MFRS 136: Analysis of Favelle Favco Berhad Financial Reporting

VerifiedAdded on 2020/10/05

|11

|2928

|193

Report

AI Summary

This report provides a comprehensive analysis of Favelle Favco Berhad's financial reporting, focusing on the application of MFRS 136, the Malaysian Financial Reporting Standard concerning the impairment of assets. The report begins with an introduction to Favelle Favco Berhad, outlining its business operations and financial performance in 2017, highlighting key financial metrics such as turnover, profit, and equity. The core of the report is structured around three main points. Point 1 explains five crucial disclosure items required by MFRS 136 in annual reports, including Property, Plant, and Equipment (PPE), goodwill, investments in associates, intellectual property, and amortization. Point 2 examines MFRS 136 disclosure compliance and the format presented by the organization, emphasizing the importance of assessing assets annually for potential impairment and providing details on required disclosures regarding impairment losses and reversals. Point 3 discusses the recognition and measurement requirements outlined in MFRS 136, clarifying how impairment losses are recognized and measured, with a focus on the treatment of individual assets and cash-generating units. The report concludes by emphasizing the significance of adhering to MFRS 136 to ensure accurate financial statements and facilitate informed decision-making by stakeholders. The report provides a solid understanding of how financial accounting plays a crucial role in the business by getting clarity in the business transactions accounted for.

Intermediate Financial

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Point 1 – Explaining five items of MFRS 136 requirements for disclosure in annual report of

company.................................................................................................................................2

Point 2 – MFRS 136 disclosure compliance and format presented by organisation..............3

Point 3 – Discussing recognition and measurement requirements in MFRS 136 standard....5

SUMMARY.....................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

Point 1 – Explaining five items of MFRS 136 requirements for disclosure in annual report of

company.................................................................................................................................2

Point 2 – MFRS 136 disclosure compliance and format presented by organisation..............3

Point 3 – Discussing recognition and measurement requirements in MFRS 136 standard....5

SUMMARY.....................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

Favello Favco Berhad is a private investment holding organization working in

manufacturing, supply and sevice, designing industry. The company was founded in 1962 and its

main branch of the company is located in Senawang, Malaysia. It is a subsidiary of Muhibbah

Engineering Berhad. It operates through inside and outside Malaysia segments. The product line

of this company includes, heavy lift offshore, tower, wharf and crawler cranes. It consists of

mainly 2 international brands working together, i.e. Favelle Favco and Kroll. Tower cranes

which include Kroll cranes are basically heavy lifting electric hammerhead cranes and Favelle

Favco cranes are high speed diesel hydraulic luffing cranes.

The company offers two main series to their customers, which include rope luffing and

ram luffing set-ups. Their crawler cranes has lattice boom and telescopic boom present in it.

Wharf cranes of this company includes level luffing bulk handling cranes. Wharf cranes offers

both luffing and hammerhead cranes with diesel hydraulic and electric setups with it. Favelle

Favco Berhad company's subsidiaries includes Favelle Favco Cranes (M) Sdn. Bhd., which

provide services related to designing, manufacturing, supply, servicing, trading and renting of

cranes, and FES Equipment Services Sdn. Bhd., which works basically in supply of spare parts

related to cranes, provision of crane maintenance services and renting of cranes. Apart from this

Favello Favco includes up-to-date and well maintained equipment to their clients and deliver

their service on time. The main activity of this company is to manufacture unique and different

cranes which can be used for the purpose of construction.

Financial accounting plays crucial role in the business in getting clarity in the business

transactions accounted for. Present report deals with Favelle Favco Berhad which is engaged in

manufacturing industry and engaged in constructing cranes in effective manner. Adequate profits

are being attained by company as financial report clarifies that turnover in 2017 was 526,484.

Profit Before Interest and Tax were 83,277 in 2017 in comparison to 79,782 in previous year.

