Specialised Financial Accounting Report: Malaysian Banks and MFRS101

VerifiedAdded on 2021/04/21

|18

|3121

|50

Report

AI Summary

This report provides an in-depth analysis of specialised financial accounting practices, specifically focusing on the Malaysian Financial Reporting Standard 101 (MFRS101) and its application within the banking sector. The report examines the financial reporting of two major Malaysian banks, Public Bank Berhad and CIMB Group Holdings Berhad, detailing their compliance with MFRS101 and the guidelines set by the Securities Commission. It outlines the requirements of MFRS101, including the presentation of financial statements, balance sheets, income statements, and cash flow statements, while also considering the guidelines for unit trust funds. Furthermore, the report offers a comparative analysis, contrasting MFRS with US Generally Accepted Accounting Principles (GAAP), using Bank of America as a case study. The report concludes with a summary of key findings and insights into the adherence of Malaysian banks to financial reporting standards, offering valuable information for students and professionals alike.

RUNNING HEAD: SPECIALISED FINANCIAL ACCOUNTING

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Specialised financial accounting 1

Contents

Introduction...........................................................................................................................................2

Description of the companies................................................................................................................2

Public bank Berhad............................................................................................................................2

CIMB group holdings Berhad............................................................................................................3

Requirements of MFRS101 and Securities Commission Guidelines.....................................................3

Compliance and format of disclosure by the selected banks..................................................................6

Comparing with another country.........................................................................................................11

Summary.............................................................................................................................................13

Conclusion...........................................................................................................................................14

References...........................................................................................................................................16

Contents

Introduction...........................................................................................................................................2

Description of the companies................................................................................................................2

Public bank Berhad............................................................................................................................2

CIMB group holdings Berhad............................................................................................................3

Requirements of MFRS101 and Securities Commission Guidelines.....................................................3

Compliance and format of disclosure by the selected banks..................................................................6

Comparing with another country.........................................................................................................11

Summary.............................................................................................................................................13

Conclusion...........................................................................................................................................14

References...........................................................................................................................................16

Specialised financial accounting 2

Introduction

Companies operating in Malaysia follow the standards provided by MASB. The main

objective of such compliance is to give fair representation of the financial position of the

company. There are numerous of standards in the framework of Malaysian Financial

Reporting that are applied by almost each and every company. Out of many, there is one

standard named as MFRS101 Presentation of Financial Statements, generally used for the

preparation of company’s financial documents reflecting the performance highlights. This

standard has certain requirements which are been discussed in the report. Apart from this,

Malaysian companies especially unit trust funds follows the guidelines of Securities

Commission while preparing their financial documents.

The report comprises of the disclosure of requirements of MFRS101 and Securities

Commission Guidelines. It considers the two big Malaysian banks named as CIMB Group

and Public Bank Berhad. The first part deals with the description of the banks and later on the

requirements of the standard and guideline are been discussed. In the later part of the report,

the compliance with the above is been discussed. The report also highlights the comparison

between MFRS and US GAAP, considering the Bank of America as a comparative

corporation. The last part deals with the summary portion containing all the discussion in the

nutshell and followed by the conclusion.

Description of the companies

Public bank Berhad

A financial institution situated in Kuala Lumpur, Malaysia engaged in offering financial

services to the country as well as to the Asia-Pacific region. Currently, the public bank is the

second largest bank of Southeast Asia and was founded back in 1966 by Teh Hong Piow. It

got listed on Malaysian Stock Exchange in 1967. In terms of shareholders’ funds and market

Introduction

Companies operating in Malaysia follow the standards provided by MASB. The main

objective of such compliance is to give fair representation of the financial position of the

company. There are numerous of standards in the framework of Malaysian Financial

Reporting that are applied by almost each and every company. Out of many, there is one

standard named as MFRS101 Presentation of Financial Statements, generally used for the

preparation of company’s financial documents reflecting the performance highlights. This

standard has certain requirements which are been discussed in the report. Apart from this,

Malaysian companies especially unit trust funds follows the guidelines of Securities

Commission while preparing their financial documents.

The report comprises of the disclosure of requirements of MFRS101 and Securities

Commission Guidelines. It considers the two big Malaysian banks named as CIMB Group

and Public Bank Berhad. The first part deals with the description of the banks and later on the

requirements of the standard and guideline are been discussed. In the later part of the report,

the compliance with the above is been discussed. The report also highlights the comparison

between MFRS and US GAAP, considering the Bank of America as a comparative

corporation. The last part deals with the summary portion containing all the discussion in the

nutshell and followed by the conclusion.

Description of the companies

Public bank Berhad

A financial institution situated in Kuala Lumpur, Malaysia engaged in offering financial

services to the country as well as to the Asia-Pacific region. Currently, the public bank is the

second largest bank of Southeast Asia and was founded back in 1966 by Teh Hong Piow. It

got listed on Malaysian Stock Exchange in 1967. In terms of shareholders’ funds and market

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Specialised financial accounting 3

capitalization, it is the largest and second largest bank in Malaysia after Maybank (Public

Bank. 2018). The main activities of the bank include offering variety of financial products

and services like personal and commercial banking, Islamic banking, nominee and trustee

services, investment banking and many more. Talking about the financial highlights, the

operating revenue RM 20,858 million which was more than the revenue of 2016 that was RM

20,103 million. The operating profit of the bank was RM 6,745 in 2016 which increased to

RM 7319 million. Apart from that, the shareholders’ equity and total assets has also risen

during the year (Reuters. 2018).

