting is governed by standards of regulatory framework such as IAS and IFRS.

Financial reporting is prepared by the framework provided by international accounting standard

board(IAS) in which standards were issued by IAS committee (Holland, 2015). International

financial reporting standards which provide framework for preparing financial statements on the

basis of standards set by International financial reporting standards board.

Qualitative characteristics which makes the financial information reliable consist of :

Relevance : It involves that the accounting information contained in the financial

statements must pertain to specific time period and also provide relevant information of

the financial transaction which assist in decision – making (Frias‐Aceituno, Rodríguez‐

Ariza and Garcia‐Sánchez, 2014).

Reliability : The financial information must be reliable in order to provide understanding

for decision making and the information contained must be reliable and based on facts

(Ge and et.al., 2018). It provides that information provide in financial report must assist

users in decision making on the basis of those reports to identify financial position of

business.

Comparability : The information disclosed in the financial statements must be

comparable with other company's to make choices which will helps in improving

performance and also asst in identifying company's performance by comparing it with

other organization (Robson, Young and Power, 2017).

Consistency : The financial information to be more reliable must be presented

consistently from year to year.

3. The main stakeholders of an organization and benefits to them of financial information

The main stakeholders of the company consist of internal and external . The following

are the various stakeholders which are provided with the financial reports to provide them

various financial information.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Internal stakeholders

Managers : Managers of the organization are provided with financial re-porting for

planning, decision- making and managing the operation of the business to increase profitability

of firm.

Employees : Employees are the internal stakeholders of the company which are provided

with the reporting providing them information for their future job prospects by

identifying performance of company and its position (Chychyla, Leone and Minutti-

Meza, 2018). Board of directors : financial information is used by BOD for identifying their

company's performance and position to formulate various policies for growth of organization.

External stakeholders

Investors : The financial information is beneficial for the investors of shareholders of the

organization to identify their returns on the capital invested by them in the firm.

Lenders : lenders of the organization require financial information to identify the interest

on loans and information regarding repayment of loans.

Customers : Financial information helps the customers to identify the stability and

various operations of the organization which assist them in identifying company's ability

to meet their demands.

Government : Government requires the financial information of the company to identify

the ability of firm for payment of taxes and for compliance of the regulation(Call And

et.al., 2017).

Financial information helps the stakeholders of the company to identify the performance

of firm and also about the position it holds to know about growth of company and its ability to

pay its various obligation.

4. Value of financial reporting for meeting organizational objectives and growth

Financial reporting assist the organization in recording the various transaction for the

operation performed by the firm(Feng and et.al., 2014). Financial reporting have its value in the

organization to achieve the business goals and growth of enterprise.

Financial reporting are required for complying with various laws and regulation top

provide information to government and various regulatory bodies for the tax purposes.

3

Managers : Managers of the organization are provided with financial re-porting for

planning, decision- making and managing the operation of the business to increase profitability

of firm.

Employees : Employees are the internal stakeholders of the company which are provided

with the reporting providing them information for their future job prospects by

identifying performance of company and its position (Chychyla, Leone and Minutti-

Meza, 2018). Board of directors : financial information is used by BOD for identifying their

company's performance and position to formulate various policies for growth of organization.

External stakeholders

Investors : The financial information is beneficial for the investors of shareholders of the

organization to identify their returns on the capital invested by them in the firm.

Lenders : lenders of the organization require financial information to identify the interest

on loans and information regarding repayment of loans.

Customers : Financial information helps the customers to identify the stability and

various operations of the organization which assist them in identifying company's ability

to meet their demands.

Government : Government requires the financial information of the company to identify

the ability of firm for payment of taxes and for compliance of the regulation(Call And

et.al., 2017).

Financial information helps the stakeholders of the company to identify the performance

of firm and also about the position it holds to know about growth of company and its ability to

pay its various obligation.