Profit attributable to shareholders in the same year was 63,097 while, total equity to investors

were amounting to 629,509. Share capital was 155,170 and EPS (Earnings Per Share) was 28.50

and net assets per share was 2.84. This means that profit is increased in 2017 financial year.

1

Favello Favco Berhad is a private investment holding organization working in

manufacturing, supply and sevice, designing industry. The company was founded in 1962 and its

main branch of the company is located in Senawang, Malaysia. It is a subsidiary of Muhibbah

Engineering Berhad. It operates through inside and outside Malaysia segments. The product line

of this company includes, heavy lift offshore, tower, wharf and crawler cranes. It consists of

mainly 2 international brands working together, i.e. Favelle Favco and Kroll. Tower cranes

which include Kroll cranes are basically heavy lifting electric hammerhead cranes and Favelle

Favco cranes are high speed diesel hydraulic luffing cranes.

The company offers two main series to their customers, which include rope luffing and

ram luffing set-ups. Their crawler cranes has lattice boom and telescopic boom present in it.

Wharf cranes of this company includes level luffing bulk handling cranes. Wharf cranes offers

both luffing and hammerhead cranes with diesel hydraulic and electric setups with it. Favelle

Favco Berhad company's subsidiaries includes Favelle Favco Cranes (M) Sdn. Bhd., which

provide services related to designing, manufacturing, supply, servicing, trading and renting of

cranes, and FES Equipment Services Sdn. Bhd., which works basically in supply of spare parts

related to cranes, provision of crane maintenance services and renting of cranes. Apart from this

Favello Favco includes up-to-date and well maintained equipment to their clients and deliver

their service on time. The main activity of this company is to manufacture unique and different

cranes which can be used for the purpose of construction.

Financial accounting plays crucial role in the business in getting clarity in the business

transactions accounted for. Present report deals with Favelle Favco Berhad which is engaged in

manufacturing industry and engaged in constructing cranes in effective manner. Adequate profits

are being attained by company as financial report clarifies that turnover in 2017 was 526,484.

Profit Before Interest and Tax were 83,277 in 2017 in comparison to 79,782 in previous year.

Profit attributable to shareholders in the same year was 63,097 while, total equity to investors

were amounting to 629,509. Share capital was 155,170 and EPS (Earnings Per Share) was 28.50

and net assets per share was 2.84. This means that profit is increased in 2017 financial year.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Point 1 – Explaining five items of MFRS 136 requirements for disclosure in annual report of

company

There are five items which are required to be included in an annual report as it is

mandatory to be included so that financials may be presented in accordance to MFRS (Malaysian

Financial Reporting Standards) 136 which is dedicated to impairment of assets. These assets

include tangible as well as intangible assets and as such, these should be showed in annual report

of the business quite effectually. The items included in annual report are listed below-

1. Property, Plant and Equipment (PPE)-

The PPE is an fixed asset which should be disclosed in annual report along with

impairment on it. There are various assets of fixed nature used in the business and economic

benefits are aroused in the future course of action (Rahman, & Mohamed 2018). It is required

that it should be disclosed so that impairment amount can be deducted for which damage is

occurred or because of time, fixed assets have lost their value. This will help in correct

ascertainment of profits as depreciation will be charged on it along with carrying amount

disclosed in financial report in the best possible manner.

2. Goodwill-

Goodwill is an intangible asset which builds because of brand image of organisation in

the market as customers are satisfied in effectual manner. This should be increased up to a high

extent as it shows that firm provides quality goods and services to customers and as such, market

value of organisation enhances in a better way. Goodwill should be disclosed at cost by

deducting impairment losses. The amount of goodwill is included in carrying amount and as a

result, it is made in relation to impairment if any.

3. Investment in associates-

The investment if made in associate firm should be included in the annual report so that

correct ascertainment may be made in the best possible manner. This means that investor has an

influence over other company and as a result, he can take participation in operating and financial

decisions. The information related to the company must be disclosed as required by MFRS 136

and impairment losses if any found must be shown as well. This will provide with useful

information to external parties and they will be benefited up to a high extent.