CIMB group holdings Berhad

It is a universal bank in Malaysia having its headquarters situated at Kuala Lumpur. CIMB

operates in high growth economy in ASEAN and has a wide network of retail branches

across the region. The entities covered by the group are CIMB Bank, CIMB Investment bank

and many more. Concerning the history, it was formed by merging various other banks in the

past. The primary activities of the group includes providing consumer banking services,

wholesale banking, treasury and markets, integrating investment and corporate banking and

making strategic investments and group strategy (Bloomberg. 2018). Main markets covered

by the group are Indonesia, Thailand, Malaysia and Singapore. Taking into account its

financial highlights, the net revenue of the group has increased from RM 3,550,792 to RM

4,410,259. However, overall it has faced a shortfall of income over expenditure worth RM

4,359,008 which is pretty less than the figure reported in 2016. Also the total assets of the

group has been reduced during the year (CIMB. 2018).

Requirements of MFRS101 and Securities Commission Guidelines

Companies operating in Malaysia are required to follows the standards issued by Malaysian

Accounting Standard Board (MASB). Such standards provide the basis for financial reporting

capitalization, it is the largest and second largest bank in Malaysia after Maybank (Public

Bank. 2018). The main activities of the bank include offering variety of financial products

and services like personal and commercial banking, Islamic banking, nominee and trustee

services, investment banking and many more. Talking about the financial highlights, the

operating revenue RM 20,858 million which was more than the revenue of 2016 that was RM

20,103 million. The operating profit of the bank was RM 6,745 in 2016 which increased to

RM 7319 million. Apart from that, the shareholders’ equity and total assets has also risen

during the year (Reuters. 2018).

CIMB group holdings Berhad

It is a universal bank in Malaysia having its headquarters situated at Kuala Lumpur. CIMB

operates in high growth economy in ASEAN and has a wide network of retail branches

across the region. The entities covered by the group are CIMB Bank, CIMB Investment bank

and many more. Concerning the history, it was formed by merging various other banks in the

past. The primary activities of the group includes providing consumer banking services,

wholesale banking, treasury and markets, integrating investment and corporate banking and

making strategic investments and group strategy (Bloomberg. 2018). Main markets covered

by the group are Indonesia, Thailand, Malaysia and Singapore. Taking into account its

financial highlights, the net revenue of the group has increased from RM 3,550,792 to RM

4,410,259. However, overall it has faced a shortfall of income over expenditure worth RM

4,359,008 which is pretty less than the figure reported in 2016. Also the total assets of the

group has been reduced during the year (CIMB. 2018).

Requirements of MFRS101 and Securities Commission Guidelines

Companies operating in Malaysia are required to follows the standards issued by Malaysian

Accounting Standard Board (MASB). Such standards provide the basis for financial reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Specialised financial accounting 4

for all the entities which are running their business in the country. They are known as

Malaysian Financial Reporting Standards (MFRS). Public bank and CIMB, being financial

institutions are required to comply with the provisions and requirements of all MFRS that are

applicable to them. Among the various standards, MFRS101 is the one which deals with the

presentation of financial statements of a company (Deloitte. 2017). The IAS 1 is equal to the

Malaysian standard 101 and the requirements are also somewhat same. The main

requirements of this standard are:

1. As per MFRS 101, the financial statements of a unit trust must include the following:

a. Balance sheet

b. Income statement

c. Statement of cash flow prepared as per MFRS 107

d. Statement showing changes in equity

e. Notes to financial statements

f. Comparative information as required by the standard (MASB. 2018).

2. It is mandatory for the unit trust fund to represent their financial statements as per

MFRS101.

3. The financial statements must present the true and fair view of the company’s

financial position, its performance and flow of cash.

4. MFRS 101 requires the management to take an assessment of the ability of the

organization to survive for the longer period. Reason being, financial statements are

prepared on the assumption that the business will be going concern. If any

uncertainties or discrepancies are there, the company must disclose the same properly.

5. The statements must be prepared on the basis of accrual accounting except the

information of cash flow.

for all the entities which are running their business in the country. They are known as

Malaysian Financial Reporting Standards (MFRS). Public bank and CIMB, being financial

institutions are required to comply with the provisions and requirements of all MFRS that are

applicable to them. Among the various standards, MFRS101 is the one which deals with the

presentation of financial statements of a company (Deloitte. 2017). The IAS 1 is equal to the

Malaysian standard 101 and the requirements are also somewhat same. The main

requirements of this standard are:

1. As per MFRS 101, the financial statements of a unit trust must include the following:

a. Balance sheet

b. Income statement

c. Statement of cash flow prepared as per MFRS 107

d. Statement showing changes in equity

e. Notes to financial statements

f. Comparative information as required by the standard (MASB. 2018).

2. It is mandatory for the unit trust fund to represent their financial statements as per

MFRS101.

3. The financial statements must present the true and fair view of the company’s

financial position, its performance and flow of cash.

4. MFRS 101 requires the management to take an assessment of the ability of the

organization to survive for the longer period. Reason being, financial statements are

prepared on the assumption that the business will be going concern. If any

uncertainties or discrepancies are there, the company must disclose the same properly.

5. The statements must be prepared on the basis of accrual accounting except the

information of cash flow.