4. Value of financial reporting for meeting organizational objectives and growth

Financial reporting assist the organization in recording the various transaction for the

operation performed by the firm(Feng and et.al., 2014). Financial reporting have its value in the

organization to achieve the business goals and growth of enterprise.

Financial reporting are required for complying with various laws and regulation top

provide information to government and various regulatory bodies for the tax purposes.

3

Financial reporting is important as it provides information to the investors and creditors

about the financial integrity and creditworthiness of the firm to pay higher returns and its

obligations. It helps in attracting more investors for the company to increase profitability

of firm which will assist in the growth of organization.

Financial reporting are useful as it helps in providing information to the management

about the performance of the firm on the basis of which various policies and strategies

are planned for improving performance of firm(Tschopp and Huefner, 2015).

Financial reporting helps in achieving the organization objective by using the previous

financial statements for planning to improve the performance and profitability of the

organization.

Financial reporting helps in making budgets to improve the performance of organization

to achieve the objectives by comparing the actual with the budgeted.

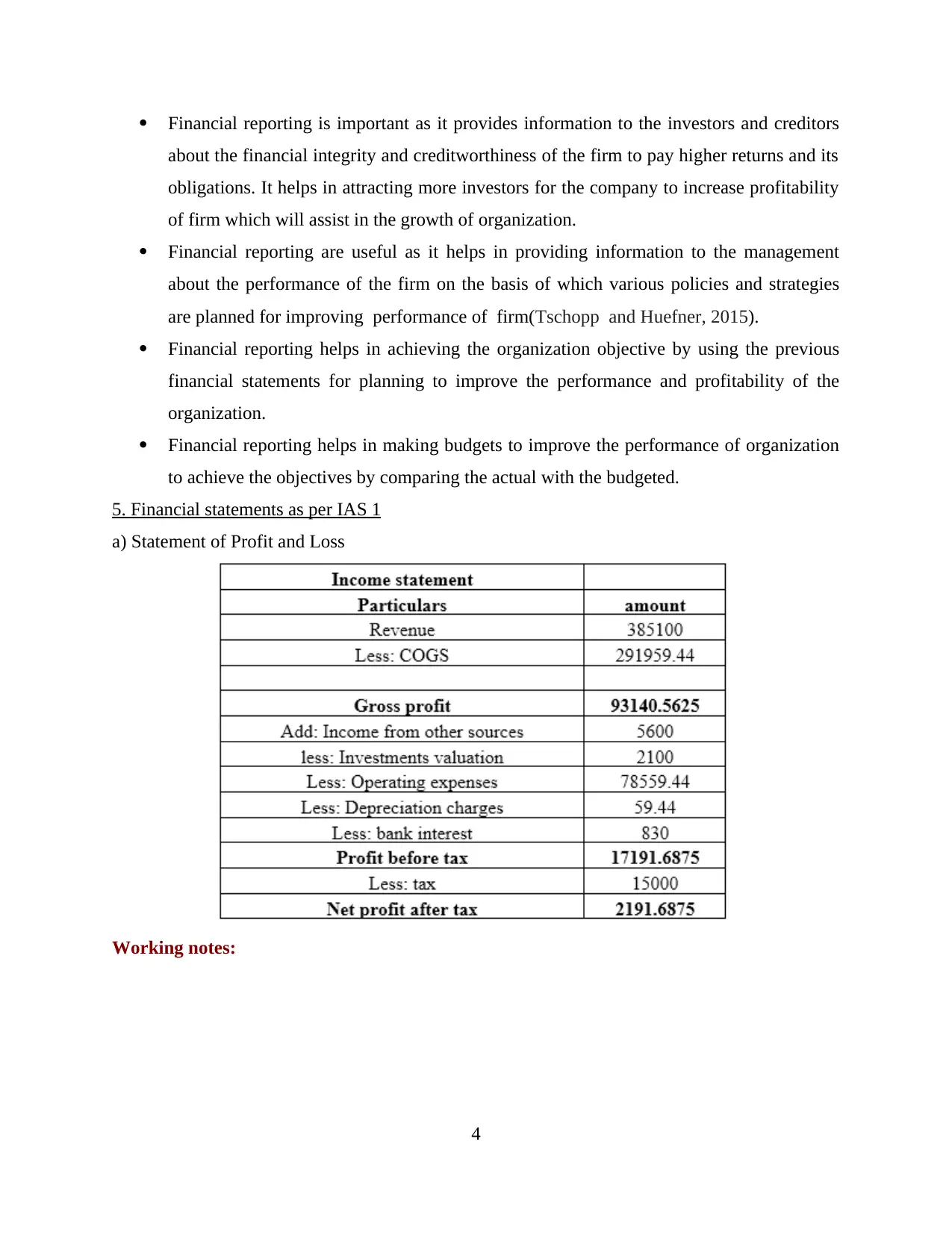

5. Financial statements as per IAS 1

a) Statement of Profit and Loss

Working notes:

4

about the financial integrity and creditworthiness of the firm to pay higher returns and its

obligations. It helps in attracting more investors for the company to increase profitability

of firm which will assist in the growth of organization.

Financial reporting are useful as it helps in providing information to the management

about the performance of the firm on the basis of which various policies and strategies

are planned for improving performance of firm(Tschopp and Huefner, 2015).

Financial reporting helps in achieving the organization objective by using the previous

financial statements for planning to improve the performance and profitability of the

organization.

Financial reporting helps in making budgets to improve the performance of organization

to achieve the objectives by comparing the actual with the budgeted.

5. Financial statements as per IAS 1

a) Statement of Profit and Loss

Working notes:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Statement of Changes In Equity