2

company

There are five items which are required to be included in an annual report as it is

mandatory to be included so that financials may be presented in accordance to MFRS (Malaysian

Financial Reporting Standards) 136 which is dedicated to impairment of assets. These assets

include tangible as well as intangible assets and as such, these should be showed in annual report

of the business quite effectually. The items included in annual report are listed below-

1. Property, Plant and Equipment (PPE)-

The PPE is an fixed asset which should be disclosed in annual report along with

impairment on it. There are various assets of fixed nature used in the business and economic

benefits are aroused in the future course of action (Rahman, & Mohamed 2018). It is required

that it should be disclosed so that impairment amount can be deducted for which damage is

occurred or because of time, fixed assets have lost their value. This will help in correct

ascertainment of profits as depreciation will be charged on it along with carrying amount

disclosed in financial report in the best possible manner.

2. Goodwill-

Goodwill is an intangible asset which builds because of brand image of organisation in

the market as customers are satisfied in effectual manner. This should be increased up to a high

extent as it shows that firm provides quality goods and services to customers and as such, market

value of organisation enhances in a better way. Goodwill should be disclosed at cost by

deducting impairment losses. The amount of goodwill is included in carrying amount and as a

result, it is made in relation to impairment if any.

3. Investment in associates-

The investment if made in associate firm should be included in the annual report so that

correct ascertainment may be made in the best possible manner. This means that investor has an

influence over other company and as a result, he can take participation in operating and financial

decisions. The information related to the company must be disclosed as required by MFRS 136

and impairment losses if any found must be shown as well. This will provide with useful

information to external parties and they will be benefited up to a high extent.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Intellectual Property-

Intellectual Property is another intangible asset to be disclosed in annual report which

organisation has hired to make its brand different from competitors and also to protect its

activities and functionalities from them (Golinghorst, 2017). It includes right of company to

trade its name which is differentiated from the rivals and customers may be attracted towards

particular brand. It should be stated at cost by deducting amortisation and impairment on it for

which loss has been occurred in the financial year. Hence, disclosure is mandatory in accordance

to MFRS standards.

5. Amortisation-

The amortisation is accounted for in effective manner. However, goodwill and related

intangible assets are not usually amortised and instead testing for impairment losses if any is

made on yearly basis. Moreover, there is an indication regarding that it may impaired in future

course of action. Other assets apart from this are amortised from the date they are hired and

organisation has started using it. The amortisation is recognised in financials of Favelle Favco

Berhad in 2017 year in Profit and Loss account on the basis of straight line method.

Point 2 – MFRS 136 disclosure compliance and format presented by organisation

The impairment of assets means that when carrying amount exceeds that of its

recoverable amount and as such, loss is suffered by company (Zhang & Ji., 2018). It is

essentially required as per the guidance of MFRS 136 that an asset should be effectively assessed

as per each year's balance sheet so as to identify whether indication prevails that an asset may be

impaired at future date or not. Hence, external and internal sources of information is recognised

to carry out analysis with regards to impaired assets. The disclosure compliance as provided by

MFRS 136 is listed as under-

Each of class of assets, financial statement must disclose related information-

Amount of impairment losses should be included in income statements and also the line

item of such statement and losses included in the Profit and Loss account.

Amount of reversal on such statements and line statement on losses on which reversal of

impairment is found.

The amount which is recognised directly in equity in the financial year

The impairment amount on reversal recognised in equity during financial year

3

Intellectual Property is another intangible asset to be disclosed in annual report which

organisation has hired to make its brand different from competitors and also to protect its

activities and functionalities from them (Golinghorst, 2017). It includes right of company to

trade its name which is differentiated from the rivals and customers may be attracted towards

particular brand. It should be stated at cost by deducting amortisation and impairment on it for

which loss has been occurred in the financial year. Hence, disclosure is mandatory in accordance

to MFRS standards.

