ACC00145: Financial Reporting, AASB & Myer Holdings Ltd. Analysis

VerifiedAdded on 2023/04/26

|13

|2254

|88

Report

AI Summary

This report provides an analysis of financial reporting, focusing on the importance of social accountability within the framework of General Purpose Financial Reports (GPFR). It examines the role and development of Australian Accounting Standards Boards (AASBs) in shaping business practices in Australia. The report further delves into the types of information disclosed by ASX-listed company Myer Holdings Ltd., including required incentive disclosures, and assesses the impact of this information on investors' decisions. Key aspects covered include the AASB's conceptual framework, disclosure requirements for various types of entities, and an evaluation of Myer Holdings Ltd.'s financial performance based on its annual report, considering factors like profitability, liquidity, and solvency. The analysis concludes that the information presented in financial reports significantly influences investor perceptions and decisions in the securities market.

Running head: FINANCIAL REPORTING

Financial reporting

Name of the student

Name of the university

Student ID

Author note

Financial reporting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL REPORTING

Executive summary

The purpose of the report is to provide the comments on importance of social accountability

as part of the GPFR objective. Further, the report will focus on the importance of

establishment and development of AASBs or the business practices in Australia. It will

further highlight the types of information provided in the ASX listed company Myer

Holdings Ltd. and the incentives disclosures required by the entity. It will further state the

impact of information provided in annual reports of the company to the investors.

Executive summary

The purpose of the report is to provide the comments on importance of social accountability

as part of the GPFR objective. Further, the report will focus on the importance of

establishment and development of AASBs or the business practices in Australia. It will

further highlight the types of information provided in the ASX listed company Myer

Holdings Ltd. and the incentives disclosures required by the entity. It will further state the

impact of information provided in annual reports of the company to the investors.

2FINANCIAL REPORTING

Table of Contents

Introduction................................................................................................................................3

Answer 1....................................................................................................................................3

Answer 2....................................................................................................................................4

Answer 3....................................................................................................................................5

Answer 4....................................................................................................................................6

Answer 5....................................................................................................................................8

Conclusion..................................................................................................................................9

Reference..................................................................................................................................11

Table of Contents

Introduction................................................................................................................................3

Answer 1....................................................................................................................................3

Answer 2....................................................................................................................................4

Answer 3....................................................................................................................................5

Answer 4....................................................................................................................................6

Answer 5....................................................................................................................................8

Conclusion..................................................................................................................................9

Reference..................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL REPORTING

Introduction

Social accountability is an important part of GPFR. Accounting standards used by the

Australian business establishments to prepare and present their financial statement in

accordance with the Corporation law are generally referred as the AASBs prepared by the

AASB (Australian accounting standard board) (Aasb.gov.au 2019).

Answer 1

“Social accountability is considered in the (AASB Conceptual) Framework as part

of the objectives of general purpose financial reports (GPFR)” – comments

The term accountability is regarded as an imprecise concept. Therefore, it is

considered as the separate objective that may require the GPFR (general purpose financial

reports) to provide different types of the information such as reporting for social

responsibility. Whereas it is already established bu AASB that there is an interrelation

between the intended scope for the GPFR and objectives, it shall be directly addressed and

shall not define the term inadvertently through expressing the objectives (Luke 2016). Based

on the suggestions of AASB, the conceptual framework as an inseparable part of the GPFR

shall –

Include accountability of objectives unambiguously for the purpose of decision

making by depicting the concept of accountability as a responsibility to deliver the

information that will assist the users of financial statement to make informed

decisions. the decisions are taken considering the performance of the entity, its

financial position and the compliance made by it while evaluated and made

decisions regarding allocation of scarce resources. This decision will also include

Introduction

Social accountability is an important part of GPFR. Accounting standards used by the

Australian business establishments to prepare and present their financial statement in

accordance with the Corporation law are generally referred as the AASBs prepared by the

AASB (Australian accounting standard board) (Aasb.gov.au 2019).