Specialised financial accounting 5

6. The unit trust fund is required to display the comparative information in respect of the

previous years’ performance, both in the statement and in the notes. It is been

provided for the narrative and descriptive purposes (MASB. 2018).

7. It is required to prepare such statements at least annually and if the reporting period

changes, the entity must disclose the same.

8. Statement of financial position must classify the assets and liabilities as current and

non-current.

The unit trust in Malaysia are governed by the guideline issued by Securities Commission on

March 2008. These guidelines are issued in order to provide a regulatory framework that

protect the interest of public investments and developing the unit trust industry in Malaysia.

According to the schedule VI of Securities commission guidelines, the unit trust funds are

required to prepare their financial statements as per the generally accepted accounting

principles, the trust deed, statutory requirements that are applicable and as per the other

regulatory requirements.

Following must be present in the statements as per the schedule:

1. Assets and liabilities statement

2. Statement of income and expenditure

3. Financial statements note and a statement of changes in the value of net assets

4. Disclosure of some specific items reported in each financial document

Preparing financial statements according to MASB and above guidelines results in the

meeting of reporting requirements of schedule VI. In addition to that, the trust must separate

the capital of unit holders from realised and unrealised gains or losses. The disclosure must

be done separately.

6. The unit trust fund is required to display the comparative information in respect of the

previous years’ performance, both in the statement and in the notes. It is been

provided for the narrative and descriptive purposes (MASB. 2018).

7. It is required to prepare such statements at least annually and if the reporting period

changes, the entity must disclose the same.

8. Statement of financial position must classify the assets and liabilities as current and

non-current.

The unit trust in Malaysia are governed by the guideline issued by Securities Commission on

March 2008. These guidelines are issued in order to provide a regulatory framework that

protect the interest of public investments and developing the unit trust industry in Malaysia.

According to the schedule VI of Securities commission guidelines, the unit trust funds are

required to prepare their financial statements as per the generally accepted accounting

principles, the trust deed, statutory requirements that are applicable and as per the other

regulatory requirements.

Following must be present in the statements as per the schedule:

1. Assets and liabilities statement

2. Statement of income and expenditure

3. Financial statements note and a statement of changes in the value of net assets

4. Disclosure of some specific items reported in each financial document

Preparing financial statements according to MASB and above guidelines results in the

meeting of reporting requirements of schedule VI. In addition to that, the trust must separate

the capital of unit holders from realised and unrealised gains or losses. The disclosure must

be done separately.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Specialised financial accounting 6