5. Amortisation-

The amortisation is accounted for in effective manner. However, goodwill and related

intangible assets are not usually amortised and instead testing for impairment losses if any is

made on yearly basis. Moreover, there is an indication regarding that it may impaired in future

course of action. Other assets apart from this are amortised from the date they are hired and

organisation has started using it. The amortisation is recognised in financials of Favelle Favco

Berhad in 2017 year in Profit and Loss account on the basis of straight line method.

Point 2 – MFRS 136 disclosure compliance and format presented by organisation

The impairment of assets means that when carrying amount exceeds that of its

recoverable amount and as such, loss is suffered by company (Zhang & Ji., 2018). It is

essentially required as per the guidance of MFRS 136 that an asset should be effectively assessed

as per each year's balance sheet so as to identify whether indication prevails that an asset may be

impaired at future date or not. Hence, external and internal sources of information is recognised

to carry out analysis with regards to impaired assets. The disclosure compliance as provided by

MFRS 136 is listed as under-

Each of class of assets, financial statement must disclose related information-

Amount of impairment losses should be included in income statements and also the line

item of such statement and losses included in the Profit and Loss account.

Amount of reversal on such statements and line statement on losses on which reversal of

impairment is found.

The amount which is recognised directly in equity in the financial year

The impairment amount on reversal recognised in equity during financial year

3

Class of assets of similar nature should be disclosed in the financial statements. The

information can be presented and reconciled on the basis of carrying amount of PPE (Property,

Plant and Equipment) at opening and closing of reporting period quite effectually (Kortokrax,

2017). On the other hand, if organisation comes under the MASB 22 relating to segmental

reporting should disclose information with regards to each of its segment such as amount that has

been recognised in the income statements and also in the equity in the financial period.

Moreover, it has to include amount on reversals of such losses recognised in Profit and Loss

account and in equity for the particular period in the best possible way.

The impaired losses have been found on an asset or cash generating unit or be it reversed,

then also it contains material information and should be disclosed in the financials. It should

have events or circumstances led to impairment recognition, amount of reversal attained on such

reversal. If individual asset is found, then nature and segment to which it is attributable should be

disclosed. On the other hand, if cash generating unit is there, then description of the same must

be made, amount of impairment losses and aggregation of assets should be disclosed in a better

way by identifying that estimate has been modified. Thus, former and current amount should be

aggregated to attain reasons for such change in cash generating unit (Ahmad, 2018).

Moreover, to assess in case of cash generating unit that recoverable amount is net selling

value or its use of value. If recoverable amount is attained as per net selling price and it is to be

utilised with reference to net selling price and if other method is used, then discount rate should

be accounted for with reference to current and previous year estimate. Apart from this, if

impaired losses are in terms of material in aggregation of financials, then enterprise must

disclose brief classifying main classes of such assets and main event leading to recognition in

case of reversals. Key assumptions must be presented for any of the impairment losses incurred