Answer 1

“Social accountability is considered in the (AASB Conceptual) Framework as part

of the objectives of general purpose financial reports (GPFR)” – comments

The term accountability is regarded as an imprecise concept. Therefore, it is

considered as the separate objective that may require the GPFR (general purpose financial

reports) to provide different types of the information such as reporting for social

responsibility. Whereas it is already established bu AASB that there is an interrelation

between the intended scope for the GPFR and objectives, it shall be directly addressed and

shall not define the term inadvertently through expressing the objectives (Luke 2016). Based

on the suggestions of AASB, the conceptual framework as an inseparable part of the GPFR

shall –

Include accountability of objectives unambiguously for the purpose of decision

making by depicting the concept of accountability as a responsibility to deliver the

information that will assist the users of financial statement to make informed

decisions. the decisions are taken considering the performance of the entity, its

financial position and the compliance made by it while evaluated and made

decisions regarding allocation of scarce resources. This decision will also include

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL REPORTING

analysis regarding the efficiency of management with regard to usage of scarce

resources (Luke 2017).

Describe the user’s decision with regard to distribution of scarce resources including

decisions regarding influence of the management’s decision making approaches.

Further, the decision shall also focus into the decisions of the management with

regard to distribution of scarce resources through voting system or lobby system

(Huber 2017).

Hence, it is determined that the social accountability forms part of AASB conceptual

framework while following the GPFR.

Answer 2

Requirement of establishment and development of AASBs for Australian business practices

AASB development in Australia involves numerous steps including the procedure for

public consultation and accompanying discussion associated with that, wherever applicable.

Different disclosure requirements are there for reporting the financial statement and the

requirements vary with the types of entity those are particularly based on the level of public

interest (Mazhambe 2014). The entities are segregated as follows –

Small proprietary concerns

Large proprietary concerns and public companies those are unlisted and fulfils at

least 2 criteria from 3 as follows –

Number of employees 50 or more than that

Value of gross asset is $ 5 million or more

Value of gross operating revenue $ 10 million or more

analysis regarding the efficiency of management with regard to usage of scarce

resources (Luke 2017).

Describe the user’s decision with regard to distribution of scarce resources including

decisions regarding influence of the management’s decision making approaches.

Further, the decision shall also focus into the decisions of the management with

regard to distribution of scarce resources through voting system or lobby system

(Huber 2017).

Hence, it is determined that the social accountability forms part of AASB conceptual

framework while following the GPFR.

Answer 2

Requirement of establishment and development of AASBs for Australian business practices

AASB development in Australia involves numerous steps including the procedure for

public consultation and accompanying discussion associated with that, wherever applicable.

Different disclosure requirements are there for reporting the financial statement and the

requirements vary with the types of entity those are particularly based on the level of public

interest (Mazhambe 2014). The entities are segregated as follows –

Small proprietary concerns

Large proprietary concerns and public companies those are unlisted and fulfils at

least 2 criteria from 3 as follows –

Number of employees 50 or more than that

Value of gross asset is $ 5 million or more

Value of gross operating revenue $ 10 million or more

5FINANCIAL REPORTING

Disclosing companies including mainly the listed entities and the managed registered

undertakings. These organisations have issued share capital or have listed securities

from circulation of prospectus (Newberry 2015)

In accordance with AASB all the above mentioned entities are obliged to maintain

records associated with the accurate transactions related to finance and accounting. Further, it

must enable the preparation of the financial statements and auditing of the statements. Except

the small proprietary concerns, all other entities shall prepare financial reports on annual

basis. Generally the financial statement includes cash flow statements, balance sheet, income

statement and statement of changes in equity (Aasb.gov.au 2019). Matters required to be

disclosed under the financial reports are mentioned in accounting standards issued by

AASBs. Apart from that, force of law is applicable on it in accordance with Corporation aw.

Further, it has been mentioned in Corporation Law that the companies shall prepare the

consolidated financial report wherever it is required by the accounting standard. Apart from

that the reported financial statement shall be circulated to the company members and must be

lodged with the ASIC (Australian securities and investment commission). Along with

meeting the annual disclosure requirements, the disclosing entities shall prepare half-year

financial report that is considered as the abridged version of annual financial statement. This

half yearly financial report shall also be lodged with the ASIC. However, it is not required to

be circulated to the members (Aasb.gov.au 2019).