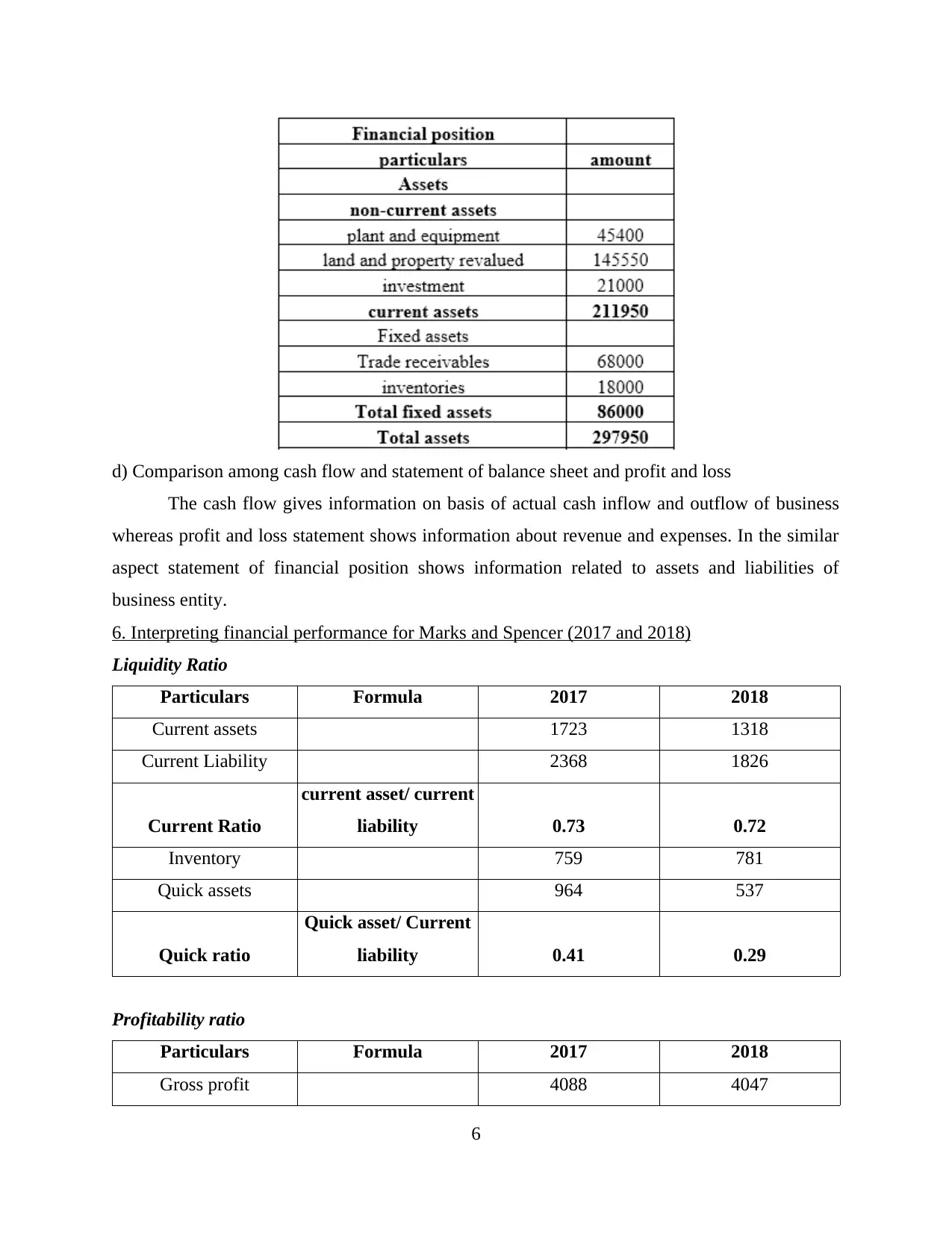

c) Statement of Financial position

5

c) Statement of Financial position

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d) Comparison among cash flow and statement of balance sheet and profit and loss

The cash flow gives information on basis of actual cash inflow and outflow of business

whereas profit and loss statement shows information about revenue and expenses. In the similar

aspect statement of financial position shows information related to assets and liabilities of

business entity.

6. Interpreting financial performance for Marks and Spencer (2017 and 2018)

Liquidity Ratio

Particulars Formula 2017 2018

Current assets 1723 1318

Current Liability 2368 1826

Current Ratio

current asset/ current

liability 0.73 0.72

Inventory 759 781

Quick assets 964 537

Quick ratio

Quick asset/ Current

liability 0.41 0.29

Profitability ratio

Particulars Formula 2017 2018

Gross profit 4088 4047

6

The cash flow gives information on basis of actual cash inflow and outflow of business

whereas profit and loss statement shows information about revenue and expenses. In the similar

aspect statement of financial position shows information related to assets and liabilities of

business entity.