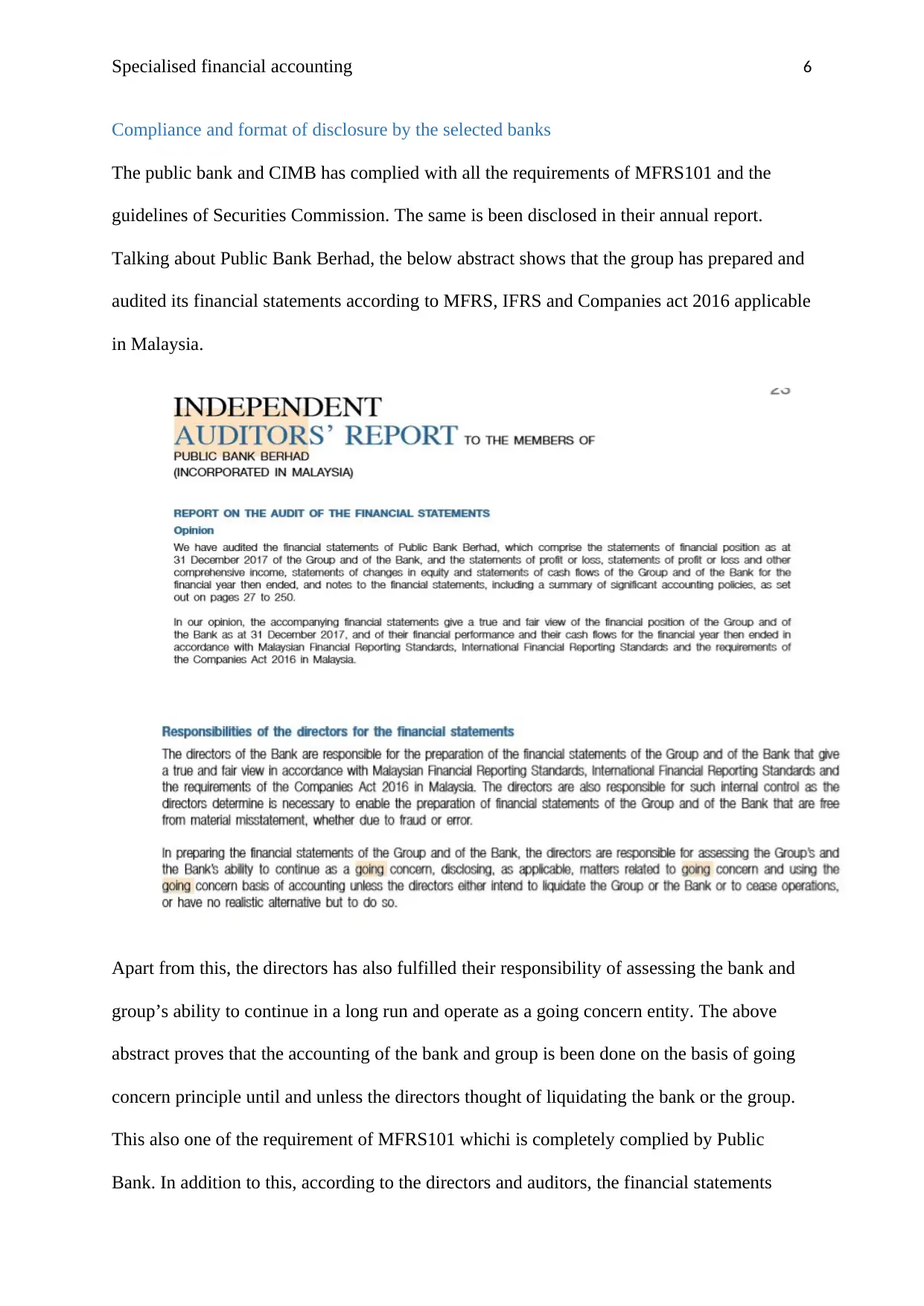

Compliance and format of disclosure by the selected banks

The public bank and CIMB has complied with all the requirements of MFRS101 and the

guidelines of Securities Commission. The same is been disclosed in their annual report.

Talking about Public Bank Berhad, the below abstract shows that the group has prepared and

audited its financial statements according to MFRS, IFRS and Companies act 2016 applicable

in Malaysia.

Apart from this, the directors has also fulfilled their responsibility of assessing the bank and

group’s ability to continue in a long run and operate as a going concern entity. The above

abstract proves that the accounting of the bank and group is been done on the basis of going

concern principle until and unless the directors thought of liquidating the bank or the group.

This also one of the requirement of MFRS101 whichi is completely complied by Public

Bank. In addition to this, according to the directors and auditors, the financial statements

Compliance and format of disclosure by the selected banks

The public bank and CIMB has complied with all the requirements of MFRS101 and the

guidelines of Securities Commission. The same is been disclosed in their annual report.

Talking about Public Bank Berhad, the below abstract shows that the group has prepared and

audited its financial statements according to MFRS, IFRS and Companies act 2016 applicable

in Malaysia.

Apart from this, the directors has also fulfilled their responsibility of assessing the bank and

group’s ability to continue in a long run and operate as a going concern entity. The above

abstract proves that the accounting of the bank and group is been done on the basis of going

concern principle until and unless the directors thought of liquidating the bank or the group.

This also one of the requirement of MFRS101 whichi is completely complied by Public

Bank. In addition to this, according to the directors and auditors, the financial statements