Hence, for Australian business establishments it is required to establish and develop

the AASB to enhance transparency, eliminating override of true and fair view and improving

the requirements related to disclosures.

Answer 3

Information delivered through the annual report of Myer Holdings Ltd

Disclosing companies including mainly the listed entities and the managed registered

undertakings. These organisations have issued share capital or have listed securities

from circulation of prospectus (Newberry 2015)

In accordance with AASB all the above mentioned entities are obliged to maintain

records associated with the accurate transactions related to finance and accounting. Further, it

must enable the preparation of the financial statements and auditing of the statements. Except

the small proprietary concerns, all other entities shall prepare financial reports on annual

basis. Generally the financial statement includes cash flow statements, balance sheet, income

statement and statement of changes in equity (Aasb.gov.au 2019). Matters required to be

disclosed under the financial reports are mentioned in accounting standards issued by

AASBs. Apart from that, force of law is applicable on it in accordance with Corporation aw.

Further, it has been mentioned in Corporation Law that the companies shall prepare the

consolidated financial report wherever it is required by the accounting standard. Apart from

that the reported financial statement shall be circulated to the company members and must be

lodged with the ASIC (Australian securities and investment commission). Along with

meeting the annual disclosure requirements, the disclosing entities shall prepare half-year

financial report that is considered as the abridged version of annual financial statement. This

half yearly financial report shall also be lodged with the ASIC. However, it is not required to

be circulated to the members (Aasb.gov.au 2019).

Hence, for Australian business establishments it is required to establish and develop

the AASB to enhance transparency, eliminating override of true and fair view and improving

the requirements related to disclosures.

Answer 3

Information delivered through the annual report of Myer Holdings Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL REPORTING

Different information delivered through the annual report of Myer Holdings Ltd for

the year closed on 25th October 2018 are as follows –

Chairman’s report

Performance review

Meet John King, CEO and Managing Director of the company

Sustainability at Myer

Year under review

Director’s report

Independence declaration of the auditor

Remuneration report

Financial statement including cash flow statements, balance sheet, income statement

and statement of changes in equity and notes to the financial reports

Declaration of directors

Report of independent auditor

Information of shareholders

Corporate directory (Investor.myer.com.au 2019).

Further, the financial report of the entity is general purpose financial report and

prepared as per the requirement of AAS and the interpretation released by AASB and

Corporation Act 2001. Myer Holdings Ltd is a for profit organisation in context for

preparation of the financial reports. Further, the reports are complied with the IFRS issued by

AASB (Investor.myer.com.au 2019).

Answer 4

Disclosure requirements for incentives

Different information delivered through the annual report of Myer Holdings Ltd for

the year closed on 25th October 2018 are as follows –

Chairman’s report

Performance review

Meet John King, CEO and Managing Director of the company

Sustainability at Myer

Year under review

Director’s report

Independence declaration of the auditor

Remuneration report

Financial statement including cash flow statements, balance sheet, income statement

and statement of changes in equity and notes to the financial reports

Declaration of directors

Report of independent auditor

Information of shareholders

Corporate directory (Investor.myer.com.au 2019).

Further, the financial report of the entity is general purpose financial report and

prepared as per the requirement of AAS and the interpretation released by AASB and

Corporation Act 2001. Myer Holdings Ltd is a for profit organisation in context for

preparation of the financial reports. Further, the reports are complied with the IFRS issued by

AASB (Investor.myer.com.au 2019).

Answer 4

Disclosure requirements for incentives

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL REPORTING

For the specified directors and specified executives disclosures are required as follows

–

Total remuneration amount for the reporting period. Remuneration generally includes

salaries, bonus, fees, allowances, perquisites, personal benefits, equity investments

and personal benefits. However, it does not include the expenses carried out by the

employee on behalf of the entity or the subsidiary of the entity. Further, the

remuneration must be measured in compliance with AASB 1028 on employee

benefits. However, if any particular item is not included under the AASB 1028, the

entity shall measure it on the basis of the expenses incurred by it for providing the

benefit (Aasb.gov.au 2019).