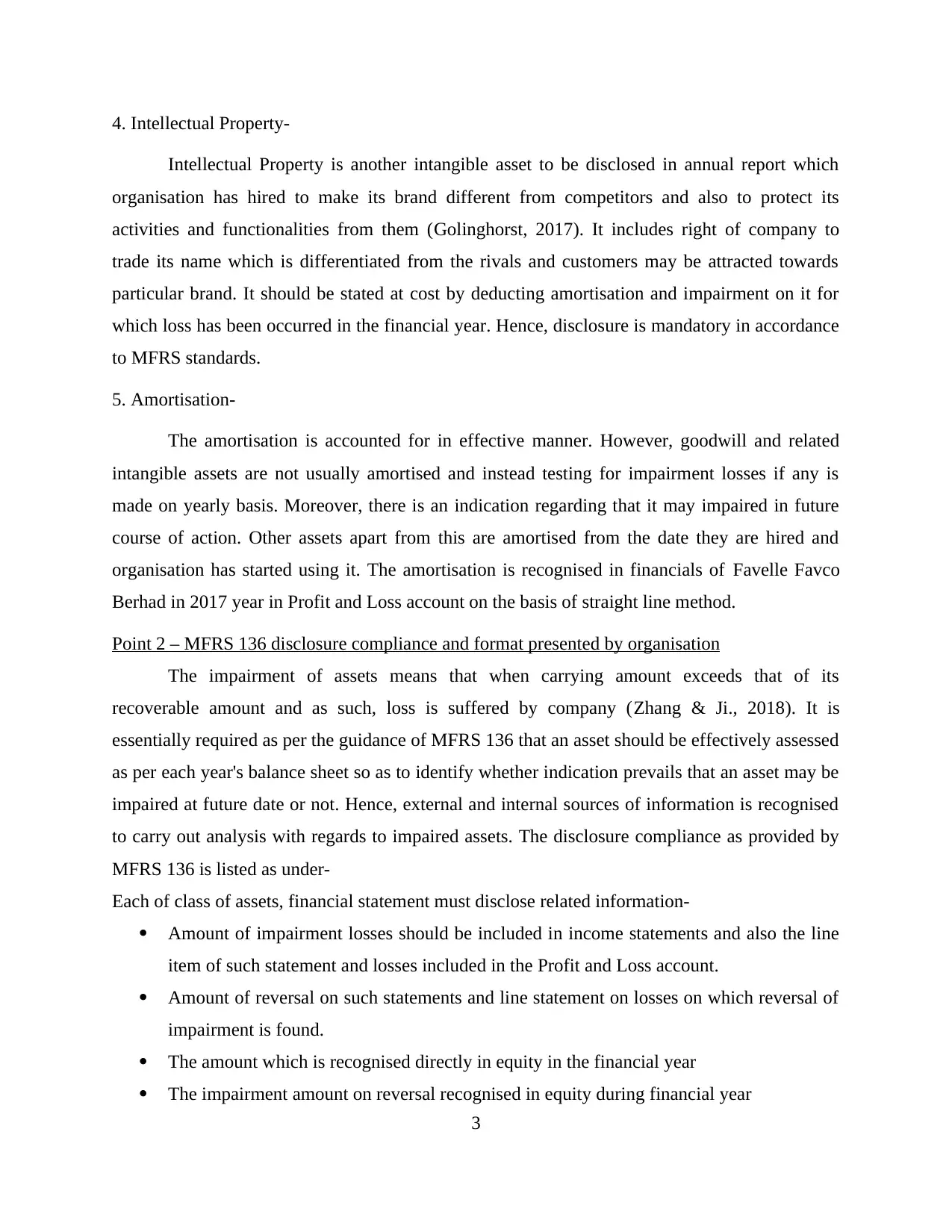

in financial year. The sample format for Favelle Favco Berhad is-

4

information can be presented and reconciled on the basis of carrying amount of PPE (Property,

Plant and Equipment) at opening and closing of reporting period quite effectually (Kortokrax,

2017). On the other hand, if organisation comes under the MASB 22 relating to segmental

reporting should disclose information with regards to each of its segment such as amount that has

been recognised in the income statements and also in the equity in the financial period.

Moreover, it has to include amount on reversals of such losses recognised in Profit and Loss

account and in equity for the particular period in the best possible way.

The impaired losses have been found on an asset or cash generating unit or be it reversed,

then also it contains material information and should be disclosed in the financials. It should

have events or circumstances led to impairment recognition, amount of reversal attained on such

reversal. If individual asset is found, then nature and segment to which it is attributable should be

disclosed. On the other hand, if cash generating unit is there, then description of the same must

be made, amount of impairment losses and aggregation of assets should be disclosed in a better

way by identifying that estimate has been modified. Thus, former and current amount should be

aggregated to attain reasons for such change in cash generating unit (Ahmad, 2018).