6. Interpreting financial performance for Marks and Spencer (2017 and 2018)

Liquidity Ratio

Particulars Formula 2017 2018

Current assets 1723 1318

Current Liability 2368 1826

Current Ratio

current asset/ current

liability 0.73 0.72

Inventory 759 781

Quick assets 964 537

Quick ratio

Quick asset/ Current

liability 0.41 0.29

Profitability ratio

Particulars Formula 2017 2018

Gross profit 4088 4047

6

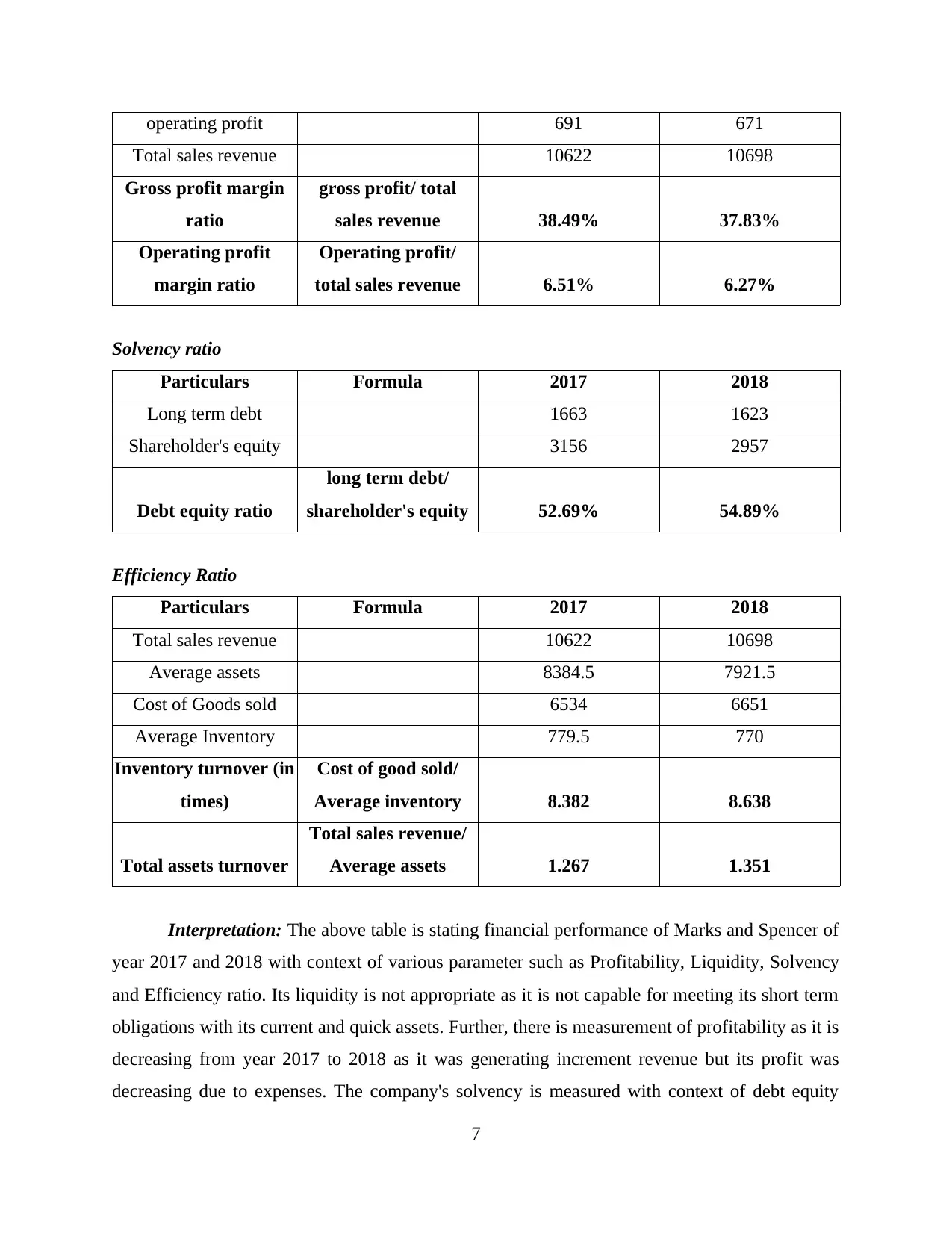

operating profit 691 671

Total sales revenue 10622 10698

Gross profit margin

ratio

gross profit/ total

sales revenue 38.49% 37.83%

Operating profit

margin ratio

Operating profit/

total sales revenue 6.51% 6.27%

Solvency ratio

Particulars Formula 2017 2018

Long term debt 1663 1623

Shareholder's equity 3156 2957

Debt equity ratio

long term debt/

shareholder's equity 52.69% 54.89%

Efficiency Ratio

Particulars Formula 2017 2018

Total sales revenue 10622 10698

Average assets 8384.5 7921.5

Cost of Goods sold 6534 6651

Average Inventory 779.5 770

Inventory turnover (in

times)

Cost of good sold/

Average inventory 8.382 8.638

Total assets turnover

Total sales revenue/

Average assets 1.267 1.351

Interpretation: The above table is stating financial performance of Marks and Spencer of

year 2017 and 2018 with context of various parameter such as Profitability, Liquidity, Solvency

and Efficiency ratio. Its liquidity is not appropriate as it is not capable for meeting its short term

obligations with its current and quick assets. Further, there is measurement of profitability as it is

decreasing from year 2017 to 2018 as it was generating increment revenue but its profit was

decreasing due to expenses. The company's solvency is measured with context of debt equity