Aggregate or total individual remuneration and aggregate for each of the component

must be disclosed with regard to –

Specific directors

Specific executives

Disclosure of comparative value for the previous reporting period is not required for

individuals who were not categorized as specific for the concerned period. However,

disclosure for comparative amount is required for aggregate components and total

remuneration

Further details regarding remuneration to specified directors and specified executives

–

How and whether principle relation is linked between remuneration paid and

performance of the company

Principle used to determine the remuneration nature and amount (Aasb.gov.au 2019).

For each of the service contract between specified directors and specified executives

and the reporting entity explanations shall be there regarding how the remuneration

For the specified directors and specified executives disclosures are required as follows

–

Total remuneration amount for the reporting period. Remuneration generally includes

salaries, bonus, fees, allowances, perquisites, personal benefits, equity investments

and personal benefits. However, it does not include the expenses carried out by the

employee on behalf of the entity or the subsidiary of the entity. Further, the

remuneration must be measured in compliance with AASB 1028 on employee

benefits. However, if any particular item is not included under the AASB 1028, the

entity shall measure it on the basis of the expenses incurred by it for providing the

benefit (Aasb.gov.au 2019).

Aggregate or total individual remuneration and aggregate for each of the component

must be disclosed with regard to –

Specific directors

Specific executives

Disclosure of comparative value for the previous reporting period is not required for

individuals who were not categorized as specific for the concerned period. However,

disclosure for comparative amount is required for aggregate components and total

remuneration

Further details regarding remuneration to specified directors and specified executives

–

How and whether principle relation is linked between remuneration paid and

performance of the company

Principle used to determine the remuneration nature and amount (Aasb.gov.au 2019).

For each of the service contract between specified directors and specified executives

and the reporting entity explanations shall be there regarding how the remuneration

8FINANCIAL REPORTING

amount is determined. Further, it determines how the terms of contract have an impact

on the future period remuneration.

Terms and condition for granting cash bonus, performance related bonus and share

based payment as compensation and impact of the grant on future period

remuneration. It includes (i) grant date (ii) nature of remuneration granted (iii)

performance criteria and service criteria used to determine amount of remuneration

(iv)alteration of terms and conditions regarding date, impact, grand date, grant amount

with all details of alteration, if any (Yong, Lim and Tan 2016).

Apart from above additional terms and conditions required to be disclosed are – (i) if

shareholder’s approval are required (ii) whether benefits are payable on annual basis

or during performance period or at end of grant period (ii) restriction on transfer of

equity instrument after vesting, if any.