Moreover, to assess in case of cash generating unit that recoverable amount is net selling

value or its use of value. If recoverable amount is attained as per net selling price and it is to be

utilised with reference to net selling price and if other method is used, then discount rate should

be accounted for with reference to current and previous year estimate. Apart from this, if

impaired losses are in terms of material in aggregation of financials, then enterprise must

disclose brief classifying main classes of such assets and main event leading to recognition in

case of reversals. Key assumptions must be presented for any of the impairment losses incurred

in financial year. The sample format for Favelle Favco Berhad is-

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration 1: Intangible assets impairment treatment

Point 3 – Discussing recognition and measurement requirements in MFRS 136 standard

The recognition of impairment loss is required to be made as over the time, measurement

and recognising becomes important in order to correctly ascertain profits by deducting such

losses on the impaired assets in the best possible manner. Furthermore, if carrying amount is

more than that of recoverable amount, then impairment exists and as such, loss prevails which

needs to be accounted by Favelle Favco Berhad to make adjustments accordingly (Annual report

of Favelle Favco Berhad. 2017). Moreover, individual and cash generating unit are differently

treated by the organisation. Hence, recognition and measurement can be easily analysed by

taking into consideration provided by MFRS 136 standard. It may be assessed that if recoverable

5

Point 3 – Discussing recognition and measurement requirements in MFRS 136 standard

The recognition of impairment loss is required to be made as over the time, measurement

and recognising becomes important in order to correctly ascertain profits by deducting such

losses on the impaired assets in the best possible manner. Furthermore, if carrying amount is

more than that of recoverable amount, then impairment exists and as such, loss prevails which

needs to be accounted by Favelle Favco Berhad to make adjustments accordingly (Annual report

of Favelle Favco Berhad. 2017). Moreover, individual and cash generating unit are differently

treated by the organisation. Hence, recognition and measurement can be easily analysed by

taking into consideration provided by MFRS 136 standard. It may be assessed that if recoverable

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

amount is lower than that of carrying one, then it should be minimised in relation to recoverable

one and as such, reduction is known as impairment loss on an asset.

The company if identifies that asset is indicated to be impaired, then it should be taken

immediately. Loss should be instantly recognised as expenditure in Profit and Loss account.

However, it does not apply when asset has been revalued. On revaluation, value should be

decreased as per the standard. Revalued asset is recognised as surplus on it which is applicable

up to some extent till loss does not exceed amount in revaluation basis of such gain or surplus.

When carrying amount is less than amount in estimated to which it relates and organisation

should identify relating to and as a liability (Dhakal, Chintzoglou & Zhang, 2018).

After company has been identified or recognised, impairment loss should be included,

depreciation should be adjusted in relation to the asset in future years for allocating revised

amount by deducting residual value recognised on useful life of an asset in effective manner.

Hence, company may be able to ascertain correct profits and external parties may be benefited as

decisions can be made by them in according to their individual requirement. Thus, by comprising

with MFRS 136 standard of Malaysia, Favelle Favco Berhad can easily attain clarity regarding

financial performance and health and can provide well-structured financial statements

highlighting true and fair view of company.

The MFRS 136 standard is required to be followed by the business so that correct

estimation of impaired assets can be made and as such, correct profit may be ascertained in the

best possible manner. The recognition is needed to be made particularly when impaired assets

are taken into consideration. The carrying amount is more in comparison to recoverable amount

and thus, impairment exists which need to be taken into account and hence, profits can be

correctly obtained. MFRS 136 states that when carrying amount is in excess, then impairment of

assets are extracted which is treated as loss. As such, it is deducted from overall profits in order

to ascertain fair net profits. Hence, Favelle Favco Berhad which is engaged in constructing of

cranes is required to make adjustments of impaired assets. If there is possibility in the future that

assets might be impaired and thus, it should be recognised by firm and measure accordingly.

Hence, by complying with such standard, impaired assets' deduction can be made and profits can

be ascertained in a better way.