7

Total sales revenue 10622 10698

Gross profit margin

ratio

gross profit/ total

sales revenue 38.49% 37.83%

Operating profit

margin ratio

Operating profit/

total sales revenue 6.51% 6.27%

Solvency ratio

Particulars Formula 2017 2018

Long term debt 1663 1623

Shareholder's equity 3156 2957

Debt equity ratio

long term debt/

shareholder's equity 52.69% 54.89%

Efficiency Ratio

Particulars Formula 2017 2018

Total sales revenue 10622 10698

Average assets 8384.5 7921.5

Cost of Goods sold 6534 6651

Average Inventory 779.5 770

Inventory turnover (in

times)

Cost of good sold/

Average inventory 8.382 8.638

Total assets turnover

Total sales revenue/

Average assets 1.267 1.351

Interpretation: The above table is stating financial performance of Marks and Spencer of

year 2017 and 2018 with context of various parameter such as Profitability, Liquidity, Solvency

and Efficiency ratio. Its liquidity is not appropriate as it is not capable for meeting its short term

obligations with its current and quick assets. Further, there is measurement of profitability as it is

decreasing from year 2017 to 2018 as it was generating increment revenue but its profit was

decreasing due to expenses. The company's solvency is measured with context of debt equity

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ratio as it is not having optimal capital structure, in both years' organization has huge debts

which is financial risk. In the similar aspect, its efficiency has been measured with reference to

inventory and total asset turnover. These both parameters are increasing which shows

organization is highly efficient (Omar and et.al., 2014).

7. Explaining difference between International Financial Reporting Standards and international

Accounting Standards

The accounting standards are issued through IASB (International accounting Standards

Board).The organization which are listed on locally aspect and undertaken in obligation with

implication of financial statements in particular countries have directly accepted these standards.

IFRS (International Financial Reporting Standards): It is considered as set of

accounting standards which is developed through independent and non profit organization is

referred as IASB.

IAS (International Accounting Standards): It is older version of standards with context

of different type of transactions along with other events which should be presented in financial

statements. Previously these standards were issued through Board of the International

Accounting Standards Committee as from year 2001, new version of standards were developed

referred as IFRS and issued via IASB. As there was no authority with need of appropriate

compliance with context of accounting standards as various countries has need of financial

statements of companies (publicly traded) must be prepared as per IAS.

There is presence to two key differences among IAS and IFRS which are stated below;

Every IFRS would include basis of any decision with reference to each standard: It

directly fit with intention of IASB for adopting principles on basis of approach to setting

standards. The IASB is reviewing on current aspect with number of IAS and it will be

linked as IAS as IASB could not refer with context of decisions taken whereas original

IAS was specified. On basis of outcome, both IAS and IFRs would be running parallel til

IAS was superseded through IFRS (Why global accounting standards, 2017).

The bold text in IFRS is considered for guiding principles of standard: The bold text

is considered as compulsory elements on basis of standards.

8. Evaluating benefits of IFRS

International Financial Reporting standards is considered as set of international

accounting standards with context of kinds of transactions and events stated in financial

8

which is financial risk. In the similar aspect, its efficiency has been measured with reference to

inventory and total asset turnover. These both parameters are increasing which shows

organization is highly efficient (Omar and et.al., 2014).

7. Explaining difference between International Financial Reporting Standards and international

Accounting Standards

The accounting standards are issued through IASB (International accounting Standards

Board).The organization which are listed on locally aspect and undertaken in obligation with

implication of financial statements in particular countries have directly accepted these standards.

IFRS (International Financial Reporting Standards): It is considered as set of

accounting standards which is developed through independent and non profit organization is

referred as IASB.