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

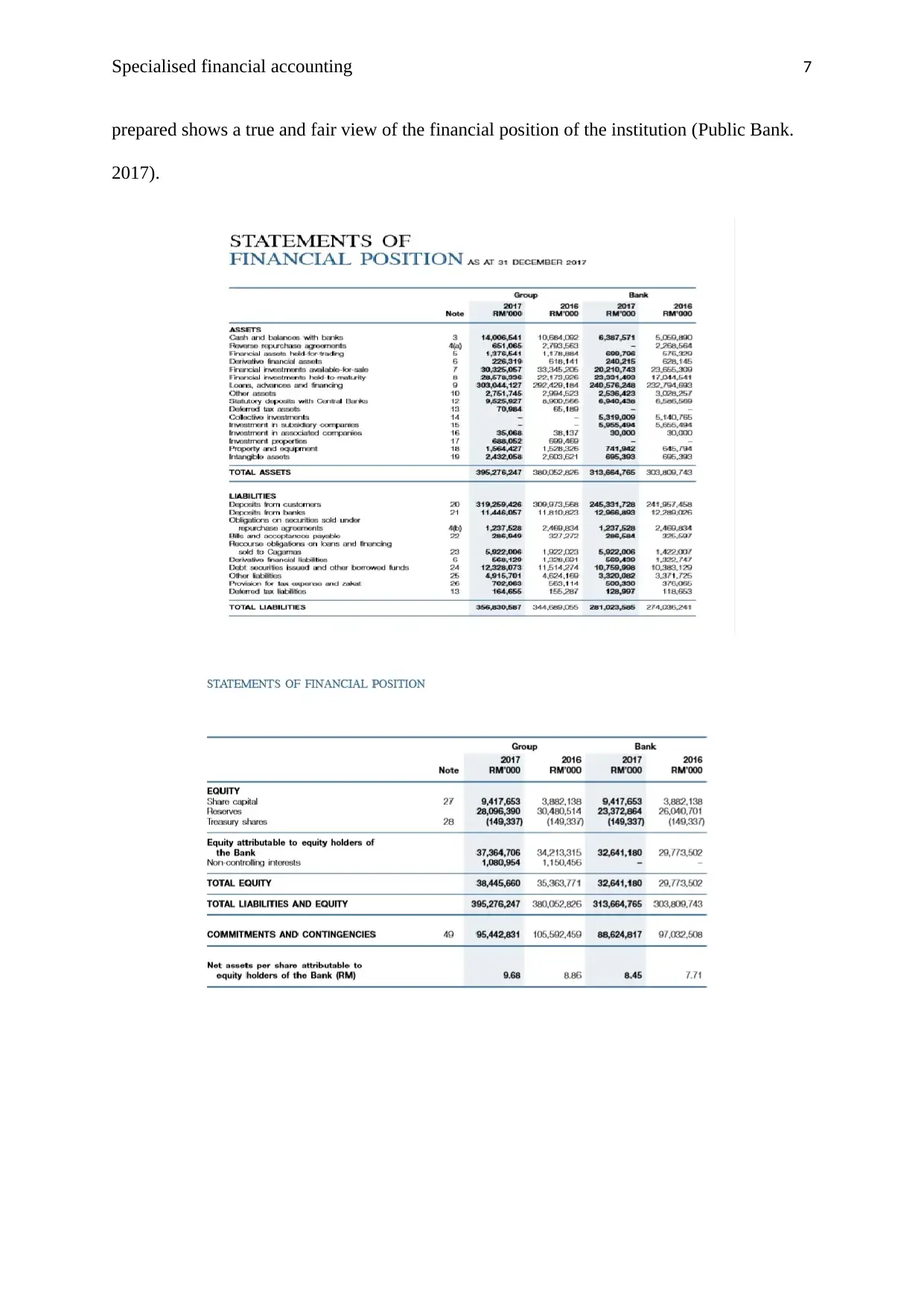

Specialised financial accounting 7

prepared shows a true and fair view of the financial position of the institution (Public Bank.

2017).

prepared shows a true and fair view of the financial position of the institution (Public Bank.

2017).

Specialised financial accounting 8

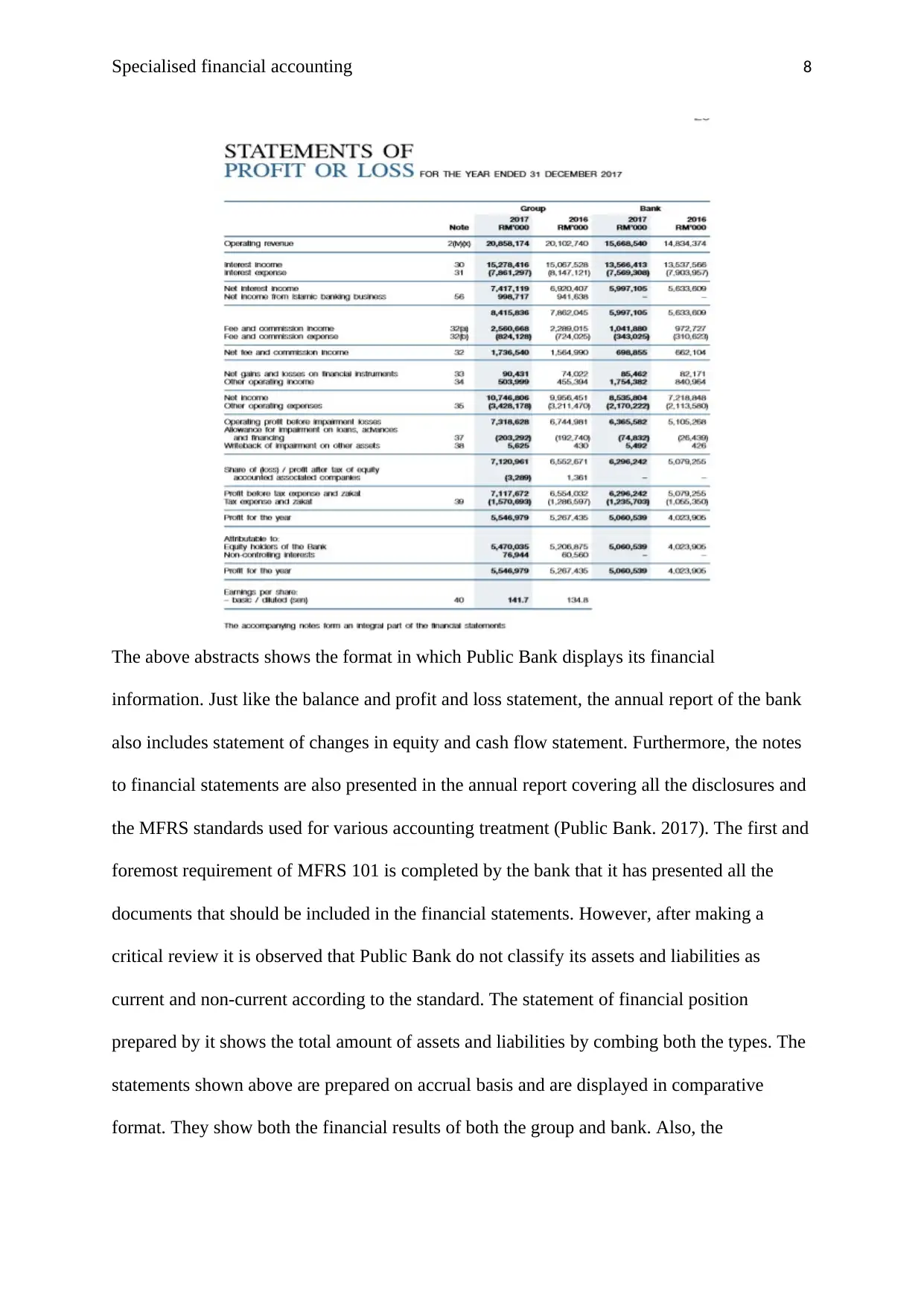

The above abstracts shows the format in which Public Bank displays its financial

information. Just like the balance and profit and loss statement, the annual report of the bank

also includes statement of changes in equity and cash flow statement. Furthermore, the notes

to financial statements are also presented in the annual report covering all the disclosures and

the MFRS standards used for various accounting treatment (Public Bank. 2017). The first and

foremost requirement of MFRS 101 is completed by the bank that it has presented all the

documents that should be included in the financial statements. However, after making a

critical review it is observed that Public Bank do not classify its assets and liabilities as

current and non-current according to the standard. The statement of financial position

prepared by it shows the total amount of assets and liabilities by combing both the types. The

statements shown above are prepared on accrual basis and are displayed in comparative

format. They show both the financial results of both the group and bank. Also, the