6

one and as such, reduction is known as impairment loss on an asset.

The company if identifies that asset is indicated to be impaired, then it should be taken

immediately. Loss should be instantly recognised as expenditure in Profit and Loss account.

However, it does not apply when asset has been revalued. On revaluation, value should be

decreased as per the standard. Revalued asset is recognised as surplus on it which is applicable

up to some extent till loss does not exceed amount in revaluation basis of such gain or surplus.

When carrying amount is less than amount in estimated to which it relates and organisation

should identify relating to and as a liability (Dhakal, Chintzoglou & Zhang, 2018).

After company has been identified or recognised, impairment loss should be included,

depreciation should be adjusted in relation to the asset in future years for allocating revised

amount by deducting residual value recognised on useful life of an asset in effective manner.

Hence, company may be able to ascertain correct profits and external parties may be benefited as

decisions can be made by them in according to their individual requirement. Thus, by comprising

with MFRS 136 standard of Malaysia, Favelle Favco Berhad can easily attain clarity regarding

financial performance and health and can provide well-structured financial statements

highlighting true and fair view of company.

The MFRS 136 standard is required to be followed by the business so that correct

estimation of impaired assets can be made and as such, correct profit may be ascertained in the

best possible manner. The recognition is needed to be made particularly when impaired assets

are taken into consideration. The carrying amount is more in comparison to recoverable amount

and thus, impairment exists which need to be taken into account and hence, profits can be

correctly obtained. MFRS 136 states that when carrying amount is in excess, then impairment of

assets are extracted which is treated as loss. As such, it is deducted from overall profits in order

to ascertain fair net profits. Hence, Favelle Favco Berhad which is engaged in constructing of

cranes is required to make adjustments of impaired assets. If there is possibility in the future that

assets might be impaired and thus, it should be recognised by firm and measure accordingly.

Hence, by complying with such standard, impaired assets' deduction can be made and profits can

be ascertained in a better way.

6

SUMMARY

Hereby it can be summarised that financial accounting play a crucial role in the company

and as such, organisation may be able to comply with financial requirements to be met in

accordance to standards issued by the board. Business transactions are needed to be accounted

for by organisation so as to maintain clarity regarding operational tasks attained. Furthermore,

firm is able to know about expenses made and income earned in effective manner. Without

complying with the financial principles, final accounts cannot be prepared accurately. Hence, it

is required that business should properly include each and every transaction so that firm may be

able to carry out final accounts in effective manner.

In relation to this, MFRS which is Malaysian Board guiding company to prepare

financials in the context of guidelines initiated by the professional body. The standard MFRS

136 which is related to impairment of assets is included in the board guidelines which provides

way to prepare and include losses identified in impairment of assets be it tangible or intangible.

This is essentially required so that financials may be formulated by correctly in the best possible

way. On the other hand, impaired amount on assets must be accounted for ascertaining correct

profits of company. Recognition and measurement of assets are required so that they may be

correctly accounted for and as a result, amount can be deducted to ascertain true value of asset.

It is compulsory required that if Favelle Favco Berhad identifies that an asset will be

impaired in the future as indication is clarified, then immediate action must be made in effective

way. The standard imparted by MFRS has to be followed to conduct operations legally and

providing true and fair view of financial information to external stakeholders with much ease.

There are various items that are to be included in annual report of organisation in order to fulfil

requirements of MFRS 136 and assets to be recognised and measured in relation to the same.

Hence, impairment losses can be effectively met and taken into account to exhibit true financials.

7

Hereby it can be summarised that financial accounting play a crucial role in the company

and as such, organisation may be able to comply with financial requirements to be met in

accordance to standards issued by the board. Business transactions are needed to be accounted

for by organisation so as to maintain clarity regarding operational tasks attained. Furthermore,

firm is able to know about expenses made and income earned in effective manner. Without

complying with the financial principles, final accounts cannot be prepared accurately. Hence, it

is required that business should properly include each and every transaction so that firm may be

able to carry out final accounts in effective manner.