IAS (International Accounting Standards): It is older version of standards with context

of different type of transactions along with other events which should be presented in financial

statements. Previously these standards were issued through Board of the International

Accounting Standards Committee as from year 2001, new version of standards were developed

referred as IFRS and issued via IASB. As there was no authority with need of appropriate

compliance with context of accounting standards as various countries has need of financial

statements of companies (publicly traded) must be prepared as per IAS.

There is presence to two key differences among IAS and IFRS which are stated below;

Every IFRS would include basis of any decision with reference to each standard: It

directly fit with intention of IASB for adopting principles on basis of approach to setting

standards. The IASB is reviewing on current aspect with number of IAS and it will be

linked as IAS as IASB could not refer with context of decisions taken whereas original

IAS was specified. On basis of outcome, both IAS and IFRs would be running parallel til

IAS was superseded through IFRS (Why global accounting standards, 2017).

The bold text in IFRS is considered for guiding principles of standard: The bold text

is considered as compulsory elements on basis of standards.

8. Evaluating benefits of IFRS

International Financial Reporting standards is considered as set of international

accounting standards with context of kinds of transactions and events stated in financial

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statements. It is issued through international accounting standards and reflects methods of

accountants for reporting and maintaining accounts. These standards address challenge by giving

the best quality and set of accounting standards which are recognised globally as they bring

accountability, efficiency and transparency to financial markets throughout the world. The

advantages are stated below:

The accountability has been strengthened with standards of IFRS as they decrease

information gap among capital providers and people where money is entrusted. It gives

information with requirement for holding management to account. The globally source of

comparable information, these standards has huge importance to its regulators throughout

the world.

These standards would be contributing to economic efficiency for helping its investor for

determining opportunities along with risk across the world along with raising capital

allocation. With reference to business, application of single and trusted language of

accounting will lower cost of capital and will decrease cost of international reporting.

These standards would be bringing transparency with reference to enhancing

international quality and comparability of financial information and it enables investors

along with other market participants for undertaking informed economic decisions.

It helps in setting benchmark for organization and it brings homogeneity with context of

financial reporting (6 Advantages and Disadvantages of Adopting IFRS, 2018).

The IFRS could help small and innovative investors through framing reporting standards

for better quality and simpler aspect as it puts investors in similar position along with

professional investors as they were not feasible with context of previous standards. Thus,

it helps in entailing for decreasing risk for these investors during trade as professionals

will be not capable for taking advantage due to financial statement's nature as it will be

simple and understood for all.

9. Identifying degree of compliance with IFRS along with factors which impact compliance

International financial reporting standards is outcome of decades for pursuing a

accounting and financial reporting standards which are universally accepted. In the present

scenario, there are more than 150 countries which are using similar accounting standards with

specific version of IFRS which are published through IASB including United States and Japan

has programs for placing converging national standards with reference to IFRS. There are

9

accountants for reporting and maintaining accounts. These standards address challenge by giving

the best quality and set of accounting standards which are recognised globally as they bring

accountability, efficiency and transparency to financial markets throughout the world. The

advantages are stated below:

The accountability has been strengthened with standards of IFRS as they decrease

information gap among capital providers and people where money is entrusted. It gives

information with requirement for holding management to account. The globally source of

comparable information, these standards has huge importance to its regulators throughout

the world.

These standards would be contributing to economic efficiency for helping its investor for

determining opportunities along with risk across the world along with raising capital

allocation. With reference to business, application of single and trusted language of

accounting will lower cost of capital and will decrease cost of international reporting.

These standards would be bringing transparency with reference to enhancing

international quality and comparability of financial information and it enables investors

along with other market participants for undertaking informed economic decisions.

It helps in setting benchmark for organization and it brings homogeneity with context of

financial reporting (6 Advantages and Disadvantages of Adopting IFRS, 2018).

The IFRS could help small and innovative investors through framing reporting standards

for better quality and simpler aspect as it puts investors in similar position along with

professional investors as they were not feasible with context of previous standards. Thus,

it helps in entailing for decreasing risk for these investors during trade as professionals

will be not capable for taking advantage due to financial statement's nature as it will be

simple and understood for all.