The above abstracts shows the format in which Public Bank displays its financial

information. Just like the balance and profit and loss statement, the annual report of the bank

also includes statement of changes in equity and cash flow statement. Furthermore, the notes

to financial statements are also presented in the annual report covering all the disclosures and

the MFRS standards used for various accounting treatment (Public Bank. 2017). The first and

foremost requirement of MFRS 101 is completed by the bank that it has presented all the

documents that should be included in the financial statements. However, after making a

critical review it is observed that Public Bank do not classify its assets and liabilities as

current and non-current according to the standard. The statement of financial position

prepared by it shows the total amount of assets and liabilities by combing both the types. The

statements shown above are prepared on accrual basis and are displayed in comparative

format. They show both the financial results of both the group and bank. Also, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Specialised financial accounting 9

performance of the current year is measured against the previous year. On a whole, it gives a

comparative view to the users (Public Bank. 2017).

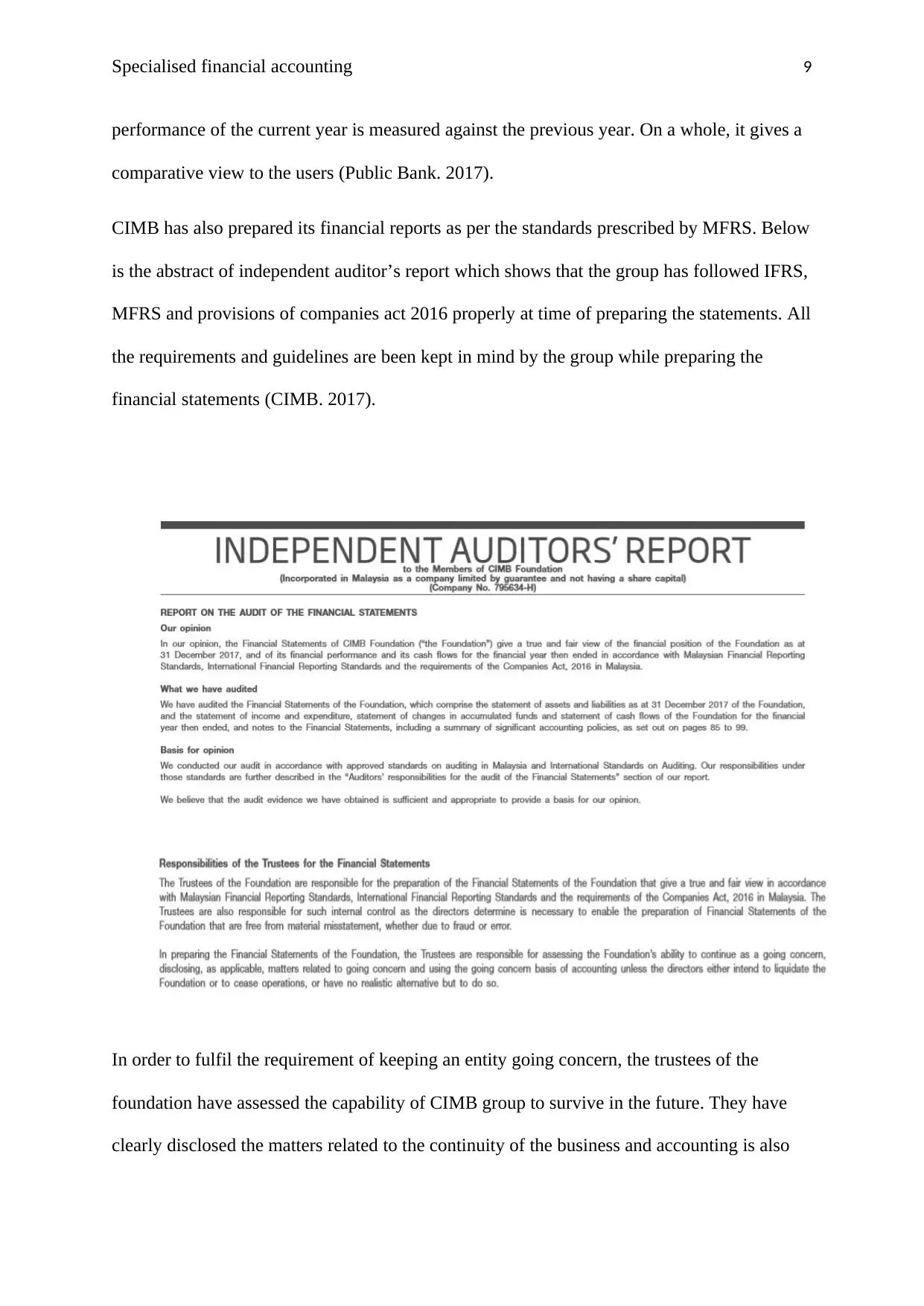

CIMB has also prepared its financial reports as per the standards prescribed by MFRS. Below

is the abstract of independent auditor’s report which shows that the group has followed IFRS,

MFRS and provisions of companies act 2016 properly at time of preparing the statements. All

the requirements and guidelines are been kept in mind by the group while preparing the

financial statements (CIMB. 2017).