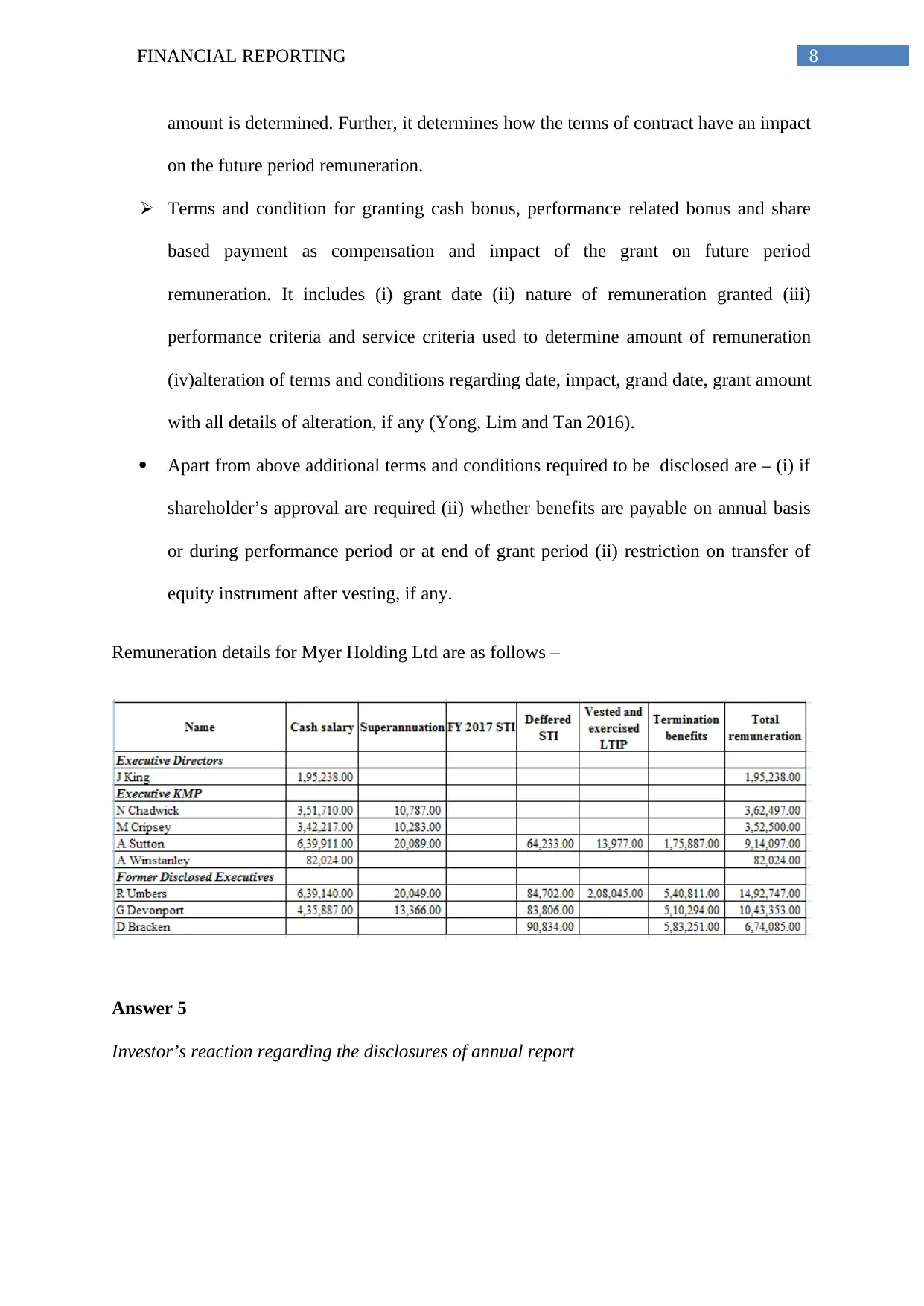

Remuneration details for Myer Holding Ltd are as follows –

Answer 5

Investor’s reaction regarding the disclosures of annual report

amount is determined. Further, it determines how the terms of contract have an impact

on the future period remuneration.

Terms and condition for granting cash bonus, performance related bonus and share

based payment as compensation and impact of the grant on future period

remuneration. It includes (i) grant date (ii) nature of remuneration granted (iii)

performance criteria and service criteria used to determine amount of remuneration

(iv)alteration of terms and conditions regarding date, impact, grand date, grant amount

with all details of alteration, if any (Yong, Lim and Tan 2016).

Apart from above additional terms and conditions required to be disclosed are – (i) if

shareholder’s approval are required (ii) whether benefits are payable on annual basis

or during performance period or at end of grant period (ii) restriction on transfer of

equity instrument after vesting, if any.