9. Identifying degree of compliance with IFRS along with factors which impact compliance

International financial reporting standards is outcome of decades for pursuing a

accounting and financial reporting standards which are universally accepted. In the present

scenario, there are more than 150 countries which are using similar accounting standards with

specific version of IFRS which are published through IASB including United States and Japan

has programs for placing converging national standards with reference to IFRS. There are

9

various multinational companies and national regulators for endorsing IFRS due to easy

comparability financial outcome of reporting entities through various countries as if public

companies, financial statements were formed with application of standards and allows investors

for understanding opportunities in better aspect.

The big public organizations with reference to multiple charts and books in numerous

jurisdiction with capability of using single accounting language from its competitors. The other

advantages is with context of AICPA within true global economy along with financial

professionals and CPA would be more mobile and organization would be capable for responding

to need of human capital of their subsidiaries throughout world with implication of one standard.

The level of compliance is identified jointly by country and company level variables as it

indicates various accounting traditions along with country specific factors which will continue to

contribute in role with application of common reporting standards with reference to IFRS. The

company level, significance of goodwill position, prior experience through IFRS, existence of

audit committees, kinds of auditor, issuing equity share and bonds and structure of ownership are

influential factors. In the same series, at country level size of national stock market, strength of

enforcement are linked with compliance. These factors does not directly influence compliance

but mediate and moderate company level factors. Simultaneously, national culture in context of

strength of national traditions will directly impact compliance in context of company level

factors (Compliance with IAS/IFRS and firm characteristics, 2018).

CONCLUSION

From this study it has been concluded about financial reporting which has been used by

stakeholders that provided information to them about organisation performance and position.

This assignment has included context and purpose of financial reporting in which it has

concluded that financial reporting main purpose is to provide information to management for

decision making to improve organisation performance. Furthermore, it has included various

stakeholders of company such as employees, managers, customers, investors, government and

suppliers. Moreover, it has provided with value of financial reporting to organisation. Also, this

study has provided with financial statements such as profit and loss, balance sheet, statement of

changes in equity and cash flow statements. This assignment has also explained about difference

between international accounting standard and international financial reporting standard.

10

comparability financial outcome of reporting entities through various countries as if public

companies, financial statements were formed with application of standards and allows investors

for understanding opportunities in better aspect.

The big public organizations with reference to multiple charts and books in numerous

jurisdiction with capability of using single accounting language from its competitors. The other

advantages is with context of AICPA within true global economy along with financial

professionals and CPA would be more mobile and organization would be capable for responding

to need of human capital of their subsidiaries throughout world with implication of one standard.

The level of compliance is identified jointly by country and company level variables as it

indicates various accounting traditions along with country specific factors which will continue to

contribute in role with application of common reporting standards with reference to IFRS. The

company level, significance of goodwill position, prior experience through IFRS, existence of

audit committees, kinds of auditor, issuing equity share and bonds and structure of ownership are

influential factors. In the same series, at country level size of national stock market, strength of

enforcement are linked with compliance. These factors does not directly influence compliance

but mediate and moderate company level factors. Simultaneously, national culture in context of

strength of national traditions will directly impact compliance in context of company level

factors (Compliance with IAS/IFRS and firm characteristics, 2018).

CONCLUSION

From this study it has been concluded about financial reporting which has been used by

stakeholders that provided information to them about organisation performance and position.

This assignment has included context and purpose of financial reporting in which it has

concluded that financial reporting main purpose is to provide information to management for

decision making to improve organisation performance. Furthermore, it has included various

stakeholders of company such as employees, managers, customers, investors, government and

suppliers. Moreover, it has provided with value of financial reporting to organisation. Also, this

study has provided with financial statements such as profit and loss, balance sheet, statement of

changes in equity and cash flow statements. This assignment has also explained about difference

between international accounting standard and international financial reporting standard.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.