In relation to this, MFRS which is Malaysian Board guiding company to prepare

financials in the context of guidelines initiated by the professional body. The standard MFRS

136 which is related to impairment of assets is included in the board guidelines which provides

way to prepare and include losses identified in impairment of assets be it tangible or intangible.

This is essentially required so that financials may be formulated by correctly in the best possible

way. On the other hand, impaired amount on assets must be accounted for ascertaining correct

profits of company. Recognition and measurement of assets are required so that they may be

correctly accounted for and as a result, amount can be deducted to ascertain true value of asset.

It is compulsory required that if Favelle Favco Berhad identifies that an asset will be

impaired in the future as indication is clarified, then immediate action must be made in effective

way. The standard imparted by MFRS has to be followed to conduct operations legally and

providing true and fair view of financial information to external stakeholders with much ease.

There are various items that are to be included in annual report of organisation in order to fulfil

requirements of MFRS 136 and assets to be recognised and measured in relation to the same.

Hence, impairment losses can be effectively met and taken into account to exhibit true financials.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Ahmad, N., (2018). Responsive Regulation and Resiliency: The Renewable Fuel Standard and

Advanced Biofuels.

Dhakal, S. K., Chintzoglou, G. & Zhang, J., (2018). A Study of a Compound Solar Eruption with

Two Consecutive Erupting Magnetic Structures. The Astrophysical Journal. 860(1). p.35.

Golinghorst, K. M., (2017). Meet Me in the Middle: The Search for the Appropriate Standard of

Review for the APA's Good Cause Exception. Iowa L. Rev.. 103. p.1277.

Kortokrax, S. A., (2017). Erroneous Deviation or Faithful Restoration: An Examination of the

NLRB's Browning-Ferris Joint-Employer Standard. Ohio St. LJ. 78. p.227.

Rahman, A. A., & Mohamed, A. S. (2018). Investigating the Early Implementation of MFRS

136 Disclosure among Top 50 Firms in Malaysia. Asian Journal of Accounting and

Governance. 8. 59-76.

Zhang, Q. M. & Ji, H. S., (2018). Vertical oscillation of a coronal cavity triggered by an EUV

wave. The Astrophysical Journal. 860(2). p.113.

Online

8

Books and Journals

Ahmad, N., (2018). Responsive Regulation and Resiliency: The Renewable Fuel Standard and

Advanced Biofuels.

Dhakal, S. K., Chintzoglou, G. & Zhang, J., (2018). A Study of a Compound Solar Eruption with

Two Consecutive Erupting Magnetic Structures. The Astrophysical Journal. 860(1). p.35.

Golinghorst, K. M., (2017). Meet Me in the Middle: The Search for the Appropriate Standard of

Review for the APA's Good Cause Exception. Iowa L. Rev.. 103. p.1277.

Kortokrax, S. A., (2017). Erroneous Deviation or Faithful Restoration: An Examination of the

NLRB's Browning-Ferris Joint-Employer Standard. Ohio St. LJ. 78. p.227.

Rahman, A. A., & Mohamed, A. S. (2018). Investigating the Early Implementation of MFRS

136 Disclosure among Top 50 Firms in Malaysia. Asian Journal of Accounting and

Governance. 8. 59-76.

Zhang, Q. M. & Ji, H. S., (2018). Vertical oscillation of a coronal cavity triggered by an EUV

wave. The Astrophysical Journal. 860(2). p.113.

Online

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Annual report of Favelle Favco Berhad. 2017 [PDF] Available Through:

<http://disclosure.bursamalaysia.com/FileAccess/apbursaweb/download?

id=186966&name=EA_DS_ATTACHMENTS>

9

<http://disclosure.bursamalaysia.com/FileAccess/apbursaweb/download?

id=186966&name=EA_DS_ATTACHMENTS>

9

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.