Remuneration details for Myer Holding Ltd are as follows –

Answer 5

Investor’s reaction regarding the disclosures of annual report

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL REPORTING

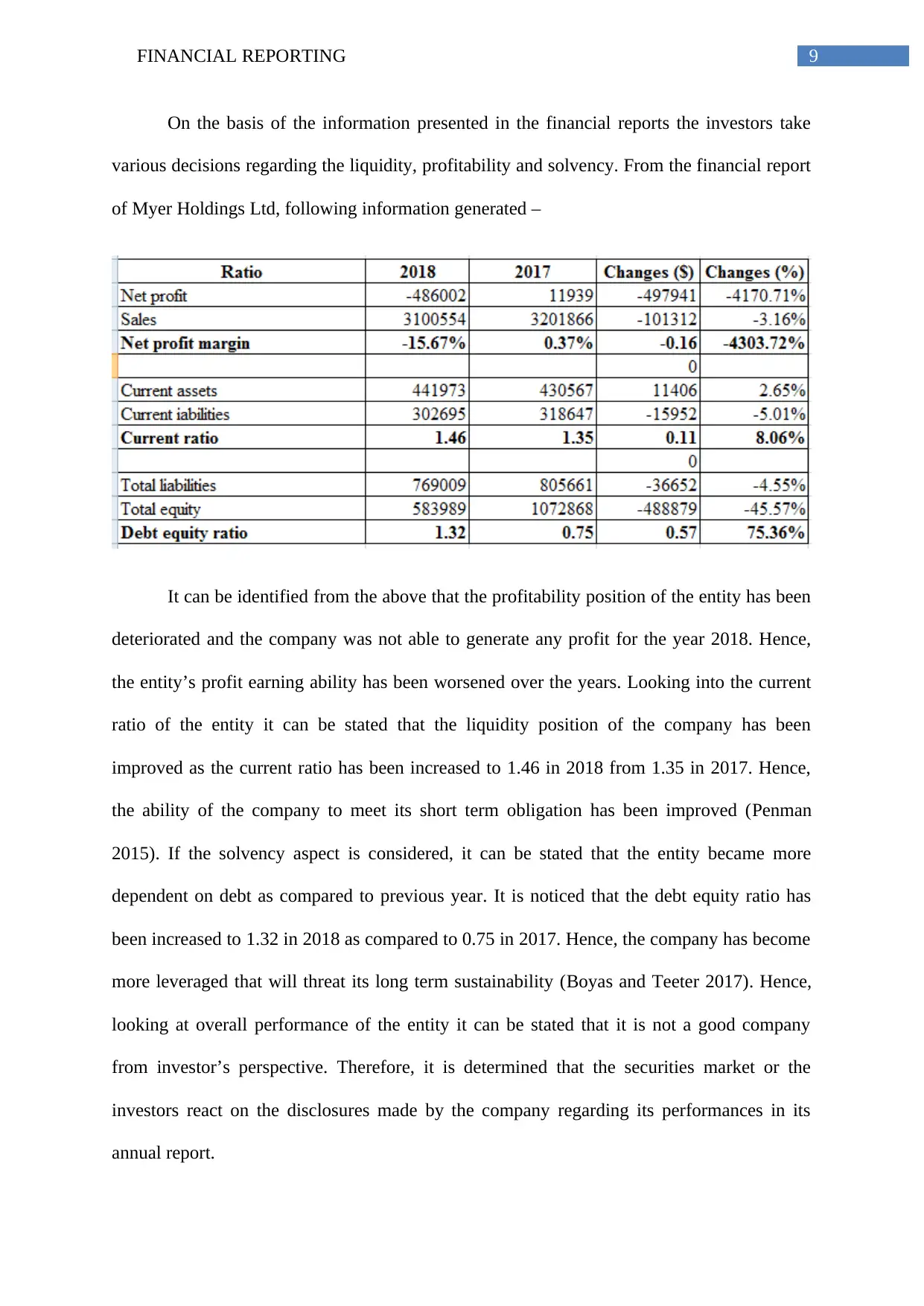

On the basis of the information presented in the financial reports the investors take

various decisions regarding the liquidity, profitability and solvency. From the financial report

of Myer Holdings Ltd, following information generated –

It can be identified from the above that the profitability position of the entity has been

deteriorated and the company was not able to generate any profit for the year 2018. Hence,

the entity’s profit earning ability has been worsened over the years. Looking into the current

ratio of the entity it can be stated that the liquidity position of the company has been

improved as the current ratio has been increased to 1.46 in 2018 from 1.35 in 2017. Hence,

the ability of the company to meet its short term obligation has been improved (Penman

2015). If the solvency aspect is considered, it can be stated that the entity became more

dependent on debt as compared to previous year. It is noticed that the debt equity ratio has

been increased to 1.32 in 2018 as compared to 0.75 in 2017. Hence, the company has become

more leveraged that will threat its long term sustainability (Boyas and Teeter 2017). Hence,

looking at overall performance of the entity it can be stated that it is not a good company

from investor’s perspective. Therefore, it is determined that the securities market or the

investors react on the disclosures made by the company regarding its performances in its

annual report.