In order to fulfil the requirement of keeping an entity going concern, the trustees of the

foundation have assessed the capability of CIMB group to survive in the future. They have

clearly disclosed the matters related to the continuity of the business and accounting is also

performance of the current year is measured against the previous year. On a whole, it gives a

comparative view to the users (Public Bank. 2017).

CIMB has also prepared its financial reports as per the standards prescribed by MFRS. Below

is the abstract of independent auditor’s report which shows that the group has followed IFRS,

MFRS and provisions of companies act 2016 properly at time of preparing the statements. All

the requirements and guidelines are been kept in mind by the group while preparing the

financial statements (CIMB. 2017).

In order to fulfil the requirement of keeping an entity going concern, the trustees of the

foundation have assessed the capability of CIMB group to survive in the future. They have

clearly disclosed the matters related to the continuity of the business and accounting is also

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Specialised financial accounting 10

done on this basis only as long as the directors have not taken any decision related to

liquidation or ceasing the operations (CIMB. 2017).

done on this basis only as long as the directors have not taken any decision related to

liquidation or ceasing the operations (CIMB. 2017).

Specialised financial accounting 11

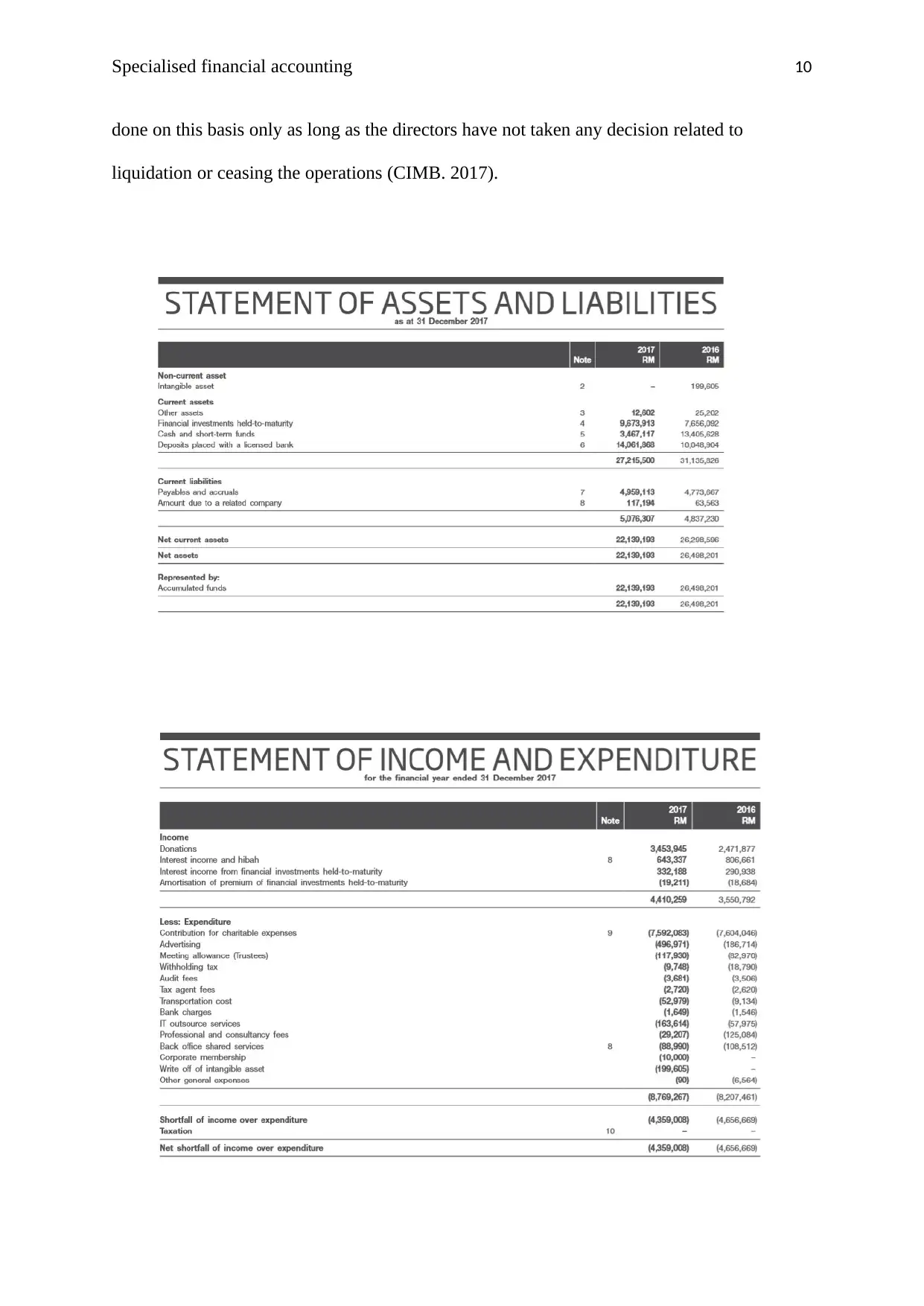

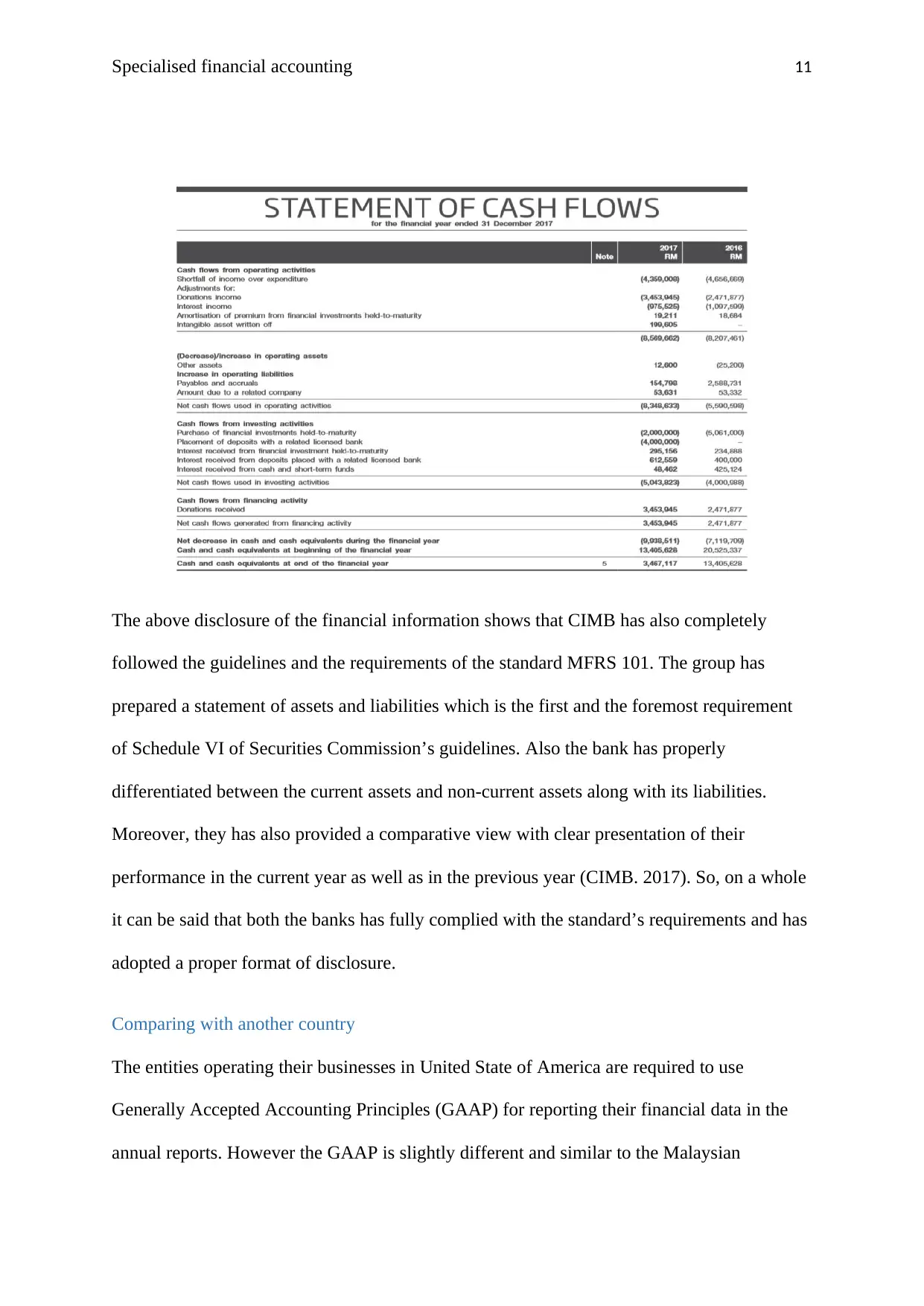

The above disclosure of the financial information shows that CIMB has also completely

followed the guidelines and the requirements of the standard MFRS 101. The group has

prepared a statement of assets and liabilities which is the first and the foremost requirement

