Financial Accounting Newsletter: Financial Reporting Updates for ASX

VerifiedAdded on 2022/10/15

|10

|972

|14

Report

AI Summary

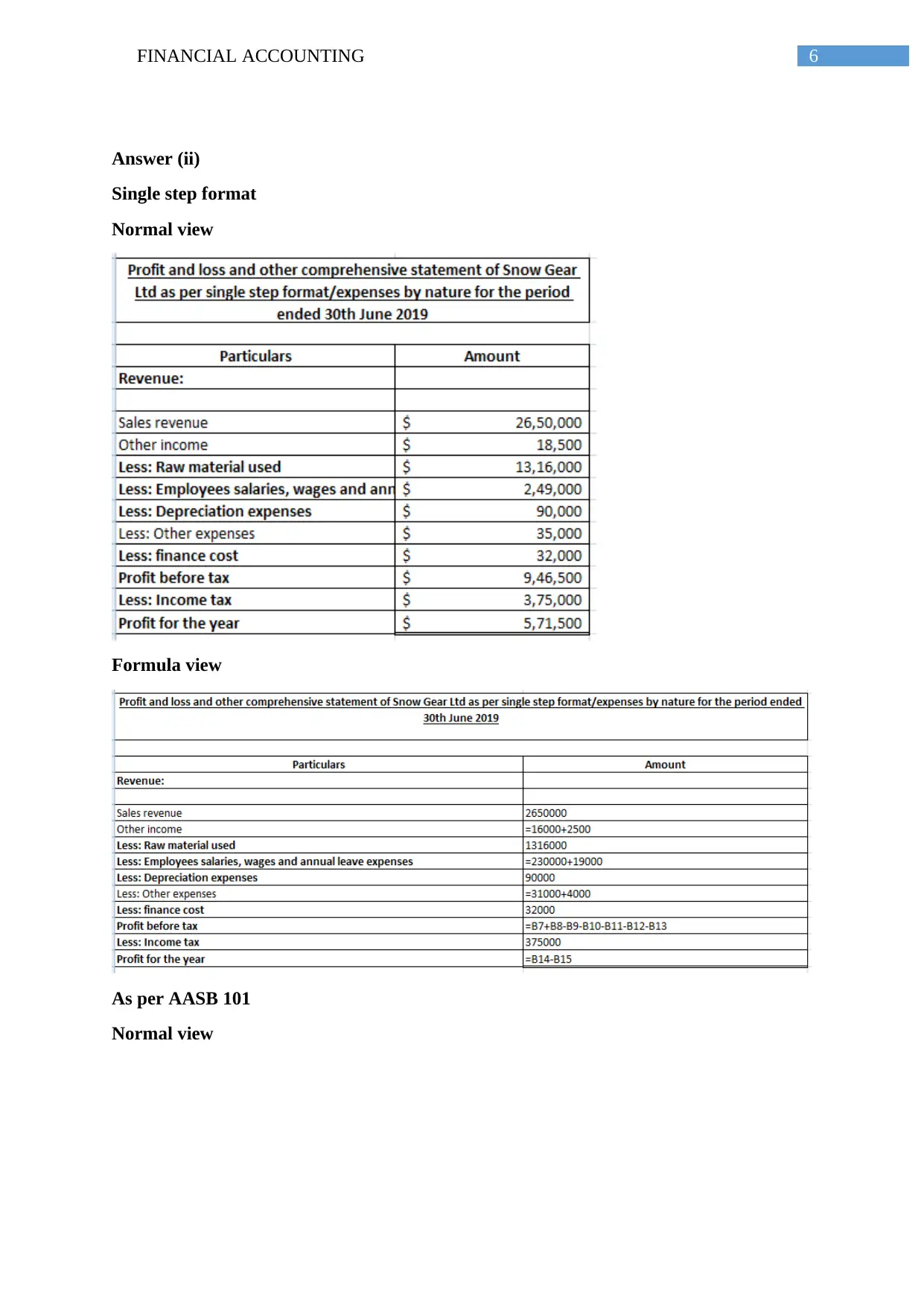

This financial accounting newsletter provides a comprehensive overview of recent developments in financial reporting from April 1, 2019, to July 31, 2019. It covers amendments to Australian Accounting Standards (AAS) regarding disclosures for special purpose financial statements, changes to AASB 112 on deferred tax, and the definition of not-for-profit companies. The newsletter also addresses amendments to IFRS 17 implementation, the conceptual framework for financial reporting, and includes a memorandum offering advice on preparing an income statement. The document also includes a comparison of expense reporting by function versus nature, along with relevant bibliography and links to further information. The newsletter format is designed to keep staff informed of changes that may impact their work and provides directions to staff on where they can access further information.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.