On the basis of the information presented in the financial reports the investors take

various decisions regarding the liquidity, profitability and solvency. From the financial report

of Myer Holdings Ltd, following information generated –

It can be identified from the above that the profitability position of the entity has been

deteriorated and the company was not able to generate any profit for the year 2018. Hence,

the entity’s profit earning ability has been worsened over the years. Looking into the current

ratio of the entity it can be stated that the liquidity position of the company has been

improved as the current ratio has been increased to 1.46 in 2018 from 1.35 in 2017. Hence,

the ability of the company to meet its short term obligation has been improved (Penman

2015). If the solvency aspect is considered, it can be stated that the entity became more

dependent on debt as compared to previous year. It is noticed that the debt equity ratio has

been increased to 1.32 in 2018 as compared to 0.75 in 2017. Hence, the company has become

more leveraged that will threat its long term sustainability (Boyas and Teeter 2017). Hence,

looking at overall performance of the entity it can be stated that it is not a good company

from investor’s perspective. Therefore, it is determined that the securities market or the

investors react on the disclosures made by the company regarding its performances in its

annual report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL REPORTING

Conclusion

Financial reports represent the financial position and performance of the entity for the

specific period of time. On the basis of the information presented in the financial reports the

investors take various decisions regarding the liquidity, profitability and solvency. Hence,

social accountability forms an important part of GPFR and Australian business shall follow

accounting standards while preparing their financial reports.

Conclusion

Financial reports represent the financial position and performance of the entity for the

specific period of time. On the basis of the information presented in the financial reports the

investors take various decisions regarding the liquidity, profitability and solvency. Hence,

social accountability forms an important part of GPFR and Australian business shall follow

accounting standards while preparing their financial reports.

11FINANCIAL REPORTING

Reference

Aasb.gov.au. 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/AASB1046_01-04.pdf [Accessed 5 Feb.

2019].

Boyas, E. and Teeter, R., 2017. Teaching Financial Ratio Analysis using XBRL.

In Developments in Business Simulation and Experiential Learning: Proceedings of the

Annual ABSEL conference (Vol. 44, No. 1).

Huber, W., 2017. Irreconcilable differences? The FASB's conceptual framework and the

public interest. International Journal of Critical Accounting, 9(5/6), pp.514-523.

Investor.myer.com.au., 2019. Myer Investor Relations. [online] Available at:

http://investor.myer.com.au/Investor-Centre/ [Accessed 5 Feb. 2019].

Luke, B., 2016. Measuring and reporting on social performance: from numbers and narratives

to a useful reporting framework for social enterprises. Social and Environmental

Accountability Journal, 36(2), pp.103-123.

Luke, B., 2017. Statement of social performance: Opportunities and barriers to

adoption. Social and Environmental Accountability Journal, 37(2), pp.118-136.

Mazhambe, Z., 2014. Review of International Accounting Standards Board (IASB) Proposed

New Conceptual Framework: Discussion Paper (DP/2013/1). Journal of Modern Accounting

and Auditing, 10(8).

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

Reference

Aasb.gov.au. 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/AASB1046_01-04.pdf [Accessed 5 Feb.

2019].

Boyas, E. and Teeter, R., 2017. Teaching Financial Ratio Analysis using XBRL.

In Developments in Business Simulation and Experiential Learning: Proceedings of the

Annual ABSEL conference (Vol. 44, No. 1).

Huber, W., 2017. Irreconcilable differences? The FASB's conceptual framework and the

public interest. International Journal of Critical Accounting, 9(5/6), pp.514-523.

Investor.myer.com.au., 2019. Myer Investor Relations. [online] Available at:

http://investor.myer.com.au/Investor-Centre/ [Accessed 5 Feb. 2019].

Luke, B., 2016. Measuring and reporting on social performance: from numbers and narratives

to a useful reporting framework for social enterprises. Social and Environmental

Accountability Journal, 36(2), pp.103-123.

Luke, B., 2017. Statement of social performance: Opportunities and barriers to

adoption. Social and Environmental Accountability Journal, 37(2), pp.118-136.

Mazhambe, Z., 2014. Review of International Accounting Standards Board (IASB) Proposed

New Conceptual Framework: Discussion Paper (DP/2013/1). Journal of Modern Accounting

and Auditing, 10(8).

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.