of Schedule VI of Securities Commission’s guidelines. Also the bank has properly

differentiated between the current assets and non-current assets along with its liabilities.

Moreover, they has also provided a comparative view with clear presentation of their

performance in the current year as well as in the previous year (CIMB. 2017). So, on a whole

it can be said that both the banks has fully complied with the standard’s requirements and has

adopted a proper format of disclosure.

Comparing with another country

The entities operating their businesses in United State of America are required to use

Generally Accepted Accounting Principles (GAAP) for reporting their financial data in the

annual reports. However the GAAP is slightly different and similar to the Malaysian

The above disclosure of the financial information shows that CIMB has also completely

followed the guidelines and the requirements of the standard MFRS 101. The group has

prepared a statement of assets and liabilities which is the first and the foremost requirement

of Schedule VI of Securities Commission’s guidelines. Also the bank has properly

differentiated between the current assets and non-current assets along with its liabilities.

Moreover, they has also provided a comparative view with clear presentation of their

performance in the current year as well as in the previous year (CIMB. 2017). So, on a whole

it can be said that both the banks has fully complied with the standard’s requirements and has

adopted a proper format of disclosure.

Comparing with another country

The entities operating their businesses in United State of America are required to use

Generally Accepted Accounting Principles (GAAP) for reporting their financial data in the

annual reports. However the GAAP is slightly different and similar to the Malaysian

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.